Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

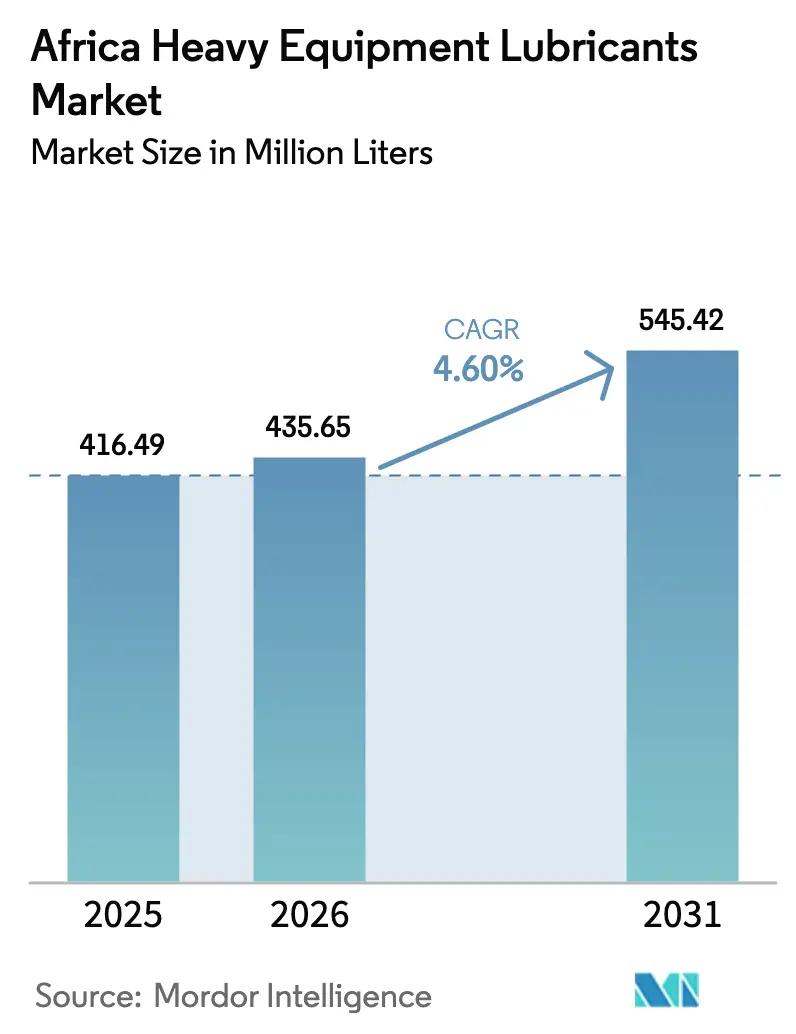

| Base Year Market Size (2025) | 416.49 Million liters |

| Market Volume (2026) | 435.65 Million liters |

| Market Volume (2031) | 545.42 Million liters |

| Growth Rate (2026 - 2031) | 4.60% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Africa Heavy Equipment Lubricants Market Analysis by Mordor Intelligence

The Africa Heavy Equipment Lubricants Market size is expected to grow from 416.49 Million liters in 2025 to 435.65 Million liters in 2026 and is forecast to reach 545.42 Million liters by 2031 at 4.60% CAGR over 2026-2031. Growth is anchored in large–scale infrastructure programs, a synchronous upturn in hard-rock mining, and policy-backed agricultural mechanization that together raise demand for engine oils, hydraulic fluids, and specialty greases. Egypt’s megaproject pipeline, Nigeria’s refinery-linked construction boom, and Algeria’s mining build-out headline the structural uptick in lubricant consumption at job sites stretching from the Maghreb to sub-Saharan Africa. Tight global Group I base-oil supply continues to push operators toward Group II/III synthetics, while government tenders that mandate oil-analysis services reward suppliers able to bundle products with technical support. Competitive strategies now revolve around end-to-end fluid-management offerings, network consolidation, and digital fleet analytics, all of which convert lubricant supply from a spot purchase into a multi-year services contract that secures wallet share.

Key Report Takeaways

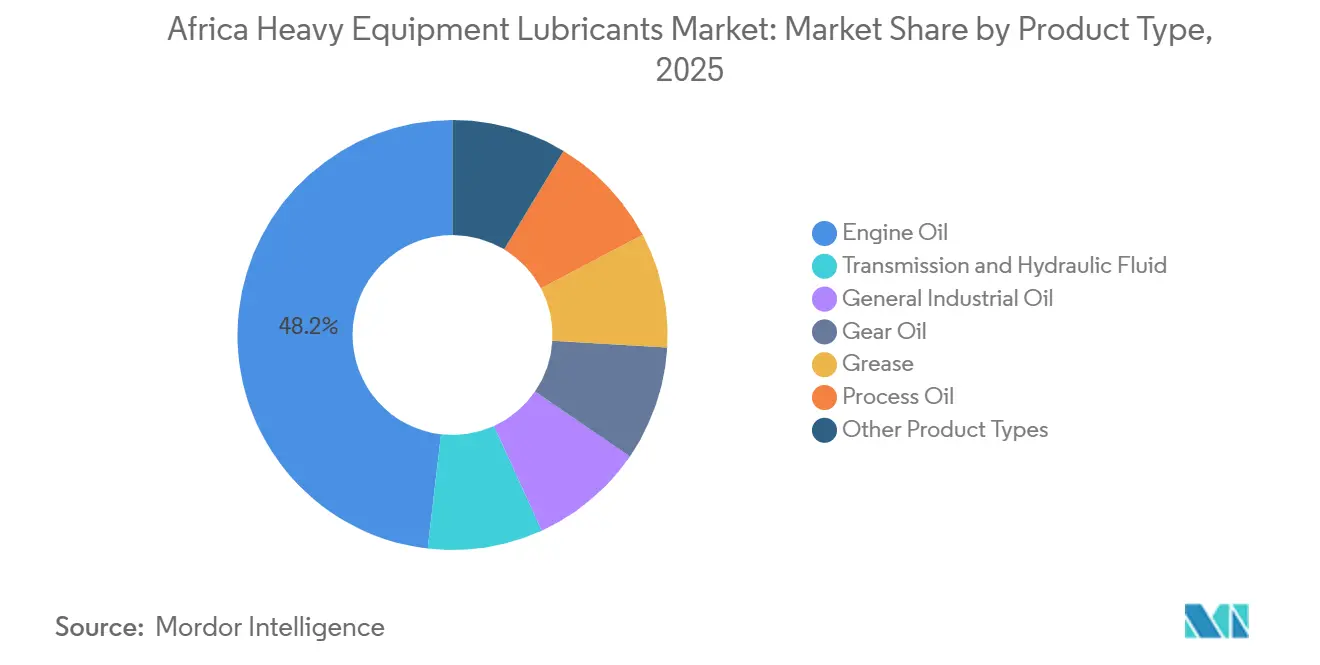

- By product type, engine oil led with a 48.17% Africa heavy equipment lubricants market share in 2025, whereas synthetic engine oil is forecast to expand at a 6.80% CAGR through 2031.

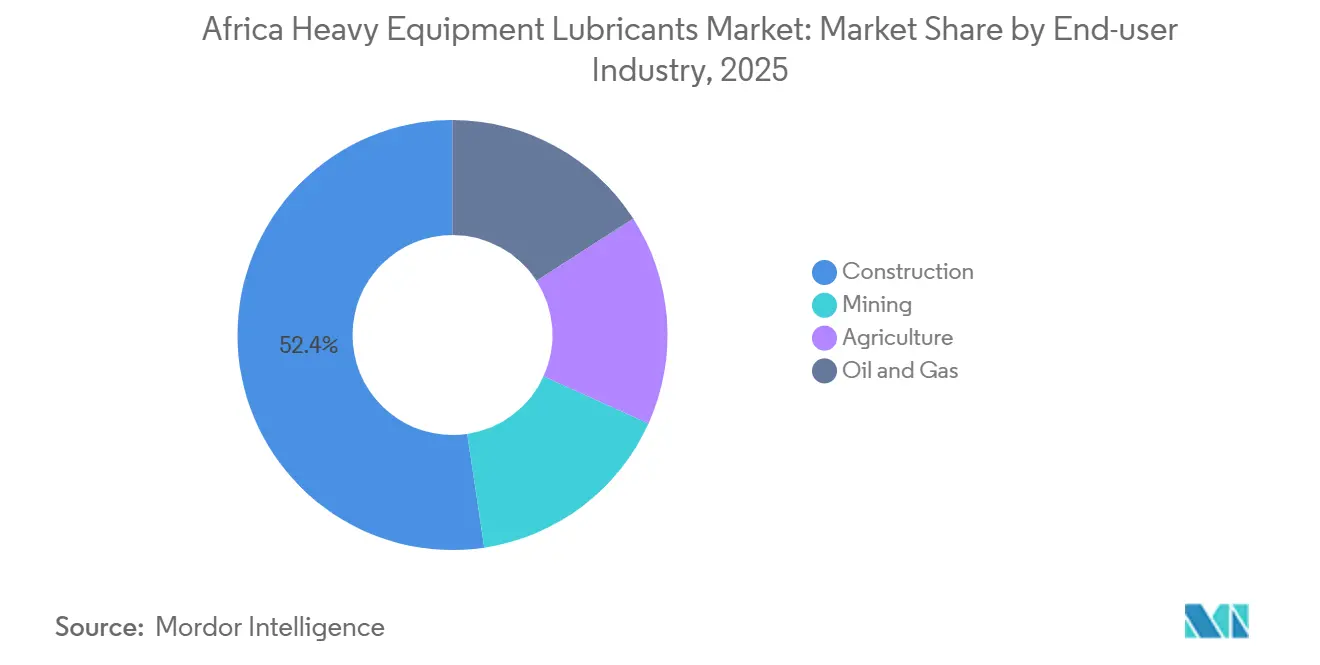

- By end-user industry, construction commanded 52.37% of 2025 volume, while agriculture is projected to post the fastest 7.50% CAGR to 2031, buoyed by tractor-finance schemes and irrigation build-outs.

- By geography, Egypt contributed 34.47% of regional demand in 2025; Nigeria is the fastest-growing country and is set to deliver a 6.20% CAGR through 2031 as local base-oil output from Dangote Refinery tightens the supply–consumption loop.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Africa Heavy Equipment Lubricants Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising construction-sector spend | +1.2% | Egypt, South Africa, Nigeria, Ghana, Algeria | Medium term (2–4 years) |

| Expansion of mining activities | +1.5% | DRC, Zambia, Guinea, South Africa, Zimbabwe, others | Long term (≥ 4 years) |

| Rapid mechanization in African agriculture | +0.8% | Ethiopia, Kenya, Nigeria, Ghana, Rest of Africa | Long term (≥ 4 years) |

| Mandatory oil-analysis clauses in tenders | +0.4% | South Africa, Kenya, Zimbabwe, Nigeria | Short term (≤ 2 years) |

| Growth of predictive-maintenance telematics | +0.3% | South Africa, DRC, Zambia, Guinea, Egypt | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Rising Construction-Sector Spend Across Africa

Infrastructure investments in Africa have surged, focusing on roads, railways, and ambitious urban projects. These initiatives are heavily reliant on high-hour fleets, leading to increased lubricant usage at each site[1]Africa Finance Corporation, “Infrastructure Investment Pipeline,” africafc.org. In Egypt's Toshka agricultural expansion, Volvo EC300D and A45G units run for extended hours daily. Given the abrasive desert conditions, there's a heightened demand for high-viscosity-index hydraulic fluids. Ghana's District Road Improvement Program, which welcomed LiuGong machines in 2024, saw an immediate uptick in local engine oil consumption. Algeria's Western Mining Railway, a project under construction since 2024, has introduced a dedicated sleeper plant, further driving lubricant needs for rail-construction machinery. Mota-Engil's recent acquisition of Liebherr rail excavators for the Kano–Maradi line highlights a growing demand for specialty greases, essential for safeguarding dual road-rail systems. These expansive programs not only signify a commitment to national capital plans but also ensure a sustained demand for lubricants in Africa's heavy equipment market.

Expansion of Mining Activities and Commodity Upswing

Mining expansion emerges as the primary driver for the Africa heavy equipment lubricants market's CAGR. In Guinea, the Simandou project has placed orders for Komatsu PC5500-11 excavators and XCMG dumpers, establishing a strong demand for engine oils, hydraulic fluids, and EP greases. Algeria's Gara Djebilet mine secures lubricant volumes for both its mining operations and rail rolling stock. In March 2025, South Africa's Mogalakwena introduced the continent's inaugural Komatsu P&H 4800XPC shovel, a hefty unit, with its slewing bearings dependent on premium calcium-sulfonate grease. With commodity prices for copper and lithium stabilizing above long-term averages, capital expenditures and equipment utilization remain robust, subsequently bolstering lubricant throughput. Concurrently, DRC, Zambia, Zimbabwe, and Madagascar are ramping up their output of battery metals, expanding the geographical reach of mining-driven lubricant demand.

Rapid Mechanisation in African Agriculture

Government subsidies and donor initiatives are boosting tractor density from a modest starting point, leading to significant growth in lubricant demand. Under the Rural Connectivity for Food Security Program, Ethiopia has invested in a fleet that includes graders, rollers, and loaders. Each of these machines requires engine oil and hydraulic fluid and has multiple grease points. In Kenya, the Swak Dam project operates XCMG excavators extensively, increasing the frequency of oil drainage. While Sub-Saharan Africa boasts a lower tractor density compared to Europe, this highlights the potential for lubricant market growth. Nigeria's push for mechanization, alongside Ghana's "Planting for Food and Jobs" initiative, is energizing dealer networks. These networks are now stocking OEM-approved UTTO and 15W-40 grades, broadening the retail landscape for heavy equipment lubricants in Africa. Distributors, aiming to meet rural demand surges during harvest seasons, face supply chain challenges but ultimately boost total sales.

Mandatory Oil-Analysis Clauses in Government Fleet Tenders

South Africa’s 36-month RT23-2025 tender obliges bidders to sample and lab-test lubricants, formalizing condition monitoring as a procurement prerequisite. Kenya’s transport guidelines set similar thresholds, while Zimbabwean municipal fleets now embed oil sampling in quarterly maintenance contracts. These clauses push buyers toward premium CK-4 and E9 formulations that tolerate extended drains, amplify technical-service revenues, and raise entry barriers against low-cost imports. Suppliers leveraging oil-analysis portals gain stickiness as lab data integrate with fleet-management platforms, shaping reorder schedules. The Africa heavy equipment lubricants market thus pivots from pure product sales toward data-enabled maintenance partnerships.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Counterfeit and sub-standard lubricants | −0.6% | Tanzania, Nigeria, Kenya, Ghana, Rest of Africa | Short term (≤ 2 years) |

| Global Group I base-oil rationalisation | −0.5% | Global, acute in Nigeria, Egypt, South Africa | Medium term (2–4 years) |

| Chronic grid instability | −0.4% | Nigeria, Ghana, Zambia, Zimbabwe, DRC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Counterfeit and Sub-Standard Lubricant Prevalence

Tanzania’s January 2025 warning underscored the scale of fake products that fail to meet API or ACEA specs, causing premature wear and voiding OEM warranties. Despite strict Petroleum Lubricant Operations Rules, limited rural enforcement enables illicit trade in Nigeria and Kenya. Puma Energy’s tamper-evident packaging and hologram authentication fight back, yet brand owners still fund raids, consumer education, and blockchain pilots, adding compliance costs. The drag is most acute over 2025-2027, after which harmonized AfCFTA standards are expected to tighten border checks and shrink counterfeit supply.

Global Group I Base-Oil Rationalisation Driving Price Spikes

Group I capacity has been on a downward trajectory, dropping significantly over the years, with projections indicating a continued decline by 2030. This decline is poised to curtail supplies for converters of conventional heavy-duty engine oils. Import-reliant markets like Nigeria now grapple with steeper premiums, largely due to freight inflation. While Dangote Refinery's base-oil slate is set to alleviate local shortages after 2028, exporters in the interim face a dilemma: pivot to Group II feedstocks or hike prices, a move that could strain smaller blenders. Ghana's Jomoro hub, currently in Phase 1, won't see any barrel additions until 2036[2]Robert Brelsford, “Ghana breaks ground on downstream petroleum hub,” ogj.com. Consequently, the African heavy equipment lubricants market is rapidly shifting towards synthetic alternatives.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Synthetics Gain Share as Drain Intervals Extend

Engine oil accounted for 48.17% of the Africa heavy equipment lubricants market size in 2025, underpinned by diesel-powered earthmovers, haul trucks, and generators. Synthetic engine oil is tracking a 6.80% CAGR to 2031 as high ambient temperatures and dust accelerate oxidation, pushing fleets toward Group II/III formulations. At Dangote Refinery, XCMG XE470D excavators routinely clock extensive operating hours each day. To protect their turbochargers, these excavators rely on premium CK-4 oils, chosen for their elevated viscosity index. Meanwhile, at Egypt's Toshka site, Volvo EC480D units, equipped with advanced electro-hydraulic systems, depend on transmission and hydraulic fluids. These fluids, the second-largest segment in the market, are selected for their anti-wear additives and robust oxidation resistance. Lastly, on Komatsu's P&H 4800XPC rope shovel, which operates in continuous shifts, gear oils and greases play a crucial role. They safeguard the machine's final drives and slewing bearings.

In a move highlighting the evolving supply chain, Chevron has teamed up with Gapuma to distribute Group II base oils in Nigeria. This partnership underscores the synthetic growth trend in the region. Meanwhile, audits from Puma Energy's Total Fluid Management reveal that longer drain intervals lead to significant cost savings. This finding is driving a shift towards higher-value fluid formulations. Retail visibility for these premium products is on the rise. For instance, Makro South Africa now offers synthetic packs from brands like Castrol, Engen, and Total. This pricing strategy makes premium lubricants more accessible to smaller contractors. Consequently, the forecast suggests a steady annual increase in the market share of synthetic lubricants, bolstering the Africa heavy equipment lubricants market's emphasis on value over volume.

By End-User Industry: Agriculture Outpaces Construction in Growth Rate

Construction absorbed 52.37% of the 2025 volume, reflecting the sector’s equipment intensity across road, rail, and urban projects. Mining follows but agriculture, aided by subsidy programs and donor finance, shows the fastest 7.50% CAGR to 2031.

In Ethiopia, a fleet of vehicles is ensuring a consistent supply of 15W-40 engine oils and UTTO products to rural depots. Meanwhile, in Kenya, Swak Dam's near-constant operation of excavators and pumps is driving up lubricant consumption for irrigation. The mining sector plays a crucial role, exemplified by the use of hydraulic and engine oils in heavy machinery at Simandou. Although smaller in volume, the oil and gas sector commands a higher value, necessitating turbine and compressor oils that adhere to stringent API specifications, especially for refinery constructions like Dangote's ambitious expansion.

Geography Analysis

Egypt delivered 34.47% of Africa's heavy equipment lubricants market size in 2025, driven by the Toshka agricultural megaproject and the New Ras el-Hekma coastal city that together employ thousands of excavators, haulers, and road machines. South Africa remains pivotal as platinum operations deploy ultra-class shovels and introduce predictive-maintenance regimes that favor premium synthetics. Nigeria, the fastest-growing geography at 6.20% CAGR, links refinery construction with in-country base-oil production, shortening logistics chains and supporting local blending at competitive cost.

Algeria’s Western Mining Railway and the Gara Djebilet iron-ore project signal long-run lubricant consumption anchored in bulk earthworks and heavy haulage. Morocco benefits from Chevron’s wider Afriquia partnership that expands coastal depot capacity, although absolute volumes trail Egypt and Algeria. In the rest of Africa cluster, Guinea’s Simandou complex and Zambia’s revised fuel-quality rules stand out: both require high-quality lubricants and traceability, raising the compliance bar. Tanzania’s enforcement gap keeps counterfeit risk elevated, dampening legitimate sales even as tractor density rises. Across the continent, Puma Energy’s station footprint and Vivo Energy’s station platform underpin route-to-market scale and enable cross-border fleet supply, centralising procurement for international contractors.

Competitive Landscape

The Africa heavy equipment lubricants market is moderately consolidated. Multinational majors anchor the Africa heavy equipment lubricants market through coastal import terminals and inland depots, while regional brands leverage local blending to win last-mile business. Chinese equipment OEMs increasingly supply lubricants alongside machinery, opening spare-parts centers. Compliance capability is another moat; Tanzania’s strict testing rules and Zambia’s fuel-marking drive favor majors that can finance labs and traceability, sidelining smaller traders. Overall rivalry remains moderate, with consolidation and service bundling tempering price wars.

Africa Heavy Equipment Lubricants Industry Leaders

Shell PLC

TotalEnergies

BP PLC

Exxon Mobil Corporation

FUCH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: BP PLC began exploring sale options for its Castrol lubricants division, valued at up to USD 10 billion, as part of a broader USD 20 billion divestment roadmap targeting completion by 2027.

- February 2025: FUCHS inaugurated a EUR 26 million capacity expansion at its Isando, Johannesburg plant, reinforcing supply to automotive, mining, and specialty sectors across Southern Africa.

Africa Heavy Equipment Lubricants Market Report Scope

Heavy equipment lubricants, tailored for large machinery such as excavators and bulldozers, play a pivotal role in reducing friction, wear, and heat. Beyond these primary functions, they also cool, clean, seal, and protect essential components from corrosion, especially in challenging conditions. This ensures not only smooth operation but also extends the machinery's lifespan and minimizes downtime across sectors like construction, mining, and agriculture. Unlike general-purpose lubricants, these specialized oils and greases are fortified with additives for extreme pressure (EP) and thermal stability, making them indispensable in high-load and high-temperature environments.

The Africa heavy equipment lubricants market is segmented by product type, end-user industry, and geography. By product type, the market is segmented into engine oil, transmission and hydraulic fluid, general industrial oil, gear oil, grease, process oil, and other product types. By end-user industry, the market is segmented into construction, mining, agriculture, and oil and gas. The report also covers the market size and forecasts for the Africa heavy equipment lubricants market in five countries across the region. For each segment, the market sizing and forecasts have been done based on volume (Litres).

By Product Type

| Engine Oil |

| Transmission and Hydraulic Fluid |

| General Industrial Oil |

| Gear Oil |

| Grease |

| Process Oil |

| Other Product Types |

By End-user Industry

| Construction |

| Mining |

| Agriculture |

| Oil and Gas |

By Geography

| Egypt |

| South Africa |

| Nigeria |

| Algeria |

| Morocco |

| Rest of Africa |

| By Product Type | Engine Oil |

| Transmission and Hydraulic Fluid | |

| General Industrial Oil | |

| Gear Oil | |

| Grease | |

| Process Oil | |

| Other Product Types | |

| By End-user Industry | Construction |

| Mining | |

| Agriculture | |

| Oil and Gas | |

| By Geography | Egypt |

| South Africa | |

| Nigeria | |

| Algeria | |

| Morocco | |

| Rest of Africa |

Key Questions Answered in the Report

What is the forecast volume for Africa’s heavy equipment lubricant demand by 2031?

The market is expected to reach 545.42 million liters by 2031, from 435.65 million liters in 2026, reflecting a 4.60% CAGR.

Which country is projected to grow fastest in lubricant consumption?

Nigeria, driven by the Dangote Refinery build-out, is forecast at a 6.20% CAGR through 2031.

Which product type holds the largest share?

Engine oil led with 48.17% of the 2025 volume.

Why are synthetics gaining popularity?

High ambient temperatures and longer drain-interval targets push fleets toward Group II/III formulations.

Which end-user segment is expanding quickest?

Agriculture, supported by mechanization programs, is slated for a 7.50% CAGR.

How are suppliers differentiating?

Service bundling, predictive-maintenance analytics, and compliance with stricter quality regulations are key levers.

Page last updated on: