Business-Process-as-a-Service Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 88.04 Billion |

| Market Size (2031) | USD 154.29 Billion |

| Growth Rate (2026 - 2031) | 11.88% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Business-Process-as-a-Service Market Analysis by Mordor Intelligence

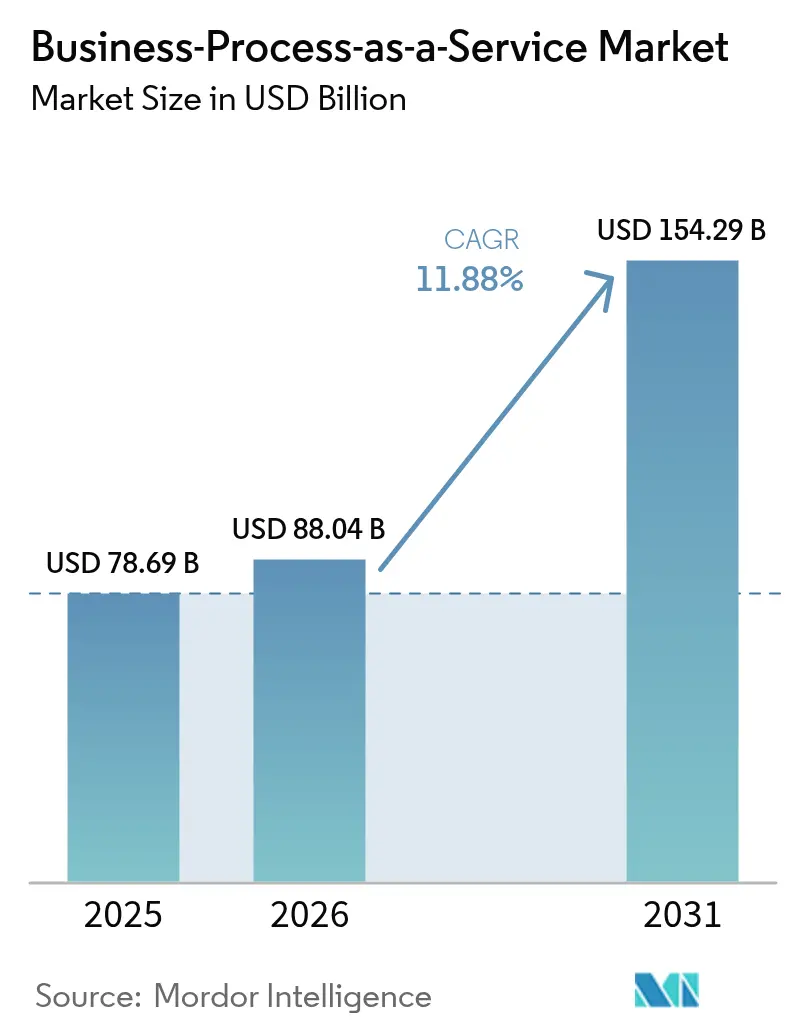

The Business-Process-as-a-Service market size is expected to grow from USD 78.69 billion in 2025 to USD 88.04 billion in 2026 and is forecast to reach USD 154.29 billion by 2031 at 11.88% CAGR over 2026-2031.

Accelerating adoption of cloud-native delivery models, rapid progress in artificial intelligence, and stronger regulatory pressure for resilient operations are reshaping organizational strategies. Enterprises are converting fixed costs into variable outlays while gaining immediate access to advanced automation, analytics, and industry-specific best practices—capabilities that once required years of capital investment. Intensifying focus on operational resilience after recent supply-chain disruptions has further positioned BPaaS as a preferred route for standardized processes that scale globally yet remain locally compliant. Vendors are responding through outcome-based commercial models, sovereign-cloud options, and ESG-linked process bundles, all of which deepen the strategic role of the Business-Process-as-a-Service market in digital transformation programs.

Key Report Takeaways

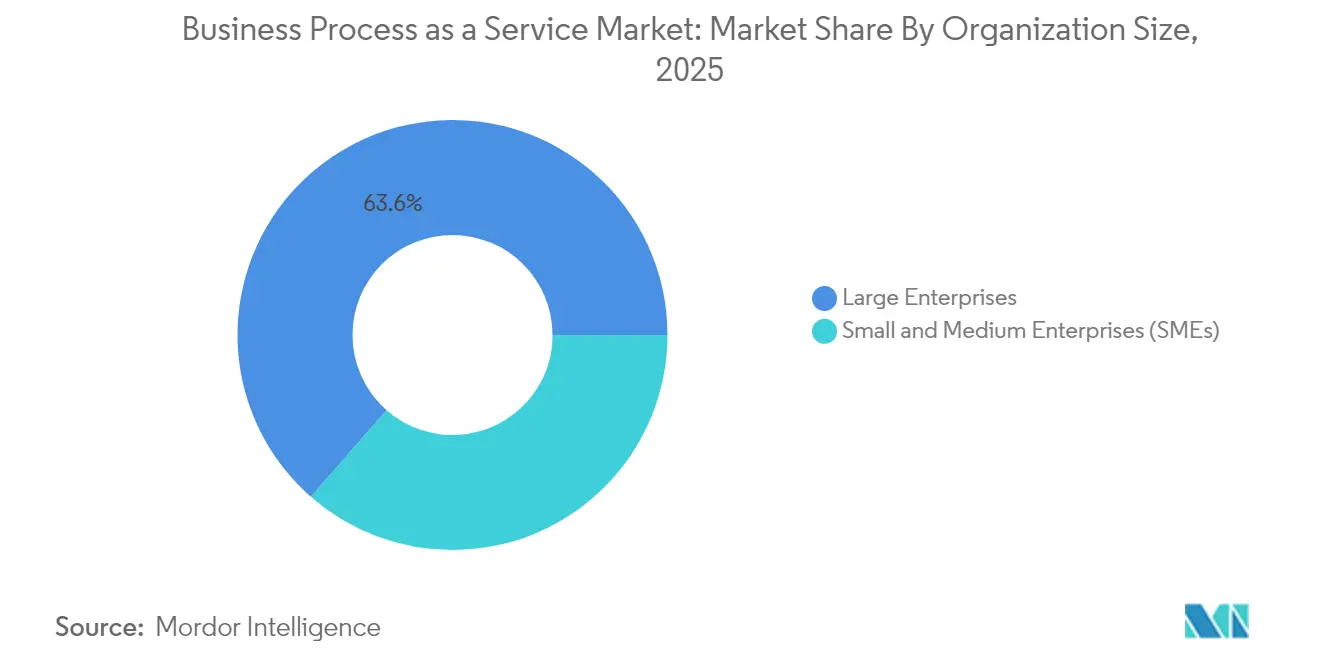

- By organization size, Large Enterprises accounted for 63.55% of the Business-Process-as-a-Service market share in 2025, while SMEs are projected to expand at a 12.97% CAGR through 2031.

- By process, Human Resource Management led with 23.85% revenue share in 2025; Customer Service and Support is expected to post the fastest 14.34% CAGR to 2031.

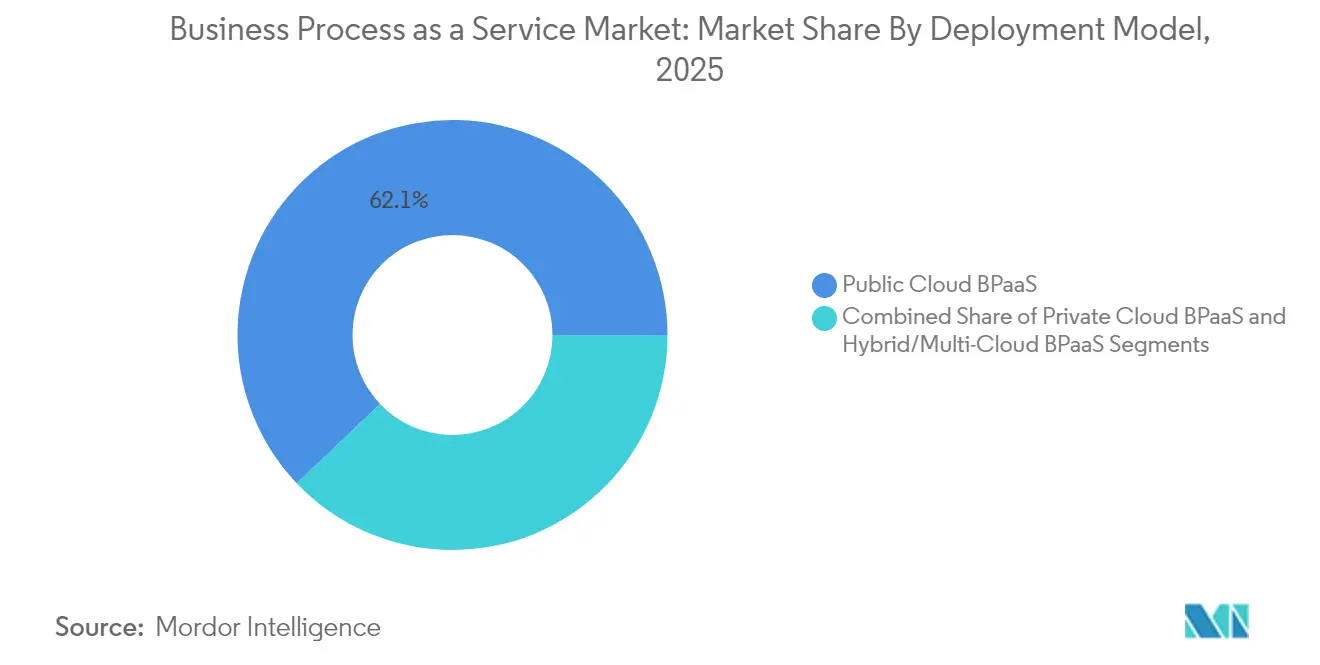

- By deployment model, Public Cloud captured 62.10% of the Business-Process-as-a-Service market size in 2025, whereas Hybrid/Multi-Cloud is set to grow at a 14.53% CAGR.

- By end-user industry, BFSI commanded 23.45% share of the Business-Process-as-a-Service market size in 2025; Healthcare and Life Sciences is anticipated to rise at a 13.95% CAGR.

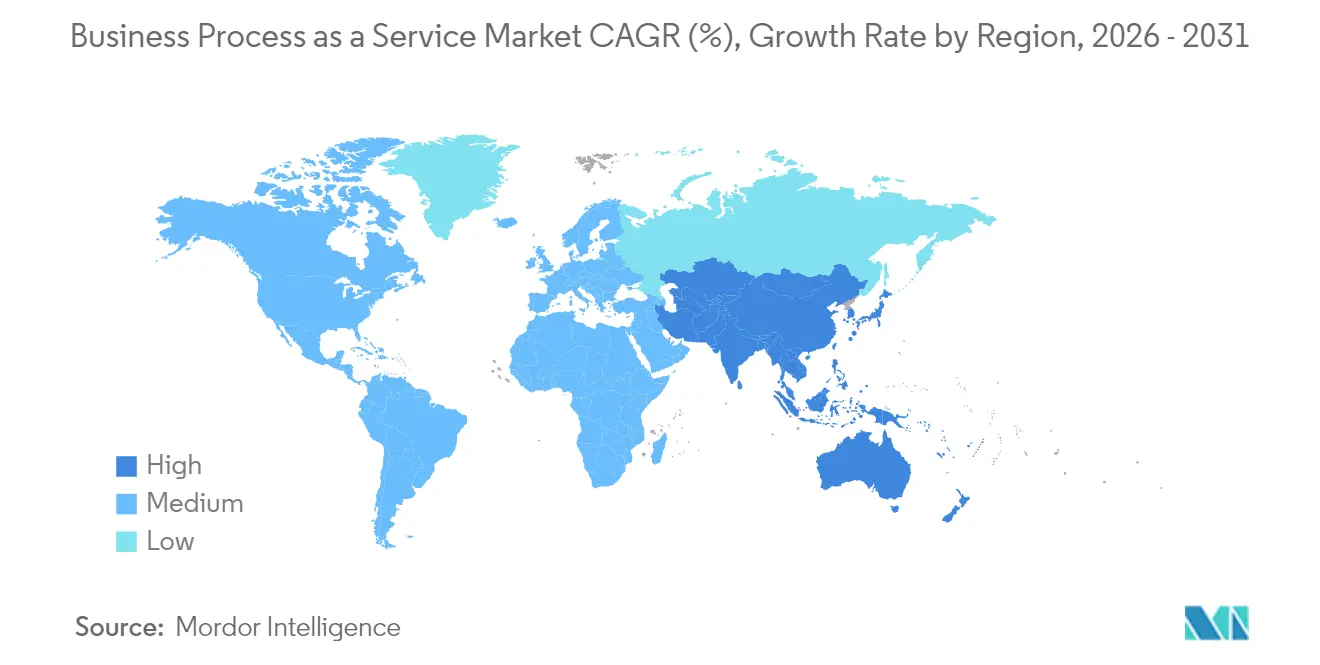

- By geography, North America led with 40.85% revenue share in 2025, and Asia-Pacific is forecast to record the highest 12.62% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Business-Process-as-a-Service Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for cloud services and standardized processes | +3.5% | Global, higher impact in North America and Europe | Medium term (2-4 years) |

| Need to reduce operational cost and boost productivity | +2.2% | Global, significant impact in Asia-Pacific | Short term (≤ 2 years) |

| Rapid adoption of AI / hyper-automation in BPaaS | +2.1% | North America, Europe, developed APAC | Medium term (2-4 years) |

| Expansion of outcome-based (gain-share) BPaaS pricing models | +1.8% | North America, Europe | Medium term (2-4 years) |

| ESG-linked reporting mandates driving sustainability BPaaS | +1.2% | Europe, North America, gradual APAC uptake | Long term (≥ 4 years) |

| Demand for industry-specific BPaaS solutions | +1.0% | Global, strongest in regulated verticals | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Cloud Services and Standardized Processes

Universal migration toward cloud platforms underpins large-scale process standardization. Ninety-four percent of enterprises now leverage cloud solutions to streamline workflows, shorten deployment cycles, and ensure consistent governance. Elastic resource allocation supports rapid pivots in demand without forcing new capital decisions. IBM notes that 77% of firms already run hybrid architectures, enabling them to unify core processes over multiple clouds while keeping strategic workloads in preferred jurisdictions. [1]IBM Corporation, “Public Cloud vs. Private Cloud vs. Hybrid Cloud,” ibm.com Standardized, cloud-native modules accelerate compliance tasks in banking and insurance, where uniform audit trails are essential. As a result, the Business-Process-as-a-Service market experiences sustained multi-year momentum across sectors that demand speed, resilience, and global reach.

Need to Reduce Operational Cost and Boost Productivity

Economic headwinds intensify pressure to replace fixed costs with consumption-based models. BPaaS converts multi-year license contracts, data-center depreciation, and labor overhead into variable fees that align with actual usage. DXC Technology reports savings of 20-30% when organizations shift from traditional outsourcing to BPaaS frameworks. [2]DXC Technology, “Modern Business Processes: Delivered as a Service and Measured by Business Outcomes,” dxc.com Process automation embedded in these services delivers additional productivity gains, with some enterprises citing 40% efficiency improvements in finance back-office tasks. These combined financial and operational benefits reinforce the Business-Process-as-a-Service market as a pragmatic lever for near-term profitability and long-term competitiveness.

Rapid Adoption of AI / Hyper-automation in BPaaS

Providers now integrate predictive analytics, natural language tools, and machine learning into core process flows. Cognizant’s USD 1 billion generative-AI program exemplifies the scale of investment aimed at raising automation to near-straight-through levels while generating high-quality insights. [3]Cognizant, “Life and Annuities Insurance BPS PEAK Matrix Assessment 2025,” cognizant.com In live deployments, straight-through processing surpasses 98% for selected insurance tasks, sharply lowering rework and compliance exceptions. Intelligent orchestration further improves service-level adherence, ensuring that the Business-Process-as-a-Service market evolves from transactional outsourcing to an engine of continuous optimization.

Expansion of Outcome-based (Gain-share) BPaaS Pricing Models

Outcome-based contracts tie provider revenue directly to cost savings, revenue gains, or compliance milestones. Infosys BPM highlights the suitability of these models for high-volume finance processes where key performance indicators can be audited in real time. [4]Infosys BPM, “The Shift Toward Next-Gen Business Services,” infosysbpm.com Shared-value structures intensify collaboration, spark quicker innovation cycles, and embed continuous-improvement mindsets. As a result, more enterprises prefer gain-share agreements, propelling sustained growth for the Business-Process-as-a-Service market during medium-term planning horizons.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Heightened data-security and privacy concerns | -2.2% | Global, higher impact in Europe and North America | Short term (≤ 2 years) |

| Integration complexity with legacy core systems | -1.8% | Global, significant in mature markets | Medium term (2-4 years) |

| Vendor lock-in and interoperability limitations | -1.3% | Global | Medium term (2-4 years) |

| Sovereign-cloud requirements restricting cross-border BPaaS | -1.2% | Europe, Asia-Pacific, rising in North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Heightened Data-Security and Privacy Concerns

BPaaS deployments involve a distributed infrastructure that can enlarge the threat surface. The South African Reserve Bank cautions that cloud computing amplifies operational and systemic risks when controls are weak. European GDPR and California CCPA regulations impose severe penalties for non-compliance, compelling providers to implement sophisticated encryption, identity management, and regional data-residency architectures. Heightened scrutiny temporarily slows decision cycles, limiting short-term adoption in sensitive verticals even as security-enhanced platforms emerge to rebuild trust in the Business-Process-as-a-Service market.

Integration Complexity with Legacy Core Systems

Many enterprises operate bespoke mainframes and fragmented application estates accumulated over decades. FasterCapital observes that integrating BPaaS with such environments can extend timelines and raise costs, occasionally eroding anticipated value. Data synchronization across hybrid platforms requires robust middleware and governance. Project teams often face unplanned interface redesigns, deep regression testing, and parallel-run overheads. These hurdles moderate uptake among risk-averse organizations, tempering near-term expansion of the Business-Process-as-a-Service market until integration toolkits mature.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Organization Size: SMEs Accelerate Digital Transformation

Large Enterprises dominated 2025 with 63.55% of the Business-Process-as-a-Service market share, leveraging standardized global workflows to simplify audits and cut duplicative platforms. They often start by outsourcing non-core finance and HR tasks, then extend coverage to customer experience and supply-chain analytics once governance structures prove resilient. Integration remains a priority; many deploy middleware layers that blend on-premise ERPs with public-cloud microservices, preserving strategic data control while maximizing vendor innovation. In parallel, fresh enterprise-wide governance councils monitor vendor performance under outcome-based contracts, ensuring continuous alignment with strategic objectives.

SMEs, though historically under-represented, now display the strongest momentum with a forecast 12.97% CAGR. Cloud-first solutions remove traditional barriers such as capital outlay, specialist talent shortages, and infrastructure maintenance. Japan’s Kubell Co. reports that its Chatwork platform served 605,000 SME clients by September 2024, underscoring the segment’s pent-up demand. SMEs typically begin with single-process modules—payroll, invoicing, or help-desk automation—before scaling to end-to-end suites as reliability is proven. The elastic fee model offers crucial cash-flow flexibility during growth spurts or economic contractions. Consequently, the Business-Process-as-a-Service market size attributable to SMEs is projected to widen substantially through 2031 as providers release pre-configured bundles tailored for industry-specific compliance.

By Process: Customer Service Innovations Drive Growth

Human Resource Management retained 23.85% of 2025 revenue, reflecting global recognition that standardized recruitment, payroll, and talent-engagement workflows lower compliance risk and enhance employee experience. Many providers now pair HR modules with predictive analytics that forecast attrition, identify skill gaps, and recommend learning content. Accounting and Finance processes also gain traction as robotic invoice matching, automated reconciliations, and AI-driven fraud checks boost accuracy while shrinking cycle times. Supply Chain and Procurement solutions improve vendor collaboration and inventory visibility, critical in volatile logistics environments.

Customer Service and Support, forecast to rise 14.34% annually, leads growth as brands pivot to omnichannel engagement. AI-driven chatbots and voice analytics deliver instant, personalized responses at far lower cost than traditional call centers. Sutherland Global’s deployments cut average response time while raising first-contact resolution, enhancing NPS scores, and reducing escalations. Sales and Marketing BPaaS complements these advances, synchronizing campaign data with front-office analytics to sharpen lead quality. Operations modules apply workflow engines to field-service dispatch, plant-maintenance scheduling, and quality assurance. Together, these innovations anchor sustained expansion of the Business-Process-as-a-Service market.

By Deployment Model: Hybrid Approaches Balance Flexibility and Control

Public Cloud commanded 62.10% of the Business-Process-as-a-Service market size in 2025, thanks to ready availability, frequent feature releases, and transparent cost models. Enterprises benefit from instant scalability during peak periods such as holiday retail surges or fiscal close cycles. Providers supplement offerings with enterprise-grade encryption and multi-factor authentication that satisfy baseline compliance in most industries. However, exclusive public-cloud reliance can conflict with data-sovereignty laws and internal risk appetites.

Hybrid/Multi-Cloud solutions, projected to grow 14.53% per year, address these concerns by enabling sensitive data to remain within private or sovereign facilities while offloading less regulated workloads to public infrastructure. TAdviser reports that 85% of Russian firms plan to adopt hybrid technology by 2025. Logical segmentation of workloads allows firms to optimize for latency, regulation, and economics simultaneously. Private Cloud BPaaS retains relevance in healthcare and banking environments where regulators stipulate explicit residency controls. The overall mix confirms that strategic balance rather than one-size-fits-all adoption will fuel the Business-Process-as-a-Service market through the decade.

By End-user Industry: Healthcare Digitalization Accelerates Adoption

BFSI led with 23.45% of 2025 revenue, motivated by intense regulatory scrutiny that rewards auditable, standardized processes. Banks deploy BPaaS for anti-money-laundering checks, loan-origination analytics, and real-time ledger reconciliation. Insurance carriers employ digital claims adjudication and policy-administration platforms to compress cycle times and elevate customer satisfaction. Providers embed rule engines to reflect multi-jurisdictional compliance, making the Business-Process-as-a-Service market indispensable to financial risk management.

Healthcare and Life Sciences, forecast at a 13.95% CAGR, exemplify next-wave demand. Cognizant’s payer solution slashed total cost of ownership by 25% while raising claims-pricing accuracy to 99%+. Automated pre-authorization, member-eligibility verification, and provider credentialing alleviate administrative bottlenecks and redirect resources to patient care. IT and Telecommunications firms deploy BPaaS to unify OSS/BSS processes and customer-support journeys. Retail and eCommerce leverage automated supply-chain orchestration to mitigate stock-out risk. Manufacturing integrates quality analytics and predictive maintenance into unified dashboards. Government entities modernize HR and citizen-service channels as 60% of public-sector staff edge toward retirement eligibility, demonstrating the Business-Process-as-a-Service industry’s cross-sector value.

Geography Analysis

North America generated 40.85% of 2025 revenue for the Business-Process-as-a-Service market, buoyed by early cloud uptake and deep provider ecosystems. Financial institutions use BPaaS to consolidate compliance documentation across jurisdictions, while retail groups pursue AI-led customer-service automation. Cloud infrastructure concentration is notable; the UK Competition and Markets Authority estimates AWS and Microsoft hold 40-50% and 30-40% of North American infrastructure, respectively. This dominance encourages BPaaS vendors to forge strategic alliances with hyperscalers for latency optimization and joint go-to-market programs.

Asia-Pacific is projected to record the fastest 12.62% CAGR between 2026 and 2031. Governments in India, the Philippines, and Indonesia promote “cloud first” mandates to reduce operating costs and improve citizen services. The Data Security Council of India notes that the national cloud market reached USD 7.70 billion by 2022, underscoring the readiness of foundational infrastructure. Indigenous providers partner with global players to address regional data-localization requirements. Japanese enterprises, challenged by labor shortages, lean on BPaaS to automate routine functions, stimulating demand across manufacturing and retail sectors.

Europe exhibits measured growth as stringent privacy rules guide deployment choices. GDPR compliance shapes contract terms, data-residency clauses, and shared-responsibility frameworks. Germany’s BPO market, forecast to hit USD 21.32 billion by 2029, already registers 81% cloud adoption among firms. Financial institutions prefer hybrid models, pairing local sovereign clouds with scalable public resources to satisfy supervisory guidance outlined by Eurofi. The region’s strong ESG agenda fuels demand for sustainability-centric BPaaS solutions that automate carbon accounting and social-impact reporting.

Competitive Landscape

The Business-Process-as-a-Service market displays moderate concentration anchored by Accenture, IBM, TCS, and Cognizant, each leveraging global delivery centers, verticalized solution portfolios, and heavy AI investment. Accenture’s USD 420 million acquisition of a sustainability analytics firm in April 2025 expanded its ESG credentials and strengthened cross-industry traction. IBM’s March 2025 launch of an AI-powered financial-services BPaaS suite fused compliance workflows with cognitive risk analytics, giving banks a turnkey option for multi-jurisdiction operations.

Mid-tier challengers include Wipro, HCLTech, and NTT DATA, which differentiate through regional expertise and niche platforms. NTT DATA’s SimpliZCloud, introduced in January 2025, caters to sovereign-cloud requirements, highlighting growing segmentation along regulatory lines. Specialist vendors such as Sutherland Global dominate customer-experience processes, while Genpact deepens finance-automation capabilities after its February 2025 acquisition of a robotic-process specialist.

Strategic alliances shape competition: Infosys BPM partnered in May 2025 with a leading workflow-automation platform to release pre-configured templates, accelerating deployment speed and extending reach to SMEs. Provider success increasingly depends on ecosystem positioning within hyperscaler marketplaces, industry consortiums, and analytics ISVs. Heightened antitrust scrutiny of dominant cloud-infrastructure suppliers may open new corridors for independent BPaaS providers eager to bundle services across multi-cloud environments.

Business-Process-as-a-Service Industry Leaders

Accenture plc

IBM Corporation

Tata Consultancy Services (TCS)

Cognizant Technology Solutions

Wipro Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Infosys BPM partnered with a workflow-automation platform to broaden end-to-end BPaaS delivery.

- April 2025: Sutherland Global upgraded its healthcare payer BPaaS with new AI capabilities aimed at cutting claims-processing costs.

- April 2025: Accenture acquired a sustainability analytics firm for USD 420 million to bolster ESG-oriented BPaaS services.

- March 2025: TCS introduced a sustainability-focused BPaaS solution that helps organizations monitor and report ESG metrics.

- March 2025: IBM launched an AI-powered BPaaS platform for financial services that combines process automation with compliance analytics.

- February 2025: HCLTech launched an enhanced HR management BPaaS offering that incorporates generative AI for talent acquisition and engagement.

- February 2025: Cognizant announced a USD 1 billion investment in generative-AI technologies to enhance BPaaS offerings across healthcare and financial services.

- January 2025: Genpact expanded its finance and accounting BPaaS capabilities through the USD 85 million acquisition of a specialized automation provider.

- January 2025: NTT DATA launched SimpliZCloud, a secure platform addressing data-residency mandates in BPaaS deployments.

- November 2024: Wipro secured a USD 300 million BPaaS contract to transform core banking operations for a European institution.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Mordor Intelligence defines the Business-Process-as-a-Service market as all cloud-hosted, multitenant business process solutions, such as payroll, finance, customer support, procurement, and supply-chain tasks, that are delivered on a usage or subscription basis and include the supporting platform, people, and run-time services required for end-to-end process outcomes. These offerings must be consumed remotely over public, private, or hybrid clouds and be priced independently of underlying software licenses.

Scope exclusion: This study removes purely technical platform services (PaaS/iPaaS) or stand-alone SaaS modules that do not include full process delivery.

Segmentation Overview

- By Organization Size

- Large Enterprises

- Small and Medium Enterprises (SMEs)

- By Process

- Human Resource Management (HRM)

- Accounting and Finance

- Customer Service and Support

- Sales and Marketing

- Supply Chain and Procurement

- Operations and Other Horizontal Processes

- By Deployment Model

- Public Cloud BPaaS

- Private Cloud BPaaS

- Hybrid/Multi-Cloud BPaaS

- By End-user Industry

- BFSI

- IT and Telecommunications

- Healthcare and Life Sciences

- Retail and E-Commerce

- Manufacturing

- Government and Public Sector

- Other End-user Industries

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Chile

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Singapore

- Malaysia

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Egypt

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

We held semi-structured interviews and short surveys with procurement heads, cloud architects, and finance controllers across North America, Europe, and key Asia-Pacific economies. Discussions validated spend shares across HR, finance, and customer-experience processes, clarified average contract values for SMEs versus large enterprises, and stress-tested the growth assumptions our team derived from secondary data.

Desk Research

Our analysts started with structured desk work, reviewing government ICT spend dashboards, U.S. SEC 10-Ks of leading service vendors, EU Digital Economy statistics, and trade association white papers such as those from NASSCOM and TechUK. Additional insights on cloud migration rates were gathered from OECD broadband indicators, while patent analytics from Questel highlighted automation intensity within BPaaS workflows. Subscription databases, D&B Hoovers for company financials and Dow Jones Factiva for deal flows, helped us benchmark vendor scale and client adoption. This list is illustrative; many other public and paid sources informed the analysis.

Market-Sizing & Forecasting

The model begins with a top-down reconstruction of global outsourced process spend, broken down by cloud penetration rates, and then is cross-checked with bottom-up roll-ups from 40 sampled vendor revenues and average selling price × user seat calculations. Key variables include cloud adoption ratio, average per-process subscription fee, SME digitalization rate, contract churn, and regional GDP-linked IT budgets. Multivariate regression driven by these variables and informed by expert consensus underpins the 2025-2030 forecast. Scenario analysis adjusts for macro-economic shocks. Data gaps in supplier disclosures were bridged using regional channel checks and normalized against public-sector contract databases.

Data Validation & Update Cycle

Separate analyst pairs review every model for variance against historical trends and peer trackers before sign-off. We refresh figures annually, triggering interim updates whenever mergers, regulation, or economic events move the market materially.

Why Mordor's Business-Process-as-a-Service Baseline Commands Reliability

Estimates from different publishers often diverge because they apply dissimilar scope, currency conversions, and refresh cadences. By anchoring only full-service, outcome-based BPaaS contracts and by updating each year, we minimize guesswork and currency drift.

Key gap drivers include: some studies bundle adjacent PaaS stacks, others use static macro multipliers without vendor cross-checks, and a few publish values on multi-year-old exchange rates. Mordor's blend of live contract data, vendor audits, and yearly refresh narrows these blind spots.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 78.69 B (2025) | Mordor Intelligence | - |

| USD 95.9 B (2025) | Global Consultancy A | Bundles engineering PaaS and analytics services; three-year refresh cycle |

| USD 63.3 B (2023) | Market Publisher B | Excludes mid-tier SaaS-led providers; relies mainly on macro GDP scalars |

Taken together, the comparison shows that our disciplined scope selection and annual data audits provide decision-makers with a balanced, transparent baseline they can trace back to clearly stated variables and repeatable steps.

Key Questions Answered in the Report

What is the projected value of the Business-Process-as-a-Service market by 2031?

The Business-Process-as-a-Service market is forecast to reach USD 154.29 billion in 2031.

Which process segment will grow the fastest through 2031?

Customer Service & Support is expected to register the highest 14.34% CAGR due to AI-driven omnichannel engagement tools.

Why are SMEs adopting BPaaS more rapidly than large enterprises?

SMEs favor BPaaS because it removes large upfront investments, offers pay-as-you-go flexibility, and grants access to enterprise-grade automation without complex infrastructure.

How does hybrid BPaaS help meet data-sovereignty rules?

Hybrid architectures keep sensitive data in controlled private or sovereign clouds while routing less regulated processes to public infrastructure, balancing compliance and scalability.

Which region will see the highest BPaaS growth rate?

Asia-Pacific is projected to expand at a 12.62% CAGR, driven by government cloud mandates, expanding infrastructure, and increasing digitalization in emerging economies.

What are the main risks hindering BPaaS adoption?

Primary risks include data-security concerns under strict privacy regulations and the complexity of integrating cloud services with longstanding legacy systems.

Page last updated on: