Bus Pantograph Charger Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

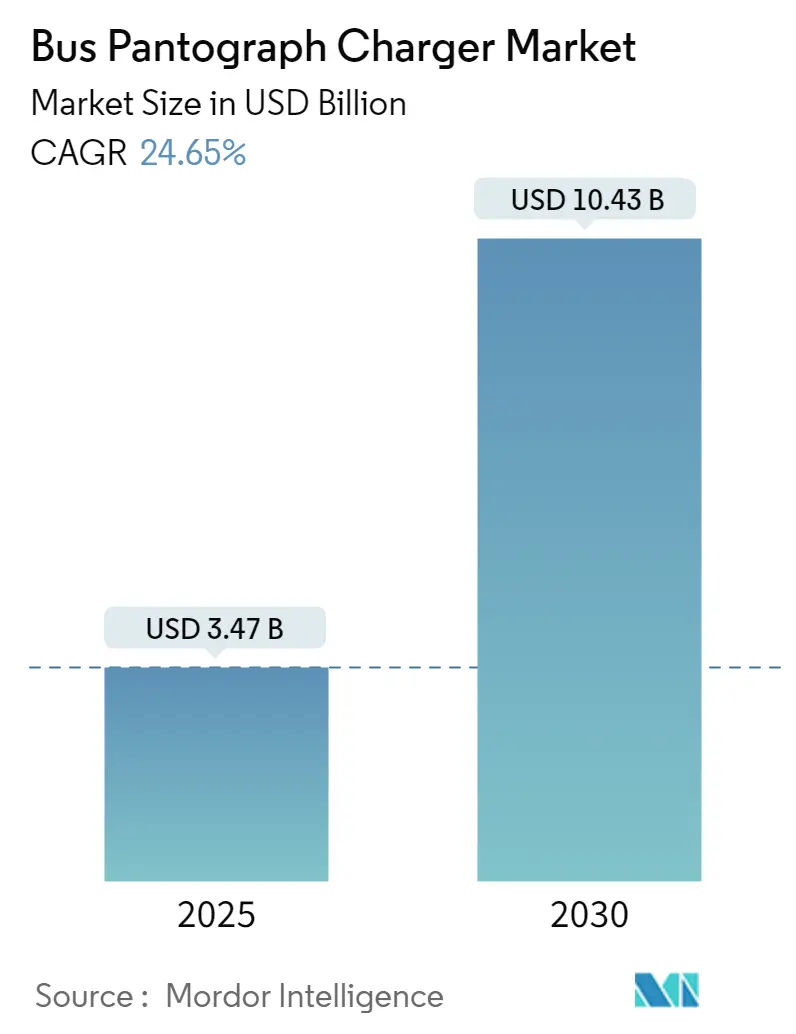

| Market Size (2025) | USD 3.47 Billion |

| Market Size (2030) | USD 10.43 Billion |

| Growth Rate (2025 - 2030) | 24.65% CAGR |

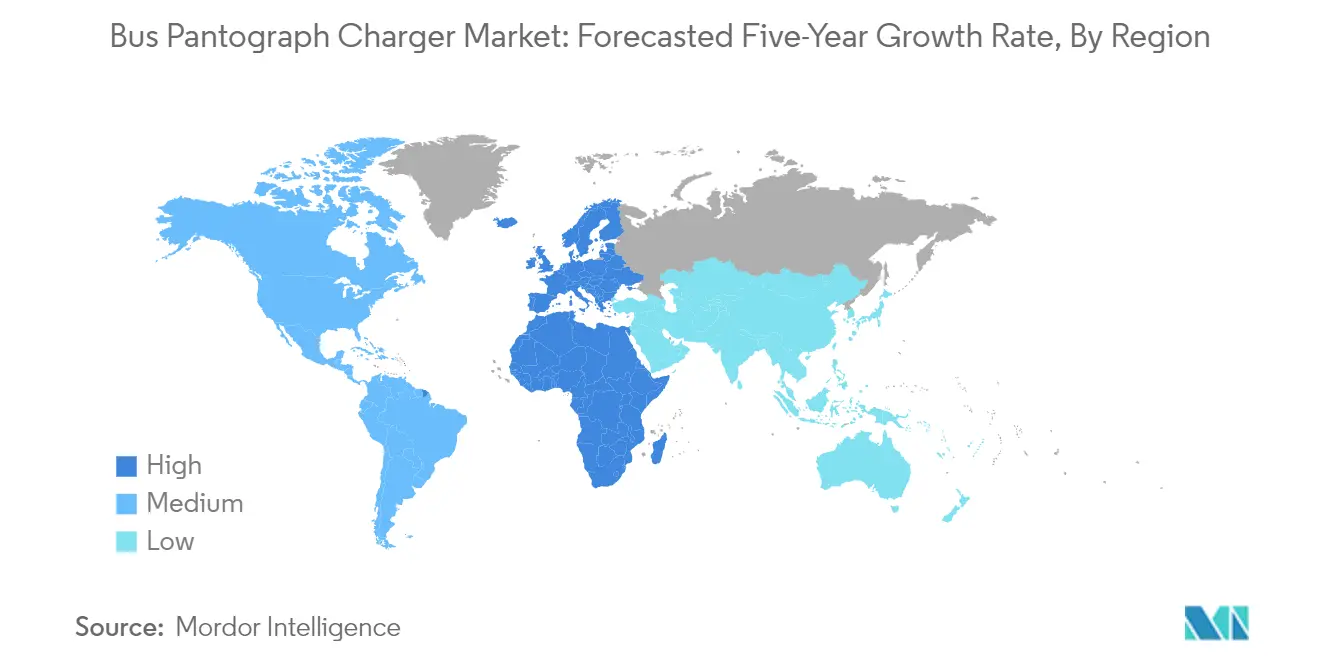

| Fastest Growing Market | Europe |

| Largest Market | North America |

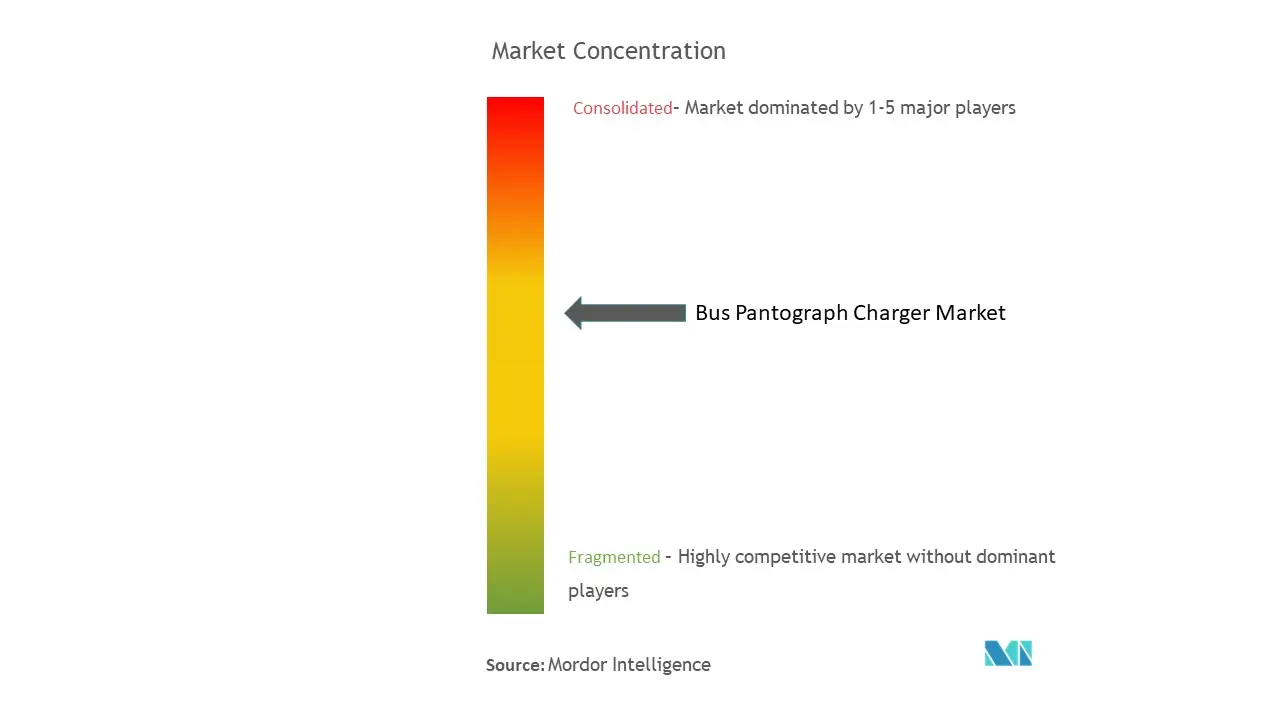

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Bus Pantograph Charger Market Analysis by Mordor Intelligence

The Bus Pantograph Charger Market size is estimated at USD 3.47 billion in 2025, and is expected to reach USD 10.43 billion by 2030, at a CAGR of 24.65% during the forecast period (2025-2030).

The bus pantograph charger industry is experiencing a transformative shift as public transportation systems worldwide embrace electrification to achieve sustainability goals. Major metropolitan areas are leading this transition, with Transport for London (TfL) setting an ambitious target to achieve net-zero emissions by 2030 through the implementation of electric bus fleets. China continues to dominate the global electric bus landscape, with plans to deploy an additional 420,000 electric buses by 2025, demonstrating the massive scale of electrification initiatives. This widespread adoption is driving innovations in electric bus charging infrastructure, with manufacturers developing increasingly sophisticated pantograph charging solutions to meet the growing demand.

Technological advancements in charging systems are revolutionizing the operational efficiency of electric bus fleets. Modern pantograph chargers, such as those developed by Siemens, now operate at up to 1,000 volts with a power range of 50 to 600 kW, enabling faster charging times and improved fleet management capabilities. The integration of smart charging features allows operators to monitor charging status, optimize power consumption, and reduce operational costs through automated charging processes. These developments are particularly evident in recent implementations, such as TfL's 2023 introduction of cutting-edge pantograph charging systems for their all-electric route 132. The incorporation of a fast charging system enhances the efficiency of these operations.

Infrastructure development initiatives are gaining momentum across major cities, supported by substantial government investments and public-private partnerships. The Pacific Economic Development Agency of Canada's USD 31.2 million investment in British Columbia exemplifies the scale of commitment to improving public transportation services and electric bus infrastructure. Cities are strategically placing pantograph charging stations along bus routes and at terminals, creating comprehensive charging networks that support the continuous operation of electric bus fleets. This systematic approach to infrastructure development is essential for the successful transition to fully electric public transportation systems.

The industry is witnessing a convergence of autonomous vehicle technology with electric bus charging systems, marking the beginning of a new era in public transportation. In 2023, Easy Mile became the first company in Europe to receive authorization for operating fully autonomous buses on public roads, incorporating advanced pantograph charging capabilities. This integration of autonomous technology with electric charging systems represents a significant advancement in the industry, promising improved operational efficiency and reduced human intervention in charging processes. Major manufacturers are increasingly incorporating autonomous-ready features in their electric buses, preparing for a future where self-driving electric buses become commonplace in public transportation systems. The advent of opportunity charging system technologies further supports this transition.

Global Bus Pantograph Charger Market Trends and Insights

Rising Emphasis of Government on Eco-Friendly Buses

Governments worldwide are implementing stringent regulations and supportive policies to encourage eco-friendly transportation, particularly focusing on public transit systems. The United States has taken significant steps through the Zero-Emission Vehicles (ZEV) Program, which mandates OEMs to sell specific numbers of clean and zero-emission vehicles, with an ambitious target of putting 12 million ZEVs, including buses, on the road by 2030. Similarly, the European Union has set comprehensive targets for clean buses, with national targets ranging from 24% to 45% in 2025 and from 33% to 65% in 2030, varying based on each country's population and GDP. The German government, for instance, anticipates a quarter of buses to be electric by 2025, supported by a significant increase in funding of EUR 650 million for electric bus procurement and electric bus charging infrastructure.

Recent government initiatives have demonstrated a strong commitment to accelerating the adoption of electric buses through substantial investments and policy support. In 2023, the Canadian Infrastructure Bank and the Regional Municipality of Durham signed a landmark Memorandum of Understanding, committing to invest up to USD 53.1 million to support Durham Region Transit's procurement of 100 battery-electric buses by 2027. This initiative marks a critical milestone in meeting the region's climate change commitments over the following 25-year plans. Additionally, the Indian government's ambitious plan to electrify 30% of total vehicle sales by 2030 is backed by a substantial investment of USD 1.4 billion through the FAME program, specifically targeting the electrification of public transportation with subsidies for over 7,000 electric buses, enhancing the electric fleet charging capabilities.

Advantages Offered Over Plug-in Charger to Propel Depot Charging Demand

Pantograph charging technology offers significant operational advantages over traditional plug-in charging systems, particularly in terms of charging efficiency and automation. The technology enables rapid charging capabilities with power outputs ranging from 50 kW to 600 kW, allowing buses to be topped up in less than 10 minutes during their regular service intervals. This quick-charging capability substantially reduces the operational downtime compared to conventional plug-in chargers that typically require overnight charging. The automated nature of pantograph systems eliminates the need for manual intervention, reducing labor costs and the requirement for trained operators at charging stations, while also minimizing the risk of human error in the charging process.

The space optimization benefits of pantograph charging systems present a compelling advantage for urban transit operators with limited depot space. Unlike plug-in charging stations that require significant spacing between buses due to side-mounted plugs, pantograph systems utilize a top-down or bottom-up approach that allows buses to be parked in close proximity to one another. This space efficiency is particularly valuable in dense urban environments where real estate is at a premium. For instance, in 2023, Solaris inaugurated an innovative charging park in Bolechowo that demonstrates the space-efficient design of pantograph charging systems, accommodating multiple buses within a 10,000 m² area while maintaining optimal operational efficiency. Additionally, the total cost of ownership can be up to 50% lower with pantograph systems, considering their average lifespan of at least 15 years and reduced maintenance requirements compared to plug-in solutions that require frequent replacement of cables and plugs. The integration of a fast charging system further enhances the efficiency of these electric bus charging station setups, making them a preferred choice for commercial EV charging needs.

Segment Analysis: By Charging Type

Level 1 Segment in Bus Pantograph Charger Market

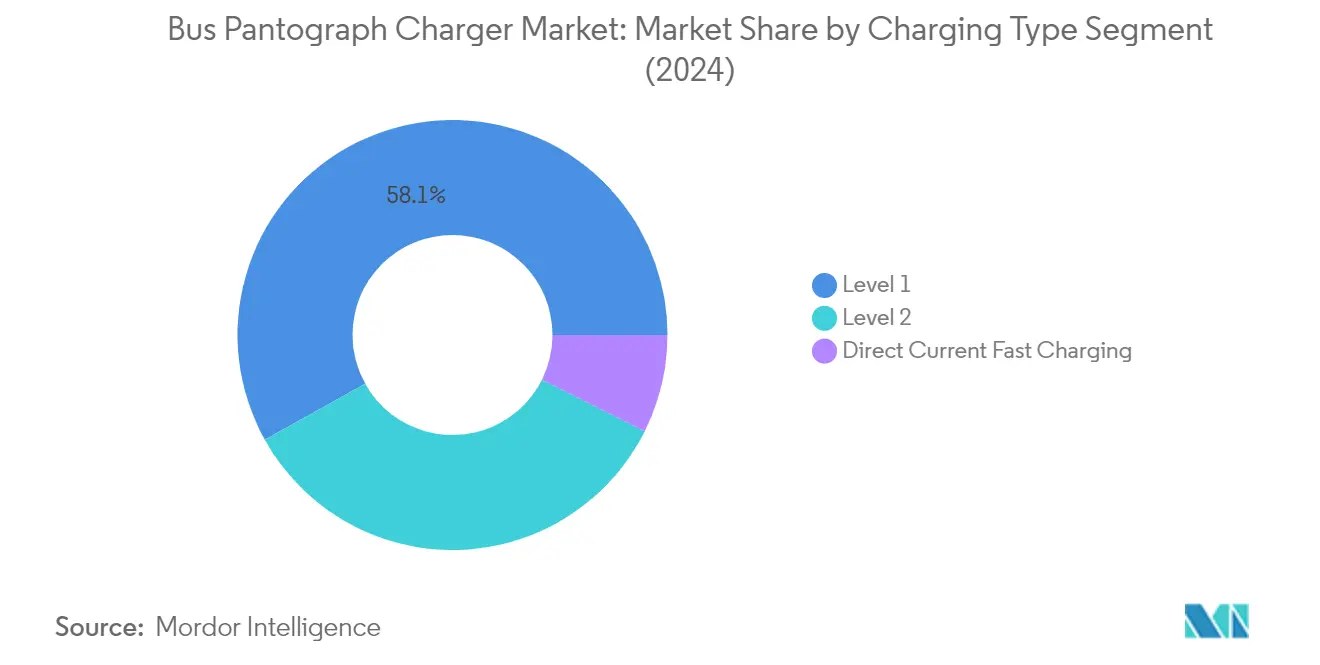

The Level 1 charging segment continues to dominate the global bus pantograph charger market, commanding approximately 58% market share in 2024. This segment, which provides power output ranging from 50 to 150 kW, has maintained its leadership position due to its widespread adoption among hybrid and mild hybrid bus systems. The segment's dominance is primarily attributed to its compatibility with the majority of electric buses currently operating globally, as most buses today incorporate hybrid propulsion systems with smaller batteries compared to full-battery electric buses. Level 1 chargers offer optimal charging capabilities for these hybrid systems, providing an efficient balance between charging speed and power delivery that meets the operational requirements of most bus fleets.

Direct Current Fast Charging Segment in Bus Pantograph Charger Market

The Direct Current Fast Charging (DCFC) segment has emerged as the fastest-growing segment in the bus pantograph charger market, with projections indicating robust growth of approximately 35% from 2024 to 2029. This remarkable growth trajectory is driven by the increasing demand for ultra-fast charging solutions that can deliver power outputs ranging from 300 kW to 650 kW. The segment's rapid expansion is fueled by the growing adoption of opportunity charging systems by municipal authorities and transit operators, who are increasingly recognizing the benefits of quick, high-power charging sessions that can be completed in as little as 5 minutes during regular route stops. This charging approach significantly enhances operational efficiency and route flexibility for electric bus fleets.

Remaining Segments in Charging Type

The Level 2 charging segment represents a significant portion of the bus pantograph charger market, bridging the gap between standard Level 1 charging and high-power DCFC solutions. This segment, which provides power outputs ranging from 150 to 300 kW, serves as a crucial middle-ground option for operators requiring faster charging capabilities than Level 1 but not necessarily needing the ultra-high power output of DCFC systems. Level 2 chargers are particularly popular among operators with medium-sized fleets and those implementing mixed charging strategies, offering a balanced combination of charging speed and infrastructure investment requirements.

Segment Analysis: By Component Type

Hardware Segment in Bus Pantograph Charger Market

The hardware segment continues to dominate the bus pantograph charger market, commanding approximately 92% market share in 2024. This substantial market presence is primarily driven by the high initial investment required for hardware components including charging equipment, pantograph arms, electrical infrastructure, and installation materials. The segment's dominance reflects the critical role of physical infrastructure in enabling electric bus charging operations. Major manufacturers are focusing on developing more efficient and reliable hardware solutions, with innovations in areas such as automated connection systems, weather-resistant materials, and improved power delivery mechanisms. The segment's strong position is further reinforced by the expanding depot charging infrastructure across major metropolitan areas globally, particularly in Europe and Asia-Pacific regions where electric bus adoption is accelerating rapidly.

Software Segment in Bus Pantograph Charger Market

The software segment is emerging as the fastest-growing component in the bus pantograph charger market, with an expected growth rate of approximately 33% during 2024-2029. This remarkable growth is being driven by increasing demand for smart charging solutions that optimize power consumption, reduce charging times, and enhance overall operational efficiency. Software solutions are becoming increasingly sophisticated, incorporating features such as real-time monitoring, predictive maintenance, automated charging schedules, and integration with fleet management systems. The segment is witnessing significant innovations in areas such as load management algorithms, remote diagnostics capabilities, and advanced analytics tools that help operators maximize their charging infrastructure utilization while minimizing operational costs.

Segment Analysis: By Charging Infrastructure Type

On-Board Bottom-Up Pantograph Segment in Bus Pantograph Charger Market

The On-Board Bottom-Up Pantograph segment continues to dominate the global bus pantograph charger market, commanding approximately 81% of the total market share in 2024. This significant market position is attributed to several key advantages offered by on-board bottom-up pantograph systems, including reduced operational complexity and lower maintenance requirements. The technology allows bus drivers to operate the charging system directly without requiring complex WiFi connectivity with charging infrastructure, resulting in reduced overall system costs. Additionally, the segment benefits from enhanced reliability as any technical issues only affect individual buses rather than impacting the entire fleet, which is a common challenge with off-board systems. Major industry players like Siemens, ABB, and Wabtec have strategically focused on developing and improving on-board bottom-up pantograph solutions, contributing to the segment's market leadership.

Off-Board Top-Down Pantograph Segment in Bus Pantograph Charger Market

The Off-Board Top-Down Pantograph segment is experiencing the fastest growth in the bus pantograph charger market, with an expected growth rate of approximately 31% during the forecast period 2024-2029. This remarkable growth is driven by increasing adoption of roof-mounted charging solutions in major urban transportation networks worldwide. The segment's growth is further supported by continuous technological advancements in automation capabilities, with newer systems offering enhanced connectivity and improved charging efficiency. Major bus manufacturers are increasingly incorporating top-down pantograph compatibility into their electric bus designs, recognizing the technology's potential for rapid charging in high-frequency transit routes. The segment is also benefiting from significant investments in charging infrastructure development across major cities, particularly in Europe and Asia-Pacific regions, where governments are actively promoting electric bus adoption.

Bus Pantograph Charger Market Geography Segment Analysis

Bus Pantograph Charger Market in North America

North America represents a growing market for bus pantograph chargers, driven by the increasing adoption of electric buses in public transportation. The United States and Canada are making significant strides in electrifying their public transit systems, with various cities implementing electric bus fleets equipped with pantograph charging technology. The region's focus on sustainable transportation and reducing carbon emissions has led to substantial investments in the electric bus charging infrastructure market development.

Bus Pantograph Charger Market in United States

The United States dominates the North American market with approximately 84% market share in 2024. The country's leadership position is strengthened by ambitious electrification goals set by major cities and transit authorities. Several metropolitan areas are actively expanding their electric bus fleets and installing pantograph charging infrastructure. The implementation of new infrastructure bills and environmental protection initiatives has accelerated the adoption of electric buses and associated charging technologies across various states, contributing significantly to the electric bus charging station market.

Bus Pantograph Charger Market in Canada

Canada demonstrates strong growth potential in the bus pantograph charger market with a projected growth rate of around 27% during 2024-2029. The country's commitment to sustainable public transportation is evident through various provincial and federal initiatives supporting electric bus adoption. Canadian cities are increasingly investing in pantograph charging infrastructure to support their growing electric bus fleets, thereby enhancing the electric bus charging station network. Transit authorities across different provinces are collaborating with technology providers to implement efficient charging solutions.

Bus Pantograph Charger Market in Europe

Europe stands as a key market for bus pantograph chargers, characterized by strong environmental regulations and widespread adoption of electric public transportation. The region's commitment to sustainable mobility has resulted in numerous cities transitioning their public transport fleets to electric buses. Countries like Germany, the United Kingdom, France, Italy, and Spain are at the forefront of this transformation, each contributing significantly to the market's growth through various initiatives and investments in electric bus infrastructure.

Bus Pantograph Charger Market in Germany

Germany leads the European market with approximately 18% market share in 2024. The country's dominant position is supported by its comprehensive approach to public transport electrification and a strong industrial base in automotive and charging technology. German cities are actively expanding their electric bus fleets and charging infrastructure networks, which are integral to the electric bus charging infrastructure market. The country's robust support for sustainable transportation initiatives and technological innovation continues to drive market growth.

Bus Pantograph Charger Market in United Kingdom

The United Kingdom shows remarkable growth potential with a projected growth rate of around 30% during 2024-2029. The country's aggressive push towards sustainable public transportation has resulted in significant investments in electric bus infrastructure. British cities are increasingly adopting pantograph charging solutions for their electric bus fleets. The government's strong support through various funding initiatives and environmental policies continues to drive market expansion, aligning with the broader electric bus charging station market.

Bus Pantograph Charger Market in Asia-Pacific

The Asia-Pacific region represents the largest market for bus pantograph chargers globally, with significant contributions from China, India, Japan, and South Korea. The region's rapid urbanization and increasing focus on sustainable transportation solutions have driven substantial investments in electric bus infrastructure. Government initiatives promoting clean energy transportation have created a favorable environment for market growth, particularly in the commercial EV charging sector.

Bus Pantograph Charger Market in China

China maintains its position as the dominant force in the Asia-Pacific market. The country's extensive electric bus fleet and comprehensive charging infrastructure network set it apart from other markets. Chinese cities continue to lead in electric bus adoption and charging technology implementation. The nation's strong manufacturing capabilities and supportive government policies have created a robust ecosystem for pantograph charging solutions, significantly impacting the electric bus infrastructure.

Bus Pantograph Charger Market in Japan

Japan emerges as the fastest-growing market in the Asia-Pacific region. The country's technological advancement and commitment to sustainable transportation drive market growth. Japanese cities are increasingly adopting innovative charging solutions for their electric bus fleets. The nation's focus on developing smart charging infrastructure and efficient public transportation systems continues to accelerate market expansion.

Bus Pantograph Charger Market in Rest of the World

The Rest of the World market, encompassing South America and the Middle East and Africa, shows promising growth potential in the bus pantograph charger sector. These regions are gradually embracing electric bus technology and developing supporting infrastructure. South America emerges as the largest market in this region, driven by significant developments in countries like Brazil and Colombia, while the Middle East and Africa show the fastest growth potential as countries in these regions increasingly focus on sustainable transportation solutions. The implementation of new charging infrastructure and government initiatives supporting electric mobility continue to shape market development in these regions.

Competitive Landscape

Top Companies in Bus Pantograph Charger Market

The bus pantograph charger market is dominated by established players like Siemens Mobility, ABB Ltd., Schunk Group, Wabtec Corporation, and other prominent manufacturers who have built strong market positions through continuous innovation and strategic expansion. These companies are heavily investing in research and development to create advanced charging solutions, with a particular focus on smart charging capabilities and improved power delivery efficiency. The industry demonstrates a clear trend toward developing integrated solutions that combine hardware and software components to enable features like remote monitoring and predictive maintenance. Companies are actively pursuing geographical expansion through strategic partnerships and joint ventures, particularly in emerging markets where electric bus charging infrastructure adoption is accelerating. Operational agility is being enhanced through localized manufacturing facilities and strengthened distribution networks, allowing companies to better serve regional markets and respond quickly to customer demands.

Consolidated Market with Strong Regional Players

The bus pantograph charger market exhibits a relatively consolidated structure, dominated by large multinational conglomerates with diverse product portfolios in the electric mobility sector. These major players leverage their extensive experience in power electronics and transportation infrastructure to maintain their market positions, while regional specialists focus on serving specific geographic markets with customized solutions. The market has witnessed increased consolidation through strategic acquisitions and partnerships, particularly as established companies seek to enhance their technological capabilities and expand their geographic presence.

The competitive dynamics are characterized by a mix of global leaders and specialized regional players, with the latter gaining prominence in their respective markets through a deep understanding of local requirements and regulations. Market entry barriers remain relatively high due to the technical complexity of pantograph charging systems and the need for established relationships with public transport authorities and bus manufacturers. Companies are increasingly focusing on vertical integration strategies to control key components of the value chain and ensure product quality while optimizing costs.

Innovation and Localization Drive Market Success

Success in the bus pantograph charger market increasingly depends on companies' ability to innovate while maintaining cost competitiveness and ensuring reliability. Incumbent players are focusing on developing comprehensive charging solutions that integrate seamlessly with existing infrastructure while offering enhanced features like faster charging speeds and improved energy management capabilities. The ability to provide localized support and maintenance services has become crucial, as end-users prioritize suppliers who can ensure minimal downtime and rapid response to technical issues.

Market contenders are gaining ground by focusing on specific market segments or geographic regions where they can build strong relationships with local transport authorities and fleet operators. The concentration of end-users in the public transport sector necessitates a strong focus on building long-term relationships and understanding specific regional requirements. While substitution risk from alternative charging technologies exists, pantograph charging maintains its appeal due to its efficiency for high-capacity transit operations. Regulatory support for electric bus adoption continues to shape market dynamics, with companies needing to maintain flexibility in their product development to meet evolving standards and requirements across different regions. As the demand for electric fleet charging and commercial electric vehicle charging solutions grows, companies are adapting their offerings to meet these emerging needs.

Bus Pantograph Charger Industry Leaders

ABB

Schunk Transit Systems GmBH

Wabtech Corporation

Siemens AG

Vector Informatik GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2022: British bus company First Bus ordered 193 electric buses worth GBP 81 million (~USD 96.4 million) from Northern Irish bus manufacturer Wrightbus. Furthermore, the company initially specifies the DC charging power at 150 kW and optional opportunity charging at 450 kW through pantograph options.

- May 2022: The San Diego Metropolitan System began construction on a USD 8.5 million overhead electric bus charging system capable of charging 24 battery-electric buses at a time. The overhead gantry charging system is expandable to add more charging capacity over the coming years, and MTS will be installing the Schunk SLS 301 series Depot Charging Pantograph, which offers a quicker and safer hands-free electric vehicle charge.

- April 2022: Transports Metropolitans de Barcelona (TMB) has announced that it has opened the tender process to acquire up to 83 battery-powered electric buses, which, in 2023, will replace diesel-powered vehicles that have reached the end of their lifespan. The tender is divided into three lots: two of the lots are standard-size cars (12m) with night load per pantograph, of which 45 units will be contracted, which can be expanded to 63. The third lot consists of 20 articulated units (18m in length) for overnight pantograph charging or other technologies.

- April 2022: The board of the operator Miejski Zakład Komunikacji in Grudziądz and representatives of Solaris Bus & Coach Sp. z o.o. signed a contract for the delivery of 17 electric buses. The tender covers not only the delivery of the vehicles but also of the charging devices, including pantograph chargers. The buses and the charging infrastructure are expected to be delivered to the city in the first quarter of 2023.

- November 2021: The Department of Transport and Road Infrastructure Development of Moscow and e FSUE NAMI State Research Center launched a pilot project by installing an innovative charging station with a bus-down pantograph at the subsidiary Mosgortrans urban surface public transport operator. On this point, two electric buses have been equipped with special contact rails that are adapted to the new charging infrastructure, and these pantographs are to be tested by the end of 2022.

Global Bus Pantograph Charger Market Report Scope

A pantograph, which makes automated contact between the bus and the charging infrastructure, is a common way to charge battery electric buses. There are currently two methods for making this contact. When charging is required, the pantograph can be mounted on the roof of the electric bus and lifted, or it can be mounted on the charging infrastructure and moved downwards.

The bus pantograph charger market is segmented by charging type (level 1, level 2, and direct current fast charging (DCFC)), component type (hardware and software), charging infrastructure (off-board top-down pantograph and on-board bottom-up pantograph), and geography (North America, Europe, Asia-Pacific, and Rest of the World). The report offers market size and forecasts for the bus pantograph charger market in value (USD million) for all the above segments.

| Level 1 |

| Level 2 |

| Direct Current Fast Charging |

| Hardware |

| Software |

| Off-board top-down pantograph |

| On-Board Bottom-Up Pantograph |

| North America | United States |

| Canada | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| South Korea | |

| Japan | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Aegentina | |

| Rest of the South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of the Middle East and Africa |

| By Charging Type | Level 1 | |

| Level 2 | ||

| Direct Current Fast Charging | ||

| By Pcomponent Type | Hardware | |

| Software | ||

| By Charging Infrastructure Type | Off-board top-down pantograph | |

| On-Board Bottom-Up Pantograph | ||

| Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| South Korea | ||

| Japan | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Aegentina | ||

| Rest of the South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of the Middle East and Africa | ||

Key Questions Answered in the Report

How big is the Bus Pantograph Charger Market?

The Bus Pantograph Charger Market size is expected to reach USD 3.47 billion in 2025 and grow at a CAGR of 24.65% to reach USD 10.43 billion by 2030.

What is the current Bus Pantograph Charger Market size?

In 2025, the Bus Pantograph Charger Market size is expected to reach USD 3.47 billion.

Who are the key players in Bus Pantograph Charger Market?

ABB, Schunk Transit Systems GmBH, Wabtech Corporation, Siemens AG and Vector Informatik GmbH are the major companies operating in the Bus Pantograph Charger Market.

Which is the fastest growing region in Bus Pantograph Charger Market?

Europe is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Bus Pantograph Charger Market?

In 2025, the North America accounts for the largest market share in Bus Pantograph Charger Market.

What years does this Bus Pantograph Charger Market cover, and what was the market size in 2024?

In 2024, the Bus Pantograph Charger Market size was estimated at USD 2.61 billion. The report covers the Bus Pantograph Charger Market historical market size for years: 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Bus Pantograph Charger Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Page last updated on: