Bridge Construction Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

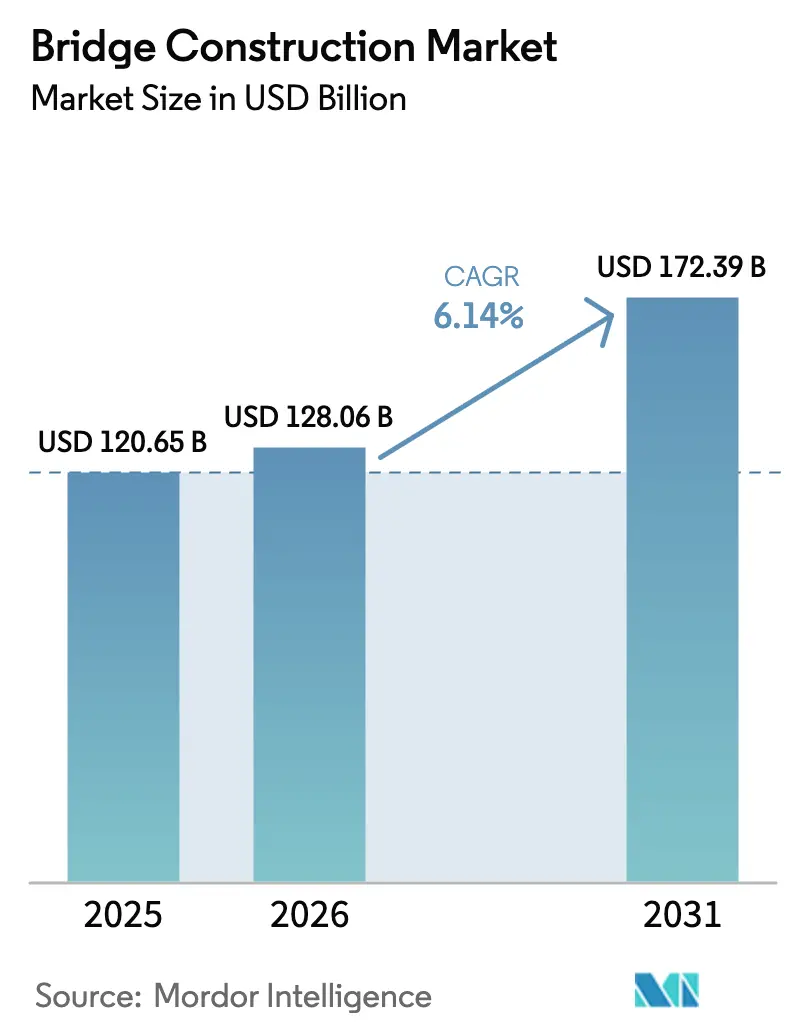

| Market Size (2026) | USD 128.06 Billion |

| Market Size (2031) | USD 172.39 Billion |

| Growth Rate (2026 - 2031) | 6.14% CAGR |

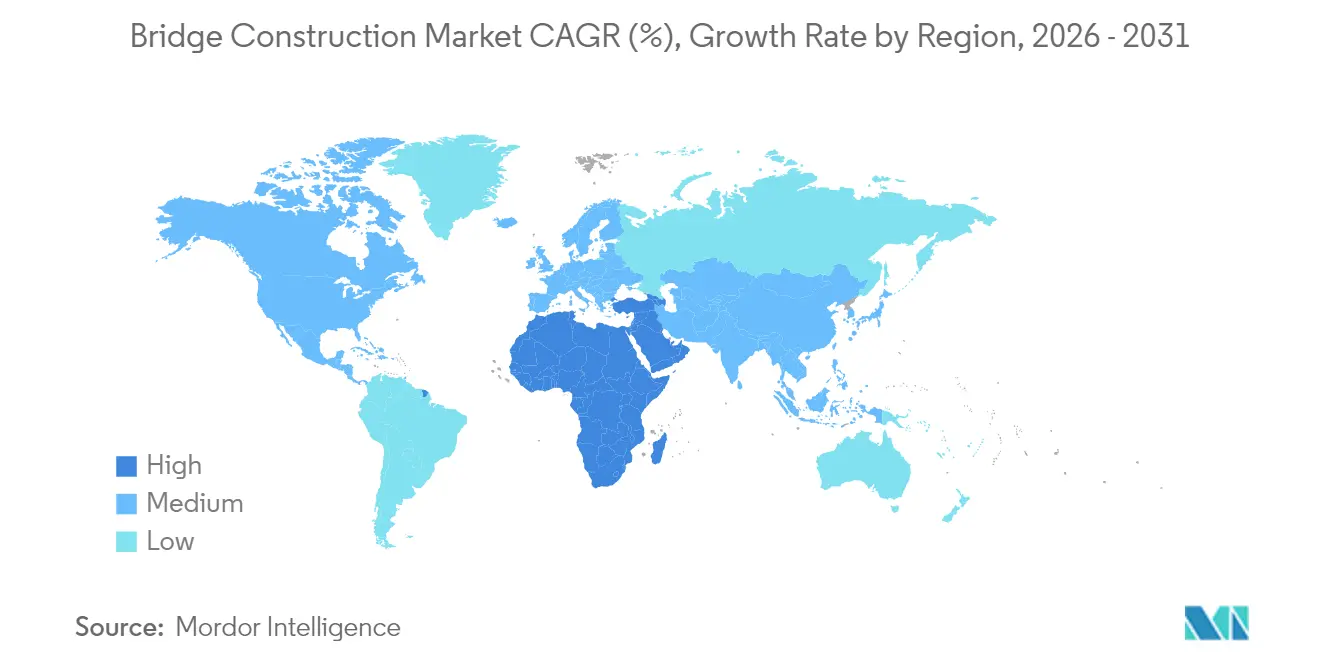

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players_-_Copy.webp) *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Bridge Construction Market Analysis by Mordor Intelligence

Bridge Construction market size in 2026 is estimated at USD 128.06 billion, growing from 2025 value of USD 120.65 billion with 2031 projections showing USD 172.39 billion, growing at 6.14% CAGR over 2026-2031. Accelerating infrastructure outlays, such as the United States Infrastructure Investment and Jobs Act (IIJA) and China’s Five-Year Plan, anchor multi-year demand visibility. Rapid uptake of prefabrication and modular assembly compresses delivery schedules by 20-40%, enabling contractors to bid more projects with tighter timelines. Contractors increasingly differentiate through technology, digital twins, AI-enabled logistics, and automated quality control, rather than lowest cost alone. Meanwhile, public agencies embed climate resilience and low-carbon specifications into procurement, nudging material choices toward ultra-high-performance concrete (UHPC) and fiber-reinforced polymers. Regional growth gaps widen: Asia-Pacific sustains the largest project pipeline, while the Middle East & Africa emerges as the fastest-expanding arena due to cross-border connectivity programs.

Key Report Takeaways

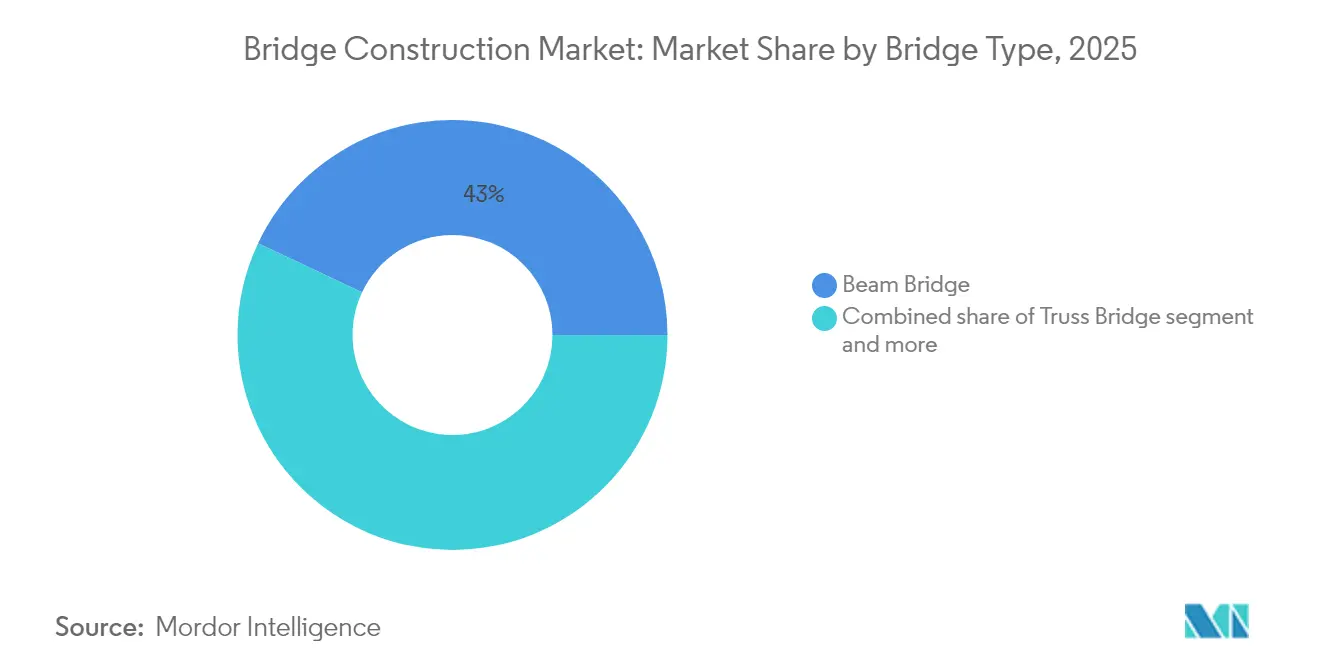

- By bridge type, beam bridges led with 42.98% of the bridge construction market share in 2025; cable-stayed designs are projected to advance at a 7.62% CAGR to 2031.

- By material, steel accounted for a 52.90% share of the bridge construction market size in 2025, while composites recorded the highest projected CAGR at 8.12% through 2031.

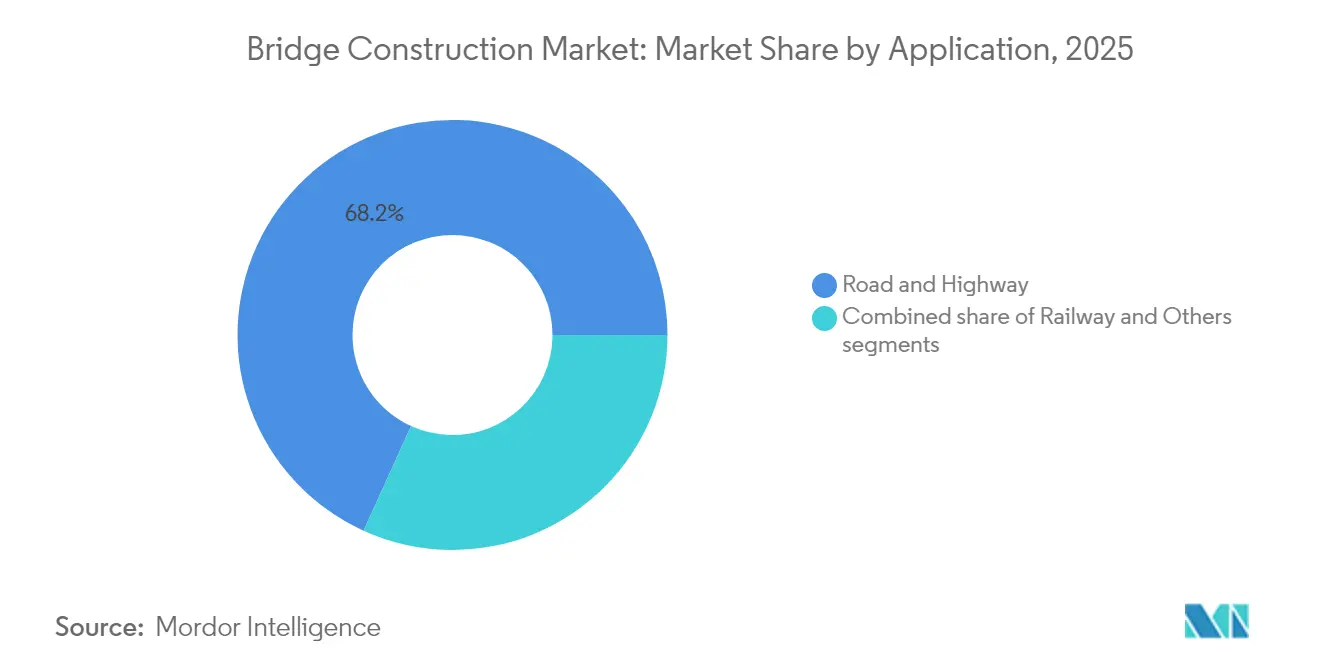

- By application, road and highway structures commanded 68.21% of the bridge construction market share in 2025, and railway bridges are set to grow at a 6.55% CAGR between 2026-2031.

- By geography, Asia-Pacific held 46.12% share of the bridge construction market in 2025; the Middle East & Africa is forecast to expand at a 7.63% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Bridge Construction Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mega-infrastructure spending plans (2025-2030) | +1.8% | North America, Asia-Pacific, Middle East & Africa | Medium term (2-4 years) |

| Preference for accelerated bridge construction (ABC) | +1.2% | North America, Europe, and spreading to Asia-Pacific | Short term (≤ 2 years) |

| Shift to low-carbon and recycled materials | +0.9% | Europe, North America, global roll-out | Long term (≥ 4 years) |

| Resilience upgrades for climate-exposed bridges | +0.7% | Global coastal and seismic regions | Medium term (2-4 years) |

| Smart-sensor structural-health-monitoring mandates | +0.6% | Advanced economies first | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in Mega-Infrastructure Spending Plans (2025-2030)

Historic funding waves underpin the bridge construction market. The IIJA directs USD 110 billion to roads and bridges, including dedicated Bridge Investment and Formula programs. China’s public-works outlays follow its current Five-Year Plan, while Mexico’s National Infrastructure Program budgets USD 12.6 billion for 551 transport projects. Multi-region synchronicity lets contractors scale prefabrication factories and workforce training, locking in supply-chain efficiencies. Long-dated visibility also attracts private capital, evident in a 40% share of 2024 AEC M&A deals funded by private equity[1]Pete Buttigieg, “Bridge Investment Program Fact Sheet,” U.S. Department of Transportation, transportation.gov.

Growing Preference for Accelerated Bridge Construction (ABC) Methods

ABC shrinks on-site activity, curbs traffic disruption, and improves safety. FHWA pilot states report 20-50% faster completions and quality gains from factory-controlled modules. UHPC joints extend spans 30-40%, cutting lifecycle maintenance. Missouri’s I-70 Missouri River crossing finished ahead of schedule by staging prefabricated segments while live lanes stayed open. Contractors investing in digital twins and logistics simulation capture procurement preference as 47 state DOTs embed ABC scoring into tenders[2]Victoria Farr, “Accelerated Bridge Construction Guide for State DOTs,” Federal Highway Administration, fhwa.dot.gov.

Resilience Upgrades for Climate-Change-Exposed Bridges

Seismic, flood, and temperature extremes reset design baselines. California’s Golden Gate Bridge retrofit deployed tuned-mass dampers and continuous monitoring to withstand magnitude-8.3 quakes at a USD 76 million budget. Australia’s policy now compels climate-risk assessments for all major crossings, spurring higher deck elevations and thermal allowances. Coastal nations elevate pile foundations to tackle sea-level rise, while arid regions specify heat-tolerant bearings. Specialized know-how commands premium margins, rewarding firms with proven extreme-environment portfolios.

Smart-Sensor-Enabled Structural-Health-Monitoring Mandates

IoT networks shift maintenance from reactive to predictive. Germany’s OpenLAB test bridge integrates 200+ multiparameter sensors, capturing load, tilt, and temperature every second with USD 4.18 million federal backing. Hamburg’s smartBRIDGE embeds 500 sensors and BIM data to forecast deterioration in real time. U.S. DOT encourages states to weave sensor suites into new builds, unlocking life-cycle savings that offset initial outlay within 7-10 years. Early adopters win O&M contracts that run decades, diversifying revenue beyond EPC scopes[3]Hendrik Wüst, “OpenLAB Research Bridge Launches in Bautzen,” Federal Ministry for Digital and Transport, bmdv.bund.de.

Restraints Impact Analysis*

| Restraints | (≈) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Skilled-labor shortages in advanced bridge engineering | -1.1% | North America, Europe, Australia | Medium term (2-4 years) |

| Inflation-driven spikes in steel & cement costs | -0.8% | Global, acute in emerging markets | Short term (≤ 2 years) |

| Lengthy environmental-impact permitting cycles | -0.6% | North America, Europe expanding | Medium term (2-4 years) |

| Rising insurance premiums in seismic zones | -0.4% | Pacific Rim, Mediterranean | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Skilled-Labor Shortages in Advanced Bridge Engineering

ABC counts 439,000 extra U.S. construction workers needed in 2025, rising to 499,000 in 2026. Australia’s pipeline needs 130,000 new hires, while the U.K. targets 500,000 across major projects. Wage premiums escalate 15-20% for segmental-bridge carpenters and UHPC specialists. Automation, robotic rebar tying, and 3-D printed formwork offset but cannot fully bridge the gap, prompting firms to establish training academies and global talent exchanges.

Inflation-Driven Spikes in Steel & Cement Input Costs

Elevated rebar at USD 47.70 per 20-ft length and RSMeans Index 296.3 squeeze project margins. Shipping bottlenecks lengthen lead times for high-spec steel and bearings. Contractors hedge with indexed contracts and multi-source procurement, yet some public owners defer bids until price clarity returns. Designers increasingly favor material-efficient layouts to keep budgets intact.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Bridge Type: Cable-Stayed Designs Lead Innovation

Cable-stayed structures post a 7.62% CAGR, the swiftest inside the bridge construction market, as governments prefer their span-to-cost efficiency and visual appeal. Beam bridges continued to dominate with 42.98% of 2025 revenue, reflecting their unmatched value for medium-length highway crossings and the well-established contractor base maintaining this format. The Pelješac Bridge’s 285-m main spans were erected through balanced cantilever, proving how stay-cables can speed construction while minimizing temporary falsework.

The segment’s outlook hinges on digital tools such as BIM Level 3, highlighted by Norway’s New Sotra Bridge, which modeled 1 million objects to optimize sequencing. Suspension alternatives still command niche demand for spans greater than 1,000-m, but higher insurance premiums in seismic belts tilt some owners toward cable-stays. Movable and arch formats continue to find specialized urban or maritime use when navigational clearance or heritage aesthetics are decisive.

By Material: Composite Materials Surge Despite Steel Dominance

Steel preserved 52.90% of the 2025 value, undergirding the bridge construction market size through mature fabrication hubs and predictable performance. Composite materials, however, accelerate at 8.12% CAGR as owners chase corrosion-free life cycles and lighter superstructures that cut foundation costs. FHWA pilot decks demonstrate UHPC joints enabling 100-plus-year lifespans, shifting whole-life economics in favor of advanced concretes.

Fiber-reinforced polymers trim dead load by up to 50%, letting designers stretch spans without deeper girders. SmartBRIDGE Hamburg shows how embedded sensors enhance confidence in newer materials by proving real-time durability. Recycling initiatives also raise steel’s sustainability profile, ensuring its continued relevance even as composites scale.

By Application: Railway Infrastructure Accelerates Growth

Road and highway projects represented 68.21% of the bridge construction market share in 2025, benefiting from sustained roadway upgrades across continents. Railway applications produce a 6.55% CAGR on the back of high-speed networks and freight-corridor modernization. The European Commission’s USD 4.31 million grant on the Havlíčkův Brod-Pardubice line typifies EU efforts to replace life-expired trusses with modern Langer beams.

Japan’s USD 2.11 billion freight-connectivity program underscores rail’s strategic value for resilient supply chains. Multi-modal bridge formats that integrate tracks with traffic lanes gain favor in dense corridors, exemplifying how smart city mandates reshape cross-section design. Pedestrian and cycling links follow broader urban-mobility spending, bringing fresh opportunities for slender composite decks and aesthetic lighting.

Geography Analysis

Asia-Pacific commanded 46.12% of global spending in 2025, anchored by China’s Belt and Road extensions and India’s USD 1.2 trillion National Infrastructure Pipeline. Japan’s USD 2.11 billion freight-link package and Australia’s climate-resilient bridge replacements reinforce regional momentum. Embedded manufacturing capacity for steel girder fabrication accelerates project execution, and governments increasingly mandate BIM, bringing digital parity with Western peers.

Middle East & Africa leads growth with a 7.63% CAGR forecast as the African Development Bank mobilizes USD 635.8 million for the ECOWAS cross-border bridge and targets USD 130-170 billion annually to close the region’s infrastructure gap. Nigeria and Egypt award EPC contracts that bundle ABC methods with seismic detailing, reflecting both schedule urgency and performance expectations.

North America benefits from the IIJA’s USD 110 billion bridge allocation, unleashing dozens of design-build tenders that prioritize prefabrication capacity. Canada’s Pattullo Bridge replacement highlights the rise of public-private partnerships, while Mexico’s USD 12.6 billion bridge backlog advances economic integration goals. Europe, focused on decarbonization, invests in digital twins and low-carbon materials, aligning procurement with the EU Green Deal.

Competitive Landscape

The bridge construction market is moderately fragmented yet trending toward consolidation. The top five players capture under 35% of global revenue, as regional contractors retain stronghold positions. Manhattan Road & Bridge’s purchase of Jensen Construction demonstrates capability-focused M&A, particularly for marine foundations and ABC expertise.

Technology adoption distinguishes leaders: companies integrating IoT sensors, AI-driven scheduling, and off-site fabrication consistently outperform schedule baselines. FHWA’s ABC endorsement in 47 states formally embeds technology readiness into bid scoring, steering market share toward digital pioneers.

Private equity’s 40% participation in 2024 AEC transactions injects capital for equipment automation, modular yard expansion, and international joint ventures. Niche disruptors, sensor manufacturers, and software developers partner with EPCs to commercialize predictive-maintenance service models, diversifying revenue streams beyond one-time construction fees.

Bridge Construction Industry Leaders

ACS Group

AECOM

Balfour Beatty

China Communications Construction Co. (CCCC)

China Railway Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Germany’s Federal Ministry for Digital and Transport opened the USD 4.18 million OpenLAB research bridge in Bautzen to trial AI-enabled structural monitoring.

- December 2024: Missouri DOT delivered the USD 220 million Lance Corporal Leon Deraps I-70 Missouri River Bridge ahead of schedule through innovative ABC staging.

- October 2024: The European Commission granted USD 4.31 million to replace a temporary rail bridge on the Havlíčkův Brod-Pardubice line with a permanent Langer beam structure.

- September 2024: African Development Bank approved USD 635.8 million for the ECOWAS bridge linking Liberia and Côte d’Ivoire, the region’s largest cross-border infrastructure commitment.

Global Bridge Construction Market Report Scope

Beam, truss, arch, suspension, and cable-stayed bridges are among the common forms of bridge construction. The term "beam bridge" refers to a horizontal structure that rests on two ends supports and acts as a beam to carry traffic. Beam bridge construction is sold by entities (organizations, partnerships, and sole proprietors).

The report provides a comprehensive background analysis of the bridge construction market, covering the current market trends, restraints, technological updates, and detailed information on various segments and the industry's competitive landscape. Additionally, the COVID-19 impact is incorporated and considered during the study.

The Bridges Construction Market is segmented by type (beam bridge, truss bridge, arch bridge, suspension bridge, cable-stayed bridge, and others), material (steel, concrete, and composite materials), application (road and highway, and railway), and region (North America, Asia- Pacific, Europe, Latin America, Middle East, and Africa). The report offers market size and forecasts for the Bridges Construction market in value (USD) for all the above segments.

| Beam Bridge |

| Truss Bridge |

| Arch Bridge |

| Suspension Bridge |

| Cable-Stayed Bridge |

| Others |

| Steel |

| Prestressed Concrete |

| Composite Material |

| Advanced Materials (FRP, UHPC) |

| Road & Highway |

| Railway |

| Others(Pedestrian & Cycle, Pipeline & Utility, etc.) |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Bridge Type | Beam Bridge | |

| Truss Bridge | ||

| Arch Bridge | ||

| Suspension Bridge | ||

| Cable-Stayed Bridge | ||

| Others | ||

| By Material | Steel | |

| Prestressed Concrete | ||

| Composite Material | ||

| Advanced Materials (FRP, UHPC) | ||

| By Application | Road & Highway | |

| Railway | ||

| Others(Pedestrian & Cycle, Pipeline & Utility, etc.) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current global value of the bridge construction market?

The bridge construction market size is USD 128.06 billion in 2026.

How fast is bridge construction spending expected to grow?

Global revenue is forecast to rise at a 6.14% CAGR from 2026 to 2031.

Which region contributes the largest share of new bridge projects?

Asia-Pacific accounts for 46.12% of 2025 spending thanks to Chinese and Indian programs.

Which bridge type is expanding the quickest?

Cable-stayed structures lead with a projected 7.62% CAGR through 2031.

Page last updated on: