Breast Lesion Localization Methods Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 636.02 Million |

| Market Size (2031) | USD 899.20 Million |

| Growth Rate (2026 - 2031) | 7.17% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Breast Lesion Localization Methods Market Analysis by Mordor Intelligence

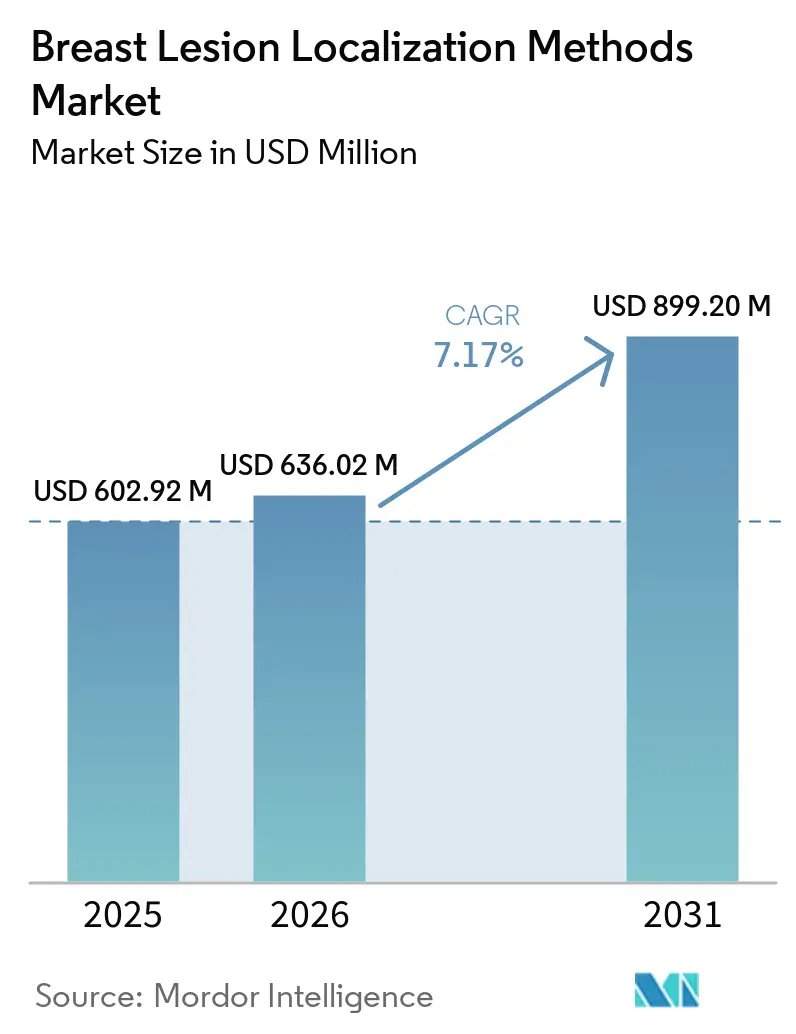

The Breast Lesion Localization Methods Market size was valued at USD 602.92 million in 2025 and is estimated to grow from USD 636.02 million in 2026 to reach USD 899.20 million by 2031, at a CAGR of 7.17% during the forecast period (2026-2031).

At the core of this solid expansion is an industry-wide pivot away from wire-guided localization toward magnetic seed, radar reflector, and RFID platforms that work reliably in dense breast tissue, integrate easily with multi-modal imaging, and remove radioisotope licensing burdens. Device vendors are coupling hardware with real-time analytics and surgical navigation tools, enabling closed-loop workflows that trim operating-room time and cut positive-margin re-excisions. Reimbursement parity for outpatient lumpectomy in the United States, dense-breast notification mandates on both sides of the Atlantic, and large-scale screening rollouts in China and India are amplifying procedure volumes even as production reshoring raises unit costs. Competitive moves such as Hologic’s USD 310 million purchase of Endomagnetics in 2024 and BD’s EnCor EnCompass launch in January 2026 underline how premium hardware capabilities now hinge on integrated software ecosystems.

Key Report Takeaways

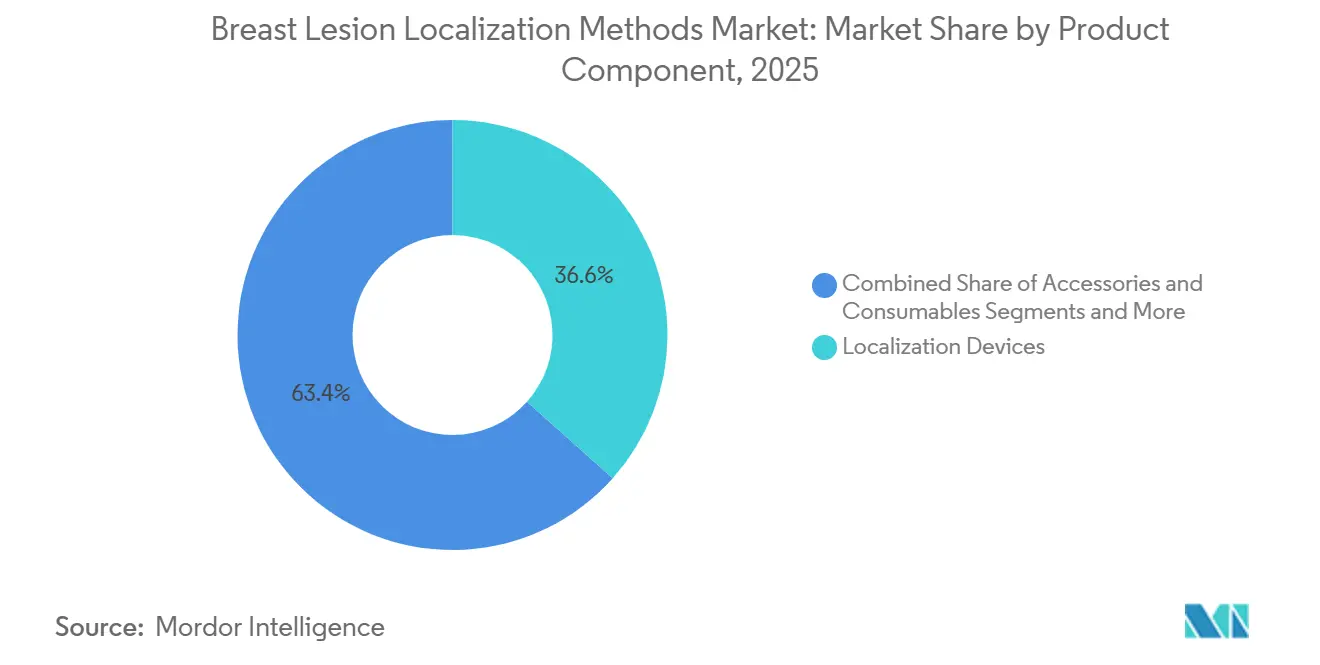

- By product component, localization devices led with 36.61% of the breast lesion localization methods market share in 2025, whereas accessories & consumables are projected to expand at a 7.63% CAGR to 2031.

- By imaging-guidance modality, ultrasound-guided procedures accounted for 50.05% of 2025 revenue, while MRI-guided workflows are poised for the fastest 7.53% CAGR through 2031.

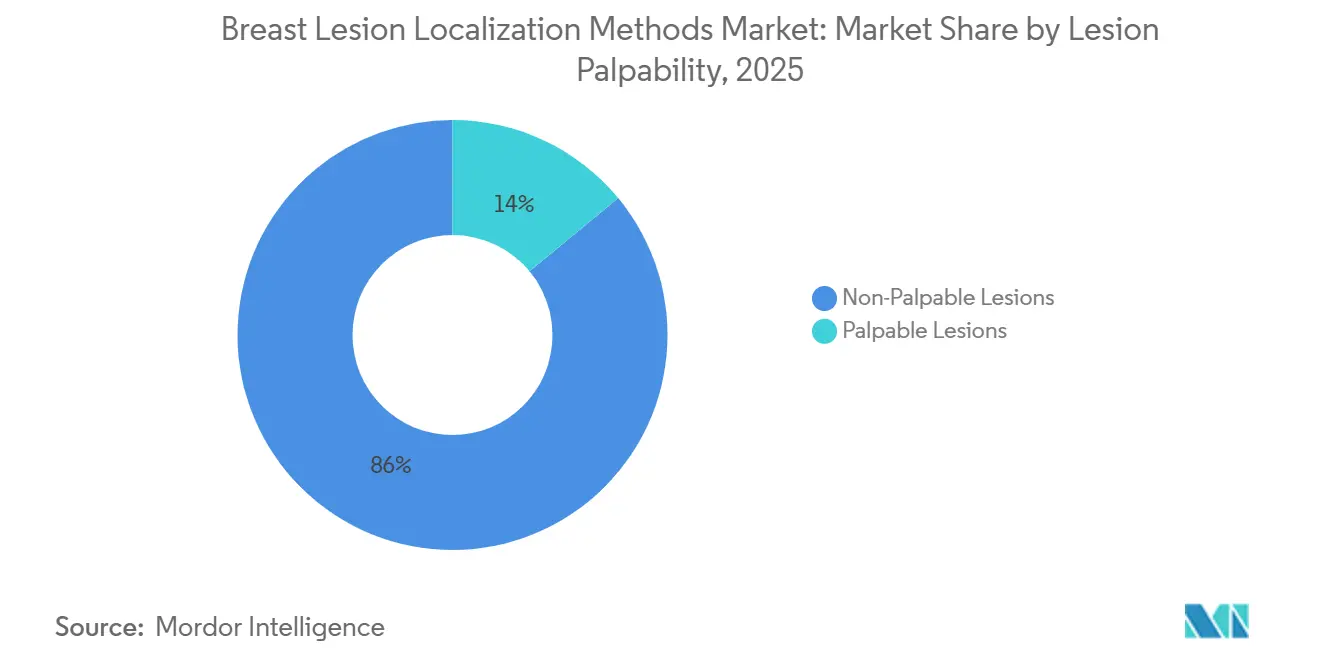

- By lesion palpability, non-palpable lesions represented 85.99% of the total share in 2025 and are advancing at an 8.49% CAGR through 2031.

- By technology, wire-guided localization retained 34.38% share in 2025, but magnetic seed localization is accelerating at a 8.49% CAGR over the forecast period.

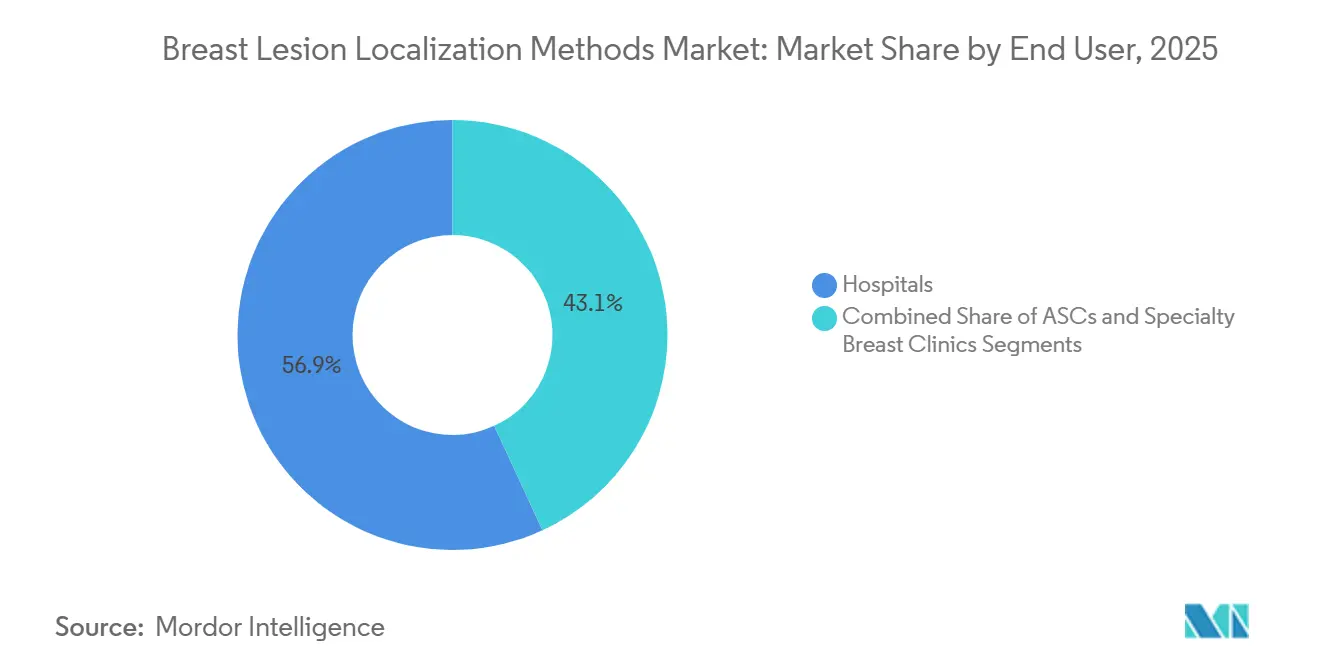

- By end user, hospitals controlled 56.87% of 2025 revenue, whereas specialty breast clinics are expanding at an 7.61% CAGR to 2031, thanks to 2025 CMS reimbursement parity.

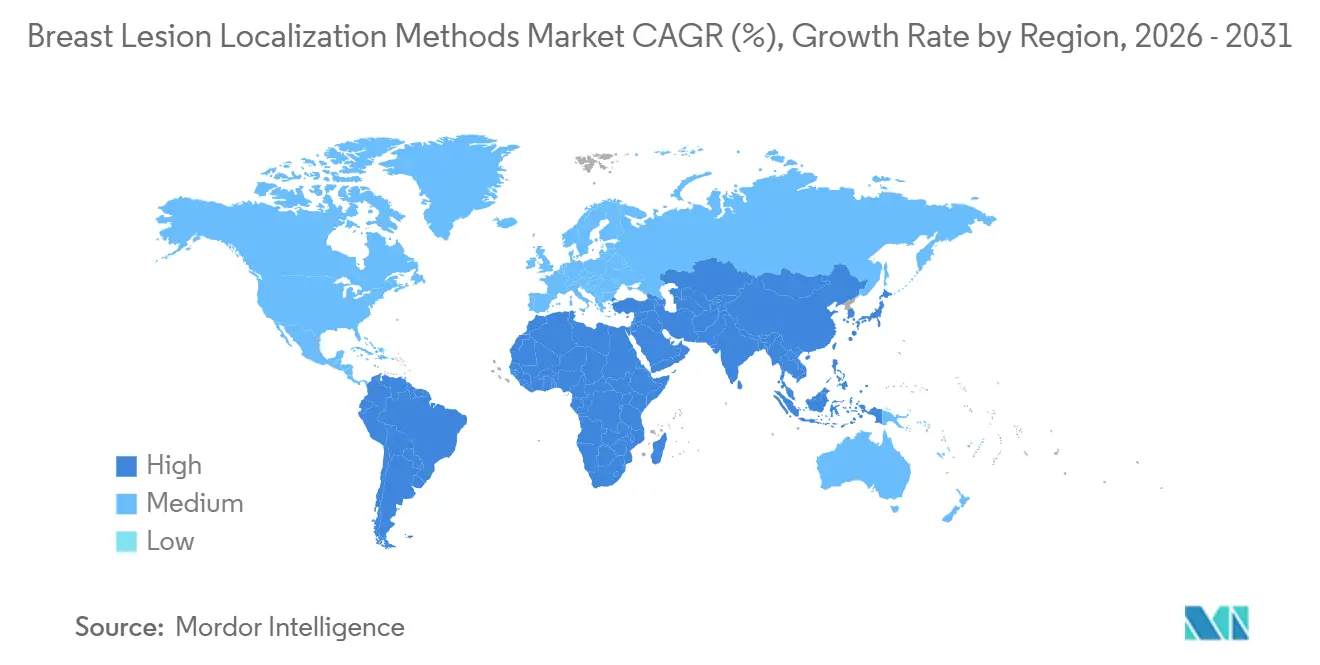

- North America was the top regional market with 40.37% of 2025 revenue, while Asia-Pacific is the fastest growing geography at an 7.93% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Breast Lesion Localization Methods Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Adoption of Non-Wire Localization Techniques in Dense Breast Tissue | +1.2% | North America, Europe, APAC urban centers | Medium term (2-4 years) |

| Increasing Early Breast Cancer Screening Rates in Emerging Economies | +1.4% | China, India, South Korea | Long term (≥ 4 years) |

| Integration of Localization Systems with Intra-Operative Navigation Platforms | +0.9% | North America, Western Europe | Short term (≤ 2 years) |

| MRI-Visible Localization Markers Enabling Multi-Modal Imaging | +0.8% | North America, Europe, Japan | Medium term (2-4 years) |

| Regulatory Push for Radiation-Free Alternatives to Radio-Seed Systems | +1.1% | North America, EU, Australia | Short term (≤ 2 years) |

| Supply-Chain Reshoring Initiatives Reducing Device Lead-Times | +0.6% | North America, select EU markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Adoption of Non-Wire Localization Techniques in Dense Breast Tissue

The September 2024 dense-breast notification rule obliges U.S. imaging centers to inform women when mammograms show dense parenchyma, driving a quick pivot toward magnetic seed and radar reflector systems that stay fixed even when patients change position. A multi-center JAMA Surgery study published in March 2025 reported that magnetic seed localization cut positive-margin rates to 11% in dense-breast cohorts compared with 21% for wire guidance.[1]Elena Martinez et al., “Magnetic Seed Localization Cuts Positive Margins in Dense Breast Cohorts,” JAMA Surgery, jamanetwork.com With 43% of American women aged 40-74 now classified as having heterogeneously or extremely dense tissue,[2]American College of Radiology, “Dense Breast Tissue Prevalence Report,” American College of Radiology, acr.org hospitals are standardizing on radiation-free devices that can be placed under ultrasound and confirmed on MRI.

Increasing Early Breast Cancer Screening Rates in Emerging Economies

China extended its national screening program to 150 million rural women between 2024 and 2025, India embedded mammography referrals in its Ayushman Bharat digital health stack in April 2025, and South Korea raised coverage to 68% by December 2025.[3]Ministry of Health and Family Welfare, “Ayushman Bharat Digital Health Stack Adds Mammography Referrals,” Ministry of Health and Family Welfare, mohfw.gov.in Rising detection of non-palpable lesions is enlarging the addressable procedure pool, yet patchy reimbursement still tilts demand toward lower-cost wire systems in rural hospitals.

Integration of Localization Systems with Intra-Operative Navigation Platforms

Medtronic’s StealthStation gained breast-surgery clearance in November 2025, showing that navigation consoles built for neurosurgery can track magnetic seeds and overlay lesion coordinates on live video, dropping re-excisions from 18% to 7% in a Memorial Sloan Kettering pilot. Hologic’s February 2026 pact with Brainlab bundles Magseed hardware with navigation software at a 25% discount, targeting community hospitals that perform 200-500 breast procedures a year.

MRI-Visible Localization Markers Enabling Multi-Modal Imaging

Hologic’s Magseed received FDA clearance in August 2024 for a paramagnetic core that can be seen on T1-weighted MRI, letting radiologists place the marker inside the scanner instead of using ultrasound first. A Radiology study from October 2025 clocked a 40% cut in median procedure time when MRI-visible seeds replaced hybrid workflows. The capability is vital for managing invasive lobular carcinoma and BRCA1/2 carriers whose lesions appear only on MRI.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited Reimbursement for Novel Localization Devices in Low-Income Markets | −0.8% | APAC excl. Japan, MEA, Latin America | Long term (≥ 4 years) |

| Stringent Radioisotope Handling Regulations Constrain Hospital Adoption | −0.6% | North America, EU, Australia | Short term (≤ 2 years) |

| Capital Budget Constraints Amid Post-Pandemic Cost Pressures | −0.7% | Global, acute in Europe & Latin America | Medium term (2-4 years) |

| Shortage of Trained Breast Surgeons for New Localization Technologies | −0.5% | Global, rural North America & APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Limited Reimbursement for Novel Localization Devices in Low-Income Markets

India’s Employees’ State Insurance covers only wire guidance at INR 5,000 (USD 60), leaving patients to pay USD 300-480 for magnetic seed or radar devices. Brazil’s SUS reimburses BRL 800 (USD 160) for Magseed, well below the BRL 1,200 (USD 240) cost, forcing public hospitals to delay adoption. South Africa’s new National Health Insurance excludes wireless localization, limiting access to private facilities.

Stringent Radioisotope Handling Regulations Constrain Hospital Adoption

NRC rules demand authorized users, leak tests, and written safety programs, adding USD 20,000-50,000 in annual compliance costs for U.S. hospitals. Similar European requirements under the Euratom directive and Australia’s June 2025 safety alert have driven smaller community centers to abandon iodine-125 seeds in favor of magnetic alternatives.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Component: Accessories & Consumables Extend Growth Run

Localization devices held 54.74% of 2025 revenue, illustrating that physical markers remain the foundation of breast-conserving surgery. However, the accessories & consumables segment is anticipated to register the fastest CAGR of 7.63% during the forecast period, owing to the recurring need for single-use deployment needles, introducers, localization wires/markers, and procedure-specific disposable accessories with every breast lesion localization procedure. Growth in breast-conserving surgeries and increasing adoption of wire-free localization systems are further driving repeat consumables demand across hospitals and breast care centers.

A parallel boost comes from proprietary accessories and consumables that lock providers into single-vendor ecosystems. BD’s FDA-cleared EnCor EnCompass combines vacuum-assisted biopsy with localization in one device, tying follow-on needle and sheath purchases to BD for the life of the system. Hospitals embrace the convenience even as procurement officers negotiate bundled pricing to blunt consumable mark-ups. Collectively, these trends cement a recurring revenue model that softens hardware price erosion and underpins vendor competitiveness within the breast lesion localization methods market.

By Imaging-Guidance Modality: MRI Workflows Accelerate

Ultrasound guidance controlled 50.05% of 2025 procedures thanks to scanner ubiquity and real-time visualization in dense tissue. Yet the breast lesion localization methods market size tied to MRI guidance is growing fastest at 7.53% a year, propelled by dense-breast mandates that encourage supplemental MR exams. Hologic’s MRI-visible Magseed eliminates two-step ultrasound-plus-MRI workflows, slicing median localization time by 40% in Brigham and Women’s analyses.

Mammography and stereotactic guidance remain common inside high-volume screening sites but face headwinds as clinicians favor radiation-free pathways. CT guidance occupies a small niche for posterior lesions near the chest wall. As emerging markets expand MRI fleets, notably in China and India, modality mix will shift further, cementing MRI as a mainstream tool inside the breast lesion localization methods market share calculus.

By Lesion Palpability: Non-Palpable Cases Dominate Growth

Non-palpable lesions already commanded 85.99% of all localization procedures in 2025 and will keep expanding at an 7.27% CAGR through 2031. Earlier screening catches smaller tumors invisible to the hand, forcing surgeons to rely on marker technologies to achieve clear margins. Within this cohort, magnetic seed and radar reflectors reduce re-excisions by anchoring firmly to the target irrespective of patient motion.

Palpable lesions are more prevalent in low-income regions where mammography penetration stays under 30%. As those nations roll out screening programs, the balance will continue to tilt toward non-palpable presentations, reinforcing demand patterns that favor advanced wireless systems across the breast lesion localization methods market.

By Technology: Magnetic Seeds Erode Wire-Guided Legacy

Wire guidance still held 34.38% of 2025 revenue because many hospitals own legacy kits that carry minimal incremental cost. Magnetic seed localization, however, is rising at 8.49% a year as facilities sidestep nuclear licensing headaches and same-day scheduling bottlenecks. Radar reflector systems and RFID tags complement growth by offering indefinite implant dwell times and multi-lesion tracking with minimal signal interference.

Radioisotope seeds are falling out of favor after new NRC rules raised compliance costs, and optical or photoacoustic alternatives remain in early trials. As procurement cycles refresh, magnetic and radar platforms are set to convert a sizable slice of the breast lesion localization methods market share currently occupied by wires.

By End User: Ambulatory Surgical Centers Capture Momentum

Hospitals generated 56.87% of 2025 revenue, reflecting their role in complex oncology care, but specialty breast clinics recorded the fastest 7.61% CAGR after CMS extended reimbursement parity in January 2025. Specialty breast clinics inside urban corridors now bundle imaging, biopsy, and localization into one visit, pushing same-day discharge rates to new highs.

Wireless localization aligns perfectly with that outpatient model, trimming scheduling friction and avoiding radiology licensing hurdles. Although startup costs between USD 2-4 million limit clinic proliferation, private-equity funding is flowing toward hub-and-spoke concepts that anchor novel technologies squarely within the breast lesion localization methods market.

Geography Analysis

North America generated 40.37% of 2025 global revenue as the dense-breast notification mandate spurred supplemental imaging and wireless marker adoption. U.S. hospitals quickly embraced Hologic’s Magseed and Merit Medical’s SCOUT, which together marked 28% of all localization procedures last year. Canada followed with Ontario approving magnetic seed reimbursement in April 2025, while Mexico’s public system expanded screening but still limits wireless coverage to private centers.

Europe is harmonizing CE-Mark pathways under the Medical Device Regulation, smoothing entry for radar reflectors and RFID tags. Germany’s insurers began paying 90% of magnetic seed costs in early 2025 and France is evaluating wireless localization across 40 centers; meanwhile, NHS capital rationing delays upgrades in the United Kingdom. Southern Europe’s austerity freezes add further drag on the regional breast lesion localization methods market size.

Asia-Pacific is the fastest riser at an 7.93% CAGR, powered by China’s 150 million-woman rural screening push, India’s digital referral engine, and South Korea’s 68% mammography coverage. Japan cleared MRI-visible Magseed in late 2025, and Australia has tightened radio-seed disposal rules, prompting tertiary centers to switch to magnetic and radar systems. Nonetheless, reimbursement lags in many ASEAN markets, tempering the near-term breast lesion localization methods market share potential.

The Middle East & Africa and South America remain constrained by limited public funding and radioisotope import hurdles. Brazil’s SUS covers magnetic seeds below cost, South Africa’s pilot NHI omits wireless localization, and Argentina’s public screening drive lacks device coverage outside private clinics.

Competitive Landscape

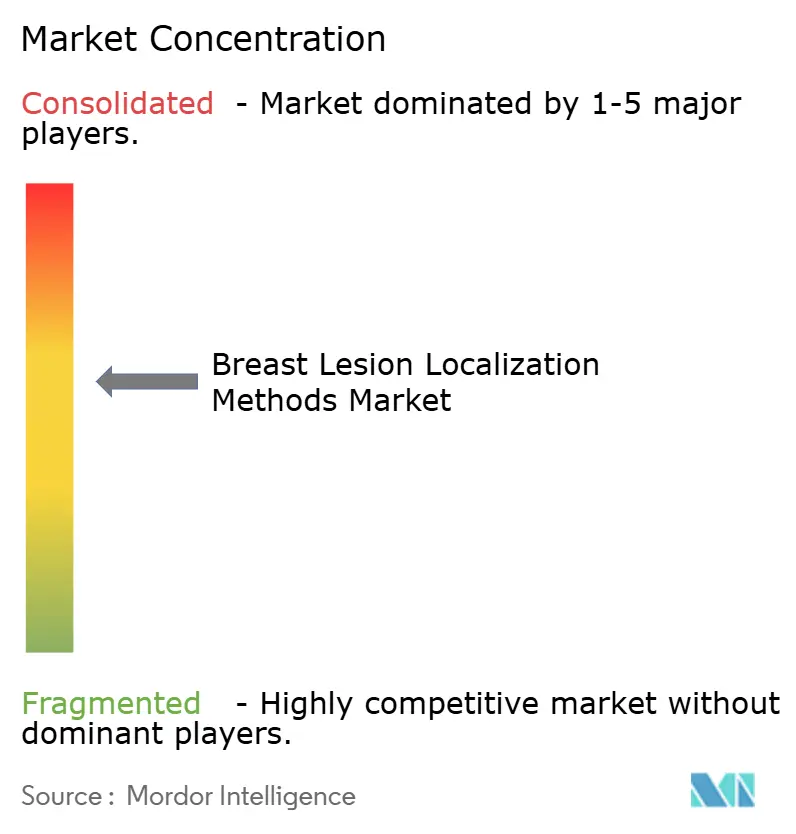

The breast lesion localization methods market exhibits moderate concentration. With Hologic cementing magnetic seed leadership after acquiring Endomagnetics. Merit Medical differentiates through a radar reflector that can stay implanted indefinitely, winning share among surgeons handling multifocal tumors.

Smaller firms such as Sirius Medical and Soteria Medical capitalize on EU regulatory windows to trial RFID and GPS-guided tags before U.S. entry. Competitive positioning now hinges on bundling hardware with navigation or AI-driven margin tools. Hologic’s Brainlab tie-up and BD’s consumables-centric EnCompass illustrate how ecosystem control is replacing single-device selling inside the breast lesion localization methods market.

Vendors also battle for clinical mindshare through education. Hologic trained 320 surgeons under its Magseed Academy in 2025, and Merit certified 180 under SCOUT programs, addressing workforce gaps that otherwise hinder adoption. Firms able to finance training, software, and hardware as a single package stand to capture incremental breast lesion localization methods market share without steep price competition.

Breast Lesion Localization Methods Industry Leaders

Hologic Inc.

Merit Medical Systems

Danaher Corporation

Stryker

Becton, Dickinson and Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: BD received FDA clearance for the EnCor EnCompass biopsy-localization system that melds real-time ultrasound with marker deployment to reduce re-excisions.

- January 2026: QT Imaging signed an exclusive UAE distribution deal for its FDA-cleared Breast Acoustic CT scanner and cloud platform, introducing a 3D, radiation-free imaging alternative to the Gulf market.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the breast lesion localization methods market as all single-use consumables and reusable guidance systems that help surgeons mark, track, or retrieve suspicious breast tissue before or during lumpectomy or biopsy procedures. Technologies covered span wire-guided needles, radioactive seeds or tracers, radar and radio-frequency tags, magnetic seeds, and radar reflectors that are sold to hospitals, ambulatory surgical centers, and specialty clinics across 17 countries.

Scope exclusion: imaging equipment such as mammography or ultrasound consoles is not included.

Segmentation Overview

- By Product Component

- Localization Devices

- Detection / Reader Systems

- Accessories & Consumables

- Software / Analytics Platforms

- By Imaging-Guidance Modality

- Ultrasound-Guided Procedures

- Mammography / Stereotactic-Guided Procedures

- MRI-Guided Procedures

- CT-Guided Procedures

- By Lesion Palpability

- Non-Palpable Lesions

- Palpable Lesions

- By Technology

- Wire-Guided Localization (WGL)

- Radioisotope Seed Localization (RSL)

- Magnetic Seed Localization

- Radar Reflector Localization

- Radiofrequency Identification (RFID) Tags

- Other Emerging Technologies

- By End User

- Hospitals

- Ambulatory Surgical Centers

- Specialty Breast Clinics

- Other End Users

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Structured interviews with breast surgeons, interventional radiologists, OR managers, and procurement heads in North America, Europe, and high-growth Asian markets helped us clarify typical localization mix, average selling prices, upgrade cycles, and reimbursement shifts that are rarely disclosed in desk sources. Their feedback closed data gaps and guided assumption ranges before final modeling.

Desk Research

Mordor analysts first compiled publicly available cancer statistics and procedure volumes from tier-1 sources such as WHO-IARC GLOBOCAN, the American Cancer Society, Eurostat, and national device registries. We enriched these with import-export shipment lines, patent filings on novel seed markers, and device approval data from the U.S. FDA and European notified bodies, then cross-checked commercial signals in company 10-Ks, investor decks, and reputable business media carried on Dow Jones Factiva and D&B Hoovers. The sources listed illustrate the breadth of literature consulted; many additional references were reviewed to complete data gathering and validation.

Market-Sizing & Forecasting

We built a blended top-down and bottom-up model. Starting with national breast-cancer screening volumes, positive screen rates, and breast-conserving surgery penetration, we calculated the addressable demand pool, which was then reconciled with sampled supplier shipments and channel checks to fine-tune totals. Key variables like procedure growth, localization method split, weighted ASP movements, female 40-plus population, and guideline-driven adoption of wire-free systems drive yearly changes. A multivariate regression linked these drivers to historic revenues, while scenario analysis handled reimbursement or technology-switch shocks. Where bottom-up estimates lagged, averages from matched facilities were imputed after expert review.

Data Validation & Update Cycle

Output tables pass a two-step peer review, variance checks against independent metrics, and anomaly resolution before sign-off. Our models refresh every twelve months, with interim updates when material events, such as product recalls, major acquisitions, or reimbursement changes, occur. A final analyst sweep ensures clients receive the latest vetted figures.

Why Mordor's Breast Lesion Localization Methods Baseline earns trust

Published values often diverge because firms pick different product mixes, price bases, and refresh rhythms.

Key gap drivers for this market include whether radar reflectors and magnetic seeds are counted alongside legacy wires, choice of exchange rates, and whether revenues are stated at ex-factory or distributor levels. Mordor reports full device revenues at manufacturer selling price and widens scope to all high-volume regions, whereas some publishers track only high-income markets or exclude newer wireless systems.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 2.46 B (2025) | Mordor Intelligence | - |

| USD 2.48 B (2025) | Global Consultancy A | Similar scope; fewer primary interviews so limited ASP validation |

| USD 0.30 B (2023) | Industry Association B | Tracks only wire devices and reports ex-factory prices for the U.S. and EU-5 |

| USD 0.42 B (2024) | Regional Consultancy C | Covers developing countries only; excludes radar and magnetic systems |

In sum, by marrying wide-ranging public data with direct clinician insight and an annually refreshed model, Mordor Intelligence delivers a balanced, transparent baseline that decision-makers can confidently rely on.

Key Questions Answered in the Report

How fast is demand for wireless breast lesion localization devices growing?

Magnetic seed localization segment is expanding at an 8.49% CAGR to 2031 as hospitals replace wires and radio-seed systems.

Which imaging modality is gaining the most share in localization procedures?

MRI-guided workflows are the fastest riser, forecast to grow 7.5% annually due to dense-breast mandates and MRI-visible markers.

Why are ambulatory surgical centers increasing procedure volumes?

CMS reimbursement parity introduced in 2025 lets ambulatory centers bill lumpectomies at hospital rates, fueling an 8.14% CAGR in their localization revenue.

What limits adoption of wireless localization in emerging markets?

Public insurance often covers only wire guidance, leaving patients to pay out-of-pocket for magnetic seed or radar systems.

How are vendors addressing the shortage of trained breast surgeons?

Companies like Hologic and Merit Medical run certification programs that give surgeons hands-on experience with wireless localization tools.

Page last updated on: