3D Projector Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 4.48 Billion |

| Market Size (2031) | USD 5.95 Billion |

| Growth Rate (2026 - 2031) | 5.86% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

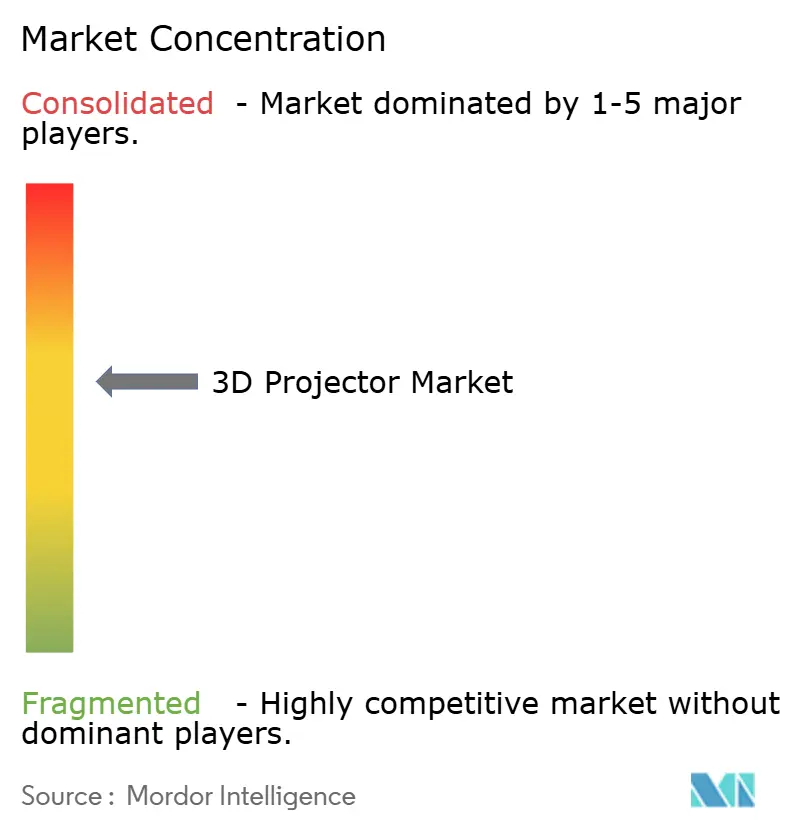

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

3D Projector Market Analysis by Mordor Intelligence

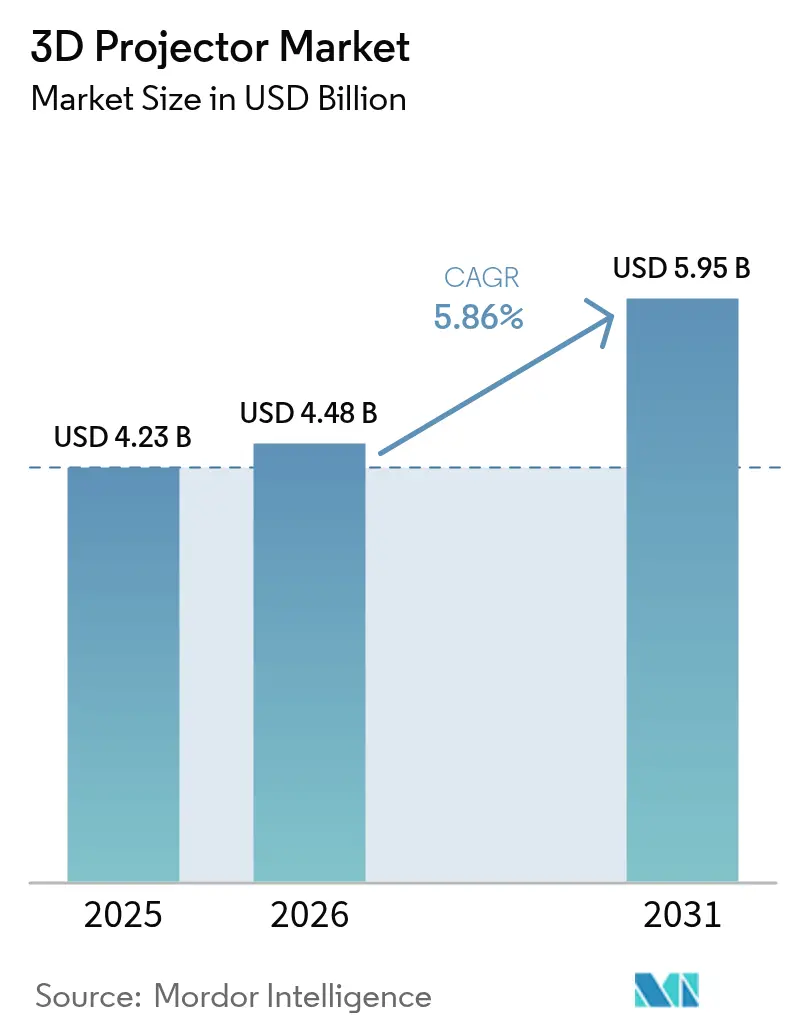

The 3D projector market size was valued at USD 4.23 billion in 2025 and estimated to grow from USD 4.48 billion in 2026 to reach USD 5.95 billion by 2031, at a CAGR of 5.86% during the forecast period (2026-2031). Progress continues despite growing interest in direct-view LED because laser illumination, advanced image processors and falling cost-per-lumen keep projection competitive for both fixed and portable uses. High-brightness laser platforms dominate professional venues, while battery-powered pico models gain traction in home entertainment and pop-up retail. Demand for 4K resolution and ≥10,000-lumen systems is expanding fastest as venues seek brighter, sharper images that stand up to ambient light. At the same time, e-commerce is changing how buyers research and procure equipment, pushing manufacturers to simplify installation and offer richer online product data.

Key Report Takeaways

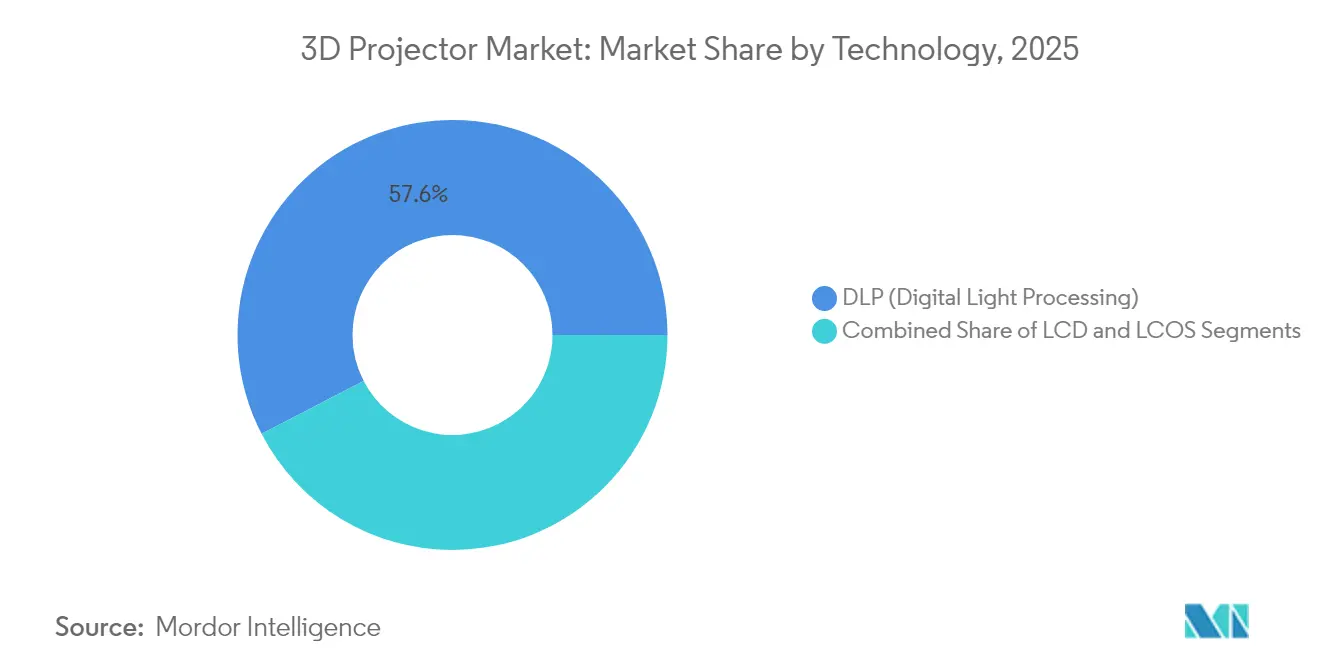

- By technology, DLP systems held 57.60% of the 3D projector market share in 2025; LCOS is projected to grow at a 5.95% CAGR through 2031.

- By light source, laser projectors commanded 46.10% of the 3D projector market size in 2025, while LED models recorded the fastest 8.05% CAGR to 2031.

- By brightness, 4,000-9,999-lumen units captured 35.50% of the 3D projector market size in 2025; ≥10,000-lumen models are rising at a 7.25% CAGR.

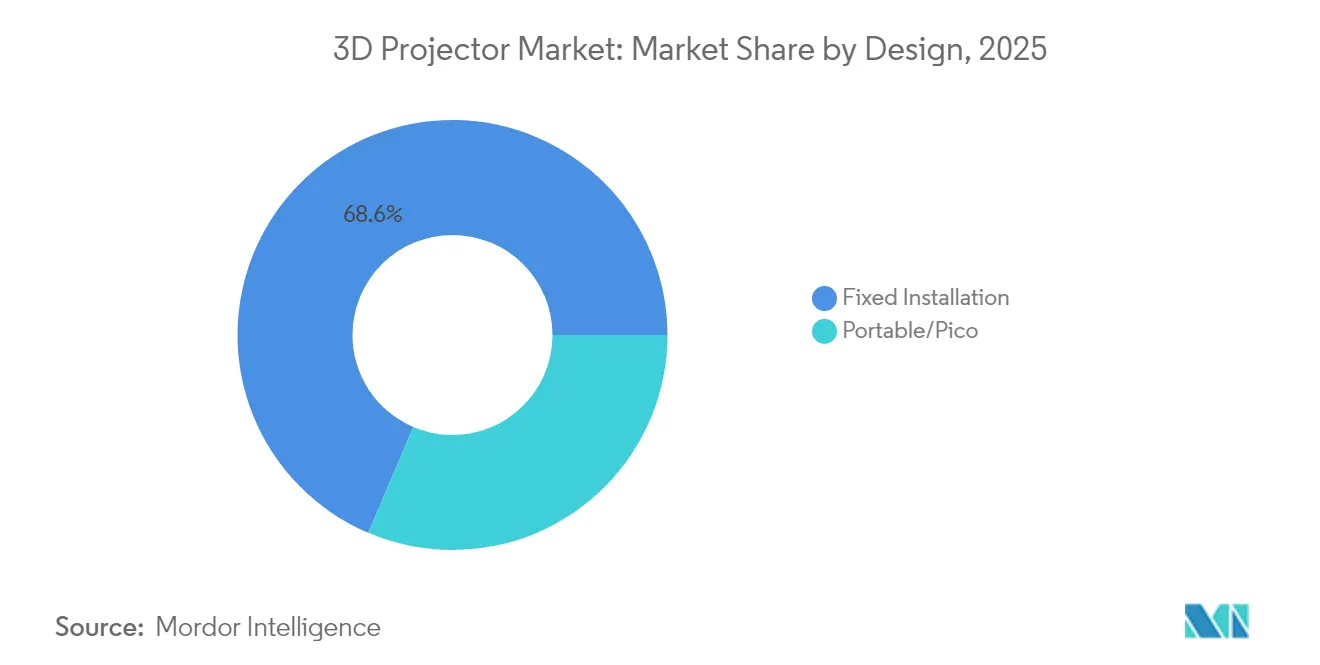

- By design, fixed-installation products led with 68.60% revenue share in 2025; portable and pico units are expanding at a 8.75% CAGR.

- By end-user, cinema accounted for 32.00% of the 3D projector market size in 2025; events and large venues post the highest 6.45% CAGR.

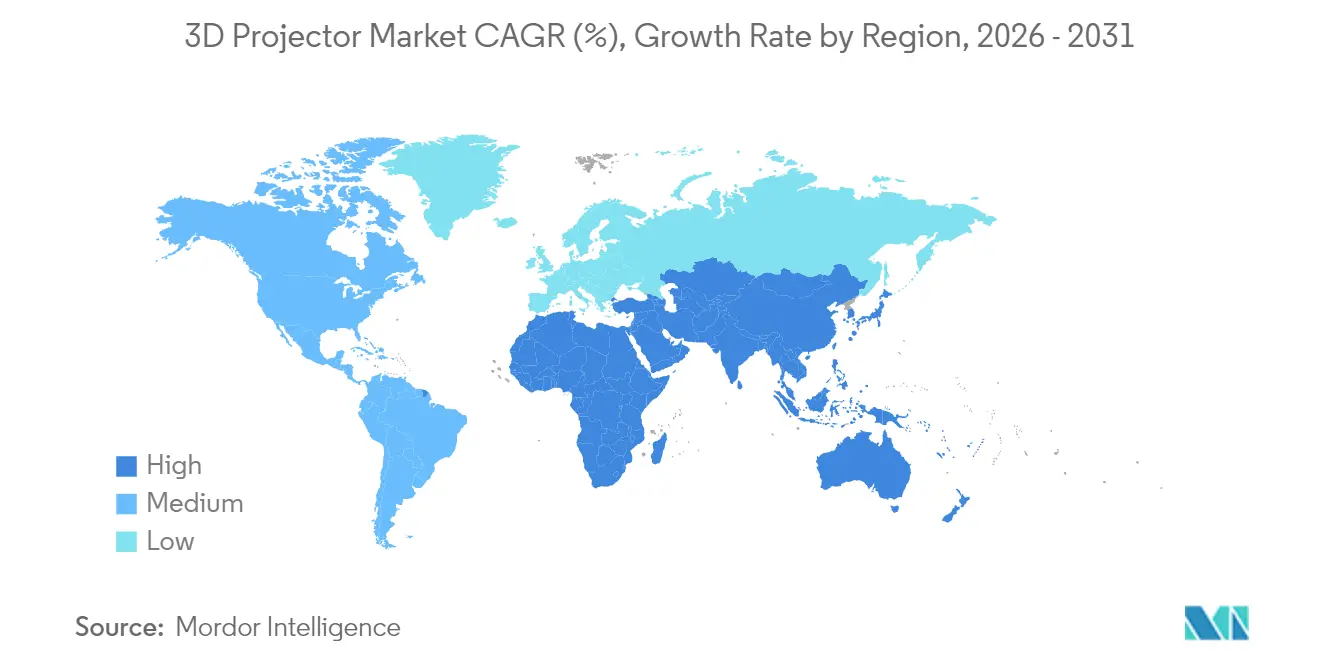

- By geography, Asia Pacific held 41.70% of revenue in 2025, while the Middle East and Africa is the fastest-growing region at 6.90% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global 3D Projector Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Laser-phosphor light sources cut TCO | +1.2% | North America and Europe | Medium term (2–4 years) |

| Immersive theme parks and attractions | +1.0% | Asia Pacific and Middle East | Medium term (2–4 years) |

| Smart-classroom rollouts | +0.8% | Asia Pacific | Short term (≤2 years) |

| Revival of 4K-HDR 3D movies | +0.6% | Global | Medium term (2–4 years) |

| Enterprise metaverse rooms | +0.7% | North America and Europe | Long term (≥4 years) |

| Urban home-theatre adoption | +0.5% | Asia Pacific | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Proliferation of Laser-Phosphor Light Sources Enhancing TCO in Pro-AV Installations

Laser-phosphor illumination extends operating life to roughly 20,000 hours, slashes lamp-replacement downtime, and can trim total cost of ownership by 40% compared with legacy lamps.[1]Christie Digital, “Laser Illumination for Cinema,” christiedigital.com Professional venues leverage this stability to negotiate longer fixed-price service contracts and reduce mid-show failures. Consistent brightness and color over the projector’s life also improves brand standards for franchise cinema chains and touring productions. As laser pricing falls, channel partners bundle longer warranties that further de-risk capital outlays. These economics will keep laser platforms at the center of premium venue upgrades through the medium term, reinforcing a quality gap over lamp-based rivals in corporate, education, and entertainment settings.

Rapid Expansion of Immersive Theme Parks and Attractions in China and GCC

Large-format attractions in Shanghai, Dubai, and Riyadh increasingly specify multi-projector arrays exceeding 10,000 lumens per unit to deliver floor-to-ceiling visuals. Such projects fuel a 7.5% CAGR for the high-brightness tier, with suppliers like BenQ offering 4K simulation models fitted with proprietary dust-proofing to handle desert climates. Premium installs set new visual benchmarks that ripple into corporate innovation centers and higher-education labs. Content creators likewise shift pipelines toward higher resolutions and frame rates to match these brighter canvases, reinforcing hardware demand.

Government-Backed Smart Classroom 3D Deployments across India and ASEAN

National procurement programs standardize interactive 3D specifications across thousands of classrooms, accelerating volume adoption. India’s projector market alone is forecast to surpass USD 2.1 billion by 2029, with STEM curricula driving the requirement for stereoscopic visualization.[2]Vijay Sharma, “Rapid Growth of the Indian Projector Market,” dqindia.com Large tenders emphasise robust connectivity, low maintenance, and content-agnostic platforms, steering vendors toward laser-phosphor engines and open software ecosystems. Positive learning-outcome studies spur private schools to mirror state specifications, expanding addressable demand without further public funding.

Revival of 4K-HDR 3D Movie Releases by Hollywood and Chinese Studios

Studio slates show renewed interest in premium 3D titles as they court theatrical revenues that outperform 2D equivalents in average ticket price. With HDR finishing workflows now mature, content arrives brighter, with deeper contrast that pushes exhibitors to adopt projectors capable of higher peak lumens. This pull-through effect stabilizes cinema demand even as some premium auditoriums migrate to LED. Ancillary markets such as themed entertainment and home cinema also benefit from the richer content pipeline, keeping the 3D projector market vibrant across tiers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Direct-view LED cannibalization of premium cinema | –0.9% | North America and Europe | Medium term (2–4 years) |

| Motion sickness and eye fatigue in education | –0.5% | Global | Short term (≤2 years) |

| Weak 3D content infrastructure in emerging markets | –0.7% | Asia Pacific and Latin America | Medium term (2–4 years) |

| High Capex for small EU cinemas | –0.6% | Europe | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Direct-View LED Walls Cannibalizing Premium Cinema Screens

LED cinema displays deliver uniform brightness, high contrast, and no projection booth requirements, making them attractive for new construction. They circumvent issues such as polarization-related dimming in 3D presentation, reducing the functional advantage of projection. Capital costs remain higher, yet some multiplex operators justify the spend by repurposing freed-up booth space for additional seats or retail concessions. As LED pixel pitch tightens and price curves descend, projector vendors must sharpen differentiation in TCO and color accuracy to defend marquee auditoriums.

Motion Sickness and Eye-Fatigue Concerns in Education Use-Cases

Prolonged viewing of stereoscopic material can induce discomfort in younger students, prompting some school districts to restrict usage to short modules. Manufacturers respond with adjustable depth cues and lower frame-interleaving frequencies, but evidence-based guidelines are still evolving. The uncertainty deters smaller institutions from investing heavily in 3D-specific hardware, marginally slowing expansion in the education vertical until best practices are standardized.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: DLP’s Dominance Meets LCOS Momentum

Digital Light Processing maintained 57.60% of the 3D projector market share in 2025, reflecting its strong contrast and compact optical engine. The segment benefits from a mature component supply chain that keeps costs predictable for integrators. LCOS, however, is posting a 5.95% CAGR as design studios and premium home cinemas value its reduced screen-door effect and smoother images. Competitive positioning is becoming application-specific; DLP often prevails in portable and rental fleets, whereas LCOS secures high-fidelity simulators.

LCOS shipments will keep eroding DLP’s lead in scenarios where pixel density and color uniformity outweigh absolute brightness. Yet, the total 3D projector market size tied to DLP platforms is expected to stay significant through 2031 because deep channel inventories, firmware familiarity, and accessory ecosystems favor continuity. LCD remains relevant in cost-sensitive education tenders, though price gaps versus entry-level DLP are narrowing as laser engines head down-market.

By Light Source: Laser Leads, LED Accelerates

Laser units captured 46.10% of revenue in 2025, a clear signal that professional venues now prioritise maintenance-free operation over lower first cost. Vendor roadmaps increasingly differentiate between pure RGB systems for flagship auditoriums and laser-phosphor hybrids that balance cost and color gamut. The 3D projector market size for laser models is forecast to expand alongside falling diode prices and wider acceptance of 120-volt compatibility, which eases electrical planning.

LED’s 8.05% CAGR owes much to the portable and pico boom. Battery operation, near-instant on/off, and low thermals create user experiences that rival smart TVs, especially when paired with integrated streaming. Lamp-based products now cater almost exclusively to budget buyers who prioritise low acquisition cost over lifetime economics, and their share will continue declining as emerging markets leapfrog straight to solid-state illumination.

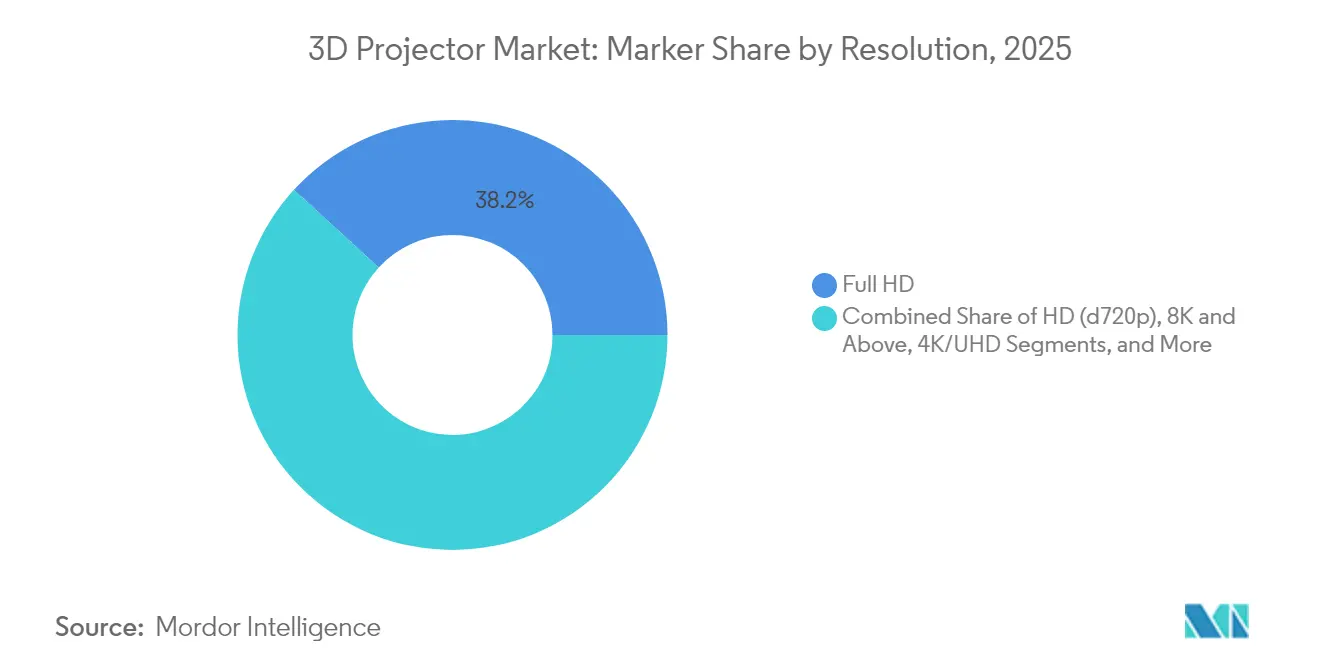

By Resolution: 4K Uptake Spreads Beyond Cinema

Full-HD kept 38.20% revenue share in 2025 because it balances clarity with bandwidth and content availability. Nevertheless, 4K/UHD shipments are climbing at 6.95% CAGR as enterprises and universities invest in higher-resolution collaboration spaces. Native-4K chips remain pricey, so brands deploy pixel-shift technologies such as JVC’s e-shiftX to deliver near-4K acuity at lower bit-rate overheads.

Above-4K, early 8K models serve as halo products, sustaining R&D in optics and image processing. While the 3D projector market share above 4K is small today, these flagships shape buyer expectations and provide technology trickle-down benefits to mid-tier lines over time.

By Brightness: High-Lumen Tier Broadens

Projectors rated 4,000-9,999 lumens held 35.50% market share in 2025, underpinning corporate auditoriums and mid-sized lecture halls. Their sweet-spot pricing wins against wall-mounted flat panels above 100 inches. Yet ≥10,000-lumen devices are advancing at 7.25% CAGR as immersive art exhibits, esports arenas, and worship venues demand ever-brighter canvases. Epson’s 20,000-lumen EB-PQ models run on standard mains power, removing a chief barrier to adoption.

Vendors also push brightness in portable form factors; 3-chip 3LCD engines now squeeze over 5,000 lumens into chassis suited for rolling racks. As buyers perceive brightness as the simplest spec for comparing value, lumen-led marketing will continue shaping product roadmaps.

By Design: Portables Disrupt Install Base

Fixed installations commanded 68.60% of revenue in 2025, supported by entrenched pro-AV channels and venue-specific rigging hardware. Long laser lifespans now stretch replacement cycles, tempering unit volumes but raising average selling price. Meanwhile, portable and pico units record 8.75% CAGR as remote work, micro-events, and pop-up retail intensify demand for displays that can travel. Users value compact chassis, auto-keystone, and smartphone mirroring—features migrating rapidly from consumer electronics into enterprise SKUs.

Manufacturers court this growth by shipping suitcase-ready lasers with integrated soundbars and Netflix certification, such as Formovie’s Google TV model. Fixed-rig vendors respond with modular lens kits and tool-free servicing to keep their platform economics compelling.

By End-User Application: Venues Diversify

Cinema kept a 32.00% share in 2025, anchored by emerging-market multiplex builds even as upper-tier screens test LED alternatives. Conversion to 4K laser maintains projection relevance by delivering HDR imagery that sustains premium ticket pricing. Education buying remains steady, but pedagogical trends toward blended learning favor interactive flat panels for front-of-class and projectors for immersive labs.

Events and large venues post a 6.45% CAGR on the back of touring concerts, esports tournaments, and experiential marketing. BenQ’s 10,000-lumen LU9800, rated for 360° operation, highlights how edge-blending and portrait orientation create new revenue models for rental houses. Home theatre and gaming continue to grow as streaming platforms release more HDR 3D titles.

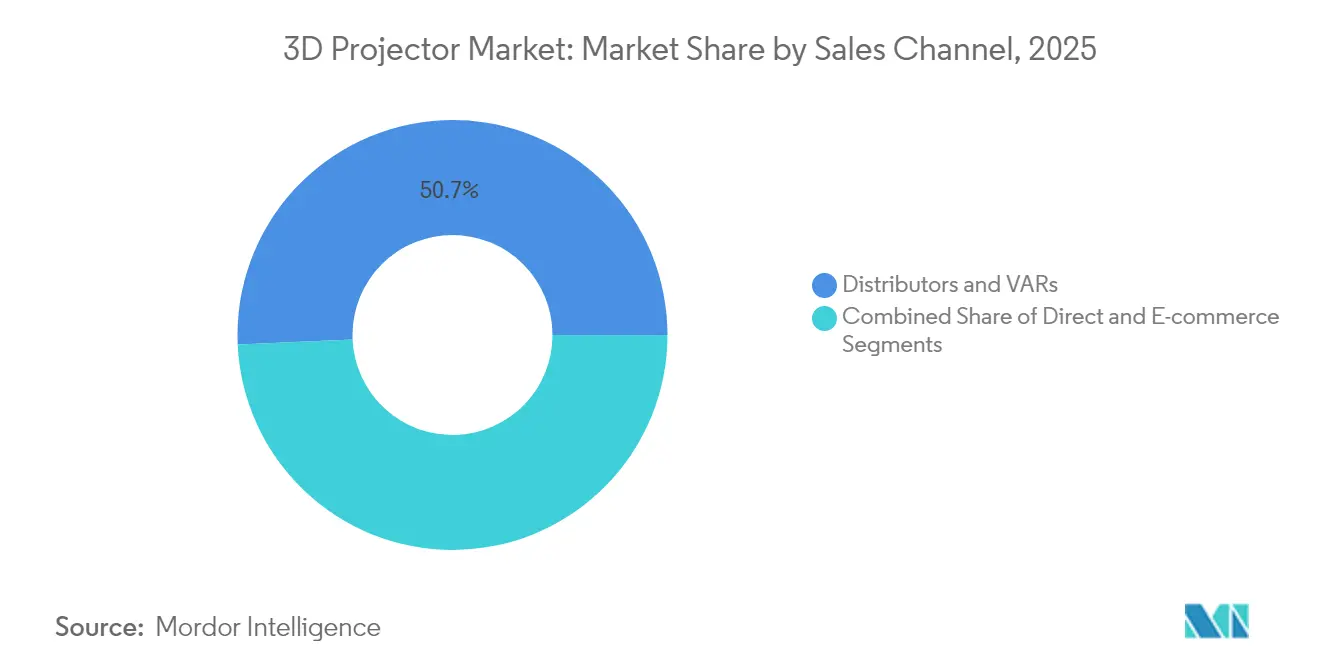

By Sales Channel: E-Commerce Rethinks Procurement

Distributors and VARs own 50.70% of 2025 revenue, leveraging deep integration know-how and bundled service agreements. Their share remains resilient in complex installs where site surveys and after-sales support are critical. E-commerce, however, is rising 9.25% CAGR, propelled by buyers in education and SMB segments who rely on granular online spec filters and peer reviews before checkout. Brands now deliver self-diagnostic firmware updates to cut support calls, aligning product design with the DIY ethos of online purchasing.

Direct OEM deals persist among top cinema chains and auto makers that negotiate bespoke optics or warranty terms. Overall, multichannel strategies become essential as buyers toggle between online research and in-person demos depending on project scope.

Geography Analysis

Asia Pacific led with 41.70% revenue in 2025, driven by China’s premium theme-park pipeline and India’s public-sector education programs. Chinese integrators source >10,000-lumen lasers for immersive rides, while Indian tenders specify mid-range interactive models for STEM labs, lifting regional shipments across price bands. Japan’s dense urban housing supports strong home-theatre uptake, reinforcing portable growth.

The Middle East and Africa post the highest 6.90% CAGR to 2031. GCC governments embed projection into cultural mega-projects and digital classrooms, often mandating RGB laser for marquee attractions. Saudi Arabia’s entertainment build-out accelerates demand for ≥20,000-lumen rigs able to withstand desert dust without external chillers. Content localization lags hardware rollouts, yet fiber upgrades and local studios are narrowing the gap.

North America and Europe see steady replacement demand as operators swap lamps for lasers to reduce service costs. Corporate users outfit metaverse visualization rooms that synergize with broader digital-twin strategies. Latin America remains challenged by currency swings, though Brazil’s cinema chains still prioritize projector upgrades over LED due to lower site-fit costs.

Regulatory Landscape

Product compliance for 3D projectors is anchored in laser and optical-radiation safety, especially as laser platforms lead (46.10% revenue share in 2025) and move into higher brightness classes. The IEC published updates that affect laser-based projection qualification and test practices, including IEC TS 60825-13:2026 (released February 2026) and the IEC 60825:2026 series for laser product safety (released July 2026). These updates shape how OEMs classify laser projectors and document measurement methods across global markets.

Accessibility and national-market certification requirements also add firmware and documentation work alongside hardware safety. In the United States, the Federal Communications Commission set a compliance deadline in August 2026 for 47 CFR 79.103(e) covering closed captioning display settings accessibility on covered devices, bringing UI and settings-menu design considerations into product roadmaps for smart and streaming-enabled projectors. In China, GB/T 4706.43-2024 for household projector safety transitions into implementation in August 2026, tightening conformity expectations for consumer-class models entering regulated retail channels.

Value Chain Analysis

Upstream component control shapes the 3D projector ecosystem: Texas Instruments remains central for DLP DMD supply, Epson is a key source of 3LCD panel engines, and laser diode supply has historically leaned on Japanese players such as Nichia, with more China-based alternatives emerging. As laser illumination extends operating life to roughly 20,000 hours and reduces maintenance interventions, OEMs and integrators increasingly treat optics, thermal design, and firmware as platform elements that support longer service contracts and remote fleet management, particularly in cinema, events, and large venues.

Midstream manufacturing and integration are adapting to trade and availability risks through dual sourcing and footprint adjustments. Industry commentary around tariffs and China-origin electronics has driven some brands to reassess assembly locations and supplier mixes, while channels continue to split between complex installs handled by distributors and VARs (50.70% revenue share in 2025) and faster-moving online procurement via e-commerce. A visible upstream localization push appeared in May 2026 when Sonnoc announced a partnership with Huawei HiSilicon to co-develop projector-relevant triple-color laser diodes and display chips, showing how some vendors are trying to reduce reliance on incumbent component geographies and improve cost control for professional-class systems.

Competitive Landscape

The top five suppliers - Epson, Sony, Barco, Christie Digital, and BenQ - controlled roughly 60% of global revenue in 2024, indicating moderate concentration. Technology roadmaps split between premium RGB laser aimed at large venues and cost-optimised LED for portables. Sony re-entered Europe with its BRAVIA Projector 7, signalling renewed regional emphasis after portfolio consolidation. Epson continues to stretch laser brightness while simplifying power requirements to defend rental-staging share.[6]Epson, “Epson Boosts the Accessibility of Large Venue Projectors,” news.epson.com

Chinese upstarts Xiaomi and Hisense leverage domestic economies of scale to undercut incumbents abroad, especially in sub-USD 1,000 smart projectors. Hisense’s Light Steering demo with Barco at CES 2025 illustrated collaboration across value-chain boundaries to address HDR limitations in projection. Niche players specialise in simulation, faith venues, or architectural mapping, often bundling software and calibration services to shield margins.

Component ecosystems also evolve: laser diode vendors push blue-pump phosphor efficiency past 5 W output per emitter, while Texas Instruments scales DMD wafer sizes to lower per-mirror cost. These upstream dynamics influence downstream pricing strategies and open space for ODM partnerships targeting white-label consumer brands.

3D Projector Industry Leaders

Seiko Epson Corp.

Sony Corp.

Barco NV

BenQ Corp. (Qisda)

Optoma Corp. (Coretronic)

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

High-brightness, premium-color laser architectures remain a key whitespace where vendors compete on performance and cost structure, not only on lumen counts. In May 2026, Sonnoc introduced its Xiaolong series built around pure triple-color laser technology and tied the push to a Huawei HiSilicon collaboration aimed at improving access to critical components (laser diodes and display chips). These moves broaden the supplier set available for professional installations and create room for new product tiers in immersive attractions, museums, and large-venue mapping, where buyers compare color volume, stability, and serviceability across multi-projector arrays.

On the demand side, procurement programs and venue formats already highlighted in this report favor platforms that reduce installation friction while supporting richer content formats. Smart-classroom tenders across India and ASEAN emphasize robust connectivity and low maintenance, reinforcing the opportunity for laser-phosphor and solid-state portfolios paired with open software ecosystems. At the same time, the shift toward higher-resolution, higher-brightness installations, including >=10,000-lumen systems, strengthens opportunities for OEMs and channel partners to attach recurring value through calibration, edge-blending, and remote monitoring. This aligns with the market shift toward longer-life light engines and service-led relationships in professional segments.

Recent Industry Developments

- June 2026: Seiko Epson announced the EB-XQ2030B, a 30,000-lumen 4K laser 3LCD projector positioned for immersive environments. The launch extends Epson’s reach in the extreme-brightness tier used by large venues and multi-projector installations, where spec leadership can influence rental and staging fleet refreshes even when projects deploy mixed 2D/3D workflows.

- November 2025: Seiko Epson expanded its professional laser projector positioning through a corporate update that supported its broader projection roadmap. The move underscored continued investment in higher-brightness, solid-state platforms that integrators standardize across venues to reduce maintenance complexity and normalize long service intervals.

- August 2024: Seiko Epson introduced Q-Series 4K laser projectors, widening availability of higher-resolution laser options for premium installs. This broadened product availability helps channel partners package 4K-capable systems for home cinema, education labs, and corporate visualization rooms where resolution and brightness are increasingly used as procurement shortcuts.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers revenues earned from 3D projectors sold for displaying stereoscopic content that creates a depth effect when viewed using compatible methods such as active or passive glasses. We count the value of the projector hardware sold into home, education, business, cinema, and large venue uses.

Scope exclusions: Excludes pure 2D projectors, temporary rentals and event services, and aftermarket 3D conversion kits sold separately from a projector.

Segmentation Overview

- By Technology

- DLP (Digital Light Processing)

- LCD

- LCOS

- By Light Source

- Laser (Solid-State and Laser-Phosphor)

- LED

- Lamp-Based

- Hybrid/Phosphor-LED

- By Resolution

- HD (≤720p)

- Full-HD (1080p)

- 4K/UHD

- 8K and Above

- By Brightness (ANSI Lumens)

- Less than 2,000

- 2,000-3,999

- 4,000-9,999

- ≥10,000

- By Design

- Fixed Installation

- Portable/Pico

- By End-user Application

- Cinema

- Education

- Home Theatre and Gaming

- Business and Corporate

- Events and Large Venues

- Other Applications

- By Sales Channel

- Direct (B2B/OEM)

- Distributors and VARs

- E-Commerce

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Saudi Arabia

- United Arab Emirates

- Turkey

- South Africa

- Rest of Middle East and Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work was used to map the demand pool and the supply landscape before assumptions were set. We referenced public sources such as USITC and UN Comtrade trade statistics for projector-related flows, World Bank and IMF macro indicators for spending context, and OECD education statistics that help explain how quickly classrooms adopt new display equipment.

To connect product trends with realistic price and replacement cycles, we also reviewed sources such as FCC filings and notes from relevant international standards where they inform compliance and design timelines, plus peer-reviewed optics and display journals for technology direction. Company annual reports, earnings call transcripts, and investor presentations were used to track shifts between lamp and laser models and how channel inventory moved. In a few places, paid subscriptions for company financials and news intelligence were used to cross-check shipment announcements and segment commentary. The desk sources listed here are illustrative only, and many other public references were also used for data collection, validation, and research clarification.

Primary Interviews and Surveys

Primary work focused on validating how 3D projector demand is purchased and replaced across key use cases, including home entertainment, education, corporate training, and cinema and large venues. We spoke with a mix of manufacturers, component ecosystem participants, distributors, and professional AV integrators across APAC, EMEA, and the Americas, and used their inputs to confirm pricing ranges, attach rates for 3D features, and the way laser adoption feeds into refresh decisions.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 37% | CXOs: 14% | APAC: 43% |

| Mid tier: 45% | Functional/Unit leaders: 38% | EMEA: 37% |

| Smaller Players: 18% | Managers: 48% | Americas: 20% |

Market-Sizing & Forecasting

Sizing started with a top-down build where import and production signals, combined with regional demand indicators, were used to reconstruct the addressable revenue pool for 3D-capable projectors. Once that frame was set, the totals were corroborated through selective bottom-up checks using sampled price bands by brightness class, channel discussions on unit volumes, and sanity checks on supplier mix where data gaps existed.

Key inputs used in the model included average selling price progression by light source (lamp versus laser), replacement cycles by use case (home versus education versus cinema), adoption rate of 3D features within the broader projector category, venue count and screen upgrades for large-format projection, and regional discretionary spending signals that affect premium electronics purchases. Forecasting relied mainly on scenario analysis supported by expert views, since adoption can swing based on content availability and capex cycles, and then the scenario outputs were cross-checked against trend smoothing on historical growth where it was consistent. Where direct volume clues were limited, ranges were set from interview feedback and narrowed using trade and macro signals so the final numbers stayed reproducible and easy to revisit.

Data Validation & Update Cycle

Model outputs were checked against independent signals like broader projector shipments, trade value movement, and announced capacity and product-cycle timing, and then variances were reviewed before sign-off. When a region showed an unusual spike or drop, we re-checked currency timing, price assumptions, and whether a one-off cinema or education procurement wave was distorting the pattern.

A second analyst review is completed to confirm that assumptions are applied consistently across regions and that growth rates align with the stated drivers. Reports are refreshed annually, and interim updates are made when material events occur, such as step changes in laser pricing or major procurement programs. Before delivery, a final pass is done so clients receive the latest view available at the time of release.

Mordor Intelligence's 3d Projector Market Size Compared Against Other Published Estimates

Published market sizes for 3D projectors often differ because each publisher draws the line differently on what counts as a 3D unit, which years are treated as the base, and how fast prices are assumed to move as laser models gain share. Differences also show up when some studies lean on long-range growth stories while others anchor more tightly on near-term replacement cycles.

The main gap drivers in this market are usually scope and timing, such as whether embedded software and light-engine value is counted with hardware, whether rental and installation services are included, and how currency conversion is handled for multi-region totals. Some estimates also start from a broader projector demand pool and apply a single 3D adoption rate, while others build separate adoption curves by use case, which can change the starting number and the slope.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 4.48 B (2026) | |

| Global Consultancy A | USD 4.70 B (2025) | Uses an earlier base year and a hardware-only framing, which can inflate the current value if 3D capability is inferred from product families rather than verified at the model level. |

| Industry Publisher B | USD 4.08 B (2024) | Anchors on an earlier historical year and applies a longer forecast horizon with faster expansion assumptions, which tends to pull the near-term size down while pushing later-year values up. |

The table shows that year choice and what is bundled into the counted revenue explain most of the spread, and those differences compound quickly once pricing and adoption curves are projected forward. By keeping rentals and add-on conversion kits out of scope and treating embedded value consistently inside projector sales, the 2026 figure stays tied to a cleaner demand pool, which is the treatment used by Mordor Intelligence.

Key Questions Answered in the Report

What is the current size and forecast growth of the 3D projector market?

The 3D projector market stands at USD 4.48 billion in 2026 and is projected to reach USD 5.95 billion by 2031, advancing at a 5.86% CAGR during the forecast period (2026-2031).

Which region holds the largest share of the 3D projector market?

Asia Pacific leads with 41.70% revenue in 2025, supported by China’s premium attractions and India’s large-scale smart-classroom rollouts.

Which projection technology is growing fastest?

LCOS is the fastest-growing technology segment, expanding at a 5.95% CAGR from 2026 to 2031 due to its high pixel density and smooth images.

How do laser light sources affect total cost of ownership?

Laser-phosphor engines offer up to 20,000 hours of maintenance-free use, cutting TCO by as much as 40% versus lamp systems while keeping brightness stable.

Why is e-commerce becoming a key channel for 3D projector sales?

Online platforms enable quick price and spec comparisons, driving a 9.25% CAGR in e-commerce sales as home-entertainment and SMB buyers prefer direct purchase.

What is the main restraint on premium-cinema 3D projectors?

Direct-view LED walls are displacing projectors in top-tier auditoriums by delivering higher brightness and contrast without a dedicated projection booth.

Page last updated on: