Cooling Tower Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 4.59 Billion |

| Market Size (2031) | USD 5.89 Billion |

| Growth Rate (2026 - 2031) | 5.09% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cooling Tower Market Analysis by Mordor Intelligence

Cooling Tower Market size in 2026 is estimated at USD 4.59 billion, growing from 2025 value of USD 4.37 billion with 2031 projections showing USD 5.89 billion, growing at 5.09% CAGR over 2026-2031.

Continued capital formation in power generation and the build-out of hyperscale data-center campuses keep high-capacity evaporative systems in demand, while hybrid wet-dry designs scale faster as operators react to tightening water-use and energy-efficiency regulations. The accelerated adoption of counter-flow configurations, growth in installations exceeding 20 MW, and the shift to PFAS-free fill materials further reinforce the cooling tower market’s growth trajectory. Suppliers capable of integrating digital twin analytics, predictive maintenance, and alternative make-up-water schemes hold an execution edge as sustainability mandates intensify.

Key Report Takeaways

- By flow type, cross-flow cooling towers led the market with a 56.90% share in 2025, while counter-flow cooling towers are forecast to expand at a 7.69% CAGR through 2031.

- By tower type, evaporative systems accounted for 66.40% of the cooling tower market size in 2025, whereas hybrid wet-dry units are expected to log the fastest growth rate of 8.34% CAGR.

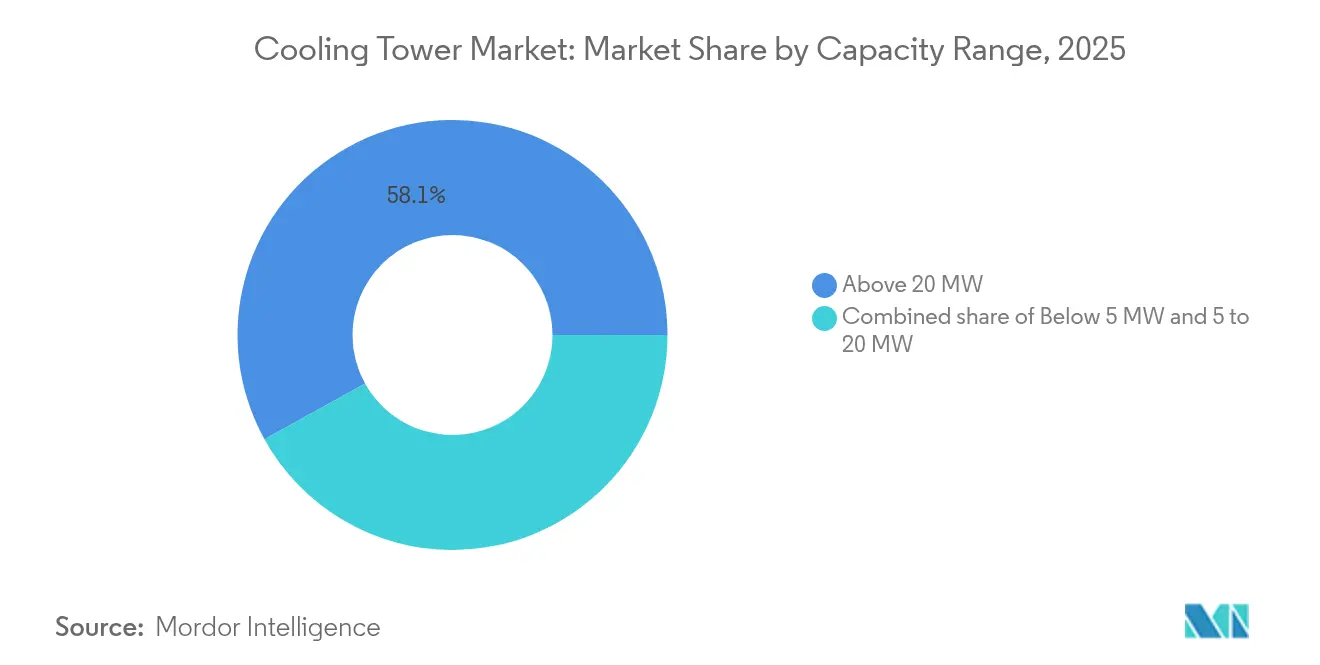

- By capacity, installations above 20 MW accounted for a 58.05% share of the cooling tower market size in 2025 and are projected to advance at a 6.08% CAGR.

- By application, power generation held 38.60% of the cooling tower market share in 2025, while data centers are projected to grow at a 9.05% CAGR through 2031.

- By geography, the Asia-Pacific region led with a 43.70% revenue share in 2025, growing at a 6.78% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cooling Tower Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding HVACR installations in commercial real-estate | 1.80% | Global, with concentration in North America and Asia-Pacific | Medium term (2-4 years) |

| Power plant capacity additions in Asia and Middle East | 0.90% | Asia-Pacific core, spill-over to Middle East | Long term (≥ 4 years) |

| Stringent water-use and energy-efficiency mandates (CTI, ASHRAE) | 0.70% | North America and Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Industrialization and refinery upgrades in emerging economies | 0.60% | Asia-Pacific, Middle East, and South America | Long term (≥ 4 years) |

| Rapid build-out of hyperscale data-center campuses | 0.50% | Global, with early gains in North America, Europe, Asia-Pacific | Short term (≤ 2 years) |

| Green hydrogen electrolyzer projects needing process cooling | 0.40% | Europe and North America, with pilot projects in Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expanding HVACR Installations in Commercial Real-Estate

The rapid commercialization of mixed-use complexes and high-specification data centers is driving developers toward higher-capacity, digitally monitored evaporative and hybrid systems. Johnson Controls reported a USD 13.1 billion order backlog as smart-building owners specify cooling towers equipped with demand-responsive controls that synchronize with building automation servers.[1] Johnson Controls, “Q1 FY25 Earnings Presentation,” johnsoncontrols.com The integration of IoT sensors enables predictive maintenance routines that reduce downtime. Projects in water-stressed localities are increasingly selecting hybrid wet-dry units to meet compliance thresholds without compromising load-following capability. Suppliers that can validate real-world energy savings through CTI-certified performance testing gain a procurement advantage when property investors audit sustainability metrics.

Power Plant Capacity Additions in Asia and Middle East

Utilities in China, India, and the Gulf states are scaling nuclear, gas-fired, and renewable-hybrid plants that require high-capacity counter-flow towers to manage variable steam loads. China’s Heqi-1 industrial steam linkage delivers 4.8 million tonnes of process steam annually, underscoring the commercial benefits of integrating cooling towers into industrial heat-recovery loops. GCC utilities adopt seawater-cooled towers at coastal Combined Cycle Gas Turbine sites, reducing freshwater withdrawal and enabling capacity factors above 40% in extreme ambient temperatures. The Middle East’s move toward solar-thermal augmentation further positions hybrid systems as compliance-ready for future carbon pricing schemes.

Stringent Water-Use and Energy-Efficiency Mandates

CTI Standard 201 certification and ASHRAE Legionella guidelines tighten drift-rate limits and raise minimum cycles-of-concentration, compelling owners to modernize fill packs and automate biocide dosing. The CDC’s updated Legionella toolkit increases enforcement risk, encouraging facilities to adopt closed-loop or hybrid designs that reduce plume risk.[2]Centers for Disease Control and Prevention, “Legionella Control Toolkit,” cdc.gov Manufacturers that self-certify with CTI are investing in third-party test rigs to prove performance under part-load conditions, a differentiator in competitive bid rounds. Regulatory momentum has also stimulated R&D into PFAS-free fill media with comparable fouling resistance and thermal conductivity.

Rapid Build-Out of Hyperscale Data-Center Campuses

Hyperscale operators specify multi-cell modular towers that can be craned into position and tied to liquid-cooling loops within compressed construction windows. Baltimore Aircoil Company’s liquid-ready modules demonstrate drift losses below 0.0005% of water flow, meeting local discharge caps without auxiliary plume abatement systems. Operators demand redundancy levels of N+2, driving procurement of standardized tower skids that can be swapped with minimal site work. The shift to liquid racks increases outlet water temperature requirements, enabling towers to operate in economizer mode for extended periods and reducing annual water consumption.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High operating cost and water-scarcity concerns | -0.80% | Global, with acute impact in Middle East and Australia | Medium term (2-4 years) |

| Plume-abatement and drift-elimination compliance costs | -0.60% | North America and Europe, expanding globally | Short term (≤ 2 years) |

| Shift toward adiabatic dry coolers in ≤1 MW range | -0.40% | Europe and North America, with adoption in water-scarce regions | Medium term (2-4 years) |

| PFAS-fill material phase-out increasing retrofit over new build | -0.30% | North America and Europe, with regulatory spill-over to Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Operating Cost and Water-Scarcity Concerns

The total cost of ownership is rising because chemical conditioning and discharge fees now exceed electricity costs in many arid markets. Pacific Northwest National Laboratory case studies show that military installations are lowering makeup water demand by recovering HVAC condensate and rainwater; however, capital outlays for integrated storage push payback periods beyond five years.[3]Pacific Northwest National Laboratory, “Alternative Water Sources for Cooling Towers,” pnnl.gov Facilities in Australia and the Middle East, where water charges exceed USD 5 per 1,000 gallons, are increasingly justifying dry cooling or hybrid designs despite efficiency penalties. Suppliers that bundle performance guarantees with water-saving retrofits secure longer-term service contracts that smooth revenue volatility during new-build lulls.

PFAS-Fill Material Phase-Out Increasing Retrofit Demand

The EPA’s January 2025 TSCA amendment bans PFAS from new chemical exemptions, limiting legacy fill supply and prompting accelerated retrofit cycles.[4] U.S. Environmental Protection Agency, “TSCA Section 5 Amendments on PFAS,” epa.gov Ceramic and non-fluorinated polymer alternatives exhibit lower thermal conductivity, so owners compensate by using larger plan dimensions or multi-cell arrays. While this raises capital expense, it expands aftermarket service demand for specialist contractors who can execute turnkey media replacements within narrow outage windows. Vendors are also exploring additive-manufactured lattice fillers that promise higher surface-area-to-volume ratios; however, commercial availability is likely not until after 2027.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Flow Type: Counter-Flow Gains Efficiency Edge

Counter-flow installations captured 43.10% of the revenue in 2025 and are growing at a 7.69% CAGR, as data-center and pharmaceutical clients prioritize high L/G ratios and smaller footprints. Industrial heat-pump projects that couple counter-flow towers with process chillers deliver annual energy savings of over 15%, directly improving OPEX sensitivity in food & beverage plants. Cross-flow towers retain an installed-base advantage, particularly at coal and gas turbines, where low static-pressure drops ease auxiliary load. However, their share is expected to erode as water tariff escalators favor a more stringent approach to temperature control. Digital twin simulations confirm that counter-flow designs can cut operating cost by 5% when integrated with predictive reservoir management, further propelling share gains.

Legacy cross-flow units remain attractive for retrofit because fill packs are more accessible, and large surface areas accommodate fouling without immediate performance loss. Owners pursuing phased compliance strategies often refurbish cross-flow cells with low-drift eliminators to postpone capital replacement. Even so, new industrial complexes in Southeast Asia are standardizing counter-flow towers sized for a design wet-bulb depression of more than 10 °C, signaling a structural pivot that will reshape manufacturer product portfolios over the decade.

By Tower Type: Hybrid Systems Lead Innovation

Hybrid wet-dry models are advancing at an 8.34% CAGR, outpacing evaporative towers, which are expected to hold a 66.40% share in 2025. Utilities in water-stressed areas appreciate hybrid designs that switch to dry mode during drought restrictions, maintaining thermal compliance while cutting seasonal water draw by 50%. Field trials of perforated dew-point indirect evaporative modules confirm that supply-air ratios below 0.5 achieve optimal thermal efficiency gains, positioning hybrids as viable replacements for plume-abatement retrofits.

Evaporative towers dominate high-capacity applications because wet operation achieves approach temperatures within 3 °C of the wet-bulb temperature, which is crucial for steam-cycle efficiency. Suppliers hedge market risk by launching modular hybrid lines that retrofit onto evaporative basins, effectively transforming legacy assets. Material advances such as hydrophilic membrane fill promise to push hybrid outlet temperatures closer to wet operation benchmarks, intensifying competition for urban hospitals and semiconductor fabs where plume mitigation is non-negotiable.

By Capacity Range: Large-Scale Dominance Continues

The above 20 MW cohort holds a 58.05% share and is forecast to expand at a 6.08% annual rate as economies of scale justify investments in digital vibration monitoring, auto-chemical dosing, and variable-frequency fan drives. Babcock & Wilcox’s installed base of over 1,900 units illustrates owner preference for tier-one suppliers capable of delivering EPC-grade services and lifecycle support. Mid-sized (5–20 MW) units target district cooling networks in ASEAN smart-city projects, where modularity trumps megawatt density.

Sub-5 MW installations face competition from adiabatic coolers that boast near-zero plume and simplified permitting. Nevertheless, OEM roadmaps indicate compact induced-draft towers with integrated drift eliminators and composite casings, specifically targeting this segment, which reflects that certain pharmaceuticals and light industrial sites still prefer wet cooling for tighter approach temperatures. Capacity upgrades across aging North American refinery fleets will also sustain demand for segments exceeding 20 MW, especially where regulatory frameworks incentivize heat-rate improvements.

By Application: Data Centers Drive Growth

Data centers represent the fastest-growing end market, with a 9.05% CAGR. Liquid-cooled racks elevate heat rejection densities, prompting tower specifications that accommodate higher condensing water temperatures, thereby operating in water-saver modes for up to 80% of annual hours. The cooling tower market benefits as hyperscale developers standardize multi-cell skids shipped fully assembled to compress commissioning timelines.

Power generation retains the largest 38.60% revenue share due to its absolute heat-load intensity. Nuclear steam-supply integration projects, exemplified by China’s Heqi-1, highlight how utility-industrial partnerships extend tower usage beyond turbine condensers into process steam circuits. Oil & gas, as well as chemical facilities, contribute steady demand through rehabilitation cycles tied to throughput expansions. Meanwhile, commercial HVACR gains momentum from mixed-use skyscrapers that integrate central plant cooling with AI-driven building management systems.

Geography Analysis

The Asia-Pacific region commands 43.70% of the cooling tower market and is expected to grow at a 6.78% CAGR, driven by synchronized investments in power, petrochemical, and data center infrastructure across China and India. China’s nuclear-steam cogeneration model exemplifies the region’s integrated approach, combining industrial decarbonization targets with process heat optimization. India’s thermal power refurbishments increasingly specify hybrid towers to conform with draft national water norms that cap withdrawal intensity.

North America registers demand primarily from data-center expansions clustered in Virginia, Texas, and the Pacific Northwest, paired with refinery retrofits to remove PFAS-based fill. Stringent ASHRAE and EPA guidelines further shape procurement toward CTI-certified, low-drift cells. Europe sustains moderate growth as district energy schemes in Germany and Scandinavia adopt hybrid wet-dry towers to balance water stewardship and seasonal load variation. The Middle East and Africa are witnessing a rising uptake of seawater and dry towers attached to solar-thermal and desalination complexes, where freshwater scarcity commands a premium on zero-discharge cycles. South American momentum concentrates in Brazil’s mining corridors and Argentina’s soy-crushing hubs, both leaning on >20 MW counter-flow towers to handle high dust and variable loading. Collectively, these regional dynamics validate the cooling tower market’s resilience across climatic and regulatory mosaics.

Competitive Landscape

The cooling tower market is moderately fragmented, with top suppliers leveraging technology differentiation and service depth to maintain their market share. SPX Technologies grew its HVAC segment revenue 32.5% year-over-year to USD 356.5 million, driven by organic gains and acquisitions that filled portfolio gaps in hybrid and adiabatic lines. Vendors invest in digital twin platforms that simulate droplet drift, fouling trajectories, and fan energy under site-specific meteorology, enabling outcome-based contracts that resonate with CFOs scrutinizing lifecycle economics.

Johnson Controls’ USD 13.1 billion backlog signals customer confidence in suppliers that can integrate cooling towers into unified building-automation ecosystems. Partnerships with hyperscalers to pre-engineer module footprints shorten procurement cycles, creating a virtuous linkage between customization and standardization. M&A activity targets niche material science firms developing PFAS-free fills and ribbed composite casings, securing intellectual property against incoming regulation.

New entrants chase white-space in water-scarce geographies by promoting adiabatic and closed-loop systems that operate on greywater. Yet hurdles include limited CTI certification history and scaling challenges for large-capacity units. Established brands blunt disruption by offering extended warranties bundled with remote monitoring services, thereby elevating switching costs for facility owners. Over the forecast horizon, competitive intensity will center on sustainability credentials and the ability to guarantee measurable reductions in water and energy use.

Cooling Tower Industry Leaders

SPX Technologies, Inc.

Baltimore Aircoil Company, Inc.

EVAPCO, Inc.

Johnson Controls International plc

Hamon & CIE (John Cockerill SA)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: EPA’s TSCA amendments became effective, categorically excluding PFAS from new chemical exemptions and accelerating the shift to alternative fill materials in cooling tower applications.

- December 2024: The U.S. Department of Energy published a hydrogen electrolysis assessment detailing cooling requirements to achieve USD 1/kg hydrogen production targets.

- June 2024: China commissioned the Heqi-1 industrial nuclear steam project at Tianwan nuclear power plant, designed to supply 4.8 million tonnes of steam annually to petrochemical operations, showcasing integrated cooling system applications.

- May 2024: Baltimore Aircoil Company introduced the Series 3000 Cooling Tower, increasing capacity by up to 16% and exceeding ASHRAE 90.1-2013 energy standards.

Global Cooling Tower Market Report Scope

The cooling tower is a specially designed heat exchanger in which air and water are brought into direct contact to lower the water temperature. As a result, a small amount of water evaporates, lowering the temperature of the water cycle through the tower. Cooling towers are typically used for heating, ventilation, air conditioning (HVAC), and industrial operations. Cooling towers enable the cost-effective and energy-efficient operation of cooling systems.

The Cooling Tower Market is segmented by application type, flow type, type, and geography. By application type, the market is segmented into the oil industry, HVACR, chemical industry, power generation, and others. By flow type, the market is segmented into cross-flow and counter-flow. By type, the market is segmented into evaporative, dry, and hybrid cooling towers. The report also covers the size and forecasts for the cooling tower market across major regions. For each segment, the market sizing and forecasts have been done based on revenue (USD Billion).

| Cross-Flow |

| Counter-Flow |

| Evaporative |

| Dry |

| Hybrid (Wet-Dry) |

| Below 5 MW |

| 5 to 20 MW |

| Above 20 MW |

| Oil and Gas |

| Chemical and Petrochemical |

| Power Generation |

| HVACR (Commercial Buildings) |

| Data Centers |

| Pulp and Paper |

| Food and Beverage |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Flow Type | Cross-Flow | |

| Counter-Flow | ||

| By Tower Type | Evaporative | |

| Dry | ||

| Hybrid (Wet-Dry) | ||

| By Capacity Range | Below 5 MW | |

| 5 to 20 MW | ||

| Above 20 MW | ||

| By Application | Oil and Gas | |

| Chemical and Petrochemical | ||

| Power Generation | ||

| HVACR (Commercial Buildings) | ||

| Data Centers | ||

| Pulp and Paper | ||

| Food and Beverage | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Qatar | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the global cooling tower market?

The cooling tower market size reached USD 4.59 billion in 2026 and is projected to hit USD 5.89 billion by 2031.

Which application segment is expanding the fastest?

Data centers are the fastest-growing application segment at a 9.05% CAGR through 2031, driven by hyperscale facility expansion.

Why are hybrid wet-dry cooling towers gaining popularity?

Hybrid towers allow operators to switch between wet and dry modes, cutting annual water use by up to 50% while meeting stringent plume-abatement rules, making them attractive in water-scarce regions.

How will the PFAS phase-out impact the market?

The EPA’s PFAS restrictions effective 2025 limit traditional fill materials, accelerating retrofit demand and creating opportunities for suppliers of alternative media.

Which region holds the largest share of the cooling tower market?

Asia-Pacific leads the market with 43.70% revenue share in 2025 and is also the fastest-growing region, posting a 6.78% CAGR through 2031.

What technological features are most sought after in new cooling tower procurements?

Buyers increasingly require CTI-certified performance, IoT-enabled predictive maintenance, variable-frequency fan drives, and the ability to integrate with building-automation systems for optimized energy and water management.

Page last updated on: