Technology, Media and Telecom

5th MayPricing Strategy for Semiconductor Components

3 Min Read

Smart Thermostat Market Report is Segmented by Connectivity Type (Wired and Wireless), Installation Type (New Construction and Retrofit), Product Type (Connected/Programmable, Connected/Programmable, and More), End-User (Residential, Commercial, and More), Connectivity Protocol (Wi-Fi, Zigbee, Z-Wave, and More), Product Intelligence Level (Learning Smart Thermostats, Connected/Programmable, and More), and Geography.

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

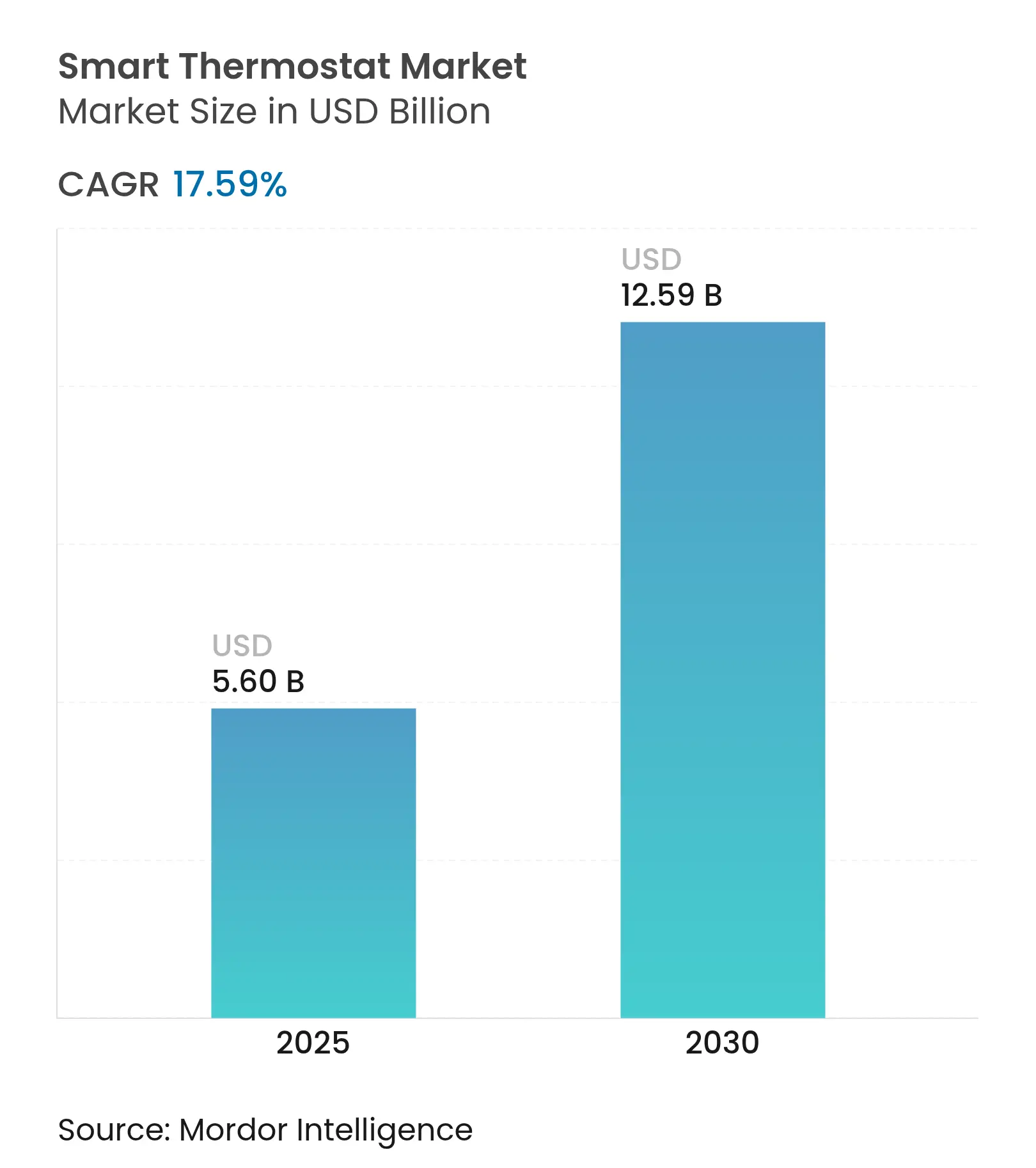

| Market Size (2025) | USD 5.60 Billion |

| Market Size (2030) | USD 12.59 Billion |

| Growth Rate (2025 - 2030) | 17.59 % CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

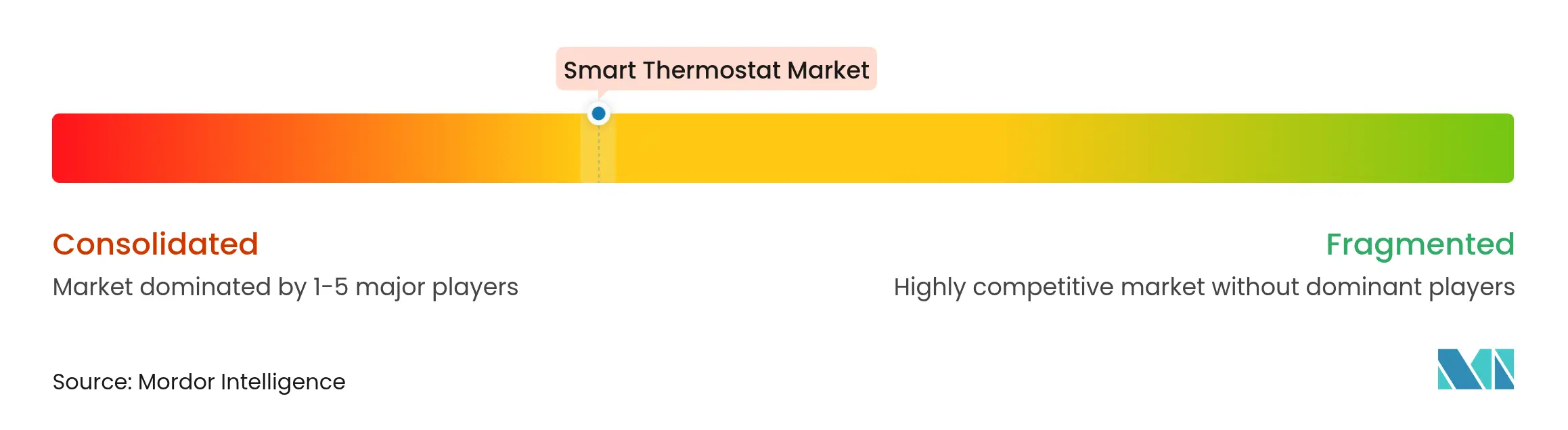

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Growth is primarily driven by a tightening policy focus on energy efficiency, steady grid modernization investments, and the adoption of the Matter interoperability standard, which removes ecosystem lock-in. Utilities are treating connected thermostats as grid assets, enrolling them in virtual power plants to shave peak demand and reduce reserve-margin costs.[1]Rocky Mountain Institute, “Virtual Power Plants and Flexible Load,” rmi.org.Uptake is further supported by falling sensor prices, the availability of Wi-Fi and Thread dual-band chips, and AI-based optimization that fine-tunes HVAC operation to weather forecasts and occupancy patterns. At the same time, manufacturers are absorbing higher semiconductor and copper costs by emphasizing premium software features rather than competing purely on hardware prices.

Key Report Takeaways

Drivers Impact Analysis

| Driver | ( ~ )% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Increasing demand for energy-saving devices Increasing demand for energy-saving devices | +3.2% | Global, strongest in North America and EU | Medium term (2-4 years) | ( ~ )% Impact on CAGR Forecast :+3.2% | Geographic Relevance :Global, strongest in North America and EU | Impact Timeline :Medium term (2-4 years) |

Government incentives and dynamic tariff roll-outs Government incentives and dynamic tariff roll-outs | +2.8% | North America, EU, Japan, South Korea | Short term (≤ 2 years) | |||

Rapid adoption of smart-home ecosystems and IoT hubs Rapid adoption of smart-home ecosystems and IoT hubs | +4.1% | Global, led by North America and APAC | Medium term (2-4 years) | |||

Virtual-power-plant monetization Virtual-power-plant monetization | +2.5% | North America, EU, Australia | Long term (≥ 4 years) | |||

Matter protocol lowers interoperability barriers Matter protocol lowers interoperability barriers | +3.7% | Global, early gains in North America and EU | Short term (≤ 2 years) | |||

AI-driven HVAC predictive-maintenance subscriptions AI-driven HVAC predictive-maintenance subscriptions | +1.9% | North America, EU, developed APAC | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Government Incentives Drive Accelerated Market Penetration

Generous subsidy programs and dynamic tariffs are moving the smart thermostat market beyond early adopters. Japan’s “Energy Saving 2025 Project” covers high-efficiency connected heating systems and offers bonus payments for removing legacy equipment, influencing replacement cycles in condominiums and single-family homes.[2]Ministry of Economy, Trade and Industry, “Energy Saving 2025 Project Overview,” meti.go.jpCalifornia has earmarked USD 50 million for low-income households to install intelligent HVAC controls, linking energy equity to flexible-load adoption. Similar rebate structures appear in France, Germany, and South Korea, trimming payback periods to less than three years for most households. Together, these measures lift adoption in regions with both high power prices and climate-policy targets, reinforcing volume growth among retrofit projects and spurring builder demand for pre-installed controls in new homes.

Smart-Home Ecosystem Integration Amplifies Value Proposition

Thread 1.4, released in late 2024, makes credential sharing and self-healing mesh networking standard features for home IoT. The update lets thermostats serve as border routers, routing traffic when Wi-Fi falters and improving whole-home reliability.[3]Thread Group, “Thread 1.4 Specifications,” threadgroup.orgApple, Google, and Amazon have publicly committed to Thread 1.4 support in their hub products by 2026, guaranteeing cross-platform pairing without vendor apps. Consumers experience faster onboarding and fewer drop-offs during initial setup, which translates to higher retention for subscription-based energy-services plans. For commercial facilities, open APIs simplify integration with existing building-management software and reduce installer training time. These network effects enlarge addressable demand by rewarding ecosystems that can span lighting, security, and HVAC in a single interface.

Virtual Power Plant Monetization Creates New Revenue Streams

Utilities now compensate households for the ability to curtail load in real time. Voltus and Resideo have enrolled roughly 11 million Mid-Atlantic customers in thermostat-based demand-response programs, paying participants for reducing HVAC draw during grid strain. Compared with constructing a 100 MW peaker plant, an aggregated thermostat fleet achieves similar reserve capacity at lower capital cost. Device vendors respond by integrating OpenADR and IEEE 2030.5 standards alongside high-speed two-way messaging that executes dispatch commands in seconds. These capabilities add service revenue for manufacturers and persistent savings for consumers, aligning utility, vendor, and homeowner interests and reinforcing long-term unit sales.

Matter Protocol Standardization Eliminates Interoperability Friction

Since its 2024 commercial launch, Matter has certified more than 670 Thread-enabled products, with thermostats representing a large share. The royalty-free framework means start-ups can enter the smart thermostat market without paying proprietary-stack fees, increasing competitive intensity and pushing down average selling prices. UL Solutions expanded its test program to Matter 1.3 in 2024, adding energy-reporting functions that let thermostats broadcast real-time consumption values. Commercial building managers, once wary of vendor lock-in, now specify Matter compliance in bid documents, ensuring multi-vendor procurement flexibility. This shift accelerates innovation cycles and broadens geographic reach as localized suppliers adopt the specification.

Restraints Impact Analysis

| Restraint | ( ~ )% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

High upfront product and installation cost High upfront product and installation cost | -2.1% | Global, particularly emerging markets | Short term (≤ 2 years) | ( ~ )% Impact on CAGR Forecast :-2.1% | Geographic Relevance :Global, particularly emerging markets | Impact Timeline :Short term (≤ 2 years) |

Data-privacy and cybersecurity concerns Data-privacy and cybersecurity concerns | -1.8% | EU, North America, developed APAC | Medium term (2-4 years) | |||

Legacy HVAC wiring fragmentation Legacy HVAC wiring fragmentation | -1.5% | North America, EU older buildings | Medium term (2-4 years) | |||

Early-adopter saturation in mature markets Early-adopter saturation in mature markets | -1.2% | North America, Western EU | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Supply Chain Cost Inflation Pressures Affordability

Semiconductor shortages and copper-price swings raised bill-of-materials costs for connected thermostats by 15–20% between 2024 and 2025. U.S. tariffs on Chinese-made smart-home devices compound the increase, leaving brands with a choice of thinner margins or higher shelf prices. Some producers are shifting final assembly to Taiwan, Vietnam, and Mexico to navigate trade barriers and diversify supply risk. Installers report that total retrofit costs, including labor, frequently exceed USD 400, outpacing willingness-to-pay in emerging economies. As a result, several vendors now bundle financing or utility rebate documentation inside their sales portals to soften the initial outlay.

Cybersecurity Vulnerabilities Undermine Consumer Confidence

Academic penetration tests published in 2024 demonstrated that many consumer-grade IoT devices still ship with default passwords and outdated TLS libraries, exposing them to credential-stuffing and denial-of-service exploits.[4]arXiv, “Security Analysis of Consumer IoT Devices,” arxiv.orgThe European Union’s Cyber Resilience Act and U.S. label programs require transparent security-support lifecycles, adding certification costs and lengthening product-development timelines. Enterprises are even stricter; hospitals and data centers demand hardware-root-of-trust chips and on-premise control servers before granting network access. Vendors able to document regular firmware-patch cadence gain a procurement edge, whereas devices perceived as risky face slowed adoption despite favorable energy-savings economics.

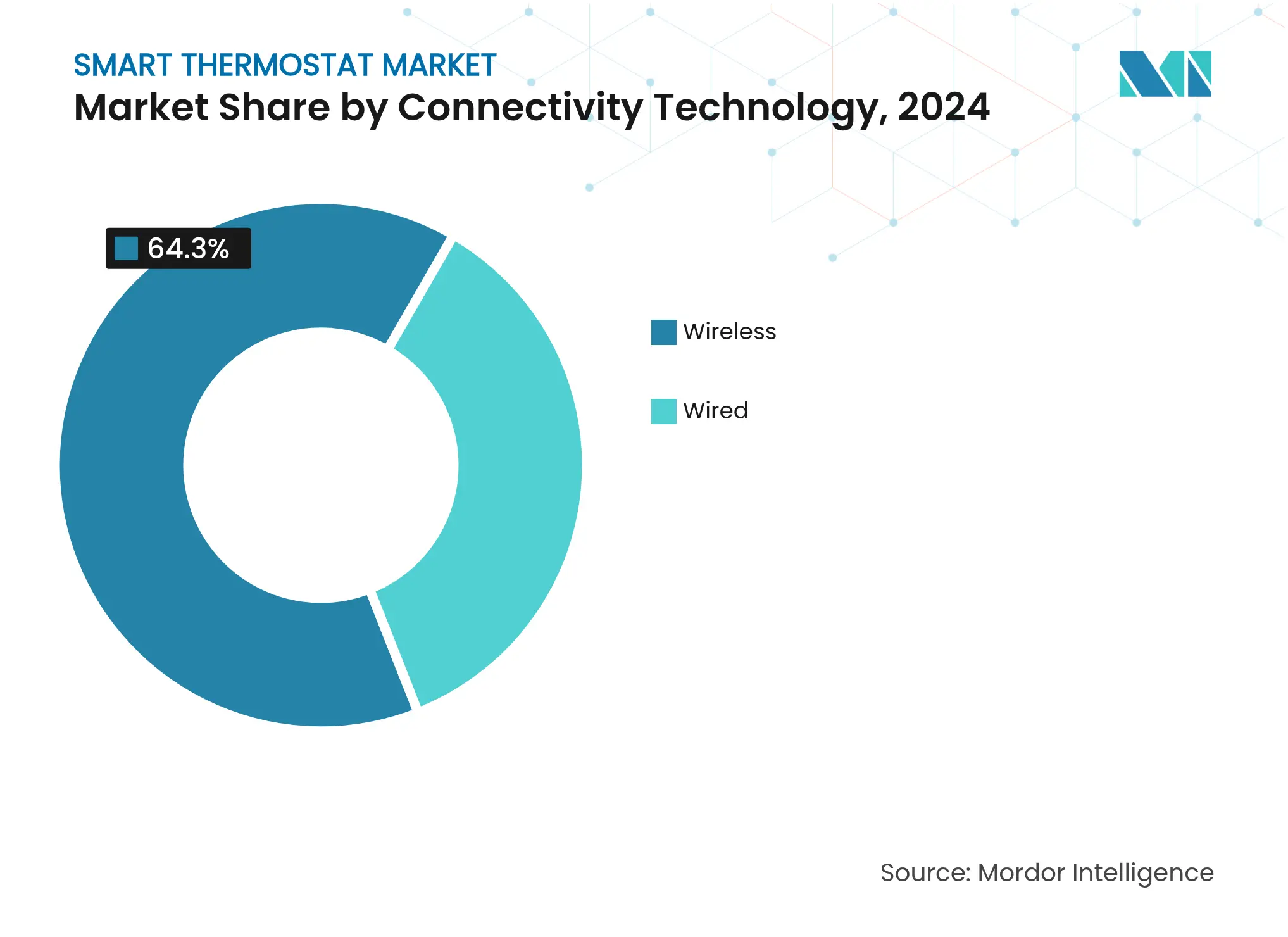

By Connectivity Technology: Wi-Fi Dominance Faces Thread Disruption

Wi-Fi-enabled units accounted for 64.30% of shipments in 2024, reflecting near-universal router penetration and straightforward installation workflows. This stronghold gives Wi-Fi the single-largest smart thermostat market share in the base year. The segment continues to benefit from higher residential replacement activity, but growth moderates as mesh-capable Thread chips enter mass production. Thread devices are expected to post 21.05% CAGR through 2030, steadily eroding Wi-Fi’s lead by offering lower power draw, seamless onboarding, and automatic network healing. Meanwhile, Zigbee remains popular in commercial retrofits because it integrates cleanly with legacy BMS software. Z-Wave keeps a niche among security-system installers that prioritize sub-GHz interference-free links. The rising ability of Matter controllers to bridge Wi-Fi and Thread traffic suggests future homes will carry mixed-stack deployments that optimize cost, range, and battery life without locking owners into one vendor.

Second-generation Thread silicon already embeds dual-stack capability, allowing fallback to 2.4 GHz Wi-Fi if border routers fail. Apple’s commitment to release Thread 1.4 firmware to its set-top boxes by 2026 will enlarge the potential addressable base by tens of millions of hubs. For commercial properties, Thread’s deterministic latency and multi-path routing improve reliability for occupant-comfort applications, which are sensitive to dropouts. Vendors anticipating this shift are loading mobile apps with network-quality dashboards that highlight Thread link status, easing installer troubleshooting and reinforcing confidence among corporate facility managers.

Note: Segment shares of all individual segments available upon report purchase

By Installation Type: Retrofit Market Drives Current Growth

Retrofit projects represented 57.80% of 2024 unit demand, capitalizing on the vast installed base of standard programmable thermostats ready for replacement. This activity positions retrofit as the largest slice of the smart thermostat market size across the forecast window. The category prospers as device makers introduce universal mounting plates and C-wire adapters that let homeowners self-install in under 30 minutes. In parallel, building-code revisions and green-bond incentives accelerate new-construction demand, driving a 20.21% CAGR for pre-installed systems in homes built after 2025. Larger multifamily developers often specify open-protocol thermostats so that property-management software can aggregate energy data portfolio-wide, enhancing ESG reporting credibility.

Commercial retrofits now draw attention because a single office tower can swap 1,000 conventional wall stats in a weekend, generating immediate energy reductions and fast payback. Regional utilities sweeten the proposition with performance-based rebates that refund up to 30% of project cost once load-shifting metrics are validated. In new buildings, integrated design approaches place thermostats on a shared IP backbone with lighting and access control, simplifying commissioning. Market participants therefore segment their product lines: value-priced do-it-yourself units target homeowners, while professional-grade, BACnet-compatible models satisfy contractors bidding large projects.

By Product Intelligence Level: Learning Algorithms Define Premium Segment

Learning thermostats claimed 45.00% of total shipments in 2024, anchoring the premium tier through adaptive scheduling and occupancy-sensing. This cluster forms the most lucrative slice of the smart thermostat market, delivering subscription revenue via monthly energy reports and predictive-maintenance alerts. Stand-alone app-controlled devices post the fastest unit growth at 19.23% CAGR, appealing to buyers mainly interested in remote access but wary of higher price tags. Mid-range connected models support rule-based automation, while multi-sensor variants target offices that need granular zone control.

Large-language-model inference at the edge now trims HVAC runtime by 33.3% compared with simple on–off cycles. Vendors integrate cloud connectors that download weather data and utility tariff schedules, optimizing set points hourly. As silicon prices fall, advanced analytics will migrate to entry models, further blurring segment boundaries. The shift challenges brands to refresh feature matrices without cannibalizing premium offerings, resulting in shorter product cycles and modular accessory ecosystems that layer capabilities over time.

Recognized by Experts. Trusted by Leaders.

A trusted intelligence partner to global decision-makers across 90+ countries.

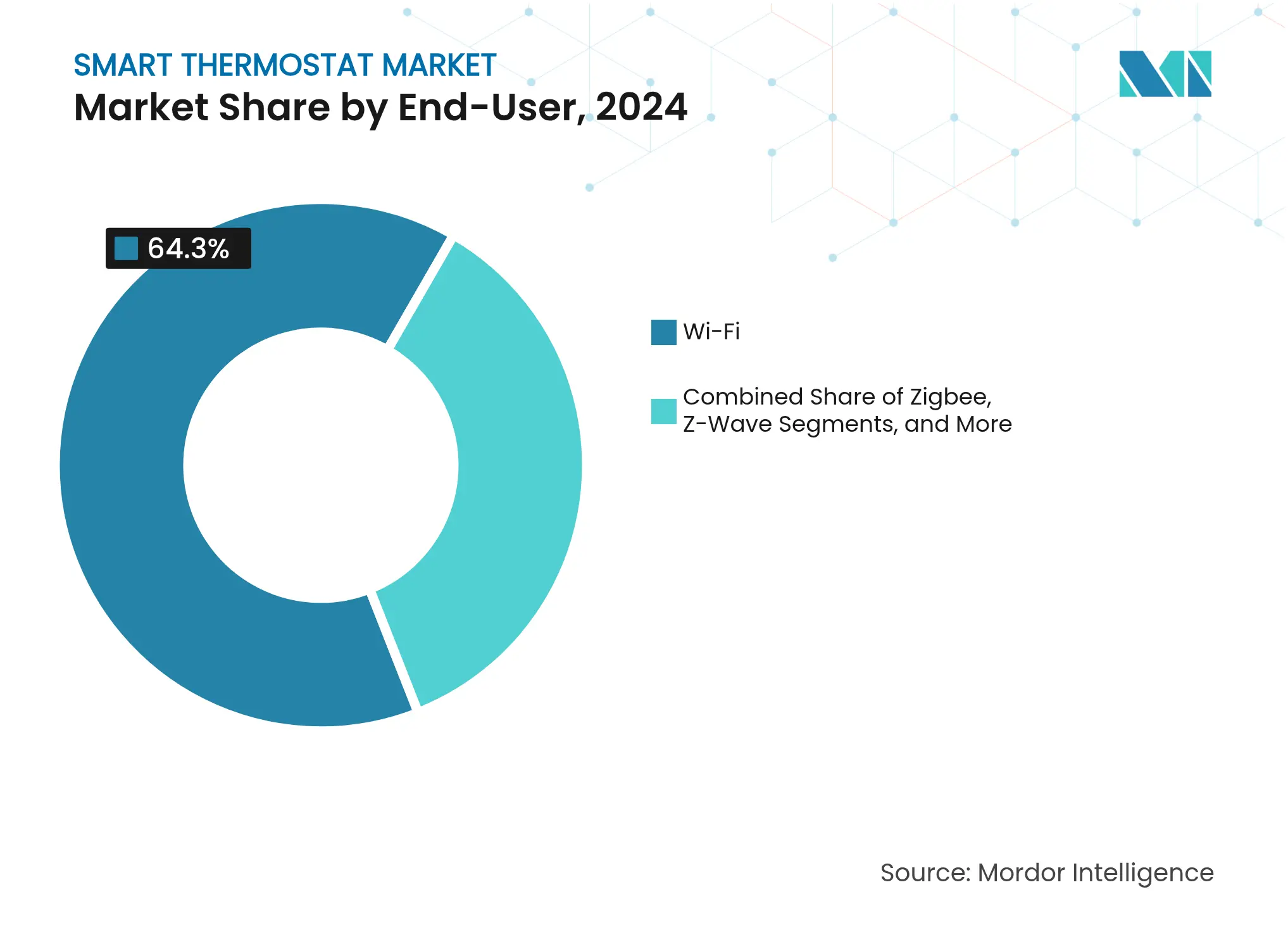

By End-User: Commercial Segment Accelerates Despite Residential Dominance

Residential buyers accounted for 71.20% of the 2024 volume, giving households the lead in the smart thermostat market. The pandemic-era home-improvement boom boosted do-it-yourself installations, and ongoing electrification of space heating keeps momentum strong. Commercial customers, however, will grow faster at 18.90% CAGR as corporate carbon neutrality pledges intensify. Offices, retail chains, and hotels favor devices that integrate occupancy analytics to balance comfort and savings. Hospitals and schools also adopt connected thermostats to meet fresh-air mandates without over-ventilating.

Virtual power plant participation is especially attractive to property owners managing thousands of square meters. Annual incentive checks offset capital expenditure, shrinking payback to under two years in many U.S. states. Facility managers, meanwhile, integrate thermostats with lighting and plug-load controls, creating unified dashboards. Vendors targeting enterprises, therefore, emphasize open APIs, role-based access, and cybersecurity certifications that align with stringent IT policies.

By Connectivity Protocol: Protocol Convergence Reshapes Competitive Dynamics

Wi-Fi continues to dominate at 64.30% share of 2024 shipments, mirroring consumer router penetration. Thread, however, shows the swiftest expansion with a 22.43% CAGR forecast to 2030. Matter certification—now viewed as table stakes—bridges the two protocols, enabling cross-vendor pairing without setup codes. Zigbee remains the workhorse in retrofit commercial controls, while Z-Wave enjoys a foothold among professional security installers. Proprietary 915 MHz links find favor in very large industrial campuses, where range trumps throughput.

Ethernet and Power-over-Ethernet models appear in data centers seeking deterministic communication and centralized power provisioning. Yet as PoE switch costs decline, such hard-wired options could gain share in mid-size offices, especially where IT teams prefer to avoid Wi-Fi congestion. Overall, the tug of war between range, bandwidth, and battery life will keep the protocol landscape plural for the next five years, but Matter’s abstraction layer hides complexity from end users, sustaining mainstream adoption.

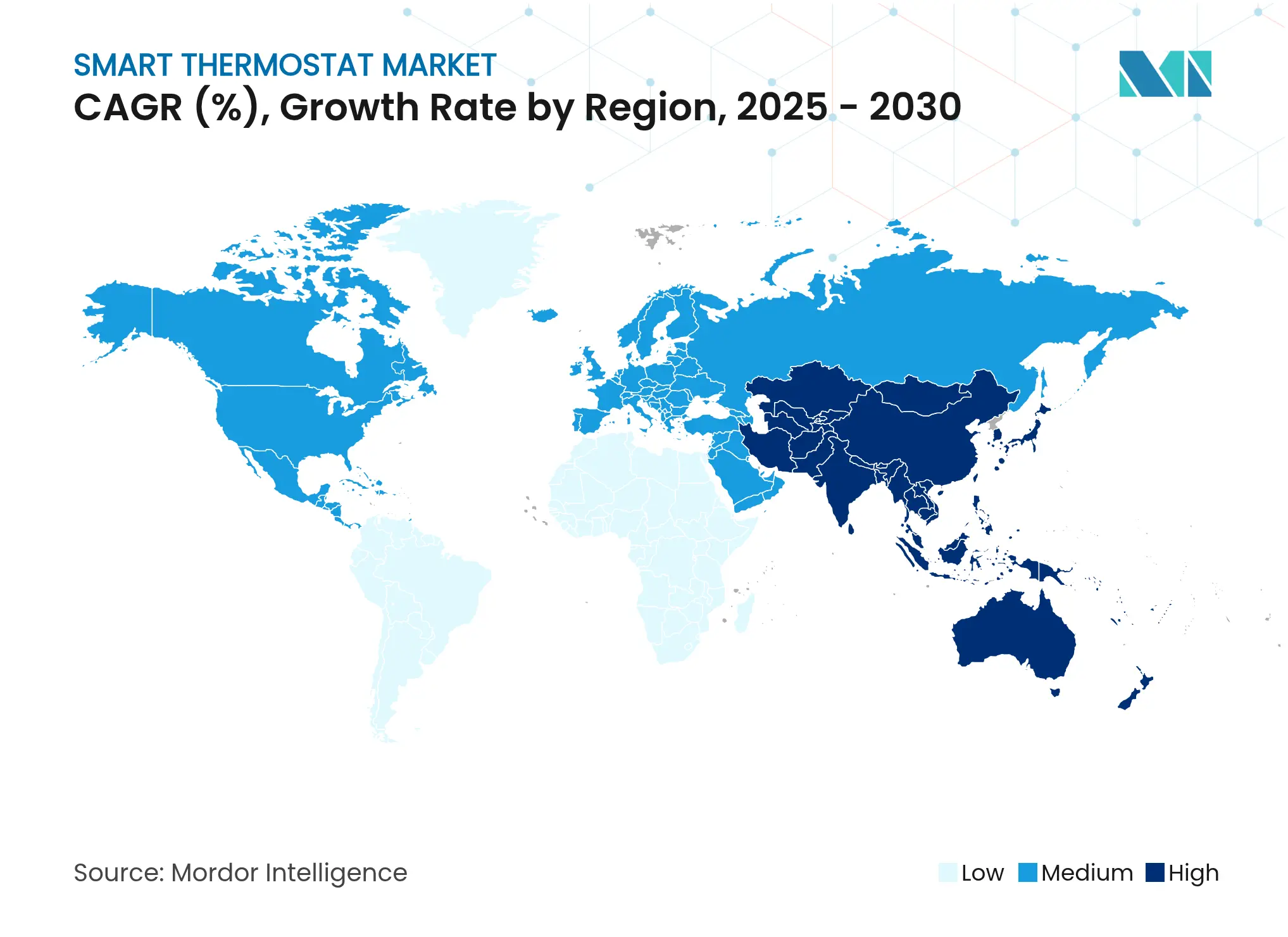

North America posted the highest 2024 revenue with 38.60% share, aided by Energy Star labeling, state-level demand-response incentives, and high per-capita HVAC penetration. Europe followed, driven by the Fit-for-55 package that compels deep building-energy retrofits by 2030. The Asia Pacific region, however, will record the fastest gains at 17.66% CAGR. China shipped 185 million air-conditioner units in 2024, providing a vast install base that primes upgrades to connected controllers. Japan’s carbon-neutrality roadmap requires efficiency upgrades in existing housing stock, and South Korea’s smart-home tax credits lower the cost of integrated HVAC controls.

In rapidly urbanizing Southeast Asia, middle-class households view smart thermostats as both status symbols and energy-saving tools during seasonal heatwaves. Government subsidy pools in Thailand and Malaysia now include connected HVAC as eligible equipment, expanding addressable demand. Elsewhere, Latin America posts moderate growth, with Brazil leveraging net-metering reforms and Mexico adopting smart-energy codes for new commercial builds. Middle East buyers focus on controlling the high cooling loads in glass-clad towers, yet cost remains a hurdle in lower-income segments. Regional disparities mean manufacturers must tailor channel strategies, offering budget SKUs in emerging economies while upselling cloud services in mature markets.

Market Concentration

Competition is moderate and intensifying. No vendor holds more than 15% of annual volume, preserving a diversified supply base. Legacy HVAC majors leverage service networks, pairing connected thermostats with heat pumps and variable-speed compressors to deliver bundled offerings. Technology firms concentrate on AI software, voice-assistant integration, and slick user interfaces, positioning themselves as platform orchestrators rather than hardware suppliers.

Matter standardization reduces connectivity as a differentiation lever, shifting rivalry toward analytics accuracy and customer-support experience. Carrier Global and Google Cloud unveiled an AI-based home-energy-management platform in 2025 that will couple heat pumps, storage batteries, and thermostats into a single optimization loop. Generac entered the category by launching the ecobee Smart Thermostat Essential at USD 129.99, aiming for mass-market adoption while cross-selling standby generators Resideo continues to cultivate professional-installer channels, announcing Honeywell Home FocusPRO models tailored to contractor preferences.

Aggressive newcomers exploit lower entry barriers created by open protocols, targeting value segments in India and Eastern Europe. Several Chinese ODMs now offer white-label Thread thermostats to retailers under store brands, increasing private-label penetration. Patent filings cluster around occupancy detection, adaptive reinforcement-learning control, and in-device edge AI. As software subscription revenue rises, vendors extend update lifespans and support windows, enhancing brand stickiness and creating annuity streams that outlast initial hardware margins.

*Disclaimer: Major Players sorted in no particular order

1. INTRODUCTION

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

5. MARKET SIZE AND GROWTH FORECASTS (VALUE)

6. COMPETITIVE LANDSCAPE

7. MARKET OPPORTUNITIES AND FUTURE OUTLOOK

Smart thermostats, used in homes and businesses alike, allow users to manage settings remotely through handheld devices. These thermostats come in wired and wireless formats, offering the same features but differing in their installation processes. Labeled as "smart," these devices can communicate with IoT systems in modern buildings, leverage AI for adaptive learning, employ active geo-fencing, reduce energy usage, and interface with next-gen virtual private assistants.

This research delves into the global sales revenue of smart thermostats, keeping an eye on key market indicators and growth catalysts. It highlights leading manufacturers in the industry, aiding in market evaluations and growth projections. Additionally, the study considers macroeconomic elements influencing the market dynamics. The report provides market sizing and forecasts across various segments.

The study on the smart thermostat market covers segmentation by type (wired, wireless), installation type (new, retrofit), component (occupation sensor, voice control, energy tracking, others), end-user vertical (residential, commercial), and geography (North America, Europe, Asia Pacific, Rest of the World). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

Pricing Strategy for Semiconductor Components

3 Min Read

Accelerating Additive Manufacturing Adoption in India

3 Min Read

US Market Entry for Taiwanese Machine Tool Manufacturers

5 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.