Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 17.25 Billion |

| Market Size (2026) | USD 17.48 Billion |

| Market Size (2031) | USD 19.04 Billion |

| Growth Rate (2026 - 2031) | 1.72% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Brazil Plastic Packaging Market Analysis by Mordor Intelligence

The Brazil plastic packaging market size is expected to increase from USD 17.25 billion in 2025 to USD 17.48 billion in 2026 and reach USD 19.04 billion by 2031, growing at a CAGR of 1.72% over 2026-2031. Rising recovery rates and recycled-content mandates, a feedstock-cost edge from sugarcane ethanol, and e-commerce-driven demand for cube-efficient formats are nudging the market away from pure volume toward higher-value solutions. Presidential Decree 12,688 obliges converters to reach 22% post-consumer recycled content by 2026, accelerating investments in near-infrared sorting and decontamination lines. São Paulo and Rio de Janeiro beverage-bottle deposit schemes are improving polyethylene terephthalate bale purity, while municipal bans on expanded polystyrene trays are steering quick-service outlets toward molded-fiber and polypropylene alternatives. Bio-attributed polyethylene derived from domestic ethanol now carries a single-digit premium over fossil grades, enabling price-sensitive food and retail uses without eroding converter margins.

Key Report Takeaways

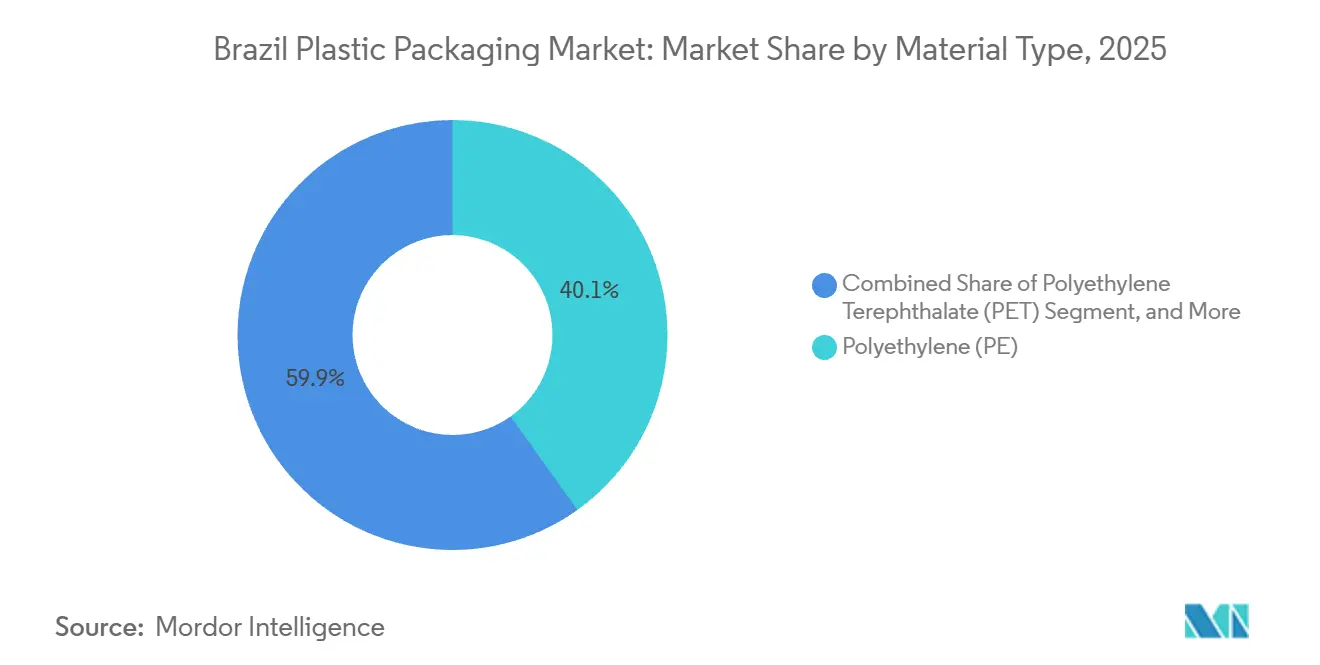

- By material type, polyethylene led with 40.13% of the Brazil plastic packaging market share in 2025, whereas polyethylene terephthalate is projected to record the fastest 2.21% CAGR through 2031.

- By packaging type, flexible formats accounted for 53.42% of the Brazil plastic packaging market size in 2025, while the rigid segment is set to trail as flexible solutions grow at a 2.46% CAGR.

- By product form, pouches and sachets captured 32.37% share in 2025, yet films and wraps are forecast to expand at a market-leading 2.63% CAGR to 2031.

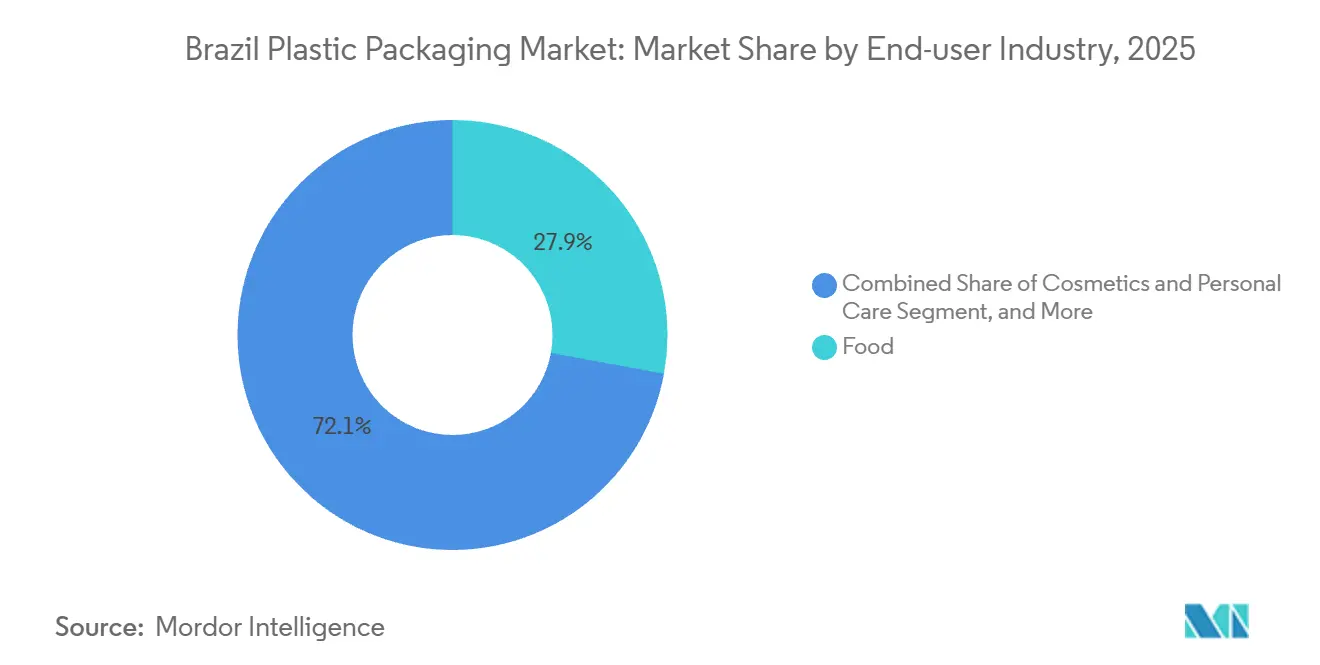

- By end-user industry, food retained the largest 27.88% share in 2025, and cosmetics and personal care is anticipated to advance at the fastest 3.01% CAGR.

- By manufacturing process, extrusion accounted for 29.54% of market share in 2025, whereas thermoforming is poised for the highest 3.12% CAGR on the back of in-mold labeling adoption.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Brazil Plastic Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sustainable-Material Mandates from ANVISA And CONAMA | +0.5% | National, early enforcement in São Paulo, Rio de Janeiro, Brasília | Medium term (2-4 years) |

| Rapid E-Commerce Cold-Chain Expansion | +0.4% | National, concentrated in Southeast and South regions | Short term (≤ 2 years) |

| Brand-Owner Pledges For ≥ 25% PCR By 2028 | +0.3% | National, led by multinational FMCG and cosmetics brands | Medium term (2-4 years) |

| Petrochemical Feedstock Advantage from Domestic Ethanol | +0.2% | National, anchored by São Paulo and Rio Grande do Sul ethanol hubs | Long term (≥ 4 years) |

| Blockchain-Enabled Traceability Pilots Elevating Premium SKUs | +0.1% | National, early adoption in cosmetics and premium food | Medium term (2-4 years) |

| Tax Incentives on Bagasse-Based Bioplastics | +0.1% | National, R and D in São Paulo and Minas Gerais | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Sustainable-Material Mandates from ANVISA and CONAMA

Presidential Decree 12,688 instituted legally binding reverse-logistics goals, compelling 32% recovery and 22% post-consumer recycled content by 2026.[1]Planalto, “Decreto nº 12.688, de 18 de Dezembro de 2024,” planalto.gov.br Companion ANVISA technical note RDC 326/2024 authorizes recycled polyethylene terephthalate and high-density polyethylene in direct food contact, provided converters validate closed-loop traceability and migration compliance under ISO 15632. Converters are therefore re-tooling with near-infrared sorting and super-clean decontamination systems that meet stringent food-grade thresholds. Brand owners risk penalties for unverifiable recycled-content claims, pushing them toward certified suppliers. Pending Bill PL 5321/2025 aims to hard-wire minimum recycled-content levels, signaling that voluntary targets will likely become statutory over the next decade.

Rapid E-Commerce Cold-Chain Expansion

Brazil’s e-grocery penetration reached 8% of food retail in 2025, doubling since 2020 as shoppers favor doorstep delivery for chilled proteins and dairy. Fulfillment centers now specify high-barrier flexible pouches that extend ambient cold life from four to twelve hours, reducing reliance on reefer vans and lowering diesel spend. Amcor’s AmFiber paper-polyethylene laminate arrived in early 2025 to serve this niche, offering curbside recyclability where mixed-fiber collection is available. Government grants worth BRL 500 million (USD 95 million) under a May 2025 biorefinery roadmap support pilot plants for bio-based barrier coatings that can displace imported ethylene-vinyl alcohol within three years. These developments reinforce demand for lighter, cube-efficient flexible packs.

Brand-Owner Pledges for ≥ 25% PCR by 2028

Grupo Boticário and Natura anchored public commitments to source at least 25% post-consumer resin by 2028, triggering a procurement pull that reshapes resin supply chains.[2]Prefeitura de São Paulo, “Lei Municipal – Proibição de EPS,” prefeitura.sp.gov.br Braskem responded by earmarking 30% of its polyethylene capacity for mechanical and bio-attributed grades by 2027. However, food-grade recycled polypropylene remains scarce because its low density hampers automatic separation, leaving converters dependent on virgin inputs. Without local licensing of NextLooPP’s advanced dissolution technology, the circularity gap for yoghurt cups and microwaveable trays persists.

Petrochemical Feedstock Advantage from Domestic Ethanol

Braskem’s 260,000 t/y bio-based polyethylene plant in Triunfo sources ethanol under fixed-price contracts that detach resin prices from Brent crude swings, narrowing the premium over fossil grades to roughly 5%. The 2025 Tax Reform delivered a 60% levy reduction for bio-attributed plastics, further tilting cost economics, while the Brazilian Sustainable Taxonomy now qualifies such resins for green-bond funding. These fiscal incentives underpin plans for brownfield debottlenecks that could lift domestic bio-polyethylene output beyond 350,000 t/y by 2028.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Municipal Waste-Collection Gaps in Tier-3 Cities | −0.3% | National, acute in North and Northeast regions | Medium term (2-4 years) |

| Consumer Backlash Against Single-Use EPS Trays | −0.2% | National, focused in São Paulo, Rio de Janeiro, Santos | Short term (≤ 2 years) |

| Shortage of Food-Grade rPP Supply | −0.1% | National, dairy and ready-meal converters | Medium term (2-4 years) |

| Currency Volatility Hampering Resin Price Pass-Through | −0.1% | National, import-dependent converters | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Municipal Waste-Collection Gaps in Tier-3 Cities

Only 25.7% of Brazilian municipalities operated segregated collection in 2024, leaving mixed-waste landfills that contaminate recyclables with organic leachate. Quality-certified feedstock is thus concentrated in São Paulo and Rio de Janeiro, while converters in Manaus and Belém import recycled polyethylene terephthalate at double-digit freight premiums. A USD 120 million Inter-American Development Bank loan approved in 2024 will finance fifteen regional sorting hubs, but commissioning extends to 2027, delaying compliance with 2026 reverse-logistics targets. The geographic imbalance suppresses circular-economy momentum outside the industrial heartland.

Consumer Backlash Against Single-Use EPS Trays

Municipal bans on expanded polystyrene food-service packaging took effect in São Paulo, Rio de Janeiro, and Santos during 2024, citing marine-litter concerns.[3]Natura, “Biome Line Launch,” natura.com.br Quick-service chains pivoted to molded-fiber clamshells and polypropylene trays, stranding roughly BRL 80 million (USD 15 million) in legacy tooling and prompting layoffs at three regional converters. Surveys conducted in February 2025 show 68% of metropolitan consumers associate expanded polystyrene with environmental harm, even when fiber alternatives carry a larger carbon footprint. The perception gap accelerates polystyrene’s structural decline and raises packaging costs for value-meals.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Deposit Schemes Propel PET Uptake

Polyethylene terephthalate secured a 2.21% forecast CAGR to 2031 as São Paulo and Rio de Janeiro deposit laws guarantee clean bale supply that meets ANVISA’s food-contact purity thresholds. Polyethylene retained 40.13% share in 2025, buoyed by flexible films and a feedstock advantage from sugarcane ethanol that limits cost volatility. The Brazil plastic packaging market size for polyethylene formats will remain dominant, yet polyethylene terephthalate growth outpaces as brand owners seek bottle-to-bottle loops. Polypropylene’s recycling lag stems from density-driven cross-contamination, keeping recycled content below 20% and constraining circular ambitions. Polystyrene continues to lose ground after municipal bans eliminated single-use trays, redirecting demand to polypropylene and molded fiber. Other resins such as polyamide fill niche high-barrier roles where regulatory thresholds limit substitution.

Indorama Ventures’ 15,000 t/y expansion in Indaiatuba now channels post-consumer polyethylene terephthalate into premium bottle-grade pellets that command 20% price premiums over fiber markets. Meanwhile, the NextLooPP dissolution pathway for food-grade recycled polypropylene lacks Brazilian licensing, perpetuating shortfalls for yogurt cups and ready-meal trays. Combined with Decree 12,688’s 22% recycled-content mandate, these dynamics pull resin sourcing toward certified mechanical and chemical streams and reinforce investment in bale-quality infrastructure.

By Packaging Type: Flexible Formats Trim Last-Mile Costs

Flexible plastic packaging captured 53.42% share in 2025, and will grow at a 2.46% CAGR through 2031 as grocery e-commerce platforms prioritize cube-efficient pouches that reduce diesel consumption in last-mile deliveries. High-barrier films with ethylene-vinyl alcohol cores extend shelf life for chilled proteins and dairy, enabling ambient delivery across peri-urban corridors. The Brazil plastic packaging market share for rigid formats remains solid in carbonated drinks and household chemicals, where drop impact and internal pressure require bottles and jars. Amcor’s curbside-recyclable AmFiber laminate aims to unlock fiber-film diversion but faces collection-system limitations outside the top metropolitan areas. Government-funded biorefinery pilots converting bagasse into barrier coatings could lower flexible-film input costs within three years, reducing the price gap with rigid options and further lifting flexible uptake.

Klabin’s BRL 200 million (USD 38 million) investment to laminate kraft paper with bio-polyethylene positions the firm to integrate pulp, polymer, and conversion under one roof. Vertical integration promises margin capture along the value chain while offering brand owners drop-in alternatives to metallized structures. Rigid converters must therefore pivot toward lightweighting and refillable innovations to defend share against flexible encroachment.

By Product Form: Films And Wraps Outpace On Cold-Chain Efficiency

Films and wraps are on track for a 2.63% CAGR through 2031, benefiting from multilayer constructions that keep chilled proteins within microbiological limits without active refrigeration. The Brazil plastic packaging market size for pouches and sachets stood at 32.37% in 2025, supported by single-serve coffee, condiments, and personal-care SKUs whose portion control matches fast-paced urban lifestyles. Bottles and jars dominate beverage service under deposit-return schemes, while trays see material substitution away from expanded polystyrene toward polypropylene and molded fiber. Agricultural bulk bags compete against low-cost woven polypropylene imports from Asia, challenging domestic converters to add value through UV stabilization and traceability features.

A sugarcane-bagasse cryogel developed in April 2025 offers expanded-polystyrene-level drop protection at 30% lower basis weight, enabling electronics exporters to reduce freight spend by double digits. ANVISA’s January 2026 consultation on refillable cosmetics packs signals regulatory openness to multiple-use containers, which could reshape form-factor demand and push converters to adopt modular closure systems.

By End-User Industry: Refillable Push Elevates Cosmetics

Food accounted for 27.88% of demand in 2025, underpinned by chilled-protein growth and e-grocery penetration. Yet cosmetics and personal care are set to post a 3.01% CAGR as refillable mandates and premium bio-polymer launches spur innovation. The Brazil plastic packaging market for beverages benefits from a deposit-return system for food-grade polyethylene terephthalate with purity exceeding 95%, facilitating closed-loop bottle recycling. Pharmaceutical and healthcare packs must meet ANVISA serialization under RDC 157/2017, sustaining demand for tamper-evident blisters.

Industrial bulk remains a stronghold of woven polypropylene thanks to its stacking strength and UV resistance. Consumer surveys expose a gap between refillable awareness (75%) and purchase behavior (22%), suggesting regulatory nudges will drive scale adoption. IFF’s research lab opened in August 2025 to explore bio-based fragrance encapsulation, which may reduce the need for virgin polymers in fine-fragrance packages.

By Manufacturing Process: In-Mold Labeling Spurs Thermoforming

Thermoforming eyes a 3.12% CAGR as dairy brands adopt in-mold labels that merge decoration and wall structure in one step, eliminating adhesives and boosting recycling yields. Extrusion dominated 29.54% of 2025 production across blown-film grocery bags, mulch, and stretch wrap. Injection molding retains leadership in closures, where high thread precision is critical, while blow molding delivers lightweight polyethylene terephthalate bottles, whose average unit weight fell by 12.5% between 2020 and 2025. Rotational and compression molding serve niche industrial containers.

Huhtamaki’s 2024 expansion added two high-speed thermoforming lines capable of producing 120 million yogurt cups per year. The expansion aims to achieve premium shelf appeal through full-coverage label fusion. The Recircula Brasil blockchain platform now audits recycled-content declarations across multiple processes, elevating transparency and discouraging greenwashing.

Geography Analysis

São Paulo, Rio de Janeiro, and Minas Gerais together host about 65% of converter capacity and 70% of certified post-consumer resin supply, reflecting mature selective-collection systems and proximity to branded fast-moving consumer goods hubs. The South region, anchored by Paraná, Santa Catarina, and Rio Grande do Sul, benefits from sugarcane and forestry biomass corridors that feed bio-attributed polyethylene and kraft-paper laminates, reducing feedstock freight. Northeast and North states lag with selective collection in just 12% of municipalities, forcing converters to ship recycled feedstock from the Southeast at premiums that erode competitiveness. Central-West zones like Goiás and Mato Grosso are emerging as agricultural-film extrusion centers, leveraging soybean and corn processors’ need for high-barrier export pouches.

Reverse-logistics targets set by Decree 12,688 will chiefly be met in wealthier regions, widening compliance gaps. IDB-funded hubs scheduled to open by 2027 aim to narrow the deficit but arrive after the 2026 benchmark, risking penalty exposure for converters dependent on under-served cities. Municipal polystyrene bans in coastal metropoles pressurized converters without thermoforming diversification, spurring capacity redeployment toward polypropylene or molded-fiber lines in the Southeast.

The Brazilian Sustainable Taxonomy designates bio-based polyethylene a transition asset eligible for green-bond issuance, catalyzing brownfield retrofits in São Paulo and Rio Grande do Sul. E-commerce penetration hits double digits in the Southeast and South, generating demand for ambient-cold pouches, whereas tier-3 northern municipalities continue to rely on heavier rigid containers due to infrastructure inertia. Over the forecast horizon, infrastructural homogeneity rather than product-design innovation may prove the chief regional differentiator in the Brazil plastic packaging market.

Competitive Landscape

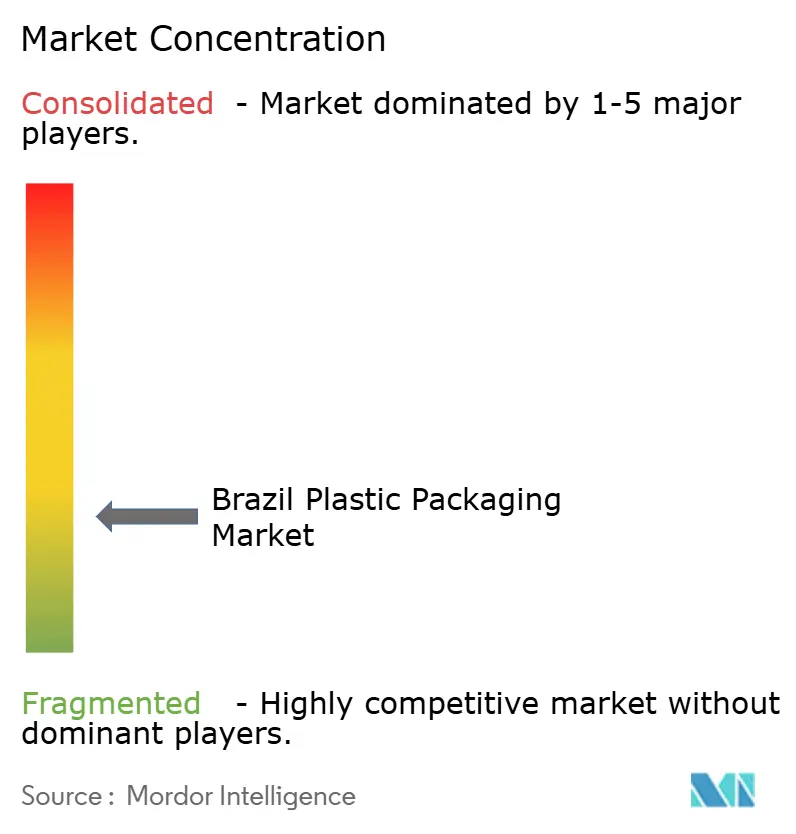

The Brazilian plastic packaging market is fragmented. Multinationals Amcor, Mondi, and Sealed Air compete alongside domestic specialists such as Klabin, Braskem, and Termotécnica. Strategic focus has migrated toward post-consumer resin certification, blockchain traceability, and low-carbon feedstocks rather than pure capacity additions. The proposed Amcor-Berry Global merger awaits antitrust clearance, which may require divestitures of film plants to safeguard competition. White-space remains around food-grade recycled polypropylene, where shortages force converters to blend virgin resin above 80%, and around refillable cosmetics packaging, pending ANVISA guidelines.

Mango Materials supplies methane-derived polyhydroxyalkanoate to Natura’s Biome line, showcasing vertical integration that bypasses fossil chains. Recircula Brasil's electronic-invoice seals enable real-time verification of recycled-content claims, pressuring tier-2 converters lacking capital for certification upgrades to consolidate or exit price-squeezed commodity segments. AptarGroup’s October 2025 purchase of Sommaplast secures closure know-how and locks in dispensing-system capacity for multinational beauty brands. Technology bifurcation is evident: tier-1 players deploy near-infrared sorters, decontamination reactors, and in-mold labeling, while cash-constrained rivals compete on price, accelerating the market shakeout.

Mid-tier converters are pivoting toward niche plays in bio-attributed resins and blockchain-verified supply chains to escape commodity-film price wars. Platforms such as Recircula Brasil now reward converters that upload electronic-invoice seals with preferential access to branded fast-moving consumer goods tenders, pressuring laggards to retrofit lines for traceability compliance. At the same time, contract manufacturers that once relied on low-margin grocery-bag extrusion are shifting toward custom thermoforming services for dairy and ready-meal brands, an upgrade path made viable by equipment leasing programs backed by the Brazilian Development Bank.

Brazil Plastic Packaging Industry Leaders

Amcor plc

Mondi plc

Huhtamäki Oyj

Sealed Air Corporation

Sonoco Products Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: ANVISA opened a consultation on reusable and refillable packaging rules for cosmetics, setting hygiene and traceability standards that could accelerate circular business models.

- January 2026: The Central Bank of Brazil released the national sustainable taxonomy, granting green-bond eligibility to bio-based polyethylene and mechanically recycled resins.

- October 2025: AptarGroup finalized its acquisition of Sommaplast, enhancing its dispensing-closures portfolio for South American personal-care brands.

- August 2025: International Flavors and Fragrances inaugurated a São Paulo lab to develop bio-based fragrance encapsulation, aiming to reduce synthetic polymer usage.

Brazil Plastic Packaging Market Report Scope

Plastic packaging encompasses the utilization of plastic materials for the containment, safeguarding, and transportation of a wide range of products. This form of packaging enables the protection, preservation, storage, and transport of goods through various methods.

The Brazil Plastic Packaging Market Report is Segmented by Material Type (Polyethylene, Polypropylene, Polyethylene Terephthalate, Polystyrene and EPS, and Other Material Types), Packaging Type (Flexible Plastic Packaging, and Rigid Plastic Packaging), Product Form (Bottles and Jars, Trays and Containers, Pouches and Sachets, Bags and Sacks, Films and Wraps, and Other Product Forms), End-User Industry (Food, Beverage, Pharmaceuticals and Healthcare, Cosmetics and Personal Care, Industrial, and Other End-user Industries), Manufacturing Process (Extrusion, Injection Molding, Blow Molding, Thermoforming, and Other Manufacturing Processes). The Market Forecasts are Provided in Terms of Value (USD).

By Material Type

| Polyethylene (PE) |

| Polypropylene (PP) |

| Polyethylene Terephthalate (PET) |

| Polystyrene and EPS |

| Other Material Types |

By Packaging Type

| Flexible Plastic Packaging |

| Rigid Plastic Packaging |

By Product Form

| Bottles and Jars |

| Trays and Containers |

| Pouches and Sachets |

| Bags and Sacks |

| Films and Wraps |

| Other Product Forms |

By End-User Industry

| Food |

| Beverage |

| Pharmaceuticals and Healthcare |

| Cosmetics and Personal Care |

| Industrial |

| Other End-user Industries |

By Manufacturing Process

| Extrusion |

| Injection Molding |

| Blow Molding |

| Thermoforming |

| Other Manufacturing Processes |

| By Material Type | Polyethylene (PE) |

| Polypropylene (PP) | |

| Polyethylene Terephthalate (PET) | |

| Polystyrene and EPS | |

| Other Material Types | |

| By Packaging Type | Flexible Plastic Packaging |

| Rigid Plastic Packaging | |

| By Product Form | Bottles and Jars |

| Trays and Containers | |

| Pouches and Sachets | |

| Bags and Sacks | |

| Films and Wraps | |

| Other Product Forms | |

| By End-User Industry | Food |

| Beverage | |

| Pharmaceuticals and Healthcare | |

| Cosmetics and Personal Care | |

| Industrial | |

| Other End-user Industries | |

| By Manufacturing Process | Extrusion |

| Injection Molding | |

| Blow Molding | |

| Thermoforming | |

| Other Manufacturing Processes |

Key Questions Answered in the Report

How large is the Brazil plastic packaging market in 2026?

The market is expected to reach USD 17.48 billion in 2026.

What CAGR is forecast for Brazil’s plastic packaging through 2031?

The market is projected to grow at a 1.72% CAGR between 2026 and 2031.

Which packaging type is expanding fastest in Brazil?

Flexible formats, especially high-barrier films, are forecast to rise at a 2.46% CAGR through 2031.

Why is polyethylene terephthalate gaining share?

Deposit-return schemes in major cities secure clean bottle bales, driving a 2.21% CAGR for polyethylene terephthalate through 2031.

What regulation most influences recycled content in Brazil?

Presidential Decree 12,688 mandates 22% post-consumer recycled content in plastic packaging by 2026.

Which end-use segment is set for the quickest growth?

Cosmetics and personal care packaging is expected to expand at a 3.01% CAGR on the back of refillable-pack initiatives.

Page last updated on: