Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 11.99 Billion |

| Market Size (2026) | USD 12.87 Billion |

| Market Size (2031) | USD 16.13 Billion |

| Growth Rate (2026 - 2031) | 4.62% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Brazil Floor Covering Market Analysis by Mordor Intelligence

The Brazil floor covering market size reached USD 11.99 billion in 2025, is expected to be USD 12.87 billion in 2026, and is projected to reach USD 16.13 billion by 2031 at a 4.62% CAGR. Ceramic tiles retain a dominant base due to scale efficiencies in domestic kilns and performance in humid climates, while resilient formats, especially stone plastic composite planks, are redefining installation speed and moisture tolerance for multifamily and renovation cycles. The Brazil floor covering market is also absorbing a reset in traditional porcelain volumes since the pandemic peak as leading producers emphasized profitability over volume, even reporting quarters where tiles moved with little to no margin. Growth levers shift toward resilient flooring that meets programmatic housing schedules and toward integrated systems that simplify compliance with acoustic and indoor air quality rules, which is reshaping assortments for national retailers and regional specialists. The Brazil floor covering market is further influenced by omnichannel retail investment that links e-commerce with in-store technical support, enabling click-lock DIY expansion and faster project turnarounds in urban centers.

Key Report Takeaways

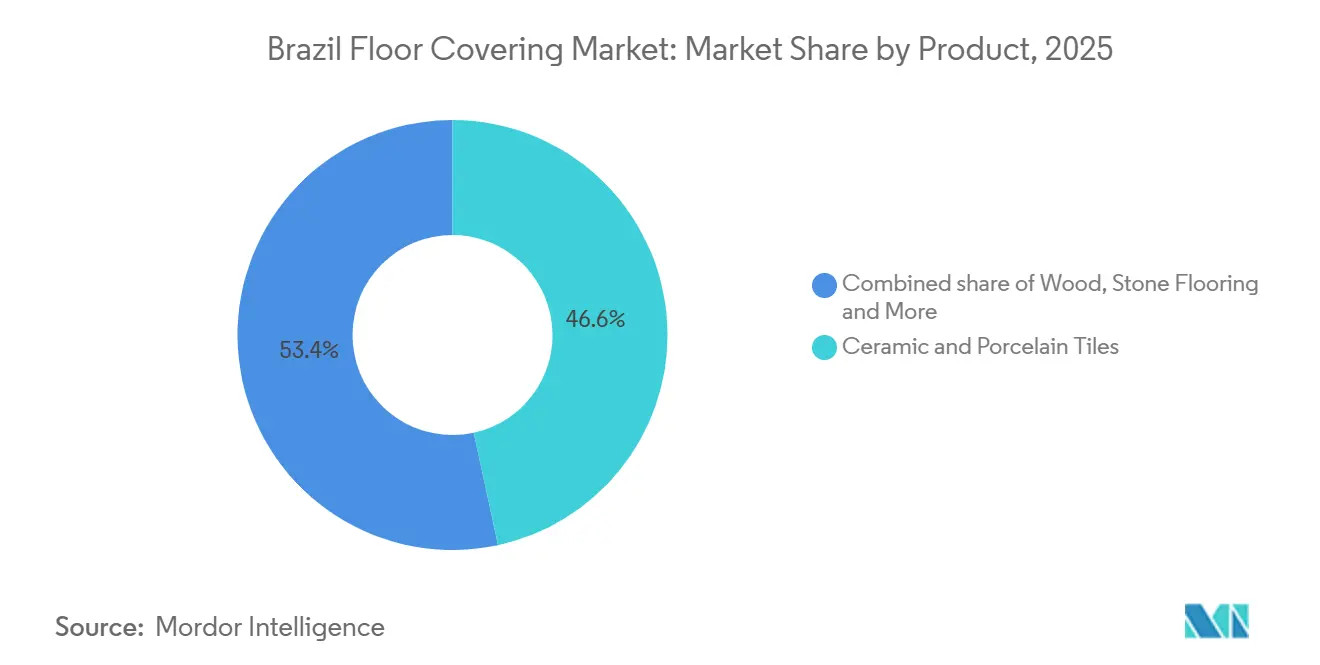

- By product type, ceramic and porcelain led with 46.61% share in 2025 in the Brazil floor covering market, while Vinyl Flooring (LVT, Sheet, VCT) is projected to expand at an 4.69% CAGR through 2031.

- By end user, residential accounted for 70.00% in 2025 in the Brazil floor covering market, while commercial is projected to record a 5.12% CAGR through 2031.

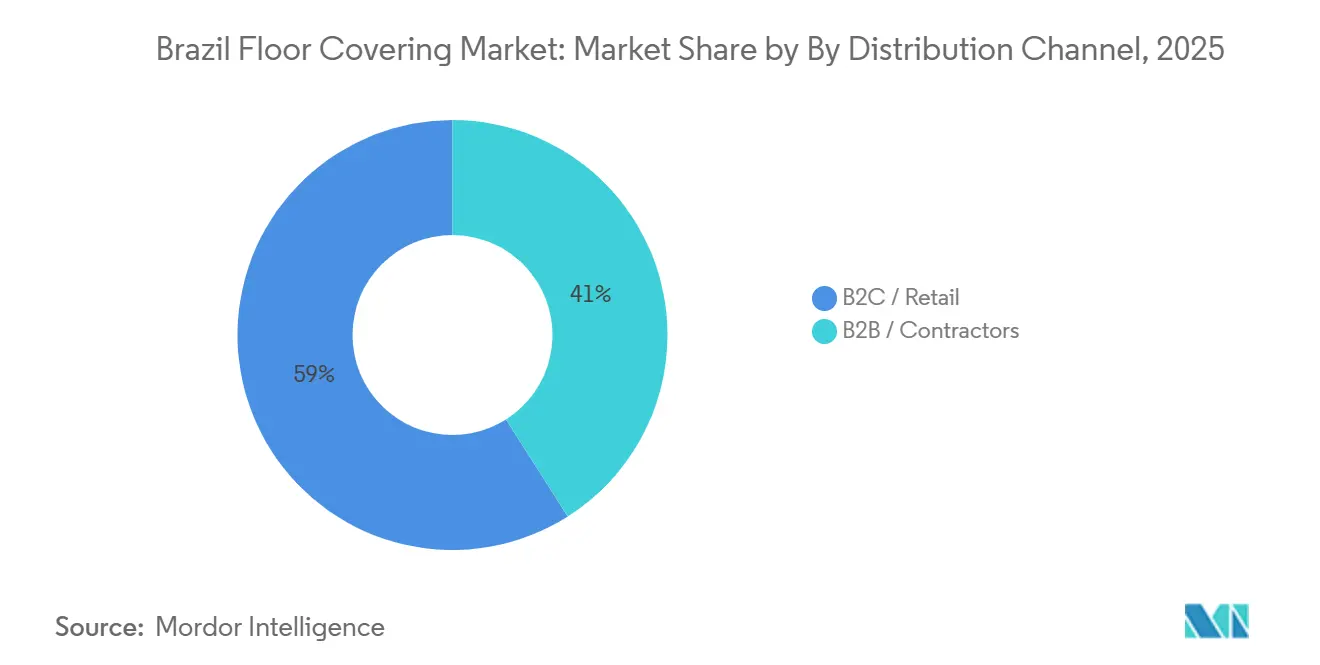

- By distribution channel, the B2C/retail segment held a 59.0% share in 2025 and is projected to expand at a 7.20% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Brazil Floor Covering Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Housing programs upcycle and robust residential launches/sales | +1.2% | National, with early gains in Southeast São Paulo and Rio, and Northeast coastal cities, Recife and Fortaleza | Medium term (2-4 years) |

| The domestic scale and climate fit support ceramic tiles' dominance | +0.8% | National core, strongest in Southeast production clusters, Santa Gertrudes and SC, and Northeast humid zones | Long term (≥ 4 years) |

| LVT/SPC adoption in renovations and moisture-prone areas | +1.5% | Southeast metro areas, Northeast coastal belt, South municipal clinic refits | Short term (≤ 2 years) |

| Omnichannel B2C expansion by home centers and specialty chains | +0.9% | Southeast São Paulo and Belo Horizonte, South Curitiba and Porto Alegre, Center-West Brasília | Medium term (2-4 years) |

| Large-format porcelain slabs elevating ASPs and specifications | +0.6% | Southeast premium residential, hospitality, and retail in São Paulo and Rio | Medium term (2-4 years) |

| Sustainability and low-VOC, digital-print performance lines | +0.5% | National compliance with Southeast and South early adopters for LEED v4.1 projects | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Housing Program Upcycle and Robust Residential Launches/Sales

Minha Casa Minha Vida Phase IV funds two million housing units by 2026, creating predictable floor demand at scale that prioritizes durable ceramic and localized SPC options that meet cost and schedule targets. By November 2024, contracts covered approximately 500,000 units, and broader 2024 sales momentum reported by the national builders’ chamber prompted developers to secure multi-quarter flooring agreements, which support new resilient and porcelain line investments. The structural lift to the Brazil floor covering market rests on the combination of a funded social-housing pipeline and steady private launches that compress installation windows and reward quick-turn, moisture-safe systems [1]CBIC Analytics Team, “Housing Programs and Real Estate Indicators 2024–2025,” Câmara Brasileira da Indústria da Construção, cbic.org.br. Outside subsidized brackets, high borrowing costs temper upgrades from entry ceramic to premium vinyl or large-format porcelain, which moderates mix improvement even as unit volumes benefit from the programmatic base. The net effect is a supportive demand floor for the Brazil floor covering market, while discretionary mix uplift proceeds more unevenly across regions and income tiers.

Ceramic Tiles Dominance Supported by Domestic Scale and Climate Fit

Brazil’s ceramic leadership is rooted in kiln scale, proximity to raw materials, and climate performance that suits humid and hot regions, which keeps ceramic the default specification in mass residential and many commercial applications. Large national producers sustain utilization through cost discipline and broad portfolios, while energy and logistics advantages in leading clusters strengthen price competitiveness against imports. The Brazil floor covering market continues to rely on ceramic to defend baseline affordability, which is especially important in subsidy-linked projects that must meet strict price per square meter. Margin strain since 2024 forced selective portfolio rationalization among diversified groups, as management teams prioritized profitability and curtailed undifferentiated SKUs. Even with these adjustments, entrenched familiarity with ceramic installation and local service density remains a durable moat, reinforcing ceramic’s share within the Brazilian floor covering market through the medium term.

LVT/SPC Adoption in Renovations and Moisture-Prone Areas

SPC rigid-core vinyl, projected to post an 11.39% CAGR through 2031, benefits from click-lock formats that compress labor time and avoid wet work, which is decisive for occupied-unit renovations and fast-track multifamily projects. Retailers in Northeast capitals have reported a strong shift to SPC within plank sales, supported by persistent humidity and the need for waterproof solutions that safeguard new-builds and retrofits. Localization matters as domestic SPC lines shorten lead times from months to weeks and enable integrated manufacturing that reduces water and energy use compared to flexible LVT. Investments at national plants also cut emissions intensity and power costs, with one leader reporting 59% energy cuts per square meter and an 83% greenhouse gas reduction after moving to 100% renewable electricity at its Brazil site [2]Tarkett Sustainability Team, “Universal Registration Document 2024,” Tarkett, tarkett.com. Feedstock and recycled PVC availability can still constrain rapid ramps, which makes planning and take-back loops more critical to balance sustainability goals with unit economics.

Omnichannel B2C Expansion by Home Centers and Specialty Chains

B2C is gaining share as large-format home centers deepen e-commerce, click-and-collect, and in-store advisory services that simplify the buyer journey for flooring systems and installation kits. One major retailer operates dozens of stores across Brazil and has expanded a large distribution center with automation for heavy products, enabling same-day availability in its largest metro area. Specialty chains leverage parent-company technical capabilities to offer complete systems, which convert transactional tile or plank sales into bundled subfloor, adhesive, and acoustic solutions that help meet compliance. Digital visualizers and calculators from manufacturers now bridge information gaps, letting consumers test designs and quantity needs before store visits, which improves conversion and compresses project timelines. As a result, the Brazil floor covering market is seeing more DIY-friendly resilient products and a greater emphasis on after-sales support that reinforces customer trust in installation outcomes.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Financing costs and construction cost pressure outside subsidy segments | -0.7% | National, especially middle-income segments in Southeast and South urban condominiums | Short term (≤ 2 years) |

| PVC resin trade measures and input volatility impacting vinyl costs | -0.4% | National vinyl converters, import-dependent supply chains through the Santos port | Short term (≤ 2 years) |

| NBR 15575 acoustic and impact requirements raising system costs | -0.3% | Multifamily residential in Southeast metros and South urban areas | Medium term (2-4 years) |

| Ceramic industry demand recovery is slower than the 2019 baseline | -0.5% | National, concentrated in Santa Gertrudes and Santa Catarina producers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Financing Costs and Construction Cost Pressure Outside Subsidy Segments

Elevated policy rates raise mortgage and construction finance costs for projects outside social-housing programs, which compresses discretionary upgrades and narrows the viable specification set for mid-market developments. Builders respond by prioritizing durable, lower first-cost materials that help preserve absorption at target price points, which supports ceramic share in the Brazil floor covering market. Household leverage and slower retail material consumption since mid-2025 have also weighed on renovation activity, which historically shaped a large portion of flooring demand. These conditions encourage longer supplier contracts for predictability as developers seek to manage input volatility and installation timelines under tighter pro formas. The headwind is cyclical by nature, though its intensity varies by region and income band, and it keeps mix improvement in check within the Brazil floor covering market through the near term.

Ceramic Industry Demand Recovery Slower Than 2019 Baseline

After a pandemic-era spike and subsequent correction, leading producers reported utilization variability and called out price aggression that eroded margins, citing quarters in which tiles moved with negligible profitability. National association data confirm that Brazil’s ceramic sector remains a global leader despite domestic demand lagging pre-2019 trends, which keeps competitive pressure high and strategic focus fixed on cost discipline. That backdrop helps explain portfolio rationalization by diversified groups, where SKU cuts concentrate resources in higher-turn or higher-margin formats. The slower recovery also encourages export activity and cross-border plays, which absorb capacity and cushion demand fluctuations at home. The net result is an industry still centered on ceramic scale that underpins the Brazil floor covering market but with a tighter rein on capital and a sharper focus on value over volume.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Vinyl's Waterproof Click Systems Narrow Ceramic's Share Lead

Ceramic and porcelain tiles held 46.61% product share in 2025, as vinyl flooring is projected to grow 4.69% annually from 2026 to 2031, steadily taking retrofit and new-build demand that once defaulted to mortar-set tiles. Brazil remained the world’s third-largest ceramic producer in 2024 at 825 million m² with 4% year-on-year growth, yet kiln utilization swung from 67% in 1Q25 to 76% in 3Q24, signaling a pandemic-era inventory overhang and the margin pressure that followed. One leading producer noted tiles sold at no margins in Q3 2025 and cut its range from 1,600 to 1,000 SKUs to target 15% to 20% medium-term EBITDA. Laminate occupied a narrowing middle at an estimated 12% to 15% share in 2025. Eucafloor’s 906x906 mm Square line launched in 2024 with an HPP substrate from FSC-certified forests, but it still faces substitution from SPC’s superior moisture resistance in Brazil’s humid climates and from ceramic’s 15% to 25% lower first cost in social-housing specifications.

Wood flooring, both solid and engineered, held an estimated 8% to 10% share and stayed concentrated in premium residential, with annual sales below 10 million m² nationwide. Coastal humidity often exceeds 1,500 mm, and termite exposure favors engineered constructions over solid planks, while imported species such as North American oak and European ash typically cost BRL 150 to 250 per m², roughly double ceramic’s BRL 45 to 65 per m². Carpet and area rugs were used mainly as hospitality and residential accents, while commercial buyers increasingly specified antimicrobial LVT for healthcare and slip-resistant vinyl for retail, eroding carpet’s traditional role. Other products, such as cork, bamboo, rubber, and recycled composite, served sustainability-driven projects, with a take-back program recycling more than 30 tons of post-installation LVT waste in 2024 to support LEED v4.1 credits. Price premiums of 20% to 40% over ceramic kept these alternatives focused on certified green buildings rather than the mass market.

By End User: Commercial Narrows Residential’s Lead via Institutional Fit-Outs

Residential accounted for the largest share in 2025, anchored by the funded pipeline of Minha Casa Minha Vida and the longstanding housing deficit that sustains steady new-built volume. Commercial is projected to grow at 5.12% through 2031, with healthcare, retail, and education showing renewed fit-out momentum and consistent demand for low-VOC resilient solutions and durable large-format porcelain in high-traffic areas. Municipal facility upgrades and retail asset refreshes set clear requirements for cleanability and uptime, which elevate materials that reduce grout lines, resist moisture, and install quickly with minimal disruption. Government and public procurement criteria that prioritize local content also reinforce ceramic and locally made resilient options, which tighten alignment between supply strategies and end-user needs within the Brazil floor covering market [3]ANFACER Team, “Top Producers and Capacity in Brazil 2023,” ANFACER, anfacer.org.br.

Residential growth moderates from the pandemic-era surge as rates remain elevated, yet programmatic housing sustains baseline volumes that favor fast, durable finishes with simple maintenance. Commercial uptrend narrows the gap as institutional backlogs convert to contracted work and as property owners seek antimicrobial and low-emission specifications to enhance tenant and patient experience. Multifamily standards that require acoustic performance are reshaping specifications into complete systems, which encourages partnerships across manufacturers, installers, and channels in the Brazil floor covering industry. Taken together, the end-user mix is evolving toward a dual-engine model in the Brazil floor covering market, where residential provides the volume base and commercial contributes mix and margin through higher-spec projects.

By Distribution Channel: B2C/Retail Gains Share via Digital-Physical Integration

B2C held the majority share at 59% in 2025 and is projected to post a 7.20% CAGR through 2031, supported by national home centers that integrate online discovery with rapid fulfillment and in-store technical support. Large-format chains have scaled distribution and automation to handle heavy flooring products, which supports same-day or next-day availability in major metro areas and accelerates project starts. Specialty retailers differentiate with services such as subfloor assessment and code-compliant underlay bundling, which addresses multiunit acoustic standards and reduces install risk. Manufacturer tools that let customers visualize patterns and estimate quantities bridge the online-offline gap, which improves conversion and reduces order errors in the Brazil floor covering market.

B2B channels remain essential for developer-driven volumes, especially in social housing and institutional projects where locked-in supply agreements reduce exposure to input volatility. Contractor preferences reflect project goals, with ceramic leading in cost-sensitive builds and SPC rising in mid-market condominiums that need fast, quiet, and moisture-safe installs. Over the forecast, B2C’s share gains are shaped by DIY-friendly resilient products and the growth of appointment-based, in-store advisory services, which make complex decisions easier for homeowners in the Brazil floor covering market. As channels converge on system solutions and verified installers, the Brazil floor covering market benefits from a clearer value proposition that links product selection, code compliance, and total installed cost.

Geography Analysis

Regional demand profiles differ by industrial base, income levels, and the mix of new-build and retrofit programs, with the Northeast projected to grow the fastest at 6.72% through 2031 on infrastructure and social-housing momentum that favors fast-install systems. Production clusters centered on major Southeastern corridors support national ceramic supply with dense networks of kilns, distributors, and installers that reinforce the ceramics' installed cost advantage. Urban rehabs and institutional projects in coastal metros also channel demand toward moisture-tolerant resilient formats that shorten downtime and simplify maintenance within the Brazil floor covering market.

In the South, health facility upgrades following severe weather events sustained resilient demand for low-VOC vinyl and durable surface solutions in public buildings and clinics, driving system specifications that value cleanability and acoustic comfort. Proximity to major tile producers further stabilizes availability and delivery times, reinforcing ceramic’s share in everyday applications and supporting specialty exports to regional markets. The Brazil floor covering market continues to see premium adoption of large-format porcelain in the largest metros, where logistics and skilled labor enable smooth installs and where commercial assets require fewer grout lines and shorter maintenance cycles.

Competitive Landscape

The Brazil floor covering market remains fragmented at the multi-material level, despite notable concentration among the largest ceramic producers where the top five controlled nearly half of tile output in 2023. This structure produces two strategic paths, one built on cost leadership through kiln scale and raw-material proximity, and the other on differentiation through premium formats, retail integration, and faster-install resilient systems. Producers and retailers are also tightening assortments and service models to protect margins, redirecting investment toward higher-turn SKUs and code-ready systems that incorporate underlays and low-VOC adhesives [4]Dexco Investor Relations, “Earnings and Strategic Update 2025,” Dexco, dexco.com.br.

Portfolio rationalization accelerated during 2025 as leaders flagged pressure from price aggression and adjusted their ceramic offerings to restore profitability. Investments in large-format porcelain production and in localized resilient capacity became key to mixed improvement and to reducing lead-time risk in social-housing schedules. International capacity, including a U.S. plant operated by a Brazil brand, is augmenting North American reach and balancing domestic cycles, which supports stable utilization at home and abroad for participants in the Brazil floor covering market.

Sustainability upgrades at national plants, including automation, electrification, and renewable power adoption, are cutting energy per square meter and emissions while supporting take-back loops that provide recycled inputs for resilient lines. Retail partners continue to strengthen omnichannel flows that reduce friction for customers, from digital visualization to same-day pickup, which in turn raises attachment of installation kits and code-compliant underlays. With public programs and commercial retrofits favoring solutions that install quickly and meet VOC and acoustic criteria, suppliers that bundle systems and deliver dependable logistics will retain an advantage in the Brazil floor covering market.

Brazil Floor Covering Industry Leaders

Portobello S.A.

Mohawk Industries

Tarkett S.A.

Dexco S.A.

Grupo Lamosa

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Tarkett invested USD 8 million in automation and waste-heat recovery at its Jacareí, Brazil, facility, cutting CO₂ emissions per square meter and expanding its ReStart take-back loop for post-installation offcuts. The plant now sources 100% renewable electricity, achieving a 59% energy reduction versus baseline.

- June 2025: Braskem completed a polypropylene plant expansion in Texas, freeing Brazilian logistics capacity and stabilizing resin supply for South American flooring converters, which eased congestion impacts on vinyl value chains.

- January 2025: Mohawk Industries reported its Brazilian operations delivered the fastest regional growth in its Global Ceramic segment, crediting demand for large-format porcelain and export momentum. The company operates Eliane and Elizabeth Revestimentos brands, with combined capacity exceeding 90 million m² annually.

- August 2024: Leroy Merlin Brasil completed an energy-optimization pilot across selected stores, targeting double-digit energy savings by the end of 2025, and expanded distribution capabilities to support heavy-product handling for flooring.

Brazil Floor Covering Market Report Scope

A floor covering is a type of material used to cover a floor. As a result, the floor covering market encompasses all operations associated with the manufacture, distribution, and installation of materials intended to cover a floor. It consists of four major product families. Textile coverings, parquet floors, plastic coverings (PVC or linoleum), and tiles are among the materials utilized. The report covers the complete background analysis of the Brazil floor covering market, which includes an assessment of the National accounts, economy, and the emerging market trends by segments, significant changes in the market dynamics, and the market overview. The Brazil floor covering Market is Segmented by Product Type (Carpet, Wood, Ceramic & Porcelain Tiles, Laminate, Vinyl [LVT, Sheet, VCT], Stone, and Others), End User (Residential and Commercial), Distribution Channel (B2C/Retail and B2B/Contractors), and Geography (Southeast, South, Northeast, Center-West, and North). Market Forecasts are Provided in Terms of Value (USD).

By Product Type

| Carpet & Area Rugs |

| Wood Flooring |

| Ceramic & Porcelain Tiles |

| Laminate Flooring |

| Vinyl Flooring (LVT, Sheet, VCT) |

| Stone Flooring |

| Other Products |

By End User

| Residential | |

| Commercial | Hospitality & Leisure |

| Retail & Shopping Centers | |

| Healthcare Facilities | |

| Education | |

| Corporate Offices | |

| Public & Government Buildings | |

| Other Commercial Users |

By Distribution Channel

| B2C / Retail | Home Centers |

| Specialty Flooring Stores | |

| Online | |

| Other Distribution Channels | |

| B2B / Contractors |

By Region

| Southeast |

| South |

| Northeast |

| Center-West |

| North |

| By Product Type | Carpet & Area Rugs | |

| Wood Flooring | ||

| Ceramic & Porcelain Tiles | ||

| Laminate Flooring | ||

| Vinyl Flooring (LVT, Sheet, VCT) | ||

| Stone Flooring | ||

| Other Products | ||

| By End User | Residential | |

| Commercial | Hospitality & Leisure | |

| Retail & Shopping Centers | ||

| Healthcare Facilities | ||

| Education | ||

| Corporate Offices | ||

| Public & Government Buildings | ||

| Other Commercial Users | ||

| By Distribution Channel | B2C / Retail | Home Centers |

| Specialty Flooring Stores | ||

| Online | ||

| Other Distribution Channels | ||

| B2B / Contractors | ||

| By Region | Southeast | |

| South | ||

| Northeast | ||

| Center-West | ||

| North | ||

Key Questions Answered in the Report

What is the current size and growth outlook for the Brazil floor covering market?

The Brazil floor covering market size reached USD 11.99 billion in 2025, is expected to be USD 12.87 billion in 2026, and is projected to reach USD 16.13 billion by 2031 at a 4.62% CAGR.

Which product categories are leading and growing fastest in Brazil?

Ceramic and porcelain lead in volume due to cost and climate fit, while Vinyl Flooring (LVT, Sheet, VCT) is the fastest growing subsegment, projected at an 4.69% CAGR through 2031.

How is the Brazil floor covering market evolving by sales channels?

B2C retail holds the largest share at 59% in 2025 and is projected to grow at 7.20% through 2031, backed by omnichannel investments and faster fulfillment for heavy flooring products.

What regulations are shaping product and system choices in Brazil?

The 2026 Green Building Code requires at least 30% low-VOC finishes, and multifamily acoustic rules are lifting demand for integrated systems that bundle underlays and adhesives.

Which regions are expected to grow the fastest?

The Northeast is projected to post the fastest growth at 6.72% through 2031, supported by infrastructure and social-housing projects that favor fast-install systems.

What factors could constrain growth in the near term?

Elevated financing costs outside subsidy programs and a slower ceramic demand recovery versus pre-2019 levels are moderating mix improvement and weighing on renovation intensity.

Page last updated on: