Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

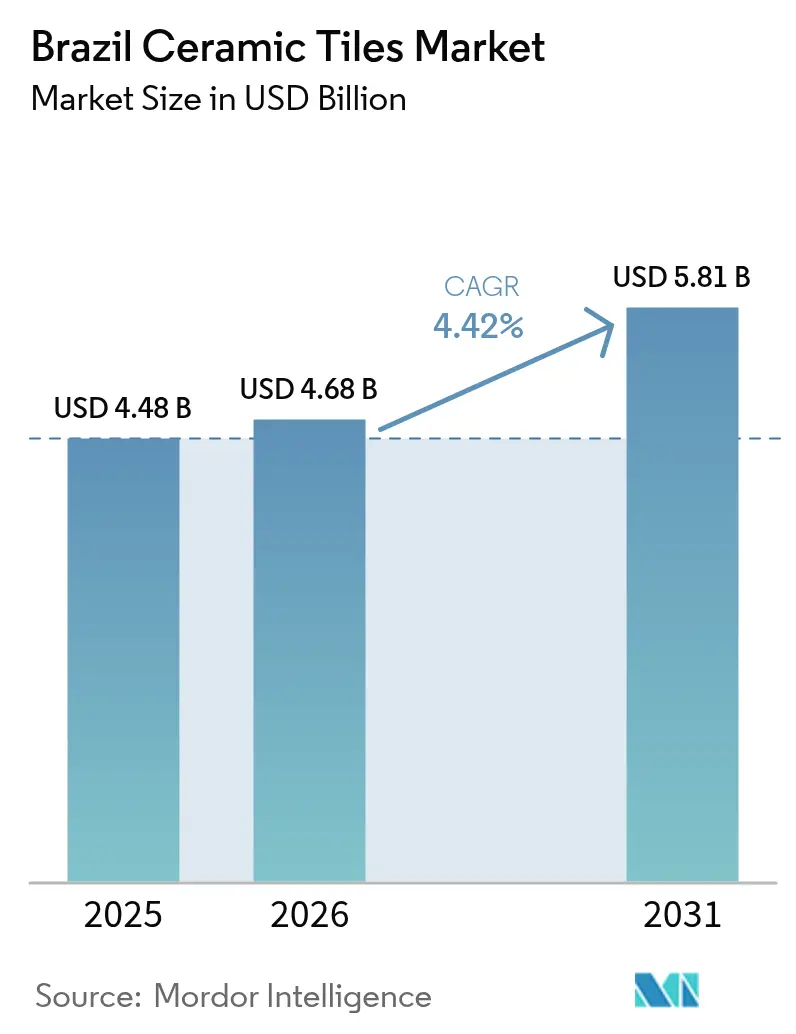

| Base Year Market Size (2025) | USD 4.48 Billion |

| Market Size (2026) | USD 4.68 Billion |

| Market Size (2031) | USD 5.81 Billion |

| Growth Rate (2026 - 2031) | 4.42% CAGR |

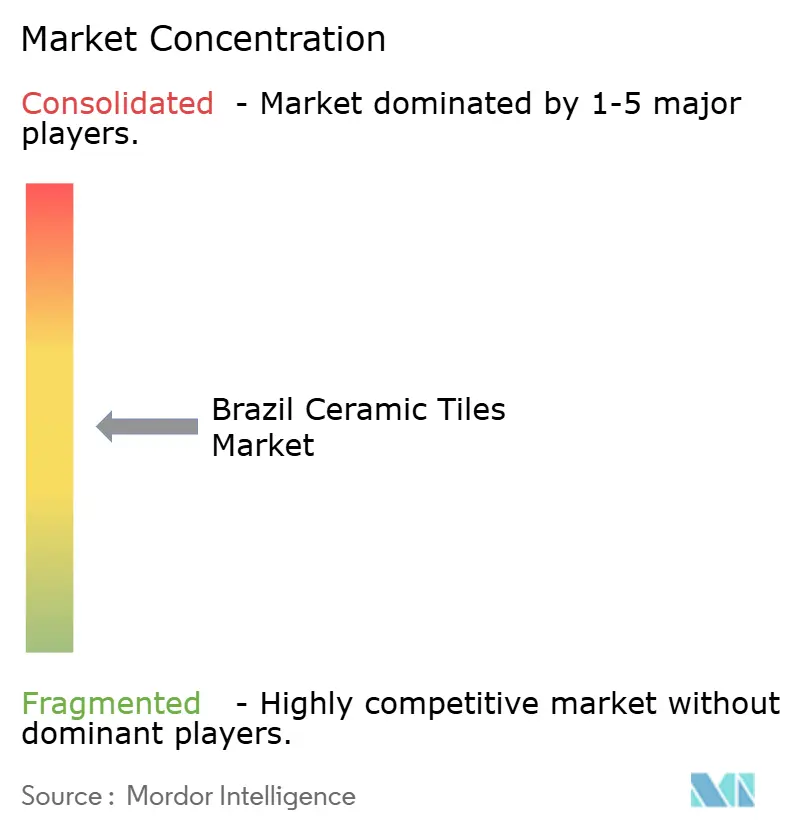

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Brazil Ceramic Tiles Market Analysis by Mordor Intelligence

The Brazil ceramic tiles market size is projected to be USD 4.48 billion in 2025, USD 4.68 billion in 2026, and reach USD 5.81 billion by 2031, growing at a CAGR of 4.42% from 2026 to 2031. Momentum in the Brazil ceramic tiles market is supported by public housing contracting that sustains baseline volume, faster adoption of large-format porcelain that lifts price mix, and better access to free natural-gas contracts that ease firing costs in key clusters. The product shift toward rectified formats and thin slabs improves installation speed and reduces grout maintenance, strengthening the competitive case for porcelain in renovation cycles. The ongoing migration to free gas contracts helped ceramic producers secure 5-7% molecule price reductions in 2024, improving utilization flexibility in São Paulo and Santa Catarina hubs that anchor the Brazil ceramic tiles market. Construction indicators turned upward as cement volumes rose 5.9% year over year in Q1 2025, even as household debt service near 48% of disposable income, constraining discretionary remodels.

Key Report Takeaways

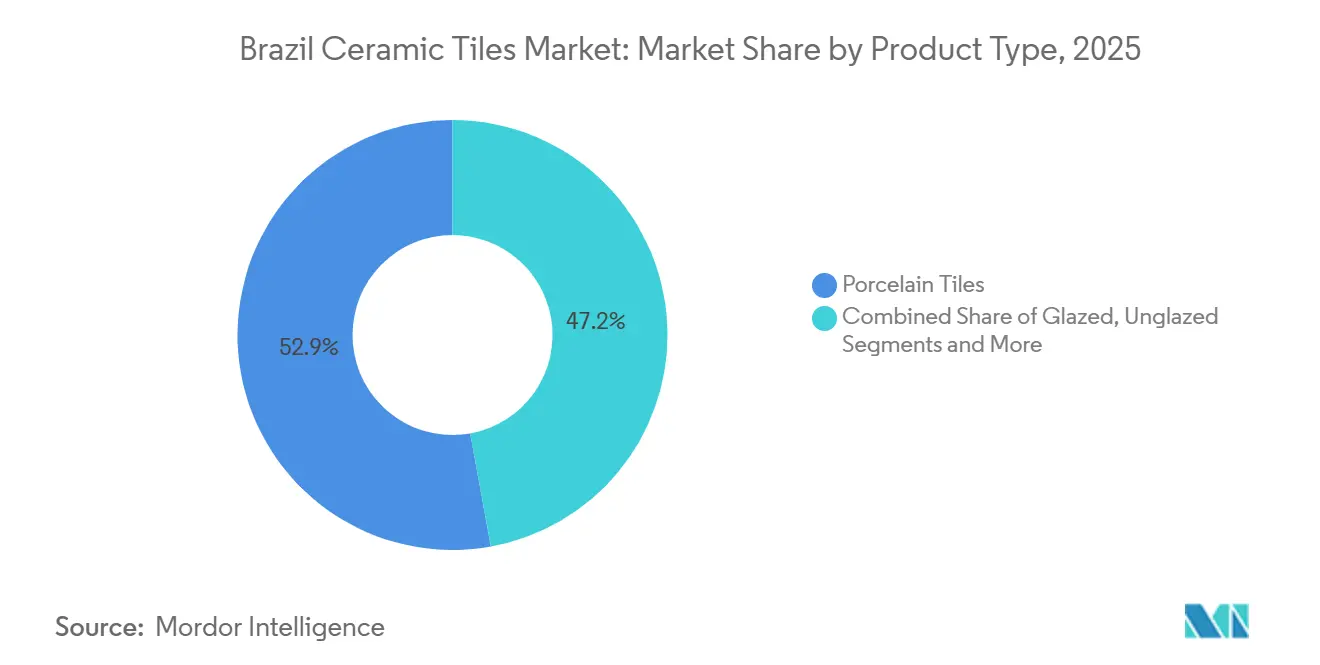

- By product type, porcelain tiles led with 52.85% revenue share in 2025, while mosaic tiles are forecast to grow at a 4.73% CAGR through 2031.

- By application, floor use accounted for a 62.12% share in 2025, and roofing is projected to expand at a 4.68% CAGR to 2031.

- By end-user, commercial projects held 60.41% of the 2025 volume, and residential demand is tracking the highest growth at a 5.52% CAGR through 2031.

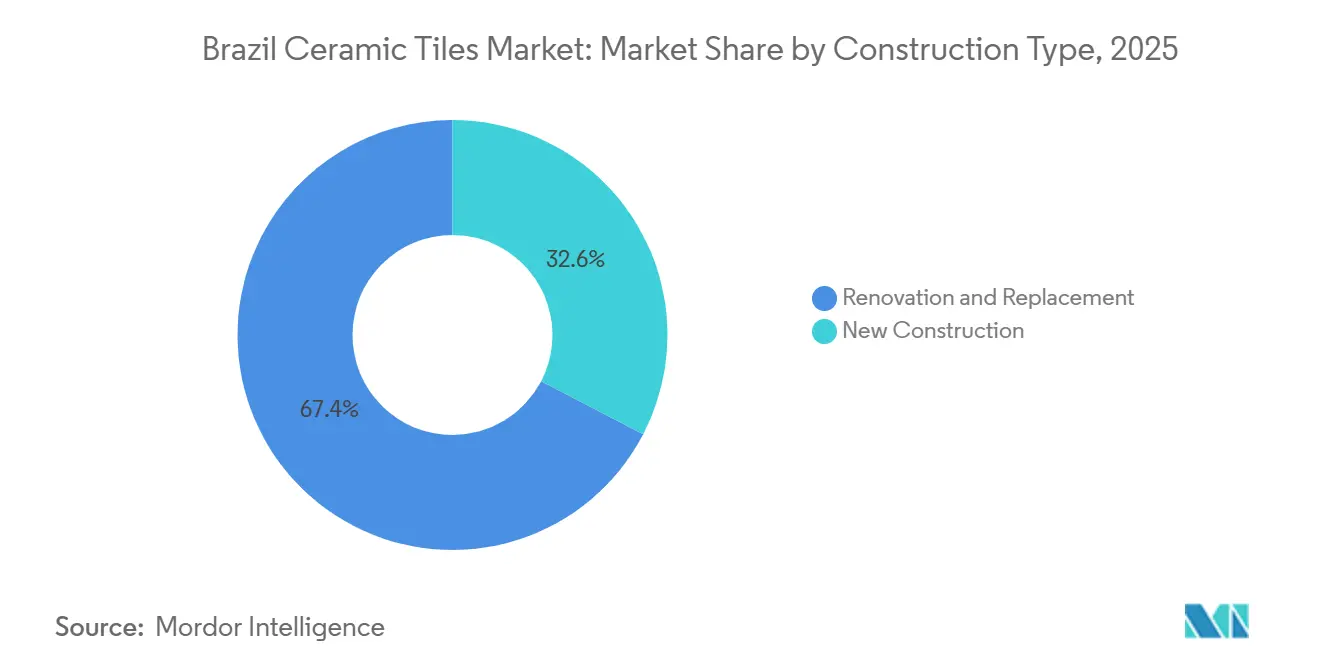

- By construction type, renovation and replacement commanded a 67.36% share in 2025, while new construction is advancing at a 5.03% CAGR to 2031.

- By distribution channel, home improvement and DIY stores captured 39.54% of 2025 distribution, and online retail is expanding at a 6.82% CAGR through 2031.

- By geography, the Southeast region accounted for a 40.60% share in 2025, while the Northeast is the fastest-growing region at a 5.28% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Brazil Ceramic Tiles Market Trends and Insights

Drivers Impact Analysis*

| Driver / Restraint (as applicable in title case) | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| 2026–2031 housing program outlays lifting affordable tile demand | +1.2% | National, with a concentration in Southeast and Northeast | Long term (≥ 4 years) |

| Fast shift to large-format porcelain and sintered surfaces | +0.8% | Global, urban concentration | Medium term (2-4 years) |

| Energy cost normalization improves plant utilization | +0.6% | National, significant impact on São Paulo and Santa Catarina clusters | Short term (≤ 2 years) |

| Easing credit and renovation financing supporting mid-cycle replacements | +0.5% | National, particularly middle-class segments in Southeast and South | Medium term (2-4 years) |

| Public health/sanitation builds in the North/Northeast, requiring hygienic surfaces | +0.5% | North and Northeast, spillover to municipal projects nationwide | Long term (≥ 4 years) |

| Omnichannel tile retail and franchise expansion into interior municipalities | +0.4% | National, metropolitan areas, and tier-2 cities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

2026–2031 Housing Program Outlays Lifting Affordable Tile Demand

The Minha Casa Minha Vida program set budgeted resources for 2025 and targeted up to 2 million contracted housing units by 2026, aided by higher eligible property ceilings that favor porcelain specifications in urban projects. Government actions to restart stalled housing units created near-term volume that ripples through ceramic supply chains and installation networks. This public pipeline supports steady factory run rates in the Brazil ceramic tiles market, helping manufacturers plan kiln schedules and procurement with fewer idle periods. Procurement frameworks increasingly require certified low-porosity porcelain for wet areas, which elevates compliant producers who meet absorption thresholds in municipal codes and tender prequalification[1]Centro Cerâmico do Brasil, “Programas de Certificação e Ensaios para Revestimentos Cerâmicos,” Centro Cerâmico do Brasil, ccb.org.br . Access to accredited programs run by the Centro Cerâmico do Brasil also translates into premium price opportunities on public bids where lifecycle performance and hygiene standards are scored.

Fast Shift to Large-Format Porcelain and Sintered Surfaces

In January 2025, Mohawk Brazil highlighted a digital-printing line capable of 100 meters per minute, improving design throughput and response to architect requests for photorealistic finishes. The transition from small legacy formats to large-format porcelain and thin slabs reduces visible grout and speeds installation, which resonates across the Brazil ceramic tiles market during tight project schedules. Dexco’s Industry 4.0 facility in Botucatu entered the sintered stone segment with significant installed capacity, positioning the group to serve countertops and façades that demand dimensional stability and UV resistance. Inventory economics also shift as distributors favor rectified large-format SKUs that streamline handling and raise shelf productivity, which enables vendors to ship mixed pallets and consistent calibers. Hygiene expectations formed after the pandemic reinforce slab adoption as fewer joints improve cleaning perceptions, while antimicrobial glaze options offer added value in healthcare and food-service builds.

Energy Cost Normalization Improving Plant Utilization

Natural gas represents a large share of ceramic production costs, and producers expanded participation in the free gas market to lower energy inputs and improve utilization flexibility. In 2024, several manufacturers negotiated free-market gas supply with international and regional marketers, reporting 5-7% molecule price reductions that stabilized kiln operations in key clusters[2]ABEGÁS Newsroom, “Contratos de Gás Livre por Setor Industrial,” ABEGÁS, abegas.org.br . Industry data show contracted volumes and the number of free clients expanded into 2025, supporting a structural shift toward shorter energy contracts and more responsive capacity planning in the Brazil ceramic tiles market. The “Gás para Empregar” agenda targets lower final industrial gas prices through adjustments across processing and transport, a policy vector that would improve ceramic cost curves if fully delivered. Plant upgrades also matter, as waste-heat recovery and process standardization deliver fast paybacks, including daily gas savings documented in recent impact reporting by a large multinational ceramics group.

Public Health/Sanitation Builds in North/Northeast Requiring Hygienic Surfaces

Public tenders in sanitation and healthcare emphasize certified low-porosity surfaces for durability and hygiene, which directs specifications toward porcelain formats that meet municipal standards. In cities where facility upgrades are underway, procurement documents increasingly call for antimicrobial finishes and low-absorption tiles to reduce maintenance risks. ABNT technical standards on performance and abrasion inform product selection for corridors, stations, and wet environments, raising the bar for compliance in the Brazil ceramic tiles market. Project owners and city agencies are adopting materials screening that aligns with lifecycle and indoor-environment quality benchmarks, which rewards suppliers that publish third-party documentation. Regional producers with nearby factories in the Northeast states can reduce freight burdens and improve bid competitiveness on municipal timelines.

Restraints Impact Analysis*

| Driver / Restraint (as applicable in title case) | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Natural gas volatility and decarbonization capex burden | -0.9% | National, severe impact on energy-intensive manufacturers | Short term (≤ 2 years) |

| Credit cost volatility and slower mortgage formation | -0.7% | National, particularly affecting middle-income segments | Short term (≤ 2 years) |

| Logistics and clay-mining licensing bottlenecks in select regions | -0.6% | North and Northeast, with freight premiums 18-22% above Southeast | Long term (≥ 4 years) |

| Substitution from LVT/SPC and other resilient floors | -0.4% | National, premium residential segment | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Natural Gas Volatility and Decarbonization Capex Burden

Natural gas remains a large input cost in ceramic manufacturing, and price fluctuations strain margins, especially where firing cycles are energy-intensive and continuous. While free-market contracting delivered molecule savings for several producers, volatility still requires hedging and shorter agreements that can limit long-term visibility in the Brazil ceramic tiles market. Policy efforts seek to lower all-in industrial gas prices by addressing processing and transport tariffs, yet reform timelines can be extended, which delays full cost relief. Capital is also needed to meet upcoming environmental and product-safety rules, including reformulations that align with low-VOC targets and hazardous-substance limits. Investments in waste-heat recovery and process optimization deliver fast paybacks and enable access to tenders with green-credit criteria, but the upfront burden can be heavy for smaller regional players.

Substitution from LVT/SPC and Other Resilient Floors

Rigid-core vinyl products are on a faster growth path through 2031, driven by waterproof performance and quick installation that appeals to time-constrained renovators across urban centers. As SPC mix gains share at retail, showrooms reallocate shelf space and promotion budgets, increasing competitive pressure on mid- and entry-level ceramic tiles in the Brazil ceramic tiles market. Some ceramic producers have repurposed infrastructure to run SPC lines, accelerating lead times and reducing reliance on imports in a defensive move to retain channel relationships. Feedstock investments in the region’s resin chain and packaging inputs support resilient-floor availability, which keeps the competitive bar high for ceramic value propositions. Ceramic leaders are countering with antimicrobial glazes and enhanced surface technologies, though these improvements can raise unit costs and face price-sensitive demand in renovation cycles.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Mosaic Tiles, Capture Design Premiums

Porcelain tiles commanded 52.85% of the Brazil ceramic tiles market share in 2025, supported by stain resistance, strength aligned to BIa classifications, and inkjet advances that deliver stone and wood looks at accessible prices. Mosaic tiles are projected to post the fastest growth at a 4.73% CAGR through 2031 as designers specify them for pools, accents, and backsplashes, where patterning drives willingness to pay in the Brazil ceramic tiles market. Glazed ceramic maintains an important role in budget-sensitive projects, while unglazed formats remain in logistics, commercial kitchens, and circulation zones that value abrasion resistance over surface effects. Product differentiation is widening as large-format slabs, thinner bodies, and textured finishes expand use cases from floors and walls to façades and countertops. The Brazil ceramic tiles industry is also using product standardization to cut waste and fuel consumption, freeing room for design refreshes in annual collections.

There is visible innovation at leading brands that strengthens the mix. Eliane’s 2025 portfolio included marble-look and wood-look lines aimed at renovation and commercial appeal across national channels. Select producers are publishing life-cycle and ISO 17889-1 documentation to meet green-procurement thresholds, which broadens access to municipal projects that include hygiene and VOC criteria[3]Marazzi Group Sustainability Office, “ESG Report 2024,” Marazzi Group, marazzigroup.com . Grupo Fragnani’s brand launches at major trade fairs and growing installed capacity confirm the push into large formats and elevated finishes in the Brazil ceramic tiles market. The Brazil ceramic tiles market size for mosaic and decorative lines is projected to expand at a mid-single-digit CAGR through 2031, with design-rich features working well in hospitality, premium residential, and wellness spaces.

By Application: Roofing Gains Momentum in Sanitation Builds

Floor applications accounted for 62.12% of 2025 demand, reflecting preference for durable, low-maintenance surfaces across residential towers, retail, and institutional corridors in the Brazil ceramic tiles market. The roofing category is projected to grow at a 4.68% CAGR as sanitation and healthcare projects specify tiles in rooftops, reservoirs, and terminal structures that need UV and moisture performance, which supports diversification beyond traditional floors and walls. Wall cladding remains standard in bathrooms and food-prep spaces, where low-porosity porcelain helps limit moisture intrusion and staining under municipal codes. Healthcare and educational facilities continue to specify antimicrobial finishes and easy-clean surfaces to align operations with post-pandemic hygiene protocols. The Brazil ceramic tiles market is also benefiting from growth in commercial transport hubs where slip resistance and deep abrasion performance are mandatory under applicable ABNT standards.

Manufacturers are tailoring product features to meet application specifics, including higher-friction finishes for terraces and roofs, and rectified edges for continuous floor planes in premium retail. Digital printing continues to expand into wood-tone and stone-look variants for wall cladding in hospitality and multi-family common areas, which supports price-mix resilience. Certification through the Centro Cerâmico do Brasil validates performance claims on water absorption and structural integrity, a requirement in many public bids where porcelain formats dominate wet zones. Energy-efficiency retrofits such as waste-heat recovery from kiln lines are lowering gas consumption, helping suppliers keep application-specific price points competitive in the Brazil ceramic tiles market. The Brazil ceramic tiles market size for roofing and specialized infrastructure-related uses is positioned to expand with planned sanitation and mobility upgrades through the forecast period.

By End-User: Residential Segment Rides Subsidy Wave

Commercial projects held 60.41% in 2025, covering hospitality, retail, healthcare, education, and transit, where durability and hygiene drive selection in the Brazil ceramic tiles market. Residential is on track for a faster 5.52% CAGR to 2031, sustained by public housing pipelines that prioritize porcelain finishes in urban projects and by a steady cadence of mid-cycle replacements. As program rules and tender templates favor compliant low-porosity formats in wet zones, porcelain becomes the default across bathrooms and kitchens within subsidized segments. Product safety standards such as NSF/ANSI 51 in food-contact areas and ISO 17889-1 sustainability scoring are more common on commercial specs, which pushes producers to publish supporting documentation across product lines. The Brazil ceramic tiles market also benefits from hospitality design cycles that demand large-format, nature-inspired finishes, which command strong margins.

In commercial environments, transit and healthcare facilities rely on slip-resistant textures with quantified friction performance, alongside deep abrasion and chemical resistance aligned to ABNT NBR ISO 10545 norms. Residential replacement remains a large and steady demand pool, supported by visualization tools that help homeowners select patterns and formats remotely before showroom engagement. Funding programs backed by worker funds and capped-rate instruments continue to support social-housing pipelines that consume material at a national scale, sustaining factory utilization and logistics flows. The Brazil ceramic tiles market size for residential refresh projects is expected to remain firm through 2031 as digital retail channels and omnichannel fulfillment simplify selection and delivery across large catchment areas.

By Construction Type: Renovation Dominance Reflects Market Maturity

Renovation and replacement commanded 67.36% in 2025, reflecting a mature building stock and the appeal of quick, value-adding remodels across urban households in the Brazil ceramic tiles market. New construction is projected at a 5.03% CAGR, lifted by public housing contracts and institutional projects with clear finish-schedule templates that standardize porcelain use in wet areas. The faster cycle time of renovations suits agile inventory models and mixed-pallet shipments that improve turns and lower working capital for distributors. Manufacturers that harmonize sizes and thicknesses cut breakage and reduce raw material consumption, which can translate into sharper price points and improved availability for both renovation and new-build timelines. Compliance with ABNT water-absorption norms and documented moisture-expansion performance reduces failure risk in legacy buildings, which builds consumer trust in refresh projects.

Renovation activity benefits from omnichannel discovery and AR design previews that lower selection friction and accelerate purchasing decisions among digital-native households. In institutional new builds, tender packages embed lifecycle and hygiene scoring that lift porcelain, antimicrobial finishes, and rectified formats into baseline specifications in the Brazil ceramic tiles market. Documented chemistries aligned to low-VOC thresholds and process disclosures consistent with ISO 17889-1 strengthen bids in cities that prioritize green-credentialed materials. The Brazil ceramic tiles market size for new-build demand is set to benefit from project pipelines in health, sanitation, and education as funding milestones are met and site mobilizations proceed. Over the forecast horizon, renovation remains the larger slice, but new-build share expands steadily as funding frameworks and accreditation pathways mature.

By Distribution Channel: Online Retail Gains Share as DIY Expands

Home improvement and DIY stores captured 39.54% of distribution in 2025, leveraging floor displays and immediate availability for a tactile, design-driven category in the Brazil ceramic tiles market. Online retail is advancing at a 6.82% CAGR through 2031, supported by augmented-reality tools and configurators that enable at-home exploration before showroom visits or click-and-collect pickup. Specialty tile and stone outlets remain essential for architect and contractor consultations, including substrate prep, grout selection, and standards compliance. Direct-to-project channels help lock specifications early in commercial bids, which stabilizes factory scheduling and reduces retail exposure for producers with balanced portfolios.

Franchise networks extend reach into interior municipalities, using centralized marketing and local stocking to capture renovation spending where big-box formats are less common. Flagship showrooms that combine physical product interaction and digital tools lower last-mile costs and consolidate premium sales in high-traffic corridors of the Brazil ceramic tiles market. Export-oriented players complement domestic channels with distributor relationships abroad, though this path requires careful management of freight and standards alignment. Posting third-party certifications and environmental documentation online helps products surface in project searches that filter by sustainability and hygiene criteria. The Brazil ceramic tiles market size for online-driven sales is expected to expand as data-rich product pages, API-integrated stock visibility, and frictionless returns match consumer expectations shaped by other durable-goods categories.

Geography Analysis

The Southeast held 40.60% of the Brazil ceramic tiles market share in 2025, anchored by São Paulo’s Santa Gertrudes cluster and higher household purchasing power that supports large-format porcelain and sintered stone adoption. The region’s proximity to Santos port facilitates export shipments, though congestion can extend vessel wait times and complicated scheduling for export programs. Producers in the Southeast expanded free-market gas contracting by early 2025, capturing 5-7% molecule price savings and improving kiln utilization flexibility. Smart-factory initiatives, including waste-heat recovery and material standardization, position local plants to qualify for green-credentialed municipal tenders in the Brazil ceramic tiles market. Certification support from CCB is readily accessible in the region, which speeds compliance work and supports tender participation.

The Northeast is the fastest-growing region at a 5.28% CAGR through 2031, supported by hospitality investments and public health and sanitation projects that rely on low-porosity porcelain and antimicrobial glazes in sensitive spaces. Local manufacturing assets cut freight costs and lead times for public bids, including a sustainable facility in Alagoas designed to supply domestic and export markets with improved logistics[4]Portobello Corporate Communications, “Unidade Sustentável em Alagoas,” Portobello, portobello.com.br . Freight premiums over the Southeast raise delivered costs, but proximity offsets part of the burden for regionally sited plants in the Brazil ceramic tiles market. Standards for slip resistance and deep abrasion guide surface selection in transit hubs and educational facilities across major Northeastern cities, which support higher-performance formats. Hygiene-led specifications in healthcare and sanitation also reinforce the role of porcelain and antimicrobial finishes as baseline requirements.

The South benefits from a deep ceramics heritage and a skilled supplier base around Santa Catarina, alongside access to maritime routes that enable internationalization strategies by leading brands. Process innovations that repurpose industrial byproducts as partial substitutes in ceramic formulations support cost control and carbon objectives within the Brazil ceramic tiles market. The Central-West advances with institutional projects that specify low-maintenance porcelain, appealing to building owners focused on lifecycle costs and hygiene credentials. In the North, infrastructure upgrades and social programs are elevating demand for easy-install surfaces and durable porcelain in public buildings, which broadens the category’s reach beyond core urban centers. Across regions, the Brazil ceramic tiles market size is supported by public procurement that scores compliance, lifecycle, and hygiene metrics alongside price, which benefits producers who maintain robust documentation and certification pathways.

Competitive Landscape

The Brazil ceramic tiles market is moderately concentrated, with the top five producers accounting for an estimated 50-60% of national revenue in 2025, which still leaves meaningful space for regional specialists and design-led challengers [User-provided market concentration data]. Mohawk Industries has built the largest footprint through acquisitions in Brazil and accelerated product refresh cycles with a high-speed digital-printing line that improves design agility in premium porcelain. Eliane and Elizabeth enhance U.S. channel access through group distribution, while domestic operations standardize formats to reduce waste and fuel consumption. Portobello’s industrial base and brand network support omnichannel strategies and regional supply for projects across Northeast states. The Brazil ceramic tiles market features agile mid-sized firms that moved early to free gas contracts, capturing molecule savings and flexibility that improved run rates without long lock-ins.

Category competition also extends to adjacent surfaces. Dexco entered sintered stone with an Industry 4.0 plant and launched a flagship showroom to integrate digital design with in-person curation for premium projects in the Brazil ceramic tiles market. Some ceramic producers set up SPC lines to defend share as rigid-core vinyl expands, keeping lead times short and strengthening channel relationships with retail partners. Certification is a key differentiator in public-sector tenders, with CCB programs and ISO 17889-1 documentation opening access to bids that weigh lifecycle and hygiene performance. Manufacturers are also investing in water recycling, packaging reduction, and closed-loop processes to qualify for green credits in municipal procurement, lifting the profile of sustainable SKUs.

Execution focuses span digital operations, sustainability, and go-to-market reach in the Brazil ceramic tiles market. Process standardization has already reduced material waste and fuel usage at leading groups, improving cost positions and environmental metrics in tandem. Franchise expansion brings brand presence to tier-2 cities and interior municipalities, while data-rich product content and real-time stock visibility improve digital discovery and conversion. Industry rankings for 2024 production volumes confirm Brazil’s global relevance, and the presence of multiple local champions supports innovation and export development. As project owners emphasize certification, hygiene, and lifecycle economics, suppliers combining operational agility, third-party validations, and omnichannel service are positioned to outpace the category.

Brazil Ceramic Tiles Industry Leaders

Mohawk Brazil (Eliane + Elizabeth)

Cerâmica Carmelo Fior

Grupo Fragnani (Incefra, Incenor, Tecnogres)

Grupo Cedasa (Cedasa, Majopar, Vistabella, Lorenzza)

Portobello Grupo

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Cerâmica Carmelo Fior marked its 85th anniversary at Expo Revestir 2026 with 25 new products across six brands, including large formats with controlled shine and textures, and new rectified wall coverings for residential and commercial use. The launches targeted nationwide availability and reinforced technical performance for engineering channels.

- January 2026: ANFACER published a global ranking that placed four Brazilian ceramic tile producers among the world’s top manufacturers based on 2024 volumes, reaffirming Brazil’s leadership in the number of major producers and the sector’s strategic weight in the national industry.

- June 2025: Braskem completed a 450,000-ton polypropylene plant in Texas that supports resin availability for South American converters, improving supply stability for rigid flooring components used by regional producers that diversified into SPC lines.

- May 2025: Brazil’s pavilion at Coverings 2025 generated significant new business and pipeline opportunities for participating companies, highlighting export momentum and the value of coordinated promotion by Anfacer and ApexBrasil.

Brazil Ceramic Tiles Market Report Scope

Ceramic Tiles are made up of sand, natural products, and clays, and once it is molded into a shape, they are fired into a kiln. Ceramic tiles are durable, resistant to water, moisture, and fire, and cheap compared to other flooring products. The report covers a complete background analysis of the Brazilian ceramic tiles market. It includes a parental market assessment, emerging trends in the segments and regional markets, and significant changes in market dynamics and market overview. The report also offers a qualitative and quantitative assessment by analyzing data gathered from industry analysts and market participants across various key points in the value chain.

The Brazil Ceramic Tiles Market is segmented by product (glazed, porcelain, scratch-free, and other products), application (floor tiles, wall tiles, and other applications), construction type (new construction, replacement and renovation), and end-user (residential and commercial). The market size and forecasts are provided in value (USD) for all the above segments.

By Product Type

| Porcelain Tiles |

| Glazed Ceramic Tiles |

| Unglazed Ceramic Tiles |

| Mosaic Tiles |

| Others (Decorative, Patterned, Handmade) |

By Application

| Floor |

| Wall |

| Roofing |

By End-User

| Residential | |

| Commercial | Hospitality (Hotels, Resorts) |

| Retail Spaces | |

| Offices & Institutions | |

| Healthcare | |

| Educational Facilities | |

| Transport Hubs (Airports, Metro, Bus Terminals) | |

| Other Commercial Users |

By Construction Type

| New Construction |

| Renovation and Replacement |

By Distribution Channel

| Specialty Tile & Stone Stores |

| Home Improvement & DIY Stores |

| Online Retail |

| Direct Sales to Contractors |

By Geography

| Southeast |

| South |

| Northeast |

| Central-West |

| North |

| By Product Type | Porcelain Tiles | |

| Glazed Ceramic Tiles | ||

| Unglazed Ceramic Tiles | ||

| Mosaic Tiles | ||

| Others (Decorative, Patterned, Handmade) | ||

| By Application | Floor | |

| Wall | ||

| Roofing | ||

| By End-User | Residential | |

| Commercial | Hospitality (Hotels, Resorts) | |

| Retail Spaces | ||

| Offices & Institutions | ||

| Healthcare | ||

| Educational Facilities | ||

| Transport Hubs (Airports, Metro, Bus Terminals) | ||

| Other Commercial Users | ||

| By Construction Type | New Construction | |

| Renovation and Replacement | ||

| By Distribution Channel | Specialty Tile & Stone Stores | |

| Home Improvement & DIY Stores | ||

| Online Retail | ||

| Direct Sales to Contractors | ||

| By Geography | Southeast | |

| South | ||

| Northeast | ||

| Central-West | ||

| North | ||

Key Questions Answered in the Report

What is the current size and growth outlook for the Brazil ceramic tiles market?

The Brazil ceramic tiles market size is USD 4.68 billion in 2026 and is projected to reach USD 5.81 billion by 2031 at a 4.42% CAGR.

Which product category leads demand in Brazil’s tile sector?

Porcelain led with 52.85% of the Brazil ceramic tiles market share in 2025, supported by low porosity, high strength, and advanced inkjet designs suited for both residential and commercial projects.

Which sales channels are expanding the fastest in the Brazil ceramic tiles market?

Online retail is growing at a 6.82% CAGR through 2031, supported by augmented-reality tools and click-and-collect models that reduce last-mile costs while preserving a tactile showroom experience.

What factors are improving cost competitiveness for Brazilian tile producers?

Migration to the free natural-gas market delivered 5-7% molecule price reductions in 2024, and process upgrades like waste-heat recovery reduced daily gas use with fast paybacks, which together improve run-rate stability.

Which regions show the strongest momentum for the Brazil ceramic tiles market through 2031?

The Southeast remains the largest with a 40.60% share in 2025, while the Northeast is the fastest-growing region at a 5.28% CAGR on hospitality and public-health project pipelines that specify low-porosity porcelain.

What is the main competitive threat from substitute materials?

Rigid-core vinyl is expanding rapidly due to waterproof performance and quick installation, prompting some ceramic producers to repurpose lines for SPC to defend share while advancing antimicrobial and sustainability features in porcelain.

Page last updated on: