Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2020 - 2024 |

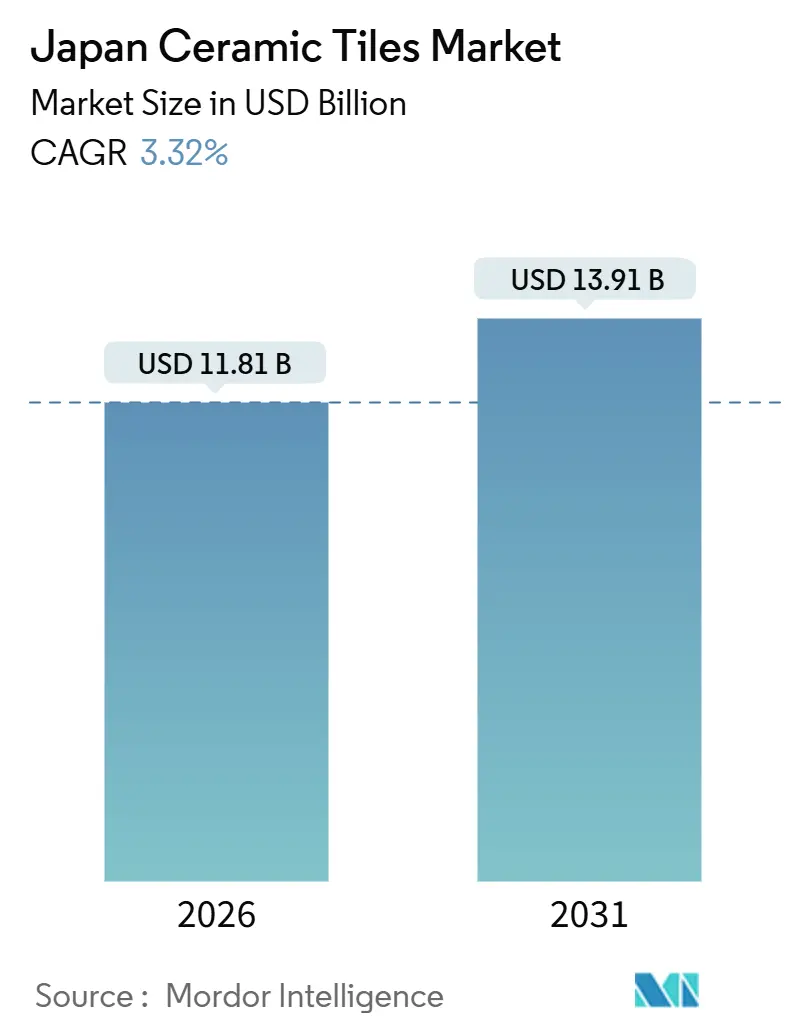

| Market Size (2026) | USD 11.81 Billion |

| Market Size (2031) | USD 13.91 Billion |

| Growth Rate (2026 - 2031) | 3.32% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Japan Ceramic Tiles Market Analysis by Mordor Intelligence

The Japan Ceramic Tiles Market size is estimated at USD 11.81 billion in 2026, and is expected to reach USD 13.91 billion by 2031, at a CAGR of 3.32% during the forecast period (2026-2031).

The market is experiencing steady growth, driven by evolving trends in both residential and commercial sectors. Renovation and replacement demand have become a key focus, as rising housing vacancies and an oversupply of properties shift consumer priorities toward upgrades rather than new construction. Porcelain tiles remain a preferred choice, particularly in high-performance and energy-efficient homes, as Japan’s zero-energy building standards encourage the use of durable, thermally efficient materials. This trend supports the premium segment of the market, maintaining strong demand for high-quality products.

In the commercial sector, luxury and upper upscale properties, especially in major urban centers like Tokyo and Osaka, continue to drive demand for refreshed interior wall and floor applications. The hospitality industry is a significant contributor, with the Japan National Tourism Organization reporting in September 2025 that several high-profile hotels opened in 2025, such as Rosewood Miyakojima, Waldorf Astoria Osaka, Fairmont Tokyo, and JW Marriott Tokyo, and additional luxury properties are planned through 2026 and beyond.[1]Japan National Tourism Organization, “Exciting Property Openings in 2025 and Beyond,” JNTO, Japan.travel.. These openings are boosting premium hospitality demand, reinforcing the need for high-quality ceramic tile specifications. Operationally, the market is shaped by labor shortages and energy cost pressures, which influence installation practices and production strategies. Manufacturers are increasingly adopting larger tile formats, prefabricated modules, and energy-efficient production methods to optimize efficiency and meet evolving market needs. The combined effect of residential upgrades, commercial refurbishments, and expanding luxury hospitality projects ensures a robust and diversified growth outlook for Japan’s ceramic tiles market.

Key Report Takeaways

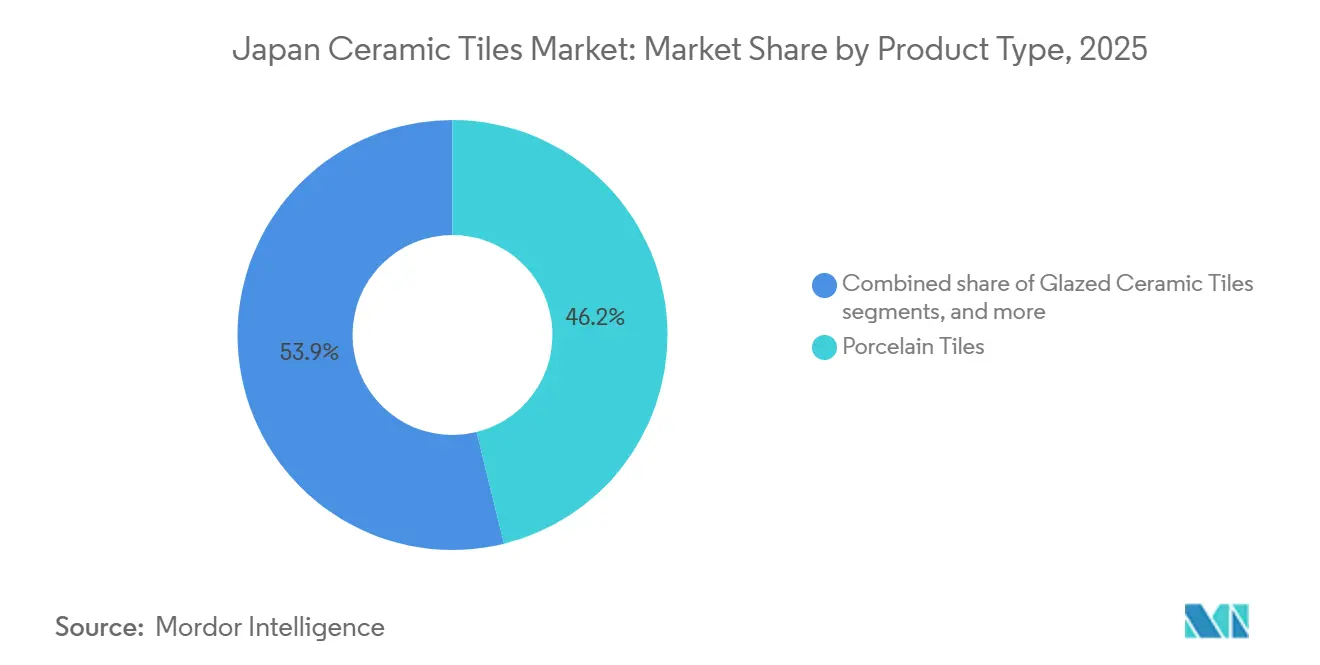

- By product type, porcelain led with 46.15% of the Japan ceramic tiles market share in 2025; mosaic tiles are forecast to expand at a 3.48% CAGR through 2031.

- By application, floor tiles accounted for 52.13% of the Japan ceramic tiles market share in 2025, and wall tiles are projected to grow at a 3.36% CAGR through 2031.

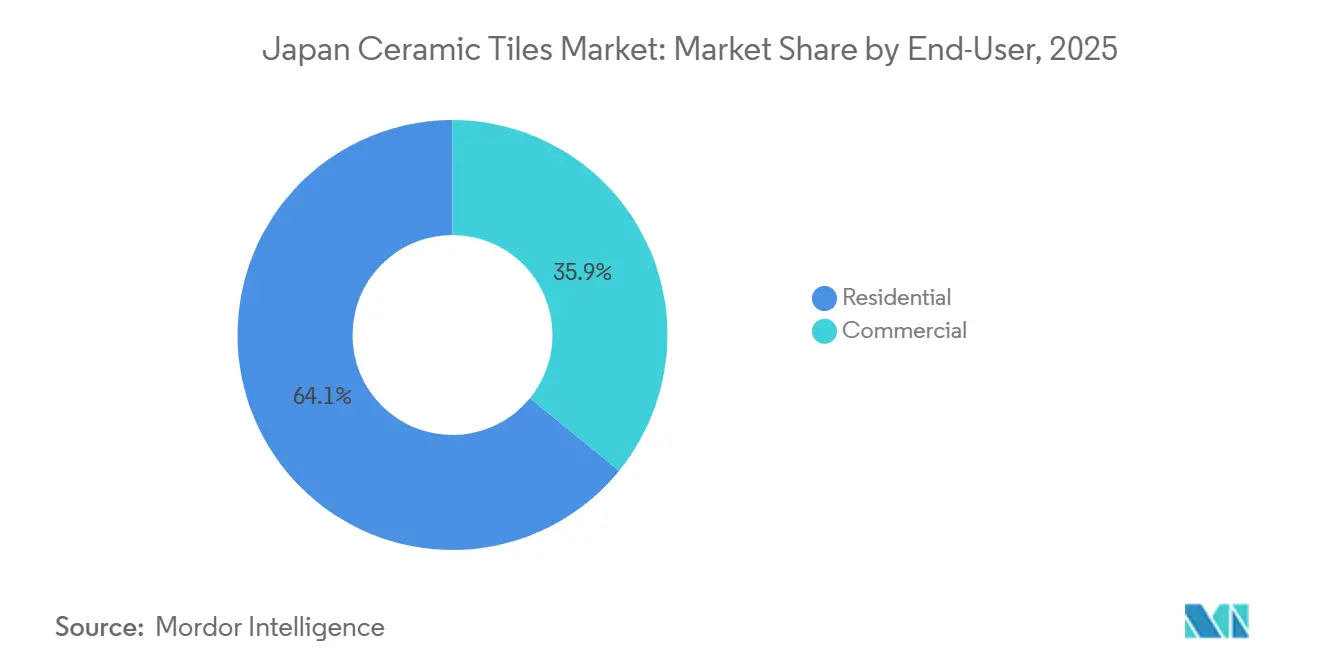

- By end-user, residential held 64.12% of the Japan ceramic tiles market share in 2025, and commercial is projected to register the fastest growth at a 3.69% CAGR through 2031.

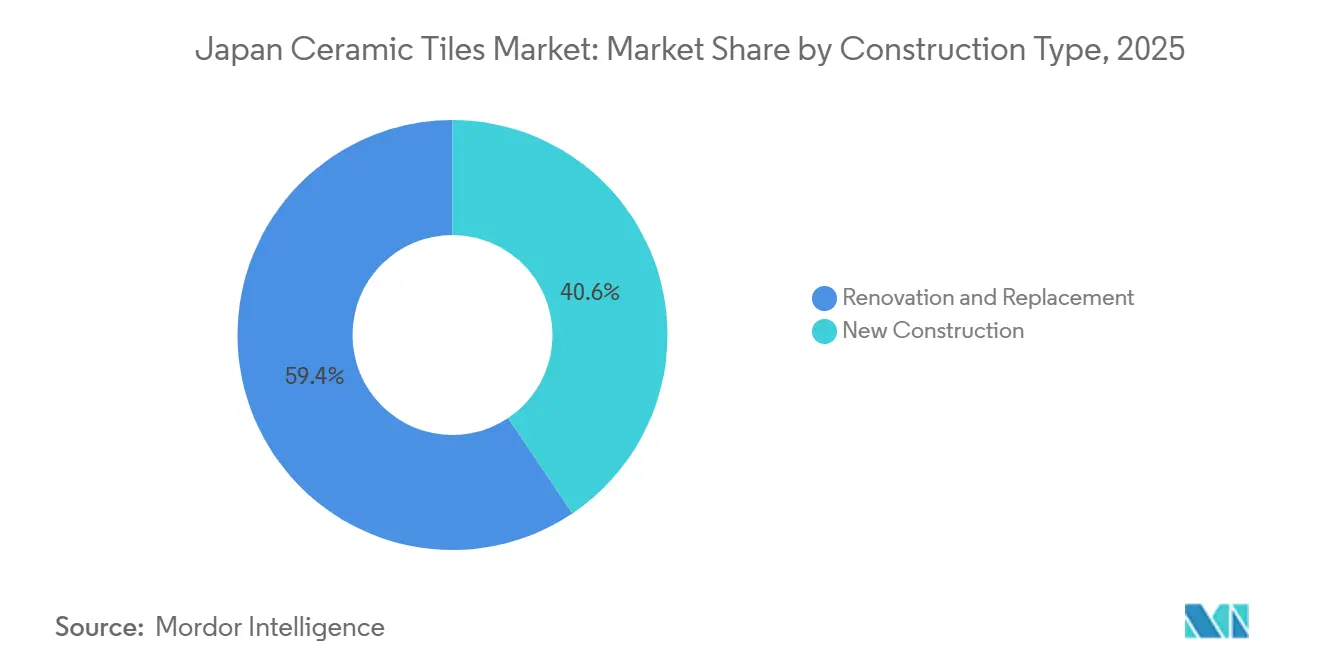

- By construction type, renovation and replacement represented 59.42% of the Japan ceramic tiles market share in 2025; new construction is projected to post a 3.42% CAGR through 2031.

- By distribution channel, specialty tile and stone stores held 37.24% of the Japan ceramic tiles market share in 2025, and online retail is set to grow at a 4.14% CAGR through 2031.

- By geography, Greater Tokyo led with 38.91% of the Japan ceramic tiles market share in 2025; Chūbu recorded the fastest projected regional CAGR at 3.61% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Japan Ceramic Tiles Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging demand for antibacterial and antiviral glazed surfaces post-COVID-19 | +0.5% | Early adoption in Greater Tokyo and Kansai hospitality and healthcare hubs | Medium term (2-4 years) |

| Government subsidies for zero-energy homes are boosting high-spec porcelain adoption | +0.8% | National, strongest in Greater Tokyo and Chūbu, with spillover to Kansai | Long term (≥ 4 years) |

| Aging housing stock is driving renovation-led floor-tile replacement | +1.2% | National, concentrated in Greater Tokyo and provincial cities | Long term (≥ 4 years) |

| Rapid growth of prefabricated modular construction requires lightweight, large-format tiles | +0.4% | Greater Tokyo and Chūbu with spillover to Hokkaido industrial sites | Medium term (2-4 years) |

| Digital printing technology is lowering custom-pattern costs for interior designers | +0.3% | Greater Tokyo and Kansai design districts, expanding to Chūbu | Short term (≤ 2 years) |

| Olympics-legacy tourism investments upgrading hospitality interiors through 2028 | +0.6% | Greater Tokyo and Kansai, with spillover to Fukuoka | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Surging Demand for Antibacterial & Antiviral Glazed Surfaces Post-COVID-19

In the post-COVID-19 landscape, Japan’s healthcare and hospitality sectors increasingly require ceramic surfaces with antibacterial and antiviral properties, driving sustained demand for premium tile products. Leading manufacturers have responded with innovative solutions such as photocatalytic and easy-to-maintain ceramic technologies that meet infection-control standards while remaining durable and practical for high-traffic environments. Major renovations and new openings in Tokyo and Osaka, particularly in luxury hotels and healthcare facilities, are specifying antibacterial wall and floor systems, reinforcing the importance of hygiene-focused applications. The combination of enhanced durability, hygiene compliance, and ease of maintenance ensures that antibacterial and antiviral tiles continue to support value-added specifications in both healthcare and premium hospitality projects.

Government Subsidies for Zero-Energy Homes Boosting High-Spec Porcelain Adoption

Public policy and industry initiatives in Japan are accelerating the adoption of zero‑energy housing standards, which in turn support demand for high‑performance building materials such as premium ceramic and porcelain tiles. Leading housing developers have significantly increased their delivery of zero‑energy homes, reflecting both government incentives and market preference for energy‑efficient construction. For example, in 2023, Sekisui House, one of Japan’s largest homebuilders, supplied tens of thousands of net-zero energy detached homes across the country. In the most recent fiscal year, nearly all of its newly built single-family houses, about 93%, met Japan's net zero energy ZEH standards, reflecting the company’s focus on energy-efficient homes and nationwide adoption of its Green First ZERO model. This sustained focus on energy conservation and decarbonization has extended beyond detached houses to other segments, including rental housing and condominium projects, with high rates of zero-energy adoption across these categories. The broad implementation of these projects underscores the effectiveness of government subsidy programs and regulatory frameworks in driving energy-efficient construction. As builders continue to meet and exceed zero-energy targets, the requirement for thermally efficient and durable materials such as premium porcelain tiles within high-performance building envelopes remains a key trend supporting the Japan ceramic tiles market.[2]Sekisui House, “Sekisui House Value Report 2025,” Sekisui House, sekisuihouse.co.jp.

Aging Housing Stock Driving Renovation-Led Floor-Tile Replacement

Japan’s housing stock exceeds the number of households, and elevated vacancy rates are shifting market activity toward renovations rather than new construction. This trend supports ongoing replacement cycles for ceramic flooring as homeowners and developers focus on upgrading existing properties. Renovation projects increasingly emphasize structural and performance improvements, with floor systems closely integrated with heating and waterproofing solutions. Declining nationwide housing starts further reinforce the shift toward retrofits, ensuring steady demand for floor-tile replacements. Manufacturers are responding with innovative tile formats and installation methods that reduce on-site labor and minimize disruption in occupied homes. Real estate practices and disclosure requirements are raising standards for structural integrity and performance, strengthening the case for high-quality tile renovations. Overall, renovation-led activity provides long-term support for the Japan ceramic tiles market, sustaining replacement volumes and driving the adoption of premium flooring solutions.

Rapid Growth of Prefabricated Modular Construction Requiring Lightweight Large-Format Tiles

Japan’s prefabricated and modular construction sector is expanding rapidly due to labor shortages, cost pressures, and demand for faster, more efficient project delivery. Off-site, factory-based construction supported by digital design, automation, and engineered materials is becoming mainstream across residential, commercial, and institutional projects. This shift toward modular assemblies increases demand for lightweight, large-format tiles that are easier to handle and integrate into prefabricated panels. Manufacturers such as LIXIL have launched new tile lines under their “DESIGNER’S TILE LAB” initiative in 2025, offering textured wall tiles and large-format floor tiles designed for expansive commercial interiors like hotels, offices, and retail spaces[3]PRTimes, “8 New INAX Tiles Launch Announcement,” PRTimes, prtimes.jp.. These products are designed to cover expansive surfaces efficiently while providing rich surface expressions, natural material aesthetics, and modern finishes suitable for commercial interiors such as hotels, offices, and retail spaces. The launch also demonstrates a strategic focus on design-led solutions that address both functional requirements, like durability and ease of installation, and evolving market preferences for high-quality, visually appealing materials.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Declining new-build housing starts in provincial prefectures | -0.7% | The rest of Japan and Chūbu secondary cities, with more limited impact on Greater Tokyo. | Long term (≥ 4 years) |

| Rising natural-gas prices are inflating kiln energy costs | -0.4% | National, acute for domestic producers concentrated in Aichi and Hyogo | Medium term (2-4 years) |

| Tight local labor market limiting tile-setter capacity | -0.5% | National, most severe in Greater Tokyo and Kansai | Medium term (2-4 years) |

| Competition from LVT and SPC rigid-core flooring in price-sensitive segments | -0.6% | National, strongest in provincial residential segments | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Declining New-Build Housing Starts in Provincial Prefectures

The residential activity in Japan has been declining in recent years, particularly in provincial and secondary cities, which limits demand for new-build ceramic tiles outside major metropolitan areas. This trend constrains volumes for commodity wall and floor tiles tied to new detached housing, reducing growth opportunities in these regions. Tile manufacturers with heavy exposure to local new-build channels face margin pressure and are increasingly required to pivot toward higher-value products or explore export markets. Structural demographic shifts suggest that future demand will rely more on renovation and retrofit activity rather than new housing construction. Consequently, suppliers with integrated renovation-focused product ranges and flexible logistics networks are better positioned to address smaller, project-based demand. This ongoing decline in provincial new-build activity acts as a key restraint on overall market expansion for ceramic tiles in Japan.

Rising Natural-Gas Prices Inflating Kiln Energy Costs

Ceramic tile production is highly energy-intensive, making domestic manufacturers particularly sensitive to fluctuations in natural-gas prices and electricity costs. Rising energy and material costs have increased operational expenses and squeezed margins, especially for commodity tile lines. To address these pressures, producers are exploring energy-transition solutions, including hydrogen-assisted kiln combustion, to lower fuel consumption and emissions. These initiatives also aim to mitigate exposure to volatile fuel prices while aligning with Japan’s decarbonization targets. However, until such energy strategies are fully implemented and stabilized, domestic manufacturers face a cost disadvantage compared with imports in certain product categories. As a result, energy-related cost inflation continues to act as a notable restraint on the Japan ceramic tiles market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Porcelain Leads, Mosaics Accelerate

Porcelain held 46.15% of the 2025 volume, anchoring premium and performance-led specifications across residential and commercial projects within the Japan ceramic tiles market. The segment benefits from energy-saving regulations and the adoption of zero-energy homes, which favor low water absorption, thermal mass, and long service life. Large-format offerings, such as LIXIL’s ViCORE floor range, reinforce porcelain’s suitability for high-traffic areas and modular construction workflows. Designers also choose porcelain for exterior envelopes and spaces exposed to temperature fluctuations or heavy wear, adding depth and reliability to the category. Meanwhile, commodity glazed ceramics continue to serve mid-tier budgets and renovation-heavy applications, particularly in bathrooms and kitchens, maintaining a stable base in the market.

Mosaic tiles post the fastest projected growth at a 3.48% CAGR on a smaller base, as digital printing enables bespoke patterns with improved unit economics and faster lead times in the Japan ceramic tiles industry. Specialty producers like Nagoya Mosaic have expanded artisanal sheets and small-format lines, catering to feature walls and compact wet areas. Unglazed mosaics maintain relevance in industrial and logistics settings where slip resistance and oil resistance are critical, outperforming porcelain or glazed options. Decorative and handmade mosaics continue to serve the luxury segment, emphasizing tactile finishes and curated color palettes through designer collaborations. Together, these trends position porcelain at the center of performance-driven applications, while mosaics grow as the preferred design-led solution in high-visibility areas.

By Application: Floor Dominance, Wall Gains in Hospitality

Floor tiles accounted for 52.13% of 2025 application volume and remain the baseline in bathrooms, kitchens, corridors, and public areas where durability and slip resistance are non-negotiable; this level indicates a notable portion of the Japan ceramic tiles market share. Radiant floor heating integrations in residential and elder-care upgrades further reinforce the preference for porcelain and higher-grade ceramics. In commercial interiors, floor systems prioritize maintenance efficiency, with larger modules reducing grout lines and simplifying cleaning cycles. Installation methods that shorten downtime and lower on-site complexity support steady replacement activity in occupied spaces. Persistent labor constraints make streamlined floor-system workflows a practical solution for maintaining throughput in high-demand urban areas across Japan.

Wall tiles are forecast to grow at a 3.36% CAGR, supported by hospitality and retail upgrades that favor large-format porcelain and high-design mosaics for lobbies, feature corridors, and branded backdrops. In kitchens and bathrooms, wall tiles extend hygiene and visual continuity with flooring while creating depth through texture and pattern. Public spaces increasingly specify antibacterial and stain-resistant finishes for high-touch vertical surfaces, emphasizing durability and safety. Roofing remains a niche segment, mainly in traditional and heritage renovations where local regulations or cultural expectations dictate material choice. Overall, floor tiles dominate by area, while wall tiles capture a higher per-square-meter value in premium, design-led projects in the Japan ceramic tiles market.

By End-User: Residential Base, Commercial Outpaces

Residential held 64.12% of 2025 volume, reflecting the structural role of home renovation in Japan, given the stock of aging dwellings and the need for performance upgrades in wet areas and living spaces. A persistent imbalance between housing supply and demand, combined with elevated vacancy levels, encourages homeowners to renovate rather than relocate, sustaining steady replacement activity in bathrooms and kitchens. Performance upgrades in wet areas and living spaces remain a priority, supporting consistent tile consumption. Senior-oriented homes place strong emphasis on slip resistance, safety, and ease of cleaning, which drives preference for higher-grade ceramic surfaces. Demand for faster installation and minimal disruption in occupied homes further supports the adoption of larger formats and overlay installation methods, helping stabilize the market despite softer new housing starts.

Commercial is projected to grow at 3.69% and outpace residential as hospitality, retail, offices, and public facilities execute multi-year upgrade cycles, a trend that is visible in Tokyo and Osaka pipelines. Hospitality projects prioritize antibacterial wall finishes, slip-resistant flooring, and large-format tiles to improve maintenance efficiency and enhance guest experience. Offices and institutional buildings are increasingly adopting prefabricated bathroom units and modular wall systems that integrate tiles during factory production. Industrial facilities and logistics hubs specify unglazed and anti-static tiles for safety and performance, expanding demand beyond traditional commercial interiors. This diverse range of commercial applications supports a balanced specification mix and helps smooth demand cycles in the Japan ceramic tiles market.

By Construction Type: Renovation Reigns Amid New-Build Decline

Renovation and replacement comprised 59.42% of the 2025 volume and represent the primary engine of demand as housing starts soften and as performance upgrades become more widespread in existing dwellings. Homeowners and building managers increasingly invest in improved floor and wall systems that integrate underfloor heating, waterproofing, and antibacterial surfaces. Modular renovation solutions that minimize disruption and allow short installation windows are particularly attractive for occupied properties. These advantages make renovation a stable and predictable demand channel with clear economic benefits. As a result, suppliers that combine high-performance materials with installation efficiency are well positioned to capture repeat renovation volumes.

New construction is projected at a 3.42% CAGR to 2031, supported by policy, energy standards, and select metro pipelines that specify high-performance tiles for floors and façades. Zero-energy home requirements influence material selection, reinforcing the use of porcelain tiles for moisture control, durability, and thermal performance. Logistics facilities, offices, and institutional buildings also specify performance-grade tiles in areas exposed to heavy foot traffic and mechanical stress. Modular construction methods are increasingly bridging renovation and new-build segments through shared large-format components and factory-installed systems. Together, renovation-led volume and targeted new construction activity help keep the Japan ceramic tiles market diversified across project types.

By Distribution Channel: Specialty Stores Hold, Online Surges

Specialty tile and stone stores held 37.24% of the 2025 channel share and provide tactile showrooms, design advisory services, and sampling support that are hard to replicate online. These outlets play a critical role in complex projects and high-end residential renovations, where in-person inspection and curated selection add clear value. Home improvement stores attract mid-market renovation demand, particularly projects driven by budget considerations, convenience, and short installation windows. Direct sales channels remain essential for large commercial and institutional projects, providing technical expertise, on-site coordination, and volume-based pricing. Collectively, offline channels retain strong relevance even as digital engagement expands across the Japan ceramic tiles market.

Online retail is the fastest-growing channel at a projected 4.14% CAGR, helped by visualization tools, web configurators, and direct-to-designer outreach from manufacturers and brands. Advances in digital printing and customization allow customers to preview and order bespoke tile designs without extended sampling cycles. International brands entering Japan with digital-first strategies are increasing product variety and competitive pricing online. These developments are creating a more agile channel structure, with faster sample delivery and richer digital content to support specification decisions. As online and offline roles increasingly overlap, the Japan ceramic tiles market is evolving toward an omnichannel model that serves both complex design-led projects and streamlined renovation needs.

Geography Analysis

Greater Tokyo led with a 38.91% share in 2025 and remains the largest regional demand center for the Japan ceramic tiles market, supported by broad renovation intensity and sustained commercial fit-outs. Luxury hospitality developments and large mixed-use projects frequently specify large-format wall and floor tiles for lobbies and shared public spaces. Office buildings and transportation infrastructure in the region rely on performance-grade tiles in high-traffic areas where durability and maintenance efficiency are critical. Residential renovation demand remains concentrated in bathrooms, kitchens, and living spaces, with a strong preference for durable, easy-to-clean surfaces that align with energy-efficiency and comfort objectives. Although new-build momentum has softened compared with earlier cycles, the breadth of project types across Greater Tokyo continues to sustain consistent tile installation volumes.

The Kansai region benefits from event-driven development and a resilient hospitality pipeline that emphasizes antibacterial wall finishes and slip-resistant flooring systems. Cities such as Osaka and Kyoto are also adopting prefabricated construction methods, including modular bathroom pods, in both new-build and renovation projects. Local manufacturers, particularly in Hyogo and surrounding industrial hubs, are adapting to energy-cost pressures by investing in sustainability-focused production improvements. The region’s construction landscape spans premium hotels, public facilities, and institutional upgrades, supporting demand for a wide range of tile specifications. This diversified project mix helps stabilize ceramic tile demand across the Kansai market.

Chūbu is projected to record the fastest regional growth at 3.61% through 2031, driven by major redevelopment initiatives and expanding logistics and transportation programs. Performance tiles are increasingly specified across concourses, public areas, and heavy-use corridors, contributing to the region’s rising share of national demand. Suppliers with strong connections to Nagoya’s construction ecosystem are well-positioned to support office, retail, and transport projects as they advance from planning to execution. Regional producers and distributors also play a key role in supplying both specification-grade products and artisanal formats favored by designers in larger metro markets. Outside core urban centers, softer housing conditions are shifting demand toward smaller-scale renovations, creating a balanced mix of large projects and steady retrofit activity across the region.

Competitive Landscape

The Japan ceramic tiles market is moderately concentrated, with a small group of leading players accounting for a significant portion of total demand. LIXIL holds a clear leadership position, followed by established manufacturers such as Danto, TOTO, Nagoya Mosaic, and Rinnai Ceramic Tiles. Large-scale players leverage extensive home-center networks and long-standing relationships with major contractors to secure volume-driven distribution. In contrast, design-focused specialists concentrate on architect-led specifications and differentiated, artisanal product portfolios. Sustainability initiatives, including energy-transition efforts in ceramic firing, increasingly serve as a competitive differentiator, particularly in major metropolitan markets.

At the product level, innovation in digital printing and large-format tiles supports competitive performance by aligning with contractor requirements for consistency, speed, and ease of installation. LIXIL’s recent product introductions emphasize large-format floor tiles tailored for modular construction and heavy-traffic environments, strengthening its position across renovation and new-build projects. TOTO continues to advance hygiene-focused ceramic solutions designed to meet infection-control requirements in healthcare and premium hospitality settings. Danto prioritizes collaboration-driven premium collections that appeal to designers seeking rich colors and tactile finishes for feature applications[4]Danto Holdings, “Company Profile,” Danto, danto.co.jp.. Nagoya Mosaic positions itself in luxury residential and boutique commercial interiors with an extensive range of sheeted mosaics and artisanal offerings.

On the supply side, manufacturers are piloting energy-transition technologies in firing processes to improve cost resilience while aligning with long-term decarbonization goals. Digital collaboration workflows between tile producers, contractors, and designers are becoming more sophisticated, helping reduce errors and accelerate approvals on large commercial projects. At the same time, digital-first entrants are increasing competition by targeting online channels and offering direct services to architects and builders. Established players continue to invest in curated catalogs and showroom experiences to preserve specification influence in premium segments. Overall, competition in the Japan ceramic tiles market centers on design innovation, performance differentiation, and efficient logistics execution.

Japan Ceramic Tiles Industry Leaders

LIXIL Corporation (INAX)

Rinnai Ceramic Tiles

Danto Tile Co., Ltd.

TOTO Ltd.

Takara Standard Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Japanese tile maker HiRATA TILE debuted its new brand YUKARI CERAMICS at Cersaie 2025 in Bologna, showcasing “Made in Japan” ceramics that blend traditional techniques and cultural craftsmanship with contemporary architectural appeal, drawing strong interest from international visitors.

- August 2025: TOTO introduced new floor‑standing ceramic sanitary products at ISH 2025, expanding its lineup with close‑coupled and back‑to‑wall versions of its popular RP toilet and bidet that can be upgraded later to WASHLET configurations. These streamlined, minimalist floor standing ceramics are designed to suit a variety of bathroom layouts.

- July 2025: Sangetsu published its “Vivente vol.1” ceramic tile collection and accompanying exteriors catalog, expanding tile offerings for integrated indoor‑outdoor applications across floors and walls. The new series enhances coordinated design options for living spaces and exterior environments in residential and commercial projects.

- March 2025: LIXIL launched eight new tile products under its “DESIGNER’s TILE LAB” lineup, including four textured interior wall tiles and four large-format floor tiles reflecting current non-residential interior trends. Featuring advanced surface finishes such as marble-look mosaics and bold patterned large tiles, these products became available nationwide, providing expanded specification options for commercial and design-focused projects.

Japan Ceramic Tiles Market Report Scope

Ceramic tiles are a mixture of clays and other natural materials, such as sand, quartz, and water. They are primarily used in houses, restaurants, offices, shops, and so on, as bathroom walls and kitchen floor surfaces. They are easy to fit, clean, and maintain, and are available at reasonable prices. This report aims to provide a detailed analysis of the Japanese ceramic tiles market. It focuses on market dynamics, technological trends, and insights into various materials, applications, and process types in Japan. Also, a thorough analysis of the major players and the competitive landscape in the Japanese ceramic tiles market is provided.

The Japan Ceramic Tiles Market Report is Segmented by Product Type (Porcelain, Glazed Ceramic, and More), Application (Floor, Wall, and More), End-User (Residential, Commercial), Construction Type (New Construction, Renovation), Distribution Channel (Specialty Tile & Stone Stores, Home Improvement & DIY Stores, and More), and Geography (Greater Tokyo, Kansai, and More). Market forecasts are provided in value terms.

By Product Type

| Porcelain Tiles |

| Glazed Ceramic Tiles |

| Unglazed Ceramic Tiles |

| Mosaic Tiles |

| Decorative / Patterned / Handmade Tiles |

By Application

| Floor |

| Wall |

| Roofing |

By End-User

| Residential | |

| Commercial | Hospitality (Hotels, Resorts) |

| Retail Spaces | |

| Offices & Institutions | |

| Healthcare | |

| Educational Facilities | |

| Transport Hubs (Airports, Metro, Bus Terminals) | |

| Other Commercial Users |

By Construction Type

| New Construction |

| Renovation & Replacement |

By Distribution Channel

| Specialty Tile & Stone Stores |

| Home Improvement & DIY Stores |

| Online Retail |

| Direct Sales to Contractors |

By Geography

| Greater Tokyo Area (Tokyo, Kanagawa, Saitama, Chiba) |

| Kansai Region (Osaka, Kyoto, Hyogo) |

| Chūbu Region (Aichi, Gifu, Mie) |

| Rest of Japan |

| By Product Type | Porcelain Tiles | |

| Glazed Ceramic Tiles | ||

| Unglazed Ceramic Tiles | ||

| Mosaic Tiles | ||

| Decorative / Patterned / Handmade Tiles | ||

| By Application | Floor | |

| Wall | ||

| Roofing | ||

| By End-User | Residential | |

| Commercial | Hospitality (Hotels, Resorts) | |

| Retail Spaces | ||

| Offices & Institutions | ||

| Healthcare | ||

| Educational Facilities | ||

| Transport Hubs (Airports, Metro, Bus Terminals) | ||

| Other Commercial Users | ||

| By Construction Type | New Construction | |

| Renovation & Replacement | ||

| By Distribution Channel | Specialty Tile & Stone Stores | |

| Home Improvement & DIY Stores | ||

| Online Retail | ||

| Direct Sales to Contractors | ||

| By Geography | Greater Tokyo Area (Tokyo, Kanagawa, Saitama, Chiba) | |

| Kansai Region (Osaka, Kyoto, Hyogo) | ||

| Chūbu Region (Aichi, Gifu, Mie) | ||

| Rest of Japan | ||

Key Questions Answered in the Report

What is the current size and growth outlook for the Japan ceramic tiles market?

The Japan ceramic tiles market reached USD 11.81 billion in 2026 and is projected to reach USD 13.91 billion by 2031 at a 3.32% CAGR, indicating steady expansion supported by renovation and premium specifications.

Which applications are leading demand across Japan?

Floor tiles lead with 52.13% of 2025 application volume due to durability and slip resistance needs, while wall tiles are projected to grow at a 3.36% CAGR on hospitality and design-led upgrades.

Which regions are most important for suppliers to prioritize?

Greater Tokyo leads with a 38.91% share, while Chūbu Region posts the fastest projected regional CAGR at 3.61%, reflecting balanced opportunities across metro renovation and large project pipelines.

What segments of buyers are expected to grow faster through 2031?

Commercial end-users are projected to grow at 3.69% as hospitality, offices, and public facilities upgrade interiors, supported by modular construction and large-format tile adoption.

Which distribution channels are gaining traction with professionals and designers?

Specialty stores still lead at 37.24% of share, but online retail is the fastest-growing channel at a projected 4.14% CAGR, supported by visualization tools and direct-to-designer communication.

Page last updated on: