Glue Laminated Beams Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 4.99 Billion |

| Market Size (2031) | USD 5.91 Billion |

| Growth Rate (2026 - 2031) | 3.42% CAGR |

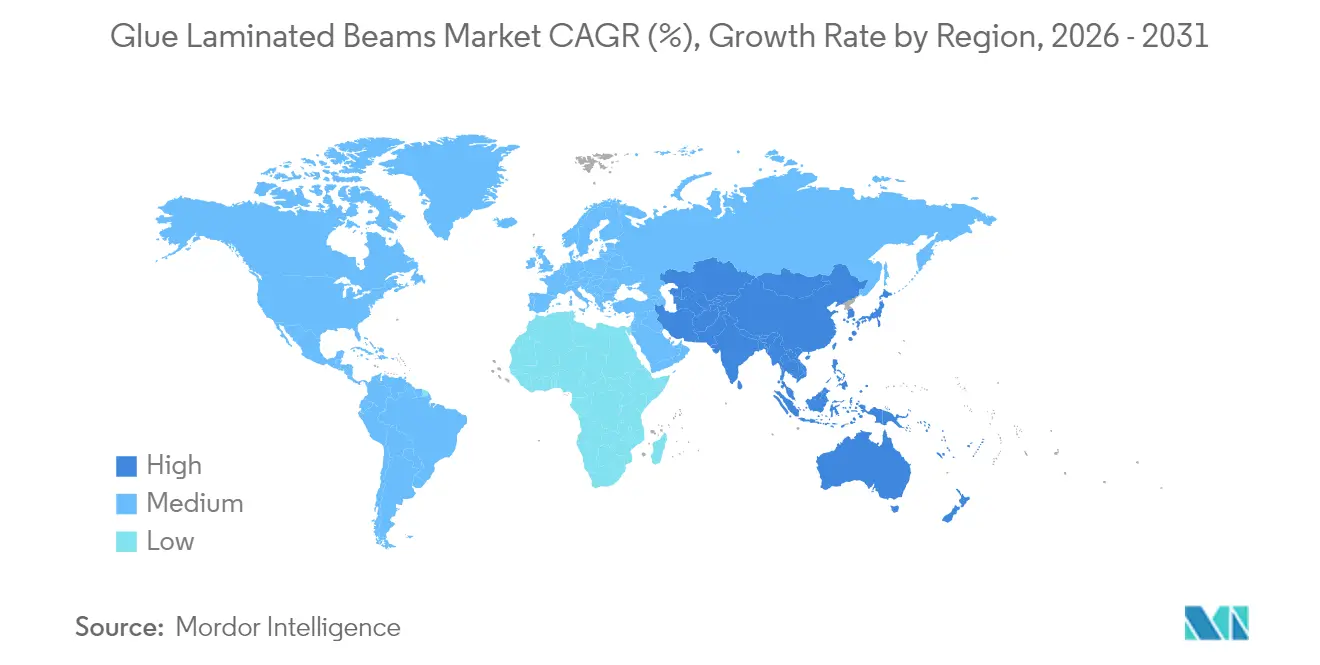

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

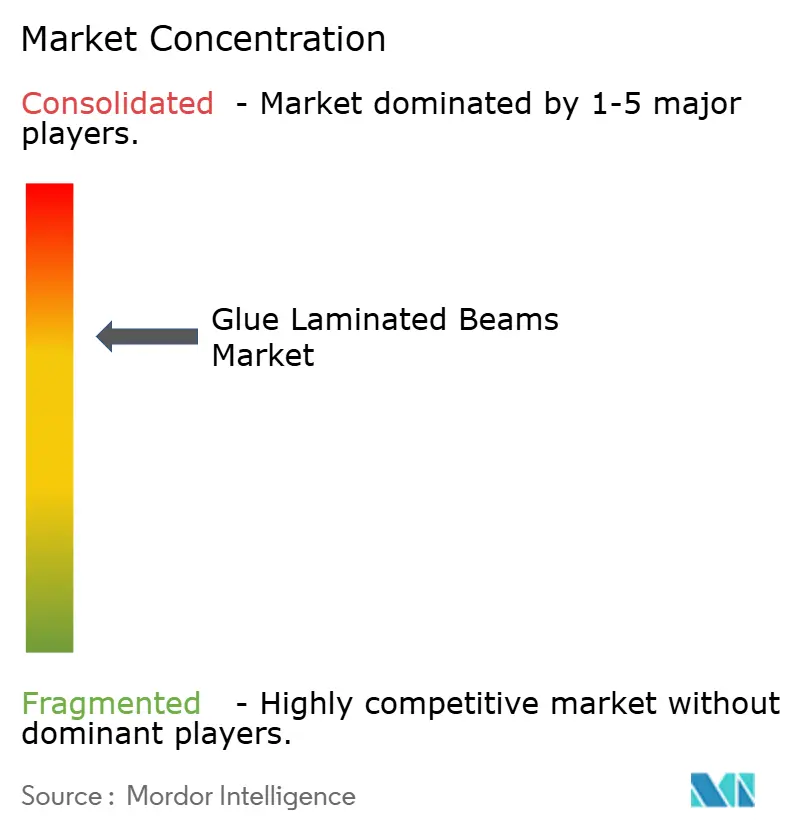

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Glue Laminated Beams Market Analysis by Mordor Intelligence

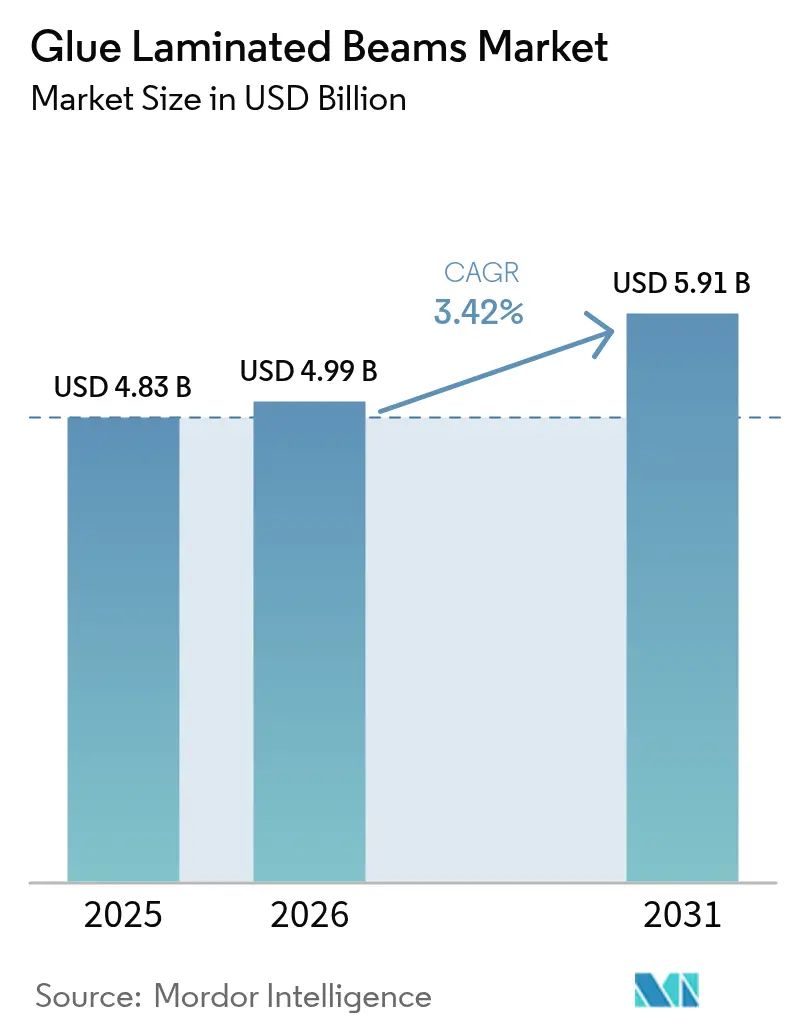

The Glue Laminated Beams market size is expected to grow from USD 4.83 billion in 2025 to USD 4.99 billion in 2026 and is forecast to reach USD 5.91 billion by 2031 at 3.42% CAGR over 2026-2031. Regulatory reforms that recognize mass-timber buildings up to 18–19 stories, incremental advances in bio-based adhesives, and mounting carbon-credit incentives are now the principal levers of growth for the glue laminated beams market. Mid-rise developers are turning to glulam to trim project schedules and lighten embodied-carbon footprints, while do-it-yourself renovations in single-family housing sustain baseline demand. Architectural preferences for curved members, the use of Building Information Modeling for design accuracy, and capital inflows from ESG-linked financing further reinforce adoption. Even so, volatile softwood pricing and region-specific durability concerns temper profit margins and expansion pace, signaling a maturing phase rather than a breakout cycle for the glue laminated beams market.

Key Report Takeaways

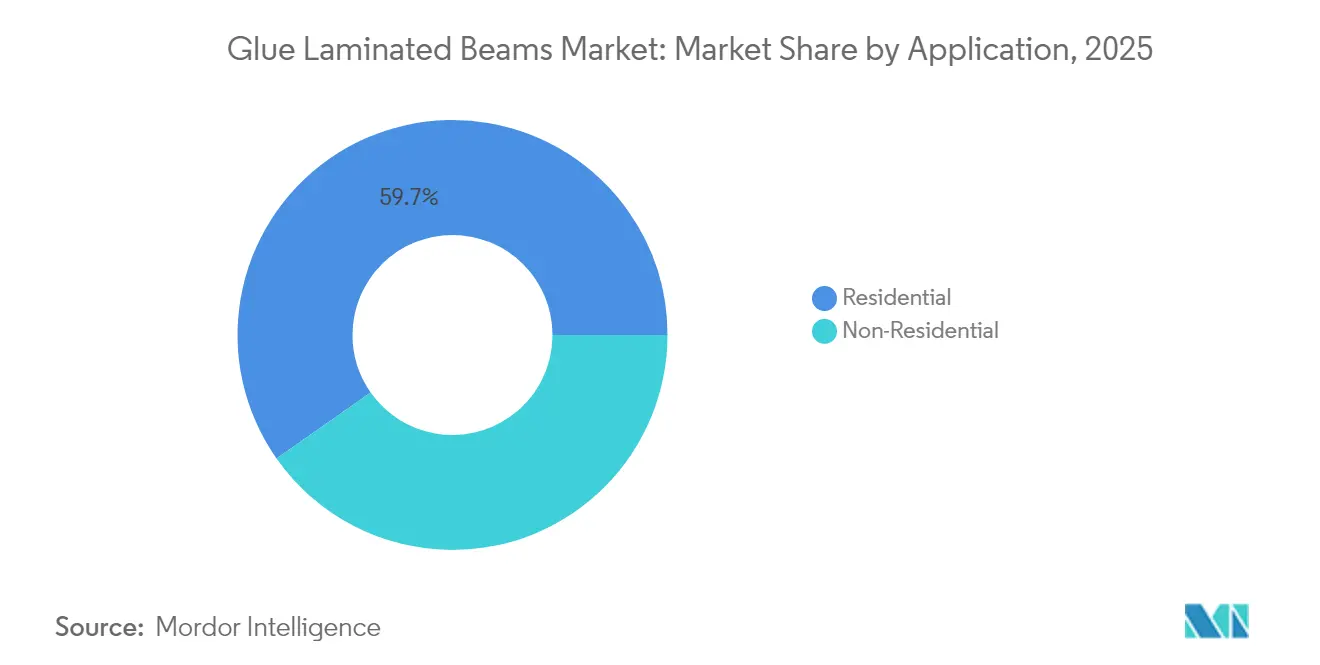

- By application, residential construction held 59.74% of the glue laminated beams market share in 2025 and is on course to register a 5.02% CAGR through 2031.

- By product type, straight beams controlled 45.31% revenue in 2025, whereas curved and arched beams are forecast to expand at a 4.28% CAGR to 2031.

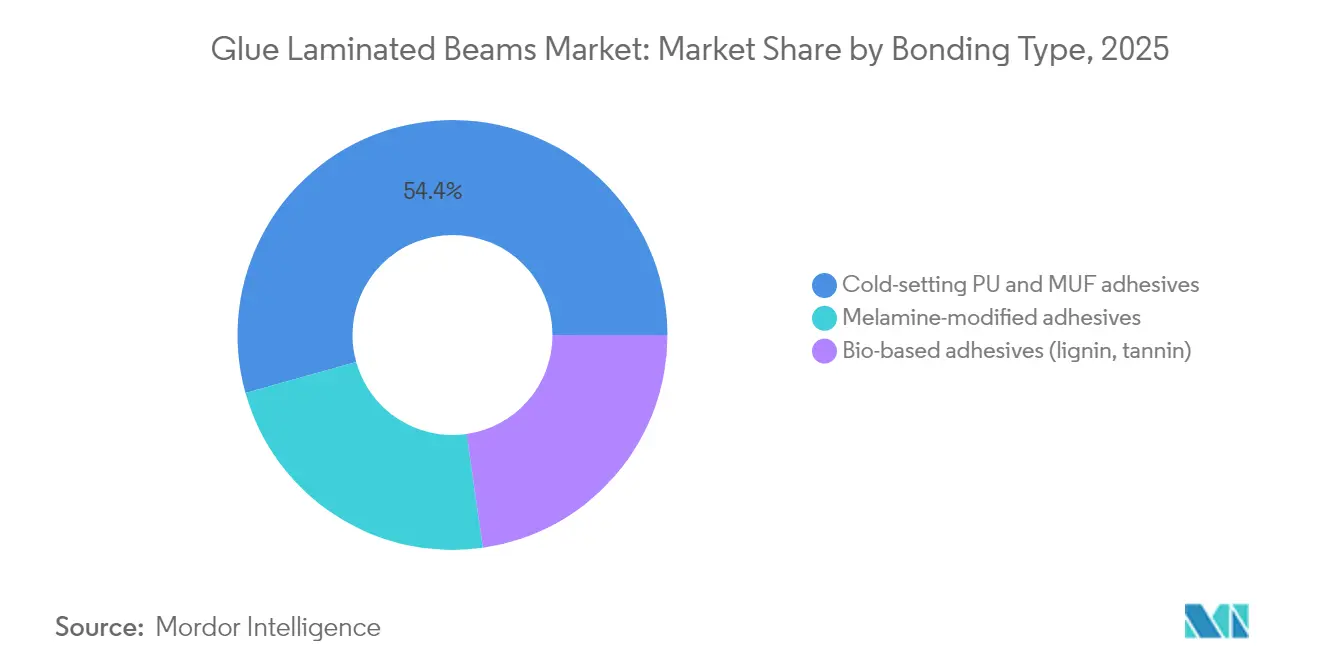

- By bonding chemistry, cold-setting polyurethane and MUF systems accounted for 54.35% of the glue laminated beams market size in 2025, while bio-based adhesives are projected to grow at 4.88% CAGR.

- By geography, Asia-Pacific captured 40.72% revenue in 2025; the region is projected to lead growth at a 4.63% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Glue Laminated Beams Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising multi-storey timber construction | +1.20% | Global, with early adoption in North America & EU | Medium term (2-4 years) |

| Carbon-credit premiums for engineered wood in ESG-linked financing | +0.80% | Global, concentrated in developed markets | Long term (≥ 4 years) |

| DIY renovation boom in single-family housing | +0.90% | North America & EU core, spill-over to APAC | Short term (≤ 2 years) |

| Building code shifts permitting exposed mass-timber elements | +1.10% | North America & EU, gradual APAC adoption | Medium term (2-4 years) |

| Increasing demand from the residential sector | +0.70% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Multi-Storey Timber Construction

Revisions to the 2021 International Building Code allowing glulam structures up to 18 stories have unlocked high-rise potential, prompting states such as Michigan to adopt the standards in April 2025. Developers benefit from lead-time reductions of roughly 20–30%, attractive installation speed, and lighter foundations that lower urban site costs. Showpiece projects like Milwaukee’s 32-story Edison tower have moved mass timber from novelty to commercial mainstream, demonstrating structural integrity as well as occupant appeal. Equipment suppliers now offer automated lamination lines sized for panels exceeding 16 meters, aligning factory capability with taller-building demand. Collectively these shifts raise design confidence and widen the addressable base for the glue laminated beams market.

Carbon-Credit Premiums for Engineered Wood in ESG-Linked Financing

Carbon accounting has become a pricing lever, allowing mass-timber projects to cut construction emissions by nearly 40% against concrete baselines[1]Stora Enso Oyj, “Carbon Benefits in Wood-Based Construction,” storaenso.com . This reduction secures lower coupon rates in sustainability-linked loans and improves eligibility for European taxonomy-aligned green bonds. Material suppliers publishing cradle-to-gate Environmental Product Declarations reinforce transparency, while insurers price builders-risk policies more favorably when glulam replaces higher-fire-load assemblies. These financial inducements are set to compound as mandatory disclosure regimes spread, underpinning longer-run demand for the glue laminated beams market.

DIY Renovation Boom in Single-Family Housing

Remote-work patterns lifted home-improvement spending, pushing softwood consumption for U.S. residential projects to 19 billion board feet in 2024. Exposed glulam beams fulfill a dual role—load bearing and aesthetic signature—so homeowners willingly absorb premium unit costs. Professional remodelers have also shifted toward engineered wood to shorten build cycles and reduce call-backs caused by dimensional lumber shrinkage. This consumer-led resilience offers a counter-cyclical cushion, sustaining the glue laminated beams market during periods when commercial starts soften.

Building Code Shifts Permitting Exposed Mass-Timber Elements

British Columbia’s 2024 code overhaul allows unencapsulated mass timber in 6- to 8-story occupancies, trimming façade costs and enhancing architectural expression. Parallel Japanese guidelines extend service life expectations for wooden buildings from 24 to over 50 years, soothing durability concerns in seismic zones. Fire-testing evidence shows predictable char layers that maintain load-bearing performance and meet two-hour ratings without gypsum protection. As a result, architects can specify glulam for visible atria, transit hubs, and sports venues, broadening design possibilities across the glue laminated beams market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile sawn-timber prices compressing margins | -0.60% | Global, acute in North America | Short term (≤ 2 years) |

| Moisture absorption & biological decay concerns in humid climates | -0.40% | APAC humid regions, Southeast US | Long term (≥ 4 years) |

| Limited certified installers outside mature mass-timber clusters | -0.30% | Global, concentrated in emerging markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Sawn-Timber Prices Compressing Margins

Softwood lumber prices rebounded in early 2025, pinching spreads between input costs and contract bids for glulam producers. The European Deforestation Regulation complicates import flows, particularly for Asian mills reluctant to share geolocation data, thereby sharpening supply tension. Because many construction contracts lock material rates months ahead, manufacturers shoulder most cost swings, which can delay capital spending on new presses and restrain near-term growth within the glue laminated beams market.

Moisture Absorption & Biological Decay Concerns in Humid Climates

Field studies in Sweden recorded surface cracking along glue lines when beams endured repeated wet-dry cycles, a phenomenon echoed by Australian research for tropical settings[2]RISE Research Institutes of Sweden, “Outdoor Glulam Performance Study,” ri.se . High humidity fosters fungal activity, eroding shear strength unless preservative treatments and detailing standards are rigorous[3]APA – The Engineered Wood Association, “Moisture Management in Mass Timber,” apawood.org . These climatic risks necessitate region-specific protective coatings that add cost and complexity, slowing uptake of the glue laminated beams market in equatorial regions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Residential Dominance Drives Market Evolution

Residential construction captured 59.74% of the glue laminated beams market in 2025, propelled by single-family preferences for vaulted ceilings and open spans that glulam readily supports. The segment is projected to grow at 5.02% CAGR, meaning its portion of the glue laminated beams market size will widen further against non-residential uses by 2031. Renovation activity, backed by home-equity financing and a flourishing DIY culture, is steering demand toward exposed beams that marry structural capacity with visual warmth.

Commercial, industrial, and institutional projects contribute the remaining 40.26%, yet their adoption curves differ. Mid-rise offices are emerging as testbeds following code reforms, whereas warehouses leverage glulam’s span-to-weight advantage to cut foundation loads. Universities showcase sustainability commitments through timber labs and dormitories, heightening public visibility and normalizing mass-timber choices. As more general contractors embed glulam connection libraries into BIM libraries, design-to-fabrication cycles shorten, reinforcing the glue laminated beams market across all use cases.

By Product Type: Architectural Innovation Reshapes Demand Patterns

Straight beams accounted for 45.31% of 2025 revenue, underpinned by economy of scale and simplistic detailing that meet builders’ cost and schedule targets. However, curved and arched variants, expanding at 4.28% CAGR, illustrate an architectural turn toward biophilic forms and signature atria. Large-format CNC bending and radio-frequency curing now enable complex geometries at throughput rates on par with straight members, reducing premium mark-ups and broadening acceptance.

Truss elements and posts serve niche yet important roles in long-span roofs and multi-storey grids enabled by new codes. Manufacturers deploying flexible lamination presses can switch between standard profiles and bespoke arches without lengthy changeovers, helping engineers meet structural and aesthetic criteria simultaneously. This responsive capacity strengthens supplier margins while attracting architects eager to differentiate, deepening penetration of the glue laminated beams market.

By Bonding Type: Bio-Based Innovation Challenges Traditional Chemistry

Conventional cold-setting polyurethane and MUF adhesives held 54.35% share in 2025, anchored by decades of reliability data and global code listings. Even so, bio-based systems integrating lignin and cellulose derivatives are scaling at 4.88% CAGR, propelled by corporate decarbonization targets and early procurement policies. Henkel’s LOCTITE HB S ECO line claims 63% bio-content yet preserves bond strength and water resistance, offering emission cuts above 60% relative to legacy formulas.

Certification pathways still favor incumbent chemistries, so hybrid melamine-modified blends act as stepping-stones, incrementally reducing formaldehyde release while fitting existing press cycles. Research published in Nature Communications Materials documents cellulose-only adhesive prototypes that rival urea-formaldehyde in shear performance, foreshadowing a structural pivot once lifecycle data matures. As clients weigh full-building carbon scores, adhesive selection becomes a frontline differentiator, reinforcing momentum within the glue laminated beams market.

Geography Analysis

Asia-Pacific leads with 40.72% revenue in 2025 and a 4.63% regional CAGR projected to 2031, making it the most dynamic locus of the glue laminated beams market. China’s expanding metro rings rely on fast-tracked timber stations, though the European Union Deforestation Regulation may reroute supply chains and raise compliance costs for exporters. Japan’s new longevity standards mitigate seismic durability skepticism and foster public-sector procurement of multi-storey mass-timber schools and hospitals. Emerging economies in Southeast Asia pilot glulam pedestrian bridges and resort villas, hinting at sizeable latent demand once installer networks mature.

North America is a significant arena, supported by more than 2,100 documented mass-timber projects and a federal R&D pipeline that subsidizes fire-testing and design-guide publication. State-level tax credits in Oregon and Wisconsin amplify private adoption, while Mexican prefab ventures explore cross-border partnerships for cost-effective laminated members. Volatile lumber pricing remains the region’s chief headwind, yet carbon-focused investors continue to allocate capital to timber developments, stabilizing order books for glulam mills.

Europe maintains a highly integrated manufacturing ecosystem spanning Germany, Austria, and Scandinavia. Mayr-Melnhof Holz’s cross-laminated timber plant, with 140,000 m³ annual capacity, exemplifies industrial scaling aligned to regional demand for climate-neutral buildings. Public procurement directives in France stipulate minimum bio-sourced content in new civic projects, entrenching glulam in cultural centers and transport hubs. Brexit-induced customs friction adds administrative overhead for United Kingdom imports, but domestic sawmills are upgrading lamination lines to localize supply, thereby anchoring the glue laminated beams market inside national borders.

Competitive Landscape

The glue laminated beams market is moderately consolidated. Integrated forestry majors such as Stora Enso and Boise Cascade combine raw-material ownership with downstream processing, yielding cost visibility and assured fibre supply. Mid-sized European specialists like HASSLACHER and Mayr-Melnhof Holz differentiate through architectural innovation—spanning bridge systems, long-curved girders, and hybrid wood-concrete panels.

Technology investment is an emerging separator. Plants equipped with robotic feed lines and inline X-ray scanning maintain tighter tolerances, reducing waste and enabling just-in-time dispatch to urban infill sites where lay-down areas are scarce. Manufacturers championing bio-adhesive testing leverage green-premium pricing and early-adopter brand equity.

Strategic consolidation accelerates capability building. Star Equity Holdings’ 2024 acquisition of Timber Technologies broadened geographic reach into the U.S. Midwest, while Sveaskog’s 2025 divestiture of its Setra stake to Mellanskog reconfigures Sweden’s production landscape, potentially reshaping regional price dynamics. White-space contenders from steel fabrication and concrete formwork sectors are entering with hybrid offerings, intensifying rivalry yet spreading installer expertise that should ultimately expand the glue laminated beams market.

Glue Laminated Beams Industry Leaders

Binderholz GmbH

Boise Cascade

Canadian Forest Products Ltd.

Mayr-Melnhof Holz Holding AG

Stora Enso

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Sveaskog has completed the sale of its 50% stake in Setra Group to Mellanskog, impacting one of Sweden's leading wood industry companies, which specializes in producing glulam and other wood products. This transaction is expected to impact Sweden's glue-laminated beams market by influencing production and competition.

- May 2024: Star Equity Holdings has completed the acquisition of Timber Technologies, a manufacturer of glue-laminated timber products, expanding its presence in the Midwest and Northwest regions. The strategic move aims to solidify the company's position in the glue-laminated beams market by expanding its offerings and reach.

Global Glue Laminated Beams Market Report Scope

The Glue Laminated Beams market report include:

| Residential | |

| Non-Residential | Commercial |

| Industrial and Institutional | |

| Others |

| Straight Beams |

| Curved/Arched Beams |

| Trusses and Truss Elements |

| Columns and Posts |

| Cold-setting Polyurethane ( PU) and Melamine-urea-formaldehyde (MUF) adhesives |

| Melamine-modified adhesives |

| Bio-based adhesives (lignin, tannin) |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Application | Residential | |

| Non-Residential | Commercial | |

| Industrial and Institutional | ||

| Others | ||

| By Product Type | Straight Beams | |

| Curved/Arched Beams | ||

| Trusses and Truss Elements | ||

| Columns and Posts | ||

| By Bonding Type | Cold-setting Polyurethane ( PU) and Melamine-urea-formaldehyde (MUF) adhesives | |

| Melamine-modified adhesives | ||

| Bio-based adhesives (lignin, tannin) | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current valuation of the glue laminated beams market?

The glue laminated beams market is valued at USD 4.99 billion in 2026 and is projected to hit USD 5.91 billion by 2031.

Which region leads the glue laminated beams market?

Asia-Pacific holds the largest regional share at 40.72% in 2025 and is forecast to grow the fastest at a 4.63% CAGR through 2031.

Why are bio-based adhesives gaining traction?

Bio-based systems deliver up to 60% CO₂ emission reductions while approaching the strength of traditional chemistries, aligning with corporate net-zero targets.

How do building-code changes influence market growth?

Updated codes in North America, Europe, and parts of Asia permit mass-timber buildings up to 18–19 stories, removing prior height and encapsulation barriers and widening the glue laminated beams market.

What limits glulam adoption in humid regions?

High moisture levels accelerate surface cracking and biological decay, necessitating costly protective measures that slow deployment in tropical zones.

Page last updated on: