Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

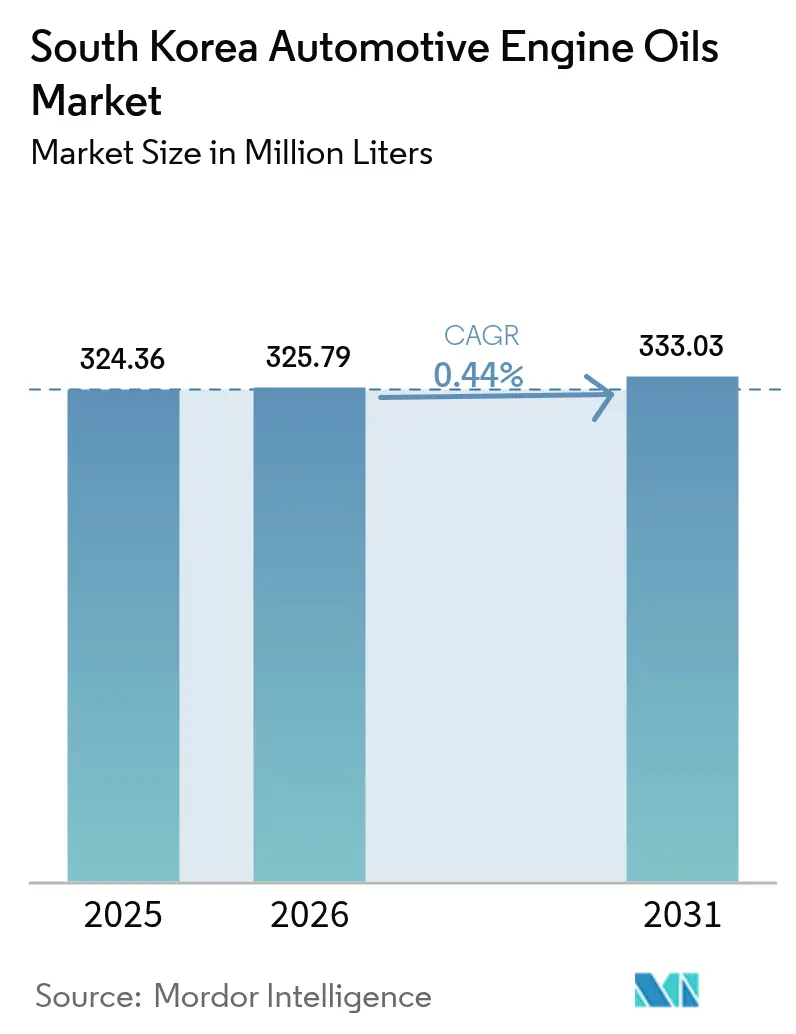

| Base Year Market Size (2025) | 324.36 Million Liters |

| Market Volume (2026) | 325.79 Million Liters |

| Market Volume (2031) | 333.03 Million Liters |

| Growth Rate (2026 - 2031) | 0.44% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Korea Automotive Engine Oils Market Analysis by Mordor Intelligence

The South Korea Automotive Engine Oils Market size is expected to grow from 324.36 Million Liters in 2025 to 325.79 Million Liters in 2026 and is forecast to reach 333.03 Million Liters by 2031 at 0.44% CAGR over 2026-2031. Market size expansion continues even as electrification policies erode internal-combustion demand, because an aging vehicle parc, mandatory inspections, and the proliferation of premium cars sustain service-fill volumes. Synthetic migration drives margin growth, while refiners leverage the world’s largest Group III base-oil capacity to defend profitability. Supply resilience, export competitiveness, and ongoing bio-base investments position the South Korea automotive engine oils market for steady, value-oriented evolution.

Key Report Takeaways

- By product type, passenger car motor oil led with a 62.85% volume share in 2025. However, motorcycle engine oil is projected to advance at a 0.63% CAGR through 2031.

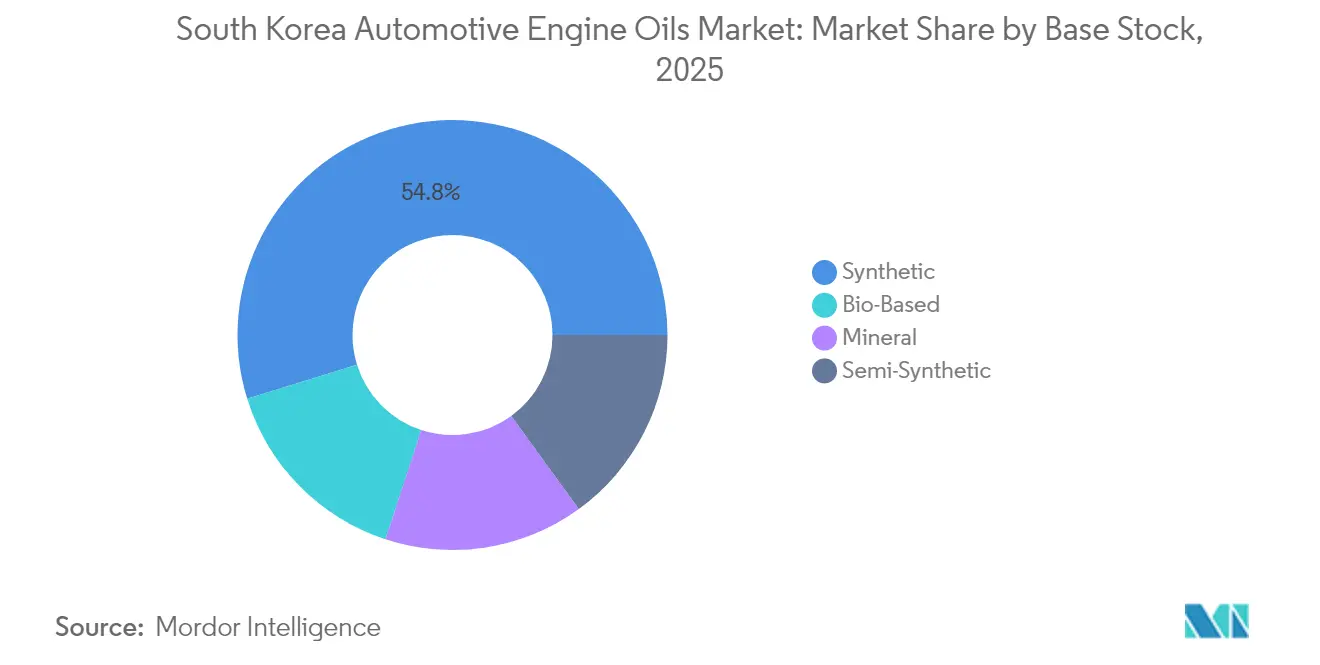

- By base stock, synthetics commanded 54.80% of the South Korea automotive engine oils market share in 2025, while bio-based oils are projected to expand at a 0.50% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

South Korea Automotive Engine Oils Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing vehicle parc and rising average vehicle age | +0.20% | National, concentrated in Seoul-Gyeonggi metropolitan area | Long term (≥ 4 years) |

| Rapid shift toward synthetic and low-viscosity oils | +0.10% | National, with premium vehicle concentration in major cities | Medium term (2-4 years) |

| Expansion of premium-segment passenger cars | +0.10% | National, with luxury vehicle clustering in affluent districts | Medium term (2-4 years) |

| Mandatory annual inspection regime boosting service-fill demand | +0.10% | National, uniform regulatory enforcement | Long term (≥ 4 years) |

| Last-mile 2-wheeler delivery boom raising oil-change frequency | +0.10% | Urban centers, particularly Seoul, Busan, and major metropolitan areas | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Vehicle Parc and Rising Average Vehicle Age

Korea's vehicle fleet dynamics generate sustained aftermarket demand despite headwinds from electrification. The nation's total registered vehicles continue to expand while the average fleet age increases, generating higher maintenance frequency and oil consumption per vehicle. This demographic shift particularly benefits service-fill channels as older vehicles require more frequent oil changes and experience higher consumption rates. LPG commercial vehicles exemplify this trend, with registrations surging 77.3% in Q1 2024 to dominate the light commercial segment at 25,271 units, approaching 2014 peak levels with projected 2024 volumes of 166,000 units. The aging parc effect compounds as vehicles transition beyond warranty periods, shifting from factory-fill to aftermarket channels where Korean refiners capture higher margins through branded retail networks.

Rapid Shift Toward Synthetic and Low-Viscosity Oils

Premium gasoline demand tripled between 2015 and 2021, signaling consumer willingness to pay for performance enhancements extending to lubricants[1]Korea Energy Economics Institute, “Premium Fuel Demand Trends,” keei.re.kr. Hybrid registrations rose 27.6% in 2024 to 394,613, requiring 0W-16 and 0W-20 oils with shorter drain intervals. All four major refiners introduced full API SQ/ILSAC GF-7 lines in 2025, expanding synthetic penetration and lifting per-liter margins.

Expansion of Premium-Segment Passenger Cars

Korea's automotive market premiumization is directly correlated with the adoption of synthetic oil, as luxury vehicles require advanced formulations. Imported hybrid vehicles captured 75.8% of the total import share in January 2025, with three out of every four imported cars featuring hybrid powertrains that require low-viscosity synthetic oils. This shift benefits Korean refiners, who have invested heavily in Group III base oil capacity. SK Enmove operates the world's largest API Group III production facility, and GS Caltex's Yeosu plant produces 1.3 million tons annually of Group II and Group III base stocks. Premium vehicle owners demonstrate higher service frequency and brand loyalty, creating stable revenue streams for Korean lubricant manufacturers who leverage OEM approvals and dealer channel partnerships to capture factory-fill and first-service business.

Mandatory Annual Inspection Regime

Korea's comprehensive vehicle inspection system generates consistent aftermarket demand through mandatory maintenance requirements. However, recent regulatory changes present mixed implications, as light truck inspection intervals have been relaxed from 1 year to 2 years, affecting 2.96 million vehicles and potentially reducing inspection-driven oil changes[2]Korea Petroleum Association, “Inspection Interval Revisions,” petroleum.or.kr. This rationalization contrasts with the heavy vehicle segments, which maintain frequent inspection schedules, thereby preserving commercial oil demand. The effectiveness of the inspection system in driving service-fill consumption depends on enforcement rigor and consumer compliance. Korean refiners are adapting through O2O platforms, which cover 22 initial locations with expansion planned to 500 AutoOasis service shops, targeting the KRW 1.5 trillion online automotive consumables market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Electrification-driven ICE share erosion | -0.20% | National, with EV concentration in Seoul and major metropolitan areas | Long term (≥ 4 years) |

| Longer oil-drain intervals via advanced formulations | -0.10% | National, affecting all vehicle segments | Medium term (2-4 years) |

| Softening motorcycle sales | -0.05% | National, with urban market concentration in delivery service hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Electrification-Driven ICE Share Erosion

Korea's electrification drive is reducing conventional engine oil demand as EV penetration rises toward 4.5 million zero-emission vehicles by 2030. In 2024, gasoline vehicles dropped to 47.8% of new registrations, while EVs and hybrids reached 14.6% and 24.1%, respectively, making up 38.7% of sales. Refiners are adapting, with S-Oil developing EV-specific lubricants and HD Hyundai Oilbank investing in bio-based feedstocks. The Ulsan industrial complex's plan to electrify 30,000 motorcycles, including 19,000 at HD Hyundai, underscores its sustainability efforts, resulting in an annual savings of KRW 120,000 per unit in engine oil costs.

Longer Oil-Drain Intervals via Advanced Formulations

Advanced synthetic formulations enable extended drain intervals, compressing volume demand despite premium pricing benefits. Modern API SQ/ILSAC GF-7 oils introduced by Korean refiners in 2025 offer superior oxidation resistance and thermal stability, allowing OEMs to extend service intervals while maintaining warranty coverage. This technical evolution creates a volume-value trade-off where Korean manufacturers capture higher per-liter margins through synthetic premiums but face reduced consumption frequency. The trend accelerates as Korean automakers, such as Hyundai, specify severe driving condition intervals of 5,000-7,500 km for Smartstream engines, while warning against mineral/semi-synthetic oils, effectively mandating synthetic formulations that last longer but cost more. This dynamic favors refiners with strong synthetic capabilities while pressuring those dependent on conventional mineral oil volumes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Passenger Car Oils Dominate While Motorcycle Oils Accelerate

Passenger car motor oils maintained a 62.85% share in 2025, primarily due to a passenger-vehicle-centric transportation mix and the rapid adoption of hybrid vehicles. The South Korea automotive engine oils market size is forecast to expand due to shorter drain intervals on hybrids. Motorcycle engine oil, though smaller, posts the fastest 0.63% CAGR as e-commerce fuels last-mile deliveries. Refiners responded with 16 new XTEER gasoline variants and six dedicated EV-hybrid oils launched in 2025, locking in synthetic migration gains.

Heavy-duty motor oil faces headwinds from alternative fuels and fleet electrification. LPG light trucks already claimed 77.3% of Q1 2024 segment registrations, curbing diesel-HDMO volumes. The South Korea automotive engine oils market hierarchy will likely hold but shift toward high-value synthetics, with MCO providing incremental growth until large-scale two-wheel electrification occurs.

By Base Stock: Synthetic Leadership Underpins Value Creation

Synthetic oils held 54.80% of 2025 volume, driven by Korea’s unmatched Group III export capability. Mineral oils retain price-sensitive segments yet suffer from crude volatility and substitution. Semi-synthetics strike a balance between cost and performance, while bio-based formulations are the most dynamic, with a 0.50% CAGR, as refiners commission biodiesel and co-processing units.

Exports climbed 15% year-on-year to 348,303 tons in February 2025, confirming Korea’s international competitiveness. Domestic bio-base adoption will advance as sustainability mandates tighten and refiners scale circular-economy feedstocks.

Geography Analysis

Regional demand is concentrated in the Seoul–Gyeonggi corridor, where premium car density and service frequency peak. Nationwide inspection rules, Euro VI emissions compliance since 2015, and aging fleets keep service-fill volumes stable. Korea’s Q1 2025 base-oil exports reached near 1.2 million tons valued at USD 1.3 billion, underscoring the global relevance of the South Korea automotive engine oils market.

The government aims to have 4.5 million zero-emission vehicles by 2030. While this erodes ICE volumes, refiners pivot toward EV fluids, immersion-cooling products, and bio-blends. Integrated value chains linking crude intake, base-oil production, and premium blending sustain margins despite headwinds in consumption.

Competitive Landscape

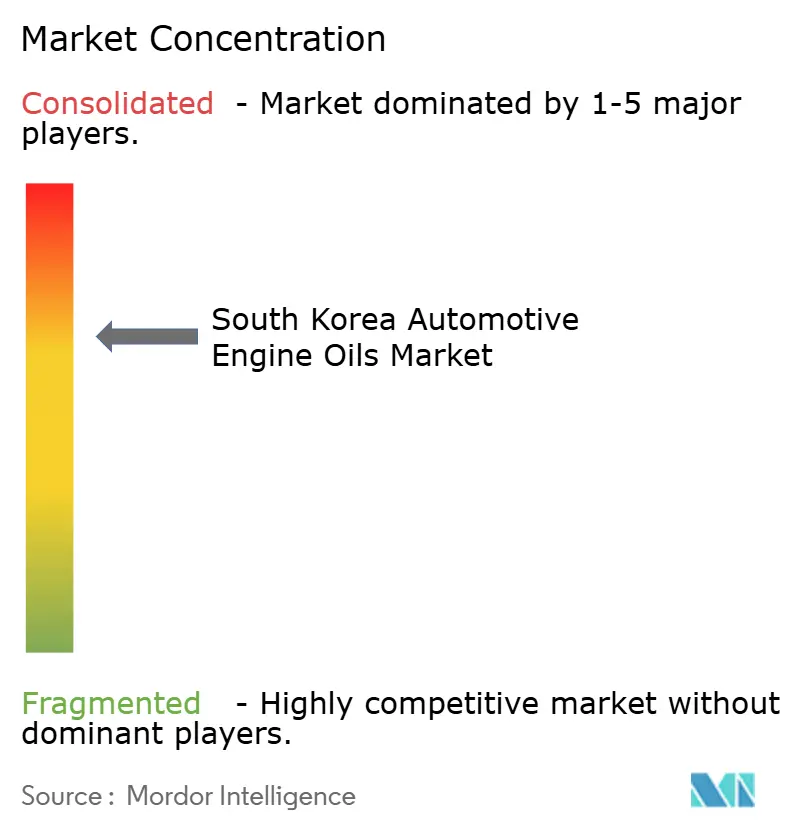

The South Korea Automotive Engine Oils Market is consolidated. Four integrated refiners dominate, booking KRW 1.9 trillion in lubricant operating profit during 2024 with margins ranging from 12.5% to 25.4%. SK Innovation led with KRW 686.7 billion, followed by S-Oil at KRW 571.2 billion, GS Caltex at KRW 474 billion, and HD Hyundai Oilbank at KRW 168.1 billion. All launched API SQ/ILSAC GF-7 synthetic portfolios in 2025. Strategic consolidation accelerated. HD Hyundai Oilbank acquired the remaining 50% of HD Hyundai Cosmo for USD 104.3 million, unlocking specialty production flexibility. Refiners are also diversifying into immersion-cooling fluids, bio-feedstocks, and EV-thermal products, widening competitive moats as the South Korea automotive engine oils industry navigates energy-transition challenges.

South Korea Automotive Engine Oils Industry Leaders

ExxonMobil Corporation

GS Caltex

Hyundai Oilbank

SK Inc.

S-OIL CORPORATION

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Auto components maker Gabriel India has formed a joint venture with South Korea's SK Enmove to diversify its product portfolio, incorporating lubricants and automotive engine oils. The strategic partnership represents a significant step forward in SK Enmove's revenue generation and expansion into new markets.

- June 2025: HD Hyundai Oilbank and Shell announced plans to enter the high-performance Group III base oil market. Their joint company, HD Hyundai Shell Base Oil, plans to commence full-scale commercial production of Group III base oils in South Korea by 2027. This will benefit the South Korean Automotive Engine Oils Market.

South Korea Automotive Engine Oils Market Report Scope

By Resin Type

| Passenger Car Motor Oil (PCMO) | 0W-XX |

| 5W-XX | |

| 10W-XX | |

| 15W-XX | |

| Monogrades | |

| Other Grades | |

| Heavy Duty Motor Oil (HDMO) | 0W-XX |

| 5W-XX | |

| 10W-XX | |

| 15W-XX | |

| Monogrades | |

| Other Grades | |

| Motorcycle Engine Oil (MCO) | 0W-XX |

| 5W-XX | |

| 10W-XX | |

| 15W-XX | |

| Monogrades | |

| Other Grades |

By Base Stock

| Mineral |

| Synthetic |

| Semi-Synthetic |

| Bio-Based |

| By Resin Type | Passenger Car Motor Oil (PCMO) | 0W-XX |

| 5W-XX | ||

| 10W-XX | ||

| 15W-XX | ||

| Monogrades | ||

| Other Grades | ||

| Heavy Duty Motor Oil (HDMO) | 0W-XX | |

| 5W-XX | ||

| 10W-XX | ||

| 15W-XX | ||

| Monogrades | ||

| Other Grades | ||

| Motorcycle Engine Oil (MCO) | 0W-XX | |

| 5W-XX | ||

| 10W-XX | ||

| 15W-XX | ||

| Monogrades | ||

| Other Grades | ||

| By Base Stock | Mineral | |

| Synthetic | ||

| Semi-Synthetic | ||

| Bio-Based | ||

Key Questions Answered in the Report

What is the current size of the South Korea automotive engine oils market in 2026?

It totals 325.79 million liters.

Which product type holds the largest share?

Passenger car motor oil accounts for 62.85% of 2025 volume.

Why are synthetic oils gaining ground?

Hybrid adoption and OEM requirements for low-viscosity formulations are pushing synthetic penetration above 54%.

How is electrification affecting lubricant demand?

EV uptake reduces ICE volumes, but refiners offset risk with EV-specific fluids and bio-based products.

Page last updated on: