Body Armor Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Market Size (2026) | USD 3.15 Billion |

| Market Size (2031) | USD 3.92 Billion |

| Growth Rate (2026 - 2031) | 4.47% CAGR |

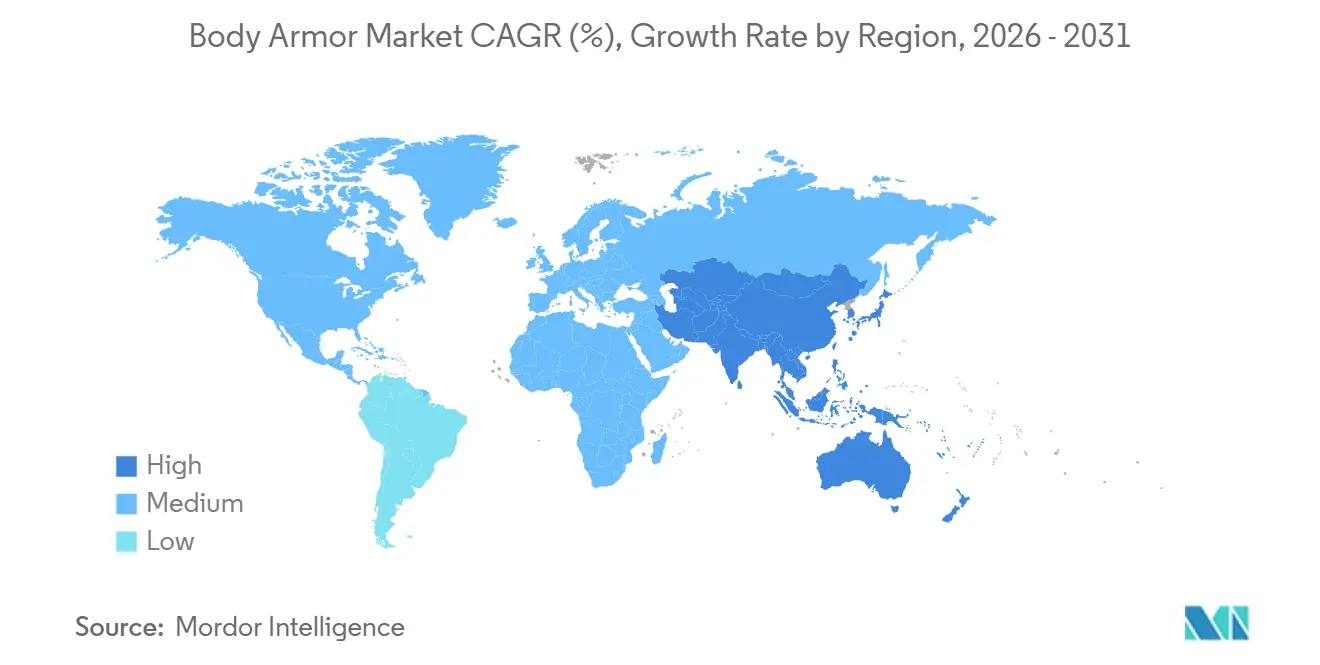

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Body Armor Market Analysis by Mordor Intelligence

The body armor market size is expected to grow from USD 3.01 billion in 2025 to USD 3.15 billion in 2026 and is forecast to reach USD 3.92 billion by 2031 at a 4.47% CAGR over 2026-2031. Procurement cycles remain lengthy, and budgets are tight; yet, demand endures as armed forces modernization, law enforcement replacements, and civilian preparedness programs move forward. Soft armor continues to dominate day-to-day patrol use, while hard-armor growth is tied to rifle threat requirements and ongoing conflicts that deplete existing stock. Protection standards are rising in parallel with material innovations that cut plate weight and blunt-trauma risk. Certification costs, fiber bottlenecks, and new environmental rules have slowed product launches but have not reversed the upward revenue trend in the body armor market.

Key Report Takeaways

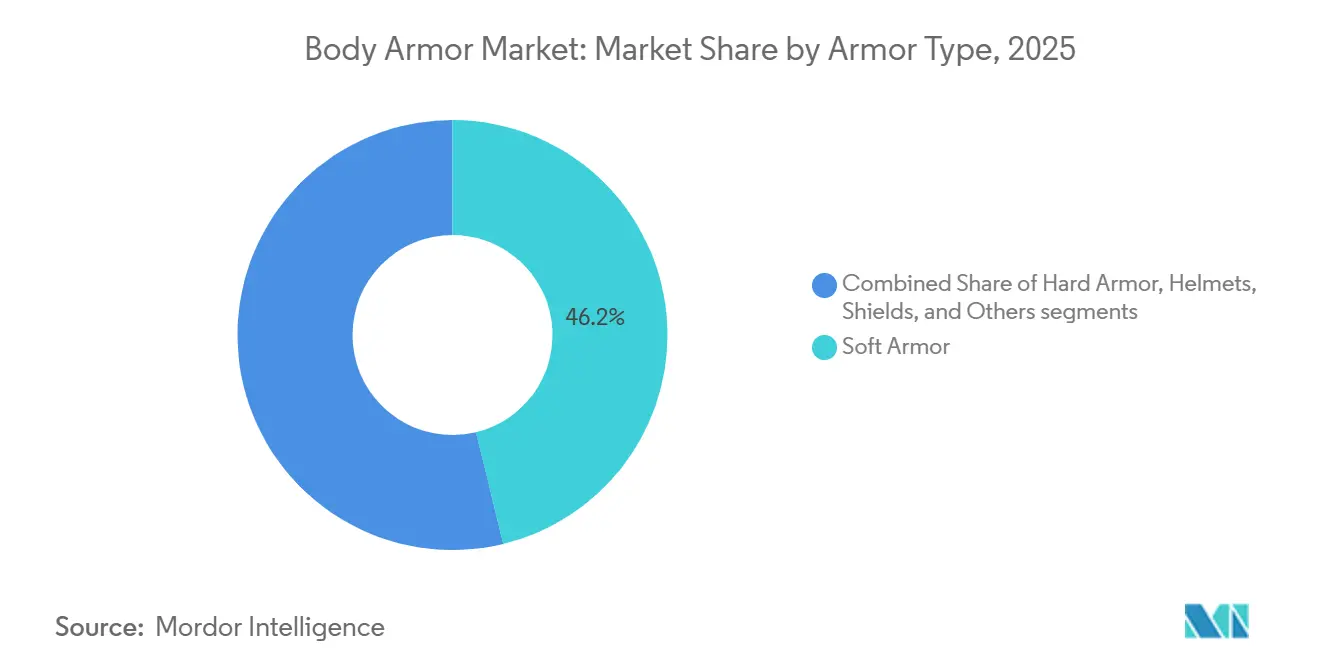

- By armor type, soft armor commanded 46.21% of 2025 revenue, while hard armor is forecast to grow at a 5.54% CAGR through 2031.

- By protection level, Level IIIA accounted for 37.65% of the 2025 share, while Level IV plates are projected to grow at a 5.32% CAGR through 2031.

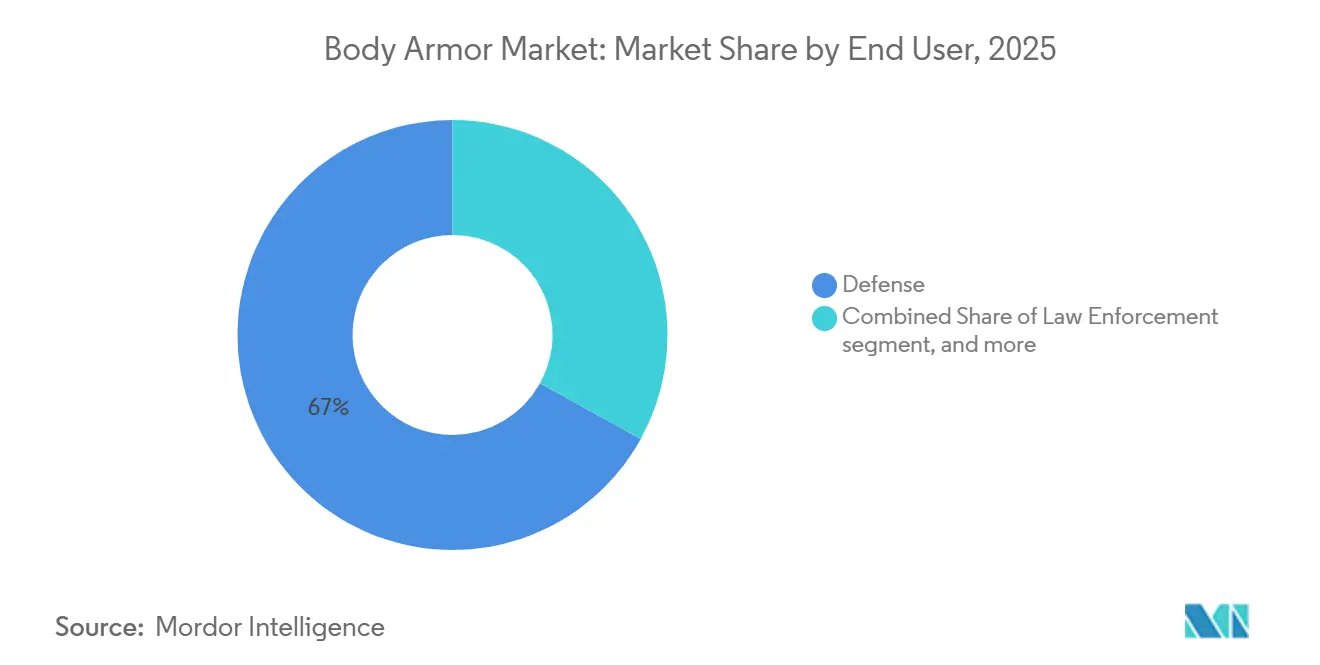

- By end user, defense users generated 66.97% of the 2025 demand; the civilian and private security segment is projected to grow at a 5.12% CAGR through 2031.

- By geography, North America led with 44.31% of the 2025 revenue, and the Asia-Pacific region is anticipated to expand at a 5.84% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Body Armor Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rise in defense budgets and soldier modernization programs | +1.2% | Global with emphasis on North America, Europe, Asia-Pacific | Long term (≥ 4 years) |

| Escalating geopolitical conflicts and terrorism threats | +1.0% | Middle East, Asia-Pacific, Eastern Europe | Short term (≤ 2 years) |

| Increasing demand for ballistic protection among law-enforcement agencies | +0.8% | North America, Europe, South America | Medium term (2-4 years) |

| Advancements in lightweight composite materials | +0.7% | Global, early adoption in North America and Europe | Medium term (2-4 years) |

| Integration of IoT-enabled health-monitoring sensors in smart armor | +0.4% | North America, Europe, select Asia-Pacific markets | Long term (≥ 4 years) |

| Surge in civilian concealed-carry license holders | +0.5% | North America, emerging South America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rise in Defense Budgets and Soldier Modernization Programs

Global military expenditure reached USD 2.44 trillion in 2024, and the resulting procurement pipelines guarantee multi-year funding for ballistic protection.[1]Stockholm International Peace Research Institute, “World Military Expenditure 2024,” sipri.org The US Army’s Integrated Visual Augmentation System (IVAS), Next Generation Squad Weapon (NGSW), and Soldier Protection System (SPS) are expected to allocate more than USD 22 billion through 2030, bundling plate carriers with thermal sights and digital networking modules. India’s Future Infantry Soldier as a System program mandates domestic production targets that spur factory expansions by MKU Limited and other local firms. South Korea’s Warrior Platform includes exoskeleton-ready carriers, slated for fielding by 2027, demonstrating the influence of ergonomics on armor decisions. Long-term visibility is positive for the body armor market, although fixed price contracts expose suppliers to the risk of raw material inflation.

Escalating Geopolitical Conflicts and Terrorism Threats

Large-scale consumption in Ukraine, Israel, and Taiwan forces NATO states to accelerate replenishment orders, creating abrupt spikes that roll through supply chains. Police tactical units in Western Europe adopted overt plate carriers following the 2024 Paris and Brussels attacks, driving overt-wear sales to higher levels. Such surges are temporary yet sizable, underscoring why inventory buffers remain small relative to battlefield burn rates. Manufacturers capitalize on urgent requirements but must manage the risk of post-conflict demand drops. The body armor market thus experiences short-term revenue bursts atop a slower but durable modernization wave.

Increasing Demand for Ballistic Protection Among Law-Enforcement Agencies

The US Department of Justice awarded USD 458 million in Bulletproof Vest Partnership grants during FY 2024, a 12% increase over the previous year, which is sufficient to outfit approximately 13,000 agencies. Germany tendered 8,500 Level IIIA vests in 2025 to counter organized crime, mirroring broader European trends toward the universal issuance of soft armor. Hybrid designs that pair soft panels with plate pockets enable swift up-armor capability during active-shooter events, an approach showcased in Point Blank’s Guardian line. Stricter NIJ 0101.06 blunt-trauma limits removed budget brands, concentrating sales among manufacturers able to finance certification. The body armor market, therefore, benefits from steady municipal refresh cycles even when headcounts remain flat.

Advancements in Lightweight Composite Materials

Ultra-high-molecular-weight polyethylene (UHMWPE) has cut plate weight per threat level by 15% since 2020, allowing Level III plates to weigh under 2 kg. Honeywell’s Spectra Shield 3000 reduces back-face deformation by 22% and supports new NIJ 0101.07 threat classes. Ceramic faces shift from alumina to boron carbide, which offers superior hardness at significantly higher cost, limiting uptake to elite units. Hybrid polyethylene-ceramic constructions, such as the Enhanced Small Arms Protective Insert, won new US Army contracts, demonstrating readiness for volume production. Lighter armor directly improves soldier endurance, strengthening demand over the forecast period.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of advanced hard-armor plates | -0.6% | Global, especially North America, South America, Africa | Medium term (2-4 years) |

| Stringent NIJ certification and testing timelines | -0.5% | North America, export-oriented firms in Europe and Asia-Pacific | Long term (≥ 4 years) |

| Supply-chain volatility for high-grade polyethylene fibers | -0.4% | Global, most acute in North America and Europe | Short term (≤ 2 years) |

| Environmental regulations on PFAS-based fabric treatments | -0.3% | North America, Europe, emerging rules in Australia, Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Cost of Advanced Hard-Armor Plates

Level IV ceramic plates retail between USD 500 and USD 900, a price range that exhausts equipment budgets at smaller law enforcement agencies and deters many civilians from purchasing them. Production relies on 2,200°C sintering and rigorous crack inspection, driving high energy bills and scrap rates. Emerging 3D-printed tiles promise a 25% cost cut but require durability data before widespread adoption. The expense gap keeps soft armor popular even though rifle-threat protection is superior. As a result, price acts as a ceiling on the body armor market, especially in civilian channels.

Stringent NIJ Certification and Testing Timelines

NIJ 0101.07 subjects each model to 18-24 months of conditioning and ballistic testing, costing thousands of dollars per design.[2]National Institute of Justice, “Ballistic Resistance of Body Armor Standard 0101.07,” nij.ojp.gov Smaller firms often endure revenue droughts during validation, sometimes withdrawing entirely from the US law enforcement segment. Varied global standards create inventory complexity for exporters. Although the protocol enhances product reliability, it slows innovation and slightly dampens the growth rate of the body armor market CAGR.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Armor Type - Hard Armor Gain Momentum

Soft armor accounted for 46.21% of 2025 revenue, while hard armor, with a forecasted 5.54% CAGR, positioned itself as a principal growth engine for the body armor market. Military forces field ceramic-polyethylene inserts that stop 7.62×51 mm armor-piercing rounds, and plate-ready carriers are the baseline issue for US infantry. Helmets and shields form smaller niches, but they benefit from the same material advances.

Soft armor remains essential for routine policing because it is lightweight and can be concealed under uniforms. Quick-release vest designs and moisture-wicking liners from Point Blank improve daily wearability.[3]Point Blank Enterprises, “Guardian Series Launch,” pointblankenterprises.com The divergence highlights how the user's mission drives purchase decisions within the body armor market.

By Protection Level - Level IV Advances Fastest

Level IIIA maintained the largest share, at 37.65% in 2025, underscoring the durability of handgun-rated products in patrol and civilian contexts. At the same time, Level IV is forecast to post a 5.32% CAGR through 2031, the fastest among all ratings, as defense ministries demand multi-hit plates against .30-06 AP threats.

Levels III and III+ serve National Guard units and reserve forces seeking rifle coverage at lower cost, while lower IIA and II classes continue to decline. Modular carriers, such as Safariland’s Apex system, enable agencies to mix and match soft and hard inserts, adjusting their inventory to meet mission and budget needs.[4]Safariland Group, “Apex Vest Product Sheet,” safariland.com This tiered architecture supports broad participation in the body armor market.

By End User - Civilian Demand Accelerates

Defense procurement generated 66.97% of 2025 revenue, reflecting sustained investments in programs such as the US SPS and India’s F-INSAS. Still, civilian and private-security channels are poised for 5.12% annual growth, making them the fastest-rising share contributors to the body armor market.

E-commerce brands achieve 40% yearly sales gains by bypassing distributors, while private security firms outfit guards at data centers and pharmaceutical plants with overt rifle-rated vests. Female-specific patterns address unmet ergonomic needs among women, who now comprise 19% of US police forces, thereby broadening product appeal and reinforcing overall market growth.

Geography Analysis

North America accounted for 44.31% of 2025 revenue, primarily driven by the USD 842 billion US defense budget, which allocates USD 12.3 billion to soldier systems. Federal vest grants and state subsidies shorten replacement cycles, while Canada’s CAD 1.90 billion (USD 1.37 billion) Integrated Soldier System Project sustains regional orders.

Asia-Pacific offers the swiftest 5.84% CAGR, propelled by China’s next-generation plate purchases for 2 million troops and India’s insistence on indigenous content under the Atmanirbhar Bharat policy. South Korea’s upcoming exoskeleton-compatible carriers further advance ergonomic innovation.

Europe accelerates spending as NATO states replenish stocks sent to Ukraine, with Germany ordering 25,000 carriers and Poland investing USD 230 million in upgrades. The Middle East remains an enduring customer amid ongoing conflicts, where Saudi Arabian Military Industries co-produces Level IV plates locally. South America and Africa trail behind due to constrained defense budgets, although Brazil’s national police procured 8,000 Level IIIA vests in 2024, signaling gradual progress.

Competitive Landscape

The body armor market shows moderate concentration; the five largest vendors (BAE Systems plc, Point Blank Enterprises, Inc., Safariland, LLC., DuPont de Nemours, Inc., and Avon Technologies plc) control more than 40% of global sales. DuPont’s 2024 exclusive Kevlar EXO supply deal with Point Blank locks down premium aramid output while elevating vertical integration margins. Honeywell spun off its Advanced Materials arm as Solstice in 2025, retaining the Spectra fiber lines but exiting the assembly business, which reshapes supply options for downstream vest makers.

MKU Limited leverages low manufacturing costs and a USD 158 million Indian Army order to win export tenders across Africa and Southeast Asia. Australian Defence Apparel’s joint venture with PT Pindad opens up Southeast Asian channels where defense budgets are rising faster than those in the West.

Technological differentiation remains pivotal. BAE Systems plc has filed 14 graphene-ceramic patents, aiming for a 20% weight reduction, while Avon Technologies plc focuses on additive manufacturing to reduce lead times to four weeks. Pricing battles intensify in the civilian web-store segment, forcing incumbents to launch economy lines or cede volume to direct-to-consumer specialists. Overall, competitive intensity remains stable, yet material supply agreements and regional joint ventures continue to reshape the share distribution in the body armor market.

Body Armor Industry Leaders

Point Blank Enterprises, Inc.

BAE Systems plc

Avon Technologies plc

DuPont de Nemours, Inc.

Safariland, LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: The Federal Bureau of Investigation (FBI) awarded Predictive Ballistics LLC a five-year, USD 61 million indefinite-delivery/indefinite-quantity (IDIQ) contract for an advanced armor system. Safariland, a subsidiary of Cadre Holdings, will provide the ballistic panels for the contract, which also makes the armor system available to other Department of Justice agencies, including the US Marshals Service and the Drug Enforcement Administration (DEA). The contract presents a significant opportunity for suppliers specializing in ballistic protection equipment for federal law enforcement agencies.

- February 2026: At the Enforce Tac 2026 trade fair, Rheinmetall launched a newly developed body armor system for military use. The new system protects against attacks involving firearms, stabbing weapons, and explosives. Its modular design enables situation-specific, individually configurable wearing options based on the purpose and location of use, ensuring optimal comfort. The ballistic protection elements include soft ballistic protection for the front, back, and abdomen, in accordance with VPAM BSW Level 3. The system also includes hard ballistic inserts for the front and back, which users can upgrade to VPAM BSW stand-alone Levels 6 or 9. Users can also add stab protection in accordance with VPAM KDIW Level K1.

- February 2026: Safe Life launched the Unity™ Hybrid, a new armor carrier system designed to move the body armor industry beyond decades of stagnation. Combining modularity, comfort, and adaptability, the Unity™ Hybrid aims to redefine “military-grade” as high-quality gear that balances innovation, Berry Compliance, and cost-effectiveness. Developed in collaboration with military and law enforcement professionals, the Unity™ Hybrid introduces a quad placard system that enables true customization. Each component locks in with millimeter-level precision, allowing users to rapidly reconfigure their setup without compromising fit or aesthetics. The design is particularly useful and cost-effective for agencies and teams that require standardized gear adaptable to multiple missions or roles.

Global Body Armor Market Report Scope

Body armor, personal armor, armored suit, and coat of armor are defined as protective clothing designed to absorb or deflect physical attacks. It has historically been used to protect military personnel. It is also used by various law enforcement agencies (riot police in particular), private security guards, bodyguards, and occasionally ordinary citizens.

The body armor market is segmented by armor type, protection level, end user, and geography. By armor type, the market is segmented into soft armor, hard armor, helmets, shields, and others. By protection level, the market is segmented into Level IIA, Level II, Level IIIA, Level III, Level III+, and Level IV. By end user, the market is segmented into defense, law enforcement, and civilian and private security. The report also provides market size and forecasts for major countries across various regions. The market size is provided for each segment in terms of value (USD).

| Soft Armor |

| Hard Armor |

| Helmets |

| Shields |

| Others |

| Level IIA |

| Level II |

| Level IIIA |

| Level III |

| Level III+ |

| Level IV |

| Defense |

| Law Enforcement |

| Civilian and Private Security |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Israel | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Armor Type | Soft Armor | ||

| Hard Armor | |||

| Helmets | |||

| Shields | |||

| Others | |||

| By Protection Level | Level IIA | ||

| Level II | |||

| Level IIIA | |||

| Level III | |||

| Level III+ | |||

| Level IV | |||

| By End User | Defense | ||

| Law Enforcement | |||

| Civilian and Private Security | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Italy | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Israel | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the body armor market in 2026?

The body armor market size is expected to grow from USD 3.01 billion in 2025 to USD 3.15 billion in 2026 and is forecast to reach USD 3.92 billion by 2031 at a 4.47% CAGR over 2026-2031.

Which protection level is expanding the fastest?

Level IV plates record the highest 5.32% CAGR through 2031driven by the demand from defense ministries for multi-hit plates against .30-06 AP threats.

Why is Asia-Pacific the quickest-growing region?

Modernization programs in China, India, and South Korea fuel a 5.84% CAGR for regional purchases.

What factors restrain price-sensitive buyers?

High Level IV plate costs of USD 500-900 and lengthy NIJ certification deter smaller agencies and civilians.

Which companies lead recent vertical integration moves?

DuPont’s exclusive Kevlar EXO supply to Point Blank and Honeywell’s Spectra-focused Solstice spin-off highlight this trend.

Page last updated on: