Blockchain In Healthcare Market Size and Share

Market Overview

| Study Period | 2022 - 2031 |

|---|---|

| Market Size (2026) | USD 8.27 Billion |

| Market Size (2031) | USD 63.58 Billion |

| Growth Rate (2026 - 2031) | 50.38% CAGR |

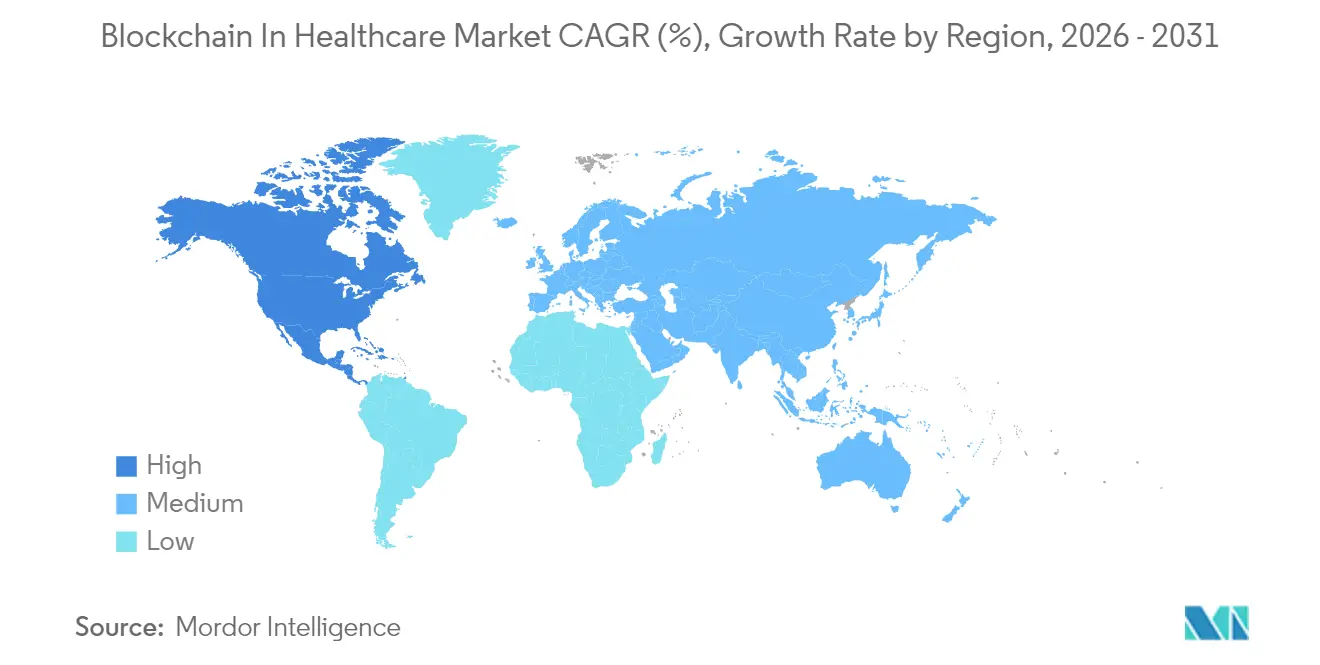

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

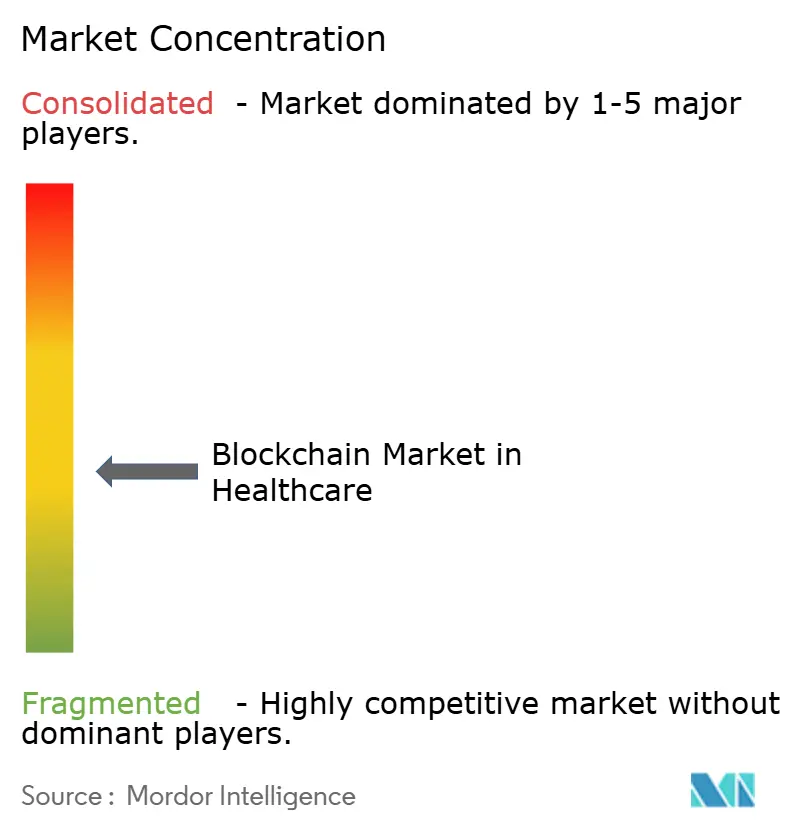

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Blockchain In Healthcare Market Analysis by Mordor Intelligence

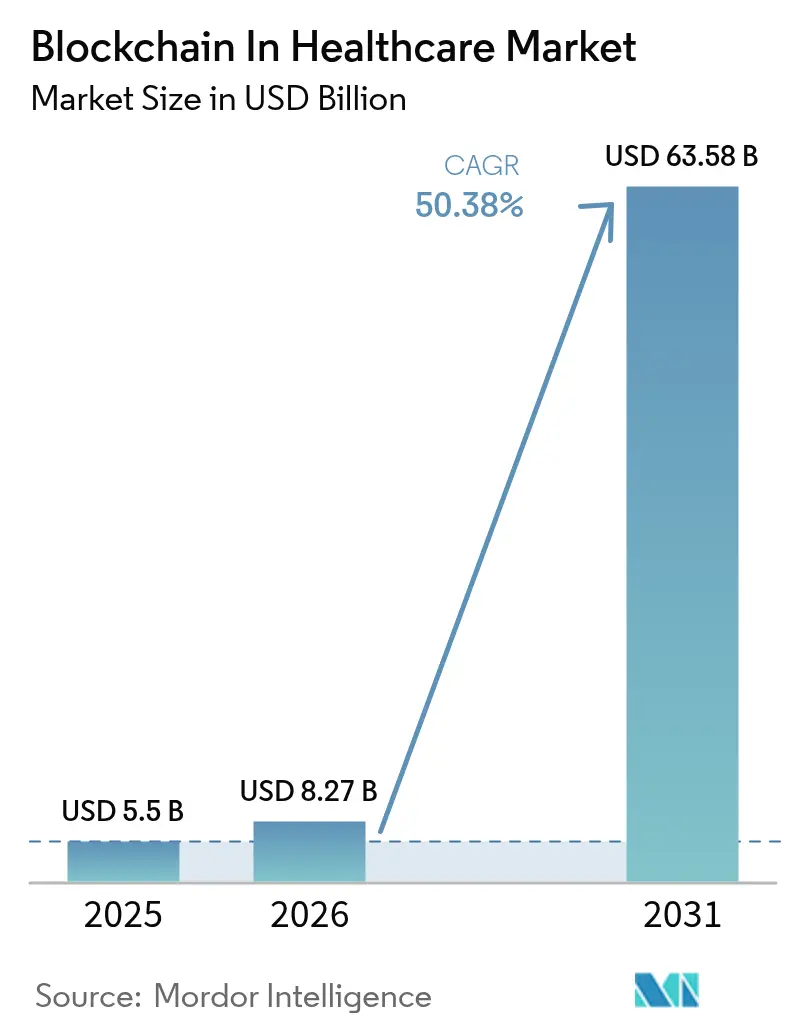

The Blockchain Market size In Healthcare market is expected to grow from USD 5.5 billion in 2025 to USD 8.27 billion in 2026 and is forecast to reach USD 63.58 billion by 2031 at 50.38% CAGR over 2026-2031.

This surge is tied to North American and European serialization laws, rising cyber-breach costs that now average USD 10.93 million per incident, and payer mandates to curb duplicate claims. Immutable ledgers increasingly serve as the backbone for regulatory compliance automation, while smart-contract adjudication reduces administrative waste and federated learning protocols unlock new data-monetization revenue for both providers and patients. CIOs view blockchain as infrastructure rather than a pilot technology, shifting budgets toward permissioned and consortium architectures that align with HIPAA, GDPR, and TEFCA requirements. As a result, the blockchain in healthcare market is pivoting from proof-of-concept projects to enterprise production deployments across clinical data exchange, drug supply chains, and tokenized health-data marketplaces.

Key Report Takeaways

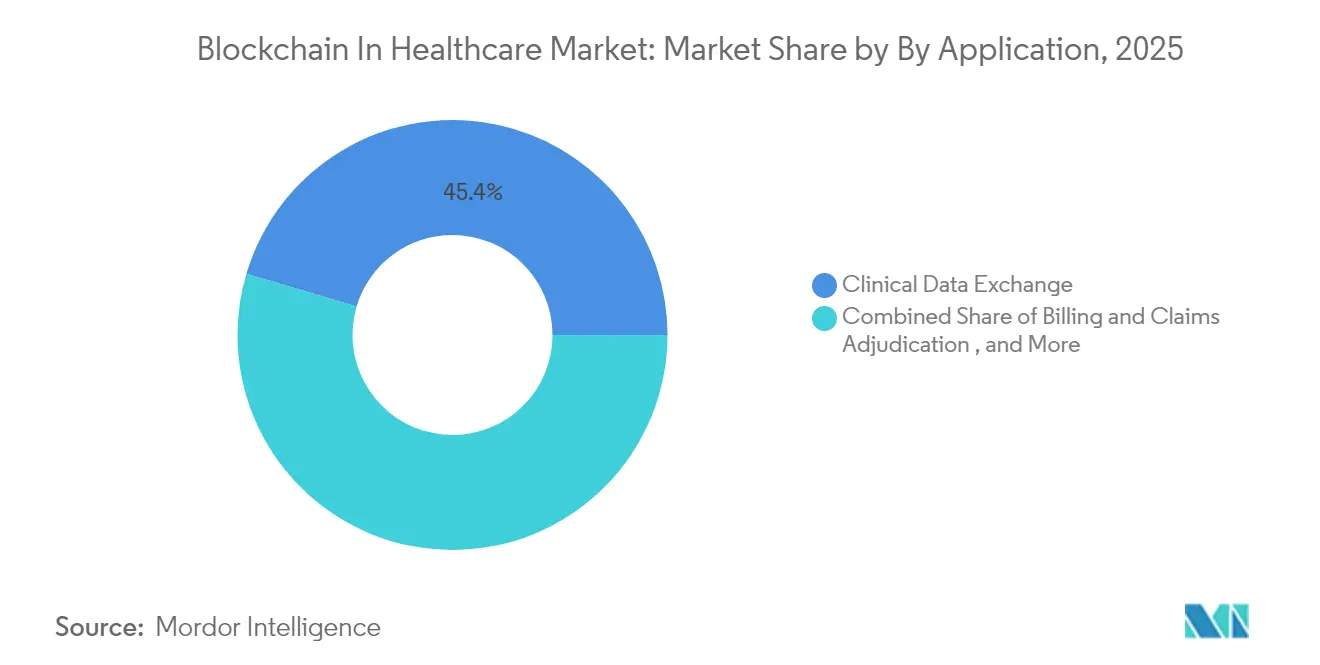

- By application, Clinical Data Exchange led with 45.40% of the blockchain in healthcare market share in 2025, while Clinical Trials & Consent Management is on track for a 71.04% CAGR through 2031.

- By end user, Providers held 53.20% of the blockchain in healthcare market share in 2025; Patients & Health-Data Brokers record the fastest 76.95% CAGR between 2026-2031.

- By blockchain type, Private/Permissioned networks commanded 62.30% of the blockchain in the healthcare market size in 2025, whereas Consortium models will advance at a 66.93% CAGR over the forecast period.

- By geography, North America accounted for 40.95% of the blockchain in healthcare market share in 2025, yet Asia-Pacific is rising at a 61.18% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Blockchain In Healthcare Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising cyber-breach costs push CIO budgets toward blockchain security | +8.20% | Global, strongest in North America & EU | Medium term (2-4 years) |

| US & EU DSCSA / FMD serialization deadlines mandate end-to-end drug traceability | +12.50% | North America & EU, extending to APAC | Short term (≤ 2 years) |

| Payer pressure to cut duplicate claims fuels smart-contract adjudication | +6.80% | North America, early uptake in EU | Medium term (2-4 years) |

| Growing EHR interoperability projects accelerate demand | +9.30% | Global, led by TEFCA in North America | Short term (≤ 2 years) |

| Tokenized health-data marketplaces create new revenue lines | +7.10% | North America & EU, pilots in APAC | Long term (≥ 4 years) |

| AI-ready federated learning pilots require blockchain-anchored model proofs | +5.40% | Global, centered on research hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Cyber-Breach Costs Push CIO Budgets Toward Blockchain Security

Healthcare breaches compromised more than 500 million records since 2020, and average incident costs reached USD 10.93 million in 2024. The February 2024 Change Healthcare attack, which halted USD 22 million in daily claims and triggered a USD 22 million bitcoin ransom, underscored centralized system vulnerabilities. Distributed ledgers fit zero-trust architectures by offering tamper-evident audit trails, data provenance, and multi-party verification that satisfy the Department of Health and Human Services’ voluntary Cybersecurity Performance Goals. As insurers tighten underwriting criteria and regulators highlight blockchain for critical data integrity, CIOs now budget blockchain as core cybersecurity spend rather than innovation-hub outlay. This shift accelerates full-scale network rollouts across provider systems and payer clearinghouses

US & EU DSCSA / FMD Serialization Deadlines Mandate End-to-End Drug Traceability

The Drug Supply Chain Security Act’s enhanced requirements, extended but firm through 2026, compress implementation windows for serialized transactions. An FDA pilot with IBM, KPMG, Merck, and Walmart delivered 100% traceability compared with 73% under legacy tools, proving blockchain efficiency. Europe’s Falsified Medicines Directive exerts parallel pressure as serialized National Drug Codes demand unbroken auditability. Trading partners lacking electronic connections risk supply-chain exclusion, pushing pharmaceutical distributors to adopt permissioned ledgers that mesh GS1 EPCIS standards with smart contracts. Regulatory clarity on electronic pedigrees, therefore, moves blockchain from an opportunity choice to an operational prerequisite.

Payer Pressure to Cut Duplicate Claims Fuels Smart-Contract Adjudication

Duplicate and erroneous claims consume 8–12% of US payer outlays and inflate administrative costs by USD 68 billion annually. Smart-contract logic can validate claims in seconds against multi-payer databases, trimming processing windows from days to near real time while encrypting protected health information. Anthem’s blockchain collaboration with IBM shows prior authorization flows dropping from 14 to 3 days and fraud detection models flagging upcoding within minutes. When paired with AI, distributed ledgers analyze billing patterns and automate multi-signature consensus among patients, providers, and payers. This linkage converts blockchain deployments into direct cost-savings engines and supportive fraud mitigation tools

Growing EHR Interoperability Projects Accelerate Demand

The Trusted Exchange Framework and Common Agreement sets national guardrails for secure, patient-centric data exchange worth an estimated USD 77.8 billion in benefits. TEFCA’s reliance on standardized APIs dovetails with blockchain’s cryptographic proof of data integrity and granular access governance. Estonia’s health system, running nationwide blockchain medical records since 2018, operates at 99.9% uptime and demonstrates real-world scalability. US health systems must now verify record authenticity and log access events to remain QHIN-compliant, pushing consortium chains into production. Hospitals, therefore, treat blockchain not merely as storage but as an interoperability overlay indispensable to TEFCA adherence.[3]Merck, “Results of FDA Blockchain Pilot for Drug Traceability,” merck.com

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High migration cost from legacy HIS limits near-term rollouts | -4.70% | Global, acute in North America | Short term (≤ 2 years) |

| Fragmented global health-data regulations complicate cross-border chains | -3.20% | Global, notably EU-US transfers | Medium term (2-4 years) |

| Public-cloud carbon-footprint targets delay PoW implementations | -2.10% | EU & North America | Long term (≥ 4 years) |

| Limited API capabilities in legacy EHRs slow blockchain integration | -1.90% | Global, greatest in mid-sized hospitals | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Migration Cost from Legacy HIS Limits Near-Term Rollouts

Large hospital systems spend USD 15-25 million on core HIS migrations and another USD 5-8 million for blockchain-ready middleware and staff upskilling. Legacy EHR stacks deployed more than a decade ago lack modern API layers, requiring custom connectors or full system overhaul—a budget strain for community hospitals. Maintaining HIPAA safeguards during transition raises legal and insurance liabilities that boards are hesitant to absorb. The Change Healthcare breach clarified the risks of inaction, but its USD 2.3 billion recovery bill also highlighted the capital burden of technology replacement. Consequently, many providers schedule blockchain adoption in phased pilots tied to broader EHR renewal cycles, moderating near-term uptake [1]Holland & Knight, “Aftermath of the Change Healthcare Cyberattack,” hklaw.com

Fragmented Global Health-Data Regulations Complicate Cross-Border Chains

GDPR’s right-to-erasure, China’s Data Security Law, and impending Indian privacy rules all impose data-localization or mutability demands that conflict with blockchain’s immutable nature. Healthcare groups operating across borders thus maintain separate node clusters with jurisdiction-specific privacy overlays, adding complexity and cost. Absence of mutual recognition agreements further limits the value of global health data pools, even as cross-border clinical trials and medical tourism require seamless exchange. Enterprises now layer zero-knowledge proofs and hashing techniques to stay compliant, but governance overhead slows multi-region network expansion and dampens blockchain in healthcare market penetration outside single-country deployments.[2]PubMed Central, “Cross-Border Data Regulations and Blockchain Challenges,” pubmed.ncbi.nlm.nih.gov

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Clinical Data Exchange Dominates While Consent Management Surges

Clinical Data Exchange secured 45.40% of the blockchain in healthcare market share in 2025, underpinned by TEFCA mandates that make verifiable information exchange a core provider obligation. The segment benefits from mature HL7-FHIR integrations and secure share-and-query workflows that minimize record duplication. Billing & Claims Adjudication follows as insurers implement smart contracts to cut USD 68 billion in duplicate payments. Conversely, Clinical Trials & Consent Management is the growth pacesetter with a 71.04% CAGR to 2031 as sponsors require immutable consent logs and decentralized recruitment. Pharmaceutical firms report 40% shorter enrollment windows after shifting to blockchain-verified permissions. Supply-Chain & Provenance solutions linked to DSCSA compliance round out the stack, ensuring serialized drug visibility down to unit level. The blockchain in healthcare market size for applications serving patient-centric consent networks is projected to expand at 71.04% annually through 2031, reshaping trial economics and patient engagement.

The convergence of AI with dynamic smart consent allows patients to grant time-boxed or condition-based data rights that expire automatically, embedding privacy by design. Automated royalty frameworks pay participants when their data drives trial insights, while zero-knowledge proofs preserve anonymity. Hospitals thereby transition from passive record custodians to active data brokers, and venture funding increasingly flows into platforms that operationalize patient ownership concepts at scale. Regulatory endorsement by the FDA for distributed trial evidence further propels adoption, turning consent management into a cornerstone for decentralized research networks.

By End User: Providers Lead While Patient Data Brokers Accelerate

Providers accounted for 53.20% of the blockchain in healthcare market share in 2025 as they shoulder HIPAA compliance and generate primary clinical data streams. Networks enable providers to reconcile disparate EHRs, prove data lineage, and feed analytics engines without central vulnerabilities. Payers & Pharmacy Benefit Managers use permissioned ledgers to authenticate claims and mitigate fraud, realizing 30-40% administrative savings. Patients & Health-Data Brokers, however, post the highest 76.95% CAGR, attaining critical mass on token-based marketplaces where individuals monetize anonymized records. This shift redefines data ownership norms and forms new revenue pools for patient communities.

Platforms such as Patientory and MedRec embed self-sovereign identity, giving individuals granular control of record sharing and financial returns. Providers, in turn, partner with these networks to improve longitudinal data quality and patient retention. Token incentives and transparent governance drive engagement, while secure wallets ensure records remain portable across providers. Pharmaceutical firms sourcing real-world evidence gain simplified consent workflows, accelerating drug discovery and personalized-medicine models. The blockchain in healthcare market therefore evolves into a tri-party ecosystem linking providers, payers, and empowered patients.

By Blockchain Type: Private Networks Dominate With Consortium Growth

Private/Permissioned chains held 62.30% of the blockchain in healthcare market share in 2025, favored for role-based access and the capacity to honor deletion requests in hybrid off-chain storage. Hospitals deploy these networks behind firewalls, integrating identity management and HSM-backed key custody for HIPAA alignment. Consortium chains are expanding fastest at a 66.93% CAGR because drug-safety pilots, health-information exchanges, and payer-provider alliances demand shared governance. Hyperledger Fabric-based frameworks now embed Fabric-X modules for regulated digital assets, offering Byzantine Fault Tolerance and data-token partitioning.

Public chains remain niche due to privacy concerns, yet advances in zero-knowledge rollups and selective disclosure spark interest in global research collaborations. Sustainability agendas further tilt decisions toward Proof-of-Stake models that consume minimal energy compared with Proof-of-Work alternatives. As sustainability reporting becomes mandatory across the EU, healthcare buyers increasingly seek emissions data for blockchain workloads, steering investments into energy-efficient networks.

Geography Analysis

North America accounted for 40.95% of blockchain in healthcare market share in 2025, sustained by DSCSA serialization, TEFCA interoperability demands, and heightened breach-containment costs. The USD 22 million daily disruption from the 2024 Change Healthcare attack underscored the stakes, driving healthcare systems to allocate 6-10% of total IT budgets to cybersecurity-centric ledger deployments. Large hospital chains such as the Mayo Clinic and payer groups, including Anthem, now combine HL7-FHIR gateways with blockchain notarization for claims and medical records, while the Department of Veterans Affairs runs pilots for longitudinal patient wallets. Federal guidance from HHS that cites blockchain in critical-data-integrity recommendations cements its role across provider and payer stacks.

Asia-Pacific is the growth nucleus with a 61.18% CAGR through 2031. China’s national health data platform mandates blockchain-anchored data provenance, though localization laws require in-country node residency. Japan’s 2024 Medical Law amendments explicitly promote digital-health tech, spurring hospital consortia to pilot blockchain for telemedicine and prescription verification. India’s Ayushman Bharat Digital Mission combines patient-controlled health IDs with sandboxed blockchain pilots, while the forthcoming Digital Personal Data Protection Act shapes privacy overlays. ASEAN nations integrate blockchain into medical-tourism corridors, ensuring secure transfer of diagnostic images and prescriptions for cross-border patients seeking treatment in Singapore and Thailand.

Europe maintains steady momentum as GDPR necessitates immutable but revocable audit trails, prompting region-wide interest in zero-knowledge proofs and off-chain storage hybrids. The European Blockchain Service Infrastructure publishes healthcare-specific guidelines that help member states converge on common consent receipts and digital signing standards. Germany’s Hospital Future Act funds blockchain proofs of record provenance, and the Nordics extend e-prescription platforms onto consortium chains. In the Middle East & Africa, Gulf Cooperation Council smart-city programs embed blockchain to manage citizen health wallets and pharmaceutical logistics, while South Africa pilots decentralized records at Frere Provincial Hospital. These deployments illustrate how resource-constrained markets leapfrog legacy IT by adopting ledger systems that bundle security, identity, and traceability.

Competitive Landscape

The blockchain in healthcare market is moderately fragmented, with global tech vendors vying against niche healthcare-specific platforms. IBM leverages its Food Trust heritage to deliver DSCSA compliance for drug traceability and partners with Anthem on claims automation, embedding Fabric-based nodes on IBM Cloud. Microsoft positions Azure Health Data Services as blockchain-ready infrastructure, furnishing identity, FHIR, and confidential computing modules that satisfy hybrid-cloud security mandates. Oracle tailors ledger services to pharmaceutical clients, integrating serialization and data analytics for supply-chain assurance.

Healthcare-native entrants such as BurstIQ, Patientory, and MedRec focus on patient-controlled data wallets and token economics, differentiating through privacy-preserving computation and federated learning integrations. Change Healthcare, now under Optum, embeds blockchain micro-services into existing clearing-house rails, easing migration for payers. Collaborations like the FDA pilot with IBM, KPMG, Merck, and Walmart show how mixed consortia blend enterprise scale with regulatory insight to meet stringent serialization targets.

Competitive positioning centers on three pillars: regulatory automation, cybersecurity resilience, and data-monetization enablement. Vendors that bundle standards-aligned governance, zero-knowledge proofs, and AI analytics position themselves to capture cross-segment share. Open-source momentum around Hyperledger’s Fabric-X release further tilts the field toward modular, audit-friendly frameworks that large hospitals and payers can tailor. Market entrants that lack compliance-grade tooling or broad partner ecosystems are increasingly restricted to pilot projects rather than full production contracts.

Blockchain In Healthcare Industry Leaders

IBM Corporation

Microsoft Corporation

Patientory Inc.

Guardtime Federal

Hashed Health

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: IBM Research contributed Fabric-X enhancements—Byzantine Fault Tolerance and advanced cryptography—to Hyperledger Fabric for regulated-asset healthcare deployments.

- February 2025: API Holdings adopted IBM Instana to bolster interoperability under India’s Ayushman Bharat Digital Mission, positioning blockchain as a future integration layer.

- January 2025: IBM, KPMG, Merck, and Walmart expanded their FDA pilot to validate global pharmaceutical integrity, confirming 100% traceability success rates.

- December 2024: Microsoft Azure launched Health Data Consortium features that enable multi-jurisdiction blockchain data-sharing with patient-centric privacy controls.

Global Blockchain In Healthcare Market Report Scope

Blockchain in healthcare can help complex transactions, such as clinical supply chains and value-based reimbursements, bring transparency between several stakeholders. Considering the fast growth toward the development of more efficient and new healthcare record systems, medical examination systems, and wearable devices, cryptography is expected to be an integral part of the entire healthcare industry in the future. With the increased number of patients globally, managing health-related data is becoming a bottleneck for healthcare providers.

The Blockchain Market in Healthcare can be segmented by Application (Clinical Data Exchange, Billing Management and Claims Adjudication, and Supply Chain Management) and Geography (North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa).

The market sizes and forecasts are provided in terms of value (in USD million) for all the above segments.

| Clinical Data Exchange |

| Billing and Claims Adjudication |

| Supply-Chain and Provenance |

| Clinical Trials and Consent Mgmt |

| Providers (Hospitals, Clinics) |

| Payers and PBMs |

| Pharma / Med-tech Manufacturers |

| Patients and Health-Data Brokers |

| Private / Permissioned |

| Consortium |

| Public |

| North America | United States |

| Canada | |

| South America | Brazil |

| Argentina | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Russia | |

| Asia-pacific | China |

| Japan | |

| India | |

| Middle East and Africa | GCC |

| South Africa |

| By Application | Clinical Data Exchange | |

| Billing and Claims Adjudication | ||

| Supply-Chain and Provenance | ||

| Clinical Trials and Consent Mgmt | ||

| By End-User | Providers (Hospitals, Clinics) | |

| Payers and PBMs | ||

| Pharma / Med-tech Manufacturers | ||

| Patients and Health-Data Brokers | ||

| By Blockchain Type | Private / Permissioned | |

| Consortium | ||

| Public | ||

| By Geography | North America | United States |

| Canada | ||

| South America | Brazil | |

| Argentina | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Asia-pacific | China | |

| Japan | ||

| India | ||

| Middle East and Africa | GCC | |

| South Africa | ||

Key Questions Answered in the Report

What is the current size of the blockchain in healthcare market?

The blockchain in healthcare market reached USD 8.27 billion in 2026.

How fast is the blockchain in healthcare market expected to grow?

The market is forecast to grow at a 50.38% CAGR, hitting USD 63.58 billion by 2031.

Which application segment holds the largest share?

Clinical Data Exchange led with 45.40% market share in 2025.

What drives blockchain adoption among payers?

Smart-contract adjudication reduces duplicate claims and cuts administrative costs by up to 40% for insurers.

Why is Asia-Pacific the fastest-growing region?

Government-backed digital-health programs and revised medical laws in China, Japan, and India are propelling a 61.18% regional CAGR.

Which blockchain type is preferred in healthcare?

Private/Permissioned networks dominate with 62.30% share, though consortium models are expanding fastest at a 66.93% CAGR.

Page last updated on: