Butylated Triphenyl Phosphate Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 29.61 Million |

| Market Size (2031) | USD 35.15 Million |

| Growth Rate (2026 - 2031) | 3.49% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

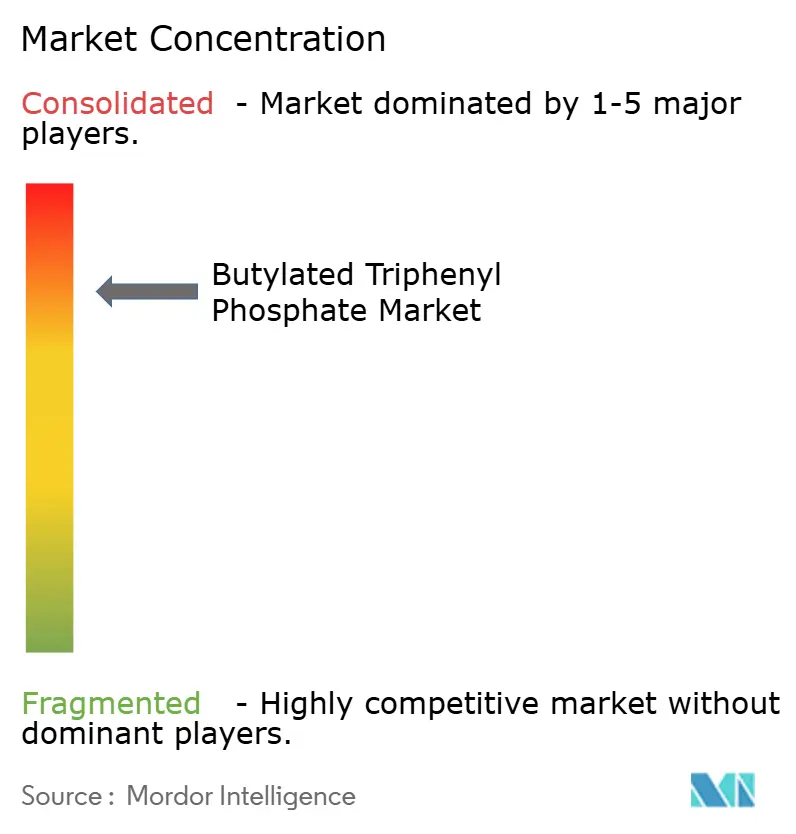

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Butylated Triphenyl Phosphate Market Analysis by Mordor Intelligence

The Butylated Triphenyl Phosphate market size is expected to grow from USD 28.61 million in 2025 to USD 29.61 million in 2026 and is forecast to reach USD 35.15 million by 2031 at 3.49% CAGR over 2026-2031. Demand is rising because regulators in North America and Europe are phasing out halogenated flame retardants, while industrial users look for safer additives that still deliver high thermal stability. Raw-material price swings in phenol and phosphorus oxychloride continue to squeeze margins, yet manufacturers are investing in process efficiency and backward integration to protect profitability. Asia-Pacific retains a leading supply position thanks to an integrated feedstock base, and producers in Japan and South Korea are scaling capacity to serve premium aerospace and electronics lines. Intensifying interest in safe lithium-ion battery chemistries has opened a fast-growing niche that rewards suppliers able to meet both safety and electrochemical performance targets. Consolidation, such as LANXESS’s purchase of Chemtura, shows that the Butylated Triphenyl Phosphate market is moving toward scale-driven competition even as start-ups explore bio-based routes.

Key Report Takeaways

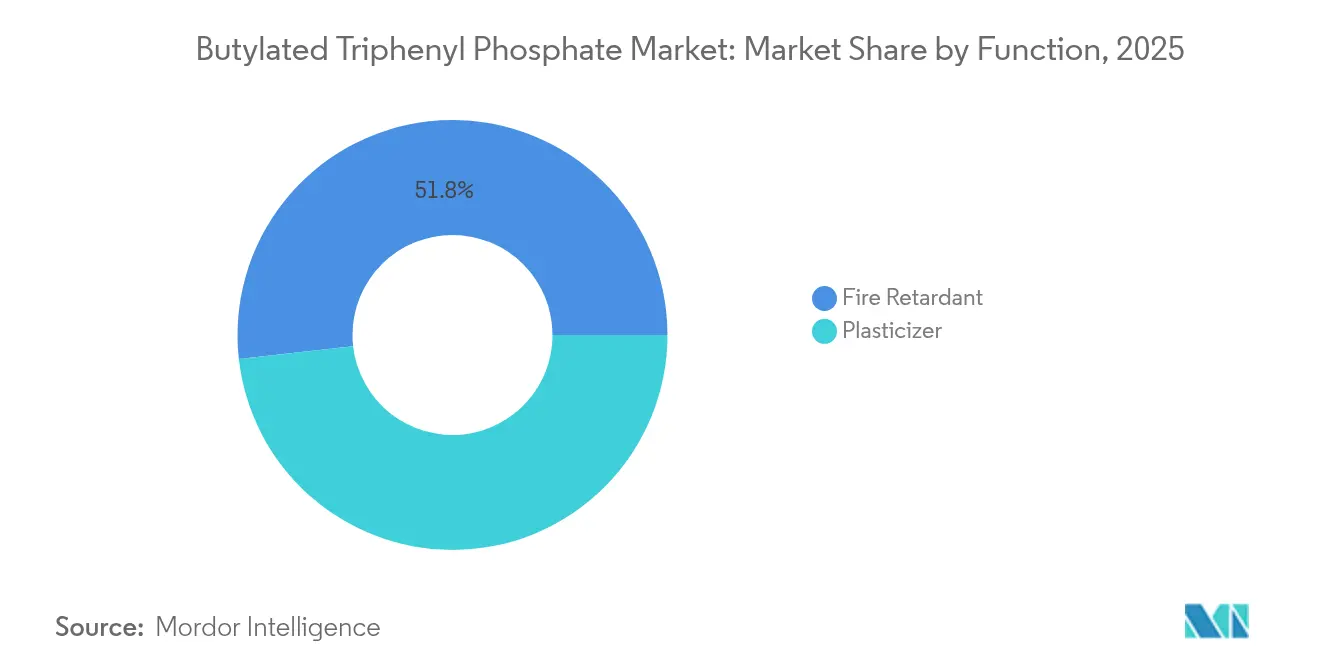

- By function, flame retardants led with 51.78% revenue share in 2025, while lubricant and hydraulic additives are forecast to post the fastest 4.84% CAGR through 2031.

- By application, PVC compounds and resins accounted for 39.10% of the Butylated Triphenyl Phosphate market share in 2025; photovoltaics and energy storage are projected to grow at a 5.23% CAGR to 2031.

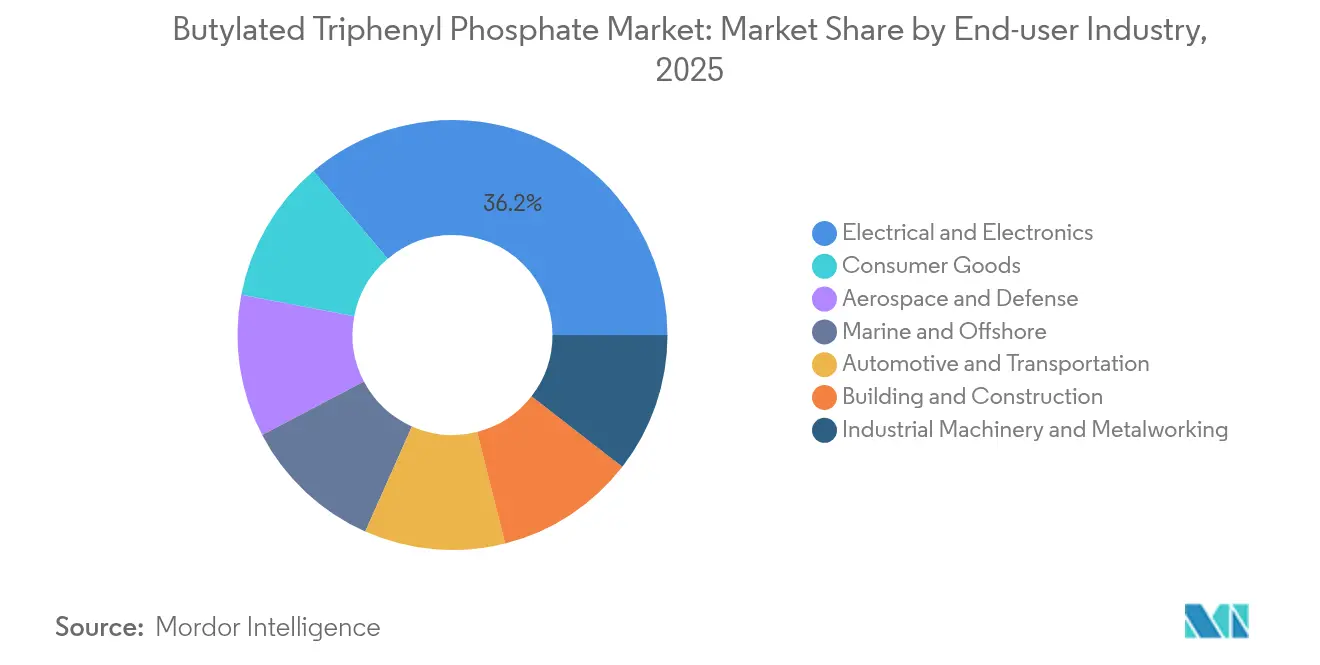

- By end-user industry, electrical and electronics dominated at 36.20% share in 2025, whereas aerospace and defense are set to record the highest 5.42% CAGR to 2031.

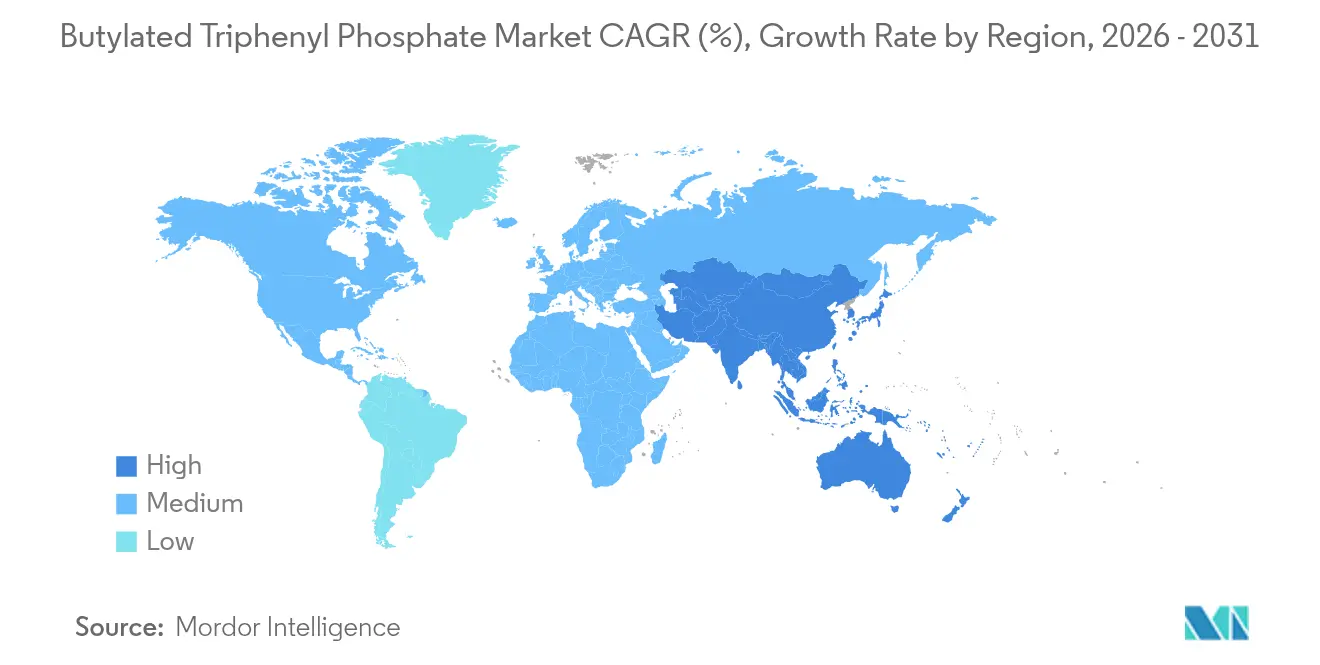

- By geography, Asia-Pacific held 38.10% of the Butylated Triphenyl Phosphate market size in 2025, and the region is poised to expand at a 4.10% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Butylated Triphenyl Phosphate Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory phase-out of halogenated flame retardants | +1.2% | Global, with early adoption in North America and EU | Medium term (2-4 years) |

| Surging demand for fire-resistant lubricants and hydraulic fluids | +0.8% | APAC core, spill-over to North America | Long term (≥ 4 years) |

| Rapid growth of flexible PVC in construction and wire-cable | +0.6% | Asia-Pacific, Middle East emerging markets | Medium term (2-4 years) |

| Safety-driven uptake in automotive and aerospace interiors | +0.5% | Global, with a concentration in automotive hubs | Short term (≤ 2 years) |

| Adoption in high-voltage Li-ion battery electrolytes | +0.4% | APAC manufacturing centers, North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Regulatory Phase-Out of Halogenated Flame Retardants

Comprehensive bans now enforce tight compliance deadlines in several jurisdictions. New York’s restriction on flame retardants in furniture and electronic displays took effect in December 2024, while the United States EPA updated its Persistent, Bioaccumulative and Toxic Chemicals rule in November 2024 to curb decabromodiphenyl ether and allied compounds[1]United States Environmental Protection Agency, “Final Rule to Manage Persistent, Bioaccumulative, and Toxic Chemicals,” epa.gov. Canada added further substances to its Schedule 1 toxic list in February 2025, intensifying reformulation pressure. As manufacturers re-engineer product lines simultaneously across regions, short-term demand spikes emerge for compliant organophosphorus alternatives. Electronics and furniture suppliers face the most urgent deadlines, whereas industrial users still enjoy longer transition windows that spread procurement over several years. Companies able to guarantee consistent quality and documentation earn preferred-supplier status.

Surging Demand for Fire-Resistant Lubricants and Hydraulic Fluids

High-temperature machinery in metalworking, mining, and offshore platforms increasingly specifies flame-retardant lubricants to lower insurance costs and meet stricter safety audits. Perimeter Solutions’ 2024 SEC filing underscored the role of phosphorus pentasulfide in anti-wear additives that raise lubricant flash points. Asian steel mills and shipyards are major adopters because confined spaces magnify fire risk. Although premium prices slow uptake in cost-sensitive segments, buyers cite lower downtime and regulatory compliance as compelling benefits. Suppliers who provide in-house testing data and rapid technical support shorten customer qualification cycles. Long-term growth is expected to align with the build-out of renewable power plants, which run at elevated operating temperatures.

Rapid Growth of Flexible PVC in Construction and Wire-Cable

Urban infrastructure investment across China, India, and Southeast Asia fuels robust consumption of flame-retarded PVC sheet, conduit, and cable. Studies show that optimized butylated triphenyl phosphate loadings push the limiting oxygen index of PVC above 50%, doubling fire resistance without sacrificing tensile strength. Green-building certifications now favor halogen-free materials, prompting compounders to refine formulations that balance cost against new safety targets. Wire-and-cable remains the fastest sub-segment as smart buildings and renewable installations call for tight flame and smoke standards. Yet formulation complexity adds research and development cost and lengthens product rollouts, prompting end-users to lock in multi-year supply contracts once validation is complete.

Safety-Driven Uptake in Automotive and Aerospace Interiors

Vehicle interiors, especially in electric models, present new thermal profiles that raise concern over cabin fires. Consumer NGOs highlight that many cars still contain carcinogenic flame retardants, encouraging automakers to pivot toward lower-toxicity phosphate esters. In aerospace, the FAA mandates stringent burn-through resistance for insulation and panels[2]Federal Aviation Administration, “Fire Test Procedures for Aircraft Materials,” faa.gov . Combined with ongoing fleet renewal, demand for certified additives has climbed. Certification processes remain lengthy, but once qualified, materials lock in for a platform’s entire life cycle. This creates stable, high-margin streams for suppliers able to navigate aviation audit protocols.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Toxicological and eco-tox concerns driving stricter regulations | -0.9% | Global, with stricter enforcement in developed markets | Medium term (2-4 years) |

| Volatile prices of phenol and phosphorus oxychloride feedstocks | -0.7% | Global supply chains, concentrated in Asia-Pacific | Short term (≤ 2 years) |

| Equipment corrosion and hydrolysis maintenance costs in lubricant circuits | -0.4% | Industrial applications globally, concentrated in marine and offshore | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Toxicological and Eco-Tox Concerns Driving Stricter Regulations

Peer-reviewed work in 2025 confirmed that organophosphate flame retardants can disrupt endocrine, hepatic, and neurological functions. Washington State enacted rules in 2025 that presume intentional addition if organophosphate flame retardants appear above specific thresholds. Regulators indicate that organophosphates could follow the same tightening path as halogenated products, injecting uncertainty into long-term planning. Brands are therefore funding trials of bio-based or polymeric substitutes that cannot migrate out of end products. While this trend caps growth for legacy chemistries, it creates headroom for innovation among suppliers that can demonstrate reduced toxicity without compromising performance.

Volatile Prices of Phenol and Phosphorus Oxychloride Feedstocks

Energy cost swings and geopolitical friction drive sharp changes in benzene and chlorine derivatives, pushing phenol and phosphorus oxychloride quotations higher and widening spreads between contract and spot markets. Asian producers dominate these intermediates, so freight rates and currency shifts amplify volatility. Sudden cost spikes compress margins because downstream buyers resist instant pass-throughs. To mitigate risk, leading producers negotiate index-linked formulas, hedge raw-material exposure and invest in captive phenol capacity. Long-term offtake agreements with consumer-electronics majors also stabilize production planning despite short-term price shocks.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Function: Lubricant Applications Drive Growth Despite Flame Retardant Dominance

The flame-retardant function captured 51.78% of the Butylated Triphenyl Phosphate market share in 2025, a position cemented by mandatory fire-safety codes in furniture, electronics, and construction. Growth, however, shifts toward lubricant and hydraulic additive roles, which are forecast to expand at 4.84% through 2031 as factories modernize and safety audits intensify. The Butylated Triphenyl Phosphate market size tied to lubricant uses is poised to widen because high-temperature equipment and offshore platforms insist on fluid that self-extinguishes quickly. Leading suppliers tailor phosphorus content and viscosity modifiers to meet OEM equipment standards, and they bundle technical guidance that shortens plant trials from months to weeks.

By Application: Energy Storage Emerges as High-Growth Segment

PVC compounds and resins accounted for 39.10% of the Butylated Triphenyl Phosphate market size in 2025 as builders across Asia-Pacific sought cables, conduits, and flooring that pass updated flame-spread tests. Photovoltaics and energy-storage systems are projected to post a 5.23% CAGR to 2031, the fastest among all applications, because BIPV panels and lithium-ion batteries must meet rigorous fire codes. Experiments show that only 3 wt% of triphenyl phosphate in electrolytes can arrest flame propagation without hurting cell capacity. Module makers, therefore, secure multi-year supply pacts to ensure chemistry consistency through certification cycles.

By End-User Industry: Aerospace Growth Outpaces Electronics Leadership

Electronics retained 36.20% of the Butylated Triphenyl Phosphate market in 2025, with every household device from televisions to routers requiring flame-retarded plastics. Still, aerospace and defense display the quickest 5.42% CAGR through 2031 as airline fleets modernize with composite-rich cabins that necessitate high-performance flame retardants. New insulation standards mandate additives that survive burn-through at 1100 °C for four minutes, thresholds met by organophosphorus esters but seldom by halogenated systems.

Automotive interiors form another sizeable user group, especially as electric models call for revised thermal management strategies. While some jurisdictions lack updated flammability statutes, automakers adopt safer chemistries voluntarily to pre-empt reputational risk. Construction maintains a steady baseline driven by urbanization, though green-building labels prefer halogen-free solutions that can boost formulation cost. Industrial machinery rounds out demand by embracing flame-retardant hydraulic fluids, yet volume upside is tempered by the slow replacement cycle of heavy equipment. Consumer goods remain the smallest slice but operate under the strictest scrutiny, as recreational foams now face additive bans in several US states.

Geography Analysis

Asia-Pacific controlled 38.10% of the Butylated Triphenyl Phosphate market in 2025 and is projected to grow at a 4.10% CAGR through 2031. China anchors regional demand with its electronics manufacturing base and ongoing urban construction that absorbs flame-retarded PVC. Japan and South Korea prioritize aerospace-grade materials, relying on established chemical clusters for phenol and phosphorus intermediates.

North America is buoyed by early regulatory moves that accelerate substitution. New York’s product ban that began in December 2024 set a high bar, while Canada’s February 2025 toxic-substances listing reinforced momentum toward organophosphates. Europe traces a flatter trajectory because the region already enforces the world’s strictest chemical rules. Producers pivot to bio-based and polymeric options, illustrated by ALTANA AG’s equity stake in Finnish innovator NORDTREAT.

South America and the Middle-East, and Africa remain emerging pockets, where infrastructure build-outs create fresh demand, yet regulatory enforcement remains nascent. Multinationals usually serve these territories via imports to avoid over-investment until policy clarity improves.

Competitive Landscape

The Butylated Triphenyl Phosphate market features consolidation. Innovation tilts toward PFAS-free and bio-derived molecules. Suppliers also experiment with reactive or polymeric grades that lock into plastic matrices, curbing leaching and environmental exposure. Raw-material volatility spurs backward-integration moves, with some players investing in captive phenol units or long-term phosphorus ore contracts to hedge cost swings. Customer stickiness remains high because qualification in safety-critical markets can exceed 18 months, raising switching barriers and fostering long contracts.

Butylated Triphenyl Phosphate Industry Leaders

LANXESS

ICL

PCC Group

Radco Industries, Inc.

Tina Organics ( P ) Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2024: The European Union imposed anti-dumping duties on certain alkyl phosphate esters, including BTPP, imported from China, affecting pricing strategies across the region.

- January 2023: ICL Group released a new eco-friendly BTPP formulation boasting improved thermal stability for electronics applications.

Global Butylated Triphenyl Phosphate Market Report Scope

The Butylated Triphenyl Phosphate Market report include:

| Fire Retardant |

| Plasticizer |

| Lubricants |

| Polyvinyl Compounds and Resins |

| Other Applications (Engineering Plastics, Coatings and Adhesives, etc.) |

| Automotive and Transportation |

| Aerospace and Defense |

| Electrical and Electronics |

| Building and Construction |

| Industrial Machinery and Metalworking |

| Marine and Offshore |

| Consumer Goods |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Function | Fire Retardant | |

| Plasticizer | ||

| By Application | Lubricants | |

| Polyvinyl Compounds and Resins | ||

| Other Applications (Engineering Plastics, Coatings and Adhesives, etc.) | ||

| By End-user Industry | Automotive and Transportation | |

| Aerospace and Defense | ||

| Electrical and Electronics | ||

| Building and Construction | ||

| Industrial Machinery and Metalworking | ||

| Marine and Offshore | ||

| Consumer Goods | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the current size of the Butylated Triphenyl Phosphate market?

The Butylated Triphenyl Phosphate market size is USD 29.61 million in 2026 and is forecast to rise to USD 35.15 million by 2031 at a 3.49% CAGR.

Which region leads demand for Butylated Triphenyl Phosphate?

Asia-Pacific holds 38.10% of global demand and is projected to grow at a 4.10% CAGR through 2031, driven by electronics manufacturing and construction activity.

Which application segment is expected to grow the fastest?

Photovoltaics and energy storage applications show the highest projected 5.23% CAGR because building-integrated PV and lithium-ion batteries require stricter fire-safety additives.

Why are lubricants an emerging opportunity in this market?

Industrial equipment and offshore platforms specify fire-resistant fluids to meet evolving safety codes, pushing lubricant and hydraulic additive demand to a 4.84% CAGR.

How are regulations shaping the competitive landscape?

Bans on halogenated flame retardants and tighter scrutiny of organophosphates force suppliers to invest in safer, often bio-based chemistries, favoring companies with strong regulatory and research and development capabilities.

Page last updated on: