Bacterial Biopesticides Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

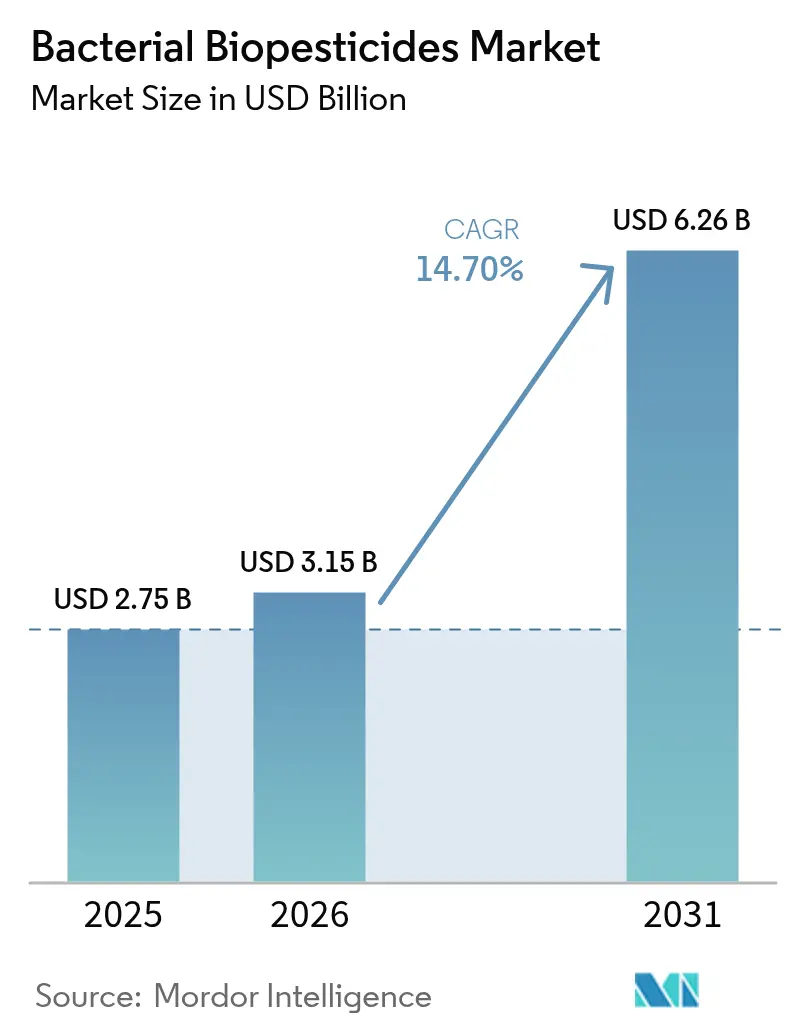

| Market Size (2026) | USD 3.15 Billion |

| Market Size (2031) | USD 6.26 Billion |

| Growth Rate (2026 - 2031) | 14.70% CAGR |

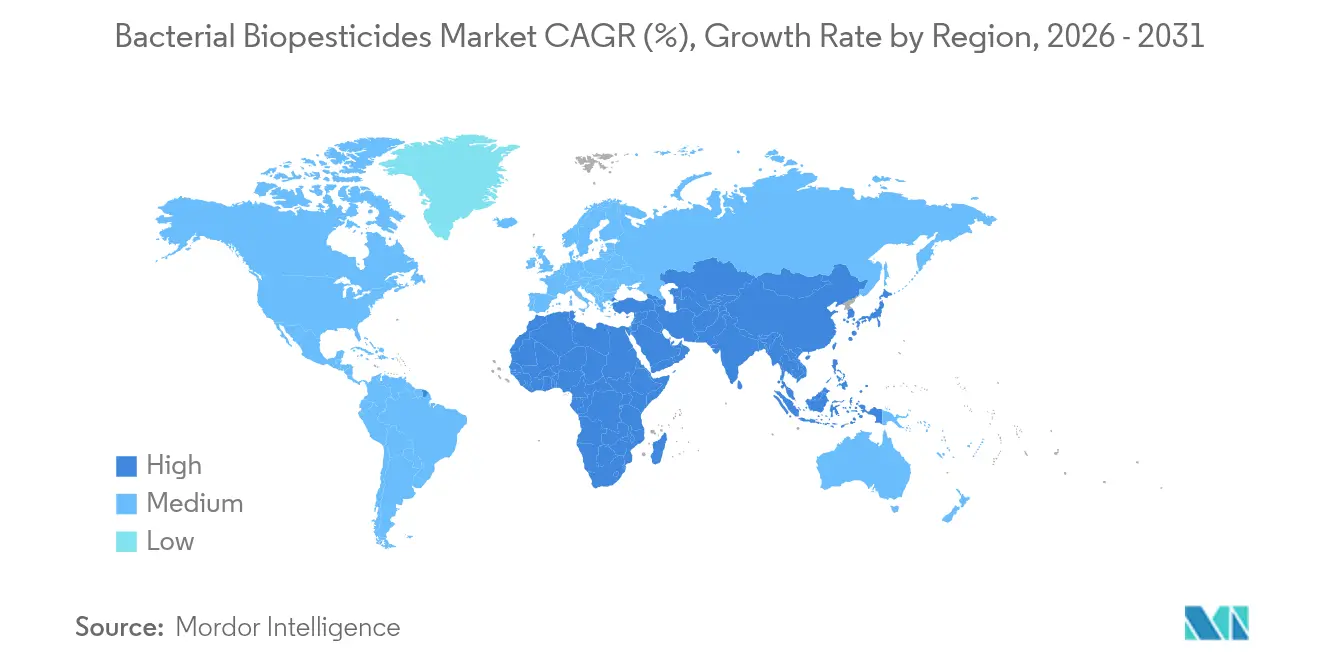

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

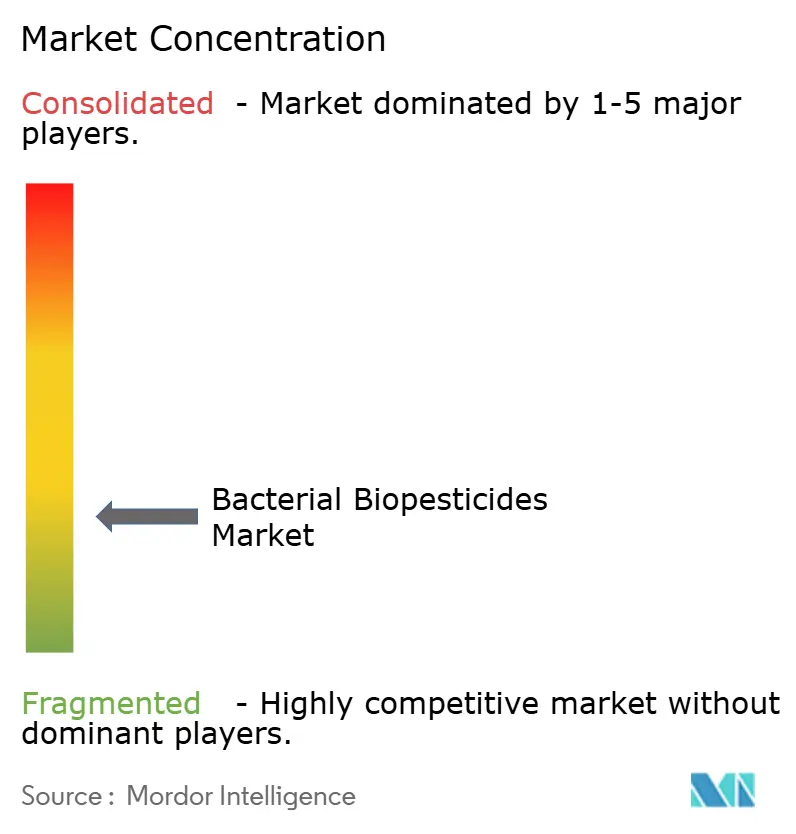

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Bacterial Biopesticides Market Analysis by Mordor Intelligence

The Bacterial Biopesticides market size is expected to grow from USD 2.75 billion in 2025 to USD 3.15 billion in 2026 and is forecast to reach USD 6.26 billion by 2031 at 14.70% CAGR over 2026-2031. The market growth is driven by expedited regulatory approvals, increasing consumer demand for residue-free produce, expansion of organic farming, and technological advancements that enhance formulation stability and field efficacy. According to FiBL, the global organic farming area reached 98.9 million hectares in 2023, representing a 2.6% increase. Bacillus thuringiensis (Bt) dominates the market with a 74% revenue share, while Bacillus subtilis shows rapid growth due to its combined pest control and plant growth promotion capabilities. Precision seed treatment applications, liquid formulations for controlled-environment agriculture, and the consolidation of portfolios among major agrochemical companies support the market expansion. Adoption rate of the bacterial biopesticides is affected by cold-chain storage requirements and slower efficacy compared to chemical alternatives, as companies work to address these challenges in an increasingly competitive market.

Key Report Takeaways

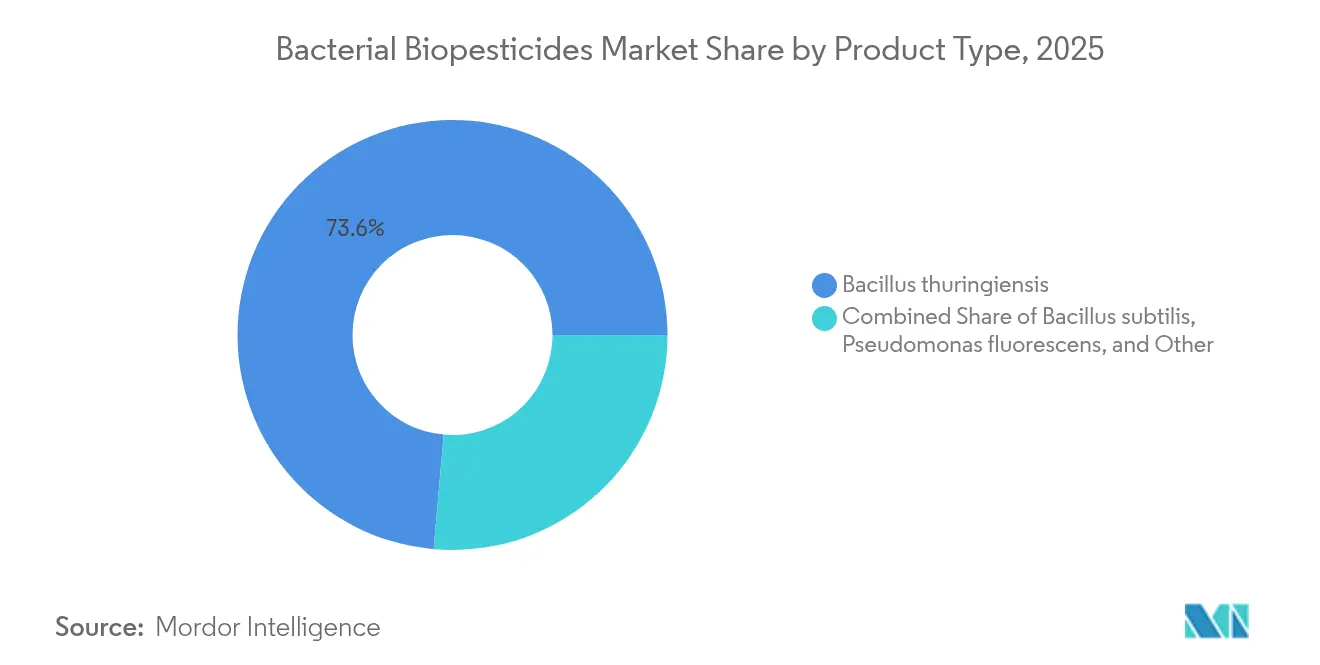

- By product type, Bacillus thuringiensis held 73.60% of the bacterial biopesticides market share in 2025; Bacillus subtilis is positioned to grow at a 16.50% CAGR through 2031.

- By mode of application, foliar sprays led with 44.30% revenue contribution in 2025; seed treatment is forecast to expand at a 16.20% CAGR between 2026 and 2031.

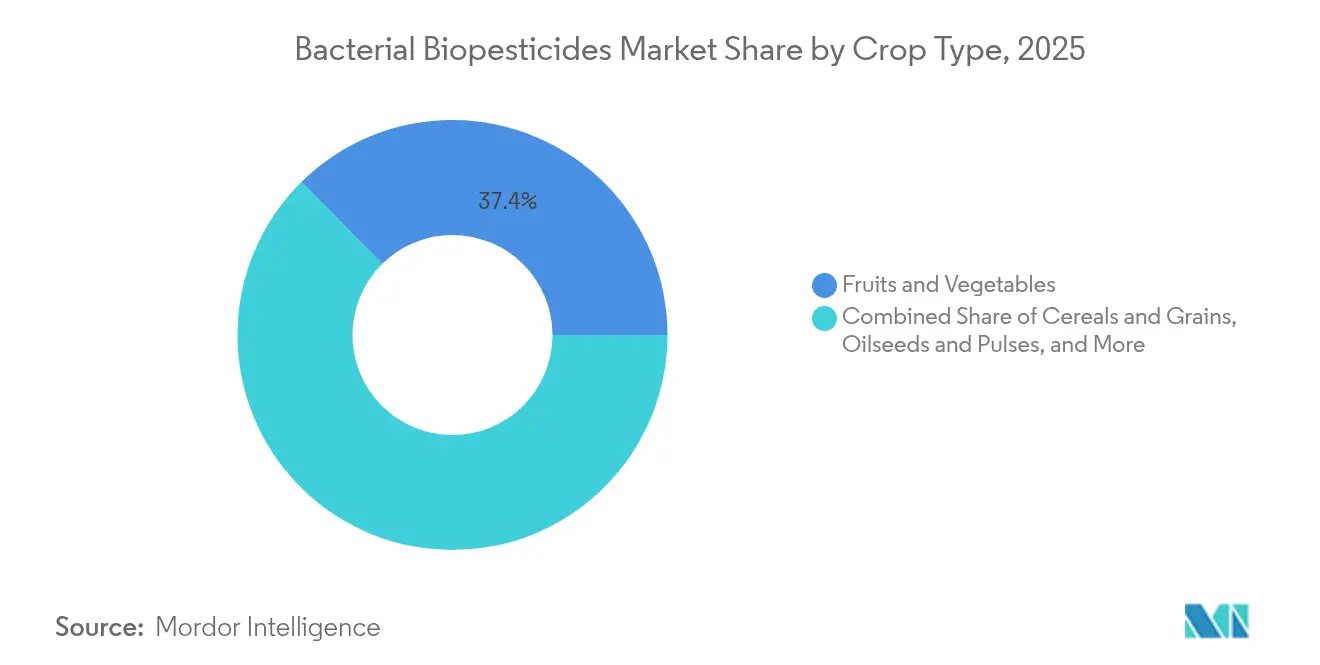

- By crop type, fruits and vegetables accounted for 37.40% share of the bacterial biopesticides market size in 2025, whereas cereals and grains are projected to rise at a 15.10% CAGR to 2031.

- By region, North America represented 37.50% of global sales in 2025, while Asia-Pacific is set to register the fastest 17.40% CAGR over the forecast horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Bacterial Biopesticides Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory and Policy Support | +2.8 | Global, with strongest influence in EU and North America | Medium term (~ 3-4 yrs) |

| Rising Awareness of the Harms of Conventional Pesticides | +1.9 | Global, particularly pronounced in Europe and North America | Medium term (~ 3-4 yrs) |

| Demand for residue-free produce driving Bt solutions | +2.4 | Global, with early adoption in developed markets | Short term (≤ 2 yrs) |

| Expansion of controlled-environment agriculture boosting demand for liquid bacterial formulations | +3.1 | North America, Europe, and urban centers in Asia-Pacific | Long term (≥ 5 yrs) |

| Increasing adoption of integrated pest management (IPM) strategies | +2.3 | Global, with highest impact in regions with strong agricultural extension services | Medium term (~ 3-4 yrs) |

| Technological advancements in formulation and delivery systems | +2.7 | Global, with initial adoption in developed agricultural markets | Medium term (~ 3-4 yrs) |

| Source: Mordor Intelligence | |||

Regulatory and Policy Support

The European approval process for biopesticides has reduced from nine years to approximately three years, addressing a backlog of over 100 pending substances. The European Commission intends to implement new EU regulations in 2025 to optimize biopesticide approval processes by Q4. The 2026 Biotech Act will focus on filling current regulatory gaps. Brazil has demonstrated similar progress by approving bio-insecticidal products derived from inactivated Burkholderia cells. The United States Environmental Protection Agency (EPA) is reducing application backlogs under FIFRA (Federal Insecticide, Fungicide, and Rodenticide Act). [3]United States EPA, “Guidance for Expedited Review of Biopesticides,” epa.gov These regulatory changes expand registration opportunities, reduce compliance costs, and enable smaller companies to enter the bacterial biopesticides market.

Rising Awareness of the Harms of Conventional Pesticides

Research demonstrating biodiversity loss and soil degradation from synthetic pesticides influences purchasing decisions in premium retail channels. A 2025 Massachusetts Institute of Technology study revealed that 31% of global agricultural soils faced high risks from pesticide contamination. North American and European retailers implement strict residue limits, favoring zero-residue biological products. As growers adapt to these requirements, bacterial agents have evolved from organic-only solutions to essential components of integrated pest management programs. This transition drives growth in the bacterial biopesticides market, especially for crops with short pre-harvest intervals.

Demand for Residue-Free Produce Driving Bt Solutions

Bacillus thuringiensis (Bt) protein's mode of action leaves no chemical residue, making it compliant with export maximum residue limits. Bt holds 74% of the bacterial biopesticides market due to its proven field effectiveness. New microencapsulated formulations enable their use in high-temperature regions and extend storage duration. Recent developments in UV-stable formulations allow applications beyond traditional evening spray periods, reinforcing Bt's dominant market position.

Expansion of Controlled-Environment Agriculture Boosting Liquid Formulations

The expansion of vertical farms and high-technology greenhouses has increased the demand for inputs that provide consistent results in controlled environments. China leads this expansion, accounting for 60% of global greenhouse facilities in 2024, according to NASA Earth Observatory. Liquid bacterial formulations are well-suited for these operations, as they can be administered through fertigation lines and misting systems. Recent developments in shelf-life technology, including a biobased carrier that maintains Gram-negative microbe viability for 540 days, have reduced storage costs and enabled market expansion in metropolitan areas. The parallel growth of controlled environment agriculture (CEA) and bacterial inputs creates a cycle that drives the bacterial biopesticides market forward.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cold-chain logistics limiting shelf-life of Biological biopesticides | -1.7 | Global, most severe in tropical regions and developing markets | Short term (≤ 2 yrs) |

| Production and Formulation Challenges | -1.2 | Global, with varying impact based on technological capabilities | Medium term (~ 3-4 yrs) |

| Perceived slower knock-down reducing adoption in farms | -2.1 | Global, particularly in regions with high pest pressure | Short term (≤ 2 yrs) |

| Higher costs compared to conventional pesticides | -1.9 | Global, most significant in price-sensitive markets and field crops | Medium term (~ 3-4 yrs) |

| Source: Mordor Intelligence | |||

Cold-Chain Logistics Limiting Shelf-Life of Biologicals

Live spore formulations typically lose viability at temperatures above 25°C, necessitating refrigerated transport and storage, which increases the final cost. This challenge is particularly significant in equatorial markets where small-scale distribution networks lack temperature-controlled storage facilities. While new encapsulation technologies are improving cell viability at room temperature and reducing distribution constraints, the processes for scale-up and regulatory approval require multiple growing seasons. These logistical limitations restrict market penetration, reducing the competitiveness of bacterial biopesticides against chemical pesticides that offer extended shelf life and minimal storage requirements.

Perceived Slower Knock-Down Reducing Adoption in Farms

Chemical insecticides typically eliminate pests within hours, while bacterial agents require several days, which makes growers hesitant to use them for immediate pest control. Field demonstrations combining bacterial products with selective chemicals in integrated pest management programs are changing this perception. Current research focuses on developing bacterial strains that produce higher toxin levels and complementary microbial combinations to achieve faster pest mortality while maintaining a residue-free status.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Bt Dominance and Emerging Multifunctionals

Bt accounted for 73.60% of 2025 revenue, maintaining its dominant position in the bacterial biopesticides market. This market leadership stems from its targeted toxicity against lepidopteran larvae, extensive organic certifications, and regulatory acceptance worldwide. The market size for Bt products is projected to expand due to new encapsulation technologies that improve field persistence in high-UV conditions. A 2024 study confirmed Bt toxins' effectiveness against lepidopteran, coleopteran, hemipteran, dipteran, and nematode pests.

Bacillus subtilis shows strong growth potential with a projected 16.50% CAGR, driven by its dual benefits of disease suppression and plant growth promotion, particularly in high-value horticulture. Pseudomonas fluorescens has established its role in controlling soil-borne pathogens, while Serratia and Streptomyces species are gaining traction in specialized applications through their chitinase activity and antibiotic metabolite production capabilities.

By Mode of Application: From Foliar Dominance to Seed-Centric Delivery

Foliar sprays accounted for 44.30% market share in 2025, driven by their flexibility in-season application across multiple crops and compatibility with conventional spraying equipment. The seed treatment segment is anticipated to grow at a 16.20% CAGR, supported by advances in polymer coatings and dormant spore technologies that maintain bacterial viability during storage and early germination phases. This approach integrates protection from the initial growth stage, reducing application requirements and increasing bacterial biopesticides adoption in seed applications. In 2024, the ICAR-Indian Institute of Oilseeds Research (IIOR) developed a biopolymer-based seed coating technology that preserves nutrient-mobilizing microbes, including microbial bio-agents used in biopesticides. This development improves microbial survival, increases crop yields by 25-30%, and enhances resilience under adverse climate conditions.

Soil drench applications remain important for growers managing nematodes and root diseases that are not effectively controlled by foliar applications. Post-harvest dip treatments serve a specialized role in extending shelf life for fresh produce supply chains seeking chemical-free alternatives. The diversity of application methods provides manufacturers with multiple revenue streams and reduces seasonal revenue fluctuations.

By Crop Type: Specialty Crops Maintain Lead, Broadacre Gains Pace

Fruits and vegetables accounted for 37.40% of revenue in 2025, driven by premium pricing, short harvest cycles, and strict retailer residue requirements. The bacterial biopesticides market for this segment continues to grow with increasing greenhouse cultivation and export volumes. According to the Environmental Working Group (EWG) Dirty Dozen list, strawberries show the highest contamination, with 99% of samples containing pesticide residues. Spinach, kale, mustard greens, collard greens, and grapes also demonstrate significant contamination, with some containing more than 100 different pesticides.

The broadacre cereals and grains segment is anticipated to grow at a 15.10% CAGR. Decreasing formulation costs and efficient aerial application of liquid concentrates, covering thousands of hectares daily, make bacterial biopesticides economically viable for staple crops. The market expansion extends to oilseeds, pulses, and turf segments, driven by sustainability requirements and environmental concerns in urban areas.

Geography Analysis

North America maintained its dominant position with a 37.50% share of the 2025 global revenue. The United States drives market volumes through widespread integration of bacterial solutions in large-scale corn and soybean operations. Canadian greenhouse clusters strengthen regional demand by utilizing liquid inoculants compatible with hydroponic fertigation systems. In 2023, Canada's 920 commercial greenhouse vegetable operations produced 802,163 metric tons of vegetables, a 7% increase from 2022.

Asia-Pacific demonstrates the strongest growth trajectory with an anticipated 17.40% CAGR through 2031. China's five-year green pest-control plan and India's bio-input subsidy programs encourage domestic production and adoption. Japan and Singapore's vertical farming operations provide established markets for liquid formulations specifically developed for controlled environment agriculture.

Europe maintains strict regulations for biopesticides, though recent changes have accelerated their adoption. The European Commission's 2025 fast-track regulation reduced dossier review times to align with North American standards, enabling more product registrations and encouraging manufacturers to expand their EU product labels. The demand for biopesticides has increased through Scandinavian public procurement policies for school meals and Germany's Farm-to-Fork pesticide reduction targets, particularly benefiting Bt and B. subtilis foliar products. Eastern European grain producers have initiated Bacillus-based seed treatment trials in response to export markets' stricter residue requirements, expanding beyond traditional high-value horticultural applications.

Competitive Landscape

The bacterial biopesticides market consists of established agrochemical companies and specialized firms. Corteva's 2025 acquisition of Symborg enhanced its fermentation capabilities and expanded its portfolio of patent-protected Bacillus metabolites, indicating that major companies consider biologics as core assets. Bayer utilizes its distribution network to combine Bt sprays with traited seeds, creating integrated solutions that secure retail presence. Certis Biologicals, Valent BioSciences, and Koppert focus on developing fast-acting strains to reduce time-to-efficacy, particularly in markets where chemical pesticides remain the standard.

The market shows significant innovation through increased patent applications for chitinase-rich Streptomyces combinations and nano-emulsion carriers that enhance field durability. Industry collaboration is increasing, with Evonik providing encapsulation polymers to multiple manufacturers, while companies like Pivot Bio license fermentation technology to established seed producers. The main competitive focus for the next five years centers on microencapsulation, synergistic consortia, and metabolite stabilization technologies.

Regulatory differences across regions influence market strategies. Large companies pursue simultaneous registrations in the EU and the US, while smaller firms often begin in South America, where data requirements are less stringent. Companies developing formulations that do not require cold-chain storage can access emerging markets in Sub-Saharan Africa and Southeast Asia. While market consolidation continues, the top five companies maintain less than 80% of combined revenue, creating opportunities for new entrants focusing on specific crops, delivery methods, or regional markets.

Bacterial Biopesticides Industry Leaders

Koppert Biological Systems

BASF SE

Syngenta AG

Valent Biosciences LLC

Novonesis

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2024: IPL Biologicals partnered with AFEPASA to streamline global registrations and accelerate market entry for bacterial biopesticides.

- July 2024: Evonik Industries introduced a novel biobased system for incorporating Gram-negative bacteria into liquid agricultural formulations, demonstrating high microbial viability for up to 540 days and addressing key shelf-life limitations

- May 2024: Bioceres Crop Solutions received regulatory approval in Brazil for three new bio-insecticidal/bio-nematicidal solutions derived from inactivated cells of its proprietary Burkholderia platform, marking the first regulatory endorsement of biological products from fully inactivated microorganisms

- August 2023: FMC India introduced Entazia biofungicide, a biological crop protection product containing Bacillus subtilis, to control bacterial leaf blight in rice. The product strengthens plant defense mechanisms while preserving environmental sustainability. Entazia is compatible with FMC's biostimulants and synthetic fungicides to improve overall plant health.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the bacterial biopesticides market as the global sale of formulated crop-protection inputs in which a live or spore-based bacterium, most commonly Bacillus thuringiensis, Bacillus subtilis or Pseudomonas fluorescens, is the primary active ingredient; values reflect manufacturer revenue from farm-gate products applied to agriculture, horticulture, turf and forestry crops.

Scope Exclusion: The assessment omits biochemical biopesticides, plant-incorporated protectants and custom application service revenues.

Segmentation Overview

- By Product Type

- Bacillus thuringiensis

- Bacillus subtilis

- Pseudomonas fluorescens

- Other Types

- By Mode of Application

- Foliar Spray

- Seed Treatment

- Soil Treatment

- Post-Harvest Treatment

- By Crop Type

- Fruits and Vegetables

- Cereals and Grains

- Oilseeds and Pulses

- Turf and Ornamentals

- Plantation Crops

- By Geography

- North America

- United States

- Canada

- Mexico

- Rest of North America

- South America

- Brazil

- Argentina

- Chile

- Rest of South America

- Europe

- Germany

- France

- United Kingdom

- Spain

- Italy

- Rest of Europe

- Africa

- South Africa

- Egypt

- Rest of Africa

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia

- Rest of Asia-Pacific

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed formulation chemists, regulatory officers, crop advisers and ag-input distributors across North America, Europe, Asia-Pacific and Latin America. These discussions validated typical dose rates, seasonality of demand, shelf-life constraints and average selling prices, filling gaps left by secondary sources and anchoring model assumptions.

Desk Research

We began by parsing trade data from UN Comtrade, crop acreage statistics from FAOSTAT and USDA, and registration lists from the US EPA, EU Pesticide Properties Database and India's CIBRC that map approved bacterial strains and use rates. Insights were supplemented with organic farming surveys by FiBL-IFOAM, peer-reviewed efficacy trials, and company 10-K filings that reveal product mix and pricing. Paid platforms such as D&B Hoovers and Dow Jones Factiva provided sales clues and news flow. The sources mentioned are illustrative; many additional references informed data collection, validation and clarification.

Market-Sizing & Forecasting

A blended top-down and bottom-up approach underpins our model. Top-down reconstruction starts with treated hectare pools, recommended application rates and bacterial penetration ratios, followed by price overlays. Bottom-up checks roll up sampled supplier revenues and distributor audits to refine totals. Key variables feeding the model include organic cultivated area, count of registered bacterial products per country, average Bt price per liter, application frequency and regulatory approval lead times. Multivariate regression links these drivers to historical revenue, and exponential smoothing projects them to 2030, while scenario analysis tests regulatory and weather shocks.

Data Validation & Update Cycle

Outputs pass a three-tier analyst review; variance flags trigger re-contact with respondents, and currency conversions use IMF average yearly rates. Reports refresh annually, with interim updates when major approvals or pest outbreaks materially shift demand.

Why Mordor's Bacterial Biopesticides Baseline Commands Confidence

We observe that published estimates diverge because firms vary product scope, price ladders and refresh cadence.

Key gap drivers include mixing biochemical products with bacterials, assuming rapid Asia uptake before registrations clear, or relying on static Bt prices without channel checks.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 2.75 B (2025) | Mordor Intelligence | - |

| USD 5.59 B (2024) | Global Consultancy A | Broader scope includes biochemicals and nematicides |

| USD 3.20 B (2026) | Industry Journal B | Aggressive Bt adoption rate, limited Asia validation |

| USD 2.59 B (2024) | Regional Consultancy C | Value derived from overall biopesticide share assumption, no primary interviews |

The comparison shows that our disciplined scope setting, variable tracking and yearly refresh deliver a balanced, transparent baseline decision-makers can depend on.

Key Questions Answered in the Report

What is the projected size of the bacterial biopesticides market by 2031?

The market is forecast to hit USD 6.26 billion by 2031, growing at 14.70% annually.

Which bacterial strain currently dominates sales?

Bacillus thuringiensis leads with a 73.60% revenue share, owing to its zero-residue profile and broad regulatory acceptance.

Why is seed treatment the fastest-growing application method?

Advances in polymer coatings and spore dormancy enable bacteria to survive storage and colonize seedlings, driving a 16.20% CAGR for seed treatments.

What regions will see the quickest uptake of bacterial biopesticides?

Asia-Pacific is set to grow at an 17.40% CAGR as China, India, and urban hubs adopt biological inputs to meet sustainability goals.

How are companies addressing cold-chain challenges?

New encapsulation carriers keep microbes viable for more than 500 days at ambient temperatures, reducing the need for refrigerated transport and storage.

Page last updated on: