Antibody Drug Conjugates Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

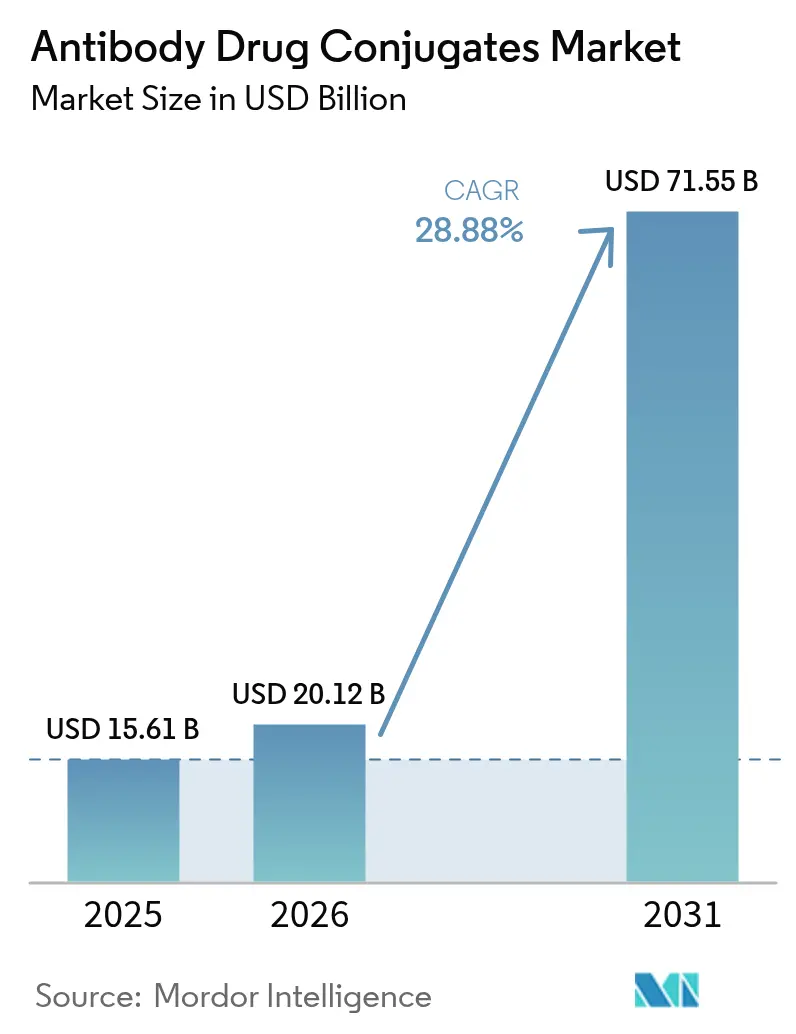

| Market Size (2026) | USD 20.12 Billion |

| Market Size (2031) | USD 71.55 Billion |

| Growth Rate (2026 - 2031) | 28.88% CAGR |

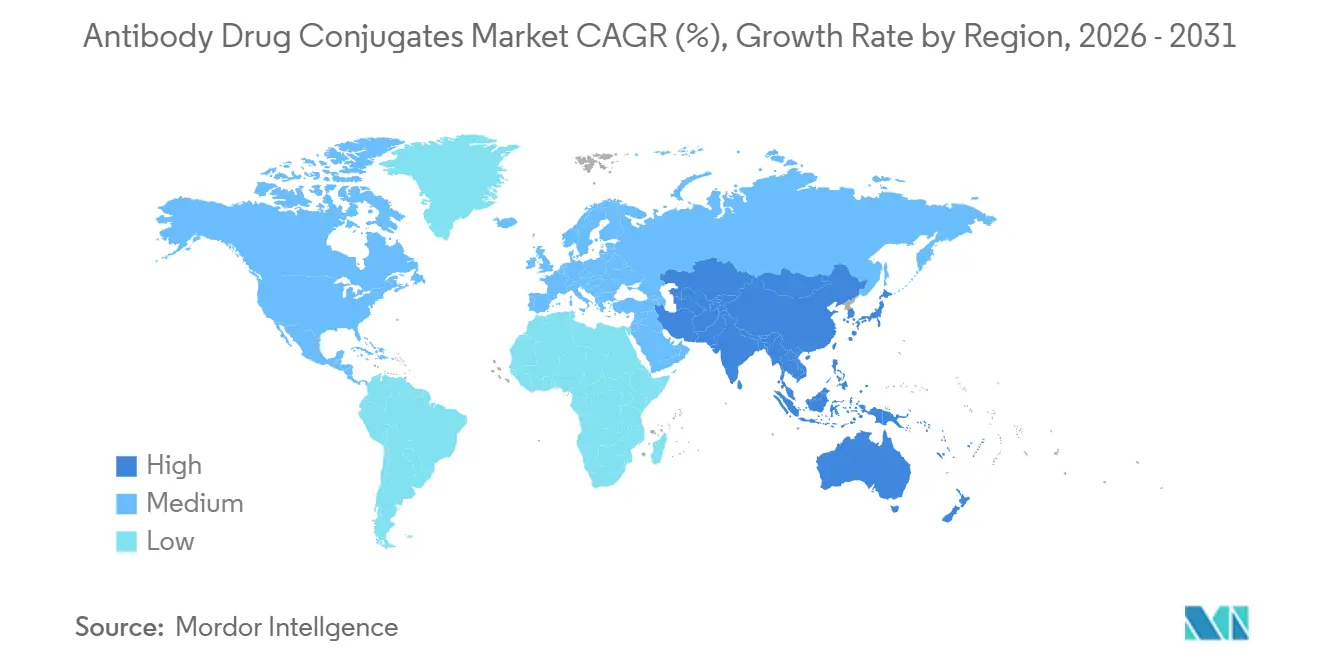

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Antibody Drug Conjugates Market Analysis by Mordor Intelligence

The Antibody Drug Conjugates Market size is expected to grow from USD 15.61 billion in 2025 to USD 20.12 billion in 2026 and is forecast to reach USD 71.55 billion by 2031 at 28.88% CAGR over 2026-2031.

Continued migration away from broad-spectrum chemotherapy toward targeted biologics, faster U.S. regulatory review of drug–antibody ratio and linker stability, and 83 new clinical entrants during 2024 are reshaping oncology treatment pathways. Large-cap acquisitions—Pfizer-Seagen for USD 43 billion and AbbVie-ImmunoGen for USD 10.1 billion—confirm that the Antibody-Drug Conjugates market now represents a core growth pillar for diversified pharmaceutical portfolios. Topoisomerase I inhibitor payloads dominate value creation, while site-specific conjugation platforms such as THIOMAB and glycoengineering improve therapeutic windows and attract premium licensing fees. North America leads global revenue because Medicare covers outpatient ADC infusions and the region houses most payload manufacturing capacity.

Key Report Takeaways

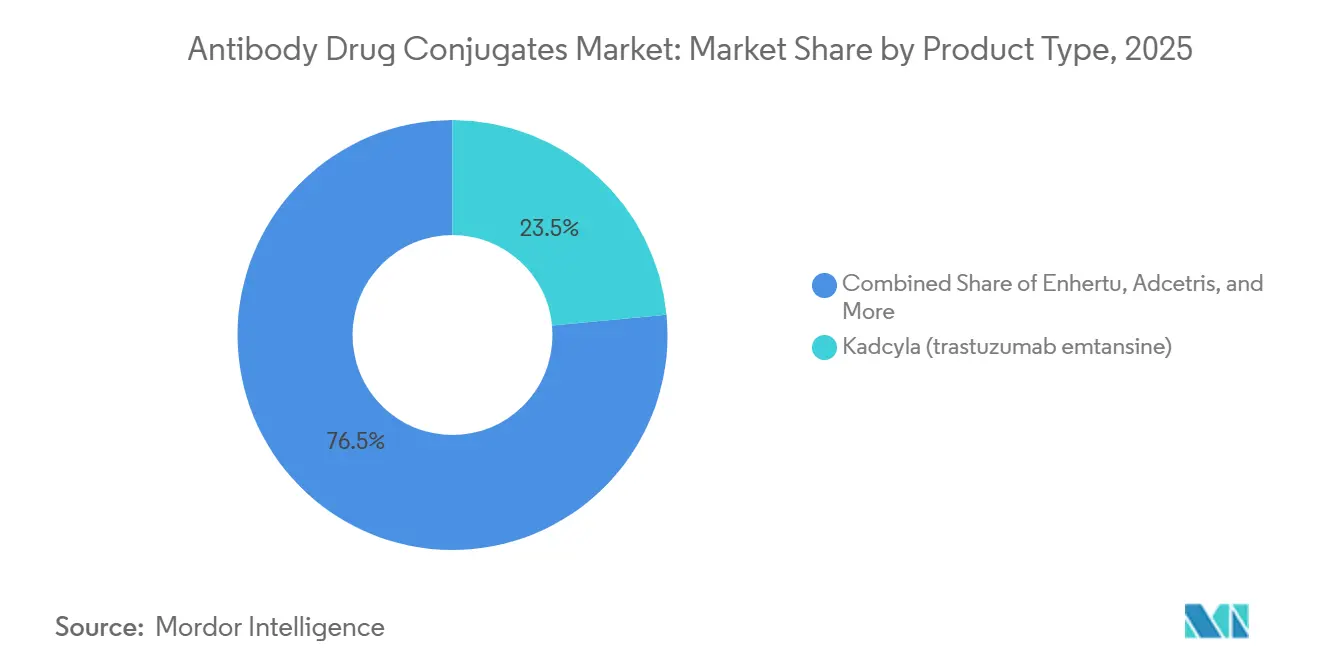

- By product, consumer oncology biologics led with 23.55% revenue share in 2025; Enhertu is projected to expand at a 29.25% CAGR to 2031.

- By payload class, topoisomerase I inhibitors captured 53.53% of the Antibody Drug Conjugates market share in 2025; microtubule inhibitors (MMAE, DM1, DM4) projected to expand at a 30.75% CAGR to 2031.

- By linker chemistry, cleavable linkers accounted for 72.15% share of the Antibody Drug Conjugates market size in 2025 while site-specific platforms are advancing at a 30.82% CAGR through 2031.

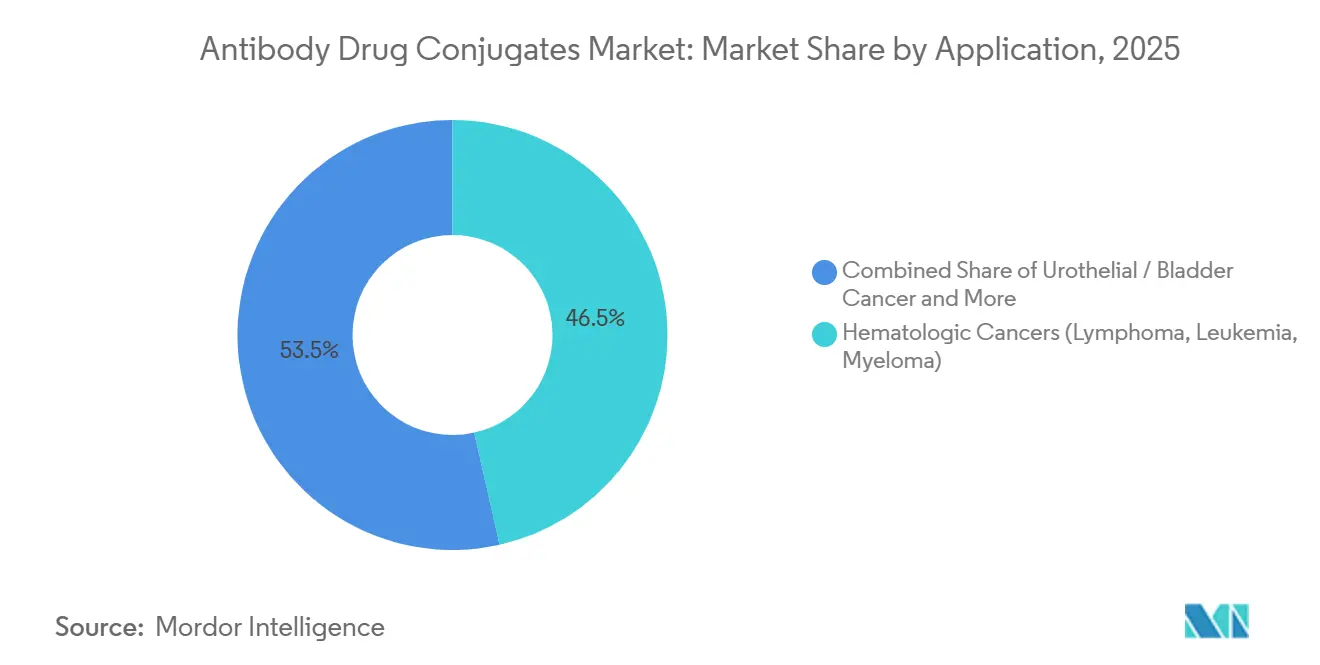

- By application, hematologic cancers held 46.55% share of the Antibody Drug Conjugates market size in 2025 and urothelial indications are rising at a 29.32% CAGR to 2031.

- By end user, hospitals generated 51.55% revenue share in 2025, whereas biopharma and CRO partnerships are the fastest-growing channel at 30.72% CAGR through 2031.

- By geography, North America led with 41.55% revenue share in 2025. Asia-Pacific is set to grow at a 29.22% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Antibody Drug Conjugates Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising incidences of solid tumors | +6.2% | Global, with concentration in North America, Europe, and East Asia | Long term (≥ 4 years) |

| Rapid expansion of ≥65-yr demographic | +5.1% | North America, Europe, Japan | Long term (≥ 4 years) |

| Accelerated R&D funding and clinical trial initiations | +7.3% | Global, led by North America and China | Medium term (2-4 years) |

| Growing pharmaceutical investments | +6.8% | Global, with M&A activity concentrated in North America and Europe | Medium term (2-4 years) |

| Increasing demand for low-toxicity and effective drugs | +4.9% | Global | Long term (≥ 4 years) |

| Reimbursement expansion for outpatient ADC administration | +3.4% | North America, Western Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Incidences of Solid Tumors

Worldwide cancer diagnoses reached 19.96 million in 2022, and models project 35 million annual cases by 2050[1]World Health Organization, “Cancer Data and Statistics,” WHO.int . Breast, lung, and colorectal cancers already anchor ADC approvals yet only 8% of eligible patients received an ADC in 2025, signaling significant headroom for the Antibody-Drug Conjugates market. Lung cancer incidence in China surpassed 800,000 cases in 2024, boosting demand for TROP2- and HER2-targeting conjugates. Solid-tumor heterogeneity spurs development of multi-antigen ADC cocktails, a strategy expected to expand the treatable population by 30% pending regulatory acceptance. Together these forces enlarge the addressable pool for precision payloads and underpin double-digit volume growth through 2031.

Rapid Expansion of ≥65-yr Demographic

The global population aged 65 years and older reached 761 million in 2024 and will exceed 1.5 billion by 2050. Cancer incidence in seniors is ten-fold higher than in younger adults, and geriatric guidelines prefer ADCs because targeted delivery lowers systemic toxicity. Japan, where 29% of citizens were over 65 in 2025, cleared four elderly-focused ADC labels, including Enhertu, which cut hospitalizations by 40% versus chemotherapy. In 2025, Medicare began reimbursing home-based ADC infusions, adding 15,000 new treatment starts annually. These demographic and policy shifts lift utilization across mature health systems and reinforce long-run demand in the Antibody-Drug Conjugates market.

Accelerated R&D Funding and Clinical Trial Initiations

R&D spending on ADC platforms climbed 38% year-on-year to USD 12.4 billion in 2024. As of January 2026, 431 active ADC studies appear on ClinicalTrials.gov, including 83 Phase 3 trials in tumor types beyond breast and hematologic cancers. China’s science foundation earmarked USD 890 million in 2025 for domestic payload innovation, reducing reliance on auristatin imports. FDA Project Optimus mandates dose-optimization studies, trimming median approval cycles from 14 to 10 months. Accelerated capital deployment, global site activation, and regulatory streamlining converge to shorten bench-to-bedside conversion and enlarge the Antibody-Drug Conjugates market.

Growing Pharmaceutical Investments

Pharma M&A exceeded USD 60 billion between 2024 and early 2026 as buyers chased derisked revenue streams. AstraZeneca paid USD 6 billion upfront for Daiichi Sankyo’s deruxtecan portfolio, while Synaffix secured USD 150 million from GSK for its GlycoConnect conjugation platform. Gilead invested USD 200 million in Mersana to co-develop fleximer payloads that release multiple drug moieties per antibody binding, potentially doubling response rates. Capital intensity crowds out smaller competitors yet ensures sustained funding for novel payloads, linker chemistries, and manufacturing expansions essential to the Antibody-Drug Conjugates market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High treatment costs | -4.7% | Global, acute in emerging markets and European public health systems | Medium term (2-4 years) |

| Payload supply constraints (auristatin/PBD) causing production bottlenecks | -3.9% | Global, concentrated in North America and Europe manufacturing hubs | Short term (≤ 2 years) |

| Competition from emerging T-cell engagers & bispecific antibodies | -3.2% | North America and Europe, with early adoption in hematologic cancer centers | Medium term (2-4 years) |

| High manufacturing complexity | -2.8% | Global, particularly affecting emerging market manufacturers and smaller biotechs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Treatment Costs

Annual U.S. therapy costs range from USD 168,000 for Enhertu to USD 174,000 for Trodelvy, exceeding median household income in 47 states. European HTA bodies rejected reimbursement for three ADCs in 2025 because incremental cost-effectiveness ratios topped EUR 100,000 per quality-adjusted life year. Manufacturing complexity deters biosimilar entrants, preserving originator pricing power through patent lifespans to 2035. Patient-assistance programs defray only 18% of out-of-pocket charges versus 40% for checkpoint inhibitors. High costs temper uptake, particularly in emerging markets, and shave 4.7 percentage points off the projected CAGR.

Payload Supply Constraints

Global MMAE payload output reached 180 kg in 2025, yet demand will exceed 320 kg by 2028, extending lead times for active pharmaceutical ingredients from six to 14 months. PBD dimer synthesis yields below 30% cap annual production at fewer than 50 kg, delaying four Phase 3 starts in 2025. Lonza and Catalent control 65% of conjugation capacity, and Catalent’s 2024 restructuring idled two suites for eight months, disrupting supply for six commercial products. Sponsors cannot easily switch suppliers because regulators demand bridging studies costing USD 15-25 million. Bottlenecks subtract 3.9 percentage points from Antibody-Drug Conjugates market growth until new facilities come online.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Enhertu’s Momentum Reshapes Portfolio Dynamics

Kadcyla held 23.55% of 2025 product revenue, but Enhertu is on track for a 29.25% CAGR through 2031, the fastest among marketed brands[2]Daiichi Sankyo Co., “Earnings Call Q4 2025,” DaiichiSankyo.com. This surge follows HER2-low breast and second-line non-small-cell lung approvals that added 180,000 addressable patients in North America and Europe during 2025. Padcev’s first-line urothelial label prompted 73% sequencing shifts away from platinum regimens, validating MMAE payloads in solid tumors. Trodelvy broadened into hormone-receptor-positive breast disease, but infusion reactions in 32% of patients slowed uptake. Polivy and Adcetris face substitution from bispecific T-cell engagers showing superior progression-free survival. Elahere lifted FRα-positive ovarian cancer outcomes, yet testing gaps in community clinics cap penetration. Overall, product churn skews toward topoisomerase payloads, realigning the Antibody-Drug Conjugates market toward solid-tumor indications.

A second-tier cohort—Zynlonta, Blenrep, Mylotarg, Tivdak—contributes incremental revenue streams but battles narrow biomarker windows and payer scrutiny. Blenrep returned to U.S. shelves in 2024 after confirmatory survival data, underscoring regulatory volatility. Pipeline entrants such as Dato-DXd and DusiTag-001 promise broader antigen targeting, suggesting competitive intensity will rise through 2031. These trends indicate ongoing rotation in brand leadership and reinforce the need for differentiated payload-linker platforms inside the Antibody-Drug Conjugates market.

By Payload Class: Topoisomerase Inhibitors Dominate, Microtubule Agents Rebound

Topoisomerase I inhibitors delivered 53.53% of 2025 revenue, powered by deruxtecan’s bystander-killing that addresses antigen-low tumors. The Antibody-Drug Conjugates market size for microtubule inhibitor programs is projected to expand 30.75% CAGR because Pfizer now controls six approved vedotin ADCs and 14 pipeline assets. DNA-damaging payloads such as PBD dimers retain niche share but face yield and safety hurdles. Emerging immunomodulatory payloads attracted USD 1.2 billion in venture backing across 2024-2025, signaling future modality shifts. Payload selection now aligns with tumor microenvironment: hypoxic tumors favor DNA-cleavers, while well-vascularized lesions respond to microtubule disruptors. Robust pipeline diversity ensures that the Antibody-Drug Conjugates market will see payload pluralism rather than single-class dominance.

In parallel, cleavable linkers enable bystander effects crucial for heterogeneous solid cancers. Site-specific conjugation further magnifies payload flexibility, allowing developers to match cytotoxins to antigens without raising systemic toxicity. Consequently, strategic control of payload chemistry has become a revenue stream via out-licensing, as evidenced by Daiichi Sankyo’s USD 3.2 billion milestone haul. This economic leverage will intensify demand for proprietary payload platforms across the Antibody-Drug Conjugates market.

By Linker Chemistry: Cleavable Dominance Faces Site-Specific Disruption

Cleavable linkers comprised 72.15% of 2025 revenue thanks to validated valine-citrulline and acid-labile motifs in eight approved products. Yet the Antibody-Drug Conjugates market size tied to site-specific conjugation is projected to climb 30.82% CAGR because engineered cysteine insertion and glycoengineering cut off-target toxicity and improve pharmacokinetics. THIOMAB-based ADCs yielded near-zero unconjugated antibody, securing four new licenses and USD 340 million in upfront fees for Genentech. GlycoConnect achieved 60% higher tumor uptake than lysine conjugation, prompting GSK to expand collaboration to eight programs. Non-cleavable linkers retain a role in stable toxins like DM1 but are ceding share as solid-tumor developers chase bystander activity. FDA’s 2024 mandate to profile drug-antibody ratio distributions favors deterministic manufacturing, accelerating the pivot to site-specific technologies inside the Antibody-Drug Conjugates market.

Front-runner CDMOs have already upgraded single-use bioreactors and real-time analytics to meet deterministic conjugation demands. Sponsors that lag in adopting homogeneous linker methods risk longer review cycles and inferior safety profiles. The strategic divide between stochastic and site-specific conjugation will likely widen revenue gaps across portfolios by 2031.

By Application: Hematologic Cancers Lead, Urothelial Indications Surge

Hematologic malignancies represented 46.55% of 2025 application revenue on the strength of Adcetris, Polivy, and Blenrep. Yet urothelial and bladder cancers are projected to expand at 29.32% CAGR to 2031 as Padcev’s frontline approval and Dato-DXd’s anticipated 2026 launch reshape treatment algorithms. The Antibody-Drug Conjugates market size for breast cancer is stabilizing; Kadcyla faces biosimilar threat post-2030 while Enhertu volumes shift into earlier-line curative settings. Lung cancer revenue will double by 2028 once TROP2-targeting Dato-DXd addresses EGFR-mutant niches affecting 150,000 Asia-Pacific patients annually.

Gynecologic indications grow from a small base; Elahere dominates FRα-positive ovarian tumors but awaits European reimbursement. Other solid tumors host 34 Phase 2-3 ADC trials targeting claudin-18.2, mesothelin, and integrin antigens. As sponsors pivot to high-incidence solid cancers, application mix will tilt away from hematology, broadening the Antibody-Drug Conjugates market and diversifying revenue risk.

By End User: Hospitals Anchor Delivery, Biopharma Partnerships Accelerate

Hospitals generated 51.55% of 2025 spending because specialized infusion suites, cold-chain storage, and pharmacist-led preparation remain compulsory. Specialty cancer centers captured 18% and achieved 92% adherence by integrating biomarker testing with infusion workflows. The Antibody-Drug Conjugates market size tied to biopharma and CRO partnerships is rising 30.72% CAGR as developers license platforms to multiple sponsors, outsourcing Phase 2-3 execution while harvesting milestones.

Contract manufacturers provide a parallel backbone. Lonza’s Ibex Solutions generated USD 680 million in ADC revenue in 2025 after installing 10,000-liter conjugation suites. WuXi XDC is adding 200 kg annual capacity in Wuxi by 2027, enhancing supply resilience for Asia-Pacific launches. FDA real-time release testing requirements forced small compounders out, consolidating preparation inside hospital systems. These structural shifts elevate integrated service models and accelerate product flow across the Antibody-Drug Conjugates market.

Geography Analysis

North America generated 41.55% of 2025 revenue after Medicare began reimbursing outpatient ADC infusions at 106% of average sales price, prompting hospital build-outs of oncology suites. The FDA cleared four new ADC labels between 2024-2025, and Health Canada aligned review timelines, cutting regional launch gaps to eight months. Payload manufacturing clusters in the United States, where Pfizer, Lonza, and Catalent run seven of 12 global conjugation plants, reducing cycle times for Phase 3 material. Biosimilar competition is minimal because reproducing drug-antibody ratios remains technically complex.

Asia-Pacific is the fastest-growing region at 29.22% CAGR through 2031 as China’s regulator authorized six domestic ADCs, capturing 23% of the country’s biologics spend in 18 months[3]National Medical Products Administration, “Drug Approval Database,” NMPA.gov.cn. Japan approved Enhertu for five indications, giving Daiichi Sankyo a 34% share of national ADC revenue. India issued accelerated nods for two biosimilar ADCs in 2025, signaling future price competition where out-of-pocket spending dominates. Australia shortened reviews to 11 months under a 2024 FDA cooperation pact, enabling simultaneous Padcev and Trodelvy launches.

Europe, the Middle East, and South America trail because HTA agencies in Germany, France, and the U.K. demanded real-world evidence before reimbursing three ADCs. EMA’s conditional approvals speed initial access yet impose post-marketing costs of USD 8-12 million per indication. Brazil approved Kadcyla and Enhertu in 2025, but private insurance limits coverage to HER2-overexpressing tumors, excluding HER2-low cases in 55% of patients. Saudi Arabia and the UAE embraced FDA reliance pathways, approving four ADCs in 2025 and positioning the Gulf as a fast-track market. Overall, regional disparities in reimbursement and manufacturing footprint influence adoption curves across the Antibody-Drug Conjugates market.

Competitive Landscape

The Antibody-Drug Conjugates market exhibits moderate consolidation: the top five originators held a significant revenue in 2025, but 14 biotechs pushed ADCs into Phase 3 during 2024-2025, eroding single-player dominance. Daiichi Sankyo monetized its deruxtecan payload through eight licenses that yielded USD 3.2 billion in milestones and transferred clinical risk to partners. Pfizer’s purchase of Seagen combined four approved ADCs and 14 pipeline candidates, enabling indication-sharing synergies between Padcev and vedotin programs. White-space opportunities concentrate in hepatocellular, pancreatic, and glioblastoma tumors where 11 ADCs entered Phase 2 in 2025 targeting claudin-18.2 and mesothelin.

CDMOs are capturing disproportionate value as payload complexity grows. Lonza will add 150 kg annual capacity in Singapore by 2028, enough to supply 30% of global commercial demand. Chinese challengers RemeGen and BeiGene bypass Western IP by inventing proprietary payloads, winning 18% of China’s ADC market within 24 months. February 2024 FDA chemistry guidance codified analytical expectations, favoring incumbents with deep QC capabilities and discouraging biosimilar entrants. Competitive intensity therefore bifurcates between platform owners and regional disruptors, shaping investment flows through the next decade.

Antibody Drug Conjugates Industry Leaders

F. Hoffmann-La Roche Ltd

Pfizer Inc. (Seagen Inc.)

AstraZeneca plc

Gilead Sciences Inc.

Takeda Pharmaceutical Co. Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: GSK and Syndivia signed an exclusive license for a preclinical ADC targeting metastatic castration-resistant prostate cancer.

- October 2025: Lisata Therapeutics granted Catalent global rights to incorporate certepetide into SMARTag-enabled ADCs.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the antibody-drug conjugates (ADC) market as global sales of branded, human or humanized monoclonal antibodies covalently linked to a cytotoxic payload through a chemical linker, approved for oncology therapy or in late-stage pipelines. Value is recorded at manufacturer selling price, inclusive of hospital and specialty-pharmacy channels, covering finished drugs across all dosage forms.

Scope exclusion: Radio-immunoconjugates and stand-alone contract manufacturing revenues sit outside this sizing.

Segmentation Overview

- By Product

- Adcetris (brentuximab vedotin)

- Kadcyla (trastuzumab emtansine)

- Padcev (enfortumab vedotin)

- Polivy (polatuzumab vedotin)

- Enhertu (trastuzumab deruxtecan)

- Trodelvy (sacituzumab govitecan)

- Elahere (mirvetuximab soravtansine)

- Other Approved ADCs

- By Payload Class

- Microtubule Inhibitors (MMAE, DM1, DM4)

- DNA-Damaging Agents (PBD, Calicheamicin, Duocarmycin)

- Topoisomerase I Inhibitors (DXd, SN-38)

- Emerging Payloads (Auristatin variants, novel alkylators)

- By Linker Chemistry

- Cleavable Linkers

- Non-cleavable Linkers

- Site-specific / Next-Gen Conjugation Technologies

- By Application (Indication)

- Breast Cancer

- Hematologic Cancers (Lymphoma, Leukemia, Myeloma)

- Urothelial / Bladder Cancer

- Lung Cancer

- Gynaecologic Cancers (Ovary, Endometrium, Cervix)

- Other Solid Tumors

- By End User

- Hospitals

- Specialty Cancer Centres

- Biopharma & Contract Research Organisations

- Others

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed medical oncologists, hospital pharmacists, CDMO scientists, and health-policy advisers across North America, Europe, and high-growth Asia Pacific. Dialogues tested therapy uptake curves, average selling price shifts, and expected launch timelines, letting us reconcile desk findings and refine risk weights inside the model.

Desk Research

We first parsed open datasets from sources such as the US FDA drug database, EMA community register, WHO GLOBOCAN cancer incidence files, UN Comtrade shipment codes, and patent families on Questel. Sector context came from American Cancer Society factsheets, ClinicalTrials.gov study logs, and company 10-Ks accessed via Dow Jones Factiva. D&B Hoovers supplied historical sales for marketed ADCs, while association portals like BIO and Japan's PMDA clarified regulatory cadence across regions. This list is illustrative; many other public and proprietary references informed the evidence stack.

Market-Sizing & Forecasting

Top-down incidence-to-treatment reconstruction anchors the model. Country-level cancer cases feed prevalence cohorts, which are then multiplied by ADC penetration rates and verified average course prices. Select bottom-up checks, aggregated manufacturer revenues, sampled tender data, and capacity utilization snapshots fine-tune totals. Key variables include the number of ADC approvals, median price erosion post-year three, pipeline attrition ratios, regional reimbursement breadth, and cleavable-linker share of launches. A multivariate regression blends these drivers to forecast through 2030, after stress testing three uptake scenarios. Any bottom-up gaps are bridged using regional ASP analogs approved during the prior two years.

Data Validation & Update Cycle

Outputs face variance screens versus independent cancer drug indices, peer data points, and prior editions. Senior reviewers sign off only after anomalies are closed. Reports refresh annually, with mid-cycle edits when material events, major approvals or safety withdrawals, shift baselines.

Why Our Antibody Drug Conjugates Baseline Commands Confidence

Published estimates differ because each publisher picks its own mix of products, geographies, and price assumptions. By selecting only marketed and late-stage ADCs, aligning currency conversions to IMF rates, and updating the model the moment a therapy wins approval, Mordor keeps the baseline decision-ready.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 15.61 B (2025) | Mordor Intelligence | - |

| USD 14.14 B (2024) | Global Consultancy A | narrower product basket; excludes pipeline launches |

| USD 9.7 B (2023) | Industry Journal B | early base year and revenue pooling from four approved drugs only |

| USD 12.36 B (2024) | Regional Consultancy C | omits Latin America and uses list prices without reimbursement discounts |

These contrasts show that when scope, variables, and refresh cadence tighten, figures converge toward Mordor's balanced, transparent midpoint, giving stakeholders a dependable starting point for strategy.

Key Questions Answered in the Report

How fast is global growth projected for Antibody-Drug Conjugates?

Revenue is forecast to expand from USD 20.12 billion in 2026 to USD 71.55 billion by 2031, implying a 28.88% CAGR for 2026-2031.

Which payload class contributes the most sales today?

Topoisomerase I inhibitor conjugates generated 53.53% of 2025 revenue, driven chiefly by deruxtecan-based products.

What recent FDA guidance accelerated approval cycles?

The February 2024 CMC guidance requiring detailed drug-antibody ratio and linker-stability data cut median U.S. review times from 14 months to 10 months.

Are supply constraints affecting commercial roll-outs?

Yes, global output of MMAE and PBD payloads lags rising demand, stretching lead times for active ingredients from six to 14 months and delaying four Phase 3 trials in 2025.

How important is North America in current sales?

The region delivered 41.55% of 2025 global Antibody-Drug Conjugates revenue, helped by Medicare reimbursement and dense manufacturing capacity.

Page last updated on: