Bioanalytical Testing Services Market Size and Share

Market Overview

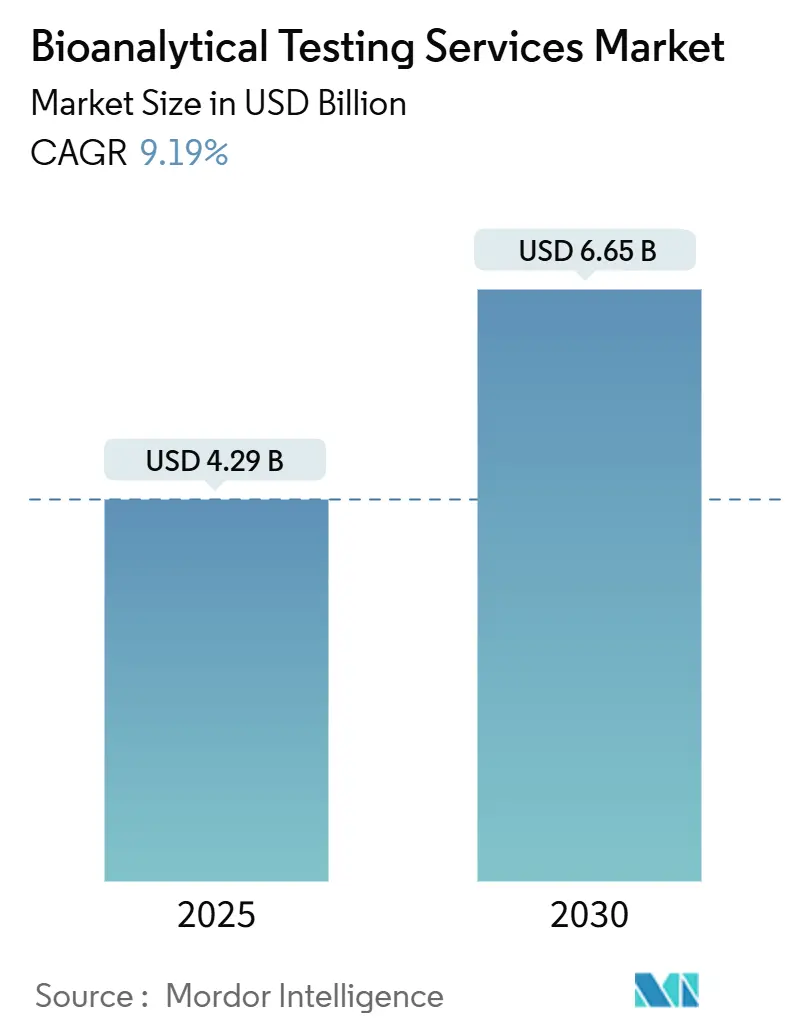

| Study Period | 2019 - 2030 |

| Market Size (2025) | USD 4.29 Billion |

| Market Size (2030) | USD 6.65 Billion |

| Growth Rate (2025 - 2030) | 9.19% CAGR |

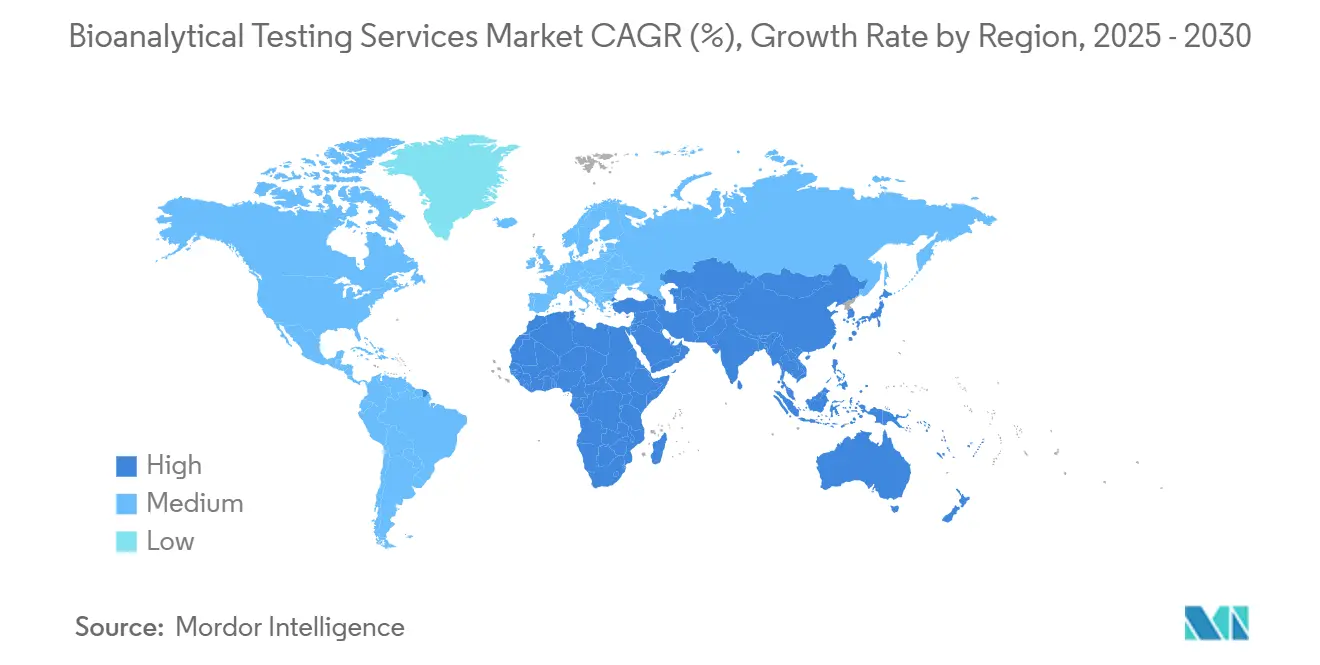

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Bioanalytical Testing Services Market Analysis by Mordor Intelligence

The Bioanalytical Testing Services Market size is estimated at USD 4.29 billion in 2025, and is expected to reach USD 6.65 billion by 2030, at a CAGR of 9.19% during the forecast period (2025-2030).

The acceleration reflects the sector’s transition from a support function to a strategic driver of precision-medicine programs, regulatory filings, and faster drug-development cycles. Outsourcing now underpins more than 50% of clinical study analytics as sponsors trim fixed laboratories and lean on specialist contract research organizations (CROs) for high-throughput capacity. Biologics, biosimilars, and complex modalities demand high-resolution instrumentation that few sponsors keep in-house, prompting multiyear service contracts for ligand-binding assays, high-resolution mass spectrometry, and immunogenicity testing. Meanwhile, the global push toward harmonized guidelines such as ICH M10 is encouraging a uniform validation approach that reduces repeat testing while simultaneously raising the technical bar for laboratories. Supply-chain disruptions during the COVID-19 pandemic further reinforced outsourcing decisions and hastened adoption of automated platforms that cut assay turn-around times.

Key Report Takeaways

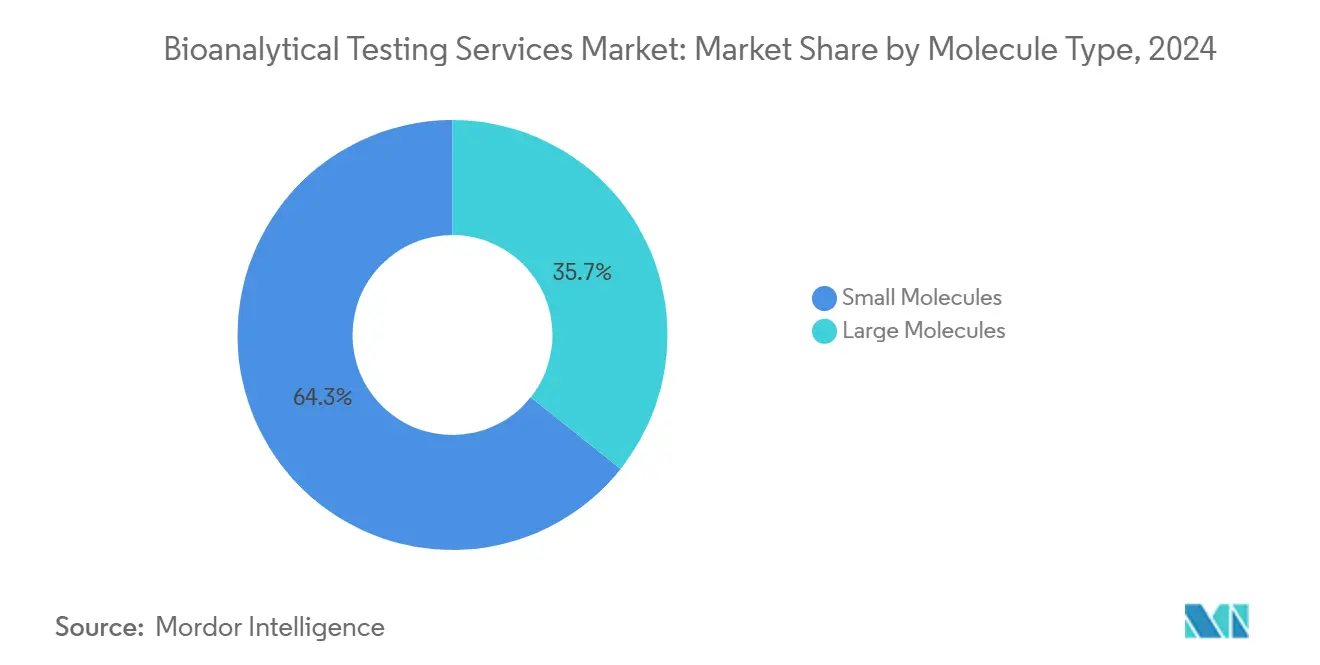

- By molecule type, small molecules retained 64.27% of the bioanalytical testing services market share in 2024, while large molecules are forecast to post an 11.55% CAGR through 2030.

- By test type, bioavailability and bioequivalence held 36.54% revenue share in 2024; biomarker assays are projected to expand at a 12.87% CAGR to 2030.

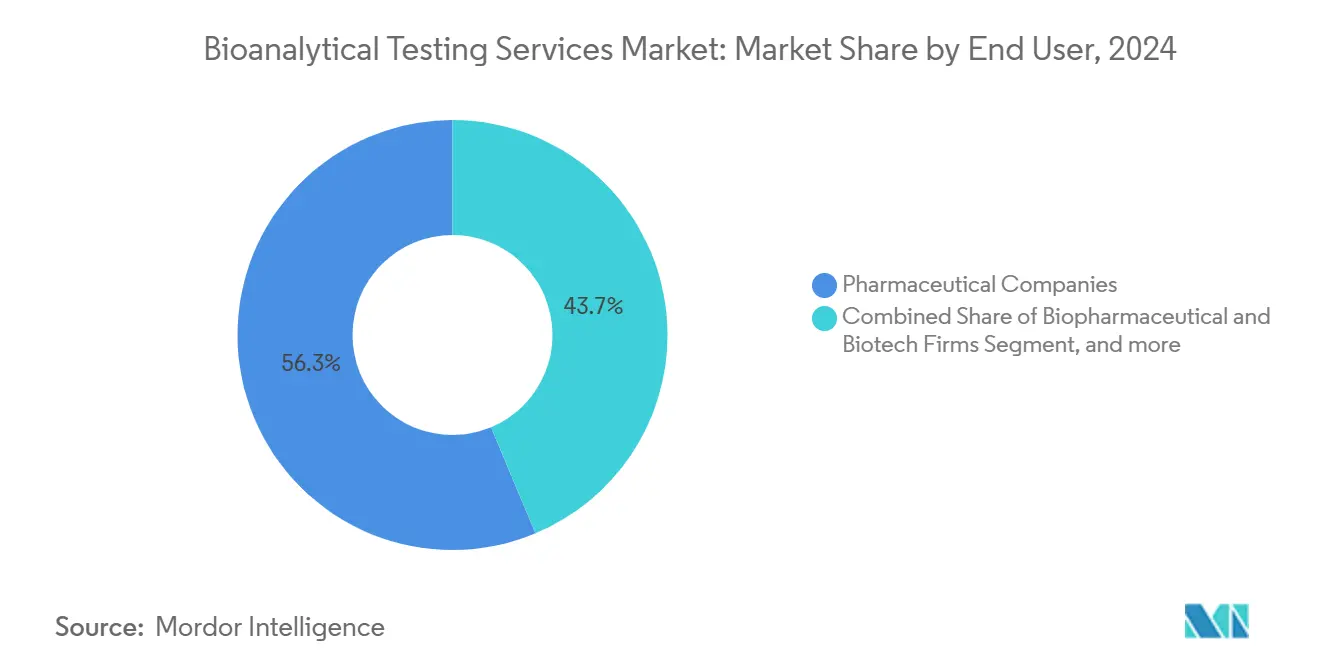

- By end user, pharmaceutical companies commanded 56.32% share of the bioanalytical testing services market size in 2024, whereas CDMOs are on course for a 13.56% CAGR between 2025-2030.

- By geography, North America led with 42.44% revenue share in 2024; Asia-Pacific is set to grow at 12.19% CAGR through 2030.

Global Bioanalytical Testing Services Market Trends and Insights

Drivers Impact Analysis

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Outsourcing of Analytical Testing | +2.1% | Global, with North America & EU leading adoption | Medium term (2-4 years) |

| Expansion of Biologics & Biosimilars Pipeline | +1.8% | Global, concentrated in US, EU, and emerging APAC markets | Long term (≥ 4 years) |

| Growing Global Clinical-Trial Volumes | +1.5% | APAC core, spill-over to MEA and Latin America | Medium term (2-4 years) |

| Stringent PK/PD & BE Regulatory Mandates | +1.2% | Global, with harmonization across FDA, EMA, and PMDA | Long term (≥ 4 years) |

| Adoption of Microsampling & DBS in Decentralized Trials | +0.9% | North America & EU, expanding to APAC | Short term (≤ 2 years) |

| AI-Driven Analytics Cutting Assay Turnaround Time | +0.7% | Global, with early adoption in developed markets | Short term (≤ 2 years) |

Source: Mordor Intelligence

Rising outsourcing of analytical testing

Pharmaceutical sponsors are reallocating capital from fixed laboratories to flexible, tech-enabled partnerships, lifting outsourcing penetration to unprecedented levels. Biologics workflows requiring sub-ppm impurity detection and multiplex ligand-binding assays now sit almost entirely with CROs. Pandemic restrictions intensified the shift as in-house labs shut down while CRO networks stayed operational through disaster-recovery protocols.[1]PMC Authors, “COVID-19 Impact on Laboratory Outsourcing,” ncbi.nlm.nih.gov Access to high-resolution mass spectrometers costing USD 500,000 per unit and automated sample-preparation robots remains a decisive factor for smaller biotech firms seeking rapid data readouts.

Expansion of biologics & biosimilars pipeline

Large-molecule approvals comprised 46% of FDA clearances in 2025, propelled by monoclonal antibodies, fusion proteins, and antibody-drug conjugates that require orthogonal assays to evaluate potency, glycosylation, and host-cell-protein content. [2]ACM Global Laboratories, “Large-Molecule Analysis Trends,” acmgloballabs.com Over 240 biosimilars are in active development, reinforcing demand for comparative analytics that focus on molecular similarity rather than expensive efficacy trials. Regulators such as the UK MHRA signal readiness to waive certain efficacy studies when analytical evidence is compelling, accelerating uptake of advanced biophysical techniques and multivariate statistics.

Growing global clinical-trial volumes

Asia-Pacific investigators logged double-digit trial growth as sponsors pursued cost-efficient enrollment, ethnically diverse cohorts, and streamlined approvals in South Korea, Taiwan, and Japan. CROs such as Novotech now process roughly 34,000 samples per month across new APAC facilities, feeding regional demand for PK, PD, and immunogenicity assays. Western geopolitical uncertainties, capacity bottlenecks, and inflationary pressures further motivate trial migration eastward.

Stringent PK/PD & BE regulatory mandates

ICH M10 harmonizes validation templates yet introduces cross-validation and parallelism checks that stretch existing quality-management systems. The FDA’s 2024 draft guidance on data integrity mandates risk-based electronic records and expands audit-trail scrutiny, prompting investments in laboratory information-management software and robotic data review pipelines able to cut manual steps by up to 86%.[3]Federal Register, “Data Integrity in Bioequivalence Studies,” federalregister.gov Labs with global submissions must now navigate differing thresholds for highly variable drugs, NTI compounds, and microsampling protocols, adding overhead to multinational projects.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Complex & Rapidly-Evolving Global Regulations | -1.4% | Global, with particular complexity in FDA-EMA harmonization | Long term (≥ 4 years) |

| Shortage of Skilled Bioanalytical Scientists | -0.9% | North America & EU primarily, emerging in APAC | Medium term (2-4 years) |

| High Capex for HR-Mass-Spectrometry Platforms | -0.7% | Global, with higher impact on smaller laboratories | Medium term (2-4 years) |

| Sample-Integrity Risks in At-Home Collections | -0.5% | North America & EU leading decentralized trials | Short term (≤ 2 years) |

Source: Mordor Intelligence

Complex & rapidly-evolving global regulations

Differing regional expectations continue to generate multi-protocol validation plans, inflating development budgets by 15-20%. Potential FDA oversight of laboratory-developed tests (LDTs) will pull clinical labs into drug-style GMP systems, demanding capital upgrades in documentation, change control, and data-integrity architecture. Smaller providers lacking embedded regulatory teams face competitive headwinds as compliance overhead rises.

Shortage of skilled bioanalytical scientists

High-resolution mass-spectrometry, data science, and regulatory affairs skills remain scarce, as academic programs lag industry technology cycles. Pandemic-era lab closures curtailed hands-on training for new graduates, widening the expertise gap. Some providers counter with “dark labs” deploying robotics and AI to deliver 24-hour throughput with minimal human intervention.

Segment Analysis

By Molecule Type: Large Molecules Drive Innovation

Large molecules generated rapid momentum, even though small molecules still held 64.27% of the bioanalytical testing services market share in 2024. The large-molecule segment is expanding at an 11.55% CAGR due to monoclonal antibodies, fusion proteins, and peptide therapeutics that necessitate ligand-binding assays, cell-based potency tests, and immunogenicity evaluations. This demand compels laboratories to install high-throughput Gyrolab immunoassay platforms and multi-attribute-method mass-spectrometry workflows that identify structural variants within minutes.

Investment intensity continues to rise. WuXi AppTec, for example, lifted peptide-manufacturing capacity to 32,000 L of solid-phase synthesis reactors, underpinning a surge in comparative analytical requests from biosimilar developers. Sponsors favor analytical similarity packages over long efficacy studies, pushing advanced orthogonal techniques into routine service. As the pipeline diversifies, the bioanalytical testing services market will rely heavily on cross-disciplinary skillsets spanning biochemistry, statistics, and automation to match rising complexity.

Note: Segment shares of all individual segments available upon report purchase

By Test Type: Biomarker Assays Lead Innovation

Bioavailability and bioequivalence work accounted for 36.54% revenue in 2024, safeguarding regulatory compliance for generics. Yet, biomarker assays headline growth with a 12.87% CAGR, mirroring precision-medicine strategies that appear in more than 40% of recent FDA approvals. Sponsors increasingly request multi-omics panels that combine proteomics, metabolomics, and lipidomics to stratify patients, a capability pioneered by firms such as Dalton Bioanalytics through single-run assays that lower cost and boost data depth.

AI-powered analytics shorten turnaround windows, allowing near real-time dose adjustments in adaptive trials. Immunogenicity and neutralizing-antibody assays also display robust demand as biologics volumes climb, requiring ultralow detection limits and confirmatory workflows. ADME studies remain fundamental, but high-resolution platforms increase metabolite mapping efficiency, anchoring their relevance within the broader service mix of the bioanalytical testing services industry.

By End User: CDMOs Accelerate Partnership Models

Pharmaceutical companies controlled 56.32% of 2024 revenue, yet contract development and manufacturing organizations are on track for a 13.56% CAGR as integrated research-to-manufacture partnerships gain traction. BioDuro’s CRDMO model illustrates the appeal: unified discovery, analytical, and GMP manufacturing reduce tech-transfer risks and compress timelines. CDMOs are scaling bioanalytical labs to support biologics pipelines and, in turn, capturing multi-year master service agreements.

WuXi Biologics reported non-COVID service revenue growth, evidencing the stickiness of integrated engagements. Academic and public research institutes remain steady but slower growth users, focused on translational research rather than commercial submissions. Overall, the bioanalytical testing services market size tied to CDMOs will widen as sponsors consolidate vendors for end-to-end accountability.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

North America generated 42.44% of global revenue in 2024, underpinned by concentrated pharmaceutical headquarters, FDA proximity, and extensive GLP infrastructure. Major providers such as Labcorp deploy more than 14,000 employees across domestic labs that underpin top-selling drug programs. Yet, talent shortages and elevated labor costs pressure margins and drive selective outsourcing to lower-cost regions. Canadian facilities complement US capacity with bilingual submissions, while Mexico’s near-shoring momentum is prompting fresh investment in GLP sites aligned with US import rules.

Europe ranks second due to cohesive EMA frameworks and leadership in biosimilars. Germany, France, and the United Kingdom host clusters of CRO and CDMO facilities that collaborate with academic hubs, and Eurofins Scientific alone runs over 900 European laboratories performing 450 million tests annually. Post-Brexit, the UK fast-tracked biosimilar pathways to sustain competitiveness, demonstrating a flexible regulatory posture that continues to attract biopharma analytical work. EU investments in biopharmaceutical manufacturing hubs and Horizon Europe R&D grants will keep demand buoyant.

Asia-Pacific represents the fastest-growing zone at 12.19% CAGR, driven by clinical-trial migration, expanding manufacturing capacity, and supportive government incentives. China leads sample volumes as local CROs scale capacity, while Japan’s status as the third-largest pharmaceutical market ensures a steady flow of complex submissions requiring bilingual documentation. South Korea and Taiwan leverage tax credits and expedited reviews, luring multinationals searching for efficient enrollment and cost controls. India’s national push for GLP compliance and Australia’s biotechnology cluster diversify regional capabilities. As a result, the bioanalytical testing services market will see APAC revenue converge with Western levels during the second half of the decade.

Competitive Landscape

The market shows moderate fragmentation yet increasing consolidation as scale and technology investments differentiate leaders. High-resolution mass-spectrometry systems above USD 500,000, coupled with expert staffing, create substantial entry barriers. Eurofins Scientific exemplifies scale leverage, offering more than 200,000 validated assays across 61 countries and completing 450 million tests per year. Acquisition activity centers on complementary biophysical platforms; Bruker’s purchase of Sierra Sensors and Waters’s takeover of Wyatt Technology extend service breadth for complex biotherapeutics.

Strategic direction favors vertical integration and regional expansion. Providers are linking discovery screening to regulated bioanalysis and commercial QC under one contract to eliminate tech-transfer friction. Robotics-driven dark labs promise 24-hour workflows that mitigate scientist shortages and lower error rates. White-space remains in multi-omics and AI-assisted data-mining niches where early movers such as Dalton Bioanalytics operate. Overall, competition hinges on marrying regulatory fluency, global logistics, and automated analytics to support sponsors navigating a more intricate therapeutic landscape.

Bioanalytical Testing Services Industry Leaders

-

SGS SA

-

Syneos Health

-

Charles River Laboratories

-

Labcorp Drug Development (Covance)

-

ICON plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Thermo Fisher Scientific reported first quarter 2025 revenue of USD 10.36 billion with 15% growth, launching innovative products including the Thermo Scientific Vulcan Automated Lab for semiconductor analysis and Olink Reveal proteomics kits for precision medicine applications. The company also entered a Technology Alliance Agreement with the Chan Zuckerberg Institute for Advanced Biological Imaging.

- March 2025: Labcorp announced the acquisition of select assets from BioReference Health's innovative oncology and related clinical testing services businesses, aimed at enhancing access to high-quality laboratory services and expanding Labcorp's portfolio in cancer care. The transaction is expected to generate significant annual revenue and close in the second half of 2025.

- February 2025: Charles River Laboratories announced a strategic agreement with Singapore General Hospital to provide CGMP-compliant master cell banking and next-generation sequencing testing services for cord blood-derived allogeneic CAR-T cells. The NGS services enhance viral contamination detection in cell banks, offering reliable testing options that meet regulatory requirements while supporting novel cancer therapeutic development.

- January 2025: Charles River Laboratories expanded its Apollo™ ecosystem with the launch of Apollo for CRADL, a cloud-based platform designed to enhance vivarium rental services and streamline drug discovery processes across nearly 30 facilities globally. This strategic initiative integrates various services including safety assessments and biologics testing, providing real-time data access and administrative task management to accelerate research timelines.

Global Bioanalytical Testing Services Market Report Scope

Bioanalysis involves quantitative measurement of xenobiotics, like small molecule drugs and their metabolites and biological molecules. Bioanalytical testing services are used in the development and validation of robust bioanalytical methods in body fluids and tissue specimens. These tests are used to support pre-clinical and Phase I through Phase IV clinical trials.

The bioanalytical testing services market is segmented by molecule type (small molecule and large molecule), by test type (bioavailability and bioequivalence studies, pharmacokinetics, pharmacodynamics, and other test types), and by geography (North America, Europe, Asia-Pacific, Middle-East and Africa, and South America). The market report also covers the estimated sizes and trends for 17 different countries across major regions globally. The report offers the value (in USD million) for the above segments.

| By Molecule Type | Small Molecules | ||

| Large Molecules | |||

| By Test Type | Bioavailability & Bioequivalence | ||

| Pharmacokinetics | |||

| Pharmacodynamics | |||

| Absorption-Distribution-Metabolism-Excretion | |||

| Immunogenicity & Neutralizing-Antibody Assays | |||

| Biomarker & Omics-Based Assays | |||

| Other Tests | |||

| By End User | Pharmaceutical Companies | ||

| Biopharmaceutical & Biotech Firms | |||

| Contract Development & Manufacturing Organizations | |||

| Academic & Government Institutes | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| Australia | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East & Africa | GCC | ||

| South Africa | |||

| Rest of Middle East & Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Small Molecules |

| Large Molecules |

| Bioavailability & Bioequivalence |

| Pharmacokinetics |

| Pharmacodynamics |

| Absorption-Distribution-Metabolism-Excretion |

| Immunogenicity & Neutralizing-Antibody Assays |

| Biomarker & Omics-Based Assays |

| Other Tests |

| Pharmaceutical Companies |

| Biopharmaceutical & Biotech Firms |

| Contract Development & Manufacturing Organizations |

| Academic & Government Institutes |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

Key Questions Answered in the Report

What is the current size of the bioanalytical testing services market?

The market generated USD 4.29 billion in 2025 and is projected to reach USD 6.65 billion by 2030.

Which geographic region is growing the fastest?

Asia-Pacific leads with a forecast 12.19% CAGR, driven by clinical-trial migration and regulatory reforms.

Why are biomarker assays expanding so rapidly?

Precision-medicine strategies require multi-omics profiling, pushing biomarker assay demand at a 12.87% CAGR through 2030.

How are CDMOs influencing the market?

CDMOs integrate discovery to manufacturing, enabling 13.56% CAGR growth by offering single-contract accountability.

What are the main regulatory challenges?

Divergent global validation standards and tighter data-integrity rules raise compliance costs and prolong project timelines.

How is automation addressing workforce shortages?

Robotics-driven “dark labs” and AI analytics deliver 24-hour throughput, reducing reliance on scarce specialist scientists.