Benign Prostatic Hyperplasia (BPH) Treatment Devices Market Size and Share

Market Overview

| Study Period | 2022 - 2031 |

|---|---|

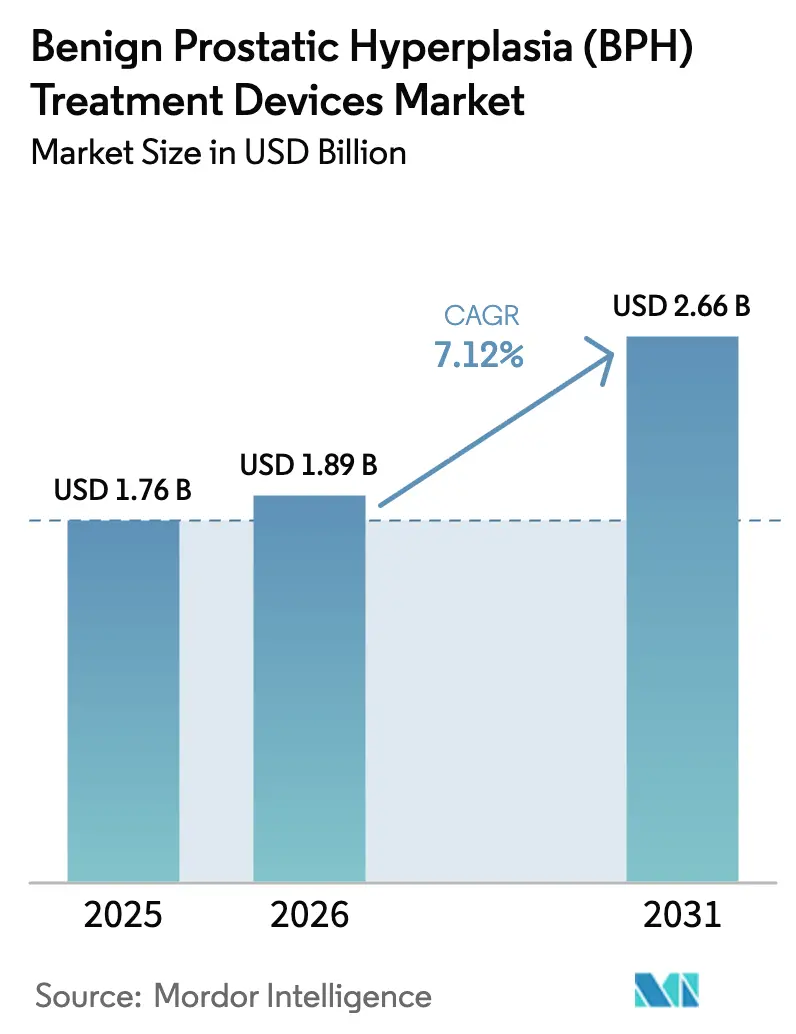

| Market Size (2026) | USD 1.89 Billion |

| Market Size (2031) | USD 2.66 Billion |

| Growth Rate (2026 - 2031) | 7.12% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Benign Prostatic Hyperplasia (BPH) Treatment Devices Market Analysis by Mordor Intelligence

The Benign prostatic hyperplasia treatment devices market size was valued at USD 1.76 billion in 2025 and estimated to grow from USD 1.89 billion in 2026 to reach USD 2.66 billion by 2031, at a CAGR of 7.12% during the forecast period (2026-2031). Robust demand is underpinned by the convergence of population aging, rapid uptake of artificial-intelligence-guided robotic systems, and insurer support for minimally invasive surgical therapies. Hospitals remain the principal channel for complex cases, yet ambulatory surgical centers (ASCs) are capturing accelerating volumes as payers and patients favor lower-cost outpatient settings. Technological differentiation is intensifying as laser, radio-frequency, and waterjet platforms compete on functional preservation, procedure time, and capital efficiency. Regulatory tailwinds, notably new Current Procedural Terminology (CPT) codes for Aquablation and iTind, are removing reimbursement uncertainty and encouraging facility investment. At the same time, supply chain vulnerabilities for semiconductors and optics as well as a global shortage of robotics-skilled urologists pose execution risks.

Key Report Takeaways

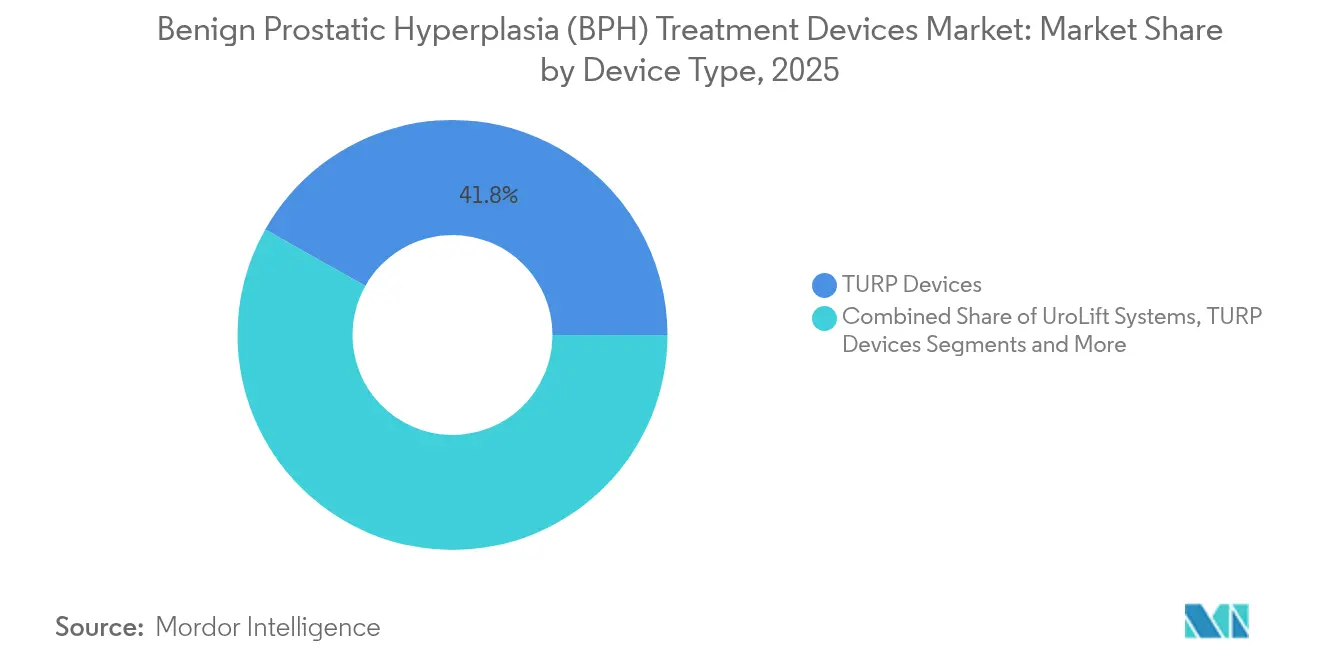

- By device type, transurethral resection of the prostate (TURP) devices held 41.83% of Benign prostatic hyperplasia treatment devices market share in 2025, while robotic Aquablation systems are projected to post the fastest 8.34% CAGR to 2031.

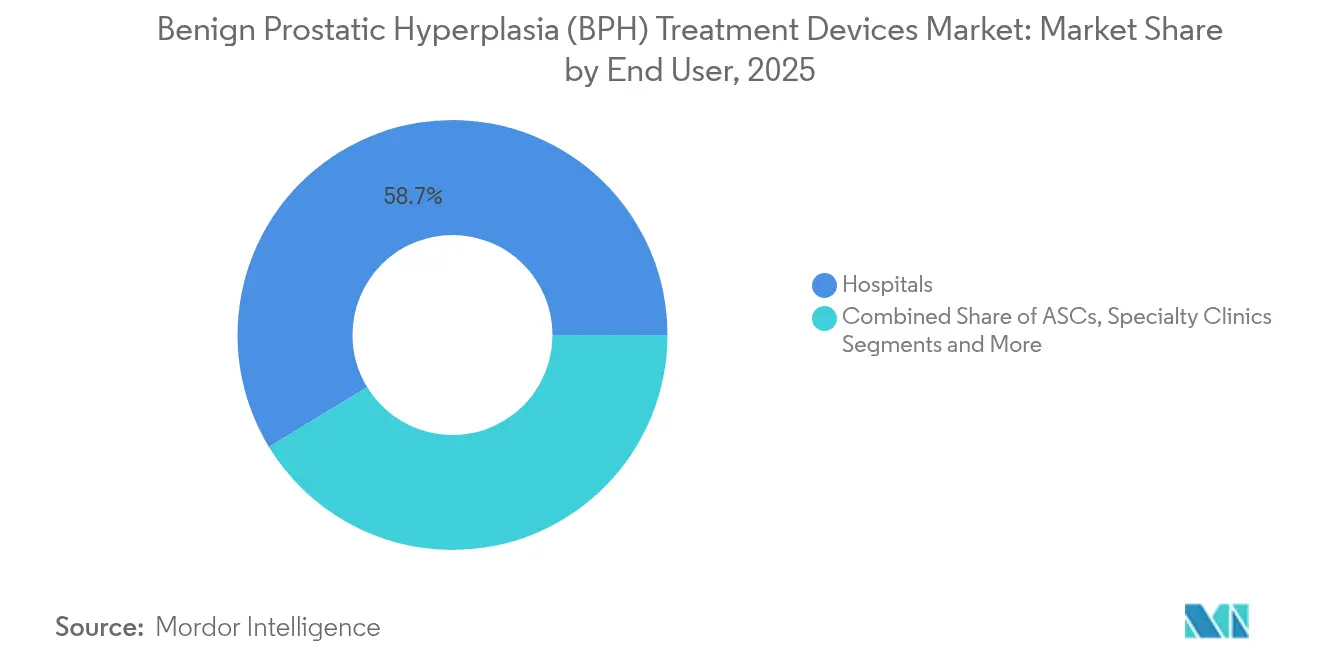

- By end user, hospitals accounted for 58.72% of the Benign prostatic hyperplasia treatment devices market size in 2025; ASCs are advancing at a 9.62% CAGR through 2031.

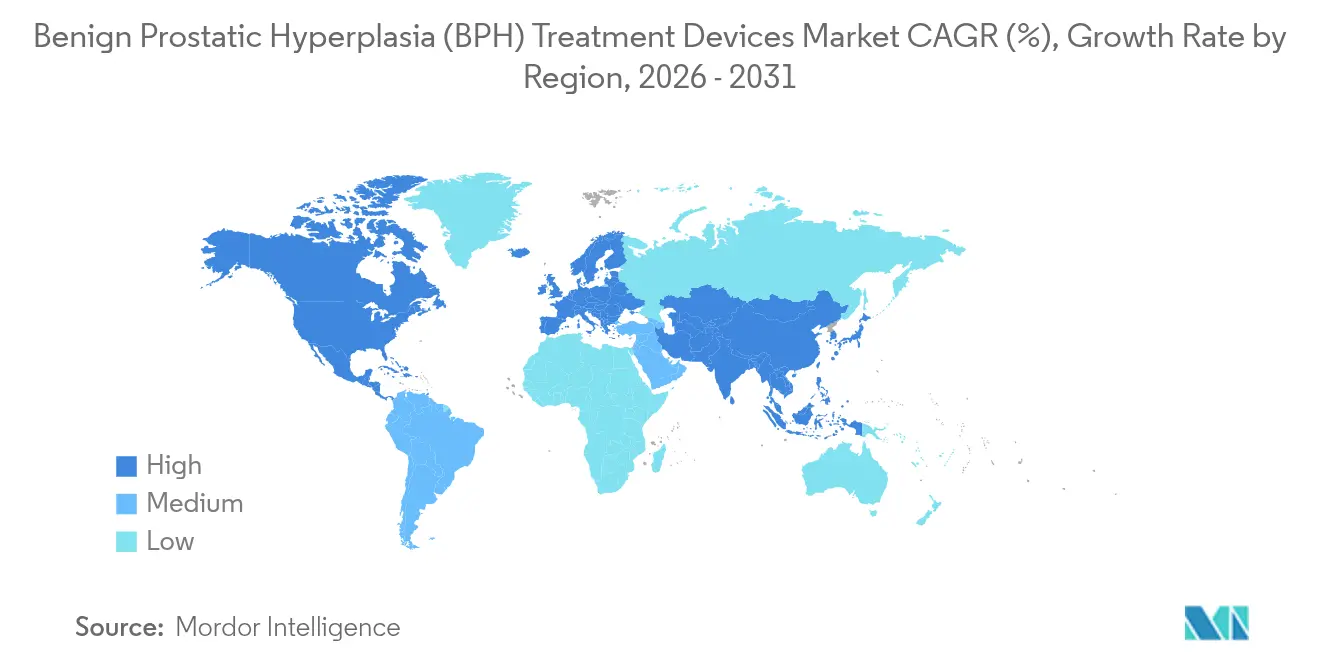

- By geography, North America commanded 36.85% revenue in 2025; Asia-Pacific is set to lead growth with an 8.08% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Benign Prostatic Hyperplasia (BPH) Treatment Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of Benign Prostatic Hyperplasia (BPH) | +1.80% | Global, with highest impact in North America and Europe | Long term (≥ 4 years) |

| Technological advances in minimally-invasive therapies | +1.50% | Global, led by North America and Europe | Medium term (2-4 years) |

| Rapid uptake of AI-guided robotic Aquablation systems | +1.20% | North America and Europe, expanding to APAC | Short term (≤ 2 years) |

| Insurer coverage expansion for MIST procedures | +0.90% | North America and Europe | Medium term (2-4 years) |

| Growing office-based procedure volumes in urology clinics | +0.70% | North America, with expansion to APAC | Short term (≤ 2 years) |

| Emerging-market demand for ambulatory laser platforms | +0.60% | APAC, LATAM, and MEA | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Benign Prostatic Hyperplasia

Global prevalent cases climbed from 50.7 million in 1990 to 112.5 million in 2021, a 122% jump that far outpaces population growth. Prevalence accelerates sharply after age 60, placing sustained pressure on healthcare systems as the cohort of men aged 60-79 enlarges. Disability-adjusted life years attributable to BPH have risen in parallel, signaling greater disease severity that pushes more patients toward device-based intervention. In the United States, the geriatric population is on track to reach 77 million by 2034, expanding the treatable pool for surgical therapies. Middle-income regions are experiencing the fastest rise, broadening demand beyond long-established mature markets.[1]Xiaofei Hou et al., “Global burden of benign prostatic hyperplasia,” Scientific Reports, nature.com

Technological Advances in Minimally Invasive Therapies

Prostatic urethral lift volumes grew 3,730% and water-vapor thermal cases rose 123% between 2014 and 2021, while TURP procedures fell 37%. New platforms combine high-resolution imaging with laser, radio-frequency, or waterjet energy to achieve tissue removal that minimizes bleeding and preserves sexual function. The United States Food and Drug Administration cleared the HYDROS robotic system with FirstAssist AI in August 2024, providing real-time ultrasound and automated resection mapping that shorten learning curves and enhance outcomes.[2]US Food and Drug Administration, “510(k) Clearance K240812,” fda.gov

Rapid Uptake of AI-Guided Robotic Aquablation Systems

Machine-learning algorithms analyze prior procedure data to identify optimal resection zones and safeguard ejaculatory structures. WATER III clinical results showed ejaculatory dysfunction in only 14.8% of Aquablation patients versus 77.1% for laser enucleation, while symptom relief remained equivalent. More than 400 AquaBeam platforms were installed in US centers by end-2024, generating USD 217 million in product revenue. Dedicated CPT Category I codes, effective January 2026, eliminate major reimbursement barriers and are expected to accelerate penetration.

Insurer coverage expansion for minimally invasive procedures

The Centers for Medicare & Medicaid Services issued Local Coverage Determinations for Aquablation and iTind in 2025 and assigned specific supply pricing that makes institutional economics predictable. UnitedHealthcare and other private payers subsequently adopted coverage with utilization-management criteria based on prostate size and symptom severity. Health-technology assessments in Canada concluded that while some minimally invasive options deliver marginally lower efficacy than TURP, their complication rates and faster recovery justify reimbursement for appropriate patients.[3]Centers for Medicare & Medicaid Services, “CY 2025 Physician Fee Schedule Final Rule,” cms.gov

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital & per-procedure cost of advanced systems | -1.40% | Global, with highest impact in emerging markets | Medium term (2-4 years) |

| Shortage of trained endoscopic & robotics-skilled urologists | -0.80% | Global, particularly acute in rural areas | Long term (≥ 4 years) |

| Reimbursement uncertainty for novel devices in APAC & LATAM | -0.60% | APAC and LATAM regions | Medium term (2-4 years) |

| Semiconductor & fiber-optic supply bottlenecks | -0.40% | Global, with highest impact on advanced laser systems | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Capital and Per-Procedure Cost of Advanced Systems

An AquaBeam console carries a USD 432,000 list price, excluding annual service contracts and single-use handpieces that cost USD 1,000-3,000 each. The economic hurdle is steepest for lower-volume community hospitals and for emerging-market facilities that operate under constrained capital budgets. Payback analyses show viability once annual procedure counts exceed 120-150, concentrating installations in urban tertiary centers. Value-based purchasing frameworks that incorporate downstream savings from reduced complications are slowly broadening adoption.

Shortage of Trained Endoscopic and Robotics-Skilled Urologists

Almost 30% of the US urology workforce is at least 65 years old and 90% practice in metropolitan counties. Advanced modalities require additional credentialing that further narrows practitioner pools, leaving rural regions underserved. Residency programs increased average logged BPH procedures from 1,449 to 1,569 between 2016 and 2021, yet the absolute number of new graduates remains insufficient to meet rising demand. Physician assistants and nurse practitioners now contribute 11% of outpatient urology visits, but they cannot replace surgical expertise.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: TURP Dominance Faces Robotic Disruption

TURP devices delivered 41.83% of 2025 revenues, anchoring the Benign prostatic hyperplasia treatment devices market through proven efficacy and widespread surgeon familiarity. Laser-based platforms have gained share where anticoagulation management and large prostate volumes demand superior hemostasis. Aquablation systems are the fastest riser, projected to expand at 8.34% CAGR and threaten the historical supremacy of electrosurgical resection. In value terms, the Benign prostatic hyperplasia treatment devices market size for Aquablation could more than double by 2031 if current adoption curves hold.

Competitive positioning within this segment is shifting toward AI integration, single-use instrumentation, and office-based readiness. Robotic waterjet platforms combine superior functional outcomes with emerging reimbursement clarity, drawing purchasing attention from high-volume centers. Laser enucleation devices retain favor for prostates exceeding 100 g, yielding a balanced technology portfolio across clinical sub-groups. Microwave thermotherapy, radio-frequency ablation, and UroLift implants fill niche preferences where anesthesia constraints or preservation of sexual function dominate decision criteria. Taken together, device choice is moving from one-size-fits-all toward algorithmic patient stratification that leverages multivariate imaging and symptom profiles.

By End User: Hospital Dominance Yields to ASC Efficiency

Hospitals captured 58.72% of global expenditure in 2025 because complex comorbid cases and large prostates require multidisciplinary support and postoperative monitoring. Academic medical centers spearhead early adoption of robotics and AI-enabled systems, channeling vendor training and peer-review data that subsequently cascade to community facilities. The Benign prostatic hyperplasia treatment devices market share within hospitals will erode gradually as outpatient reimbursement continues to align with minimally invasive techniques.

Ambulatory surgical centers are forecast to log the steepest 9.62% CAGR, reflecting 40-60% lower procedure costs and patient preference for same-day discharge. Employer and payer steering toward lower-cost settings accelerates migration of water-vapor thermal therapy, UroLift, and Aquablation once anesthesia protocols are optimized for outpatient care. Specialty urology clinics represent a small but expanding niche that benefits from local anesthesia products such as iTind. Their growth underscores decentralization trends that emphasize throughput, consumer convenience, and bundled payment frameworks.

Geography Analysis

North America generated 36.85% of 2025 revenue on the back of comprehensive insurance coverage, early-stage AI adoption, and dense networks of fellowship-trained urologists. The Benign prostatic hyperplasia treatment devices market size in the region is growing steadily as CMS and major commercial payers finalize dedicated codes that enhance predictability of capital returns. Clinical-society guidelines increasingly endorse minimally invasive options, reinforcing physician confidence.

Asia-Pacific is projected to achieve an 8.08% CAGR to 2031, the fastest worldwide, as health-care infrastructure investment coincides with rapid demographic aging. China and India present significant unmet need where procedure volumes remain well below epidemiologic incidence. Government initiatives to expand private insurance and public-hospital capacity are unlocking funding for laser and waterjet systems, while local distributors form joint ventures with multinationals to navigate regulatory pathways. Japan and South Korea continue to function as early adopters for premium features such as 3-D imaging and AI modules, creating reference sites that influence neighboring markets.

Europe exhibits mature characteristics but still offers selective growth pockets. Stringent Medical Device Regulation (MDR) processes lengthen approval timelines, yet they also raise confidence in safety profiles, encouraging reimbursement once cleared. Germany and France prioritize cost-effectiveness analyses that reward technologies able to demonstrate shorter catheterization times and improved functional outcomes. Meanwhile, Central- and Eastern-European countries rely on European Union structural funds to upgrade surgical suites, providing incremental volume for value-oriented devices. The Middle East, Africa, and South America trail in penetration owing to price sensitivity and limited specialist density, though private-sector hospital chains in the Gulf Cooperation Council and Brazil are earmarking capital for flagship robotic programs.

Competitive Landscape

Competitive intensity is moderate as Boston Scientific, Teleflex, and Olympus bring scale advantages in procurement, sales reach, and service, while PROCEPT BioRobotics and Axonics emphasize focused innovation. Boston Scientific’s USD 3.7 billion acquisition of Axonics in February 2025 expands its urology portfolio into neuromodulation, indicating strategic convergence of continence and BPH management. PROCEPT BioRobotics leverages proprietary FirstAssist AI to lock in procedure algorithms that foster surgeon dependence and recurring disposables revenue.

Technology roadmaps highlight the integration of ultrasound, cystoscopy, and artificial intelligence into unified consoles that streamline workflow and data capture. Mid-tier challengers are developing lower-cost fiber-laser systems to penetrate emerging markets where per-patient budgets remain tight. At the opposite end of the spectrum, developers of prostatic artery embolization and drug-device combination implants seek to carve a share from traditional surgical modalities.

Supplier differentiation increasingly rests on health-economic dossiers that quantify reduced sexual side-effects and shortened length of stay, elements now central to payer contracting.

Benign Prostatic Hyperplasia (BPH) Treatment Devices Industry Leaders

Boston Scientific Corporation

Teleflex Incorporated.

Karl Storz

Cook Medical

Olympus Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: PROCEPT BioRobotics released WATER III data showing 14.8% ejaculatory dysfunction after Aquablation versus 77.1% for laser enucleation in prostates 80-180 mL.

- February 2025: Boston Scientific completed the USD 3.7 billion acquisition of Axonics, adding sacral neuromodulation devices for overactive bladder.

- December 2024: Teleflex launched UroLift 2 System with Advanced Tissue Control for prostates up to 100 g.

- August 2024: FDA granted 510(k) clearance for PROCEPT BioRobotics’ HYDROS AI-powered robotic system.

Global Benign Prostatic Hyperplasia (BPH) Treatment Devices Market Report Scope

Benign prostatic hyperplasia (BPH) treatment devices refer to medical tools and technologies specifically designed to manage and alleviate the symptoms of benign prostatic hyperplasia, a condition characterized by the non-cancerous enlargement of the prostate gland in men.

The prostatic hyperplasia (BPH) treatment devices market is segmented by device type, end user, and geography. By device type, the market is segmented into laser-based devices, transurethral resection devices (TURP), radiofrequency ablation devices, UroLift systems, microwave thermotherapy devices, high-intensity focused ultrasound (HIFU) devices, and others (catheters, prostatic stents, among others). By end user, the market is segmented into hospitals, ambulatory, surgical centers, and specialty clinics. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and Middle East and Africa. The report also offers the market size and forecasts for 17 countries globally. For each segment, the market sizing and forecasts were made on the basis of value (USD).

| Laser-Based Devices |

| Transurethral Resection Devices (TURP) |

| Radio-frequency Ablation Devices |

| UroLift Systems (Prostatic Urethral Lift) |

| Microwave Thermotherapy Devices |

| High-Intensity Focused Ultrasound (HIFU) |

| Robotic Waterjet Aquablation Systems |

| Other Devices |

| Hospitals |

| Ambulatory Surgical Centers (ASCs) |

| Specialty / Urology Clinics |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Device Type | Laser-Based Devices | |

| Transurethral Resection Devices (TURP) | ||

| Radio-frequency Ablation Devices | ||

| UroLift Systems (Prostatic Urethral Lift) | ||

| Microwave Thermotherapy Devices | ||

| High-Intensity Focused Ultrasound (HIFU) | ||

| Robotic Waterjet Aquablation Systems | ||

| Other Devices | ||

| By End User | Hospitals | |

| Ambulatory Surgical Centers (ASCs) | ||

| Specialty / Urology Clinics | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the Benign Prostatic Hyperplasia Treatment Devices market?

It is valued at USD 1.89 billion in 2026 and is forecast to reach USD 2.66 billion by 2031.

Which device segment is growing fastest?

Robotic Aquablation systems are projected to expand at an 8.34% CAGR through 2031, the highest among all device categories.

Why are ambulatory surgical centers gaining share?

ASCs perform BPH procedures at 40-60% lower cost than hospital outpatient departments and offer same-day discharge, driving a 9.62% CAGR.

How is artificial intelligence influencing BPH surgery?

AI platforms such as FirstAssist optimize resection zones and guide surgeons in real time, improving functional preservation and shortening learning curves.

What recent reimbursement changes favor market growth?

CMS assigned Category I CPT codes for Aquablation (effective 2026) and iTind (effective 2025), creating predictable payment pathways that encourage adoption.

Page last updated on: