Behavioral Health EHR Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

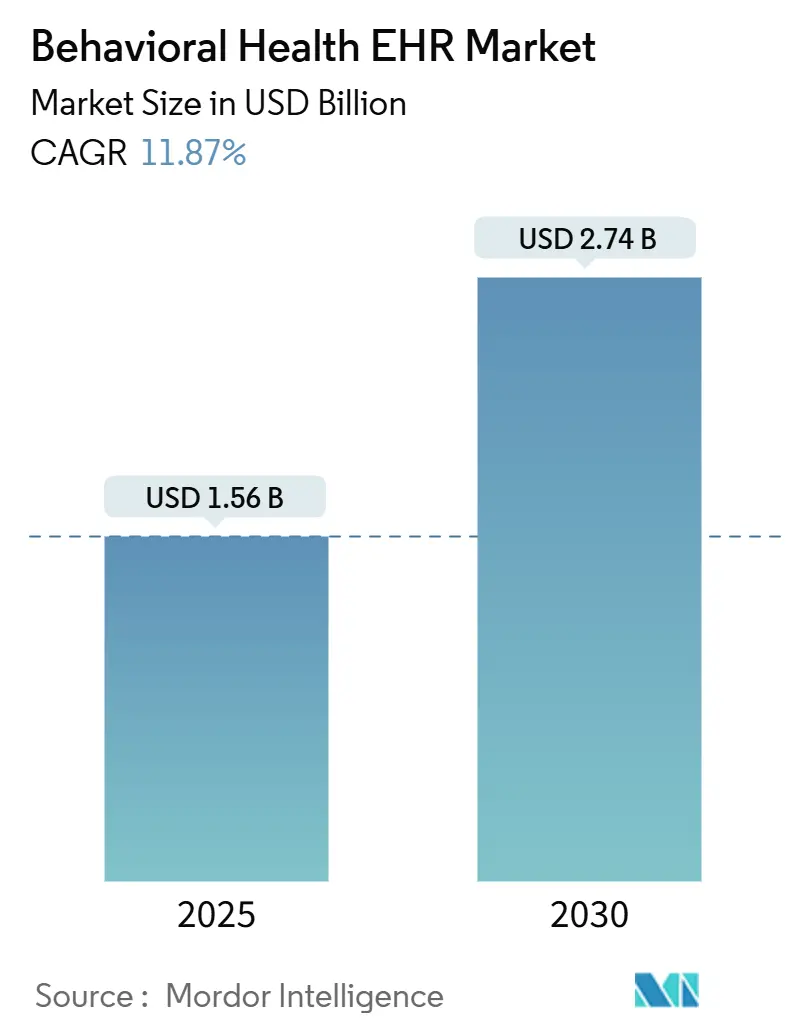

| Market Size (2025) | USD 1.56 Billion |

| Market Size (2030) | USD 2.74 Billion |

| Growth Rate (2025 - 2030) | 11.87% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Behavioral Health EHR Market Analysis by Mordor Intelligence

The behavioral health EHR market size reached USD 1.56 billion in 2025 and is projected to advance to USD 2.74 billion by 2030, reflecting an 11.87% CAGR. Robust demand stems from surging mental-health caseloads, stronger reimbursement incentives for integrated care, and rapid adoption of AI documentation tools that ease clinician burnout. The Centers for Medicare & Medicaid Services (CMS) Innovation in Behavioral Health Model, introduced in 2024, has opened new billing pathways for Rural Health Clinics and Federally Qualified Health Centers, directly accelerating platform uptake. Regulatory alignment of 42 CFR Part 2 with HIPAA in February 2024 lowered privacy-compliance complexity, especially for cloud vendors.[1]U.S. Department of Health and Human Services, “42 CFR Part 2 Final Rule Fact Sheet,” HHS, hhs.govMeanwhile, AI-driven ambient note capture, value-based outcome tracking, and seamless telehealth integration continue to differentiate vendors, prompting competitive acquisitions and venture funding across the ecosystem.

Key Report Takeaways

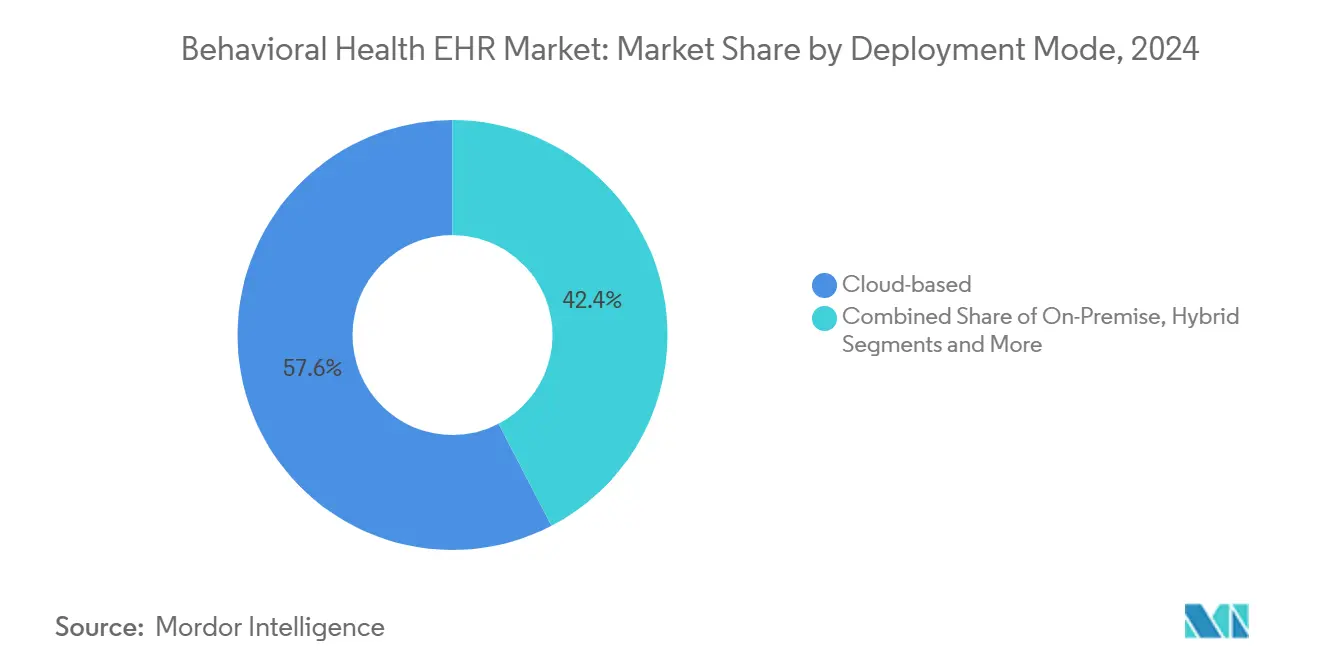

- By deployment mode, cloud-based systems captured 57.62% behavioral health EHR market share in 2024 and are on track for 15.79% CAGR through 2030.

- By functionality, clinical EHR cores held 41.57% of the behavioral health EHR market size in 2024, while telehealth integration modules are expanding at a 15.83% CAGR.

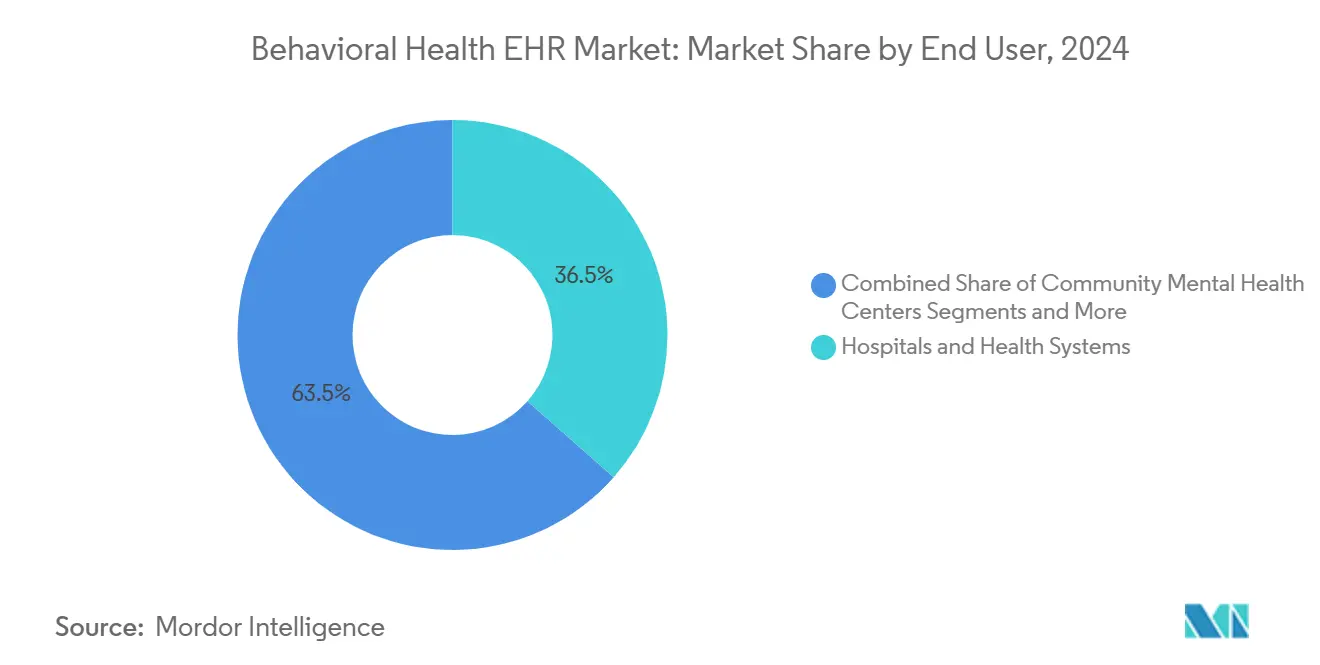

- By end user, hospitals and health systems commanded 36.51% behavioral health EHR market share in 2024, but private practices are set to post the fastest 14.32% CAGR.

- By component, software generated 68.74% of the behavioral health EHR market size in 2024, whereas services revenue is growing at 14.66% CAGR.

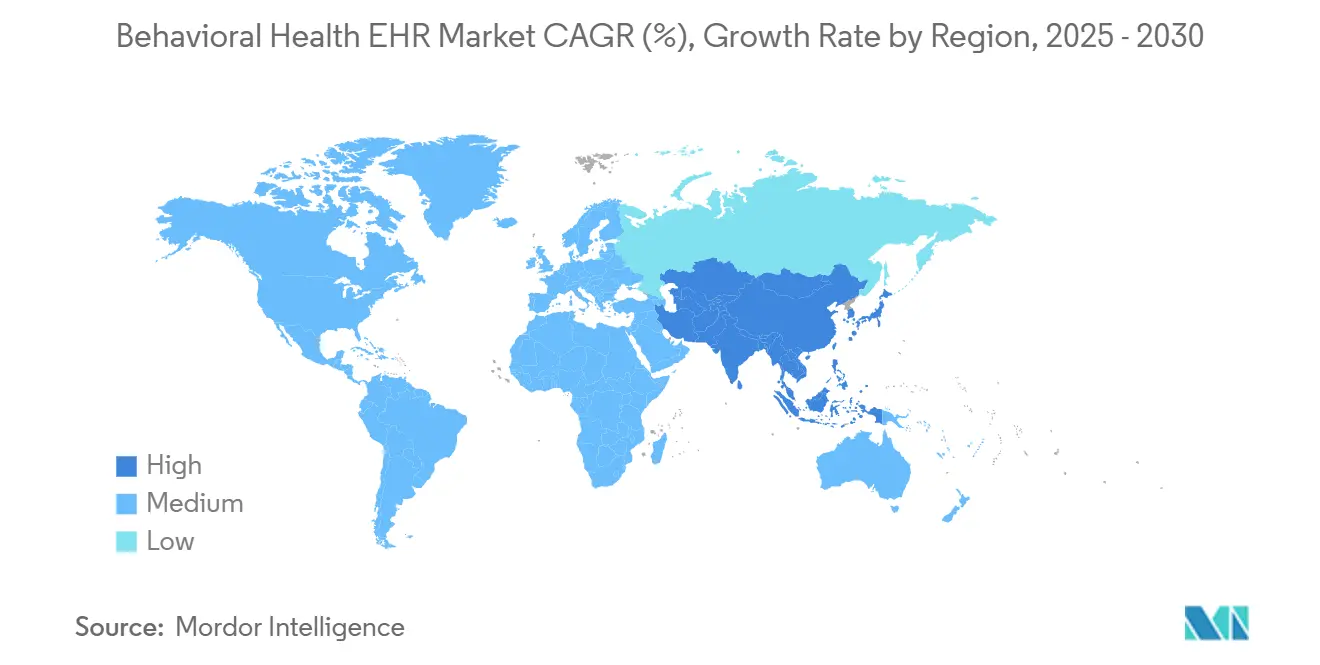

- By geography, North America led with 46.51% behavioral health EHR market share in 2024, yet Asia-Pacific is forecast to climb at a 13.72% CAGR to 2030.

Global Behavioral Health EHR Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| CMS Innovation in Behavioral Health Model reimbursement incentives | +2.8% | North America; spillover to Canada & Mexico | Medium term (2-4 years) |

| Telehealth-driven surge in cloud deployments | +2.1% | Global; highest in North America & Europe | Short term (≤ 2 years) |

| Interoperability mandates linking physical & mental-health data | +1.9% | Global; led by North America & Europe | Long term (≥ 4 years) |

| AI-powered clinical documentation assistants | +2.4% | Global; early adoption in developed markets | Medium term (2-4 years) |

| CCBHC Medicaid reporting requirements | +1.2% | United States | Short term (≤ 2 years) |

| Value-based contracts needing behavioral-outcome metrics | +1.3% | North America & Europe; expanding to Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

CMS Innovation in Behavioral Health Model Reimbursement Incentives

CMS launched the Innovation in Behavioral Health Model in 2024, letting Rural Health Clinics and Federally Qualified Health Centers bill new Behavioral Health Integration CPT codes. Reimbursement now hinges on outcome metrics such as depression-remission rates, intensifying demand for EHRs that capture behavioral-outcome data. The 2025 Medicare Physician Fee Schedule reinforces this shift by increasing payments for collaborative-care services. As population-health management becomes mandatory, platforms offering embedded analytics and value-based dashboards gain adoption. Together, these incentives accelerate purchases of purpose-built behavioral health EHR market solutions, particularly among community clinics serving high-acuity patients.

Telehealth-Driven Surge in Cloud Deployments

Post-pandemic hybrid care models depend on cloud infrastructure that allows real-time data sync, embedded video visits, and offline mobile charting. The February 2024 42 CFR Part 2 Final Rule harmonized behavioral-health privacy rules with HIPAA, streamlining cloud compliance. Telehealth modules consequently recorded the fastest 15.83% CAGR, driven by clinician demand for single-pane-of-glass workflows. Cloud hosting also supports automated billing-code pre-population, cutting administrative cycles that once constrained remote therapy expansion. As CMS introduces digital-mental-health reimbursement in 2025, cloud-first vendors are expected to consolidate behavioral health EHR market share across small practices and rural hubs.

Interoperability Mandates Linking Physical & Mental-Health Data

Federal initiatives such as TEFCA and the HTI-4 Final Rule, effective October 2025, mandate frictionless data-exchange and electronic prior authorization.[2]Steven Posnack, “Health Data, Technology, and Interoperability (HTI-4) Final Rule,” ONC / HealthIT.gov, healthit.gov Vendors like Netsmart, now a Qualified Health Information Network candidate, and Epic, pledging TEFCA participation, illustrate vendor realignment toward unified patient records. Behavioral health organizations must upgrade legacy systems or face non-compliance penalties, generating a replacement cycle favoring integrated platforms. The drive toward enterprise-wide interoperability positions solutions with robust APIs and standards-based exchange protocols for behavioral health EHR market growth.

AI-Powered Clinical Documentation Assistants Reduce Provider Burnout

Staff shortages intensify interest in AI ambient note-taking, which cuts session-note time by 23% according to clinical pilots.[3]Restraint (~) % Impact on CAGR Forecast Geographic Relevance Impact Timeline High customization costs & limited IT budgets -1.8% Global; higher in developing markets Medium term (2-4 years) Strict privacy regulations (e.g., 42 CFR Part 2) -1.2% United States; similar frameworks emerging globally Short term (≤ 2 years) Behavioral-health IT workforce attrition -1.6% Global; acute in rural regions Long term (≥ 4 years) Non-standardized behavioral-health coding -0.9% Global; varies by region Long term (≥ 4 years) Qualifacts’ iQ assistant, released July 2025, and NextGen’s ambient tools illustrate rapid mainstreaming of AI copilots. Slingshot AI’s “Ash,” the first therapy-specific large-language model, underscores movement toward specialized behavioral health AI rather than general medical NLP. With 1 in 4 clinicians already using AI tools, solutions that cut documentation time without eroding clinical rapport are poised for sustained adoption within the behavioral health EHR market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High customization costs & limited IT budgets | -1.8% | Global; higher in developing markets | Medium term (2-4 years) |

| Strict privacy regulations (e.g., 42 CFR Part 2) | -1.2% | United States; similar frameworks emerging globally | Short term (≤ 2 years) |

| Behavioral-health IT workforce attrition | -1.6% | Global; acute in rural regions | Long term (≥ 4 years) |

| Non-standardized behavioral-health coding | -0.9% | Global; varies by region | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Customization Costs & Limited IT Budgets

Community mental-health centers often face implementation fees topping USD 50,000, well beyond reach for many small providers. The 2025 HIPAA Security Rule update is projected to add USD 9 billion in first-year compliance spending, disproportionately straining mental-health organizations. Budget constraints push some facilities toward stripped-down solutions that lack AI tools or tight telehealth integration, hampering efficiency gains. Delays in upgrades stunt interoperability readiness, exposing providers to reimbursement penalties tied to federal programs. Without targeted grants or vendor financing, high costs remain a stubborn drag on behavioral health EHR market expansion.

Strict Privacy Regulations (42 CFR Part 2)

Although 2024 revisions aligned 42 CFR Part 2 with HIPAA, substance-use data still requires explicit patient consent for every disclosure, complicating information-exchange workflows. Vendors must engineer granular consent-management modules, adding development expense and prolonging implementation. Smaller practices, lacking compliance staff, may postpone EHR adoption to avoid legal exposure. Emerging global privacy statutes modeled on U.S. standards could replicate these barriers in new markets. Consequently, privacy regulation remains a measured headwind to behavioral health EHR market adoption, even amid regulatory harmonization.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Mode: Cloud Migration Accelerates

Cloud solutions dominated the behavioral health EHR market size with 57.62% share in 2024 and are advancing at a 15.79% CAGR. Vendors benefit from the 2024 alignment of 42 CFR Part 2 with HIPAA, which removed key data-segmentation hurdles for hosted environments. On-premise installations persist at large health systems prioritizing sovereign data control, yet their growth remains tepid. Hybrid models provide a stepping-stone for institutions moving workloads gradually to the cloud while preserving local servers for archival data.

A landmark project at Brattleboro Retreat deployed MEDITECH Expanse via a fully hosted model in 2024, enabling clinicians to document on mobile tablets directly at patient bedsides. Real-time data-exchange through Netsmart’s 360X referrals and Epic’s planned TEFCA connectivity illustrate how cloud platforms enhance care-coordination across fragmented networks. As value-based contracts multiply, cloud analytics deliver actionable insights at lower total cost of ownership, cementing cloud as the preferred deployment for the behavioral health EHR market.

By Functionality: Telehealth Integration Drives Innovation

Core clinical modules accounted for 41.57% behavioral health EHR market share in 2024, yet telehealth integration is the fastest-growing component at 15.83% CAGR. The rise of hybrid care demands embedded video visits, automated charge capture, and mobile-optimized scheduling. CMS reimbursement for digital mental-health treatments, slated for 2025, is fueling rapid functionality bundling within single platforms. Administrative and revenue-cycle modules grow in importance as practices juggle multiple payer rules and new Behavioral Health Integration CPT codes.

The University of Utah Health demonstrated AI-generated treatment plans inside its enterprise EHR, signaling convergence between decision support and traditional charting. Analytics suites that visualize depression-remission trends or medication adherence are turning once-static records into population-health engines. This functionality mix positions integrated suites to outpace point solutions in the behavioral health EHR market.

By End User: Private Practices Embrace Specialization

Hospitals and health systems held 36.51% behavioral health EHR market share in 2024, leveraging enterprise budgets for system consolidation. Private practices, however, are growing at a 14.32% CAGR as they seek specialized workflows and AI-native tools absent in generic medical systems. ProsperityEHR, launched in March 2025 by former Epic executives, specifically targets small behavioral-health offices with AI-ready architecture and streamlined revenue-cycle automation. Community mental-health centers remain important early adopters, often piloting novel features before hospital uptake.

White Bird Clinic’s partnership with Qualifacts Credible illustrates workflow transformation achievable through domain-specific platforms, cutting intake time and boosting appointment throughput. As reimbursement models grow more complex, small providers gravitate toward purpose-built behavioral health EHR market offerings that align with niche billing and documentation needs.

By Component: Services Growth Reflects Implementation Complexity

Software licenses represented 68.74% of the behavioral health EHR market size in 2024, yet services revenue is growing 14.66% CAGR as organizations grapple with customization, training, and compliance. LA County Department of Mental Health’s network—serving 250,000 individuals through 150 providers—relies on extensive Netsmart consulting to manage data governance across its ecosystem. Training services also mitigate workforce shortages by developing in-house super-users who can optimize templates and analytics dashboards post-go-live.

Rapid regulatory changes such as HTI-4 certification for prior authorization elevate ongoing support costs. Consequently, total cost of ownership is tilting toward services, a trend vendors now monetize through subscription-based managed-services packages, driving incremental behavioral health EHR market revenue.

Geography Analysis

North America controlled 46.51% behavioral health EHR market share in 2024, buoyed by federal reimbursement programs and mature health-IT infrastructure. CMS incentives, TEFCA mandates, and widespread broadband access give U.S. providers the tools—and penalties—to adopt integrated systems rapidly. Canada and Mexico benefit from cross-border vendor ecosystems and knowledge transfer, although funding variability affects adoption pace.

Asia-Pacific is the fastest-growing regional cluster at 13.72% CAGR through 2030. Australia’s National Interoperability Plan, Japan’s AI-enabled psychiatry pilots, and India’s expanding mental-health budget collectively spur demand. Implementation barriers remain—Indonesia confronts rural connectivity gaps, while China’s evolving data-sovereignty laws impose hosting constraints—yet state-funded digitization drives sustained behavioral health EHR market growth.

Europe maintains steady expansion under GDPR and forthcoming European Health Data Space regulations. Stringent privacy standards create competitive openings for vendors offering granular consent management. In the Middle East, Gulf Cooperation Council states boast 75% EHR penetration across public facilities, aligning with Saudi Arabia’s Vision 2030 telemedicine goals. Africa’s progress is uneven, but Botswana’s teaching-hospital go-live on MEDITECH Expanse proves advanced deployments are feasible when paired with donor funding. South America’s digital-mental-health pilots in Brazil and Colombia further illustrate global appetite for integrated solutions.

Competitive Landscape

The behavioral health EHR market is fragmented. Netsmart leads satisfaction rankings at 9.7/10 due to community-care depth. Epic’s vast footprint in acute hospitals translates into cross-sell opportunities but less specialization. Oracle Health, despite AI upgrades, faces inertia in behavioral-health specific features.

Consolidation is accelerating. TT Capital Partners bought Cantata Health Solutions in January 2025 to blend revenue-cycle strengths with behavioral-health workflows. Warburg Pincus acquired Qualifacts for USD 300 million, signaling private-equity confidence in niche platforms. Venture capital also flows to AI-native challengers: JotPsych raised USD 5 million for a fully agentic EHR, while Slingshot AI secured seed funding to embed therapy-honed language models inside existing platforms.

Strategic roadmaps now converge on three pillars: AI-driven documentation, TEFCA-ready interoperability, and value-based analytics. Vendors scoring high on these capabilities are projected to outstrip peers and consolidate behavioral health EHR market positions over the next five years.

Behavioral Health EHR Industry Leaders

Netsmart Technologies

Oracle Health (Cerner)

Epic Systems

Qualifacts (Credible)

NextGen Healthcare

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: HHS finalized the HTI-4 rule enhancing prior authorization and e-prescribing interoperability, setting new EHR certification criteria effective October 2025.

- July 2025: Slingshot AI launched “Ash,” the first AI designed exclusively for therapy sessions.

- May 2025: Silver Hill Hospital selected MEDITECH Expanse EHR to integrate care across psychiatric services.

- March 2025: Official launch of ProsperityEHR, an innovative electronic health record platform designed specifically for behavioral health organizations

Global Behavioral Health EHR Market Report Scope

| Cloud-based |

| On-Premise |

| Hybrid |

| Clinical (EHR core) |

| Administrative & Scheduling |

| Financial / Revenue-Cycle |

| Telehealth Integration |

| Analytics & Population Health |

| Community Mental Health Centers |

| Hospitals & Health Systems |

| Private Practices |

| Residential & Long-term Care Facilities |

| Payers & Managed Behavioral Health Orgs |

| Software |

| Services (Implementation, Training, Support) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Deployment Mode | Cloud-based | |

| On-Premise | ||

| Hybrid | ||

| By Functionality / Module | Clinical (EHR core) | |

| Administrative & Scheduling | ||

| Financial / Revenue-Cycle | ||

| Telehealth Integration | ||

| Analytics & Population Health | ||

| By End User | Community Mental Health Centers | |

| Hospitals & Health Systems | ||

| Private Practices | ||

| Residential & Long-term Care Facilities | ||

| Payers & Managed Behavioral Health Orgs | ||

| By Component | Software | |

| Services (Implementation, Training, Support) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How big is the behavioral health EHR market in 2025?

It is valued at USD 1.56 billion and is projected to reach USD 2.74 billion by 2030 at an 11.87% CAGR.

Which deployment mode is growing fastest?

Cloud-based platforms lead with a 15.79% CAGR, driven by privacy-rule harmonization and telehealth demand.

Which region is set for the quickest expansion?

Asia-Pacific is forecast to grow at 13.72% CAGR through 2030 as governments mandate EHR adoption.

What’s the main driver behind recent EHR upgrades?

CMS reimbursement incentives that now pay for integrated behavioral-health services are spurring system replacements.

Why are services revenues rising?

Complex customization, training, and compliance needs are pushing organizations to buy consulting and managed services.

Which functionality segment is expanding fastest?

Telehealth integration modules are advancing at 15.83% CAGR as hybrid care becomes standard.

Page last updated on: