Barretts Esophagus Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

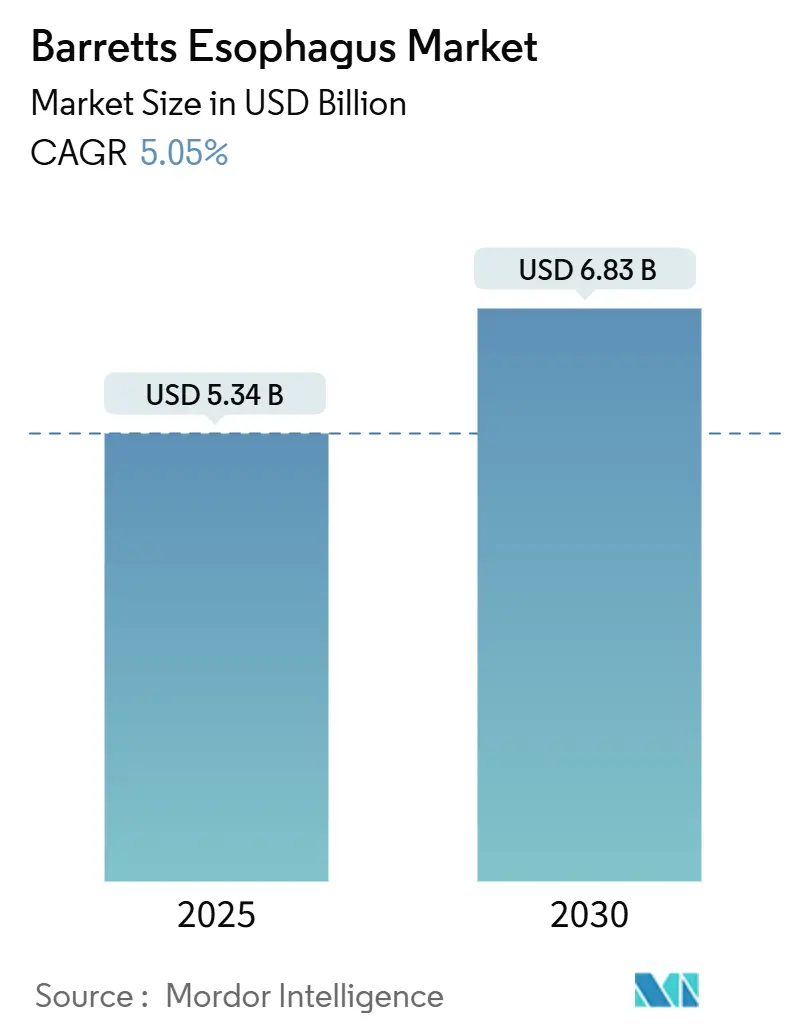

| Market Size (2025) | USD 5.34 Billion |

| Market Size (2030) | USD 6.83 Billion |

| Growth Rate (2025 - 2030) | 5.05% CAGR |

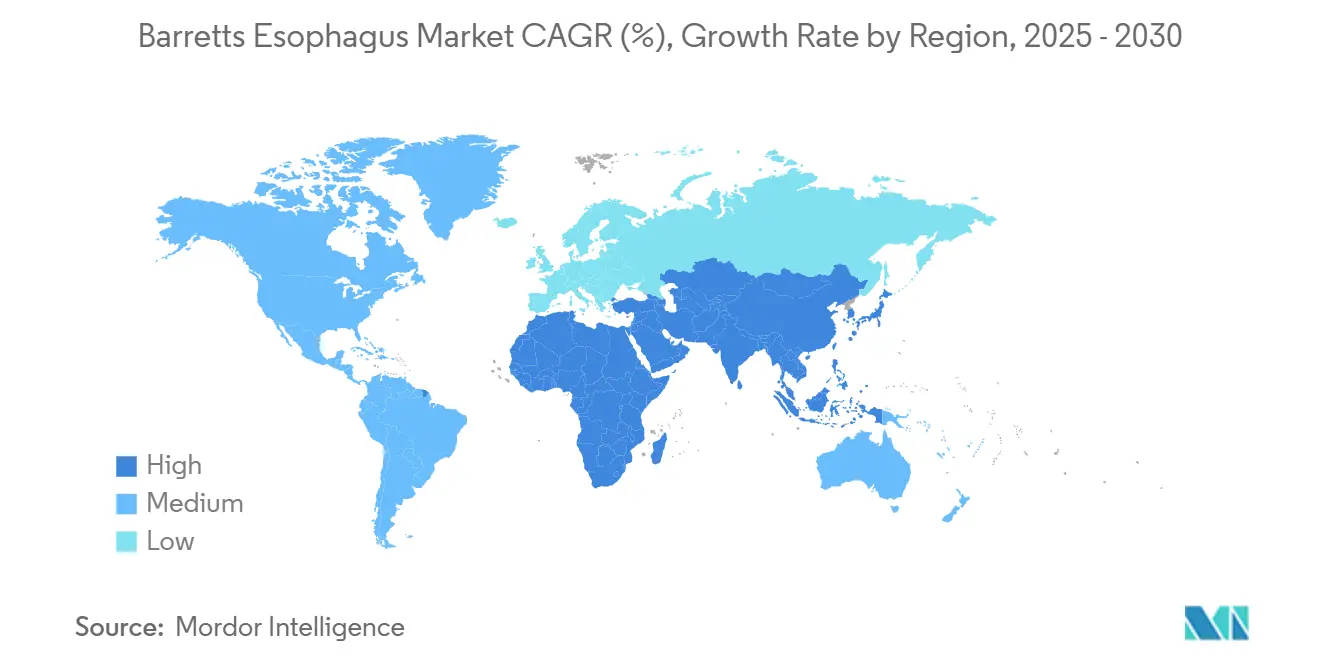

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Barretts Esophagus Market Analysis by Mordor Intelligence

The Barrett's esophagus market size reached USD 5.34 billion in 2025 and is projected to climb to USD 6.83 billion by 2030, reflecting a 5.05% CAGR over the forecast window. Demand momentum stems from the confluence of rising gastroesophageal reflux disease (GERD) prevalence, rapid uptake of computer-aided endoscopy, and expanding reimbursement for ablative therapies. Market incumbents are deploying artificial-intelligence (AI) modules that raise dysplasia detection accuracy while shortening procedure times, an advance that strengthens product differentiation and pricing power. Cryotherapy’s favorable tolerance profile is broadening patient acceptance, whereas regenerative cell-sheet research signals a longer-horizon shift toward tissue-restoration protocols. Competitive intensity is moderate, with technology partnerships and targeted acquisitions—most notably Olympus’s 2025 purchase of cloud-AI startup Odin Vision—demonstrating a willingness among leading firms to internalize data-science capabilities.

Key Report Takeaways

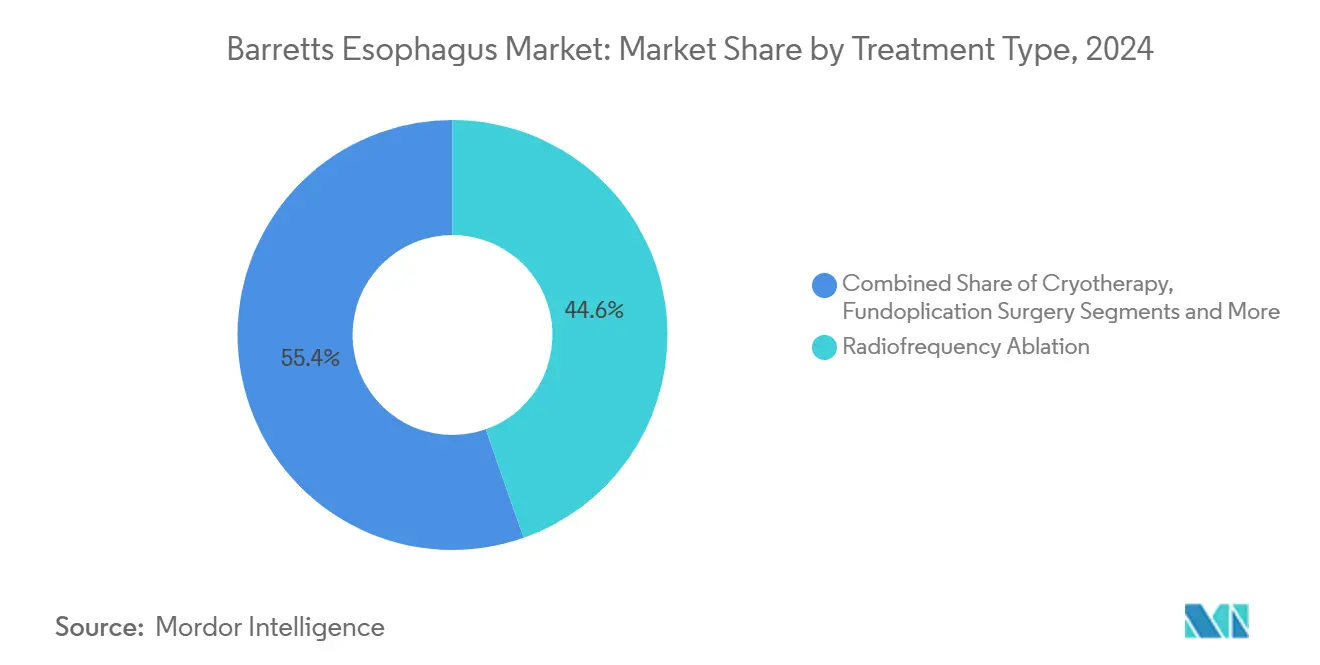

- By treatment type, radiofrequency ablation retained 44.62% of Barrett's esophagus market share in 2024, while cryotherapy is advancing at a 9.26% CAGR through 2030.

- By diagnosis modality, endoscopy captured 61.36% of the Barrett's esophagus market size in 2024; advanced imaging methods are set to expand at an 8.35% CAGR.

- By disease stage, non-dysplastic Barrett’s accounted for 49.25% of 2024 revenue; high-grade dysplasia is forecast to post the fastest 7.32% CAGR to 2030.

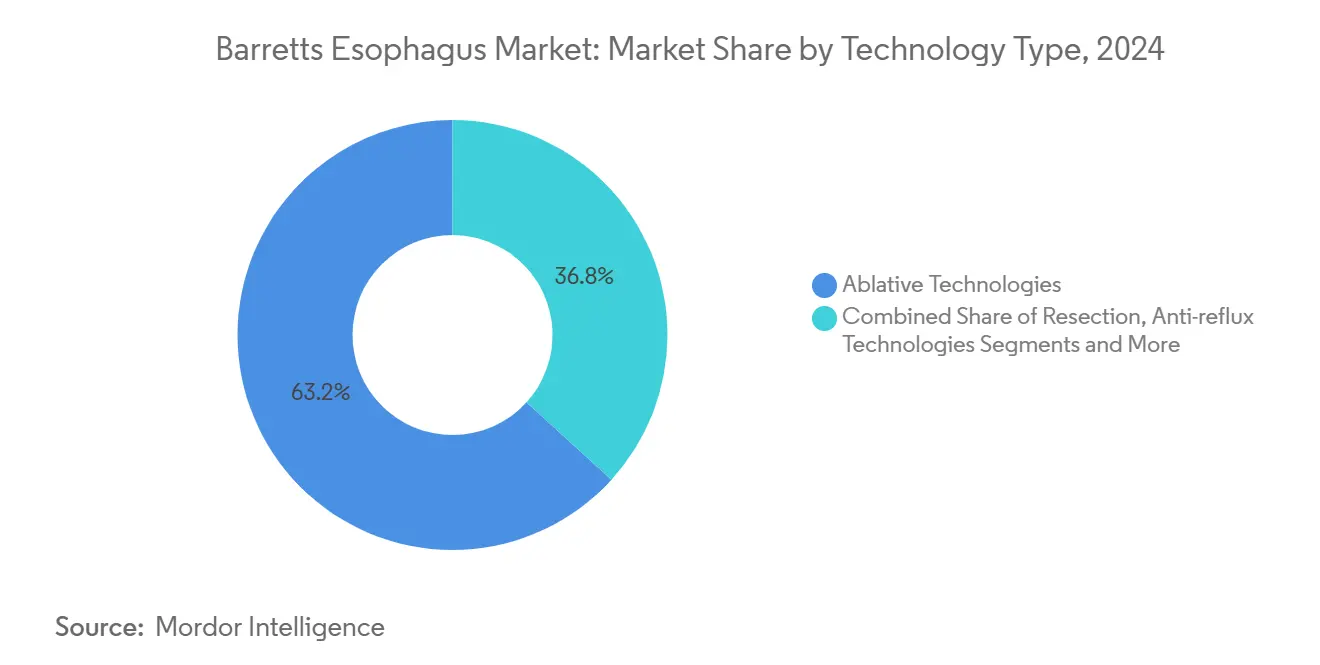

- By technology type, ablative platforms dominated with 63.24% revenue in 2024, whereas diagnostic imaging and molecular tests are growing at an 8.42% CAGR.

- By end user, hospitals controlled 57.81% of 2024 spending; ambulatory surgical centers are projected to rise at a 7.03% CAGR as outpatient protocols gain traction.

- North America led with 39.66% of 2024 global revenue; Asia-Pacific is expected to log the highest 7.64% regional CAGR through 2030.

Global Barretts Esophagus Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Prevalence Of GERD & Obesity | +1.2% | Global, with early gains in North America, Europe | Medium term (2-4 years) |

| Increasing Adoption Of Minimally-Invasive Endoscopic Ablation Techniques | + 0.9% | North America & EU, spill-over to APAC | Short term (≤ 2 years) |

| Growing Availability Of Reimbursement For RFA Procedures | + 0.8% | North America core, expanding to EU markets | Medium term (2-4 years) |

| Expansion Of Screening Programs For High-Risk Populations | + 0.7% | APAC core, spill-over to MEA | Long term (≥ 4 years) |

| AI-Enabled Real-Time Dysplasia Detection Tools Improving Procedure Yield | + 1.1% | Global, with concentrated adoption in tertiary centers | Short term (≤ 2 years) |

| Emergence Of Regenerative Cell Sheets To Restore Esophageal Mucosa | + 0.3% | Japan, South Korea, with early research in North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of GERD and Obesity

The sharp climb in global GERD incidence, now affecting roughly 20% of adults, creates a direct feeder pool for Barrett’s metaplasia.[1]Sung-Ho Kim et al., “Unveiling the Intricacies: Insight into GERD,” wjgnet.com Population-level studies covering 2.3 million patients pinpoint obesity as an independent risk factor, with an odds ratio of 1.08 and stronger effects observed in women and Caucasian cohorts.[2]Peter Kahrilas et al., “Obesity and Reflux Complications,” onlinelibrary.wiley.com Visceral adiposity raises intra-abdominal pressure, thereby intensifying reflux episodes that accelerate columnar transformation in the distal esophagus. Bariatric interventions such as sleeve gastrectomy can paradoxically elevate Barrett’s risk over five-year horizons, underscoring the multifactorial nature of disease progression. The resulting patient backlog fuels sustained demand for surveillance and eradication therapies within the Barrett's esophagus market.

Accelerating Shift to Minimally Invasive Endoscopic Ablation

Endoscopic eradication therapy now supplants esophagectomy for most dysplastic cases, with radiofrequency ablation (RFA) eliminating dysplasia in more than 90% of treated patients while conserving healthy tissue layers.[3]Mass General Hospital, “Radiofrequency Ablation Treatment for Barrett's Esophagus,” massgeneral.org Liquid-nitrogen cryotherapy reduces procedure-related pain fivefold versus RFA, which spurs accelerated adoption among centers prioritizing patient-reported outcomes.[4]Joshua Melson et al., “Liquid Nitrogen Spray Cryotherapy Reduces Pain,” lww.comSpray cryotherapy achieves 76% complete remission in RFA-refractory disease, addressing an otherwise undertreated subgroup. Combination strategies pairing endoscopic mucosal resection with subsequent ablation deliver 98.8% eradication and furnish histologic staging data that guide personalized follow-up. Collectively, these minimally invasive options reinforce procedural migration toward outpatient platforms, amplifying growth across device and service lines of the Barrett's esophagus market.

AI-Enabled Real-Time Dysplasia Detection Improving Yield

Machine-vision algorithms embedded in next-generation endoscopes register 93.8% sensitivity and 90.7% specificity for Barrett’s neoplasia, decisively outperforming unaided examiners. Fujifilm’s CAD EYE adds 17% to adenoma detection rates and cuts lesion measurement time to 2.8 seconds, illustrating tangible workflow efficiencies. Prospective trials at Mayo Clinic recorded a 38.6% adenoma detection rate with AI assistance versus 34.2% in comparator arms, indicating real-world clinical gain. Beyond identification, automated report generation and quality-metric dashboards reduce documentation omissions that can hinder reimbursement. As tertiary centers validate these benefits, adoption cascades into secondary facilities, enlarging the install base for premium imaging systems inside the Barrett's esophagus market.

Expanding Reimbursement for Radiofrequency Ablation

The 2025 MIPS Quality Measure #249 obliges U.S. providers to document Barrett’s morphology and dysplasia, linking compliance to performance incentives that stimulate procedure volumes. Medicare now reimburses RFA for both high- and low-grade dysplasia upon expert confirmation, broadening eligibility beyond earlier narrow guidelines. Private payers mirror federal policy; Capital BlueCross in late 2024 deemed RFA medically necessary for low-grade cases, smoothing prior authorization pathways. These policies collectively remove financial friction, accelerate referral patterns, and elevate device utilization across hospital and ambulatory settings, directly bolstering the Barrett's esophagus market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital Cost Of Advanced Endoscopic Systems | -0.6% | Global, particularly affecting emerging markets | Medium term (2-4 years) |

| Limited Specialist Skillset Outside Tertiary Centers | -0.4% | APAC, MEA, with training gaps in rural North America | Long term (≥ 4 years) |

| Uncertain Long-Term Durability Of Some Ablative Modalities | -0.3% | Global, affecting treatment selection protocols | Medium term (2-4 years) |

| Competition From Non-Endoscopic Cell-Capture Diagnostics | -0.2% | North America & EU, with FDA-cleared alternatives | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Capital Outlay for Advanced Endoscopic Platforms

Comprehensive AI-ready imaging towers, 4K monitors, and disposable ablation catheters command upfront investments that can exceed USD 400,000 per suite, straining budgets for smaller hospitals and public institutions. Annual maintenance contracts, software licensing, and staff certification fees compound the barrier. Emerging markets face import tariffs and currency volatility that widen the affordability gap, delaying technology refresh cycles. Although financing options and pay-per-procedure models exist, uptake remains inconsistent, capping device penetration in cost-sensitive geographies. As a result, revenue expansion within segments of the Barrett's esophagus market that rely on premium capital equipment sees pockets of underperformance relative to headline growth.

Limited Specialist Skillsets Beyond Tertiary Centers

Technically demanding procedures such as circumferential endoscopic mucosal resection or hybrid dissection require expertise concentrated in academic hubs. Rural providers often lack exposure to high-volume training curricula endorsed by societies like ESGE, impeding diffusion of advanced care protocols. Without skilled operators, community centers default to surveillance or refer patients long distances, prolonging wait times and elevating disease-progression risk. Tele-mentoring and simulation models, including Fujifilm’s EndoGel, are closing knowledge gaps yet scale-up remains gradual. This workforce imbalance tempers growth potential across secondary and tertiary catchment areas of the Barrett's esophagus market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Treatment Type: Cryotherapy Gains Ground Against Thermal Dominance

Radiofrequency ablation commanded 44.62% of 2024 revenue, making it the single-largest contributor to Barrett's esophagus market size. Nevertheless, cryotherapy’s 9.26% forecast CAGR signals a pivot toward cold-energy modalities that promise deeper tissue penetration with milder post-procedure discomfort. Liquid nitrogen systems record 76% complete remission in cases unresponsive to RFA, thereby converting salvage cohorts into viable revenue streams for device manufacturers. Endoscopic mucosal resection fills a specialized role, excising discrete nodules while supplying en-bloc histology that guides subsequent ablation schedules. Photodynamic therapy declines due to prolonged photosensitivity and reimbursement attrition, whereas anti-reflux surgery maintains relevance for anatomical repair coupled with durable dysplasia regression. Clinical protocols now favor staged combinations—mucosal resection followed by thermal or cryo ablation—to maximize complete eradication and minimize recurrence, reinforcing multi-device utilization patterns in the Barrett's esophagus market.

The therapeutic mix shapes procurement cycles: hospitals invest in both RFA and cryo consoles to cover heterogeneous pathology, while ambulatory centers select platforms that balance capital cost with procedure breadth. Training accreditation from specialty societies encourages cross-modality competence, and manufacturers bundle devices with performance dashboards that track eradication rates, easing quality reporting obligations. These dynamics create a layered competitive field where differentiated disposables, service contracts, and algorithm-enabled consoles vie for share within the Barrett's esophagus market.

By Diagnosis Modality: Imaging Innovation Redefines Gold Standards

Endoscopy remained the diagnostic anchor with 61.36% of 2024 sales, yet imaging-enhanced systems are slated to outpace base-scope growth at an 8.35% CAGR. Narrow-band imaging and chromoendoscopy raise dysplasia detection without adding dye costs, and Olympus’s EZ1500 series employs Extended Depth of Field optics that sharpen lesion visualization at variable distances. Biopsy remains essential for histologic confirmation, but wide-area transepithelial sampling (WATS3D) lifts incremental dysplasia yield by 140% over Seattle-protocol biopsies, expanding laboratory revenue. Non-endoscopic devices such as EsoCheck win 95% patient preference, serving as triage tools that funnel high-risk candidates toward confirmatory endoscopy. Regulatory frameworks adapt: the U.S. FDA accelerates 510(k) pathways for adjunctive AI software, while ISO committees draft new QA metrics for digital pathology. Together, these milestones sustain double-digit growth trajectories in the diagnostic slice of the Barrett's esophagus market.

Market participants now cross-license AI libraries, marry cloud analytics with hardware, and roll out subscription models that monetize software updates. Payors observe rising diagnostic sensitivity and, in turn, authorize billing codes for computer-assisted procedures, reinforcing revenue uplifts. In emerging economies, portable capsule endoscopy with machine-learning triage promises to democratize early detection at primary-care clinics, underscoring a future where imaging innovation drives geographic expansion of the Barrett's esophagus market.

By Disease Stage: High-Grade Dysplasia Escalates Intervention Urgency

Non-dysplastic Barrett’s formed 49.25% of 2024 revenue, underscoring the surveillance workload that endoscopy units shoulder every three to five years. Yet high-grade dysplasia will deliver the swiftest 7.32% CAGR as improved imaging pushes earlier identification and guideline updates favor active eradication over watchful waiting. Annual malignant transformation risk jumps from 0.12% in non-dysplastic to multi-percentage territory in dysplastic subtypes, driving therapeutic conversion. Low-grade dysplasia now moves quickly to RFA once expert confirmation is obtained, reflecting mounting evidence that early ablation halves cancer progression. Early esophageal adenocarcinoma benefits from submucosal dissection, especially in East-Asian centers reporting 61% curative resections with low perforation rates. Adjunctive aspirin regimens undergo trial evaluation for post-ablation recurrence prevention. This stage-specific care escalation increases procedure frequency per patient, pushing up device utilization rates and recurring revenues across the Barrett's esophagus market.

Commercial implications include rising demand for multi-band ligation caps, electrosurgical generators with fine energy modulation, and disposable snare kits tailored to lesion morphology. Pharmaceutical tie-ins emerge as acid suppression and anti-inflammatory medications become standard adjuncts, creating co-marketing opportunities between device firms and drug manufacturers. As electronic health-record prompts flag dysplasia grade, referral pipelines to interventional endoscopists shorten, lifting quarterly case volumes and fortifying the stage-driven revenue mix in the Barrett's esophagus market.

By Technology Type: Diagnostics Challenge Ablative Supremacy

Ablative systems contributed 63.24% of 2024 turnover, but diagnostics are on track for an 8.42% CAGR on AI momentum. Fujifilm’s CAD EYE, Olympus’s EVIS X1, and Medtronic’s GI Genius expand detection accuracy and push consumable demand for enhanced imaging catheters. Resection devices sustain mid-single-digit growth as training programs propagate, and Duette kits enable circumferential mucosectomy for >10 cm segments with video-guided precision. Anti-reflux implants such as magnetic sphincter augmentation add a functional dimension, achieving 72% regression in short-segment Barrett’s after one year. Diagnostic advances further include epigenetic assays like Esopredict, now under Castle Biosciences, forecasting progression risk and shaping individualized follow-up intervals. Patient-derived organoids, although still pre-commercial, foreshadow ex vivo drug screening that could redirect therapy selection. Combined, these innovations narrow the historical dominance of ablation and diversify revenue sources inside the Barrett's esophagus market.

Manufacturers increasingly bundle capital hardware with cloud dashboards and disposable kits, locking in recurring revenue while elevating switching costs. Venture financing flows toward software-defined imaging modules, whereas established players hedge with targeted M&A to acquire algorithmic IP. Technology breadth thereby becomes a key determinant of vendor rankings, intensifying differentiation warfare across the Barrett's esophagus market.

By End User: Ambulatory Rise Redefines Site-of-Service Economics

Hospitals maintained 57.81% of 2024 receipts owing to critical care backup and multidisciplinary case review boards. Yet ambulatory surgical centers (ASCs) will increase at a 7.03% CAGR as procedure times shrink to 25-35 minutes and same-day discharge becomes routine. ASCs appeal to payors for lower facility fees and to patients for streamlined scheduling, driving network operators to add endoscopic suites equipped for both RFA and cryotherapy. Specialty clinics tied to academic hospitals blend research, advanced imaging trials, and continuing-education programs that attract regional referrals. Cost-containment measures favor high-throughput outpatient settings, prompting device firms to tailor training and service packages for ASC staff who manage post-procedural bleeding and stricture risks. Regulatory oversight through CLIA and CAP ensures quality parity; molecular assays like EsoGuard submit to proficiency testing, embedding laboratory workflows within community practices. Shifts in site-of-service mix reallocate capital expenditures and reorder procurement cycles, enhancing outpatient visibility within the Barrett's esophagus market.

Value-based-care contracts increasingly reimburse per-episode rather than per-setting, prompting hospitals to develop joint-venture ASCs to retain procedural revenue. Device makers respond with compact consoles and modular towers that fit space-constrained facilities, while offering cloud connectivity for remote troubleshooting. These dynamics cement outpatient channels as growth engines in the Barrett's esophagus market.

Geography Analysis

North America held 39.66% of 2024 global revenue, anchored by Medicare expansion for RFA and mandated Barrett’s documentation under MIPS #249. The region benefits from early AI adoption; Mayo Clinic and leading integrated-delivery networks standardize computer-assisted imaging that lifts detection benchmarks while supporting quality-metric compliance. Johnson & Johnson’s LINX labeling extension brings anti-reflux implants into Barrett’s care pathways, allowing 71% of treated patients to discontinue daily reflux medication, a statistic that underpins robust procedural growth. NIH grants, including a USD 8 million award to University Hospitals, invigorate translational research into non-endoscopic screening, enlarging the addressable cohort in community settings. However, rural shortages of advanced endoscopists persist, sustaining interest in capsule-sponge technologies that primary-care teams can administer.

Asia-Pacific is forecast to log the fastest 7.64% CAGR as GERD prevalence catches up with Western levels and health systems invest in optical magnification platforms. Japanese centers report short-segment Barrett’s rates approaching 2%, while Vietnamese studies cite 2.4% prevalence with hiatal hernia presenting a 7.53 odds ratio. Iran displays regional spikes to 10.7% in Yazd province, hinting at genetic or dietary modifiers that may guide future preventive strategies. The Asia-Pacific Barrett’s Consortium promotes narrow-band imaging, yet heterogeneous training standards hamper uniform uptake. Regulatory agencies prioritize local-data submissions; thus, multinationals often partner with domestic academic hubs to secure product registrations, feeding localized innovation loops. Hospitals in tier-1 Chinese cities and metropolitan India adopt AI-ready scopes, while outer-province facilities lean on cost-efficient capsule screening, together widening the regional revenue base of the Barrett's esophagus market.

Europe maintains mid-single-digit expansion, shaped by Medical Device Regulation (MDR) timelines that extend into 2028 and require comprehensive clinical evidence for product recertification. Olympus’s Odin Vision integration enhances cloud-analytics availability across EU endoscopy suites, while Fujifilm’s EndoGel model aids proficiency in submucosal dissection techniques. Prescription of novel potassium-competitive acid blockers such as vonoprazan expands pharmacologic control of reflux, complementing procedural interventions and reinforcing demand for diagnostic follow-up. Regional reimbursement varies: Germany’s statutory insurers broadly cover RFA and endoscopic resections, while southern European systems move slower, causing uneven penetration. Nevertheless, harmonized training curricula and cross-border clinical networks sustain knowledge transfer, fostering gradual but resilient growth in the Barrett's esophagus market.

Competitive Landscape

The Barrett's esophagus market supports moderate concentration: top global suppliers Medtronic, Boston Scientific, and Olympus collectively leverage diversified product portfolios that incorporate RFA, cryotherapy, and AI-enabled imaging. Medtronic’s Barrx franchise remains the procedural mainstay for dysplasia eradication, strengthened by a decade of safety data and widespread physician familiarity. Olympus escalated its digital strategy via a USD 66 million acquisition of Odin Vision, securing proprietary computer-vision algorithms that boost real-time lesion recognition and record-keeping efficiency. Boston Scientific reported USD 4.663 billion in Q1 2025 revenue, pointing to robust endoscopy-segment sales and underscoring the commercial durability of its hemostasis and retrieval toolkits.

Adjacent technology firms pursue strategic bolt-ons: Castle Biosciences absorbed Previse to acquire the Esopredict molecular test that predicts progression to high-grade dysplasia, giving the company a foothold in surveillance-centric revenue streams. Merit Medical invested USD 105 million to purchase Endogastric Solutions, anchoring competitiveness in anti-reflux implants that complement ablation therapies. Emerging disruptors such as Cyted receive 510(k) clearance for capsule sponge collection devices, lowering screening barriers in primary-care contexts. Lumicell’s NIH-backed fluorescence platform targets early lesion mapping, indicating that imaging sophistication remains a core battleground.

Strategic differentiation hinges on AI integration, user experience, and outcome documentation. Vendors bundle cloud dashboards, predictive analytics, and streamlined billing modules to secure long-term contracts. Training ecosystems—spanning virtual reality simulators, on-site proctoring, and performance certificates—further lock in customer loyalty. As a result, market leaders fortify their positions even as nimble entrants exploit niche segments, maintaining a dynamic yet balanced competitive environment within the Barrett's esophagus market.

Barretts Esophagus Industry Leaders

Medtronic plc

Boston Scientific Corp.

Cook Medical LLC

Olympus Corp.

STERIS plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: ProPhase Labs received U.S. Patent No. 12379378-B2 for BE-Smart biomarker methods that achieved more than 95% technical success in cytology and forceps biopsy specimens.

- May 2025: Olympus gained FDA clearance for EZ1500 endoscopes with Extended Depth of Field technology to enhance lesion visualization during Barrett’s surveillance.

- May 2025: Castle Biosciences finalized the acquisition of Previse, incorporating the Esopredict test that stratifies progression risk in Barrett’s patients.

Global Barretts Esophagus Market Report Scope

| Radiofrequency Ablation (RFA) |

| Cryotherapy |

| Endoscopic Mucosal Resection (EMR) |

| Photodynamic Therapy (PDT) |

| Fundoplication Surgery |

| Others |

| Endoscopy |

| Biopsy |

| Imaging (NBI, Chromoendoscopy) |

| Others |

| Non-dysplastic Barrett’s Esophagus (NDBE) |

| Low-grade Dysplasia (LGD) |

| High-grade Dysplasia (HGD) |

| Early Esophageal Adenocarcinoma (EAC) |

| Ablative Technologies |

| Resection Technologies |

| Anti-reflux Technologies |

| Diagnostic Imaging & Molecular Tests |

| Hospitals |

| Ambulatory Surgical Centers |

| Specialty Clinics |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Treatment Type | Radiofrequency Ablation (RFA) | |

| Cryotherapy | ||

| Endoscopic Mucosal Resection (EMR) | ||

| Photodynamic Therapy (PDT) | ||

| Fundoplication Surgery | ||

| Others | ||

| By Diagnosis Modality | Endoscopy | |

| Biopsy | ||

| Imaging (NBI, Chromoendoscopy) | ||

| Others | ||

| By Disease Stage | Non-dysplastic Barrett’s Esophagus (NDBE) | |

| Low-grade Dysplasia (LGD) | ||

| High-grade Dysplasia (HGD) | ||

| Early Esophageal Adenocarcinoma (EAC) | ||

| By Technology Type | Ablative Technologies | |

| Resection Technologies | ||

| Anti-reflux Technologies | ||

| Diagnostic Imaging & Molecular Tests | ||

| By End User | Hospitals | |

| Ambulatory Surgical Centers | ||

| Specialty Clinics | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the Barrett's esophagus market in 2025?

The Barrett's esophagus market size stands at USD 5.34 billion in 2025 with a 5.05% CAGR outlook to 2030.

Which treatment is growing fastest?

Cryotherapy leads growth, projected at a 9.26% CAGR due to superior tolerance and efficacy in RFA-refractory cases.

Which region offers the highest growth opportunity?

Asia-Pacific is forecast to record the fastest 7.64% CAGR, driven by rising GERD prevalence and expanding endoscopy infrastructure.

How is AI transforming Barrett’s diagnosis?

AI modules such as CAD EYE raise dysplasia detection sensitivity above 90% and shorten lesion measurement time, improving procedural quality.

What drives outpatient migration of Barrett’s procedures?

Shorter procedure times, lower facility costs, and same-day discharge protocols are shifting ablation and surveillance into ambulatory surgical centers.

Which companies lead the competitive landscape?

Medtronic, Boston Scientific, and Olympus dominate with comprehensive portfolios spanning ablation, imaging, and AI while newer entrants focus on non-endoscopic diagnostics.

Page last updated on: