Gastroesophageal Reflux Disease Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

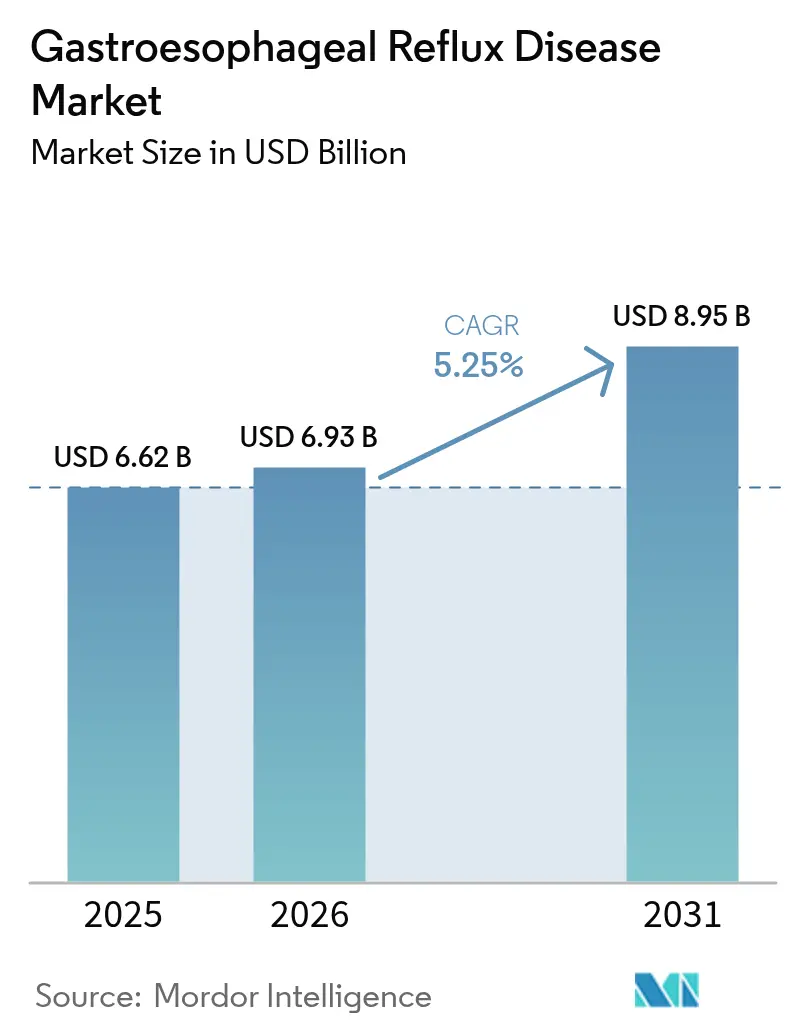

| Market Size (2026) | USD 6.93 Billion |

| Market Size (2031) | USD 8.95 Billion |

| Growth Rate (2026 - 2031) | 5.25% CAGR |

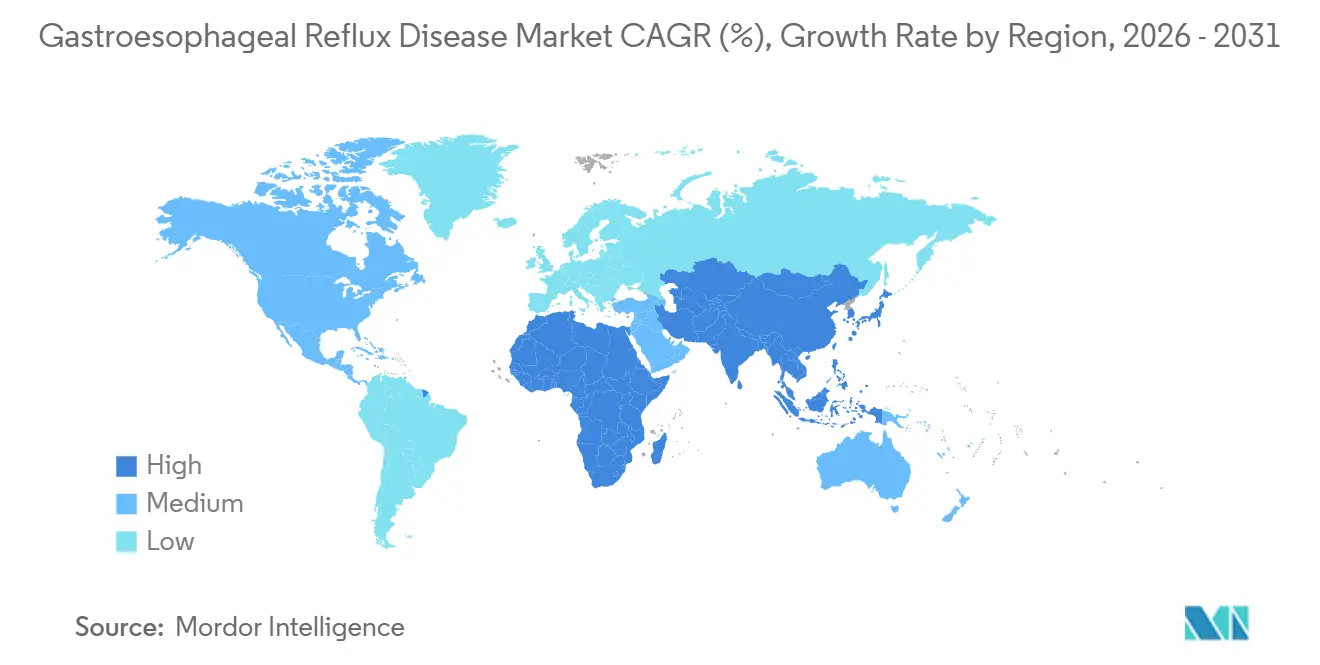

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

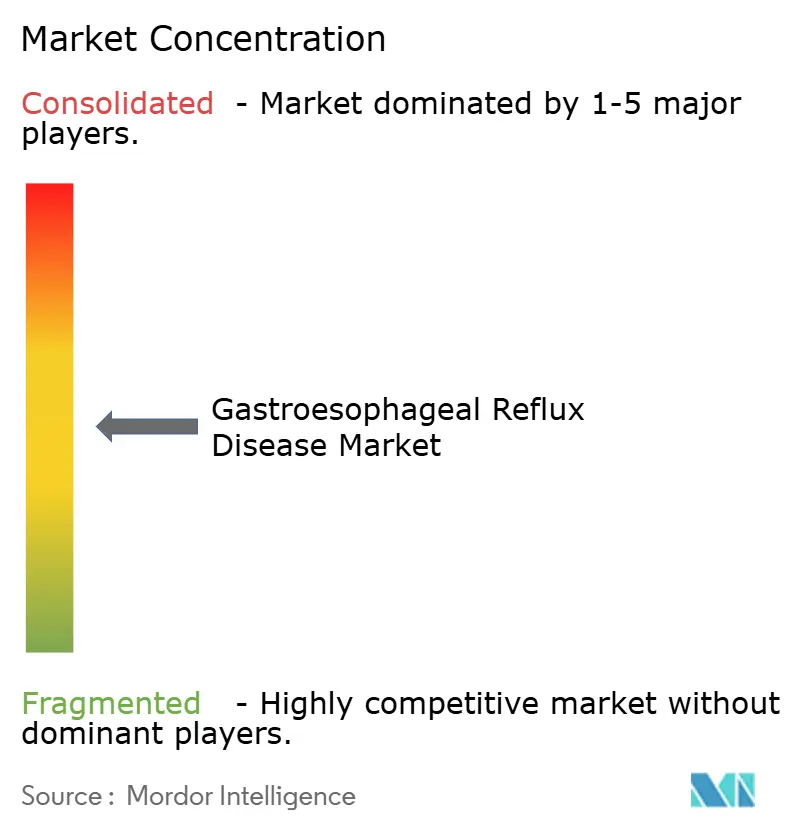

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Gastroesophageal Reflux Disease Market Analysis by Mordor Intelligence

The Gastroesophageal Reflux Disease Market size is projected to expand from USD 6.62 billion in 2025 and USD 6.93 billion in 2026 to USD 8.95 billion by 2031, registering a CAGR of 5.25% between 2026 to 2031.

Momentum comes from rising global obesity, population ageing, and the commercialization of potassium-competitive acid blockers that promise faster nocturnal acid control. Diagnostics are accelerating on the back of single-use endoscopy mandates, while AI-enabled pH wearables shorten work-ups in tele-gastroenterology programs. Device-based solutions such as magnetic sphincter augmentation and endoscopic plication are winning share among younger cohorts who prefer minimally invasive, anatomy-sparing options. Competitive intensity stays moderate as branded proton-pump inhibitor franchises face generic erosion, yet incumbents still wield scale advantages in manufacturing and detailing.

Key Report Takeaways

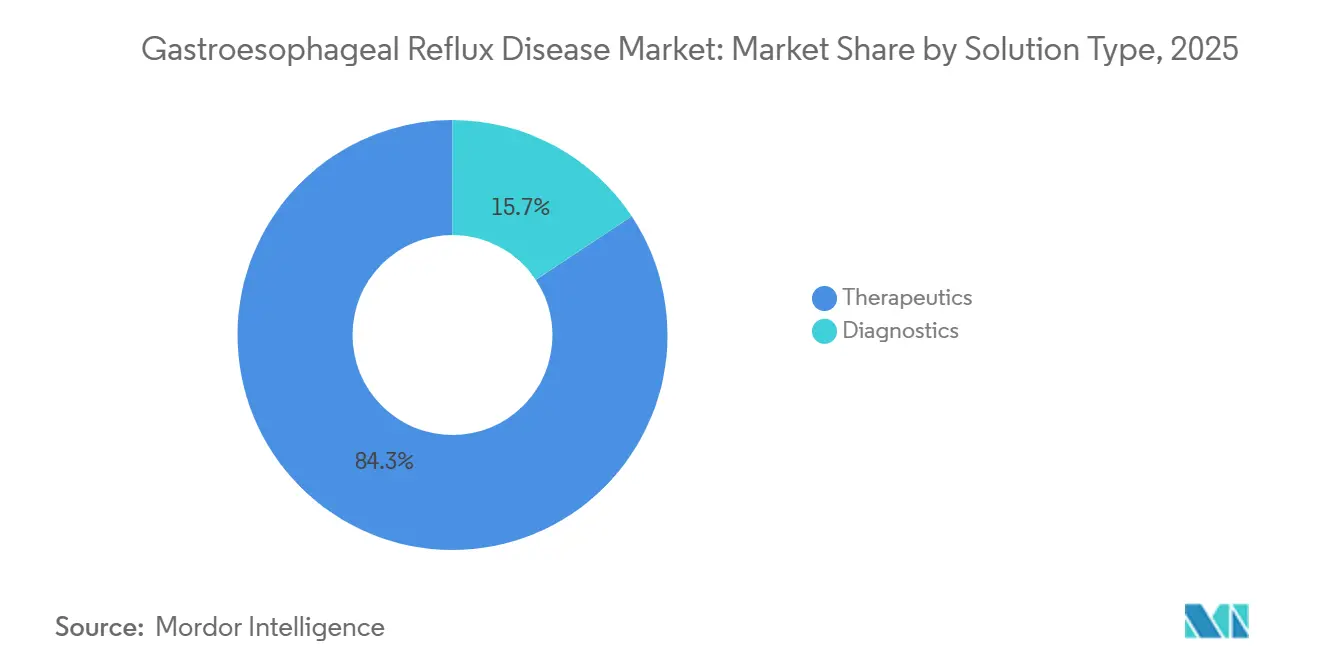

- By solution type, therapeutics led with 84.32% revenue share in 2025, while diagnostics is projected to post the fastest 9.33% CAGR through 2031.

- By disease phenotype, non-erosive reflux disease accounted for 67.25% share in 2025; Barrett’s esophagus and complicated GERD is set to expand at an 8.53% CAGR to 2031.

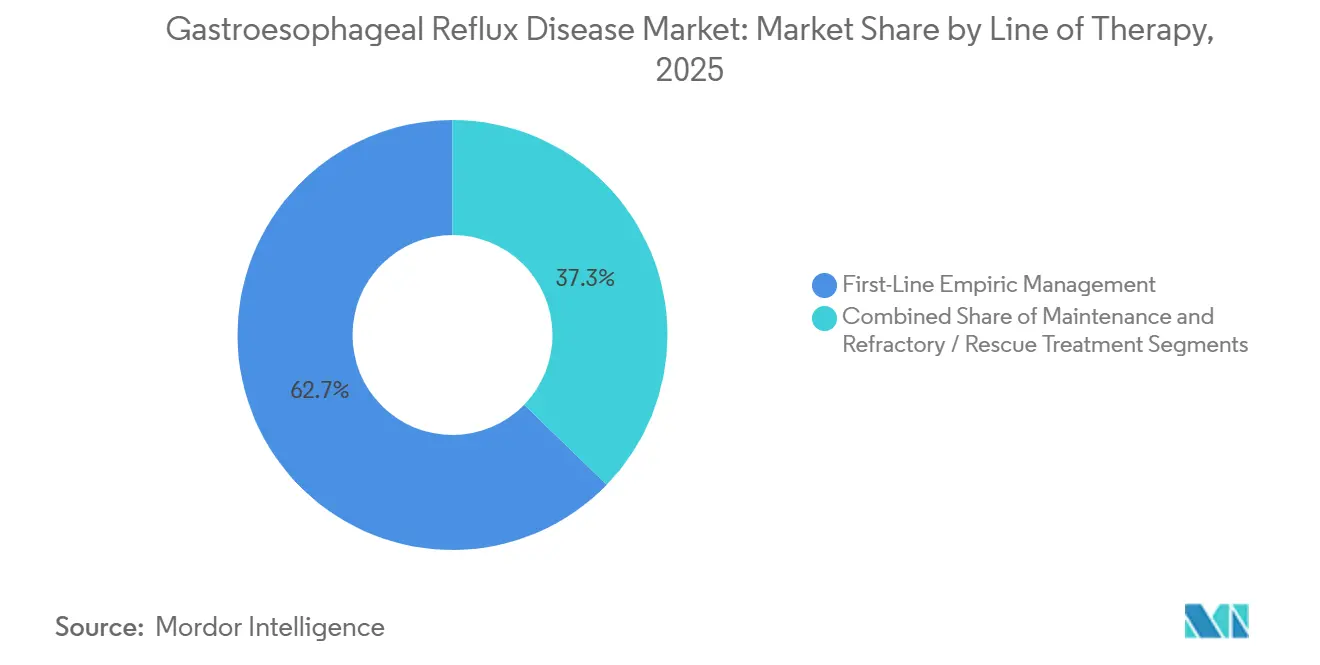

- By line of therapy, first-line empiric management captured 62.73% share in 2025, whereas refractory and rescue treatment is forecast to grow at an 8.24% CAGR over the same period.

- By patient demographics, adults aged 18–64 years held 66.66% share in 2025, but the geriatric cohort is poised for the quickest 7.26% CAGR through 2031.

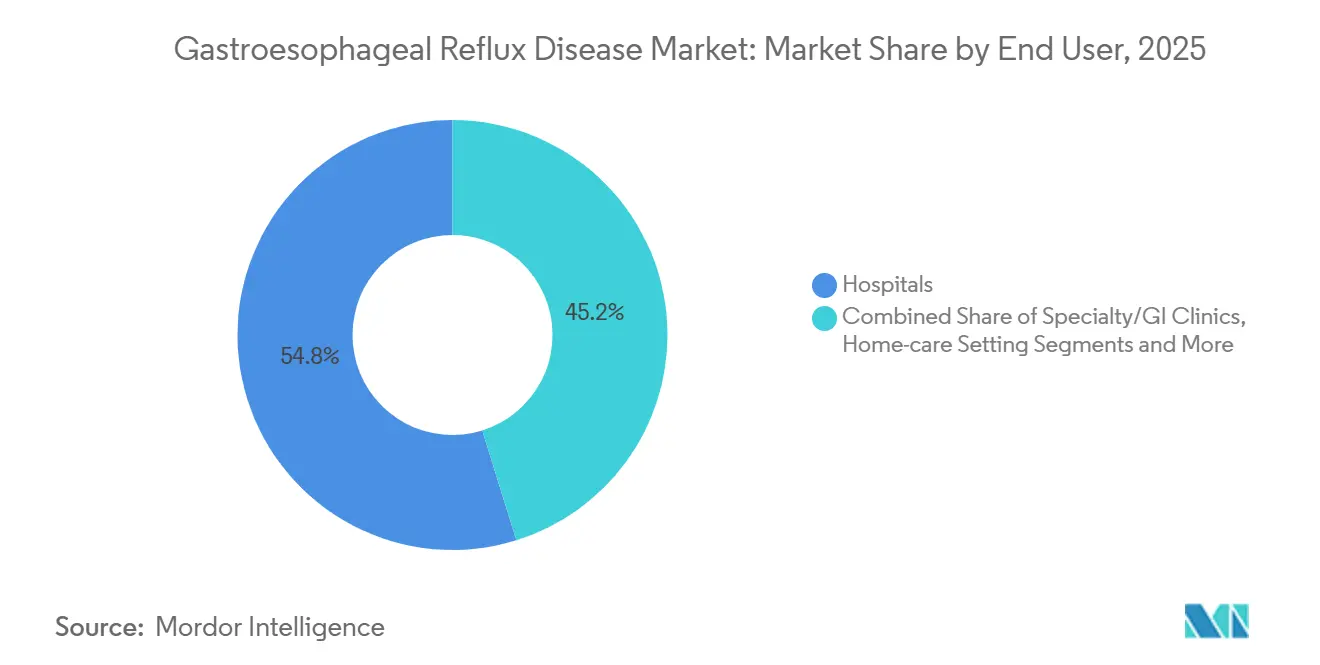

- By end user, hospitals commanded 54.82% revenue share in 2025, yet ambulatory surgical centers are advancing at a 7.67% CAGR.

- By geography, North America secured 37.34% share in 2025, while Asia-Pacific is projected to lead growth with a 7.42% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Gastroesophageal Reflux Disease Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising GERD prevalence from obesity and ageing | +1.2% | North America, Europe, urban Asia-Pacific | Long term (≥ 4 years) |

| OTC availability and generic penetration of acid suppressants | +0.8% | South America, Middle East & Africa, South Asia | Medium term (2–4 years) |

| Breakthroughs in minimally invasive anti-reflux devices and diagnostics | +1.0% | North America, Europe, early APAC uptake | Medium term (2–4 years) |

| Surge in single-use endoscopy driven by infection-control mandates | +0.9% | North America, Europe, high-income APAC | Short term (≤ 2 years) |

| Commercialization of potassium-competitive acid blockers | +0.7% | Japan established, North America & Europe emerging | Medium term (2–4 years) |

| AI-enabled pH wearables powering tele-gastroenterology | +0.6% | North America, select Europe, pilot APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising GERD Prevalence from Obesity and Ageing

Global obesity reached 42.4% of U.S. adults in 2024, while those aged ≥65 formed 17.3% of the world’s population, intensifying reflux incidence.[1]Karen Smith, “Obesity Data and Statistics,” Centers for Disease Control and Prevention, cdc.gov Visceral fat raises intra-abdominal pressure and drives transient lower-esophageal sphincter relaxations, explaining why bariatric-surgery candidates show erosive esophagitis prevalence above 30% versus 10% in age-matched controls. Japan logged an 18% rise in GERD diagnoses among citizens over 70 between 2020 and 2025 as life expectancy lengthened and calcium-channel-blocker use climbed.[2]Hiroshi Tanaka, “Health Statistics 2025,” Ministry of Health, Labour and Welfare Japan, mhlw.go.jp China saw reflux consultations surge 22% in tier-1 cities from 2023-2025 amid Westernized diets and sedentary office work. These demographics underpin sustained demand for geriatric-friendly formulations and Barrett’s surveillance.

OTC Availability and Generic Penetration of Acid Suppressants

Over-the-counter omeprazole and esomeprazole captured 35% of U.S. PPI unit volume in 2025, enlarging the treated pool beyond formally diagnosed cases. Indian generic pantoprazole sold below USD 0.05 per 20 mg dose in 2024, spurring a 28% pharmacy-sales jump across tier-2 cities. Brazil permitted OTC pantoprazole in August 2025, a change distributors expect to lift national consumption 15% within two years.[3]Maria Oliveira, “Regulatory Approvals,” Agência Nacional de Vigilância Sanitária, gov.br/anvisa While price competition trims branded margins—Protonix revenue slipped 12% in 2025 despite flat volume—innovators are pivoting to PCABs and alginate blends.

Breakthroughs in Minimally Invasive Anti-Reflux Devices and Diagnostics

Medicare expanded reimbursement for magnetic sphincter augmentation in January 2025, eliminating prior-authorization delays. U.S. LINX implant volumes climbed 34% year-on-year as 48-year-old median-age patients sought PPI-free relief. A multicenter trial reported 72% freedom from daily PPI use three years after transoral incisionless fundoplication, prompting private insurers to add coverage for PPI non-responders. Medtronic’s cloud-linked impedance-pH platform, launched mid-2025, cut diagnostic uncertainty and shaved 21 days off time-to-procedure.

Surge in Single-Use Endoscopy Driven by Infection-Control Mandates

FDA guidance issued February 2024 mandated microbiological surveillance every 50 scopes, prompting capital reviews at 38% of U.S. hospitals. Ambu’s disposable gastroscopes shipped to North America soared 47% in 2025 as facilities moved to zero-cross-contamination workflows. In Europe, Boston Scientific’s EXALT Model D gained early uptake following a GBP 18 million NHS allocation for disposable scopes. Japan aligned reimbursement in 2025 to favor single-use devices, and Olympus expects 12% of its domestic base to hybridize by 2027

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Long-term PPI safety concerns triggering regulatory scrutiny | -0.5% | North America, Europe | Medium term (2–4 years) |

| Rapid price erosion following blockbuster patent expiries | -0.7% | Europe, emerging markets worldwide | Short term (≤ 2 years) |

| Weak reimbursement for novel anti-reflux procedures in emerging markets | -0.4% | Asia-Pacific, MEA, South America | Long term (≥ 4 years) |

| Supply-chain fragility for endoscopy consumables in LMICs | -0.3% | Sub-Saharan Africa, South Asia, Latin America | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Long-Term PPI Safety Concerns Triggering Regulatory Scrutiny

The European Medicines Agency ordered new PPI labels in January 2025 warning of hypomagnesemia after three months of continuous use. A JAMA Internal Medicine cohort of 73 000 users showed a 1.44 hazard ratio for dementia, prompting FDA advisory review in September 2025. By late 2025, 54% of U.S. primary-care doctors attempted PPI tapering within 12 weeks of uncomplicated GERD onset, up from 38% in 2023. Japan’s regulator now demands five-year post-marketing bone-density studies, straining smaller generic makers

Rapid Price Erosion Following Blockbuster Patent Expiries

Generic esomeprazole reached EUR 0.12 per 40 mg dose six months after Nexium lost exclusivity in major EU markets, slashing AstraZeneca’s regional GERD revenue 41% for fiscal 2025. U.S. Dexilant generics seized 68% unit share by end-2025, trimming Takeda’s national GI franchise by USD 310 million. Indian exporters shipped 1.2 billion PPI units to Africa and Latin America at 70–90% discounts, forcing multinationals out of low-margin channels. Commoditization is pushing R&D toward premium, differentiation-friendly assets such as combination PPI–alginate sachets and extended-release PCABs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Solution Type: Diagnostics Outpace Therapeutics on Procedural Shift

Endoscopy, impedance-pH monitoring, manometry, and imaging together expanded at a 9.33% CAGR between 2026 and 2031, almost double the 5.25% pace of the overall Gastroesophageal Reflux Disease market. This outperformance reflects infection-control mandates that nudged providers toward single-use scopes priced at USD 300–500 per use and cloud-linked tests that clarify refractory phenotypes before high-cost interventions. Therapeutics still delivered an 84.32% revenue contribution in 2025, anchored by low-priced proton-pump inhibitors and an embryonic but fast-moving potassium-competitive acid-blocker class that wins share in severe erosive esophagitis.

The diagnostic tailwind is strengthened by guideline changes recommending Barrett’s surveillance every three years for chronic reflux patients aged >50, a protocol that widens the procedure pool by an estimated 2.1 million cases in North America alone. Device and procedural lines—laparoscopic fundoplication, endoscopic suturing, magnetic sphincter augmentation, and radiofrequency ablation—migrated from tertiary centers to ambulatory surgical suites, helped by Medicare claims that showed a 29% jump in community facility volumes between 2024 and 2025. Digital therapeutics remain small but logged 1.4 million downloads in 2025, and early evidence suggests smartphone-based posture coaching can cut daily PPI use, a metric payers in Germany now reimburse under chronic-disease codes.

By Disease Phenotype: Barrett’s Surveillance Drives Fastest Growth

Non-erosive reflux disease contributed 67.25% of 2025 revenue, sustained by high prevalence and chronic pharmacotherapy dependence that translates into repeat prescription income, the single largest annuity line in the Gastroesophageal Reflux Disease market. Erosive esophagitis, defined by Los Angeles grades A–D, supplied the remainder of uncomplicated cases and spurred device usage, as grade C and D lesions often trigger fundoplication or LINX implantation when pharmacologic control stalls.

Barrett’s esophagus and other complicated GERD phenotypes are advancing at an 8.53% CAGR through 2031 after 2024 guidelines lowered the male screening age to 50 and endorsed radiofrequency ablation protocols that record 92% intestinal-metaplasia eradication. Medicare actuaries estimate that a population-based Barrett’s program would insert 800 000 extra endoscopies annually if approved, a surge that would add roughly USD 320 million in incremental diagnostic revenue to the Gastroesophageal Reflux Disease market size for 2028. Down-staged NERD users generate fewer scopes—0.3 per patient over five years—but higher OTC PPI and alginate turns, a pattern that benefits generics producers whose volumes outstrip branded scripts four-to-one in most emerging economies.

By Line of Therapy: Refractory Cases Fuel Rescue-Treatment Expansion

First-line empiric management commanded 62.73% of therapy revenue in 2025 thanks to eight-week PPI trials that remain the universal starting algorithm. Maintenance and step-down phases kick in after symptom control, shifting some patients to lower daily doses, on-demand usage, or H2-receptor antagonists; payers now insist on documented step-down attempts after 12 weeks to curb long-term exposure risk. Refractory and rescue interventions are expanding at an 8.24% CAGR, lifted by the 30–40% of patients who do not respond to twice-daily PPIs and who therefore move to impedance-pH work-ups and eventually devices.

A 2025 multicenter registry showed that impedance testing re-classified 34% of presumed refractory GERD to non-acid reflux states, enabling baclofen, alginate, or visceral-hypersensitivity regimens instead of immediate surgery. Google Trends logged a 63% uptick in searches for “LINX surgery” and “TIF procedure” from 2024 to 2025, reflecting patient-initiated care escalation. Shared-decision mandates now require multidisciplinary sign-off before payers fund high-ticket implants, stretching wait times but improving candidate selection and protecting future value in the Gastroesophageal Reflux Disease market.

By Patient Demographics: Geriatric Segment Leads Growth Amid Safety Concerns

Adults 18–64 years contributed 66.66% revenue in 2025, mirroring the life-stage peak for obesity, Western diet exposure, and work-related stress triggers. The ≥65 cohort grows fastest at a 7.26% CAGR, pushed by extended life spans, polypharmacy, and vigilance over fracture and kidney risk associated with long-term PPIs. A U.K. audit of 12 000 seniors found 41% on PPIs >12 months, yet only 19% had confirmatory endoscopy, highlighting under-diagnosis of erosive lesions.

Liquid suspensions and orally disintegrating PCAB granules now address pediatric and frail-elderly swallowing barriers; Takeda’s vonoprazan granules launched in Japan in late 2025 and aim for U.S. filing in 2027. Younger, healthier adults gravitate to anatomy-sparing devices to avoid lifelong tablets, whereas multi-morbidity in middle-age pushes continued drug reliance. Demographic math signals that geriatric spend will close on 30% of total Gastroesophageal Reflux Disease market size by 2031, underlining the case for age-specific dose-de-escalation pathways.

By End User: ASC Migration Reshapes Procedural Economics

Hospitals held a 54.82% revenue share in 2025 by hosting complex fundoplication repairs, Barrett’s ablations, and urgent bleeds, cementing their place as the safety-net hub of the Gastroesophageal Reflux Disease market share. Ambulatory surgical centers clock the highest trajectory at 7.67% CAGR because payers reimburse LINX and TIF at lower unit prices yet allow same-day discharge savings. The 2025 Medicare Fee Schedule bumped ASC reimbursement for transoral fundoplication 8% while freezing hospital outpatient rates, a lever expected to redirect 12,000 extra cases per year to ASC suites by 2027.

SCA Health committed to equipping 22 new centers with single-use duodenoscopes and AI imaging in 2025, focusing on Medicare Advantage lives amenable to narrow networks. Specialty hepatology-GI clinics build ancillary loops with in-office dilation and impedance-pH testing, enhancing referral depth. Home-care grows from a tiny base: Anthem’s 2025 pilot paid 70% of in-office rates for remote pH capsules, a level that analysts expect more commercial plans to mirror if data sustain equivalent diagnostic success. Hospitals are responding by bundling complex-case contracts and deepening R&D links to retain stature inside the wider Gastroesophageal Reflux Disease market.

Geography Analysis

North America contributed 37.34% revenue in 2025, far ahead of any other region. The market benefits from high payer coverage, early PCAB uptake, and a deep installer base for magnetic sphincter augmentation. Single-use endoscopy also penetrates fastest here because legal exposure around infection drives proactive procurement. ASC migration is most pronounced in Texas, Florida, and California, where light certificate-of-need barriers allow rapid capacity swings. Although PCAB scripts accelerate, step-therapy rules keep low-cost PPIs dominant first line, a fact that tempers overall price lifts yet boosts unit turns in the Gastroesophageal Reflux Disease market.

Asia-Pacific is on track for a 7.42% CAGR through 2031, the quickest worldwide, as obesity rises in China and India and public programs pilot Barrett’s screening that funnels more scopes into provincial hospitals. China’s ten-province pilot will finance 500,000 endoscopies by 2027, creating volume that local manufacturers such as Aohua are ready to supply. India exported USD 420 million in generic PPIs during 2025, handing domestic firms global reach and margin despite sub-dollar pricing at home. Japan shows a decade-deep PCAB curve, with vonoprazan cornering 40% of new GERD starts in 2025, an adoption blueprint for the wider region.

Europe’s mature PPI environment slows top-line growth to low single digits, yet single-use scopes and PCABs revive momentum. Germany, the United Kingdom, and France allocate infection-prevention budgets that speed disposable scope buys, whereas southern and eastern markets stick with reused fleets for capital reasons. Regulatory coherence under the European Medicines Agency accelerates device approvals but also amplifies safety alerts that trim long-term PPI days-of-therapy. South America’s expansion is steady but capped by reimbursement ceilings; Brazil’s OTC PPI penetration rose after ANVISA’s 2025 rule change, but high-cost devices stay a private-pay preserve.

The Middle East and Africa fracture into high-income Gulf Cooperation Council states investing in tertiary GI hubs and sub-Saharan economies plagued by endoscope shortages. Nigeria reported more than four-week consumable stock-outs at 62% of public hospitals in 2025. Sub-Saharan Africa averages 0.8 scopes per million inhabitants, compared with 47 per million in OECD peers, a structural obstacle that confines screening to late-stage disease and keeps pharmaceutical volume high in the regional Gastroesophageal Reflux Disease market.

Competitive Landscape

The Gastroesophageal Reflux Disease market remains moderately concentrated. AstraZeneca, Takeda, and Pfizer maintain historical strength through Nexium, Dexilant, and Protonix, yet generic waves from Indian exporters hamper margin. Phathom Pharmaceuticals is carving a niche around Voquezna, trading rebate-backed contracts for healing-rate guarantees that appeal to pharmacy-benefit managers. Device leaders Boston Scientific, Medtronic, and Johnson & Johnson chase refractory share with low-invasion implants that resonate with younger consumers.

Lifecycle extensions dominate brand defense: AstraZeneca deploys authorized generics, Takeda bundles Dexilant with savings cards, and Pfizer co-packs Protonix with alginates for OTC channels. Single-use scope pioneers Ambu and Boston Scientific differentiate via infection-control messaging, while Olympus leverages hybrid fleets to retain hospitals that cannot afford full disposable conversion. Digital startups pitch AI meal-timing and posture apps that German sickness funds reimburse when dose-spare evidence exists, foreshadowing a service layer within the wider Gastroesophageal Reflux Disease industry.

White-space lies in pediatric and frail-elderly formulations; vonoprazan granules and orally disintegrating PCAB tablets meet swallowing challenges. Medtronic’s 2025 patent on a closed-loop dosing app hints at software-as-a-device pathways that could reposition pharmacotherapy compliance as an outcomes-priced service. Asia-Pacific challengers—including Lupin, Zydus Cadila, and Aohua Endoscopy—exploit cost efficiencies and regional distribution reach, pressuring multinationals into risk-sharing partnerships.

Gastroesophageal Reflux Disease Industry Leaders

Johnson & Johnson

Takeda Pharmaceutical Company Limited

Pfizer Inc.

Medtronic

AstraZeneca

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Braintree Laboratories submitted an NDA to FDA for tegoprazan targeting heartburn in NERD, healing of erosive esophagitis, and maintenance of healed EE.

- January 2026: Renata PLC secured U.K. marketing authorization for esomeprazole 20 mg and 40 mg tablets from the MHRA, expanding low-cost OTC choice.

- January 2026: Implantica won EUR 1.2 million in Italian public tenders for RefluxStop, boosting European reimbursement traction for its mechanical anti-reflux implant.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the gastroesophageal reflux disease (GERD) market as the global spending on prescription and over-the-counter pharmacologic therapies, primarily proton-pump inhibitors, H2 receptor antagonists, potassium-competitive acid blockers, antacids, alginates, and selected pro-kinetics used to relieve or prevent pathologic reflux of gastric contents into the esophagus. GERD prevalence-based demand, supported by treatment days and average selling prices, sets the value baseline.

Scope exclusion: Devices and surgical procedures such as fundoplication systems, LINX implants, or diagnostic manometry kits sit outside this sizing.

Segmentation Overview

- By Solution Type

- Diagnostics

- Endoscopy

- pH & Impedance Monitoring

- Manometry

- Imaging & Ancillary Tests

- Therapeutics

- Phramacological

- Proton Pump Inhibitors (PPIs)

- Potassium-Competitive Acid Blockers (PCABs)

- Histamine-2 Receptor Antagonists (H2RAs)

- Others (Combinational Formulations, Prokinetic Agents, Alginates)

- Device / Procedural

- Laparoscopic Fundoplication

- Anti-Reflux Endoscopic Suturing / Plication

- Magnetic Sphincter Augmentation

- Transoral Incisionless Fundoplication (TIF)

- Others (Radio-Frequency Ablation, LES Electrical Stimulation)

- Lifestyle & Digital Therapeutics

- Phramacological

- Diagnostics

- By Disease Phenotype

- Non-Erosive Reflux Disease (NERD)

- Erosive Esophagitis (Grades A–D)

- Barrett’s Esophagus / Complicated GERD

- By Line of Therapy

- First-Line Empiric Management

- Maintenance / Step-Down Therapy

- Refractory / Rescue Treatment

- By Patient Demographics

- Pediatric (0-17 yrs)

- Adult (18-64 yrs)

- Geriatric (65 yrs +)

- By End User

- Hospitals

- Ambulatory Surgical Centres

- Specialty / GI Clinics

- Home-care Settings

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed gastroenterologists, community pharmacists, and payer advisors across North America, Europe, China, India, and Brazil. These discussions validated real-world prescription patterns, out-of-pocket self-medication rates, and the early uptake curve for vonoprazan, thereby closing gaps left by desk research and guiding final assumptions.

Desk Research

We collected prevalence and treatment data from public sources such as the World Health Organization Global Health Observatory, the CDC National Health Interview Survey, Eurostat health statistics, and Japan's National Health and Nutrition Survey. Drug utilization and pricing came from FDA Orange Book listings, EMA product information, UN Comtrade export codes for omeprazole and pantoprazole, and peer-reviewed meta-analyses indexed on PubMed. Market signals were further tracked through company 10-Ks and investor decks, supported by D&B Hoovers and Dow Jones Factiva for revenue splits. The sources cited are illustrative only and not exhaustive; many additional references informed our desk work.

Market-Sizing & Forecasting

A top-down prevalence-to-treated-patient model converts adult GERD incidence, treatment penetration, and average daily therapy cost into 2025 revenue. Results are corroborated with selective bottom-up channel checks on sampled PPI and antacid unit sales, which are then adjusted for parallel trade and private-label discounts. Key variables include obesity prevalence, aging-index shifts, over-the-counter antacid unit growth, regulatory approvals for novel PCABs, and forecast prescription days per patient. A multivariate regression projects these drivers through 2030 under baseline, optimistic, and restrained scenarios, followed by expert consensus weighting. Data gaps in bottom-up estimates are bridged with analog country proxies before final reconciliation.

Data Validation & Update Cycle

Outputs pass anomaly checks against independent import values, OTC panel data, and historic currency trends. A senior reviewer signs off after variance is within two percent. Reports refresh annually, with interim updates triggered by material events such as new drug launches or major guideline revisions.

Why Mordor's Gastroesophageal Reflux Disease Market Baseline Always Stays Dependable

Published estimates often diverge because each firm picks its own mix of drug classes, price corridors, and refresh timing.

Key gap drivers include narrow scopes that omit low-priced generics, aggressive discount assumptions that over-correct average selling prices, or conservative refresh cycles that still use pre-COVID prevalence. Mordor's frame captures OTC volumes, recent PCAB approvals, and region-specific payer mixes, letting our clients work with a grounded present-day figure.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 6.39 B (2025) | Mordor Intelligence | - |

| USD 5.11 B (2024) | Global Consultancy A | Excludes OTC antacids and uses constant 2020 price points |

| USD 5.24 B (2024) | Regional Consultancy B | Applies uniform treatment rate, ignores Asia obesity surge |

| USD 4.90 B (2024) | Industry Association C | Counts only prescription channels, omits self-medication spend |

The comparison shows that when variables, channels, and update cadence align with clinical reality, Mordor delivers a balanced and transparent baseline clients can retrace and replicate for confident decision-making.

Key Questions Answered in the Report

What is the projected value of the Gastroesophageal Reflux Disease market in 2031?

It is expected to reach USD 8.95 billion by 2031, growing at a 5.25% CAGR from 2026.

Which solution type is growing fastest?

Diagnostics, powered by single-use endoscopy and AI-enabled pH wearables, is forecast to rise at a 9.33% CAGR through 2031.

Why are ambulatory surgical centers gaining share?

Payers favor their lower costs, and Medicare raised ASC reimbursement for transoral fundoplication, driving a 7.67% CAGR for the setting.

How significant is the geriatric opportunity?

The ≥65 cohort expands at a 7.26% CAGR and is on track to approach 30% of total revenue by 2031, fueling age-specific therapeutics and diagnostics.

What restrains device adoption in emerging markets?

Limited reimbursement under schemes such as Ayushman Bharat and SUS Brazil leaves most patients to self-pay, curbing volumes.

Are potassium-competitive acid blockers replacing PPIs?

PCABs deliver faster acid control and are penetrating severe erosive cases, yet step-therapy rules and higher prices keep PPIs dominant first-line.

Page last updated on: