Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

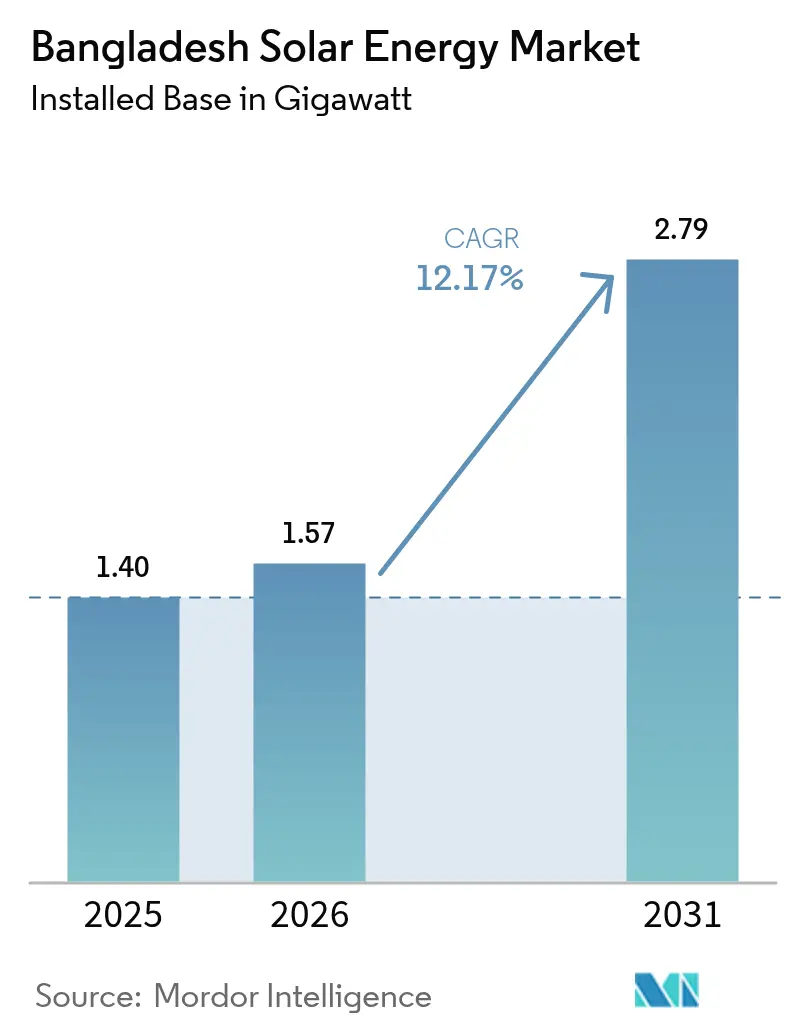

| Base Year Market Size (2025) | 1.40 gigawatt |

| Market Volume (2026) | 1.57 gigawatt |

| Market Volume (2031) | 2.79 gigawatt |

| Growth Rate (2026 - 2031) | 12.17% CAGR |

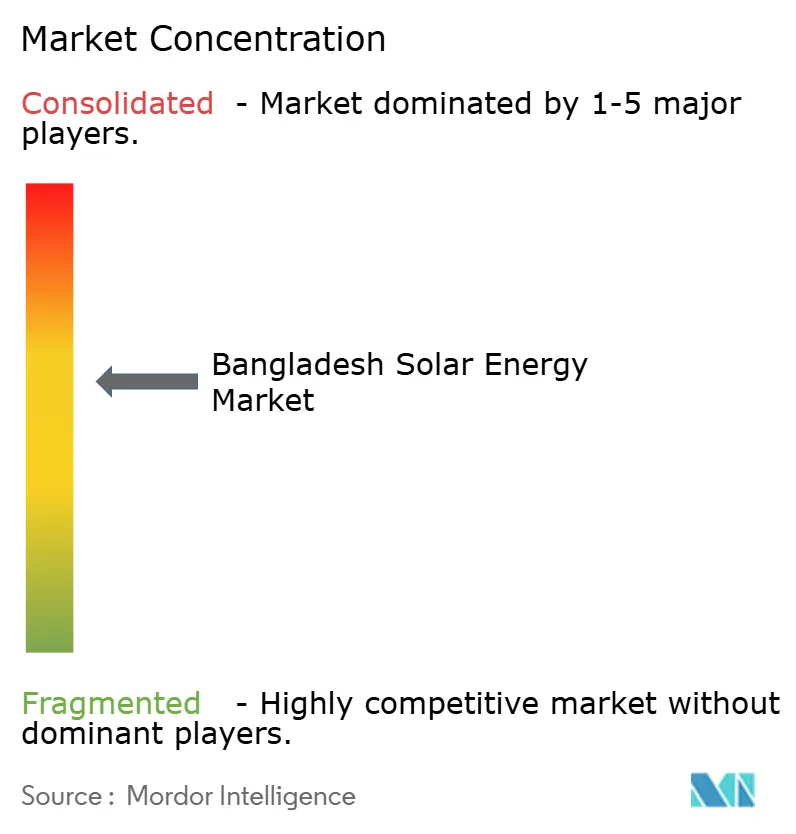

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Bangladesh Solar Energy Market Analysis by Mordor Intelligence

Bangladesh Solar Energy Market size in 2026 is estimated at 1.57 gigawatt, growing from 2025 value of 1.40 gigawatt with 2031 projections showing 2.79 gigawatt, growing at 12.17% CAGR over 2026-2031.

Continued policy reform, concessional multilateral financing, and swelling LNG import bills are reshaping cost curves in favor of solar, while a shift from government-to-government deals to fully competitive tenders is compressing tariffs toward USD 0.04–0.05 /kWh and widening private-sector access. Chinese module oversupply and higher-efficiency mono-PERC and TOPCon products are pushing turnkey system prices down to USD 600–800/kW for utility plants and USD 1,000–1,200/kW for rooftops, accelerating new build. Corporate buyers in the ready-made garment supply chain are ratcheting up decarbonization clauses that compel factories to displace captive diesel with onsite PV or corporate PPAs, creating a new growth lane for distributed generation. Multilateral development banks (MDBs) have committed more than USD 150 million in 2024 alone for sub-100 MW projects that bypass transmission bottlenecks, further de-risking investment.[1]Asian Development Bank, “Renewable Energy Program Updates,” adb.org

Key Report Takeaways

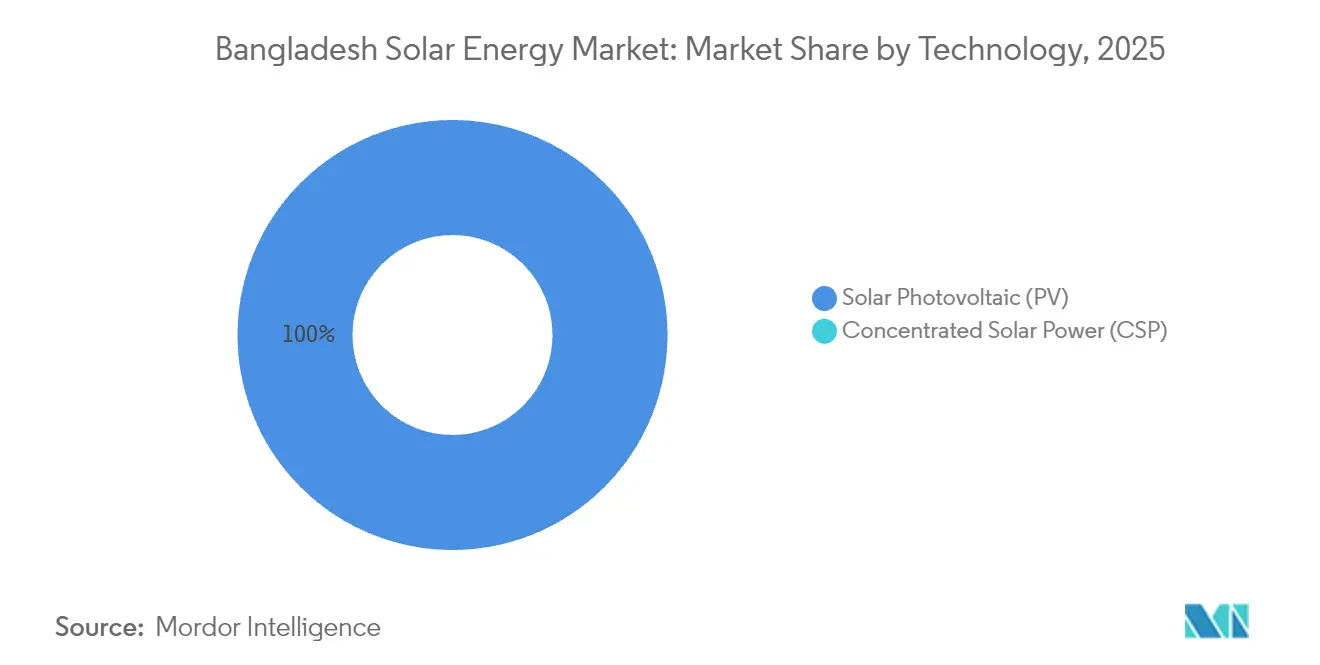

- By technology, solar photovoltaic captured 100% of capacity and is projected to expand at a 12.17% CAGR through 2031.

- By grid type, on-grid systems held 79.12% of Bangladesh's solar energy market share in 2025 and are slated to grow at a 14.36% CAGR to 2031.

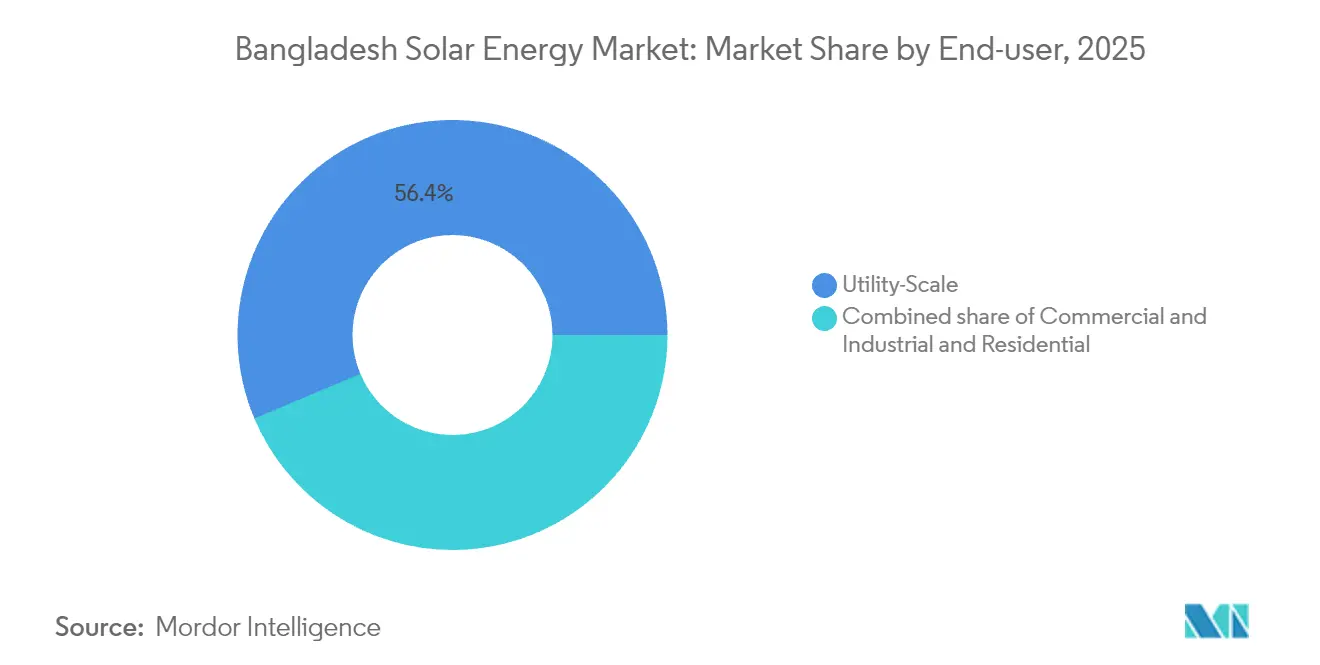

- By end user, the residential segment is poised to grow at a 32.09% CAGR through 2031, overtaking utility-scale additions in annual deployment.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Bangladesh Solar Energy Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mandatory rooftop-solar regulation for new grid connections | 2.50% | Dhaka, Chattogram, Gazipur | Short term (≤ 2 years) |

| Rapid decline in PV module prices & BOS capex | 2.00% | National | Short term (≤ 2 years) |

| Export-buyer decarbonization pressure on the RMG sector | 1.80% | Dhaka, Gazipur, Narayanganj | Medium term (2–4 years) |

| Rising LNG/oil import bills inflating grid tariffs | 1.50% | National | Medium term (2–4 years) |

| Concessional climate-finance inflows via MDBs | 1.20% | Pabna, Mymensingh, Jamalpur | Short term (≤ 2 years) |

| Land-scarcity push toward floating & agro-PV pilots | 0.80% | Kaptai Lake, Teesta basin | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Mandatory Rooftop-Solar Regulation for New Grid Connections

A November 2024 directive requires every new residential, commercial, or industrial grid entrant after July 2025 to install a rooftop PV array scaled to the standing load, instantly creating a guaranteed demand floor. Revised net-metering rules let consumers export 100% of excess generation at avoided-cost tariffs, removing the earlier 70% cap.[2]Naimul Karim, “Solar tariffs fall under 5 cents amid new tender rules,” thebusinessstandard.com SREDA estimates 5 GW of rooftop potential could materialize by 2030, though enforcement protocols under the Bangladesh Energy Regulatory Commission are still in formation. Third-party commissioning certificates are likely to become mandatory to curb quality lapses observed in earlier subsidy-driven rollouts.

Rapid Decline in PV Module Prices & BOS Capex

Average import prices for mono-PERC modules sank to USD 0.10–0.12/W in 2024 from USD 0.15–0.18/W a year earlier, undercut by polysilicon oversupply and aggressive Chinese export strategies. Balance-of-system (BOS) equipment now makes up 40–50% of plant cost, pressuring EPC margins while 5% import duty on modules and 15% VAT on inverters remain in force. Utility-scale EPC prices narrowed to USD 600–800/kW, whereas urban rooftops run USD 1,000–1,200/kW due to higher labor intensity and smaller parcel economies. Local assembly plans announced by LONGi Solar in March 2025 could shave another 8–10% off turnkey pricing once production ramps in 2026.

Export-Buyer Decarbonization Pressure on the RMG Industry

Ready-made garments contribute 85% of exports and face intensifying carbon audits from European and North American brands. H&M’s April 2025 MoU with Pran Group and IFC for Bangladesh’s first solar corporate PPA breaks the monopoly of utility PPAs, offering factories direct access to renewable electrons.[3]International Finance Corporation, “Greener Garments Initiative Progress Note,” ifc.org More than 200 garment facilities have already deployed 7 MW of rooftops under IFC’s Greener Garments Initiative, a threefold rise in 18 months, yet still under 1% of the industry’s 3 GW captive diesel-gas fleet. Access to IDCOL concessional finance is widening, but many subcontractors still lack structured credit pathways.

Rising LNG/Oil Import Bills Inflating Grid Tariffs

LNG procurement now tracks 13–13.5% of Brent, up from 9–10% in 2022, swelling Bangladesh Power Development Board (BPDB) losses to USD 1.1–2.2 billion in fiscal 2024 and forcing quarterly tariff hikes that lifted residential retail prices above BDT 8/kWh. Captive industrial generators exceeding 3 GW are pivoting to solar-plus-storage hybrids to limit exposure to volatile fuel imports. MDB-supported tariff rationalization is expected to erode the price gap between grid supply and on-site PV, strengthening the solar value proposition.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Land acquisition bottlenecks for utility-scale parks | –1.5% | Dhaka, Chattogram, Sylhet | Medium term (2–4 years) |

| Grid evacuation lags prompting curtailment risk | –1.8% | Rajshahi, Rangpur, Khulna | Short term (≤ 2 years) |

| Import duties & VAT on inverters/BOS | –0.9% | National | Short term (≤ 2 years) |

| Limited solar project bankability for local lenders | –0.7% | National | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Land Acquisition Bottlenecks for Utility-Scale Parks

Projects above 100 ha require negotiations with hundreds of smallholders under the Land Acquisition Act, inflating timelines by 18–24 months. China Huadian’s 160 MW Maheshkhali plant needed 150 ha and spent months clearing environmental hurdles, while CREC’s 100 MW Jamalpur build involved over 200 landowners.[4]Sam Jahan, “Transmission grid lags stall northern solar parks,” thedailystar.net The new tender regime shifts acquisition risk onto private developers who lack eminent-domain leverage, steering investors toward floating and rooftop options until pre-cleared solar zones are operational post-2026.

Grid Evacuation Lags Prompting Curtailment Risk

Northern divisions record 15–20% solar curtailment during midday peaks for want of substation upgrades. PGCB’s 2025 master plan earmarks USD 1.2 billion for capacity expansion through 2028, but the near-term mismatch leaves completed projects absorbing off-take risk. Joules Power’s 100 MW Chandpur plant alone budgets USD 15 million for a 37 km dedicated line, an unwelcome cost add for developers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: PV Monopoly Reflects Cost and Land Realities

Solar photovoltaic accounts for the full Bangladesh solar energy market size today and is on track for a 12.17% CAGR to 2031. Mono-PERC imports held an 84.20% share in 2025, with TOPCon rising to 15.80% as developers chase >23% efficiencies that mitigate land scarcity. CSP remains absent, burdened by ≥USD 3,000/kW capex and unviable DNI levels. LONGi’s upcoming local factory aims to trim import logistics, helping crystalline PV keep its hold on the Bangladesh solar energy market. Continued dominance of crystalline silicon is supported by bifacial adoption in 20-25% of ground-mount builds, raising yields 10-15% without enlarging footprints. Thin-film and perovskite tandem modules stay relegated to pilot status, pending commercial durability data beyond 2028.

By Grid Type: On-Grid Expansion Mirrors Electrification Gains

On-grid systems commanded 79.12% of the Bangladesh solar energy market share in 2025 and are forecast to grow 14.36% annually through 2031. National electrification above 95% and net-metering reforms that waive battery requirements give rooftop adopters simple grid export pathways. Off-grid capacity, mainly 6 million solar home systems totaling 360 MW, cycles down as villages connect to the main grid, but solar irrigation pumps and hybrid mini-grids remain viable niches. Competitive tenders for 500 MW of utility plants further anchor the Bangladesh solar energy market to on-grid dominance.

By End-User: Residential Surge Challenges Utility-Scale Dominance

Utility-scale plants still account for 56.35% of the Bangladesh solar energy market size, but mandatory rooftop rules will propel residential installations at a 32.09% CAGR, signaling the fastest trajectory in the forecast window. Average system prices of USD 1,000-1,200/kW and six-to-eight-year paybacks attract urban homeowners, especially in Dhaka and Chattogram. Commercial and industrial buyers leverage PPAs to skirt system-size caps, yet uptake remains under 2% of factories’ 3 GW captive capacity, signaling large headroom for future conversion.

Geography Analysis

Dhaka Division houses roughly 35-40% of nationwide installations thanks to dense garment clusters in Gazipur and Narayanganj. Chattogram follows with 20-25%, anchored by the 160 MW Maheshkhali coastal plant and rooftop demand in the port city. Northern Rajshahi and Rangpur divisions enjoy higher irradiation but wrestle with transmission congestion that curtails 15-20% of mid-day output. Sylhet’s hilly terrain limits ground-mount opportunities, though a recent MoU envisions a new solar park once land parcels are consolidated. Khulna’s cyclone-prone coast turns to floating arrays over shrimp ponds, leveraging water surfaces that also cool modules. Mymensingh is emerging as a utility-scale hub with MDB-financed projects that piggyback on the national 400 kV backbone. Government plans to spend USD 1.2 billion on grid reinforcement by 2028 are expected to unlock an extra 1 GW across the northern belt. Administrative friction remains the hidden variable, with Dhaka projects securing land in 18 months versus 30 months in Sylhet.

Regulatory Landscape

Bangladesh solar is governed by the Power Division under the Ministry of Power, Energy and Mineral Resources, with SREDA administering key solar programs (including the net-metering portal) and BERC overseeing safety and compliance frameworks that shape rooftop interconnection. A November 2024 directive makes rooftop PV mandatory for new residential, commercial, and industrial grid connections after July 2025. Revised net-metering rules also allow export of 100% of excess generation at avoided-cost tariffs, which improves the economics for on-grid distributed PV.

Compliance has become more formalized through approved-module pathways and harmonized standards. PV modules are required to meet BSTI-aligned IEC standards, including BDS IEC 61215 and BDS IEC 61730 series, and SREDA maintains approved module listings used for program eligibility. On the investment side, Renewable Energy Policy 2025 introduces frameworks for Renewable Energy Certificates (RECs) and Service Level Agreements (SLAs) for grid-connected projects. A 10-year tax holiday commencing July 2025 and reduced customs duties through set windows support bankability alongside IDCOL technical requirements for financed systems.

Competitive Landscape

The Bangladesh solar energy market features moderate fragmentation: no single firm exceeds 10% share, yet supply chains lean heavily on Chinese. Local EPCs such as Rahimafrooz Renewable Energy (50 MW) and Solarland Bangladesh (30 MW) dominate rooftops, while China Huadian, CREC, and Alfanar corner utility parks via BPDB joint ventures. Chinese manufacturers supply over 80% of modules and inverters, and LONGi’s 2025 factory pledge underscores a pivot toward local value-addition that can pare 8–10% from plant costs.

Strategic maneuvers cluster around three white spaces: corporate PPAs in the garment belt, floating solar on 11,000 km² of inland water, and solar-plus-storage hybrids to counter curtailment up north. The IFC-H&M-Pran pilot spotlights merchant-risk appetite, even as tariff frameworks evolve. Smaller entrants like Symbior Solar chase sub-50 MW projects that dodge evacuation constraints, whereas ACWA Power’s interest hinges on transparent tender pipelines. Technology choices divide along project size: bifacial glass-glass modules with string inverters for large parks, microinverters and rapid-shutdown kits for rooftops to meet BERC safety codes.

Bangladesh Solar Energy Industry Leaders

Solarland Bangladesh Co. Ltd.,

Bangladesh China Renewable Energy Company (Pvt.) Limited

Joules Power Ltd

Rahimafrooz Renewable Energy Ltd

Trina Solar Co. Ltd

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Large-scale procurement has reopened as an actionable pipeline, creating near-term whitespace for utility-scale EPCs, module suppliers, and developers that can package land, permitting, and financing under BPDB tender requirements. In 2026, BPDB issued multiple grid-tied solar tenders, including a 495 MW tender across 10 sites in April 2026, additional tenders totaling 77.6 MW in April 2026, and 95 MW across two sites in June 2026. These competitive bidding rounds offer a clearer route for new entrants than earlier bilateral deal structures, while also bringing execution gaps around land acquisition and grid evacuation into focus for developers with strong local delivery partners.

Industrial and behind-the-meter solar is a second opportunity lane anchored by compliance and infrastructure programs rather than purely voluntary adoption. Renewable Energy Policy 2025 sets national targets of 20% electricity from renewables by 2030 and 30% by 2040, and it pairs these targets with investment incentives. Corporate decarbonization pressure in the garment value chain is already translating into templates such as the April 2025 IFC-H&M-Pran corporate PPA pilot. A third whitespace is emerging around integrated projects that use public land and PPP structures to reduce reliance on fragmented private land assembly. BEZA initiated plans in May 2026 for a 140 MW pilot solar project with integrated battery storage in Sonagazi, Feni, under a PPP model, pointing to demand for hybrid integration and structured offtake in industrial zones.

Recent Industry Developments

- July 2026: Rahimafrooz Renewable Energy Ltd. launched a hybrid solar instant power supply (IPS) product aimed at residential users seeking lower electricity bills and backup power. The launch supports higher-value distributed solar adoption by bundling PV, storage-ready power electronics, and consumer-facing service delivery through a known local brand.

- May 2026: Bangladesh Economic Zones Authority (BEZA) advanced plans for a 130-140 MW solar power plant in Sonagazi, Feni, under a PPP model using BEZA land. Placing the project in an economic zone links solar build-out to industrial load centers and creates a reference for utility-scale projects that aim to avoid multi-owner land-acquisition delays.

- June 2024: China Railway Engineering Corporation (CREC) signed a 100 MW joint venture with B-R Powergen for a solar project in Jamalpur. The deal reinforced the role of foreign-backed developers and local partners in utility-scale project execution, including land aggregation and grid-connection responsibilities.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this report, the Bangladesh solar energy market is defined as solar power development in Bangladesh, measured through installed solar capacity additions and the operating base, covering on-grid and off-grid systems across key end users.

Scope exclusions: Excludes non-solar renewables like wind and hydro, and it does not treat standalone battery storage as solar capacity unless it is deployed as part of a solar hybrid system.

Segmentation Overview

- By Technology

- Solar Photovoltaic (PV)

- Concentrated Solar Power (CSP)

- By Grid Type

- On-Grid

- Off-Grid

- By End-User

- Utility-Scale

- Commercial and Industrial (C&I)

- Residential

- By Component (Qualitative Analysis)

- Solar Modules/Panels

- Inverters (String, Central, Micro)

- Mounting and Tracking Systems

- Balance-of-System and Electricals

- Energy Storage and Hybrid Integration

Data Sources, Market Sizing, and Validation

Desk Research

Desk research started with public capacity series and policy context so the model has a grounded demand pool for Bangladesh. We referred to official and non-paywalled sources such as Bangladesh Power Development Board updates, Sustainable and Renewable Energy Development Authority publications, Bangladesh Energy Regulatory Commission tariff orders, International Renewable Energy Agency capacity statistics, and International Energy Agency or World Bank indicators for power demand and the investment climate.

Next, project announcements and pipelines were reviewed using developer and EPC press releases, tender portals, and utility procurement notices, and then checked against reputed news coverage. To reduce gaps in company-level scale and timing, we used a paid subscription for company financials and news intelligence selectively, and we referenced a patent database when we needed to confirm technology direction, for example inverter and solar hybrid system activity. The desk sources listed here are illustrative only, and several other public references and subscriptions were also used for data collection, cross-checking, and research clarification.

Primary Interviews and Surveys

Primary work was used to validate what desk sources cannot fully show, such as typical project execution timelines, the split between rooftop and utility additions, and realistic commissioning slippage. We spoke with developers, EPC contractors, equipment distributors, industrial rooftop adopters, and sector advisors across Bangladesh, and the inputs were used to test assumptions on utilization, pricing direction, and pipeline conversion for the forecast window.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 38% | CXOs: 14% | APAC: 42% |

| Mid tier: 43% | Functional/Unit leaders: 34% | EMEA: 37% |

| Smaller Players: 19% | Managers: 52% | Americas: 21% |

Market-Sizing & Forecasting

Sizing was built using a top-down installed-capacity reconstruction, where national solar additions and the operating base are pieced together from official capacity reporting, project award data, and commissioning timelines. Once the annual capacity path was formed, it was corroborated with selective bottom-up checks, such as sampled project sizes multiplied by expected project counts in key use cases (utility, commercial and industrial rooftops, and residential or solar home systems), and then adjusted when the two views did not align.

The model uses a small set of repeatable inputs, including announced and tendered solar capacity, expected commissioning lags, grid connection readiness, rooftop adoption pace in industrial clusters, and policy signals such as net metering rules and tariff revisions. We also track component price movement and exchange-rate timing as a sensitivity, since these can change procurement volumes and project viability even when the pipeline looks strong.

For forecasting, scenario analysis was used with a base case anchored to expert consensus on pipeline conversion and grid integration, then tested under slower and faster execution paths. Where bottom-up information was incomplete, gaps were handled through conservative adoption ratios, reviewed in interviews and constrained so they do not exceed what the country's observable project pipeline can realistically deliver.

Data Validation & Update Cycle

Outputs are checked in several steps so the final market size remains consistent with independent signals. We compare modeled capacity totals with official capacity statements, tender activity, and reported commissioning events, and then investigate variances before sign-off, particularly when a single project could swing the annual total.

Before publishing, the work goes through analyst review for unit consistency, timing alignment, and assumption logic, and interview follow-ups are triggered when a key input moves outside the expected range. The report is refreshed annually, and interim updates are made when there are material policy changes, major tender rounds, or significant commissioning delays, followed by a final pre-delivery pass to keep numbers current.

Mordor Intelligence's Bangladesh Solar Energy Market Size Compared Against Other Published Estimates

Published sizes for Bangladesh solar can look far apart because some sources measure installed capacity, some blend solar with broader renewable power, and others mix in storage or generation metrics. Even when the unit is the same, the base year, commissioning cutoffs, and the treatment of pipeline versus operating assets can change the number.

Solar home systems and other off-grid installations sit inside Mordor Intelligence's scope when they are deployed as solar capacity in Bangladesh, but some published figures lean mostly on grid-connected utility projects and therefore report a smaller base. Spreads also come from how fast future additions are assumed to convert from tendered capacity to commissioned capacity, and whether currency timing is refreshed or held constant across the forecast window.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.40 B (2025) | |

| Investment Agency B | USD 1.27 B (2024) | Uses a stated current renewable capacity snapshot where solar is a subset, and the year marker is not explicit in the capacity split, which can miss late-year commissioning and portions of distributed off-grid additions. |

| Market Aggregator A | USD 0.76 B (2025) | Often reflects a narrower installed solar PV view and can implicitly emphasize utility-scale tracking, which may exclude parts of distributed and off-grid deployments that still contribute to total solar capacity. |

Across the three figures, most of the difference comes down to what is counted as solar capacity and how the timing is handled for commissioning versus announced pipeline. By keeping the inputs tied to observable capacity signals and then stress-testing assumptions with interviews, the estimate stays easier to trace and repeat when new projects or policy changes appear.

Key Questions Answered in the Report

How fast will nationwide solar capacity grow in Bangladesh by 2031?

Capacity is projected to reach 2,788.6 MW in 2031, clocking a 12.17% CAGR from the 2026 base of 1,570.4 MW.

What drives the surge in residential rooftop systems?

A July 2025 rule makes rooftop PV mandatory for every new grid connection, while 100% net-metering export rights shorten homeowner paybacks to 6-8 years.

Which divisions face the highest curtailment risk?

Rajshahi, Rangpur, and Khulna divisions experience 15-20% midday curtailment due to transmission bottlenecks.

Are corporate power purchase agreements now possible in Bangladesh?

Yes, the April 2025 IFC-H&M-Pran pilot created a template for factories to buy solar power directly from generators, bypassing the utility.

Why is concentrated solar power absent from the country’s build-out?

CSP’s high capex (≥USD 3,000/kW), land demand (>500 ha), and insufficient direct normal irradiance make it uneconomic compared with PV.

What incentives support new solar investments?

A 10-year tax holiday commencing July 2025 eliminates income tax, VAT, and customs duty on qualifying solar projects.

Page last updated on: