Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

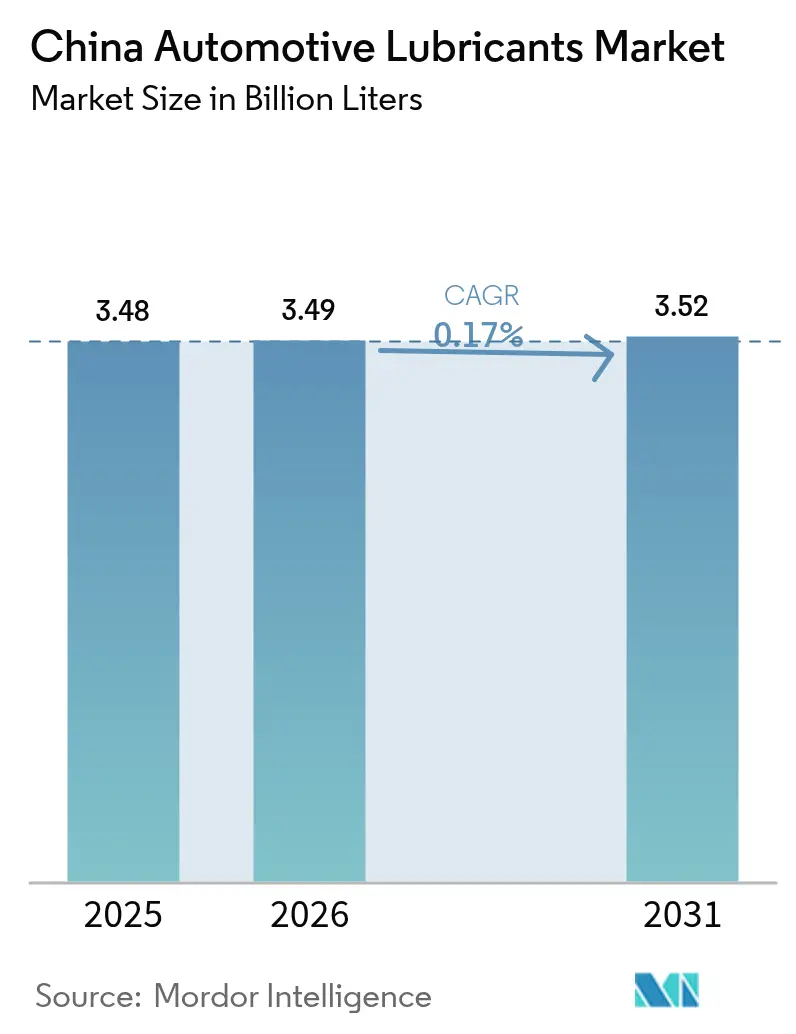

| Base Year Market Size (2025) | 3.48 Billion Liters |

| Market Volume (2026) | 3.49 Billion Liters |

| Market Volume (2031) | 3.52 Billion Liters |

| Growth Rate (2026 - 2031) | 0.17% CAGR |

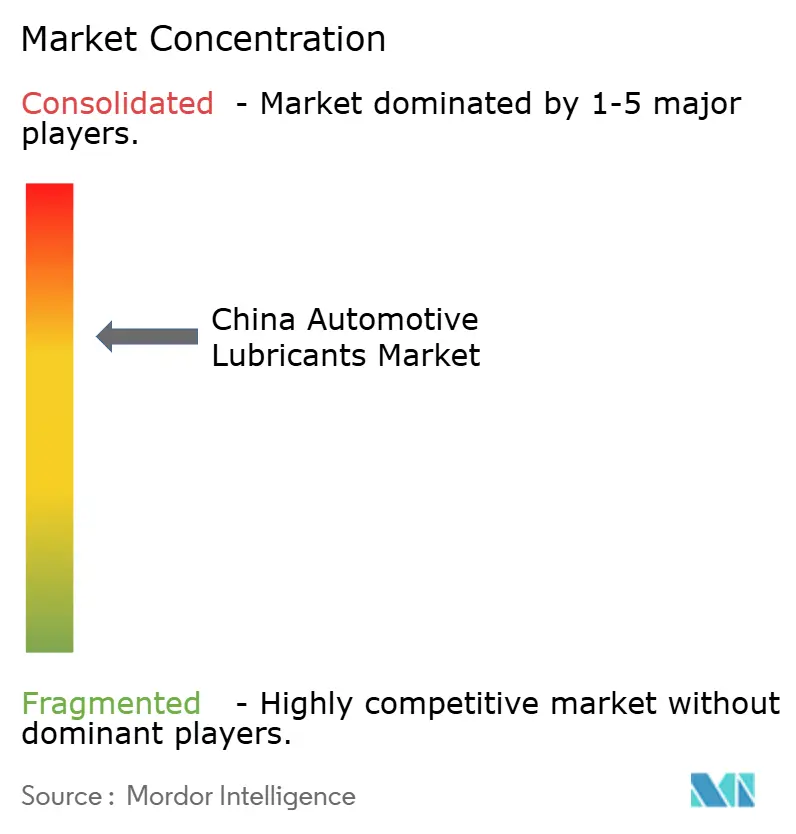

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Automotive Lubricants Market Analysis by Mordor Intelligence

The China Automotive Lubricants Market size is expected to grow from 3.48 Billion Liters in 2025 to 3.49 Billion Liters in 2026 and is forecast to reach 3.52 Billion Liters by 2031 at 0.17% CAGR over 2026-2031. Behind that fractional growth lie far-reaching shifts driven by electric vehicle penetration above 50%, the nationwide roll-out of China VI-B emission standards, and an accelerating pivot toward premium synthetic formulations. Engine oils still underpin demand, but wider adoption of continuously variable and dual-clutch transmissions is lifting specialist automatic transmission fluid volumes. Commercial vehicle electrification, the uptake of natural gas trucks, and the tightening of logistics footprints are reshaping lubricant viscosity preferences, while e-commerce channels are extending premium brands into Tier-3 cities. Suppliers are responding with localized factory-fill partnerships, RMB-scale capacity additions, and anti-counterfeit initiatives that together reposition value capture from simple volume to chemistry, service, and data-enabled solutions.

Key Report Takeaways

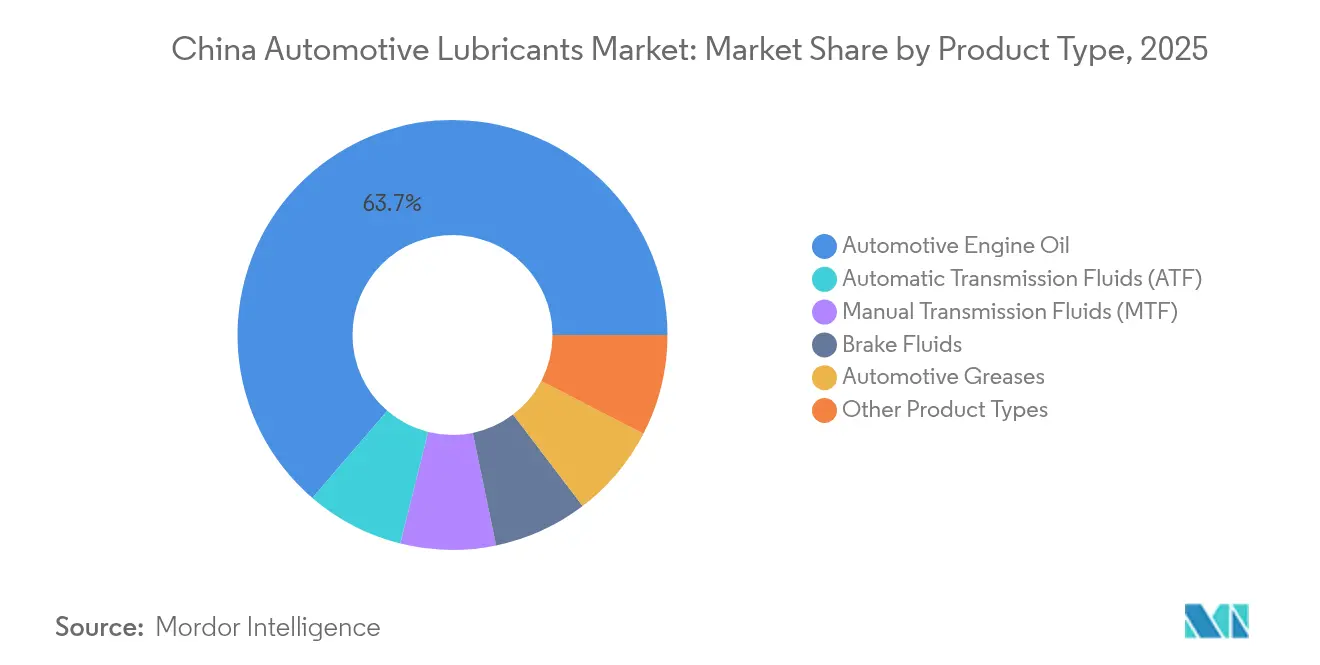

- By product type, automotive engine oil held 63.70% of the China automotive lubricants market share in 2025, while automatic transmission fluids are projected to clock the fastest 0.23% CAGR through 2031.

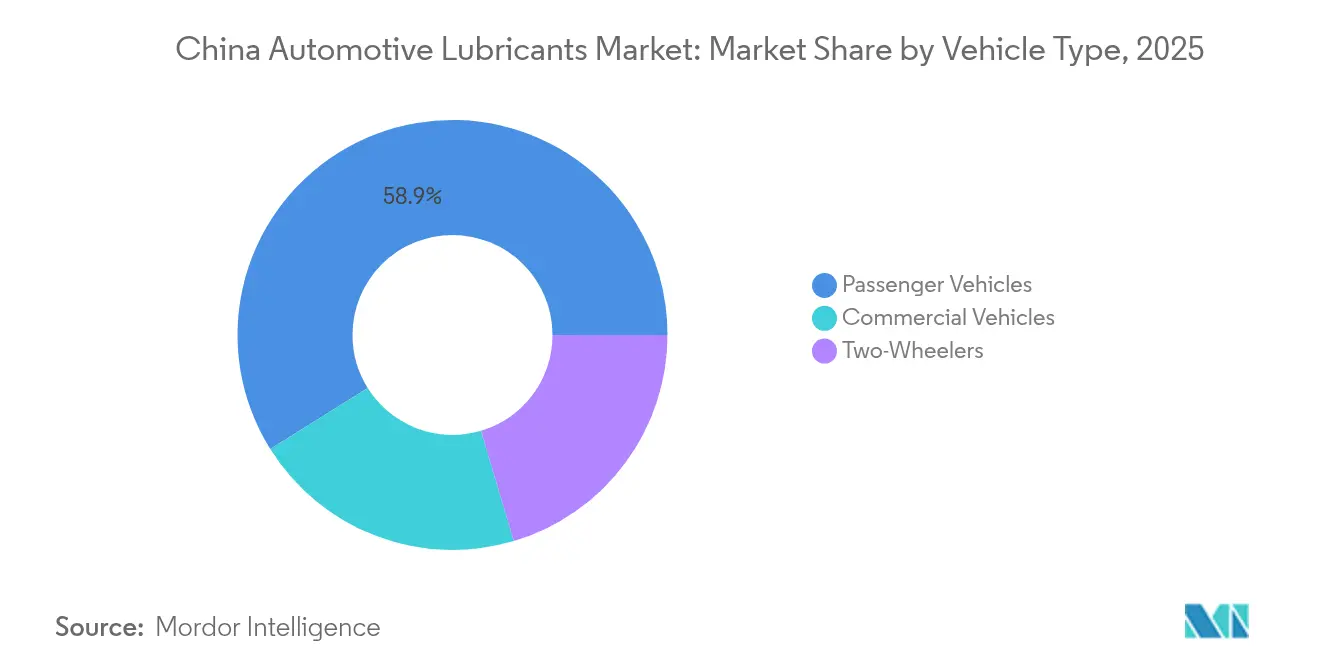

- By vehicle type, passenger vehicles accounted for 58.90% of 2025 demand, whereas commercial vehicles are expected to expand at a 0.35% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

China Automotive Lubricants Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Preference shift to OEM-approved synthetics | +0.8% | National, concentrated in Tier-1 cities | Medium term (2-4 years) |

| Electrified-powertrain lubricant reformulations | +0.4% | National, early adoption in Beijing, Shanghai, Shenzhen | Long term (≥ 4 years) |

| E-commerce aftermarket reach to Tier-3 cities | +0.3% | Tier-3 cities, rural markets | Short term (≤ 2 years) |

| Stricter China VI-B emission limits | +0.6% | National implementation | Medium term (2-4 years) |

| Localized OEM factory-fill partnerships | +0.5% | Manufacturing hubs: Guangdong, Jiangsu, Shanghai | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Preference Shift to OEM-Approved Synthetics

Automakers now specify low-ash API SP or ILSAC GF-7 oils that protect gasoline particulate filters and mitigate low-speed pre-ignition. The new ILSAC standard, effective March 2025, requires suppliers to reformulate with higher-purity synthetic basestocks and advanced antioxidant packages[1]Editorial Team, “GF-7 Standard Ushers New Era for Engine Oils,” LUBEZINE.COM. Consumers in Tier-1 cities value extended drain intervals and fuel-economy benefits, driving rapid penetration of 0W-20 and 5W-30 grades. Higher certification costs raise barriers to entry, favoring incumbents with robust research and development (R&D) capacities. As warranty compliance becomes a key purchase trigger, premium synthetics command pricing power that offsets the volume softness caused by electrification.

Electrified-powertrain lubricant reformulations

Hybrid and electric platforms impose intermittent combustion cycles, elevated thermal loads, and coolant contamination risks that legacy oils cannot manage. Suppliers are developing ester-rich synthetics with modified additive chemistries to stabilize viscosity during repeat start-stop events and maintain dielectric strength near high-voltage components. A 2025 white paper from Lubrizol identifies viscosity shear control, copper corrosion resistance, and multi-fuel compatibility as key research priorities[2]Technical Committee, “White Paper on Hybrid Lubricant Challenges,” AIQICHE.COM. These demands reward companies that can invest in tribology modeling and battery-coolant interaction studies, tilting the competitive advantage toward technology-led multinationals and well-capitalized domestic innovators.

E-commerce aftermarket reach to Tier-3 cities

Digital marketplaces now integrate short-video demonstrations, live-stream commerce, and click-to-install services, letting premium brands bypass fragmented wholesaler networks. Partnerships, such as Shell-JD and ExxonMobil-JD, pair algorithmic targeting with storefront visibility, pushing synthetic offerings into price-sensitive regions without incurring heavy bricks-and-mortar outlays. Tier-3 consumers gain access to authentic lubricants backed by online authenticity codes, shrinking the counterfeit trade and lifting average transaction values. Early data from the 2024-2026 China Lubricants White Paper shows double-digit online volume gains in smaller prefectures, evidence that channel innovation is a measurable demand lever.

Stricter China VI-B emission limits

The nationwide roll-out of China VI-B during 2025-2026 obliges low-SAPS chemistries to safeguard after-treatment devices. Meeting the tighter sulfur and phosphorus caps necessitates Group III or GTL basestocks plus boosted detergent and dispersant systems. Compliance testing stretches development cycles to more than 12 months and locks in OEM approval fees, discouraging opportunistic new entrants. Established majors leverage refined additive know-how and engine bench access, consolidating share as smaller blenders retreat. The regulation, therefore, elevates average price points and accelerates the shift toward the higher-margin synthetic tier.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising EV parc cannibalizing ICE oil demand | -2.1% | National, concentrated in Tier-1 cities | Long term (≥ 4 years) |

| Counterfeit lubricant proliferation | -0.4% | Tier-2 and Tier-3 cities, rural markets | Short term (≤ 2 years) |

| Extended oil-change intervals via IoT sensors | -0.8% | Commercial fleets, premium passenger vehicles | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising EV parc cannibalizing ICE oil demand

With fully electric cars expected to reach a 50% sales share in 2024, engine oil volumes in metropolitan centers are declining. E-scooters already hold a 25% share of two-wheel mobility, and forecasts indicate a near doubling by 2029, potentially sidelining small-engine lubricants. Logistics operators are piloting battery-electric vans that eliminate the need for crankcase oil, although they introduce a minor demand for gear-reducer fluids and dielectric coolants. Regional charging-infrastructure density correlates strongly with engine oil declines, forcing suppliers to hedge with EV-specific SKUs and service bundles that preserve wallet share even as liters fall.

Counterfeit lubricant proliferation

Seizures of more than 160 barrels of fake premium oil in single raids underline the scale of illicit blending operations. Counterfeiters mirror labels, QR codes, and even tamper-evident closures, eroding consumer trust and compressing legitimate price bands. The risk peaks in rural areas, where technical literacy is lower and seller verification is less effective. In response, major trials of blockchain-based traceability and mobile verification apps increase overheads that weigh on smaller legitimate brands. While enforcement campaigns create temporary supply disruptions, the long-term resolution hinges on systemic improvements in supply-chain transparency.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Engine-oil leadership counter-balanced by transmission-fluid momentum

Automotive engine oil retained 63.70% of 2025 demand, underscoring its centrality to the China automotive lubricants market. The segment’s resilience stems from China VI-B regulations that favor low-viscosity synthetics, lifting premium mix and price realization even as volume inches down. Semi-synthetic conversion is largely complete in Tier 1 workshops, but Tier 3 penetration remains an upside lever. On the other hand, automatic transmission fluids (ATF) claim only mid-single-digit volumes yet lead growth at a 0.23% CAGR through 2031, thanks to the uptake of CVT and dual-clutch technology in hybrids. Brake fluids and greases occupy niche but technology-intensive roles, with EV motor-bearing greases and DOT 4-plus brake fluids showing incremental upside. Power-steering fluids trend lower as electric systems proliferate, partially offset by the nascent demand for dielectric coolants in high-voltage battery packs, which fall outside traditional lubricant categories. Suppliers that package engine oils with ATF and emerging EV fluids stand to deepen wallet share while buffering against volume erosion in legacy lines.

The competitive hierarchy by product favors players with both API / ACEA certifications and local OEM endorsements. Synthetic formulations employing Group III+ or GTL basestocks enjoy an expanding proportion of the China automotive lubricants market share due to better oxidative stability and fuel-economy edge. Technical service, used-oil analysis, and drain-interval advisory increasingly differentiate offers in workshops and fleet depots, steering the market away from commodity barrels toward integrated aftersales ecosystems. This pivot stresses the importance of investment in additive science, bench testing, and field validation—capabilities concentrated among multinationals and the largest domestic refiners.

By Vehicle Type: Commercial-fleet outperformance amid passenger-car plateau

Passenger cars accounted for 58.90% of the 2025 lubricant volume, cementing their market share lead within the China automotive lubricants market. Yet the segment sits at a turning point: rising hybrid and battery-electric adoption clips growth, while stricter emissions shorten OEM-specified oil-change intervals via higher-grade synthetics, paring liters per service. Consequently, the China automotive lubricants market size attributed to passenger vehicles is expected to hover just above 2.05 billion liters through 2031. Commercial vehicles, meanwhile, post a modest but market-leading 0.35% CAGR. Long-haul trucking upgrades to LNG and CNG powertrains, each demanding specialized low-ash diesel oils with reinforced nitration control. Last-mile e-commerce fleets increase runtime hours, raising lubricant stress and frequency, even where mild electrification is implemented. Two-wheelers slide steadily as city bans on ICE mopeds and incentives for e-scooters bite into gasoline-engine usage.

Distinct duty cycles create divergent technical needs. Fleets value high-TBN, extended-drain diesel formulations paired with IoT monitoring, whereas passenger-car owners prioritize fuel economy and warranty compliance. These contrasts shape channel strategy: fleet supply gravitates toward direct contracts and on-site service trucks, while consumer sales lean on e-commerce and branded fast-fit chains. Suppliers straddling both arenas must tailor viscosity ladders, package sizes, and digital-service wraps, leveraging shared R&D yet customizing delivery models.

Geography Analysis

The eastern coastal provinces dominate the Chinese automotive lubricants market due to a confluence of vehicle assembly plants, petrochemical feedstock, and extensive after-sales networks. Guangdong, Jiangsu, and Shanghai collectively process more than 40% of lubricant blending output and host flagship OEM factory-fill contracts. Proximity to refineries enables cost-efficient supply of Group III basestocks, helping local blenders pivot swiftly to China VI-B compliant synthetics. In absolute terms, the coastal cluster contributed an estimated 1.45 billion liters in 2025, accounting for approximately 41.67% of the national total. Workshop density and higher consumer purchasing power in Tier-1 cities accelerate synthetic penetration, buttressing the premium mix even as EV adoption cannibalizes engine oil liters.

Moving inland, central provinces such as Hubei, Henan, and Sichuan represent expanding consumption corridors tied to rising car ownership and logistics investments. Tier-2 urban centers are linked to Belt and Road rail freight routes, which stimulate commercial-fleet lubricant demand. E-commerce-enabled reach propels premium brand availability beyond provincial capitals, narrowing historical quality gaps. Market-share analysis indicates that the adoption rates of ATF and low-viscosity engine oil in these locales now sit only two to three years behind coastal benchmarks, a lag that continues to shrink.

The western region, though smaller in absolute volume, registers the fastest relative growth. Government infrastructure outlays and energy-commodity projects lift heavy-duty equipment lubricant needs, while state incentives encourage domestic automakers to site plants in Chongqing and Guizhou. EV infrastructure trails the east, extending the life of ICE-centric demand. Supply-chain challenges linger, including counterfeit risks and limited cold-chain lubricant storage in high-altitude areas. Still, the rise of digital procurement portals is easing access to OEM-approved fluids, improving lubricant quality and expanding service-interval compliance.

Competitive Landscape

The China Automotive Lubricants Market is consolidated. Their refinery-to-retail reach, government fleet contracts, and robust dealer footprints establish formidable economies of scale. International majors—Shell, ExxonMobil, and TotalEnergies—control about one-quarter of demand by leveraging premium positioning, global OEM endorsements, and strong R&D pipelines. Smaller blenders lacking digital budgets face margin erosion or exit. Regulatory scrutiny on VOC emissions and waste-oil recycling further separates players: firms with closed-loop regeneration systems and compliance audit trails strengthen corporate procurement appeal.

China Automotive Lubricants Industry Leaders

BP p.l.c.

Exxon Mobil Corporation

Shell plc

China Petrochemical Corporation

PetroChina Company Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: China released its first independently developed diesel engine oil standard, known as the D1 standard. Developed over eight years and backed by an investment of nearly USD 27.5 million, the D1 standard has undergone more than 60,000 hours of bench testing and consumed 3,300 tonnes of fuel.

- July 2025: Lubrizol announced that its cutting-edge lubricant technology played a key role in the launch of a new hybrid-specific engine oil developed by Jiangsu Lopal Tech Co., Ltd., one of China’s independent lubricant brands.

China Automotive Lubricants Market Report Scope

By Product Type

| Automotive Engine Oil | 0W-XX |

| 5W-XX | |

| 10W-XX | |

| 15W-XX | |

| Monogrades | |

| Other Grades | |

| Manual Transmission Fluids (MTF) | |

| Automatic Transmission Fluids (ATF) | |

| Brake Fluids | |

| Automotive Greases | |

| Other Product Types (Power Steering Fluid etc.) |

By Vehicle Type

| Passenger Vehicles |

| Commercial Vehicles |

| Two-Wheelers |

| By Product Type | Automotive Engine Oil | 0W-XX |

| 5W-XX | ||

| 10W-XX | ||

| 15W-XX | ||

| Monogrades | ||

| Other Grades | ||

| Manual Transmission Fluids (MTF) | ||

| Automatic Transmission Fluids (ATF) | ||

| Brake Fluids | ||

| Automotive Greases | ||

| Other Product Types (Power Steering Fluid etc.) | ||

| By Vehicle Type | Passenger Vehicles | |

| Commercial Vehicles | ||

| Two-Wheelers |

Key Questions Answered in the Report

How large is China’s automotive lubricants consumption in 2026?

Total demand equals 3.49 billion liters in 2026 and is projected to edge up to 3.52 billion liters by 2031.

What share of demand comes from engine oil versus transmission fluids?

Engine oil accounts for 63.70% of national volume, whereas automatic transmission fluids are smaller but rising the fastest at a 0.23% CAGR through 2031.

How does surging electric-vehicle adoption affect lubricant suppliers?

EV penetration above 50% trims traditional engine-oil liters, yet it creates new need for specialized coolants, gear-reducer oils, and dielectric fluids, prompting suppliers to diversify their chemistry portfolios.

Which vehicle class will post the strongest lubricant volume growth to 2031?

Commercial vehicles lead with a 0.35% CAGR, helped by e-commerce logistics expansion and wider use of LNG/CNG trucks that need higher-performance low-ash oils.

Why are synthetic formulations gaining momentum in Tier-1 cities?

Stricter China VI-B standards, OEM warranty mandates, and consumer preference for longer drain intervals push Tier-1 workshops toward low-viscosity API SP or GF-7 synthetics.

Page last updated on: