Bandage Contact Lenses Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 6.88 Billion |

| Market Size (2031) | USD 9.96 Billion |

| Growth Rate (2026 - 2031) | 7.68% CAGR |

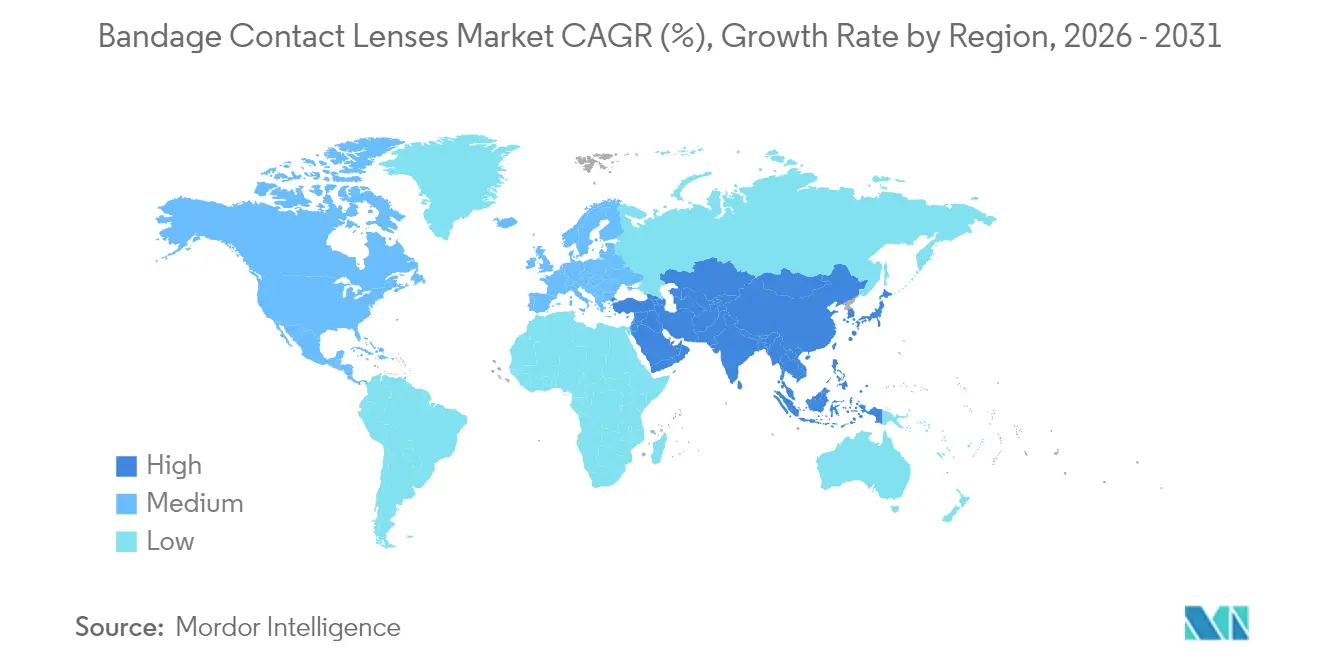

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Bandage Contact Lenses Market Analysis by Mordor Intelligence

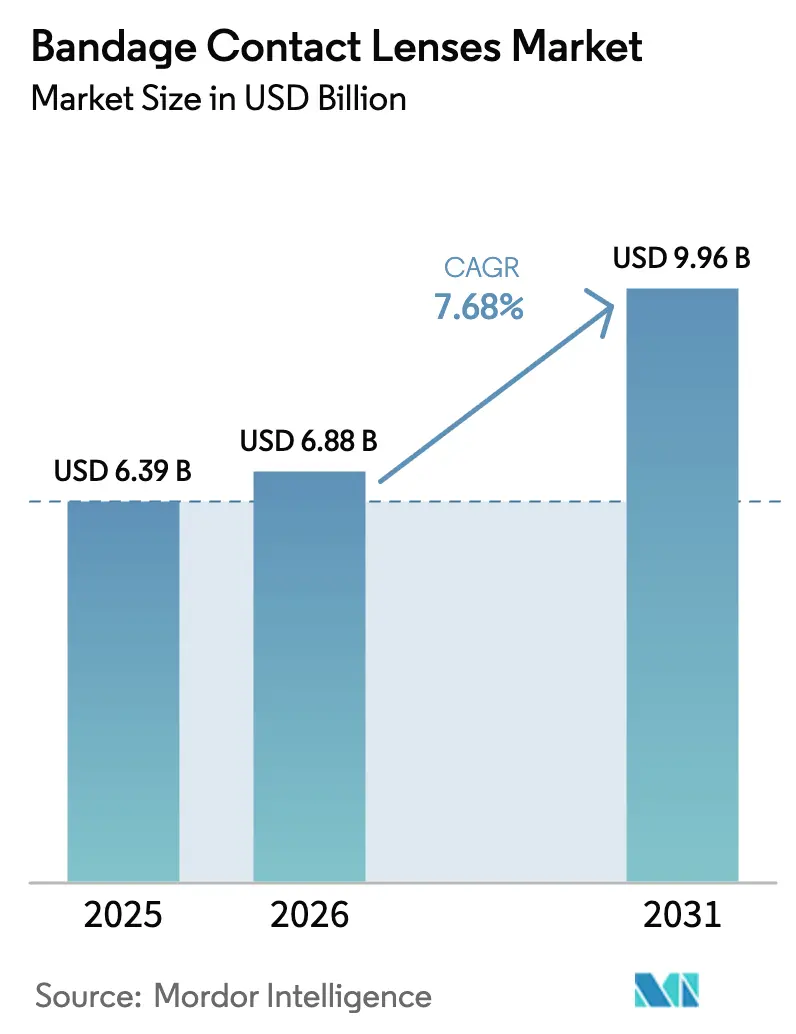

The Bandage Contact Lenses Market size was valued at USD 6.39 billion in 2025 and estimated to grow from USD 6.88 billion in 2026 to reach USD 9.96 billion by 2031, at a CAGR of 7.68% during the forecast period (2026-2031).

The uptrend reflects steady gains in silicone-hydrogel material science, widening post-surgical use, and accelerating therapeutic adoption for chronic ocular surface disease. High oxygen-permeability lenses now achieve 91% clinical-improvement and 94% patient-comfort ratings in therapeutic settings. Scleral and hybrid designs are scaling fastest as advanced fitting software tackles severe dry-eye and graft-versus-host disease cases. North American reimbursement that treats therapeutic lenses as prosthetic devices sustains premium pricing, while Asia-Pacific surgery growth funnels new postoperative users. On the supply side, moderate consolidation lets large incumbents fund R&D pipelines for AI-guided fitting and drug-eluting platforms that reinforce clinical differentiation.

Key Report Takeaways

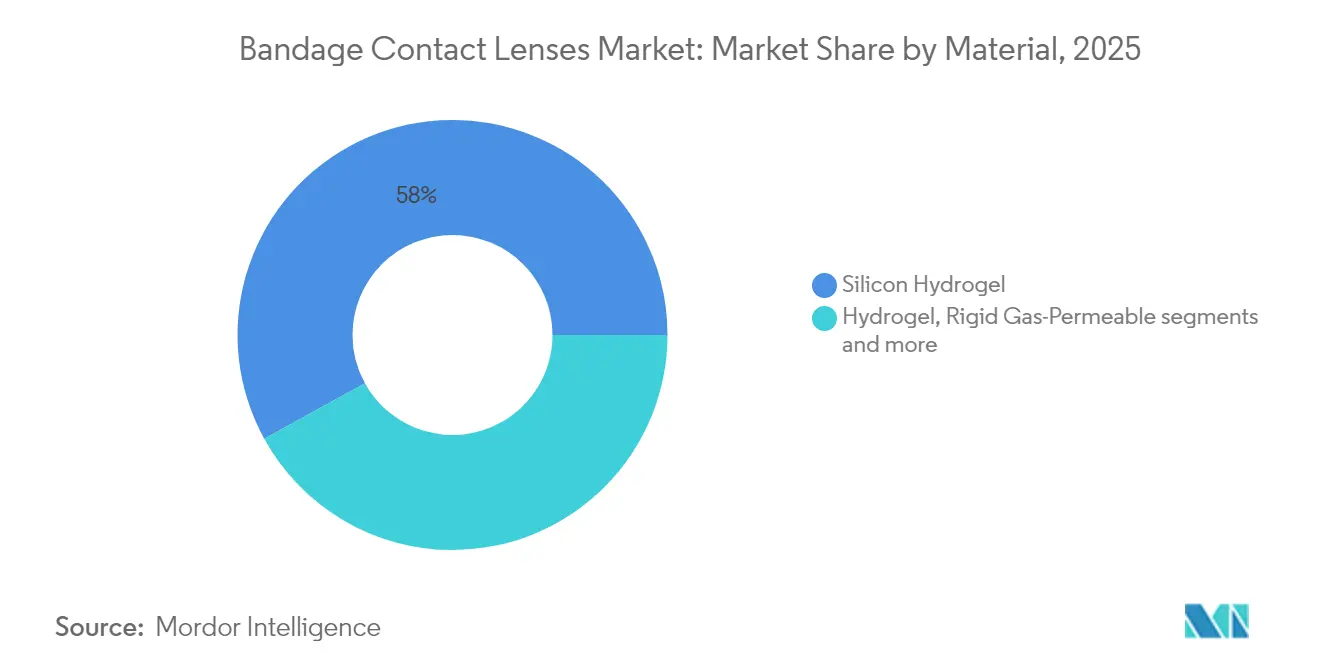

- By material, silicone hydrogel led with 58.02% of bandage contact lens market share in 2025; scleral & hybrid lenses are projected to expand at an 8.34% CAGR through 2031.

- By therapeutic application, post-refractive surgery accounted for 33.10% of the bandage contact lens market size in 2025, while dry-eye & ocular surface disorders are advancing at an 8.49% CAGR to 2031.

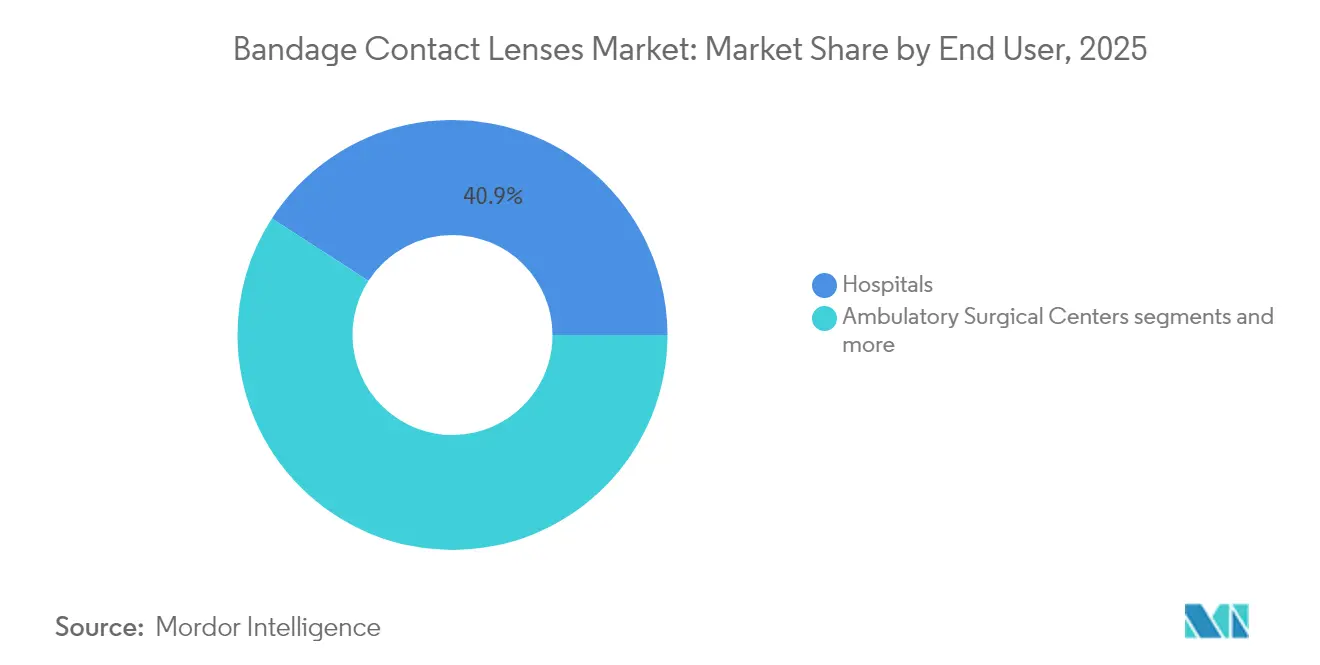

- By end user, hospitals held 40.88% of the bandage contact lens market share in 2025, whereas ophthalmology & optometry clinics are forecast to grow at an 8.63% CAGR through 2031.

- By geography, North America dominated with 44.90% revenue share in 2025; Asia-Pacific is set to post the fastest 8.85% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Bandage Contact Lenses Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Silicone-hydrogel dominance improves post-op outcomes | +1.2% | Global; North America & Europe lead adoption | Medium term (2-4 years) |

| Growing refractive & cataract surgery volumes in emerging Asia | +1.8% | APAC core, spill-over to MEA | Long term (≥ 4 years) |

| Surge in scleral/BCL use for chronic dry-eye & GVHD relief | +1.5% | North America & EU; expanding to APAC | Medium term (2-4 years) |

| Reimbursement expansion for therapeutic lenses | +0.9% | North America & EU | Short term (≤ 2 years) |

| Drug-eluting bandage lens pipelines | +1.1% | Global | Long term (≥ 4 years) |

| AI-guided custom lens design | +0.7% | North America & EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Silicone-hydrogel dominance improves post-op outcomes

Clinical studies report 83.78% complete corneal-healing and 91.16% pain-relief rates when silicone-hydrogel bandage lenses are applied after PRK. Oxygen transmissibility above 100 Dk/t mitigates hypoxia, cutting follow-up visits and lowering complication-related costs. Comparative trials show Senofilcon A outperforming Lotrafilcon A in visual recovery at 15 days and 1 month post-surgery. Superior material performance, economic savings, and readiness for drug-eluting upgrades cement silicone-hydrogel as the backbone of the bandage contact lens market.

Growing refractive & cataract surgery volumes in emerging Asia

Asia-Pacific performs the highest number of cataract and refractive surgeries worldwide, a trend linked to aging populations and rising myopia prevalence. Alcon’s regional investments in manufacturing and R&D target screen-time-related dry eye and myopia management using therapeutic lenses. As surgical suites upgrade from basic cataract extraction to laser refractive platforms, demand for postoperative bandage lenses escalates, yet fitting capacity disparities in rural areas signal opportunities for tele-fitting services.

Surge in scleral/BCL use for chronic dry-eye & GVHD relief

Early application of therapeutic lenses in severe dry-eye disease improves OSDI scores and fluorescein staining for at least 1 month. Specialty designs such as OmniLenz combine amniotic membrane with a protective lens, redefining chronic-disease management. Cost burdens remain high—median USD 1,500 annually for scleral-lens users versus USD 500 for conventional therapy—underlining the unmet need for durable comfort solutions.

Reimbursement expansion for therapeutic lenses (US, Europe)

Medicare categorizes therapeutic contact lenses as prosthetic devices when medical criteria are met, shielding patients from USD 1,000 to USD 7,000 per-eye costs in complex fits. Several European payers mimic this stance, although prior-authorization hurdles persist. Favorable coverage reduces long-term ocular-complication costs and encourages private insurers to follow suit

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Risk of microbial keratitis in extended wear | -1.4% | Global; higher in developing regions | Short term (≤ 2 years) |

| High unit cost versus traditional patching | -0.8% | Price-sensitive emerging economies | Medium term (2-4 years) |

| Limited specialist fitting capacity in South America & MEA | -1.1% | South America & MEA | Long term (≥ 4 years) |

| Regulatory lag for drug-device combinations | -0.6% | Global; FDA & EMA jurisdictions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Risk of microbial keratitis in extended wear

Contact-lens use predisposed 31.4% of infectious keratitis presentations in a 10-year multicenter review, with Pseudomonas aeruginosa the top pathogen. Although silicone-hydrogels enhance oxygen flux, overnight wear remains a vulnerability, raising compliance and education imperatives. Severe cases can cause irreversible vision loss, inflating treatment costs and medico-legal exposure.

High unit cost vs. traditional patching

Therapeutic lenses deliver superior outcomes, yet a single specialty fit can cost multiples of traditional eye-patch regimens. In lower-income markets this price gap curbs adoption until reimbursement or tiered-pricing schemes narrow the differential.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Silicone‐hydrogel leads therapeutic adoption

Silicone-hydrogel lenses held a 58.02% bandage contact lens market share in 2025, far outpacing other materials thanks to oxygen transmissibility that underpins safe extended wear. Within this bandage contact lens market size, silicone-hydrogel revenue is expected to compound in line with the overall 7.68% CAGR as new surface-treatment chemistries cut protein build-up. Drug-loading trials now attach cyclosporine nanomicelles to silicone-hydrogel matrices without degrading Dk/t, an advance poised to differentiate premium tiers.

Scleral and hybrid lenses, although accounting for smaller volume, are forecast to grow at 8.34% through 2031 as clinicians tackle complex ocular-surface disorders. These designs vault over corneal irregularities, creating a fluid reservoir that dampens pain and supports epithelial recovery. Traditional hydrogel materials continue a volume retreat due to hypoxia-related complications, while rigid gas-permeables keep niche indications in orthokeratology and high-astigmatism postsurgical eyes.

By Therapeutic Application: Post-surgical base with dry-eye outperformance

Post-refractive surgery retained the largest 33.10% slice of 2025 revenue, underpinned by standardized protocols that pair LASIK and PRK with immediate lens application to shield corneal flaps and ablation zones. This anchor segment's steady flow secures economic scale for manufacturers.

Dry-eye and ocular surface disorders are expected to grow at an 8.49% CAGR, contributing disproportionately to bandage contact lens market growth as autoimmune disease prevalence and digital-device fatigue increase. Corneal abrasions, ulcers, and infectious keratitis fill acute-care niches demanding antimicrobial-coated variants that shorten topical-drop regimens.

By End User: Hospitals retain bulk orders; clinics power incremental growth

Hospitals commanded 40.88% of 2025 revenue by virtue of handling most refractive and trauma cases requiring immediate bandage lens application. Teaching hospitals also serve as early-access sites for investigational drug-eluting designs, giving vendors clinical-trial throughput.

Ophthalmology and optometry clinics will post the highest 8.63% CAGR as postoperative follow-up and chronic-disease management shift to outpatient settings. Ambulatory surgery centers capture refractive volume migrating from inpatient theatres, while veterinary and academic labs provide small but innovative demand for specialty geometries that later migrate to human use.

Geography Analysis

North America accounted for 44.90% of global revenue in 2025, buoyed by Medicare and private-payer policies that reimburse therapeutic lenses as prosthetics, thereby softening patient out-of-pocket costs. Robust specialist density and advanced imaging equipment underpin high fitting success, encouraging surgeons to prescribe lenses immediately after laser correction. Regulatory momentum is strong; the FDA recently cleared Bruno Vision’s FusionTechnology daily therapeutic lens, validating an agile 510(k) pathway for incremental innovations.

Europe follows with well-established yet heterogeneous reimbursement rules. Scandinavian payers cover 100% of medically indicated scleral-lens costs, whereas Southern European systems often require prior authorization that extends wait times. EU centers publish influential evidence; multicountry trials on silicone-hydrogel drug delivery for bacterial keratitis are shaping clinical guidelines. Cross-border referral agreements also let patients in smaller member states access specialist fitting labs in Germany and France, enhancing overall adoption.

Asia-Pacific will expand at a 8.85% CAGR, the fastest worldwide, driven by surging refractive surgery throughput, rising screen-induced dry eye, and expanding middle-class healthcare budgets. Japan and South Korea exhibit mature therapeutic protocols and early drug-eluting trials, while China’s volume rests on vast myopia prevalence yet constrained by uneven specialist supply. Menicon’s partnership with Sigo aims to bridge that gap via localized supply and optometrist.

South America and Middle East-Africa together hold a modest share but represent sizable untapped pools. Fitter shortages delay scleral adoption; tele-mentoring pilots in Brazil show clinics can raise first-fit accuracy by 25% once remote corneal-topography review is integrated. Government import duties on medical devices remain another friction point that suppliers mitigate through regional assembly hubs.

Competitive Landscape

The bandage contact lens industry features a mid-level consolidation profile. Alcon led 2024 Vision Care revenue at USD 4.1 billion, channeling 7–9% of annual sales into 90-plus active projects focused on material science and drug-device integration. Bausch + Lomb’s INFUSE daily lens line marries high-water-content silicone-hydrogel with an OpticAlign stabilizer to capture astigmatic users. CooperVision’s clariti 1 day multifocal extensions broaden its presbyopia reach while direct-to-consumer campaigns raise brand stickiness.

Strategic M&A sharpen competitive moats. Alcon’s USD 430 million takeover of Lensar adds femtosecond-laser platforms that feed postoperative lens demand and create cross-selling synergies. EssilorLuxottica bought Espansione Group to bolster dry-eye therapeutics, aligning hardware with its lens portfolio. Johnson & Johnson Vision’s equity stake in TECLens positions it for future refractive technology convergence.

Innovation pipelines converge on AI and sustained drug delivery. MediPrint Ophthalmics is in late-stage trials for a dexamethasone-eluting lens to treat postoperative inflammation, potentially reducing drop-compliance issues. Smaller firms differentiate via niche coatings that resist midday fogging, a chronic complaint among scleral-lens users. Nevertheless, compliance costs for post-market surveillance and infection tracking favor well-capitalized players, sustaining the market’s moderate concentration.

Bandage Contact Lenses Industry Leaders

Alcon Inc.

Bausch & Lomb Incorporated (Bausch Health Companies, Inc.)

CooperVision (The Cooper Companies, Inc.)

Johnson & Johnson Vision Care, Inc. (Johnson & Johnson)

Advanced Vision Technologies

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Alcon completed its USD 430 million acquisition of Lensar, adding femtosecond-laser capabilities that expand therapeutic lens demand.

- February 2025: EssilorLuxottica acquired Cellview Imaging to enhance diagnostic hardware for custom lens fitting.

- January 2025: Bausch + Lomb announced plans to buy InflammX Therapeutics to advance drug-eluting lens R&D

Global Bandage Contact Lenses Market Report Scope

As per the scope of the report, bandage contact lenses are worn in the eyes for an extended period. A bandage contact lens is worn to protect the front part of the eye (cornea) during healing.

The bandage contact lenses market is segmented by lens type (soft lens and rigid lens), application (corneal disorders, post-ocular surgery, and other applications), distribution channel (hospital pharmacy, retail pharmacy, and online pharmacy), and geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report offers market sizes and forecasts in terms of value (USD) for the above segments.

| Hydrogel |

| Silicone Hydrogel |

| Rigid Gas-Permeable |

| Scleral & Hybrid |

| Post-Refractive Surgery |

| Post-Cataract Surgery |

| Corneal Abrasions & Erosions |

| Corneal Ulcers & Infectious Keratitis |

| Dry-Eye & Ocular Surface Disorders |

| Others (Trauma, Bullous Keratopathy) |

| Hospitals |

| Ambulatory Surgical Centers |

| Ophthalmology & Optometry Clinics |

| Others (Veterinary, Research) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa |

| By Material (Value) | Hydrogel | |

| Silicone Hydrogel | ||

| Rigid Gas-Permeable | ||

| Scleral & Hybrid | ||

| By Therapeutic Application (Value) | Post-Refractive Surgery | |

| Post-Cataract Surgery | ||

| Corneal Abrasions & Erosions | ||

| Corneal Ulcers & Infectious Keratitis | ||

| Dry-Eye & Ocular Surface Disorders | ||

| Others (Trauma, Bullous Keratopathy) | ||

| By End User (Value) | Hospitals | |

| Ambulatory Surgical Centers | ||

| Ophthalmology & Optometry Clinics | ||

| Others (Veterinary, Research) | ||

| By Geography (Value) | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the bandage contact lens market?

The Bandage Contact Lenses Market was valued at USD 6.88 billion in 2026 and is projected to reach USD 9.96 billion by 2031.

Which material dominates the bandage contact lens market?

Silicone-hydrogel lenses hold 58.02% of 2025 revenue owing to superior oxygen permeability and comfort.

Which application segment will grow fastest through 2031?

Dry-eye and ocular surface disorders are forecast to register the highest 8.49% CAGR as digital-device usage and autoimmune conditions rise.

How important is reimbursement to market growth?

Medicare and European coverage that classify therapeutic lenses as prosthetics significantly lower patient costs, accelerating adoption.

Page last updated on: