Contact Lens Solution Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 10.97 Billion |

| Market Size (2031) | USD 12.97 Billion |

| Growth Rate (2026 - 2031) | 3.40% CAGR |

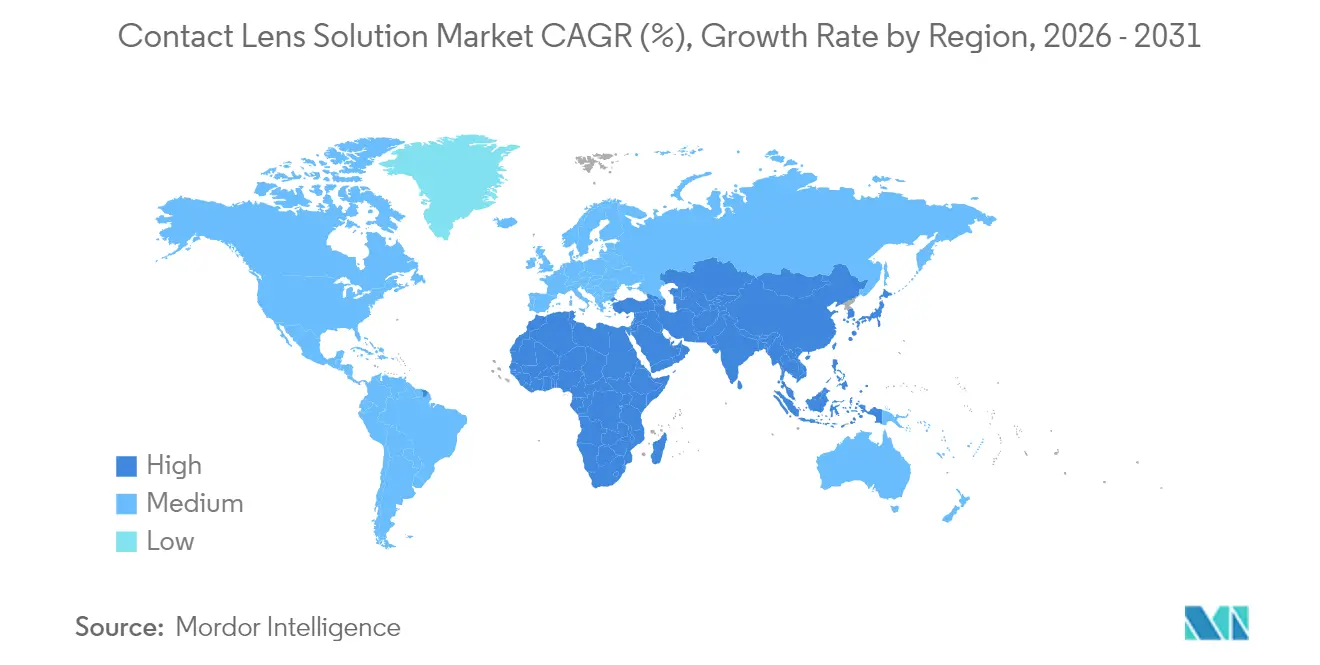

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

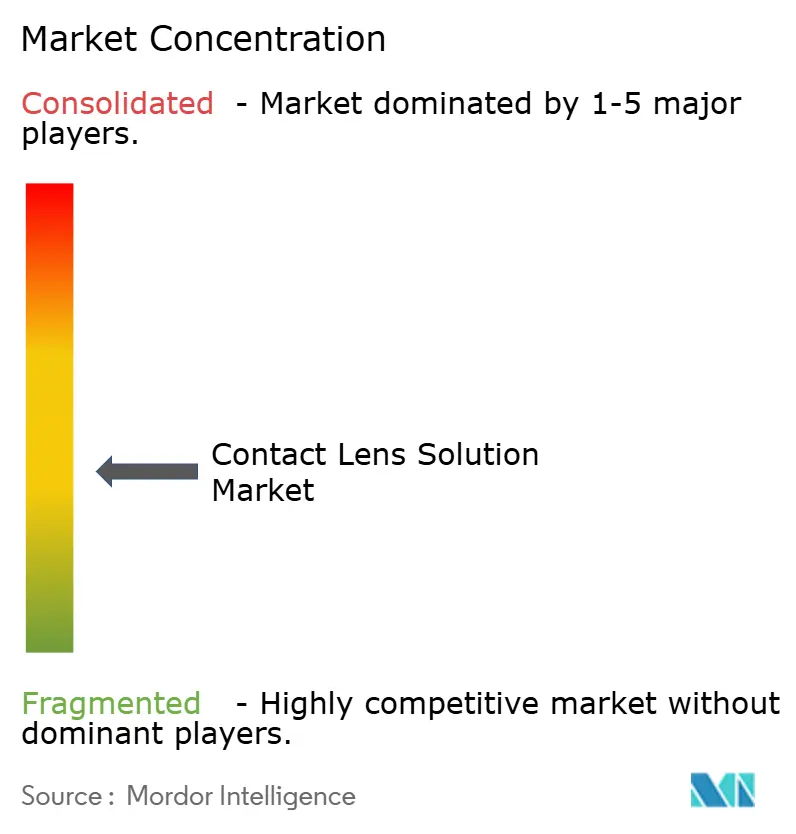

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Contact Lens Solution Market Analysis by Mordor Intelligence

Contact Lens Solution Market size in 2026 is estimated at USD 10.97 billion, growing from 2025 value of USD 10.61 billion with 2031 projections showing USD 12.97 billion, growing at 3.4% CAGR over 2026-2031.

Steady growth reflects a mature landscape in which incremental chemistry improvements, stricter sterility rules, and packaging-related sustainability mandates shape competitive advantage more than volume expansion. Multi-purpose mixes remain prevalent, yet peroxide-based systems are gaining favor as clinicians push for preservative-free disinfection that neutralizes emerging pathogens. Demand also rises for solutions compatible with drug-eluting and orthokeratology lenses, underscoring the market’s pivot toward specialty care. Regionally, Asia-Pacific’s surging myopia prevalence drives outsized consumption, while e-commerce subscriptions challenge brick-and-mortar outlets for share of replenishment transactions. At the same time, hydrogen-peroxide supply constraints and the European Union’s recycled-content targets heighten cost pressure, pushing producers to vertically integrate raw-material sourcing and revamp bottle designs.

Key Report Takeaways

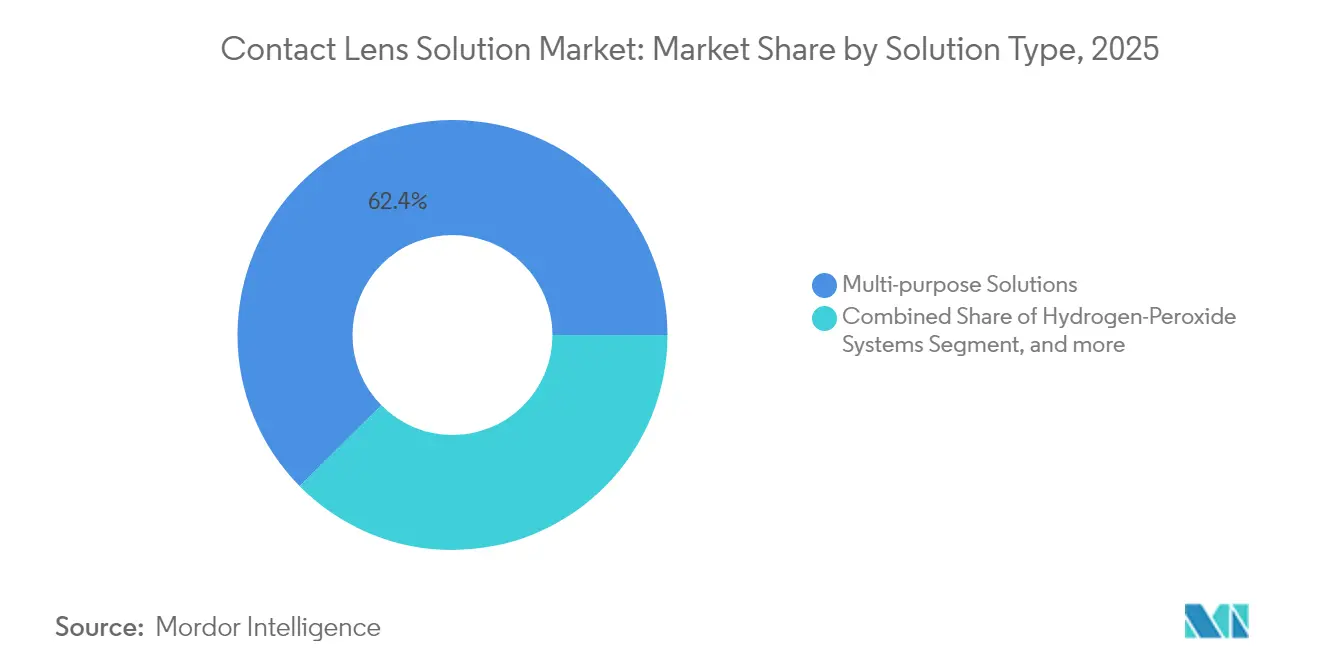

- By solution type, multi-purpose formulas accounted for 62.42% of the contact lens solution market share in 2025, whereas peroxide systems post the fastest 6.33% CAGR to 2031.

- By lens material, silicone-hydrogel applications represented 52.41% of overall demand in 2025, while rigid gas-permeable care is rising at a 5.85% pace as orthokeratology adoption spreads.

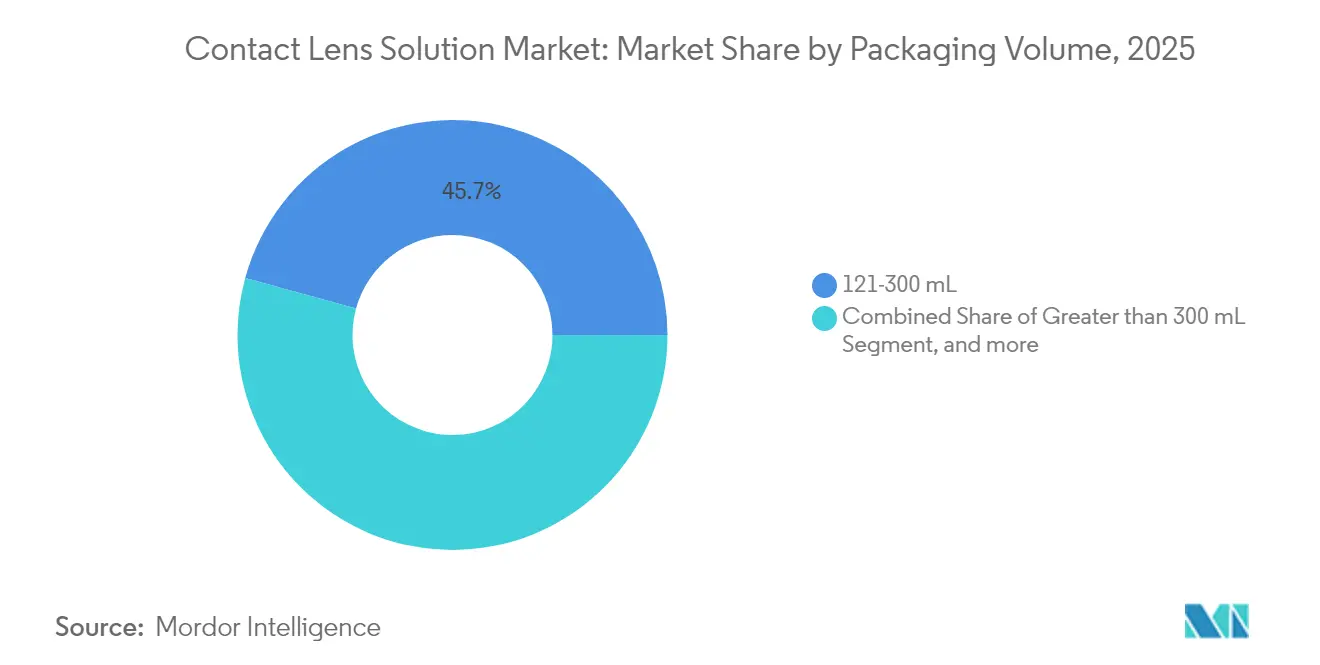

- By packaging volume, 121–300 mL bottles held 45.72% of revenue in 2025; formats ≤120 mL are growing at 7.76% CAGR on travel convenience and lower contamination risk.

- By distribution channel, retail pharmacies and optical stores controlled 42.05% of 2025 sales, yet e-commerce is accelerating 7.28% annually through 2031 on subscription uptake.

- By geography, North America held 37.62% of contact lens solution market size in 2025, while Asia-Pacific is poised to expand at an 8.61% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Contact Lens Solution Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing prevalence of refractive errors | +0.8% | Global, APAC concentration | Long term (≥ 4 years) |

| Digital-device–linked dry eye fueling hygiene product sales | +0.5% | Global urban centers | Short term (≤ 2 years) |

| Aging population demanding safer disinfection regimes | +0.4% | North America, EU, Japan | Long term (≥ 4 years) |

| Regulatory push toward preservative-free formulations | +0.2% | Global, EU-led | Medium term (2-4 years) |

| Rise in daily-disposable lens adoption boosting ancillary purchases | +0.6% | North America & EU | Medium term (2-4 years) |

| Drug-releasing soft lenses requiring compatible care fluids | +0.3% | Japan, expanding to US/EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Prevalence of Refractive Errors

Rising myopia, hyperopia, and astigmatism now account for 42% of vision impairment worldwide, a trend expected to place 4.7 billion people in need of correction by 2050. The United States alone is projected to reach 44.5 million myopic citizens by mid-century, with prevalence highest among African and Hispanic populations.[1]National Academies of Sciences, Engineering, and Medicine, “Understanding Myopia and Its Prevalence,” nationalacademies.org This epidemiological momentum enlarges the contact lens solution market by expanding the wearer base and by spurring demand for formulations tailored to orthokeratology and myopia-control lenses that require enhanced protein removal. Education-linked myopia growth in emerging economies further tilts future consumption toward Asia-Pacific. As governments recognize myopia as a public-health challenge, reimbursement frameworks may broaden, lifting uptake of premium peroxide and specialty solutions.

Digital-Device–Linked Dry Eye Fueling Hygiene Product Sales

Nearly 70% of U.S. adults suffer digital eye strain, and 99% of symptomatic users actively seek relief, translating screen-time exposure into higher solution turnover and a surge in rewetting drops.[2]CooperVision, “Research Reveals U.S. Screen Time and Digital Eye Strain Continue to Rise,” coopervision.com Reduced blinking from prolonged device use destabilizes the tear film and accelerates lipid deposition on lenses, prompting more frequent cleaning cycles. A 2024 Bausch + Lomb survey found 75% of dry-eye sufferers regard symptoms as bothersome, yet many are unaware that lens-care products can alleviate discomfort.[3]Bausch + Lomb, “Millions of Americans Experience Dry Eye Symptoms,” bausch.com Manufacturers respond with moisture-rich formulas containing humectants and anti-inflammatory agents that specifically target digitally induced dryness, driving premiumization within the contact lens solution market.

Aging Population Demanding Safer Disinfection Regimes

Populations in Japan, Germany, and the United States are aging rapidly, heightening sensitivity to preservatives such as benzalkonium chloride. Hydrogen-peroxide systems, which inactivate 99.9% of pathogens without using preservatives, therefore gain traction among seniors and command price premiums. Academic work has shown that benzalkonium concentrations as low as 0.0002% impair limbal stem-cell viability, underscoring the need for gentler care fluids. Rising disposable income in older cohorts supports the shift to advanced solutions, reinforcing the market’s tilt toward peroxide chemistry.

Regulatory Push Toward Preservative-Free Formulations

FDA and European regulators are tightening scrutiny of preservative-related adverse events, issuing guidance that elevates labeling standards and accelerates the shift toward preservative-free products. New EU Medical Device Regulation identifiers for contact lenses effective November 2025 will require firms to re-validate compatibility claims, effectively channeling R&D toward peroxide and single-dose units. Alcon’s February 2025 launch of SYSTANE PRO Preservative-Free demonstrates industry alignment with evolving rules.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift to no-solution daily disposables | -0.7% | Global, led by North America | Medium term (2-4 years) |

| Environmental scrutiny of single-use plastic bottles | -0.4% | EU leadership, global adoption | Long term (≥ 4 years) |

| Growing share of ortho-K overnight lenses | -0.5% | APAC core, spill-over to North America | Long term (≥ 4 years) |

| Volatile supply of medical-grade hydrogen peroxide | -0.3% | Global manufacturing hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Shift to No-Solution Daily Disposables

Daily disposable lenses eliminate the need for cleaning liquids and therefore divert spend away from the contact lens solution market. Brands position dailies as more hygienic and convenient, and clinical data confirm lower infection rates relative to reusable lenses. Scale economics are narrowing the cost gap, making daily disposables accessible to younger demographics who favor simplicity. As these cohorts mature, base-year demand for solutions could plateau unless care-fluid makers innovate around adjunct products such as rewetting drops and substrate-compatible cleaners for specialty

Environmental Scrutiny of Single-Use Plastic Bottles

The EU Packaging and Packaging Waste Regulation 2025/40 mandates 30% recycled content by 2030, forcing manufacturers to redesign bottle formats and absorb higher resin costs. Carbon-footprint studies reveal that when solution packaging is counted, the environmental difference between daily and monthly lenses narrows, putting additional spotlight on bottle waste. Brands now explore concentrated formulas in smaller vials and biodegradable materials, but transition costs may lift prices and dampen demand.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Solution Type: Multi-Purpose Dominance Faces Peroxide Disruption

Multi-purpose mixes controlled 62.42% of the contact lens solution market size in 2025 as the all-in-one proposition remains convenient for most wearers. Yet peroxide systems are riding a 6.33% CAGR to 2031 as practitioners favor their preservative-free profile and 99.9% antiviral efficacy.

Adoption accelerates in elder cohorts and in geographies with stringent sterility guidelines, pushing manufacturers to expand peroxide portfolios despite handling-time barriers. Meanwhile, protein remover tablets lose relevance as modern silicone-hydrogels resist deposits, and saline remains niche for rinsing. Market leaders bundle surfactant cleaners with peroxide kits to retain users within proprietary ecosystems, deepening brand loyalty in the contact lens solution market.

By Contact-Lens Material: Silicone-Hydrogel Leadership Drives Innovation

Silicone-hydrogel wearers generated 52.41% of solution demand in 2025, cementing the material’s central role in driving formulation R&D. Rigid gas-permeable applications, while smaller, are growing 5.85% annually because orthokeratology lenses use specialized overnight care regimens that command premium liquids.

Solution chemists address silicone’s lipid attraction by adding amphiphilic agents that lift oils without compromising lens hydrophilicity, while RGP fluids focus on high-viscosity wetting layers to maintain overnight comfort. Specialty scleral and drug-eluting materials create further micro-niches, widening the product matrix that sustains revenue growth in the contact lens solution market.

By Packaging Volume: Convenience Drives Smaller Formats

Containers between 121 mL and 300 mL captured 45.72% of 2025 sales as they balance unit cost and shelf life, yet bottles less than 120 mL are expanding 7.76% yearly due to travel convenience and reduced contamination risk. Smaller sizes align with airline liquids restrictions and meet rising consumer hygiene expectations for single-use packages.

EU recycled-content mandates further nudge producers toward compact bottles that use less resin per dose, while concentrated drops in ampoules may skirt plastics rules altogether. By coupling mini-vials with subscription e-commerce, brands create higher-frequency purchase cycles that lift the contact lens solution market size in value terms even if total liquid volume flattens.

By Distribution Channel: E-Commerce Disrupts Traditional Retail

Brick-and-mortar pharmacies and optical stores held 42.05% revenue in 2025, but online portals grow 7.28% annually through 2031 as prescription-portability rules enlarge digital share. Subscription models lock in replenishment, raising customer lifetime value for brands that curate bundles of lenses and care fluids.

Hospital dispensaries remain key for post-surgical kits and therapeutic lenses yet contribute limited incremental growth. Hybrid omnichannel strategies, in which users get fit offline and reorder online, blur historical boundaries and distribute bargaining power more evenly between producers and retailers operating in the contact lens solution market.

Geography Analysis

North America led with 37.62% market share in 2025, supported by clear FDA pathways, employer-based insurance, and high lens penetration. Growth moderates as daily disposables cannibalize multipurpose volumes, but peroxide upgrades cushion revenue. Canada mirrors U.S. regulatory frameworks, allowing cross-border supply optimization even amid currency swings.

Asia-Pacific drives the fastest 8.61% CAGR through 2031 on myopia’s meteoric rise and a burgeoning middle class eager for premium eye-care products. China’s pending 2027 NMPA reforms should expedite approvals, while Japan commands price premiums for specialty fluids compatible with drug-releasing lenses. India combines demographic youth with growing screen time, positioning it as a long-term demand node for moisture-rich solutions.

Europe posts stable mid-single-digit gains, navigating Medical Device Regulation complexities and the 2025/40 packaging law that forces bottle redesigns. Western markets are mature, yet Eastern Europe offers room for penetration as disposable incomes climb. The region serves as a test bed for recycled-content bottle innovation that could later diffuse to other regions, reinforcing Europe’s strategic role in the global contact lens solution market.

Competitive Landscape

The global contact lens solutions market is moderately fragmented and competitive. Four multinationals Alcon, Bausch + Lomb, Johnson & Johnson Vision, and CooperVision collectively hold significant revenue share, giving the sector a moderate concentration. Peroxide supply shocks, notably the 2022 recall triggered by reagent contamination, pushed leaders to intensify vertical integration and secure hydrogen-peroxide inputs. Technology differentiation drives edge: Johnson & Johnson’s FDA-cleared ketotifen-eluting lens rewrites compatibility demand, and Alcon’s USD 356 million acquisition. Start-ups pivot to sustainability, offering plant-based bottles or concentrated ampoules that appeal to eco-minded consumers. Private-label lines from online sellers undercut pricing yet struggle with sterility validation an entry barrier that favors incumbents. Global players fund real-world evidence studies to cement clinical trust, protecting margins as the contact lens solution industry evolves.

Contact Lens Solution Industry Leaders

Alcon

Bausch & Lomb Incorporated

CooperVision, Inc.

Johnson & Johnson Vision Care

Allergan (AbbVie)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Bausch + Lomb introduced Zenlens CHROMA HOA to the U.S. market a cutting-edge wavefront-guided scleral contact lens designed to correct higher-order aberrations (HOA). This custom lens technology enhances visual clarity by targeting complex optical distortions, significantly reducing symptoms like halos, glare, and blurred vision. Zenlens CHROMA HOA represents a major leap forward in precision optics, offering tailored solutions for patients with challenging visual profiles.

- April 2025: The FDA has approved Deseyne, a daily disposable contact lens developed by Bruno Vision Care, marking a significant advancement in ocular comfort technology. These lenses are embedded with bioactive substances that are gradually released throughout the day, enhancing hydration and wearer comfort.

- March 2025: Bausch + Lomb announced the U.S. launch of Arise, an advanced orthokeratology (Ortho-K) lens fitting system that leverages intelligent, cloud-based technology to revolutionize myopia management. Arise integrates directly with corneal topographers, enabling real-time, precision lens design using 3D imaging data. Notably, it features the first FDA-approved Ortho-K lens design with toric peripheral curves, allowing overnight myopia correction with enhanced customization for patients with astigmatism.

- January 2025: EyePrint Prosthetics, Advanced Vision Technologies, and Wave Contact Lens System have officially merged to form Wave Eye Care, a new division dedicated to specialty contact lenses. This strategic consolidation brings together deep expertise in custom lens fitting, enabling Wave Eye Care to offer a comprehensive portfolio of orthokeratology lenses, scleral lenses, and corneal gas-permeable lenses. The unified entity aims to streamline innovation and expand access to fully customized vision solutions for complex ocular needs.

Global Contact Lens Solution Market Report Scope

Contact lens solution is useful for cleaning, disinfecting, and storing contact lenses. There are many kinds of contact lens solutions, usually containing a binding agent, preservative buffer, and wetting agent. It kills the bacteria and keeps the lens safe for usage. The Market is Segmented by Solution Type (Multi-Purpose, Hydrogen Peroxide Based, and Other Solution Types), Material of Contact Lens (Gas Permeable Lens, Silicon Hydrogel, and Other Materials), Distribution Channel (E-Commerce, Retail, and Others), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions, globally. The report offers the value (in USD million) for the above segments.

| Multi-purpose Solutions |

| Hydrogen-Peroxide Systems |

| Saline & Daily Cleaners |

| Enzymatic Protein Removers |

| Other Solution Types |

| Silicone-Hydrogel Lenses |

| Hydrogel / Soft Lenses |

| Rigid Gas-Permeable (RGP) |

| Others |

| ≤120 mL |

| 121–300 mL |

| >300 mL |

| Retail Pharmacies & Optical Stores |

| E-commerce Platforms |

| Hospitals & Eye-Care Clinics |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Solution Type | Multi-purpose Solutions | |

| Hydrogen-Peroxide Systems | ||

| Saline & Daily Cleaners | ||

| Enzymatic Protein Removers | ||

| Other Solution Types | ||

| By Contact-Lens Material | Silicone-Hydrogel Lenses | |

| Hydrogel / Soft Lenses | ||

| Rigid Gas-Permeable (RGP) | ||

| Others | ||

| By Packaging Volume | ≤120 mL | |

| 121–300 mL | ||

| >300 mL | ||

| By Distribution Channel | Retail Pharmacies & Optical Stores | |

| E-commerce Platforms | ||

| Hospitals & Eye-Care Clinics | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the global contact lens solution market in 2026?

The contact lens solution market size is USD 10.97 billion in 2026.

Which solution type is growing the fastest?

Hydrogen-peroxide systems lead with a 6.33% CAGR through 2031.

Why is Asia-Pacific the key growth region?

Rising myopia prevalence and expanding middle-class access to vision correction push Asia-Pacific to a 8.61% CAGR.

How are environmental regulations affecting packaging?

EU rules require 30% recycled content by 2030, prompting bottle redesigns and pushing smaller volume formats.

What drives the shift toward e-commerce sales?

Prescription portability and subscription services allow online platforms to undercut traditional retail pricing by significant margins.

Which companies hold the majority market share?

Alcon, Bausch + Lomb, Johnson & Johnson Vision, and CooperVision together control about significant global revenue.

Page last updated on: