Automotive Throttle Position Sensor Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

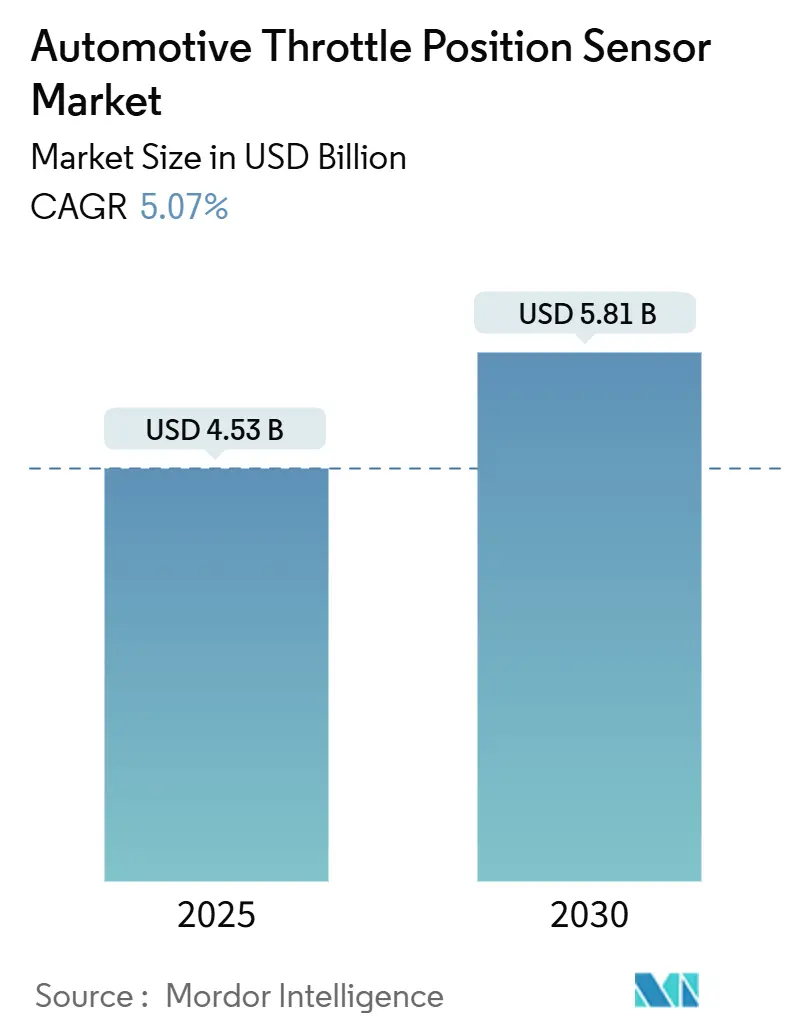

| Market Size (2025) | USD 4.53 Billion |

| Market Size (2030) | USD 5.81 Billion |

| Growth Rate (2025 - 2030) | 5.07% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

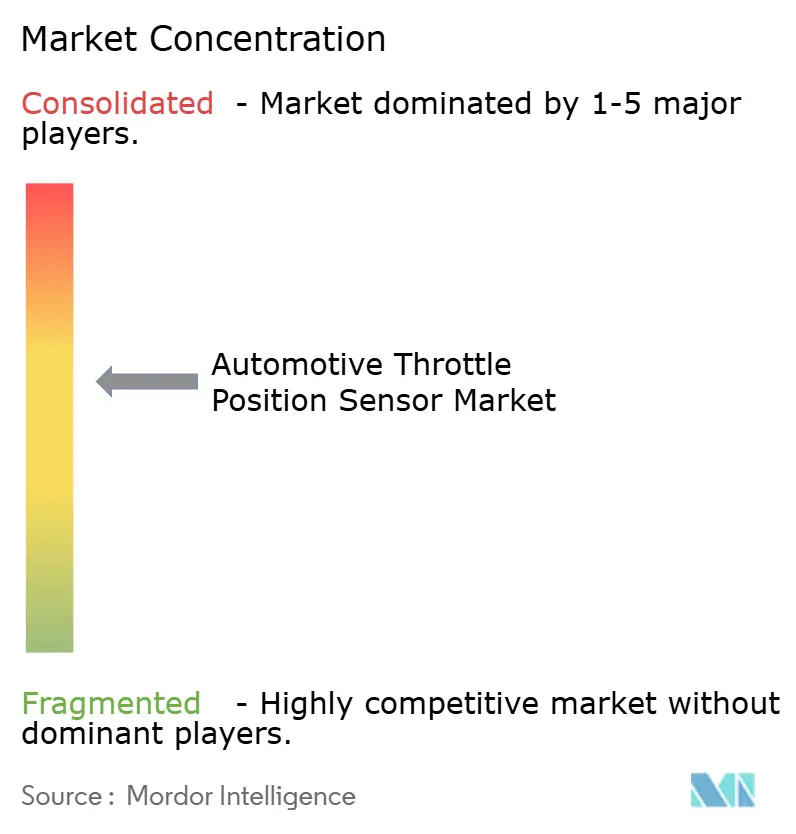

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Automotive Throttle Position Sensor Market Analysis by Mordor Intelligence

The Automotive Throttle Position Sensor Market size is estimated at USD 4.53 billion in 2025, and is expected to reach USD 5.81 billion by 2030, at a CAGR of 5.07% during the forecast period (2025-2030). Growing regulatory pressure for lower tailpipe emissions, the mainstreaming of battery-electric and hybrid drivetrains, and a near-universal shift to electronic throttle control architectures anchor this expansion. Non-contact Hall-effect and inductive magnetic sensing technologies are scaling quickly as OEMs replace potentiometers to gain durability and functional-safety benefits. Asia-Pacific’s deep electric-vehicle manufacturing base supports volume growth, while Europe’s Euro 7 framework drives demand for dual-channel, ISO 26262-compliant sensors. Supply-chain diversification and AI-enabled self-calibration are emerging as differentiators as Tier-1s and start-ups compete for design wins with BEV and ADAS platforms.

Key Report Takeaways

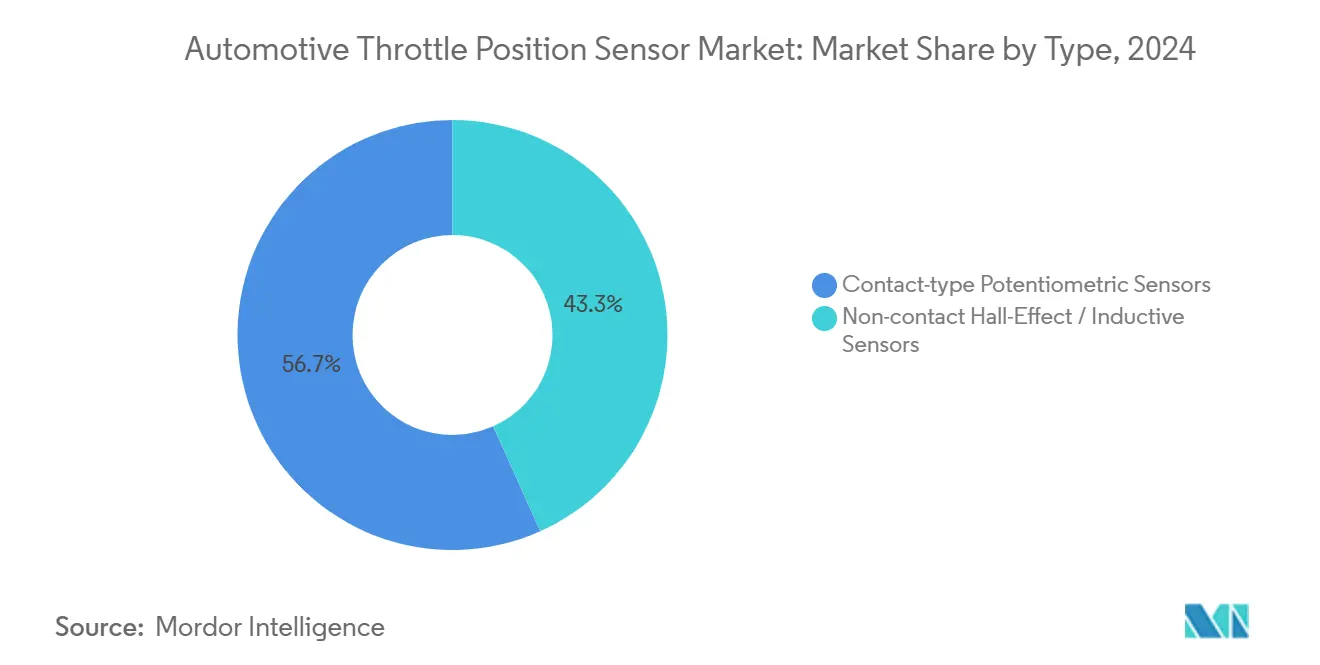

- By type, contact-type potentiometric sensors led with a 56.71% share of the Automotive Throttle Position Sensor Market in 2024, whereas non-contact Hall-effect and inductive devices are projected to expand at a 5.09% CAGR during the forecast period (2025-2030).

- By vehicle type, passenger cars commanded a 73.46% share of the Automotive Throttle Position Sensor Market in 2024; commercial vehicles are expected to grow at a 5.14% CAGR during the forecast period (2025-2030).

- By sales channel, OEM installations captured a 68.32% share of the Automotive Throttle Position Sensor Market in 2024; the aftermarket is expected to grow at a 5.15% CAGR during the forecast period (2025-2030) as global fleets age and replacement cycles shorten.

- By output type, analogue sensors held a 64.55% share of the Automotive Throttle Position Sensor Market in 2024; due to ADAS and drive-by-wire integration, digital interface units are expected to grow at a 5.11% CAGR during the forecast period (2025-2030).

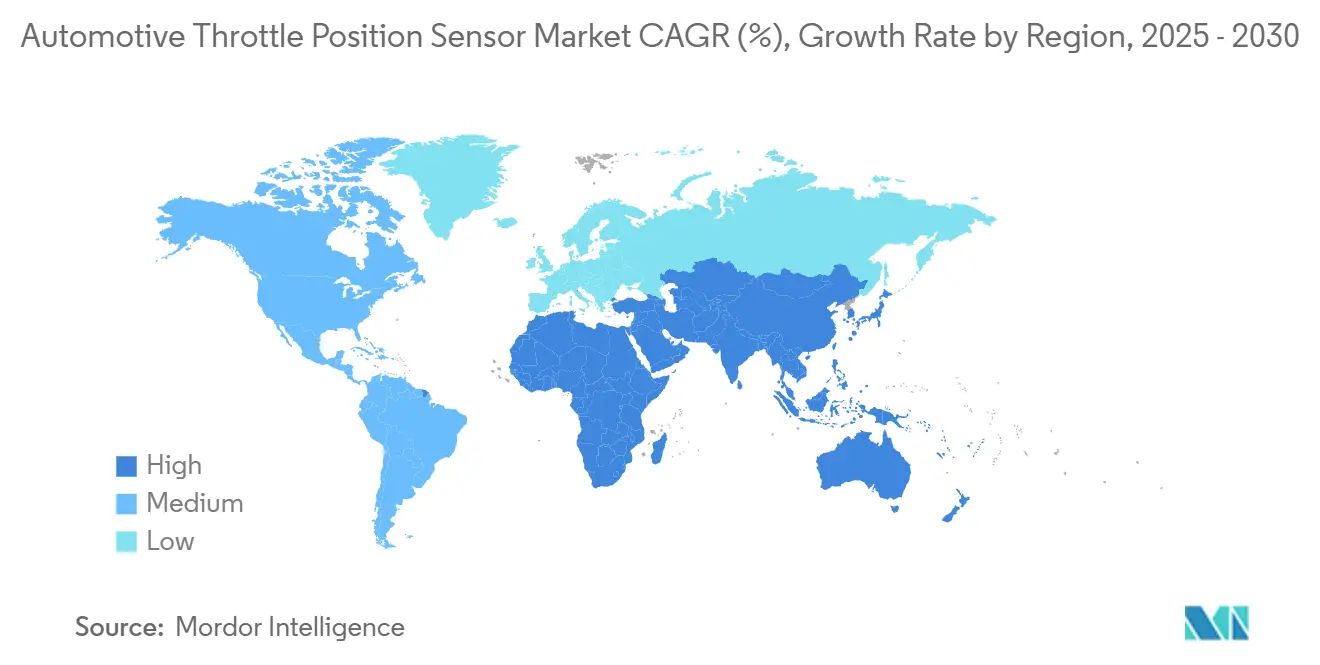

- By geography, Asia-Pacific accounted for a 42.28% share of the Automotive Throttle Position Sensor Market in 2024, while the Middle East and Africa are the expected to grow at a 5.12% CAGR during the forecast period (2025-2030).

Global Automotive Throttle Position Sensor Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging BEV/HEV Production | +1.8% | Asia-Pacific core, spill-over to Europe and North America | Medium term (2-4 years) |

| Rapid OEM Shift To Electronic Throttle Control Architectures | +1.5% | Global, led by Asia-Pacific manufacturing hubs | Short term (≤ 2 years) |

| Stricter Emissions and Fuel-Economy Legislation | +1.2% | Global, with early adoption in EU and North America | Medium term (2-4 years) |

| Rising ADAS & Drive-By-Wire Adoption | +0.9% | North America and EU, expanding to Asia Pacific premium segments | Long term (≥ 4 years) |

| Magnetic-Core Dual-Channel TPS | +0.7% | Global, with emphasis on safety-critical applications | Medium term (2-4 years) |

| AI-Enabled Self-Calibrating TPS | +0.4% | Global, with early adoption in premium vehicle segments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging BEV/HEV Production in Asia-Pacific & Europe

China continues to lead the global shift toward electrification, with record-breaking sales of new-energy vehicles reinforcing its dominant position in the market[1]"NEV Sales Report 2024," China Association of Automobile Manufacturers, caam.org.cn . As high-voltage SiC inverters subject sensors to intense temperatures and powerful magnetic fields, there's a swift pivot towards non-contact designs, bolstered by sophisticated thermal compensation. European production growth, backed by government incentives, echoes this requirement and emphasises cybersecurity for over-the-air diagnostics. Mild-hybrid 48V platforms, especially across ASEAN, seek low-cost magnetic sensors that still meet immunity thresholds, broadening the customer base. Suppliers that can tailor ASIC filters for EMI suppression gain a competitive advantage.

Rapid OEM Shift to Electronic Throttle Control Architectures

Mechanical cables have virtually disappeared from new powertrains, replaced by drive-by-wire systems that depend on continuous dual-channel position sensing. The architecture enables variable-valve timing, cylinder deactivation, and seamless EV-ICE transitions, each demanding millisecond-level throttle resolution[2]"Electronic Throttle Control Systems," Society of Automotive Engineers, sae.org . Hall-effect and tunnel-magnetoresistance (TMR) chips are now preferred over potentiometers for their wear-free operation and relaxed mounting tolerances. ISO 26262 criteria foster dual-core magnetic designs that offer independent plausibility checking. Migration also underpins predictive cruise control and collision-avoidance features that modulate torque with less latency than mechanical linkages.

Stricter Emissions & Fuel-Economy Legislation

The Euro 7 regulation tightens standards for new vehicle types, mandating on-board monitoring systems that continuously track throttle positions. Durability standards are heightened, compelling OEMs to utilize sensors with minimal drift and built-in diagnostics. Cybersecurity measures in the regulation are hastening the adoption of encrypted communication protocols like SENT and PSI5. Frameworks in China, India, and the United States echo the EU's stance, spurring global demand for compliant sensor technologies. Moreover, new rules for driver-distraction warning systems necessitate precise throttle input data to link pedal actions with camera-based gaze tracking, intensifying performance demands.

Rising ADAS & Drive-By-Wire Adoption Demanding Redundant TPS Feedback

Level 2+ driver-assist features rely on accurate throttle data to forecast speed changes during adaptive cruise, lane-merge, and automated parking. OEMs are integrating dual AMR or hybrid magnetic-inductive stacks to provide a 2-of-3 voting logic, underscoring the necessity of fail-operational redundancy without a mechanical fallback[3]"ADAS Safety Standards," National Highway Traffic Safety Administration, nhtsa.gov. Digital SENT links support checksum and error signalling, allowing controllers to degrade gracefully upon fault detection. As autonomous systems advance, latency in position sensors is emerging as a critical bottleneck, driving vendors to develop advanced 360-degree TMR arrays with strong immunity to magnetic interference. Cloud-connected diagnostics also enable remote calibration updates, helping manufacturers reduce warranty-related costs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility In Automotive-Grade ASIC | -0.8% | Global, with acute impact on cost-sensitive segments | Short term (≤ 2 years) |

| High ASIL-D Validation Costs | -0.6% | Global, affecting premium and safety-critical applications | Medium term (2-4 years) |

| Cyber-Security Risks | -0.4% | North America and EU, expanding to connected vehicle markets | Long term (≥ 4 years) |

| Thermal Drift Issues | -0.3% | Global, concentrated in BEV/HEV applications | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatility in Automotive-Grade ASIC & Rare-Earth Magnet Pricing

Supply shocks in 2024 raised ASIC lead times and pushed TMR magnet costs higher as Chinese export policies tightened. Sensor makers experienced a margin squeeze under OEM cost-down contracts and scrambled to secure multi-foundry wafer allocations. Recycling programs for neodymium and dysprosium are emerging to curb exposure, while some vendors prototype rare-earth-free inductive sensors. Dynamic pricing clauses and commodity hedging are becoming standard in long-term agreements. Smaller suppliers without hedging capacity risk losing bids in the highly price-sensitive aftermarket.

High ASIL-D Validation Costs

ISO 26262 ASIL-D certification, while crucial, inflates development costs and prolongs project timelines, complicating safety-critical automotive initiatives. Engineering budgets feel the strain from dual-path hardware, in-depth fault-injection testing, and mandatory third-party audits, a challenge more easily navigated by larger Tier-1s boasting established safety infrastructures. Start-ups venturing into AI-driven calibration grapple with heightened scrutiny; their machine-learning algorithms demand novel validation frameworks, a topic still in regulatory debate. This financial strain fuels M&A activity, with industry giants swiftly onboarding niche innovators to expedite compliance. Meanwhile, some OEMs adopt a segmented sourcing strategy, opting for ASIL-D units in drive-by-wire systems while using lower-grade components for non-critical applications, striking a balance between cost and safety.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Magnetic Sensing Gains Ground

The Automotive Throttle Position Sensor market share for contact-type potentiometric devices in 2024 was 56.71% of the global value. Yet non-contact Hall-effect and inductive options are rising at a 5.09% CAGR and are forecast to eclipse three-fifths of the market by 2030. Hall-effect chips eliminate wear and meet extended emission warranty durations. TMR technology delivers signal-to-noise improvements up to 1,000 times greater than legacy Hall cells, enabling finer torque control for hybrid transitions.

Demand for inductive sensors accelerates in premium BEVs because the design tolerates 360-degree rotation and rejects stray fields from high-current busbars. Magnetic-core dual-channel layouts fulfil ISO 26262 requirements without complex secondary shafts, reducing assembly cost. Potentiometers continue to serve cost-sensitive entry models where drive-by-wire redundancy is not mandatory. Vendors are phasing hybrid packages with resistive and magnetic tracks to smooth migration for mixed powertrain portfolios within regional OEM line-ups.

By Vehicle Type: Commercial Segment Accelerates

Passenger cars generated 73.46% of the Automotive Throttle Position Sensor market share 2024. Growth moderates as penetration nears saturation, but new ADAS features still attract higher-value digital sensors. Commercial vehicles, however, post the briskest 5.14% CAGR to 2030 as logistics fleets electrify in response to zero-emission delivery mandates.

Heavy-duty engines demand highly durable sensors capable of withstanding intense vibration and thermal shock, leading OEMs to favor dual-channel Hall or inductive designs with robust housings. AI-enabled self-calibration is gaining traction among fleet operators as it helps minimize costly downtime. Regulatory frameworks such as Euro 7 are extending onboard monitoring requirements to larger trucks, increasing the importance of throttle-feedback accuracy. Suppliers integrating sensor data into predictive maintenance platforms are seeing strong adoption, as large fleets prioritize reducing unplanned service interruptions.

By Sales Channel: OEMs Anchor Volume, Aftermarket Grows

OEMs absorbed 68.32% of global shipments in 2024. Factory installations benefit from direct engine controller integration and proprietary calibration data access. Aftermarket channels, however, are expanding at a 5.15% CAGR through 2030, reflecting both ageing vehicle fleets and the proliferation of diagnostic tools that pinpoint throttle-sensor faults.

Replacement cycles for electronic throttle bodies are shortening compared to mechanical predecessors, especially in regions with harsh climates. The aftermarket faces technical challenges as OEMs shift to digital-output sensors that require specialised programming tools. Euro 7 type-approval rules will restrict non-compliant replacement parts from 2026, raising the barrier for independent suppliers. Genuine OEM parts retain three-fifths of the replacement segment due to complex calibration requirements, though third-party manufacturers are gaining share with sensors that self-adjust to vehicle-specific parameters.

By Output Type: Digital Interfaces Outpace Analogue

Analogue-output sensors held 64.55% of the Automotive Throttle Position Sensor market share in 2024 but are losing ground to digital alternatives that expand at a 5.11% CAGR. SENT, PSI5, and Short PWM Code interfaces deliver higher bandwidth and support advanced diagnostics that cannot match analogue voltage signals. Digital sensors also enable redundancy checks and error detection, essential for ISO 26262 compliance.

Hybrid designs providing analogue and digital outputs help OEMs manage the transition across mixed-architecture fleets. Self-calibrating features in digital units reduce warranty claims by compensating for drift in real time. The shift to digital is most pronounced in electrified and autonomous platforms, where throttle-position data feeds multiple control modules simultaneously. Regulatory frameworks increasingly specify digital communication standards for safety-critical sensors, accelerating the move from analogue-only solutions.

Geography Analysis

Asia-Pacific commanded 42.28% of the Automotive Throttle Position Sensor market share in 2024, generating a massive revenue. China remains the dominant force in global electrification, with strong domestic sales of new-energy vehicles anchoring regional growth and reinforcing its leadership in BEV and HEV manufacturing. ASEAN countries are emerging as significant contributors as they localise domestic consumption and export supply chains. The proliferation of high-voltage architectures and SiC power electronics in Asian BEVs drives the adoption of advanced magnetic-core and TMR sensors that withstand electromagnetic interference.

Europe maintains its position as the regulatory pacesetter with Euro 7 and the General Safety Regulation imposing stringent sensor accuracy, durability, and cybersecurity requirements. The region's established OEM base and Tier-1 ecosystem foster innovation in functional safety and digital diagnostics. European automakers have adopted dual-channel, ASIL-D certified throttle position sensors, particularly in premium segments. The EU's focus on lifecycle emissions compliance creates demand for sensors with extended operational life and robust self-diagnostic capabilities. Market growth receives further support from investments in BEV and hybrid vehicle production, with mandatory on-board monitoring systems reinforcing the critical role of throttle position feedback.

North America steadily adopts advanced throttle position sensor technologies as regulations converge with European standards and electrified vehicle offerings expand. The region's competitive landscape features global suppliers and domestic manufacturers, emphasising functional safety and cybersecurity. Aftermarket demand rises as the vehicle parc ages and electronic throttle systems become ubiquitous. ADAS integration and autonomous vehicle development accelerate the adoption of digital and redundant sensor architectures, positioning North America as a key market for next-generation solutions. While smaller in absolute terms, the Middle East & Africa region is growing at a 5.12% CAGR during the forecast period (2025-2030), driven by automotive sector diversification and gradual adoption of emissions standards modelled on EU frameworks.

Competitive Landscape

The Automotive Throttle Position Sensor market remains moderately consolidated, with global Tier-1 suppliers like Bosch, Continental, and Denso dominating OEM channels through established relationships and comprehensive functional safety expertise. These incumbents leverage ISO 26262 ASIL-D certified product lines and magnetic-core dual-channel architectures to maintain market share amid evolving regulatory requirements. Strategic moves in 2025 include vertical integration across sensor portfolios and expansion into AI-enabled self-calibrating solutions that address OEM warranty priorities.

Emerging players target high-growth segments such as BEV platforms, ADAS integration, and aftermarket diagnostics. Companies specialising in TMR and hybrid magnetic-inductive technologies gain traction by offering superior accuracy and stray-field immunity. Patent filings reveal an industry-wide focus on dual-sensor architectures and self-diagnostics to support fail-operational requirements in drive-by-wire applications. Competitive intensity increases with supply chain disruptions affecting automotive-grade ASICs and rare-earth magnets, prompting investments in alternative sourcing and rare-earth-free sensor technologies.

Regulatory influence shapes competitive dynamics, with Euro 7 and the EU Cyber Resilience Act raising standards for sensor cybersecurity and data integrity. Suppliers unable to meet these requirements risk market exclusion, while those with advanced compliance infrastructure capture share as enforcement tightens. Strategic partnerships accelerate as established and emerging players seek to close capability gaps and secure access to next-generation sensor platforms. TDK's January 2024 collaboration with Goodyear exemplifies this trend, combining sensor hardware with tyre expertise to develop integrated intelligence systems.

Automotive Throttle Position Sensor Industry Leaders

-

Robert Bosch GmbH

-

Continental AG

-

Denso Corporation

-

BorgWarner Inc.

-

HELLA GmbH & Co. KGaA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2024: Bosch unveiled cutting-edge technologies at the Bosch Mobility Experience, spotlighting advancements tailored for electric vehicles (EVs). Emphasising a holistic approach, the company presented a suite of solutions centred on electrification, prioritising the seamless integration of advanced hardware and software to boost performance and efficiency.

- January 2024: TDK and Goodyear announced a collaboration to develop next-generation tyre intelligence systems, integrating TDK's sensor hardware and software with Goodyear's tyre expertise. The partnership targets real-time road-to-tire-to-vehicle intelligence, with implications for sensor integration in advanced vehicle platforms.

Global Automotive Throttle Position Sensor Market Report Scope

| Contact-type Potentiometric Sensors |

| Non-contact Hall-Effect / Inductive Sensors |

| Passenger Vehicles |

| Commercial Vehicles |

| OEM |

| Aftermarket |

| Analog |

| Digital |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle-East and Africa |

| By Type | Contact-type Potentiometric Sensors | |

| Non-contact Hall-Effect / Inductive Sensors | ||

| By Vehicle Type | Passenger Vehicles | |

| Commercial Vehicles | ||

| By Sales Channel | OEM | |

| Aftermarket | ||

| By Output Type | Analog | |

| Digital | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is driving growth in the throttle position sensor industry?

Growth is primarily driven by stricter emissions regulations like Euro 7, rapid electrification with 12.85 million NEVs sold in China in 2024, and the industry-wide shift to electronic throttle control systems that require precise position feedback. The market is projected to grow at a 5.07% CAGR, reaching USD 5.81 billion by 2030.

Which sensor technology is replacing traditional potentiometers?

Non-contact Hall-effect and magnetic inductive sensors are replacing potentiometers, growing at a 5.09% CAGR through 2030. These technologies eliminate wear points, offer better EMI immunity, and provide the redundancy needed for ISO 26262 functional safety compliance in modern drive-by-wire systems.

How are electric vehicles changing sensor requirements?

EVs create challenging environments with high EMI from SiC power inverters and operating temperatures exceeding 170°C. This drives demand for magnetic-core dual-channel sensors with enhanced thermal stability, stray-field immunity up to 4.39 mT, and digital interfaces that support diagnostic communication across multiple control modules.

Which region leads the throttle position sensor market?

Asia-Pacific leads with 42.28% market share in 2024, driven by China's 12.85 million NEV sales and expanding manufacturing across ASEAN countries. Europe follows as the regulatory pacesetter with Euro 7 standards, while the Middle East & Africa region shows the fastest growth at 5.12% CAGR through 2030.

What challenges do sensor manufacturers face?

Key challenges include volatility in automotive-grade ASIC and rare-earth magnet pricing, high ASIL-D validation costs adding 15-25% to development expenses, cybersecurity risks in networked throttle-by-wire systems, and thermal drift issues near SiC power inverters that require specialised compensation algorithms.

How is the aftermarket for throttle position sensors evolving?

The aftermarket is growing at a 5.15% CAGR as vehicle fleets age and electronic throttle systems become ubiquitous. Challenges include transitioning to digital-output sensors requiring specialised programming tools and Euro 7 type-approval rules restricting non-compliant replacement parts from 2026, raising barriers for independent suppliers.

Page last updated on: