Automotive Pressure Sensors Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

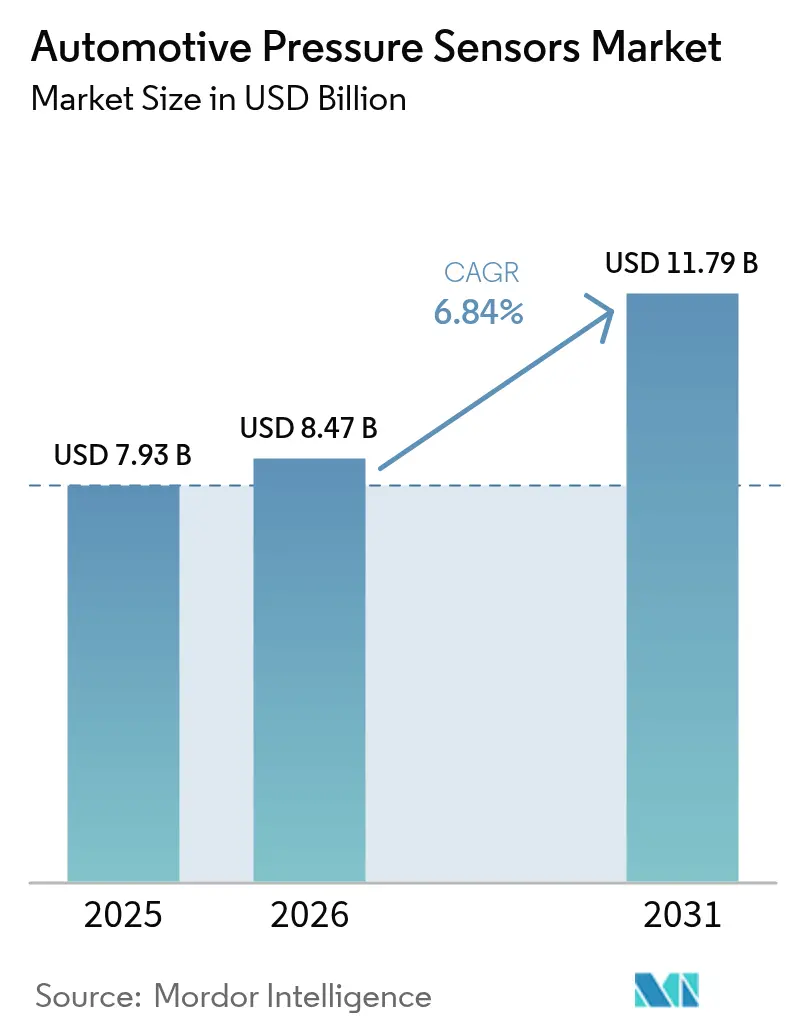

| Market Size (2026) | USD 8.47 Billion |

| Market Size (2031) | USD 11.79 Billion |

| Growth Rate (2026 - 2031) | 6.84% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive Pressure Sensors Market Analysis by Mordor Intelligence

The automotive pressure sensors market size was valued at USD 7.93 billion in 2025 and estimated to grow from USD 8.47 billion in 2026 to reach USD 11.79 billion by 2031, at a CAGR of 6.84% during the forecast period (2026-2031). Robust demand arises as manufacturers replace mechanical gauges with solid-state devices that feed data into software-defined vehicle platforms. Electric propulsion, autonomous-ready brake-by-wire systems, and globally harmonized emission limits each call for more pressure nodes per vehicle, lifting both unit volumes and average sensor value. Asia-Pacific continues to set the pace in production scale and new-energy-vehicle rollouts, while Europe and North America upgrade fleets to comply with the EU General Safety Regulation II that obliges tire pressure monitoring on every new vehicle class [1]European Commission, “General Safety Regulation II,” ec.europa.eu. Meanwhile, suppliers invest in silicon-carbide and capacitive MEMS designs that survive hotter exhaust and lower battery-coolant pressures, expanding the total addressable scope of the automotive pressure sensors market.

Key Report Takeaways

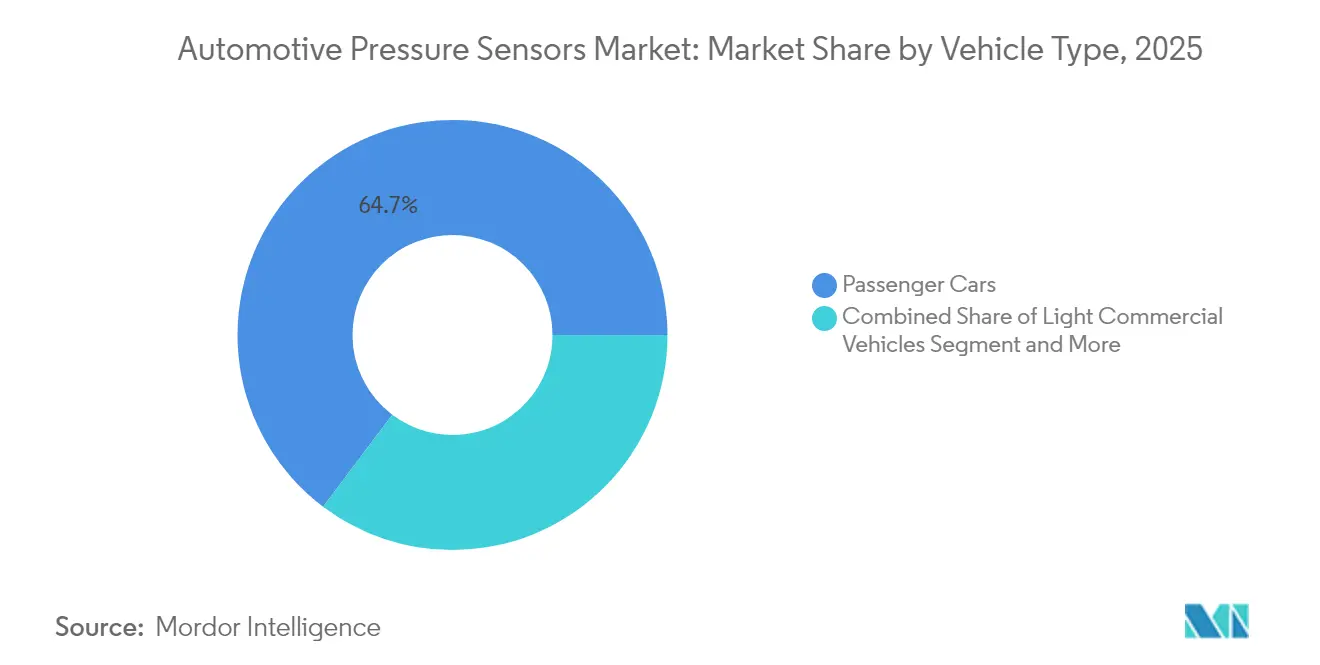

- By vehicle type, passenger cars held 64.72% of the automotive pressure sensors market share in 2025 while advancing at an 7.78% CAGR through 2031.

- By application, tire pressure monitoring systems accounted for 38.90% share of the automotive pressure sensors market size in 2025, whereas exhaust-gas-recirculation sensing is expected to grow at a 10.02% CAGR.

- By pressure type, absolute sensors led with 44.30% revenue share in 2025; gauge sensors are forecast to expand at a 8.72% CAGR to 2031.

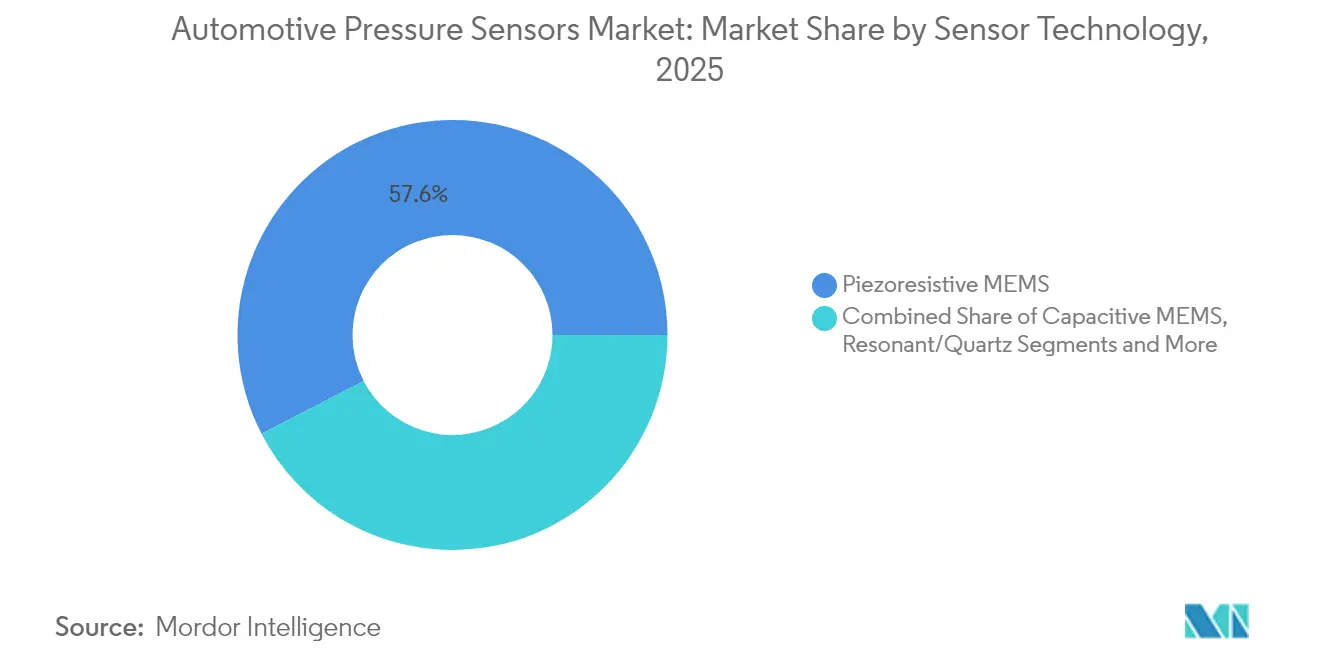

- By sensor technology, piezoresistive MEMS devices captured 57.60% of 2025 revenue, while capacitive MEMS is the fastest-rising class at an 8.38% CAGR.

- By sales channel, OEM-fitted sensors accounted for 87.10% of 2025 revenue, while the aftermarket channel is expected to grow at a 9.74% CAGR.

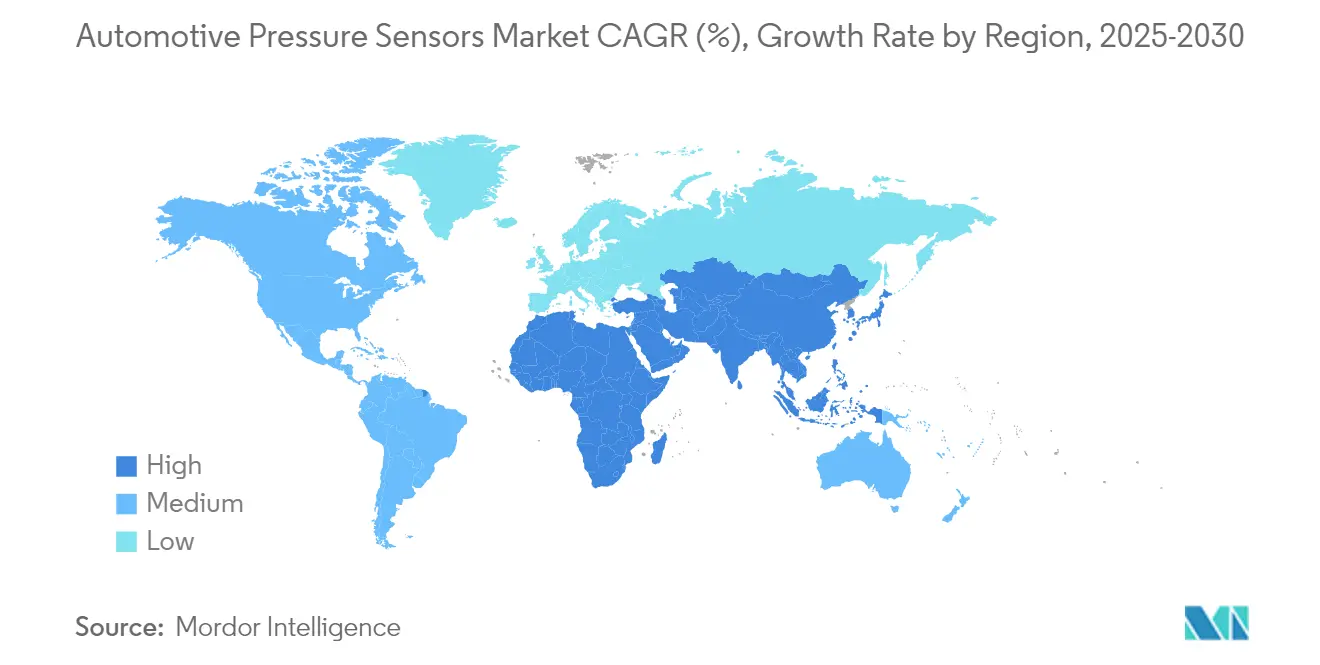

- By geography, Asia-Pacific captured 49.20% of the automotive pressure sensors market share in 2025, and is projected to expand at a 9.21% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Automotive Pressure Sensors Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government Mandates for TPMS Fitment | +1.8% | Europe, North America, expanding globally | Short term (≤ 2 years) |

| Escalating Electrified-Powertrain Production | +1.5% | Asia-Pacific core, spill-over worldwide | Medium term (2-4 years) |

| Rising Integration of ADAS and Autonomous Systems | +1.2% | North America and Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Stricter Global Emission and Fuel-economy Norms | +1.0% | Global, led by EU and China | Long term (≥ 4 years) |

| SiC-based High-temperature Sensors open Exhaust-side Use-cases | +0.8% | Global, early uptake in premium segments | Long term (≥ 4 years) |

| OTA Prognostics Require Self-diagnosing Smart Sensors | +0.7% | North America and Europe, scaling globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Government Mandates for TPMS Fitment

Regulators now treat tire-pressure data as frontline safety information. From July 2024, the EU General Safety Regulation II requires TPMS on every new passenger car, bus, truck, and trailer [2]Continental AG, “TPMS and Safety Innovations,” continental.com. Comparable mandates already exist in the United States, while South American and Southeast Asian governments draft matching rules. OEMs exploit the mandatory wireless backbone to layer tread-wear analytics and cloud alerts, increasing sensor value, and they prefer vendors offering encrypted protocols that pass cybersecurity audits.

Escalating Electrified-Powertrain Production

Battery-electric platforms introduce extra pressure nodes in coolant loops, brake-by-wire circuits, and closed refrigerant systems; accurate feedback prevents thermal runaway and optimizes fast-charge temperature windows. Chinese assemblers embed several low-pressure MEMS dice per module, whereas European premium brands migrate to 800-volt architectures needing stronger electrical isolation. The growing datapoint count enlarges both volume and complexity, rewarding suppliers that marry robust hardware with pack-health algorithms inside the automotive pressure sensors market.

Rising Integration of ADAS and Autonomous Systems

Hands-off highway pilots demand synchronized brake and chassis data that align with camera, radar, and lidar streams. MEMS sensors inside electro-hydraulic actuators feed real-time brake-force signals compliant with ISO 26262 ASIL-D. Level-3 prototypes specify redundant channels, doubling sensor counts. Continuous over-the-air upgrades favor parts preloaded with calibration hooks, generating recurring software revenue for pressure-sensor vendors and strengthening their role in software-defined vehicle ecosystems.

Stricter Global Emission and Fuel-Economy Norms

Euro 7 mandates continuous back-pressure and particulate-filter monitoring from 2025, spurring demand for silicon-carbide MEMS that survive 800 °C exhaust streams. China VI-b and California LEV IV are set to mirror these rules, ensuring worldwide alignment. Because every powertrain—gasoline, diesel, hybrid, or hydrogen—faces tougher real-world verification, high-temperature pressure sensing secures a long-term growth runway for established SiC suppliers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sensor Price-erosion and Margin Pressure | –1.2% | Global, most acute in Asia-Pacific fabs | Short term (≤ 2 years) |

| Semiconductor Supply-Chain Volatility | –0.9% | Global automotive tier suppliers | Medium term (2-4 years) |

| Cyber-risk of TPMS Signal Spoofing | –0.6% | North America and Europe, connected-vehicle markets | Long term (≥ 4 years) |

| Complex Multi-Standard Certification Burden | –0.5% | Global, highest barrier in emerging markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Sensor Price-Erosion and Margin Pressure

Automakers negotiate yearly 2-3% cost reductions on legacy manifold and TPMS gauges, while Southeast Asian contract foundries replicate mature designs, compressing margins. To defend pricing, suppliers bundle diagnostics and predictive-maintenance APIs that create subscription revenue. Nonetheless, relentless cost-down targets demand lean packaging, outsourced test, and aggressive die shrinks, challenging smaller firms and tempering short-term profitability inside the automotive pressure sensors market.

Semiconductor Supply-Chain Volatility

Automotive MEMS (Micro-Electro-Mechanical Systems) production relies on scarce 200 mm capacity, yet foundries prioritize higher-margin smartphone logic, leaving older more than 65 nm analog nodes bottlenecked. Tier-one suppliers hedge with dual sourcing and buffer stock, but earthquakes, power failures, or sanctions still disrupt deliveries. Each missed batch ripples through just-in-time lines, forcing OEM output cuts that can trim quarterly growth for the automotive pressure sensors market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: Passenger Cars Drive Volume Growth

Passenger cars dominate deployments, reflecting both global production scale and the rapid shift toward electric propulsion. In 2025, passenger platforms held 64.72% of the automotive pressure sensors market share and are tracking an 7.78% CAGR to 2031. Adoption accelerates as luxury marques integrate adaptive air suspension, active aerodynamics, and predictive brake servicing. Electric sedans place additional low-pressure nodes in battery chillers and cabin heat pumps, expanding sensor counts per vehicle. Commercial vans and light trucks trail in volume yet attract attention from last-mile delivery fleets that demand load monitoring and regenerative braking optimization. Medium and heavy trucks face EU mandates for TPMS on new approvals, spurring higher-range gauges that thrive in harsher duty cycles. Autonomous freight pilots employ redundant pressure circuits to satisfy fail-operational criteria. Consequently, diversified offerings across vehicle classes allow suppliers to hedge cyclical softness in any single segment, supporting sustainable gains for the automotive pressure sensors market.

Second-tier growth comes from specialized off-highway vehicles where hydraulic workloads and extended duty drive demand for high-proof-pressure diaphragms. Agricultural machinery integrates digital tire inflation control for soil compaction management, while construction equipment adopts real-time hydraulic health tracking. Though unit volumes are modest, ASPs rise because these sensors pack stainless or ceramic cells and sealed connectors. Passenger car leadership therefore coexists with profitable niches in heavy applications, enriching the overall value capture of the automotive pressure sensors industry.

By Application: TPMS Dominance Challenged by Exhaust Monitoring

Tire pressure monitoring systems generated 38.90% of 2025 revenue, cementing their role as the entry point for new regulations. Each light vehicle carries four to six wheel-well sensors, and premium fitments add a fifth spare-wheel unit. Sensor batteries last up to 10 years, creating an annuity-like aftermarket. Yet Euro 7 shifts incremental expenditure toward exhaust gas recirculation, particulate trap, and SCR dosing subsystems that now need continuous pressure feedback. These exhaust modules post the fastest 10.02% CAGR and require high-temperature silicon-carbide dies that command double the ASP of common TPMS units. Brake and ABS pressure sensing remains a steady core, though migration to brake-by-wire introduces finer resolution and redundancy that raise device count. Engine manifold, fuel rail, and turbo boost sensing evolve toward higher accuracy at large pressure swings, keeping legacy demand intact even as electrification proceeds. Across every bandwidth, the automotive pressure sensors market benefits from diversified application pull, with compliance spend fueling near-term spikes and software-enabled health features creating longer-cycle revenue.

Inside the cabin, smart airbag modules employ barometric pressure information to improve occupant classification. Next-generation climate control leverages vapor-compression monitoring to optimize refrigerant charge in heat pumps common to EVs. Ride-control systems embed fast 10 kHz pressure pick-ups to regulate semi-active dampers. As sensor counts expand, multiplexed digital buses replace analog lines, simplifying harness weight and boosting reliability. The widening scope underlines how the automotive pressure sensors market continues to migrate from single-purpose analog gauges to networked digital nodes that feed centralized domain controllers.

By Pressure Type: Absolute Sensors Anchor, Gauge Sensors Accelerate

Absolute pressure cells, tied to a sealed reference vacuum, retained a 44.30% share in 2025 thanks to broad engine management use. They govern fuel vapor recovery, intake manifold dynamics, and barometric compensation in altitude-sensitive calibrations. However, gauge sensors that read relative to ambient now post an 8.72% CAGR, driven by electric-vehicle coolant loops and electro-hydraulic brake systems where atmospheric offset is more relevant. High-differential devices measure pressure drops across particulate filters and EGR coolers; they carry wider dynamic range specifications and robust diaphragms able to survive soot and acid condensates. Low-vacuum units have found new life in electromechanical vacuum pumps for brake assist in battery-electric cars. Such diversity ensures each pressure modality captures a defined performance envelope, supporting balanced expansion of the automotive pressure sensors market.

Hybrid dual-port packages merge absolute and differential measurement in one die, trimming the bill-of-materials for tight engine bays. Suppliers also co-integrate temperature elements, reducing component count in thermal management loops. As vehicle platforms converge on centralized domain architectures, a single digital node issuing multiple pressure frames simplifies software maintenance. This integration thrust elevates the total functional density sent to the automotive pressure sensors market while curbing wiring complexity.

By Sensor Technology: Piezoresistive MEMS Dominance Under Pressure

Piezoresistive MEMS kept 57.60% share in 2025, underpinned by low cost, well-established process controls, and stable drift behavior. Decades of failure-mode data make these devices easy for OEMs to qualify. Yet capacitive MEMS registers an 8.38% CAGR because its moving-plate topology excels at sub-100 kPa readings and uses minimal quiescent current—an advantage in battery-electric packs whose parasitic draw budgets are tight. Capacitive cells also exhibit superior shock resistance, useful in wheel-end TPMS. Resonant-based microstructures appear in high-precision manifold gauges, exploiting frequency shifts for sub-0.1% full-scale accuracy over temperature. Silicon-carbide sensors, originally developed with NASA for extreme aeronautics, now migrate into diesel particulate filters where 600 °C operation is routine. Optical fiber and surface-acoustic-wave approaches stay niche but offer electromagnetic immunity, valuable in high-voltage drive units. The technology stack’s breadth keeps the automotive pressure sensors market open to innovation while preserving a stable baseline in mainstream piezoresistive chips.

Foundries experiment with wafer-level vacuum encapsulation to lock reference cavities during die singulation, slashing trim time. ASIC co-design merges analog front-end, ADC, and SENT or PSI5 interfaces on a single companion die, enabling digital calibration at line speed. These packaging and test economies help suppliers offset price erosion in commoditized segments and defend margins, sustaining investment capacity across the automotive pressure sensors industry.

By Sales Channel: OEM Integration Prevails, Aftermarket Evolves

Original-equipment installation represented 87.10% of 2025 shipments as automakers specify sensors early in platform lifecycles. Tier-one suppliers co-develop modules that meet ASIL, EMC, and functional-safety audits, locking in design wins for 7-year model runs. The aftermarket segment, while smaller, gains momentum and is projected to grow with 9.74% CAGR, as TPMS battery depletion cycles trigger replacement demand and fleets chase up time through predictive maintenance kits. Independent distributors stock programmable multi-protocol sensors able to clone OEM IDs, simplifying service bay logistics. Cyber-secure TPM receivers are entering the replacement channel, tapping concern over radio-frequency spoofing attacks that research groups have publicized. As vehicles age longer than 12 years, lifecycle opportunities expand, giving the automotive pressure sensors market a durable tail of high-margin service parts.

Remanufacturing and core-return programs are emerging for stainless-steel sensors used in heavy diesel exhaust systems. Suppliers refurbish housings and fit new diaphragms, cutting costs and environmental impact. Digital marketplaces integrate sensor diagnostic history with VIN databases, recommending precise part numbers and installation tutorials. Such convenience expands aftermarket penetration, reinforcing the automotive pressure sensors market’s resilience to new-vehicle demand cycles.

Geography Analysis

Asia-Pacific remains the volume engine for the automotive pressure sensors market, leading with 49.20% share in 2025. The region is further projected to grow with a 9.21% CAGR by 2031, as China accelerates electric-vehicle production and embeds multiple low-pressure nodes for battery safety. Local makers benefit from national content mandates that incentivize domestic MEMS sourcing, reducing import reliance. India scales automotive assembly clusters in Gujarat and Tamil Nadu, fostering regional sensor supply chains alongside powertrain electronics. Japan sustains leadership in micro-machining tools, feeding outsourced wafer fabrication for global brands, while South Korea leverages its consumer-electronics fabs to push sensor miniaturization. Government subsidies for smart mobility labs keep regional design cycles short, enhancing competitiveness.

North America combines regulatory pull with technology push. NHTSA rules on TPMS and EPA emission standards ensure baseline demand, while Silicon Valley software stacks accelerate the shift to centralized domains that favor digital pressure protocols. Detroit OEMs localize battery pack assembly and thermal management integration, increasing domestic sensor content. Canada’s heavy-truck sector adopts high-accuracy tire inflation control for fuel-efficiency gains, extending sensor use into vocational applications. Mexico’s Tier-2 ecosystem supplies molded housings and lead frame stampings, supporting regional cost optimization across the automotive pressure sensors market.

Europe’s policy landscape is the most stringent. Euro 7 legislation forces real-time exhaust monitoring, driving uptake of SiC high-temperature sensors . The General Safety Regulation obliges TPMS on every vehicle class, elevating sensor density in trailers and coaches. Germany’s premium OEMs specify dual-redundant brake pressure modules for Level-3 autonomous approval. France and Italy channel recovery funds into electric-bus projects that integrate advanced battery coolant sensing. Eastern European plants attract new MEMS packaging investments, exploiting competitive labor while staying inside the common market. Altogether, synchronized regulations and sophisticated end-users stabilize long-run demand across the automotive pressure sensors market.

Regulatory Landscape

Safety and emissions rules continue to hard-code pressure sensing into vehicle type-approval and compliance testing. In the European Union, the General Safety Regulation (EU) 2019/2144 expands mandated safety content across vehicle classes, reinforcing TPMS fitment and related diagnostics as a baseline requirement from the July 2024 implementation window highlighted in the report context. In the United States, NHTSA enforces TPMS requirements through FMVSS 138 (49 CFR 571.138), keeping TPMS as a durable, regulated application pull for OEM and replacement demand.

Beyond vehicle-level regulations, suppliers also qualify devices and processes to automotive electronics standards that OEMs and Tier-1s commonly require for sourcing. AEC-Q103-002 is used to qualify MEMS sensor devices via failure-mechanism-based stress tests, and China has a dedicated automotive pressure sensor standard in QC/T 822-2024 covering requirements, test methods, and inspection rules across engine, braking, and urea-system use cases. For specialized applications, ISO standards such as ISO 20766-21:2023 (pressure and temperature sensors for LPG systems) and ISO 15638-23:2025 (data communication frameworks for commercial-vehicle tyre pressure monitoring) add additional compliance layers that affect design documentation, validation scope, and multi-region certification workloads.

Value Chain Analysis

The value chain runs from MEMS wafer fabrication and companion analog or mixed-signal IC supply through packaging, calibration or trim, module integration, and then Tier-1 delivery into OEM platforms, with a smaller but growing service pathway into the aftermarket. Upstream, pressure sensors depend on mature-node semiconductor capacity and specialized MEMS processes (deep silicon etching, wafer bonding, and wafer-level packaging). Downstream value concentrates in calibration capability, functional-safety diagnostics integration, and RF or security features for TPMS modules. Major Tier-1s such as Bosch, Continental, and DENSO sit at the center of integration, often combining MEMS die, ASICs, and firmware into application-specific assemblies delivered under long platform-cycle contracts.

Supply risk concentrates around constrained automotive-grade chip availability and long re-qualification timelines that make rapid second-sourcing difficult once a module is frozen. Reuters coverage in 2025 highlighted renewed automotive semiconductor supply-chain disruption tied to export restrictions affecting standard automotive chips, underscoring vulnerability for pressure-sensor modules that rely on discrete semiconductors and qualified components with lengthy change-control. To reduce disruption exposure, suppliers emphasize dual sourcing where possible, shift more steps into controlled internal lines (or tightly governed contract manufacturing), and add regional manufacturing footprints, while still relying on globally distributed equipment and materials ecosystems for MEMS processing and test.

Competitive Landscape

Industry structure is moderately concentrated, with several key suppliers controlling a dominant position in the market. Sensata Technologies derived sales from automotive sensing, pairing piezoresistive dies with ASICs for hybrid powertrains. Continental integrates TPMS transceivers into its domain controller, selling a bundled platform that shortens OEM validation cycles. Bosch unveiled its Bluetooth-enabled SMP290 MEMS wheel sensor in June 2025, extending design life to 10 years while sharing the RF module with passive-entry networks. Each front-runner invests in in-house software stacks, enabling over-the-air calibration and prognostics that attract fleet customers.

Mid-tier challengers focus on SiC exhaust sensing or capacitive EV-thermal nodes where incumbents own fewer patents. Chinese specialist Trensor recently revealed plans to open a Malaysian plant to diversify risk and shorten lead times for ASEAN assembly lines. European fab-light players license wafer processes from research institutes, leveraging public grants for pilot production. The growing emphasis on functional safety pushes collaborative development; NOVOSENSE and Continental teamed up in October 2024 to co-engineer ASIL-D-qualified pressure ASICs. Cybersecurity compliance creates openings for software vendors that encrypt RF payloads, a niche traditional component houses rarely address. Such cross-domain collaboration keeps the automotive pressure sensors market dynamic and innovation-rich.

Forward-looking strategies include glass-frit wafer bonding to cut package count, additive manufacturing of ceramic diaphragms for harsh media, and on-sensor machine-learning engines that flag drift before it breaches calibration limits. Patent filings cluster around wafer-level hermeticity and high-voltage isolation for 1,000-V battery packs. Mergers remain selective as boards weigh geopolitical risk and fab capital intensity. Overall, solid profit pools support sustained R&D, enabling the automotive pressure sensors market to meet upcoming safety and sustainability milestones.

Automotive Pressure Sensors Industry Leaders

DENSO Corporation

Robert Bosch GmbH

Infineon Technologies AG

Sensata Technologies, Inc.

Continental AG

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Electrified powertrains and software-defined vehicle architectures widen the addressable scope for pressure sensing beyond traditional manifold and TPMS nodes. Key whitespace is in battery safety, thermal management, and digitally networked sensing. A concrete in-scope product example is Infineon’s XENSIV KP467 digital absolute pressure sensor positioned for battery management systems to monitor pressure pulses associated with thermal runaway events, aligning pressure sensing with battery safety requirements and higher-value sensing use cases. This supports opportunities for suppliers that can combine robust low-pressure accuracy, functional safety diagnostics, and digital interfaces that reduce harness complexity while fitting centralized compute architectures.

Regulation-driven content expansion and standardization activity also reinforce the need for compliant, interoperable sensor and data frameworks that vendors can productize across platforms. In Europe, evolving type-approval and on-board monitoring requirements (for example, Commission Implementing Regulation (EU) 2025/1707 cited in the evidence pack) keep OEM focus on measurable, diagnosable performance across powertrain and safety functions, which increases demand for sensors with self-test and traceability. On the technology side, production-maturing approaches such as ASIC-on-MEMS integration, gel-free encapsulation, and digitally native outputs create room for platform solutions that scale across TPMS, brake-by-wire hydraulics, EV coolant loops, and exhaust aftertreatment sensing. Suppliers that simplify multi-standard certification and cybersecurity validation can shorten OEM qualification cycles and secure broader design-in coverage.

Recent Industry Developments

- March 2026: Infineon Technologies AG updated the KP467 XENSIV digital absolute pressure sensor documentation (datasheet revision 1.20). Positioning the device for battery management systems to detect pressure pulses associated with thermal runaway links pressure sensing more directly to EV safety architectures and higher-value sensing nodes.

- June 2025: Robert Bosch GmbH unveiled the SMP290, a Bluetooth-enabled MEMS tire pressure sensor with dual-axis acceleration sensing and a 10-year design life. The move supports OEM and service-channel adoption of standardized wireless connectivity while strengthening Bosch’s TPMS portfolio for regulated fitment markets.

- October 2024: NOVOSENSE and Continental formed a strategic alliance to co-develop automotive-grade pressure sensor chips with functional-safety diagnostics. This collaboration targets ASIL-oriented design requirements in brake and chassis applications, reinforcing the trend toward integrated diagnostics and safety-qualified sensor ASICs.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market counts the revenue earned from pressure sensors installed in motor vehicles to measure gas or fluid pressure and feed signals into vehicle control and safety systems. Coverage includes both OEM fitment and aftermarket replacement, reported at a global level.

Scope exclusions: Standalone mechanical gauges and general industrial pressure sensors that are not designed and qualified for automotive use are excluded.

Segmentation Overview

- By Vehicle Type

- Passenger Cars

- Light Commercial Vehicles

- Medium and Heavy Commercial Vehicles

- By Application

- Tire Pressure Monitoring System (TPMS)

- Brake Booster and ABS

- Engine and Fuel/Manifold Management

- Exhaust Gas Recirculation/After-treatment

- Airbag and Safety Restraint Systems

- Vehicle Dynamics and ESC

- By Pressure Type

- Absolute

- Gauge (Sealed/Vent)

- Differential

- Vacuum/Low-pressure

- By Sensor Technology

- Piezoresistive MEMS

- Capacitive MEMS

- Resonant/Quartz

- Opto-electronic and Others

- By Sales Channel

- OEM-Fitted

- Aftermarket

- By Geography

- North America

- United States

- Canada

- Rest of North America

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- United Arab Emirates

- Saudi Arabia

- Egypt

- South Africa

- Rest of Middle East and Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build a demand view and to reduce double counting across vehicle systems that use multiple sensors. We referenced public vehicle production and sales statistics and parc indicators from sources such as OICA, national transport agencies, and customs and trade databases that publish import and export totals for relevant sensor categories.

On the supply side, we reviewed public information such as company annual reports, investor presentations, earnings transcripts, and product catalogs to understand typical sensor use cases and replacement behavior. We also used paid database subscriptions for company financials and intelligence, along with patent databases, to track technology shifts (for example MEMS adoption) that can change average selling prices over time. These desk sources are not exhaustive, and many other public references were checked to collect, validate, and clarify inputs.

Primary Interviews and Surveys

Primary interviews and surveys were run with a mix of component suppliers, vehicle OEM ecosystem participants, and service and distribution contacts to confirm sensor content per vehicle and pricing direction by application. Because this is a global market, inputs were balanced across APAC, EMEA, and the Americas so the regional platform mix, regulation-led adoption (such as TPMS), and aftermarket dynamics could be reflected in the final model.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 37% | CXOs: 19% | APAC: 45% |

| Mid tier: 43% | Functional/Unit leaders: 29% | EMEA: 31% |

| Smaller Players: 20% | Managers: 52% | Americas: 24% |

Market-Sizing & Forecasting

Sizing starts from a top-down demand pool rebuilt from vehicle production and parc signals. Sensor demand is then derived using average sensor content per vehicle across key systems like TPMS, engine management, braking assist, EGR, airbags, and vehicle dynamics. To keep the model practical, a limited set of inputs is tracked each year, including global light and heavy vehicle output, regional powertrain mix (ICE versus alternative fuel), TPMS penetration by platform, average sensors per vehicle by application, and average selling price movement tied to MEMS technology and signal accuracy requirements.

Those totals are checked with selective bottom-up approximations. Sampled shipment and revenue disclosures, channel checks, and price band discussions from interviews help correct any overstatement in high-growth applications. Where direct data is missing for smaller applications or countries, gaps are handled using proxy relationships, such as vehicle output shares and application-level penetration ranges validated by respondents. For forecasting, scenario analysis is used around vehicle production, electrification pace, and regulation-led penetration changes, and the final trajectory is selected only after the assumptions are agreed as realistic by primary inputs.

Data Validation & Update Cycle

Outputs are cross-checked against independent signals such as vehicle production trends, sensor penetration patterns, and the direction of OEM and aftermarket pricing. If a region or application shows an unusual jump, assumptions are reopened and follow-up calls are triggered to confirm whether the change reflects a real shift or a modeling artifact.

Before sign-off, the model goes through multi-step analyst reviews that include variance checks across regions and a final consistency pass across historic and forecast years. Reports are refreshed annually, and interim updates are made when material events affect vehicle production, regulation timelines, or pricing, followed by a last review right before delivery so clients receive the latest view.

Mordor Intelligence's Global Automobile Pressure Sensors Market Market Sizing Compared With Other Published Estimates

Different publications can show different market sizes even when they use similar words, because underlying scope and year alignment are not always the same. The biggest differences usually come from what gets counted as an automotive pressure sensor, how OEM versus aftermarket is treated, and whether price assumptions reflect current mix shifts across applications.

Mechanical pressure gauges and other non-electronic pressure measuring parts sit outside Mordor Intelligence's scope. That is one reason some public figures can look higher or lower when they mix adjacent hardware or use broader sensor buckets. Gaps also show up when one estimate anchors on 2024 pricing with aggressive ASP escalation, while another uses a calmer price curve linked to MEMS cost-down and a different split of TPMS versus powertrain demand.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 7.93 B (2025) | |

| Regional Consultancy A | USD 6.80 B (2024) | Uses an earlier base year and does not clearly state whether aftermarket replacement and full application coverage are included, which can undercount regions with higher in-service demand. |

| Trade Journal B | USD 8.30 B (2024) | A broader 2024 value is paired with a higher-growth outlook and limited disclosure on how ASP progression and technology mix are modeled, which can inflate totals when TPMS and powertrain sensors are priced too aggressively. |

The spread in the table mostly tracks year alignment and what gets bundled into the definition, followed by differences in pricing and mix assumptions. By tying demand to vehicle output and application penetration first, then pressure-testing prices and replacement patterns through interviews, the final value stays traceable to clear inputs and repeatable checks.

Key Questions Answered in the Report

What is the current size of the automotive pressure sensors market?

The automotive pressure sensors market size stands at USD 8.47 billion in 2026 and is forecast to reach USD 11.79 billion by 2031.

Which application segment is growing the fastest?

Exhaust-gas-recirculation and aftertreatment pressure sensing leads growth with a projected 10.02% CAGR through 2031 as Euro 7 rules demand continuous exhaust monitoring.

Why are capacitive MEMS sensors gaining popularity in electric vehicles?

Capacitive MEMS offer higher sensitivity at low absolute pressures and lower standby current, making them ideal for EV battery-coolant loops and braking systems.

How do new regulations influence demand for pressure sensors?

Mandatory TPMS fitment across all vehicle classes and Euro 7 exhaust requirements each add multiple new sensor points per vehicle, driving sustained market growth.

Page last updated on: