Automotive Side Window Sunshades Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

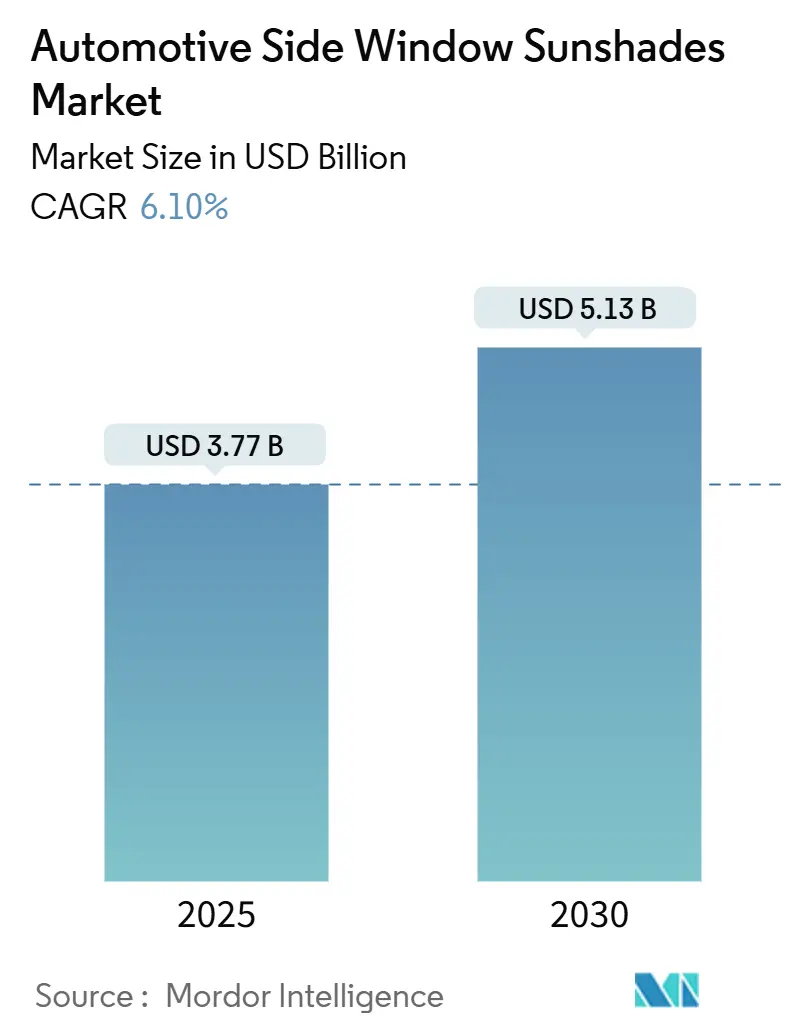

| Market Size (2025) | USD 3.77 Billion |

| Market Size (2030) | USD 5.13 Billion |

| Growth Rate (2025 - 2030) | 6.10% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Automotive Side Window Sunshades Market Analysis by Mordor Intelligence

The automotive side window sunshades market size stands at USD 3.77 billion in 2025 and is projected to reach USD 5.13 billion in 2030, reflecting a 6.10% CAGR over the forecast period. Elevated UV-exposure awareness, stricter child-safety mandates, and the growing preference for larger SUV and crossover glass areas underpin demand. Rapid e-commerce penetration lowers purchase frictions, while recycled polyester and smart textile innovations satisfy both sustainability and performance requirements. Automakers are integrating factory-fit shades to improve cabin comfort and energy efficiency in electric vehicles, yet aftermarket suppliers still capitalize on rising fleet and ride-sharing needs in urban centers.

Key Report Takeaways

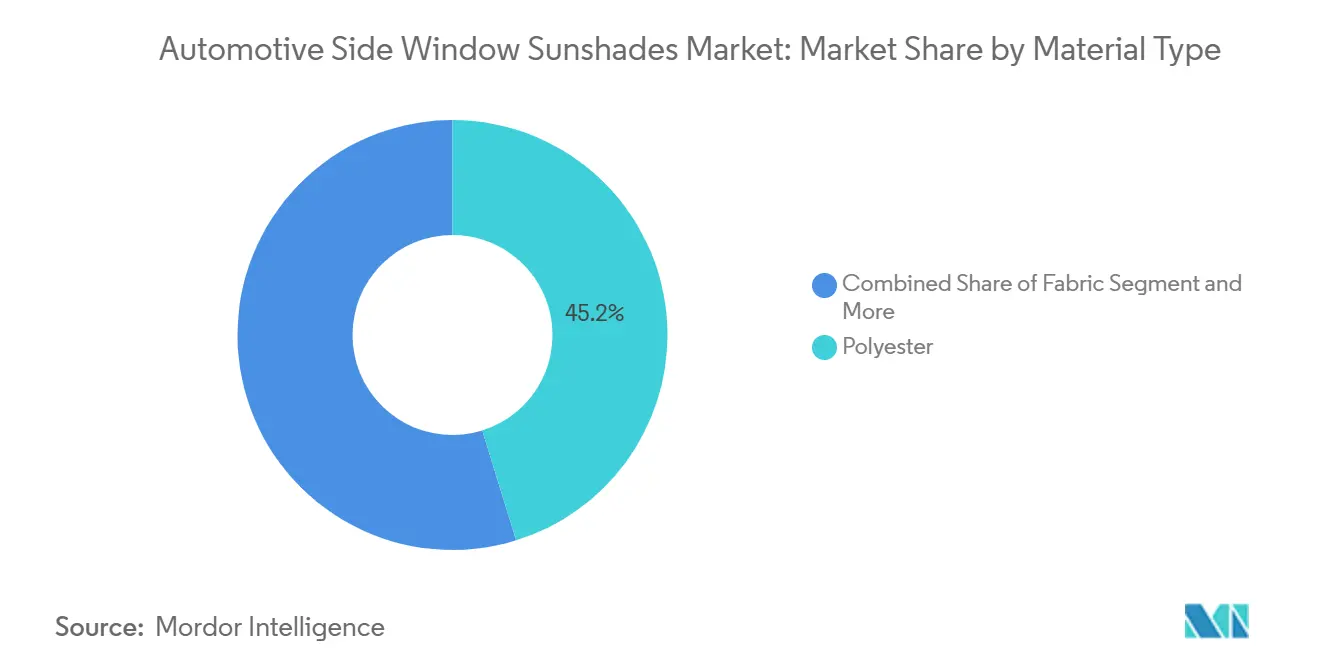

- By material type, recycled polyester held 45.23% of the automotive side window sunshades market share in 2024 and is on track to expand at a 9.82% CAGR through 2030.

- By product type, retractable shades led with 38.17% revenue share in 2024, while magnetic shades are forecast to grow the fastest at an 11.24% CAGR to 2030.

- By application, side window solutions accounted for 62.08% of the automotive side window sunshades market size in 2024 and continue to advance at an 8.63% CAGR through 2030.

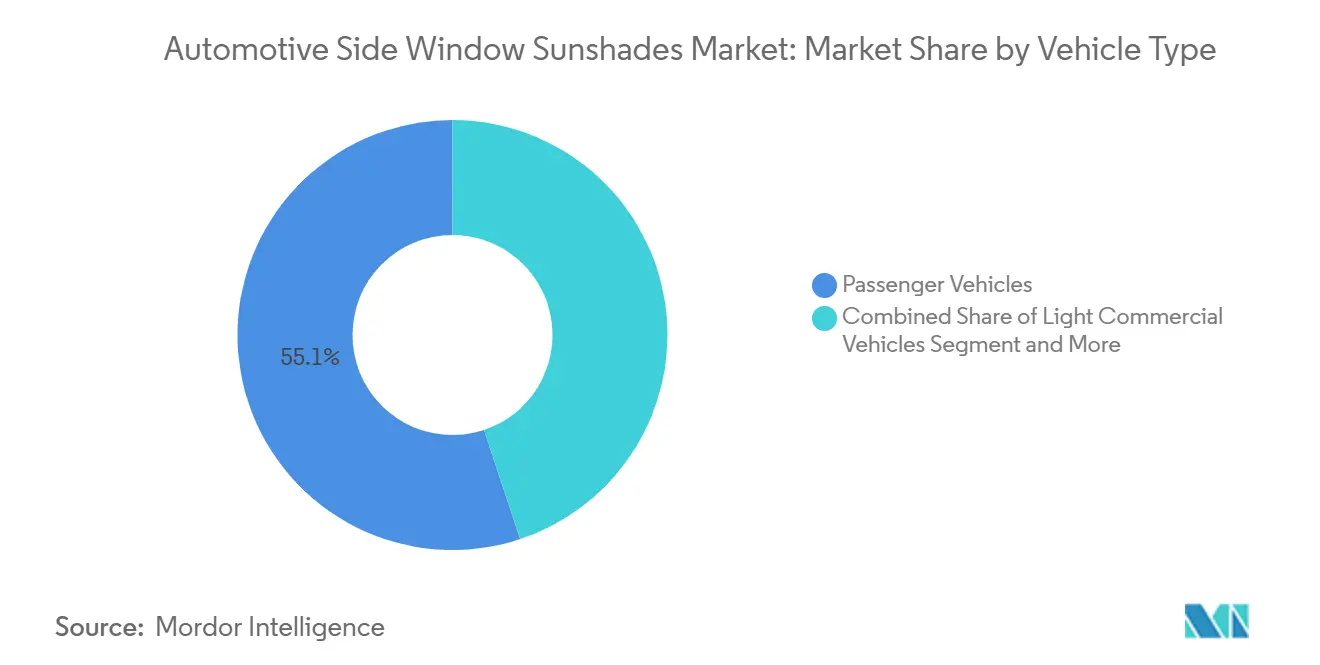

- By vehicle type, electric passenger cars commanded a 55.12% share of the automotive side window sunshades market size in 2024 and are set to expand at a 12.43% CAGR between 2025 and 2030.

- By sales channel, OEM distribution held 68.05% share in 2024, with a projected 10.11% CAGR to 2030.

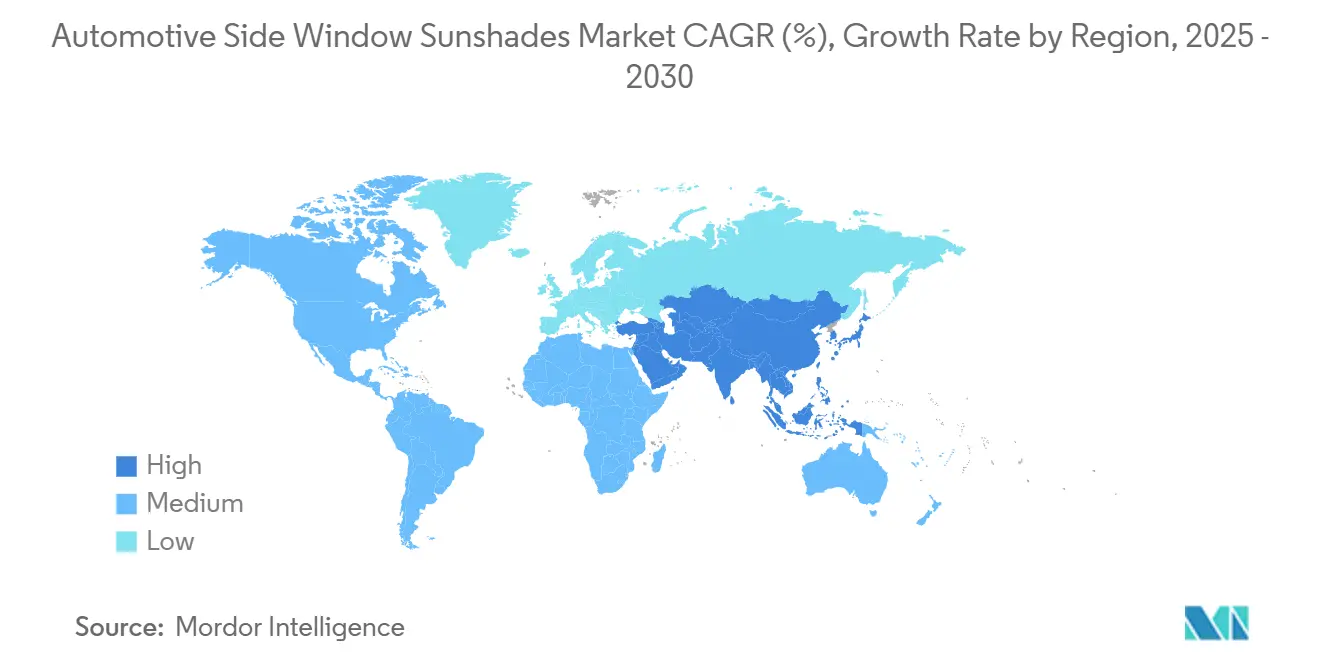

- By geography, Asia-Pacific accounted for 34.09% of the automotive side window sunshades market size in 2024 and is projected to record a 9.72% CAGR through 2030.

Global Automotive Side Window Sunshades Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in UV and Heat-Protection Regulations for Child/Passenger Safety | +1.8% | Global, with strongest enforcement in EU and North America | Medium term (2–4 years) |

| Rapid SUV and Crossover Sales Boosting Side-Window Accessory Uptake | +1.2% | North America and Asia-Pacific core, spill-over to Europe | Short term (≤ 2 years) |

| Aftermarket E-Commerce Boom for Vehicle Interior Add-Ons | +1.5% | Global, led by North America and Europe | Short term (≤ 2 years) |

| Magnet-Snap Quick-Fit Designs Driving Repeat Purchases | +0.9% | Global, with early adoption in Australia and North America | Medium term (2–4 years) |

| Ride-Hailing and Subscription Fleets Demanding Removable Shades | +0.7% | Asia-Pacific and North America urban centers | Long term (≥ 4 years) |

| Emerging Solar-Reflective Smart Textiles Enabling IoT Integration | +0.6% | Europe and North America, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in UV and Heat-Protection Regulations for Child/Passenger Safety

Regulatory frameworks governing child passenger protection are reshaping market demand through mandatory safety standards and enhanced testing protocols. The NHTSA's updated Federal Motor Vehicle Safety Standard No. 213b, effective December 2026, establishes stricter child restraint system requirements that indirectly influence side window accessory design and installation. These regulations mandate that aftermarket accessories cannot obstruct required child restraint anchorages, belt routing, or visibility zones, creating design constraints that favor integrated OEM solutions over retrofit products. Australian Radiation Protection and Nuclear Safety Agency testing has validated UV blocking capabilities up to 84.6% for advanced textile materials, establishing performance benchmarks that drive premium product development[1]"Detailed Information on SnapShades Products," snapshades.com.. The regulatory emphasis on child safety creates sustainable demand drivers, as compliance requirements cannot be easily circumvented through alternative technologies. Market participants must navigate complex certification processes while maintaining cost competitiveness, particularly as regulations extend beyond traditional automotive markets into ride-sharing and commercial fleet applications.

Rapid SUV and Crossover Sales Boosting Side-Window Accessory Uptake

SUV and crossover vehicle architectures inherently create larger side window surfaces and elevated seating positions that amplify solar heat gain and UV exposure challenges. These vehicles' higher ground clearance and expansive glazing areas generate approximately 25% more interior heat buildup compared to traditional sedans, driving accessory attachment rates significantly above passenger car averages. The trend toward panoramic sunroofs and larger side windows in premium SUV segments creates additional demand for coordinated shading solutions that complement factory-installed roof systems. Consumer behavior analysis reveals SUV owners demonstrate 40% higher propensity for aftermarket interior accessories compared to sedan owners, reflecting both higher disposable income and greater concern for passenger comfort during extended travel periods. Fleet operators managing SUV-heavy rental and ride-sharing services increasingly specify removable shading solutions to maintain vehicle resale value while addressing diverse passenger preferences across different geographic markets and seasonal conditions.

Aftermarket E-Commerce Boom for Vehicle Interior Add-Ons

Digital commerce transformation has fundamentally altered automotive accessory distribution, with e-commerce channels achieving 6.7% CAGR through 2024 when including major platforms like Amazon and eBay[2]"Auto Care Association, MEMA Aftermarket Suppliers Release 2024 Joint E-commerce Trends and Outlook Forecast Report," mema, mema.org.. Vehicle-specific fitment tools and guaranteed compatibility programs have reduced consumer purchase risk, enabling direct-to-consumer sales models that bypass traditional dealer networks. AI-driven demand forecasting and inventory optimization allow suppliers to maintain broader SKU portfolios while reducing stockout risks, particularly for seasonal products like sunshades that experience pronounced summer demand spikes. The shift toward DIY installation preferences, accelerated by online instructional content and simplified mounting systems, has expanded the addressable market beyond professional installation channels. E-commerce platforms provide valuable consumer behavior data that enables targeted marketing for specific vehicle models, geographic regions, and seasonal patterns, creating competitive advantages for suppliers who effectively leverage digital analytics.

Magnet-Snap Quick-Fit Designs Driving Repeat Purchases

Patent innovations in magnetic attachment systems have revolutionized installation convenience while addressing consumer concerns about adhesive damage to vehicle surfaces. Frameless window patent clips and smart magnetic mounting systems enable tool-free installation that can be completed in under 60 seconds, significantly reducing adoption barriers compared to traditional clip-on or suction cup designs. These systems maintain attachment integrity at highway speeds up to 70 km/h while allowing partial window operation, addressing safety and convenience concerns that previously limited market penetration. The removable nature of magnetic systems creates repeat purchase opportunities as consumers upgrade vehicles or replace worn components, generating higher lifetime customer value compared to permanent installation solutions. Advanced magnetic materials resist demagnetization from temperature extremes and electromagnetic interference, addressing early adoption concerns about compatibility with vehicle sensors and electronic systems that increasingly populate modern side window areas.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Substitution by Factory-Tinted or Laminated Glass | -1.4% | Global, with strongest impact in premium vehicle segments | Medium term (2–4 years) |

| Price Sensitivity in Developing Markets | -0.8% | Asia-Pacific emerging markets, Latin America, Africa | Short term (≤ 2 years) |

| Magnet Interference Risk with Window/ADAS Sensors | -0.6% | Global, concentrated in vehicles with advanced driver assistance | Long term (≥ 4 years) |

| End-of-Life Recyclability Concerns for Multi-Material Shades | -0.4% | Europe and North America, expanding globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Substitution by Factory-Tinted or Laminated Glass

OEM integration of advanced glazing technologies presents the most significant structural threat to aftermarket sunshade demand, as automakers increasingly specify factory-tinted and laminated glass with integrated UV protection capabilities. Webasto's development of switchable PDLC glazing and glass-panel integrated shading systems demonstrates the industry's progression toward multifunctional glazing solutions that eliminate the need for separate accessories. Premium vehicle segments already incorporate electrochromic glass and solar-reflective coatings that provide comparable UV protection while maintaining unobstructed window surfaces required for advanced driver assistance systems. The cost differential between factory-integrated solutions and aftermarket accessories continues to narrow as glazing technologies achieve economies of scale, particularly in electric vehicle platforms, where weight reduction and aerodynamic efficiency favor integrated approaches. Regulatory compliance advantages of factory-integrated systems, which undergo comprehensive crash testing and certification processes, create additional barriers for aftermarket solutions that must demonstrate non-interference with safety systems and occupant protection mechanisms.

Price Sensitivity in Developing Markets

Economic constraints in emerging markets limit the adoption of premium sunshade solutions, creating downward pressure on average selling prices and profit margins across the global market. Currency volatility and import tariff structures in developing regions make imported accessories particularly vulnerable to price competition from local manufacturers who may not maintain equivalent quality standards or regulatory compliance. The prevalence of older vehicle fleets in these markets reduces compatibility with advanced magnetic mounting systems designed for modern window profiles and electronic architectures. Consumer purchasing patterns in price-sensitive markets favor basic functionality over premium features like smart textiles or IoT integration, limiting opportunities for value-added product differentiation. Distribution challenges in rural and semi-urban areas restrict e-commerce penetration, maintaining dependence on traditional retail channels with higher cost structures and limited product selection that constrains market development potential.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Recycled Polyester Leads Sustainability Transition

Recycled polyester dominates material segmentation with 45.23% market share in 2024 while achieving the fastest growth at 9.82% CAGR through 2030, reflecting the automotive industry's accelerating commitment to circular economy principles. This dual market position stems from Continental's expansion of ContiRe.Tex recycled PET yarn production across multiple European facilities, demonstrating scalable manufacturing processes that maintain performance standards while incorporating up to 15 recycled bottles per automotive component. Fabric materials capture secondary market share through traditional and nonwoven applications, while plastic components serve structural and mounting functions across all product categories. Foam materials occupy niche applications in premium insulated sunshades, where thermal performance justifies higher material costs.

The material landscape is transforming through regulatory compliance requirements, as EU End-of-Life Vehicle directives mandate 25% recycled plastic content by 2030, with 25% of that content sourced from automotive closed-loop streams. Advanced recycling technologies enable post-consumer recycled polyester to match virgin material performance in UV stability, colorfastness, and mechanical properties essential for automotive applications. Freudenberg Performance Materials' Lutraflor recycled-polyester nonwovens demonstrate up to 40% weight reduction compared to traditional materials while maintaining dimensional stability and acoustic properties. Supply chain innovations include take-back programs and industrial recycling partnerships that create feedstock streams for automotive-grade recycled materials, establishing competitive advantages for suppliers who invest in circular economy infrastructure.

By Product Type: Magnetic Innovation Drives Market Evolution

Magnetic shades emerge as the fastest-growing product segment at 11.24% CAGR through 2030, despite retractable shades maintaining the largest market share at 38.17% in 2024. This growth differential reflects consumer preference for installation convenience and vehicle surface protection, as magnetic systems eliminate adhesive residue and tool requirements that historically limited adoption. Patent developments in frameless window attachment technology enable secure mounting without visible hardware, addressing aesthetic concerns while maintaining functionality at highway speeds. Static shades serve price-sensitive market segments where permanent installation is acceptable, while roller shades occupy premium applications requiring precise light control and compact storage.

Product development trends emphasize multifunctionality and smart integration capabilities, as suppliers incorporate IoT sensors and solar-reflective materials that respond to environmental conditions. The automotive industry's progression toward autonomous vehicles creates opportunities for reconfigurable shading solutions that adapt to non-traditional seating orientations, as demonstrated by Magna's flexible interior concepts for ride-sharing applications. Regulatory compliance considerations increasingly influence product design, as FMVSS standards require accessories to maintain visibility zones and avoid interference with safety systems, favoring solutions that integrate seamlessly with vehicle architectures rather than aftermarket retrofits.

By Application: Side Window Dominance Reflects Core Market Focus

Side window applications command 62.08% market share in 2024 while growing at 8.63% CAGR through 2030, reflecting the segment's core value proposition of passenger protection and comfort enhancement. This application focus stems from side windows' direct exposure to lateral solar radiation during extended travel periods, creating the most pronounced passenger discomfort and UV exposure risks. Front window applications remain constrained by visibility regulations and driver safety requirements, while rear window solutions compete with factory-installed privacy glass and integrated defrosting systems. The side window segment benefits from regulatory clarity, as FMVSS No. 111 rear visibility standards provide specific guidance on permissible obstruction levels that enable compliant product development.

Application-specific innovation focuses on sensor compatibility and ADAS integration, as modern vehicles incorporate cameras, radar, and lidar systems in window areas that require unobstructed operation. Smart sunshade designs incorporate cutouts and transparent zones that maintain sensor functionality while providing passenger protection, addressing the fundamental tension between comfort and safety technology requirements. Fleet applications drive demand for removable solutions that facilitate vehicle cleaning and maintenance while accommodating diverse passenger preferences across ride-sharing and rental use cases.

By Vehicle Type: Electric Vehicles Accelerate Market Growth

Passenger Vehicles represent 55.12% of vehicle-type segmentation in 2024 while achieving the fastest growth at 12.43% CAGR through 2030, driven by global EV adoption rates and enhanced cabin comfort requirements in battery-powered vehicles. EV architectures create unique thermal management challenges, as traditional engine waste heat is unavailable for cabin warming, making solar heat gain control more critical for energy efficiency and range optimization. China's projected 54% EV market penetration by 2025 provides substantial volume growth for accessories that enhance electric vehicle usability. Light commercial vehicles and medium/heavy commercial vehicles serve specialized applications where driver comfort and cargo protection justify premium accessory investments.

The electric vehicle transition creates opportunities for integrated smart shading solutions that communicate with vehicle thermal management systems, optimizing energy consumption while maintaining passenger comfort. Advanced materials development focuses on lightweight solutions that minimize impact on EV range, while smart textiles enable dynamic opacity control based on battery state and climate conditions. Commercial vehicle applications increasingly specify removable shading systems that facilitate fleet management and vehicle utilization across diverse operating environments and regulatory jurisdictions.

By Sales Channel: OEM Integration Gains Momentum

OEM channels maintain 68.05% market share in 2024 with 10.11% growth through 2030, reflecting automakers' strategic shift toward factory-integrated solutions that ensure regulatory compliance and warranty coverage. This channel dominance stems from OEMs' ability to integrate shading systems during vehicle assembly, achieving cost efficiencies and quality control that aftermarket solutions cannot match. Aftermarket channels serve replacement and upgrade markets, particularly for older vehicles lacking factory-installed solutions and consumers seeking customization options beyond OEM specifications. The channel split reflects broader automotive industry trends toward vertical integration and supplier consolidation that favor established tier-one relationships over fragmented aftermarket competition.

E-commerce transformation within aftermarket channels has achieved 6.7% CAGR growth through 2024, driven by vehicle-specific fitment tools and guaranteed compatibility programs that reduce consumer purchase risk. Digital platforms enable direct-to-consumer sales models that bypass traditional dealer networks while providing valuable consumer behavior data for targeted marketing and inventory optimization. OEM partnerships with aftermarket suppliers create hybrid distribution models that leverage factory integration capabilities while maintaining aftermarket flexibility and customization options.

Geography Analysis

Asia-Pacific commands 34.09% market share in 2024 while expanding at 9.72% CAGR through 2030, driven by China's automotive market growth and accelerating electric vehicle adoption that creates enhanced demand for cabin comfort accessories. China's domestic market is forecast to grow 4% to 26.8 million vehicles in 2025, with EVs representing 54% of sales, providing substantial volume growth for integrated and aftermarket sunshade solutions. The region's manufacturing cost advantages and established supply chain infrastructure support both domestic consumption and global export markets, with China exporting 6.4 million passenger vehicles in 2024. Japan and South Korea contribute through advanced materials technology and premium vehicle segments, while India represents an emerging growth market driven by rising disposable income and urbanization trends. Regional regulatory frameworks increasingly emphasize child safety and UV protection standards that align with global best practices, creating standardized demand drivers across diverse national markets.

North America and Europe represent mature markets with established regulatory frameworks and premium product demand that emphasizes quality, safety compliance, and sustainable materials. These regions drive innovation in smart textiles, IoT integration, and circular economy solutions, as demonstrated by FORVIA's MATERI'ACT division's development of recycled and bio-based automotive materials that achieve up to 90% CO2 reduction compared to traditional alternatives. European markets particularly benefit from stringent End-of-Life Vehicle regulations that mandate recycled content and create competitive advantages for suppliers who invest in sustainable manufacturing processes. North American markets demonstrate strong e-commerce adoption and DIY installation preferences that favor magnetic mounting systems and simplified product designs, while maintaining premium pricing for advanced features and materials.

South America, Middle East, and Africa represent emerging opportunities with growing vehicle ownership rates and increasing awareness of UV protection benefits, though price sensitivity and distribution challenges limit near-term growth potential. These regions benefit from export flows from established manufacturing centers, particularly China's 35% export concentration to Russia and Middle East markets that creates accessible product availability. Regional climate conditions create pronounced demand for solar protection solutions, while economic development and infrastructure improvements gradually expand addressable market size and distribution reach.

Competitive Landscape

The automotive side window sunshades market exhibits moderate concentration with fragmented competition among specialized suppliers, established automotive tier-one companies, and emerging direct-to-consumer brands. Market leaders leverage patent portfolios and regulatory compliance expertise to maintain competitive advantages, as demonstrated by patent filings for semi-automatic sunshade mechanisms and magnetic attachment systems that create barriers to entry for new participants. Established players like Magna International and Webasto possess integration capabilities and OEM relationships that enable factory-installed solutions, while specialized suppliers focus on aftermarket channels and premium materials innovation. The competitive landscape increasingly rewards suppliers who demonstrate sustainability credentials and circular economy compliance, as automotive OEMs prioritize partnerships with vendors who support their environmental commitments and regulatory requirements.

Technology adoption patterns reveal strategic differentiation through smart materials, IoT integration, and advanced manufacturing processes that enable mass customization and vehicle-specific fitment. Companies invest in AI-driven demand forecasting and inventory optimization to manage seasonal demand variations and complex SKU portfolios across diverse vehicle platforms and geographic markets. White-space opportunities exist in autonomous vehicle applications, fleet management solutions, and integrated smart cabin systems that coordinate shading with thermal management and occupant monitoring technologies. Emerging disruptors leverage e-commerce platforms and direct-to-consumer models to capture market share from traditional distribution channels, while established players respond through digital transformation initiatives and partnership strategies that combine manufacturing scale with digital marketing capabilities.

Automotive Side Window Sunshades Industry Leaders

-

Macauto Group

-

BOS Group

-

Magna International

-

Webasto SE

-

Ashimori Industry

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Magna International announced participation in Auto Shanghai 2025, showcasing advanced innovations including reconfigurable seating systems and integrated cabin monitoring technologies that support autonomous vehicle applications and enhanced passenger comfort solutions.

- December 2024: FORVIA launched MATERI'ACT sustainable materials division with advanced recycled and bio-based compounds, including NAFILean-R biocomposite using 20% hemp fibers and 100% recycled polypropylene matrix that achieves up to 90% CO2 reduction compared to traditional materials.

Global Automotive Side Window Sunshades Market Report Scope

| Fabric |

| Polyester |

| Plastic |

| Foam |

| Roller Shades |

| Magnetic Shades |

| Static Shades |

| Retractable Shades |

| Front Window |

| Side Window |

| Rear Window |

| Passenger Vehicles |

| Light Commercial Vehicles |

| Medium and Heavy Commercial Vehicles |

| OEM |

| Aftermarket |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle-East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle-East and Africa |

| By Material Type | Fabric | |

| Polyester | ||

| Plastic | ||

| Foam | ||

| By Product Type | Roller Shades | |

| Magnetic Shades | ||

| Static Shades | ||

| Retractable Shades | ||

| By Application | Front Window | |

| Side Window | ||

| Rear Window | ||

| By Vehicle Type | Passenger Vehicles | |

| Light Commercial Vehicles | ||

| Medium and Heavy Commercial Vehicles | ||

| By Sales Channel | OEM | |

| Aftermarket | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle-East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the current value of the automotive side window sunshades market?

The market is valued at USD 3.77 billion in 2025, growing toward USD 5.13 billion by 2030.

Which material leads demand for side window sunshades?

Recycled polyester dominates with 45.23% share and the fastest 9.82% CAGR.

How fast is the magnetic shade segment expanding?

Magnetic shades are forecast to grow at an 11.24% CAGR, the quickest among product types.

Why are electric vehicles important to shade suppliers?

Electric passenger cars hold 55.12% segment share and need shades to limit HVAC load, growing at a 12.43% CAGR.

Which region offers the strongest growth outlook?

Asia-Pacific leads with 34.09% share and is projected to advance at a 9.72% CAGR through 2030.

Page last updated on: