Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

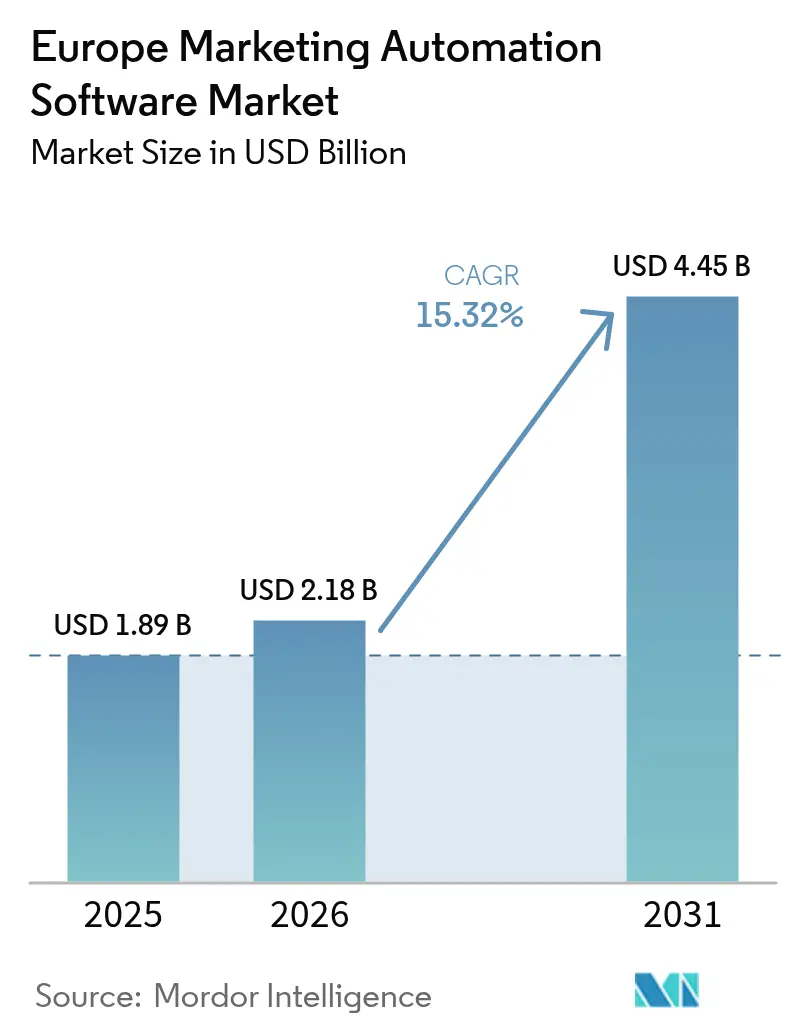

| Base Year Market Size (2025) | USD 1.89 Billion |

| Market Size (2026) | USD 2.18 Billion |

| Market Size (2031) | USD 4.45 Billion |

| Growth Rate (2026 - 2031) | 15.32% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Marketing Automation Software Market Analysis by Mordor Intelligence

The Europe marketing automation software market size was valued at USD 1.89 billion in 2025 and estimated to grow from USD 2.18 billion in 2026 to reach USD 4.45 billion by 2031, at a CAGR of 15.32% during the forecast period (2026-2031). [1]European Commission, “The Digital Europe Programme,” europa.eu Ongoing EU Digital Single Market measures that target 75% cloud adoption by 2030, together with the EUR 7.9 billion (USD 8.55 billion) Digital Europe Programme, underpin near-term expansion by subsidizing SaaS adoption among small and medium-sized enterprises. Meanwhile, the region’s EUR 887 billion (USD 960 billion) e-commerce economy in 2023 fuels demand for customer-centric engagement tools that remain compliant with GDPR while still delivering granular personalization. Competitive intensity is increasing as global platform vendors reinforce European footprints while local specialists differentiate through multilingual and regulatory expertise. Cloud deployment models dominate because they offer scalable compliance controls, yet the fastest corporate spending shift is toward managed services that bundle technology with GDPR-fluent implementation talent. Germany’s 18.5% CAGR and the DACH–Nordics focus on AI-driven personalization highlight the link between AI readiness and marketing automation uptake, whereas EU AI Act obligations and a scarcity of certified data-privacy architects temper roll-out velocity.

Key Report Takeaways

- By component, software led with 71.30% revenue share of the Europe marketing automation software market in 2025; managed services are advancing at a 15.92% CAGR through 2031.

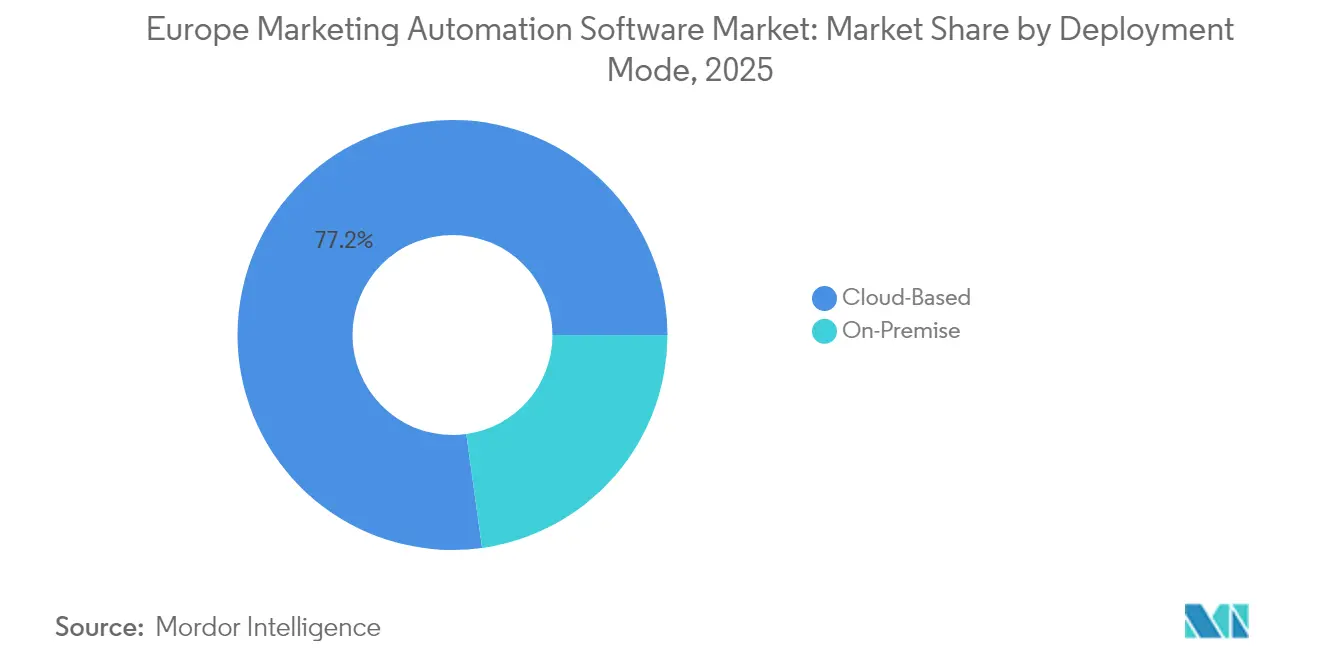

- By deployment mode, cloud solutions held 77.20% share of the Europe marketing automation software market in 2025, while cloud remains the fastest-growing option at a 15.62% CAGR to 2031.

- By organization size, large enterprises accounted for 59.20% of Europe marketing automation software market share in 2025; the SME segment is projected to expand at 17.32% CAGR to 2031.

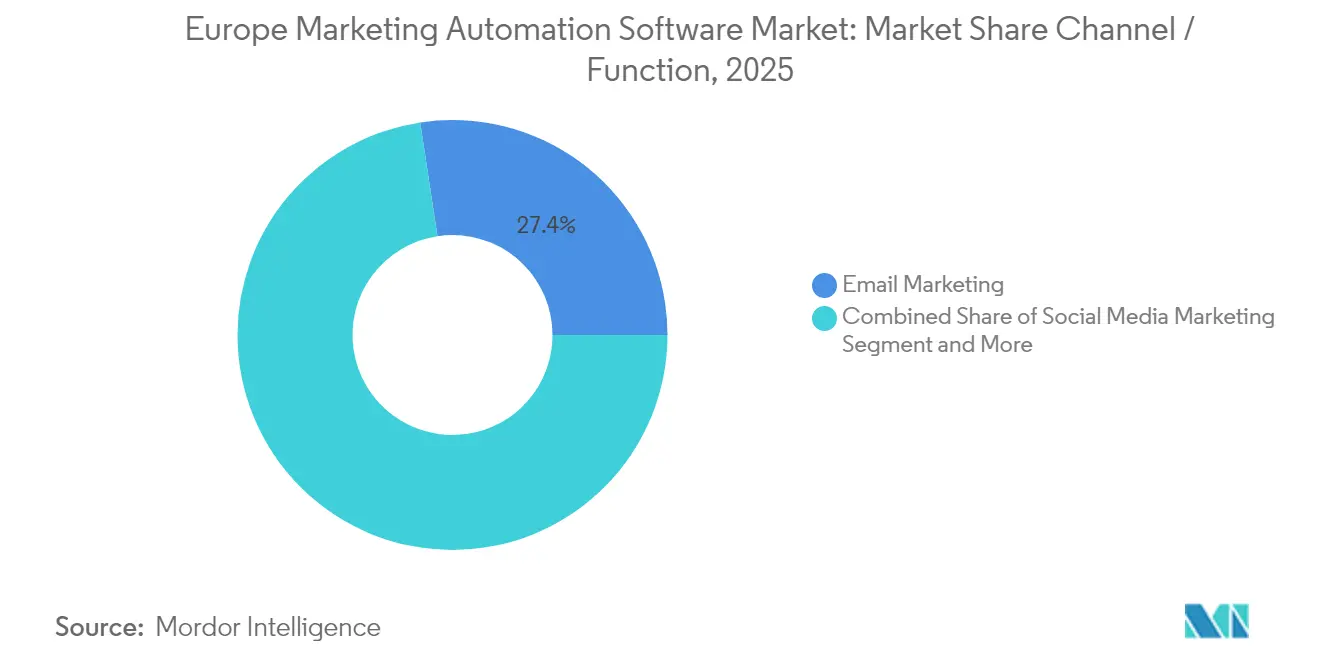

- By channel/function, email marketing commanded 27.40% share of the Europe marketing automation software market size in 2025, whereas customer-journey orchestration is forecast to grow at 17.48% CAGR.

- By end-user industry, retail and e-commerce captured 23.60% of the Europe marketing automation software market size in 2025; BFSI is delivering the fastest CAGR at 15.98% through 2031.

- By geography, the United Kingdom contributed 33.40% revenue in 2025; Germany posts the strongest country-level CAGR at 18.12% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Marketing Automation Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| AI-Powered Personalisation Surge in DACH and Nordics E-commerce | +3.2% | Germany, Netherlands, Nordics | Medium term (2-4 years) |

| EU Digital Single-Market Initiatives Boosting SME SaaS Uptake | +2.8% | EU-wide, concentrated in DACH | Long term (≥ 4 years) |

| Account-Based Marketing Adoption in B2B Tech Hubs | +2.1% | Netherlands, Germany, UK | Short term (≤ 2 years) |

| Open-Banking API Integration in European Financial Services | +1.9% | UK, Germany, France | Medium term (2-4 years) |

| Multi-Lingual Journey Orchestration Across Fragmented Markets | +1.7% | EU-wide, emphasis on multilingual regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

AI-Powered Personalisation Surge in DACH and Nordics E-commerce Drives the Market

AI-enabled engines have permeated DACH and Nordic retail, with 65% of executives naming AI a core growth lever in 2025. [2]Adobe Inc., “Adobe 2025 AI and Digital Trends Report,” Adobe Marketers exploit the regions’ advanced cloud infrastructure and high data-sharing consent rates to roll out recommendation models that elevate conversion. Telmore recorded an 11% uplift in sales after adopting AI-driven personalization, illustrating quantifiable ROI that accelerates peer adoption. As 80% of companies earmark higher AI budgets yet only 12% prove ROI, early adopters with strong measurement frameworks gain competitive distance. German practitioners use generative AI to streamline campaign production and reporting, cutting repetitive tasks and redeploying staff toward analytics. Consequently, the DACH–Nordic corridor functions as a test bed for next-wave personalization capabilities that subsequently diffuse across Europe.

EU Digital Single-Market Initiatives Boosting SME SaaS Uptake

The EUR 7.9 billion (USD 8.55 billion) Digital Europe Programme lowers barriers for SMEs by harmonizing cloud regulations and funding European Digital Innovation Hubs that provide hands-on guidance. Standardized APIs improve data portability, easing integration among disparate marketing applications and mitigating vendor lock-in risks. Cloud adoption among EU enterprises stands at 41% and is slated to reach 75% by 2030, translating into a sizeable new customer pool for SaaS-based marketing automation. These policy tailwinds curtail compliance complexity for mid-market buyers and amplify addressable demand within the Europe marketing automation software market.

Account-Based Marketing Adoption in B2B Tech Hubs Drives the Market

European B2B software vendors confront long buying cycles and multi-stakeholder purchasing, prompting a shift toward account-based marketing (ABM). Dutch and German tech clusters spearhead ABM deployment, combining AI insights and predictive scoring to pinpoint high-value accounts. Vendors that seamlessly integrate ABM modules with CRM workflows win traction because they unify pipeline visibility across marketing and sales teams. Growth in hybrid working intensifies the need for synchronized digital interactions, reinforcing ABM as a mainstream tactic in the Europe marketing automation software market.

Open-Banking API Integration in European Financial Services Drives the Market

PSD2-mandated open banking compels financial institutions to enable secure data sharing, allowing marketers to tie real-time transaction triggers to personalized messaging. Nearly 90% of European banks already utilize unified communications platforms, and 62% plan larger IT budgets to speed up digital initiatives. Marketing automation tools that can ingest banking APIs and adhere to stringent security norms position BFSI users to realize 16.2% CAGR in platform spend. Vendors that map regulatory reporting straight into their data pipelines reduce compliance overhead for clients and consolidate stickiness.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Scarcity of GDPR-Fluent Marketing-Automation Architects | -2.4% | EU-wide, acute in smaller markets | Short term (≤ 2 years) |

| High TCO for Multi-Language Personalisation Modules | -1.8% | Multilingual regions, fragmented markets | Medium term (2-4 years) |

| Stringent EU Anti-Spam Rules Impacting Email Deliverability | -1.3% | EU-wide, varying enforcement | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Scarcity of GDPR-Fluent Marketing-Automation Architects

Implementation projects increasingly stall because only a narrow cadre of professionals combines martech proficiency with legal insight. Banking workforce realignment illustrates cross-industry competition for data specialists after a 21% employment contraction in traditional roles between 2007 and 2022. SMEs are disproportionately affected, leading to a reliance on external managed services, which explains their 16.1% CAGR within the services component. Certification initiatives by European Digital Innovation Hubs provide relief, but near-term talent gaps constrain uptake within smaller economies.

High TCO for Multi-Language Personalisation Modules

Running localized campaigns across 24 EU official languages strains budgets, especially for content adaptation and compliance reviews. Even where AI translation tools exist, brands still fund cultural editing and tone checks that escalate total cost of ownership. Companies phase linguistic expansion, beginning with core markets before incremental roll-outs, slowing revenue capture for vendors. AI localisation advances hold promise, yet human oversight remains mandatory for regulated sectors, maintaining downward pressure on growth for the Europe marketing automation software market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Acceleration Outpaces Software Dominance

Software continued to generate 71.30% of Europe marketing automation software market revenue in 2025, though managed services outpaced with a 15.92% CAGR to 2031, underscoring corporates’ preference for outsourced compliance know-how. The services surge signals that enterprises consider technical execution and regulatory validation equally critical as core functionality. Within software, integrated suites eclipse point tools because buyers demand one source of truth for data privacy audits and AI model governance. Professional services thrive on legacy-system integration and GDPR gap analysis, positioning consultancies and system integrators as gatekeepers for vendor selection.

Heightened AI Act scrutiny places a premium on solution blueprints that embed auditability by design. Vendors combine packaged software with advisory retainers, generating annuity-style revenue. The Europe marketing automation software industry will therefore see blended business models, where software margins pair with high-touch services to address dynamic rule-sets spanning GDPR, PSD2, and sector-specific mandates.

By Deployment Mode: Cloud Infrastructure Drives Regulatory Compliance

Cloud options owned 77.20% of the Europe marketing automation software market in 2025, bolstered by EU backing for sovereign and trusted cloud frameworks. Cloud deployments are expanding at 15.62% CAGR because continuous platform updates help clients absorb new data-handling obligations without capex spikes. Marketing teams benefit from elastic compute to run AI models that personalize journeys in real time. On-premise persists only where public-sector or defense clients demand strict data residency.

Regulators favor cloud’s centralized control planes that support automated consent logging, breach notification, and encryption management. This regulatory alignment reduces perceived risk, spurring broader cloud migration. Partnerships, such as Oracle’s tie-up with Palantir for secure EU cloud regions, illustrate how hyperscale providers localize stacks to satisfy sovereignty narratives. As uptake matures, cloud vendors will compete on value-add layers like zero-trust architectures and pre-certified AI sandboxing.

By Organisation Size: SME Digital Transformation Accelerates Market Expansion

Large enterprises retained 59.20% revenue share in 2025 yet SMEs will drive volume growth at 17.32% CAGR, reflecting EU subsidies that close affordability gaps. The Europe marketing automation software market size for SMEs is set to expand as European Innovation Council financing of EUR 1.4 billion (USD 1.52 billion) fuels adoption. Freemium packaging, intuitive UX, and self-serve templates shorten onboarding cycles for resource-constrained firms.

In contrast, large enterprises negotiate enterprise-wide licenses with advanced AI tooling, cross-border compliance modules, and premium support SLAs. They also allocate budgets for custom feature requests that embed proprietary algorithms, reinforcing their spending weight. SMEs, however, dominate incremental customer counts, reshaping vendor go-to-market playbooks toward partner-led channels and localized onboarding academies.

By Channel/Function: Journey Orchestration Disrupts Email Marketing Leadership

Email remained the top individual channel with 27.40% share in 2025, yet customer-journey orchestration plus analytics is climbing fastest at 17.48% CAGR, redefining feature roadmaps across the Europe marketing automation software market. Brands shifting from campaign blasts to lifecycle management need AI to coordinate content, timing, and channel mix. Adobe’s 2025 Marketo Engage update embeds generative content engines that align messages with behavioral triggers, pointing to escalating innovation cycles.

Orchestration suites integrate inbound, social, mobile, and loyalty datasets into one decision hub, increasing incremental ROI over siloed tools. As measurement sophistication grows, attribution demands unify analytics, pushing vendors to deploy built-in dashboards that surface revenue impact at segment, cohort, and persona levels. Regulatory concerns about consent and tracking cookies accelerate first-party data strategies, further fuelling orchestration uptake.

By End-user Industry: BFSI Transformation Challenges Retail Dominance

Retail and e-commerce delivered 23.60% of the Europe marketing automation software market in 2025 because large catalogues and high purchase frequency make personalization pay off quickly. BFSI’s 15.98% CAGR reflects banks harnessing open-banking APIs for contextual offers that align with transaction events, lifting cross-sell. Use cases extend to credit-card upsell journeys and wealth-management nudges, where compliance logging is mandatory.

Manufacturing, guided by Industry 4.0 digital twins, adopts automation for account-based marketing targeting OEM buyers. Creative Foam’s CRM revamp illustrates how industrial firms leverage segmentation to deepen aftermarket sales. Healthcare, telecom, and public sectors follow, each demanding verticalized consent rules, thus encouraging vendors to package industry accelerators that compress deployment.

Geography Analysis

The United Kingdom contributed 33.40% of 2025 revenue, benefitting from fintech density, early cloud concession frameworks, and long-standing digital marketing sophistication. Post-Brexit divergence prompts dual compliance architectures that manage both UK GDPR and EU GDPR, incentivizing multi-tenant instances with jurisdiction-aware data routing. Germany rises fastest at 18.12% CAGR as Industry 4.0 factories integrate marketing data streams into PLM and ERP systems while DACH retailers pilot AI personalization engines.

France emphasizes data-sovereignty certifications like SecNumCloud, pushing vendors to offer localized hosting pods. Italy and Spain exhibit high mobile-commerce growth that propels SMS and WhatsApp automation features. The Netherlands operates as a regional hub for software headquarters, attracting ABM usage that drives platform expansion. Nordic states showcase the most advanced AI personalization use cases due to high digital literacy and willingness to share behavioural data.

Eastern and South-Eastern Europe, covered under Rest of Europe, benefit from EU Structural Funds and Digital Europe grants aimed at SME digitization, yet purchase cycles remain longer because of budget constraints. EU initiatives standardizing e-commerce taxation and sustainability disclosures reduce compliance burdens, encouraging cross-border marketing campaigns. Vendors that package language packs and country-specific rule templates position themselves to win multi-country tenders, amplifying the addressable share of the Europe marketing automation software market.

Competitive Landscape

Industry structure shows moderate consolidation. Alphabet’s aborted bid for HubSpot underscored the strategic premium attached to unified marketing, sales, and service stacks. Salesforce invests in autonomous multi-agent systems that cut manual campaign management, while Adobe integrates IBM watsonx AI to bolster compliance-first personalization inside its Experience Platform. Regional players emphasize multilingual orchestration and sector-specific templates.

Platform differentiation revolves around: 1) embedded compliance engines that automate consent retrieval and proof; 2) AI-driven content generation tuned for European languages; and 3) low-code connectors to ERP and banking APIs. Ecosystem alliances matter, as shown by UiPath and HCLTech’s agentic automation lab that packages martech workflows with robotic process automation. SAP’s RISE cloud migration path ensures its ERP clients gain native access to marketing automation modules, expanding the stickiness of its suite. Competitive intensity pivots on time-to-value and the ability to guarantee audit-grade data lineage across journeys.

Europe Marketing Automation Software Industry Leaders

Salesforce Inc.

Oracle Corporation

Microsoft Corporation

Hubspot Inc.

Adobe Inc.(Marketo Inc.)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: UiPath partnered with HCLTech to develop agentic automation solutions, establishing an AI Lab that will ship repeatable marketing, finance, and customer-service blueprints aimed at European clients seeking faster compliance validations.

- March 2025: Adobe used its annual Summit to unveil generative AI upgrades in Marketo Engage and Journey Optimizer B2B Edition, injecting automated content creation and improved omnichannel orchestration that directly target enterprise cost reduction.

- February 2025: Salesforce announced autonomous multi-agent systems designed to optimize marketing paths in real time, signalling next-generation AI emphasis on decision-making with minimal human oversight.

- January 2025: Microsoft expanded Premium connectors across Europe to strengthen integration between Dynamics 365 and third-party automation tools, enhancing unified martech stacks for enterprises.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Europe marketing automation software market as revenue generated from licensed or subscription-based platforms that automate tasks such as email distribution, social-media scheduling, lead nurturing, campaign analytics, and cross-channel orchestration for business users across the region. Solutions bundled inside bundled CRM suites or broader digital marketing stacks are counted only when sold and billed as distinct automation modules.

Scope exclusion: pure-play web-analytics tools, stand-alone CRM systems, and agency service fees are not included.

Segmentation Overview

- By Component

- Software

- Integrated Platforms

- Stand-Alone Tools

- Lead Management

- Social Media

- Email and Analytics

- Services

- Professional Services

- Managed Services

- Software

- By Deployment Mode

- Cloud-Based

- On-Premise

- By Organisation Size

- Small and Medium Enterprises

- Large Enterprises

- By Channel / Function

- Email Marketing

- Social Media Marketing

- Campaign Management

- Mobile / SMS Marketing

- Inbound and Content Marketing

- Other Channels

- By End-user Industry

- Retail and E-commerce

- BFSI (Banking, FinServ and Insurance)

- IT and Telecom

- Manufacturing

- Healthcare and Life-Sciences

- Media and Entertainment

- Government and Public Sector

- Other End-user Industries

- By Country

- United Kingdom

- Germany

- France

- Italy

- Spain

- Netherlands

- Nordics

- Rest of Europe

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interview European chief marketing officers, martech procurement heads, implementation consultants, and regional software resellers across the United Kingdom, DACH, Nordics, Benelux, and Southern Europe. These guided discussions validate adoption rates, average seat prices, and deployment preferences while filling quantitative gaps uncovered during desk analysis.

Desk Research

We begin with structured reviews of public sources such as Eurostat ICT usage surveys, Ofcom and BNetzA telecom indicators, the Interactive Advertising Bureau Europe ad-spend database, and national data-protection authorities' GDPR enforcement dashboards. Financial filings, investor decks, and product catalogs help us map vendor revenue splits between software and services. Subscription access to D&B Hoovers and Dow Jones Factiva lets analysts track company performance and news flows that signal pricing shifts. The sources listed illustrate the evidence pool; many additional publications and datasets inform our work.

Market-Sizing & Forecasting

A top-down model reconstructs addressable spend by applying marketing-budget penetration ratios to country-level digital ad outlays and then adjusting for cloud software adoption and SME density before results are cross-checked with selective bottom-up vendor revenue roll-ups. Key variables include average annual license price per user, marketing personnel counts, cloud-migration pace, GDPR-driven platform upgrades, and e-commerce share of retail sales, all trended from 2019 onward. Multivariate regression blended with ARIMA smoothing projects each driver through 2030, while scenario analysis captures regulatory or macro shocks. Where supplier data are partial, missing values are bridged using regional peer medians that we later reconcile through expert feedback.

Data Validation & Update Cycle

Model outputs pass variance thresholds versus historical spend, vendor disclosures, and macro indicators; anomalies trigger re-runs and senior-analyst review. Reports refresh every twelve months, with interim updates when material events, such as funding rounds and policy changes, shift the baseline.

Why Our Europe Marketing Automation Software Baseline Earns Trust

Published figures often diverge because firms pick different module mixes, pricing logics, and refresh cadences. Our disciplined scoping and annually refreshed driver set keep estimates aligned with real buying behavior.

Key gap drivers include whether SMEs are counted, if email-only tools or full suites are modeled, and how EUR revenues are converted to constant USD. Our balanced approach, blending public evidence with direct buyer insight, tempers over-optimism and avoids undue conservatism.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.89 B (2025) | Mordor Intelligence | - |

| USD 2.10 B (2024) | Regional Consultancy A | Adds CRM modules and broader digital marketing software revenues |

| USD 1.56 B (2024) | Global Consultancy B | Focuses on email automation and omits SME demand |

| USD 5.62 B (2023) | Trade Journal C | Converts unsegmented martech revenue pools without country-level adjustment |

These comparisons show that when scope, currency, and refresh cadence are harmonized, Mordor's figure sits near the mid-point, giving decision-makers a dependable, transparent baseline backed by repeatable steps and clearly cited variables.

Key Questions Answered in the Report

What is the value of the Europe marketing automation software market in 2026 and how fast is it growing?

The market stands at USD 2.18 billion in 2026 and is projected to expand at a 15.32% CAGR to reach USD 4.45 billion by 2031.

Which deployment model is preferred by European buyers?

Cloud-based solutions account for 77.20% of 2025 revenue because they offer scalable GDPR-compliant infrastructure and easier AI upgrades.

Why are small and medium enterprises driving the fastest growth?

EU funding initiatives, freemium pricing, and low-code platforms cut adoption barriers, propelling the SME segment at a 17.32% CAGR through 2031.

Which country shows the highest growth momentum?

Germany leads with an 18.12% CAGR, supported by Industry 4.0 investment and DACH region AI-personalization pilots.

What end-user industry is expanding quickest?

Banking and financial services are increasing spending at a 15.98% CAGR as open-banking APIs enable real-time, regulated customer outreach.

What is the main talent-related obstacle to wider adoption?

There is a shortage of professionals who combine marketing-automation skills with deep GDPR expertise, slowing roll-outs and boosting demand for managed services.

Page last updated on: