Automotive Power Module Packaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

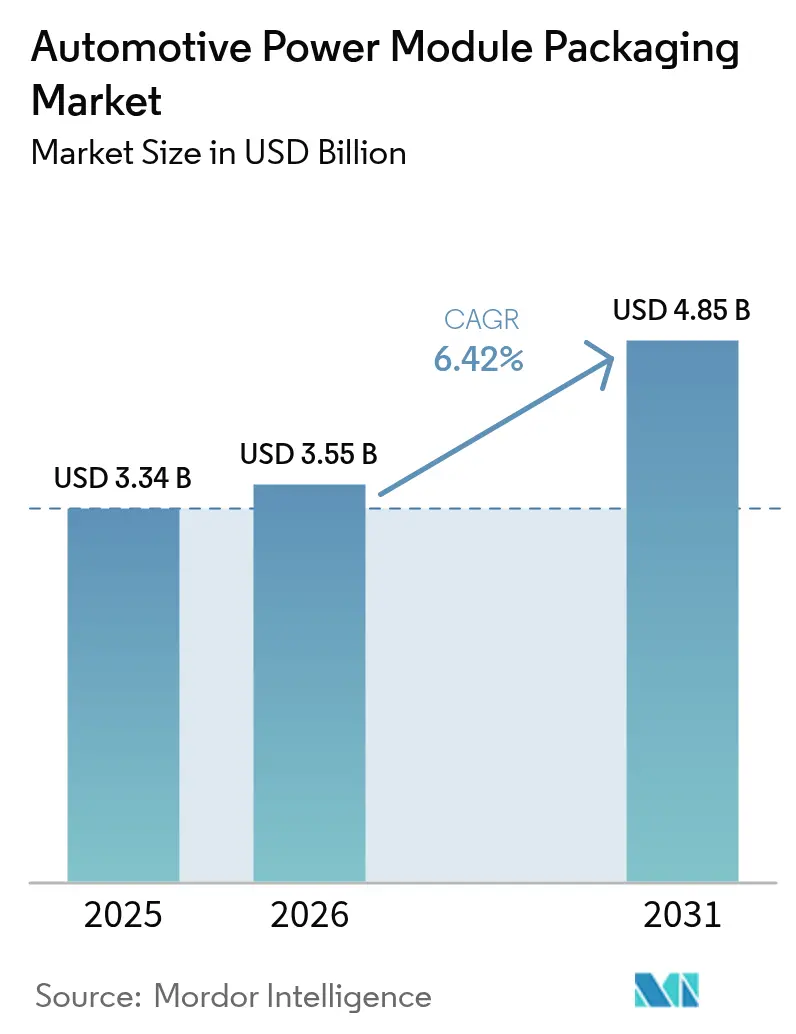

| Market Size (2026) | USD 3.55 Billion |

| Market Size (2031) | USD 4.85 Billion |

| Growth Rate (2026 - 2031) | 6.42% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive Power Module Packaging Market Analysis by Mordor Intelligence

Automotive power module packaging market size in 2026 is estimated at USD 3.55 billion, growing from 2025 value of USD 3.34 billion with 2031 projections showing USD 4.85 billion, growing at 6.42% CAGR over 2026-2031. The automotive power module packaging market is expanding because automakers accelerated electrification programs, pushed higher voltage architectures into volume production, and demanded advanced thermal-management solutions for wide-bandgap devices. Rising investments in 200 mm SiC wafer fabs, partnerships that compress development cycles, and tighter emission standards collectively reinforce long-term demand. Suppliers that master wire-bondless interconnects, double-sided cooling, and silver sintering are securing design wins in traction inverters, on-board chargers, and DC-DC converters. Meanwhile, supply constraints for SiC substrates and fragmented qualification rules remain headwinds.

Key Report Takeaways

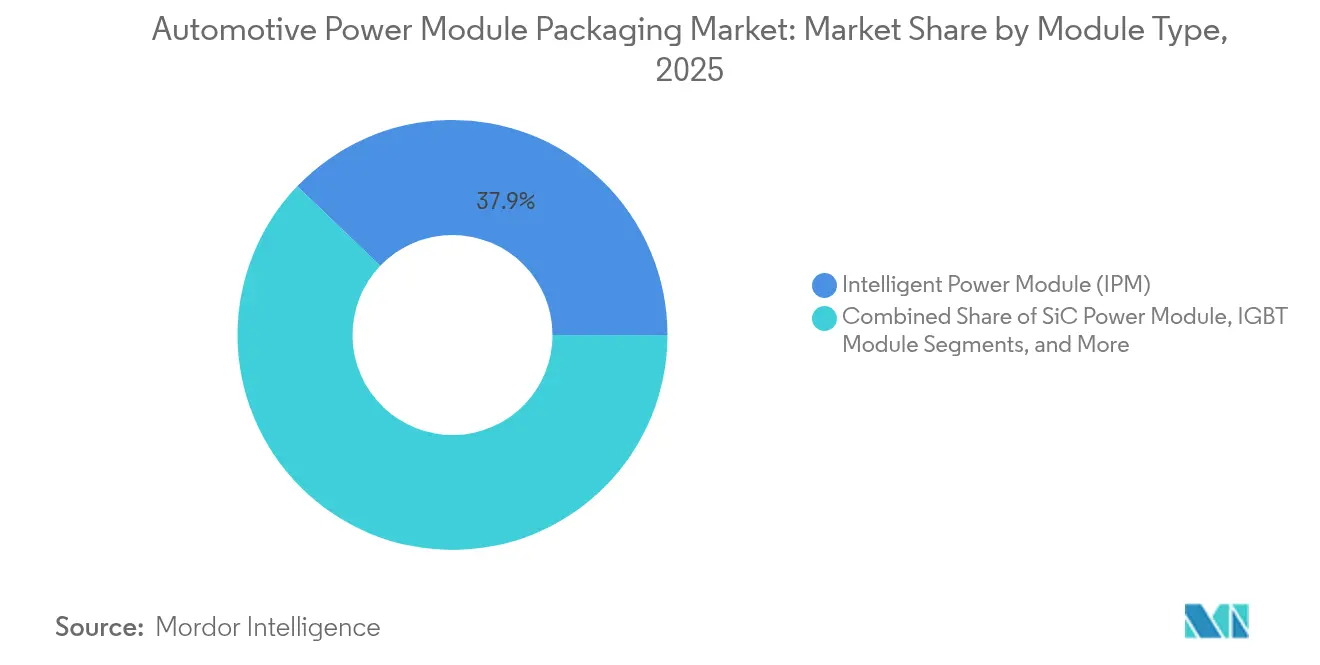

- By module type, Intelligent Power Modules led with 37.85% revenue share in 2025; SiC Power Modules are projected to expand at a 14.7% CAGR through 2031.

- By power rating, the Up to 600 V segment held 44.05% of the automotive power module packaging market share in 2025, while the 601-1200 V category is forecast to grow at 6.84% CAGR to 2031.

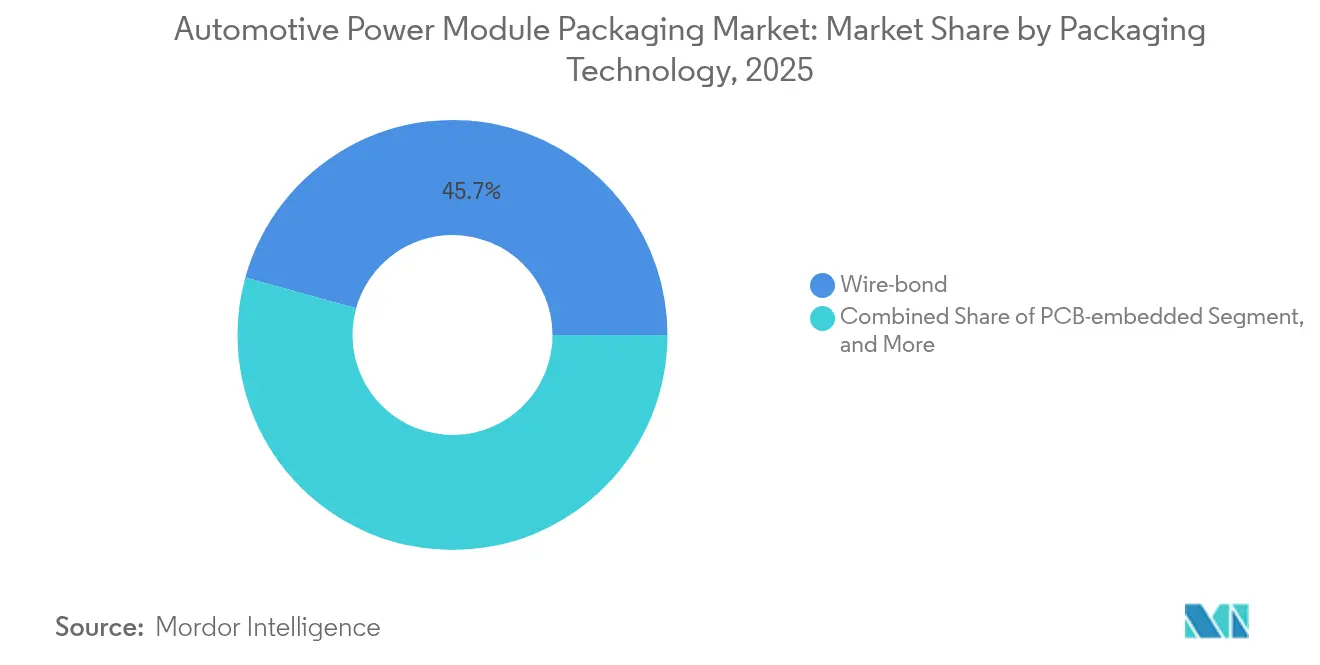

- By packaging technology, Conventional Wire-bond captured 45.70% share in 2025; Wire-bondless/Power Overlay is poised for a 9.18% CAGR through 2031.

- By propulsion type, Battery-Electric Vehicles commanded a 61.10% share in 2025; Fuel-Cell Electric Vehicles are set for a 16.3% CAGR to 2031.

- By vehicle type, Passenger Cars accounted for 67.60% share in 2025, whereas Heavy Commercial Vehicles and Buses are projected to advance at 7.98% CAGR.

- By application, Traction Inverters represented 49.10% of the automotive power module packaging market size in 2025; On-board Chargers are expected to post a 13.1% CAGR between 2026 and 2031.

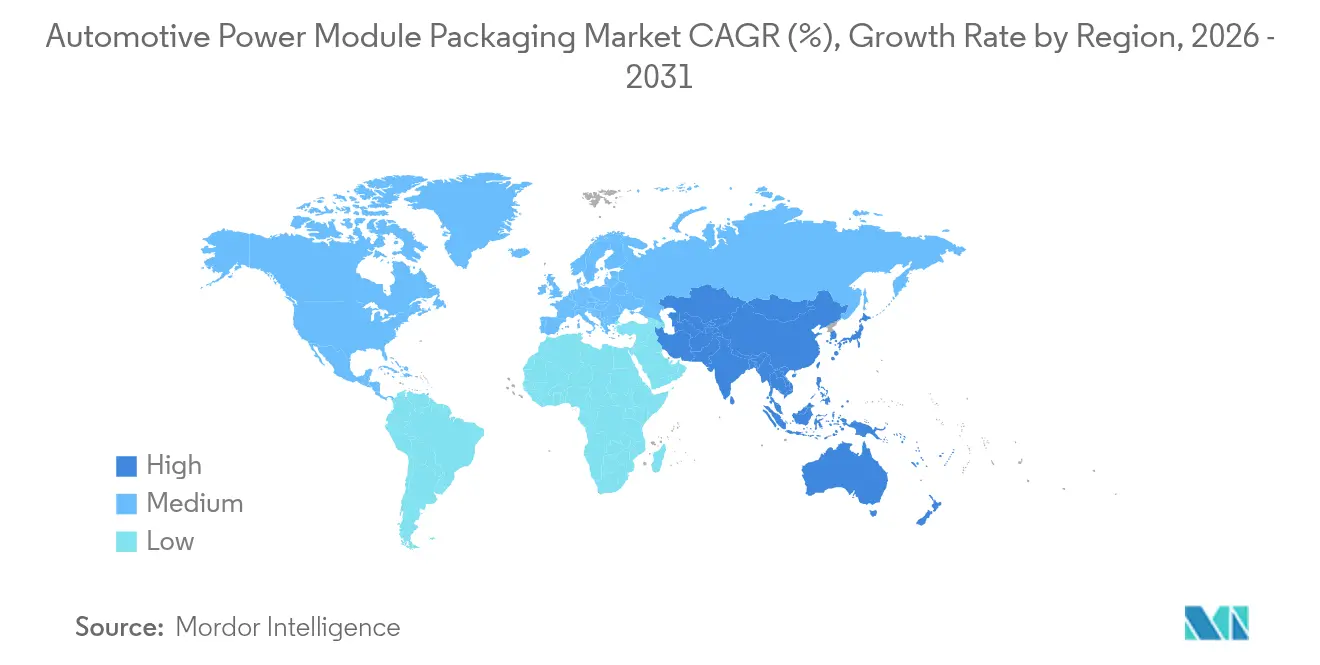

- By geography, Asia-Pacific held a 56.80% share in 2025 and is likely to record an 8.72% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Automotive Power Module Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid EV and HEV production growth | +1.8% | Global, with Asia-Pacific leading | Medium term (2-4 years) |

| Shift toward SiC and GaN wide-bandgap devices | +1.2% | North America and the EU leading, Asia-Pacific following | Long term (≥ 4 years) |

| Vehicle electrification demands higher power-density modules | +1.0% | Global | Medium term (2-4 years) |

| Stringent global emission regulations | +0.8% | EU and North America core, spill-over to Asia-Pacific | Long term (≥ 4 years) |

| OEM adoption of wire-bondless / top-side-cooling packages | +0.6% | Global, with early adoption in premium segments | Medium term (2-4 years) |

| Cell-to-pack architectures integrating power modules | +0.4% | Asia-Pacific core, expanding to global markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid EV and HEV production growth

Global battery-electric and hybrid output climbed sharply in 2024, and automotive applications already accounted for more than 70% of SiC demand. Tesla’s Cybertruck power converter illustrated how 800 V platforms double voltage stresses and intensify thermal management needs. Tier-1 suppliers such as BorgWarner reported 47% year-on-year eProduct sales growth, signaling that established drivetrain specialists are pivoting resources toward high-density modules.[1]BorgWarner, “First Quarter 2025 Results,” borgwarner.com Commercial vehicle programs, including ZF’s 300 kW eBeam axle, further widen the addressable base for ruggedized packaging.

Shift toward SiC and GaN wide-bandgap devices

Fourth-generation SiC MOSFETs now sustain junction temperatures above 200 °C, intensifying the need for copper clips, silver sintering, and direct die cooling. Infineon forecasts 2025 as an inflection year for automotive GaN, especially in on-board chargers and high-frequency DC-DC converters. Supply bottlenecks for SiC substrates sharpened focus on 200 mm wafer transitions and on multi-source agreements that stabilize capacity.

Vehicle electrification demands higher power-density modules

Automakers pursued lighter drivetrains and more compact electronic housings in 2024. Texas Instruments demonstrated a 50% footprint reduction through its MagPack concept by integrating magnetic components within the module package. Academic benchmarks showed that double-sided cooling cut SiC junction temperatures by 30 °C, enabling further power-density gains. Emerging cell-to-pack architectures embed modules directly into the battery enclosure, an approach supported by thermally conductive urethane adhesives that double as structural fillers.

Stringent global emission regulations

EU CO₂ targets and China’s dual-credit policy tightened in 2024, prompting OEMs to specify lower switching and conduction loss figures. Semikron Danfoss responded with double-sided sintering, eliminating fatigue-prone bond wires to boost current handling and reliability. Qualification standards such as AEC-Q101 became stricter, and Navitas secured an “AEC-Plus” rating for top-side-cooled SiC MOSFETs that meet extended automotive stress profiles.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lack of standardized qualification protocols | -0.8% | Global, with varying regional standards | Medium term (2-4 years) |

| High cost and supply constraints of SiC / GaN substrates | -1.2% | Global, with Asia-Pacific supply concentration | Short term (≤ 2 years) |

| Thermal-management limits in emerging 800V platforms | -0.6% | Global, affecting premium vehicle segments | Medium term (2-4 years) |

| Potential SiC supply-chain over-capacity | -0.4% | Global, with regional variations | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Lack of standardized qualification protocols

Power-electronics suppliers faced repeated test loops because AEC-Q100, AEC-Q101, and AEC-Q200 were interpreted differently by regional OEMs, prolonging time-to-market and inflating non-recurring expenses. IECQ launched its Automotive Qualification Programme to harmonize procedures, yet adoption remained uneven.

High cost and supply constraints of SiC/GaN substrates

Physical vapor transport still limited SiC boule growth rates to millimeters per hour, keeping wafer prices elevated; substrates accounted for around 47% of device value. Concentrated capacity in Asia introduced geopolitical risk, and some European fabs deferred expansion because of uncertain near-term demand outlooks.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Module Type: SiC Modules Drive Premium Adoption

Intelligent Power Modules held 37.85% of 2025 revenue and remained the volume choice for entry-level EVs and hybrids. SiC Power Modules, though costlier, achieved 14.7% CAGR forecasts as premium and commercial platforms prioritized efficiency. The automotive power module packaging market size for SiC devices is projected to capture an additional 7.3 percentage-point share by 2031. ROHM and Valeo’s TRCDRIVE pack showed how SiC enables inverter downsizing without thermal compromise. Meanwhile, GaN penetrated on-board chargers where high-frequency switching outweighed current limits. IGBT and FET modules continue to serve mid-range and auxiliary loads, and recent Mitsubishi Electric releases reduced switching losses by 15% while extending moisture tolerance.

Market diversification persisted across the automotive power module packaging market as OEMs balanced cost, efficiency, and availability. SiC cost declines are expected once 200 mm wafers reach scale and vertical-integration strategies mature. Hence, suppliers that bundle design tools, gate drivers, and thermally optimized housings are positioning themselves to capture multi-year platform awards. The competitive split between integrated device makers and specialized assembly firms is likely to narrow as customers demand turnkey module sub-systems.

By Power Rating: 800 V Transition Reshapes Demand

Systems up to 600 V retained a 44.05% share in 2025, anchored by existing 400 V passenger-car platforms. However, the 601-1200 V band is the automotive power module packaging market’s fastest climber at 6.84% CAGR, mirroring the shift to 800 V topologies that cut fast-charging times. Aptiv outlined insulation challenges and creepage requirements that raise the value of robust packaging. Above-1200V modules remain niche, targeting heavy-duty and infrastructure roles.

Higher voltage demands intensified the development of thicker insulation gels, copper clips with lower inductance, and press-fit pins rated beyond 1.5 kV. Infineon’s 1200 V CoolSiC MOSFETs were selected by Forvia Hella for 800 V DC-DC converters, underscoring the platform shift. Packaging suppliers that guarantee partial discharge endurance and field-failure analytics will win specifications as OEMs standardize on next-generation high-voltage domain controllers.

By Packaging Technology: Wire-Bondless Solutions Gain Momentum

Conventional wire-bond designs still made up 45.70% of 2025 shipments thanks to mature tooling and cost efficiency. Yet, wire-bondless or power overlay formats are set for a 9.18% CAGR to 2031, driven by the need to limit parasitics and distribute heat evenly across the SiC die. Shinko Electric’s POL platform applied PCB fabrication know-how to achieve sub-10 nH loop inductance and fine-pitch copper pillars. Direct-pressed-die variants found acceptance in heavy-duty traction because chip front-side cooling reduced thermal resistance.

PCB-embedded packages are beginning to surface in space-constrained auxiliary converters. Hybrid bonding, promoted by several substrate vendors, promises further vertical integration, and 400 V/800 V stackable modules are under evaluation for shared cooling plates. As reliability databases grow, an accelerated migration away from aluminum bond wires is probable across the automotive power module packaging market.

By Propulsion Type: FCEV Growth Outpaces BEV Expansion

Battery-Electric Vehicles dominated at 61.10% in 2025 and continued to anchor volume demand for power modules. Fuel-Cell Electric Vehicles, although smaller, are forecast to grow at 16.3% CAGR because commercial fleets value rapid refueling and extended range. Honda’s next-generation 150 kW fuel-cell stack halved costs and doubled durability, elevating module integration requirements. Hybrid and plug-in hybrid architectures still require versatile modules that tolerate bidirectional energy flows.

Module suppliers optimized cooling plates and gate drivers to accommodate hydrogen stack voltage fluctuations. Bosch delivered scalable fuel-cell power modules up to 300 kW, pointing to higher amperage interconnects and reinforced substrates. The propulsion mix implies that design flexibility and cross-platform compatibility will be central to long-term share gains in the automotive power module packaging industry.

By Vehicle Type: Commercial Vehicles Drive Innovation

Passenger cars held a 67.60% share in 2025 as high-volume EV models proliferated. Heavy commercial vehicles and buses showed the quickest uptake at 7.98% CAGR, spurred by fleet emission targets and predictable duty cycles that justify higher upfront costs. Semikron Danfoss’ SKAI 2 HV platform reached 24 kVA per liter and IP67 sealing, signaling distinct rugged-packaging needs.

Light commercial vans followed, particularly in urban logistics. Hyundai Mobis invested USD 256.7 million in Slovakia for European power-system manufacturing, reflecting regional content rules. The vehicle-type split reinforces a dual-track roadmap: cost-sensitive passenger modules and high-reliability heavy-duty solutions that often pioneer new thermal interfaces.

By Application: Traction Inverters Dominate, Chargers Accelerate

Traction inverters commanded 49.10% of the 2025 value because every electrified drivetrain relies on a high-power motor controller. Automotive power module packaging market size for on-board chargers is forecast to expand fastest at 13.1% CAGR as OEMs adopt 11-22 kW AC and 25-50 kW DC units that demand higher-frequency GaN or SiC devices. ROHM’s HSDIP20 SiC module achieved a 38 °C temperature drop versus discrete configurations, underscoring the thermal benefits of monolithic packages.

DC-DC converter and auxiliary module demand increased in 48 V systems that support electric power steering and climate compressors. Vicor’s conversion module solved dual 400V V/800 800V battery compatibility, demonstrating how packaging design can resolve system-level voltage diversity. Integration trends point to multifunction modules that collapse inverter, charger, and converter roles into a single thermal domain.

Geography Analysis

Asia-Pacific retained a 56.80% share in 2025 and posted the highest outlook at 8.72% CAGR to 2031. China’s dual-credit rules and scale advantages drew major SiC investments, including Infineon’s USD 2 billion 200 mm fab in Malaysia that addressed regional capacity resilience. Local supply chains spanning substrates, metallization pastes, and molding compounds shortened lead times and trimmed costs.

North American demand accelerated as domestic OEMs unveiled new 800 V pickups and SUVs. onsemi committed USD 2 billion to build an end-to-end SiC line in the Czech Republic, ensuring wafer-to-module control and reducing import dependency. Federal manufacturing tax credits also encouraged module assembly within the United States.

Europe focused on premium EV brands and strict emissions mandates. Vitesco Technologies invested EUR 576 million (USD 650 million) to expand advanced-electronics production in Ostrava, signaling confidence in regional electrification momentum. Collectively, regional diversification initiatives are diluting single-region risk and fostering technology transfers that elevate global quality benchmarks.

Regulatory Landscape

Automotive power module packaging is shaped by automotive reliability and qualification regimes that translate into design rules for SiC and high-voltage modules. In 2026, SEMI revised SEMI F71 (F71-0526) to mandate thermal cycling for Kelvin source pins in >=1200 V SiC MOSFET modules used for AEC-Q101 certification, effective October 1, 2026. The update increases scrutiny on interconnect robustness, power cycling durability, and design-for-reliability practices.

Industrial policy is also affecting where advanced packaging and assembly capacity is built. In July 2026, the US Department of Commerce signed a USD 225 million CHIPS Act direct funding agreement with Robert Bosch Semiconductor LLC to expand SiC semiconductor production in Roseville, California, supporting domestic supply for automotive-grade power electronics. In Europe, the European Commission proposed Chips Act 2.0 in June 2026, reinforcing resilience measures across the value chain, including advanced packaging and assembly, and aligning with the report's emphasis on local content and multi-region backend strategies.

Value Chain Analysis

The value chain covers SiC and GaN materials and wafers, device fabrication, automotive-grade assembly and packaging (substrates, sintering or interconnect, molding, thermal interface materials), test and qualification, and delivery into Tier-1 power electronics (traction inverters, on-board chargers, DC-DC converters) and OEM vehicle platforms. For automotive power module packaging, the most critical upstream inputs remain substrates and packaging materials (ceramic substrates, metallization pastes, mold compounds, and thermal interface stacks), while downstream differentiation is increasingly tied to wire-bondless interconnects, top-side or double-sided cooling architectures, and the ability to clear qualification programs such as AQG 324.

Supply-chain behavior also shows tighter coupling between device makers, packaging specialists, and OEM platforms to shorten design cycles and manage high-voltage requirements. In January 2026, Sanken Electric entered a technical partnership with Minebea Power Semiconductor Device Inc. for joint product development and back-end production collaboration, including installing a new back-end production line at MPSD's Haramachi Plant. In June 2026, Nexperia and Semikron Danfoss signed an MoU to co-develop SiC-based power modules for automotive traction inverters, combining SiC device expertise with module packaging and integration capability. On the demand side, onsemi expanded collaboration with Geely (April 2026) and with NIO (April 2026) around EliteSiC solutions for 900 V-class EV architectures, reinforcing early co-design of device, package, and system-level constraints rather than treating packaging as a late-stage assembly step.

Competitive Landscape

The automotive power module packaging market remained moderately fragmented in 2024. Infineon, STMicroelectronics, and onsemi leveraged vertical integration to secure wafer capacity, internal assembly, and system knowledge. Semikron Danfoss, JCET, and Shinko Electric specialized in advanced interconnects and custom substrates, winning orders from Tier-1 inverter makers. Market entry barriers centered on qualification cost, thermal-simulation expertise, and supply-chain relationships.

Strategic partnerships intensified. ROHM allied with TSMC for GaN, accelerating automotive qualification cycles, while STMicroelectronics collaborated with Semikron to co-optimize SiC module stacks. Acquisition activity also rose: onsemi bought Qorvo’s SiC JFET assets for USD 115 million to deepen its EliteSiC portfolio.[4]Semiconductor Today, “onsemi Completes Acquisition of SiC JFET Business,” semiconductor-today.com

Competitive advantages shifted toward holistic offerings that include digital twin modeling, embedded diagnostic firmware, and thermal interface materials. Companies able to supply turnkey subsystems, support local content rules, and guarantee multi-sourced substrates are positioned to gain share as platform contracts consolidate through 2030.

Automotive Power Module Packaging Industry Leaders

Amkor Technologies

Infineon Technologies

STMicroelectronics

Fuji Electric Co. Ltd.

Toshiba Electronics Device & Storage Corporation

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Whitespace is concentrated around packaging architectures that enable higher voltage and temperature operation while reducing inverter and charger size, as OEMs shift from 400 V toward 800 V to 900 V platforms and expand adoption of SiC and emerging automotive GaN. In 2026, suppliers showed product and platform evidence for industrializing wire-bondless, high-thermal-performance designs: Infineon introduced a 1300 V HybridPACK Drive SiC module capable of 205 C continuous junction temperature operation (May 2026), and also presented its EasyPACK S platform with .XT interconnection technology paired with 1200 V CoolSiC MOSFET G2 (June 2026). USI announced SiC chip-embedded packaging technology using multilayer ABF substrates and a wire-bondless architecture (May 2026), which aligns with the need to reduce parasitics and improve power cycling robustness in compact automotive power stages.

A second opportunity area is advanced thermal management, moving beyond conventional cold-plate approaches toward integrated cooling structures that support higher continuous power density without compromising reliability. At IEEE APEC 2026 (March 2026), researchers demonstrated a 1.2 kV half-bridge SiC module with double-sided cooling and embedded microchannel coolers, illustrating a pathway for next-generation traction inverter packaging where thermal constraints drive system design. Suppliers that pair these thermal innovations with automotive qualification readiness (for example, AQG 324-aligned power cycling and fatigue modeling) and scalable backend manufacturing partnerships can address OEM demand for smaller, higher-voltage modules across traction inverters and fast-growing on-board charger designs.

Recent Industry Developments

- June 2026: Infineon introduced the EasyPACK S power module platform concept at PCIM Europe 2026, targeting compact, high-power-density applications and leveraging .XT interconnection with 1200 V CoolSiC MOSFET G2 options. The platform approach supports faster module standardization across traction inverter and auxiliary converter designs while shifting packaging differentiation toward interconnect and thermal performance.

- December 2024: STMicroelectronics entered a multi-year supply agreement with Renault Group and Ampere for silicon carbide power modules starting in 2026 for use in electric powertrain inverters. The deal reinforces long-cycle automotive sourcing patterns and increases the importance of qualified packaging capacity and predictable backend supply for platform launches.

- May 2024: STMicroelectronics announced a EUR 5 billion investment program, supported by the EU Chips Act and the State of Italy, to build a 200 mm SiC manufacturing facility in Catania, integrating substrate, epitaxy, and back-end module assembly, with production targeted for 2026. The expansion tightens vertical integration for SiC devices and packaging, strengthening regional supply resilience for automotive power modules.

Research Methodology Framework and Report Scope

Market Definition and Coverage

The automotive power module packaging market includes the materials, package designs, and assembly approaches used to protect and connect automotive power semiconductor modules, while managing heat dissipation, insulation, and reliability under vehicle operating conditions.

The sizing excludes upstream wafer fabrication and standalone discrete power devices sold without an automotive power module package.

Segmentation Overview

- By Module Type

- Intelligent Power Module (IPM)

- SiC Power Module

- GaN Power Module

- IGBT Module

- FET Module

- By Power Rating

- Up to 600 V

- 601 – 1200 V

- Above 1200 V

- By Packaging Technology

- Wire-bond

- Wire-bondless / Power Overlay

- Press-fit / Direct Pressed-Die

- PCB-embedded

- By Propulsion Type

- Battery-Electric Vehicle (BEV)

- Hybrid Electric Vehicle (HEV)

- Plug-in Hybrid (PHEV)

- Fuel-Cell Electric Vehicle (FCEV)

- By Vehicle Type

- Passenger Cars

- Light Commercial Vehicles

- Heavy Commercial Vehicles and Buses

- By Application

- Traction Inverter

- On-board Charger

- DC-DC Converter

- Auxiliary / Climate / EPS

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Rest of South America

- Europe

- Germany

- France

- United Kingdom

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research starts by mapping how automotive electrification drives power module volumes, packaging format demand, and then converting that demand into value using pricing benchmarks. We use public statistical and technical sources such as International Energy Agency EV outlook data, US DOE vehicle technology publications, USITC trade statistics, Eurostat Comext trade tables, and standards and guidance from IEC and SAE for operating requirements and application context.

To keep assumptions grounded, we also review annual reports, investor presentations, press releases, and application notes that describe packaging formats, qualification cycles, and typical use cases across propulsion and auxiliaries. Where needed, a paid subscription was referenced for company financials and another for patent lookups to cross-check activity levels and product direction. The desk sources listed above are illustrative only, and additional public documents and datasets were used across collection, validation, and clarification.

Primary Interviews and Surveys

Primary work is used to pressure test areas where desk sources cannot fully explain, such as packaging adoption by vehicle program, ASP movement for leadframes and substrates, and the pace of qualification for new materials. We speak with participants across the value chain, including packaging material suppliers, module assemblers, and automotive tiered integrators, and we validate patterns across APAC, EMEA, and the Americas so regional production footprints are reflected correctly.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 30% | CXOs: 14% | APAC: 41% |

| Mid tier: 55% | Functional/Unit leaders: 40% | EMEA: 35% |

| Smaller Players: 15% | Managers: 46% | Americas: 24% |

Market-Sizing & Forecasting

Sizing is built using a top-down logic, where vehicle production, the EV and hybrid mix, and power electronics content per vehicle are used to reconstruct the demand pool for packaged power modules. Once that demand pool is established, it is translated into value using packaging intensity assumptions by module type and typical price ranges for substrates, interconnects, and encapsulation steps.

To avoid over-reliance on one lens, the results are corroborated with selective bottom-up approximations, such as sampled ASP times estimated module shipment volumes, channel checks on substrate and leadframe demand, and sanity checks using capacity expansion signals. The input variables include EV and hybrid production by region, inverter and on-board charger penetration, shifts toward higher temperature operation that change material choices, substrate mix (such as DBC versus alternatives), and qualification timelines that delay new package rollouts. For forecasting, we run scenario analysis supported by expert consensus on EV adoption paths and packaging technology transition speed, and we fill data gaps using proxy ratios anchored to vehicle output and confirmed with interview feedback.

Data Validation & Update Cycle

Outputs are validated using checks for outliers across regions, propulsion types, and implied pricing, followed by a second pass to confirm the trend direction matches independent market signals. If a variance is detected, assumptions are revisited and, where needed, respondents are re-contacted to confirm whether the change is real or driven by temporary items such as inventory correction or program delays.

Before sign-off, the model is reviewed across multiple analysts to keep unit logic, currency treatment, and time alignment consistent. Reports are refreshed annually, with interim updates triggered by material events such as major capacity announcements, new qualification milestones, or sharp changes in the vehicle production outlook. Right before delivery, a final refresh pass is completed so clients receive the latest updated view.

Mordor Intelligence's Automotive Power Module Packaging Market Estimate Compared With Other Published Estimates

Published market sizes for automotive power module packaging can differ even when the topic name looks similar, because each publisher defines its own scope for what counts as packaging value and which years are treated as the base period. The gap also widens when different EV adoption paths are used, or when pricing is assumed to decline quickly without being checked against qualification timelines and supply constraints.

In practice, the biggest drivers are whether substrate and interconnect materials are fully counted versus partially treated as upstream components, whether packaging tied to traction inverters only is counted or both propulsion and auxiliary power electronics are included, and how currency conversion timing is handled for Asia-based production. The spread in the table is largely explained by keeping the scope limited to automotive module packaging and anchoring volumes to vehicle and powertrain build rates with interview-backed ASP bands, a choice applied by Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 3.55 B (2026) | |

| Industry Publisher A | USD 3.80 B (2024) | Uses an earlier base year and a longer horizon, and the higher growth profile suggests more aggressive EV adoption and faster package value uplift, with limited visibility on how substrate versus module value is separated. |

| Global Consultancy B | USD 1.90 B (2024) | Appears to apply a narrower value capture, which can happen when only selected module types or packaging steps are counted, and when regional vehicle production weights are not fully aligned to where packaging is manufactured. |

Looking across the three figures, the range is mostly created by differences in what is counted as packaging spend and how the demand pool is tied back to actual vehicle builds. By keeping assumptions traceable to clear volume and pricing drivers, the estimate stays easier to reproduce and easier to update when the market shifts.

Key Questions Answered in the Report

What is the current size of the automotive power module packaging market?

The market reached USD 3.55 billion in 2026 and is projected to grow to USD 4.85 billion by 2031.

Which module type leads revenue share today?

Intelligent Power Modules held 37.85% of 2025 revenue, serving cost-sensitive EV and hybrid platforms.

Why is the 601-1200 V power-rating segment expanding fastest?

Automakers are migrating to 800 V architectures that reduce charging time, driving 6.84% CAGR in this voltage band.

How do wire-bondless packages improve performance?

They lower parasitic inductance and enhance thermal paths, supporting high-temperature SiC and GaN devices.

Which region dominates the market?

Asia-Pacific held a 56.80% share in 2025 due to integrated EV and semiconductor manufacturing ecosystems.

What restrains faster market growth?

High SiC substrate costs and fragmented qualification standards extend product development cycles and limit capacity expansion.

Page last updated on: