Power Module Packaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 3.01 Billion |

| Market Size (2031) | USD 4.78 Billion |

| Growth Rate (2026 - 2031) | 9.69% CAGR |

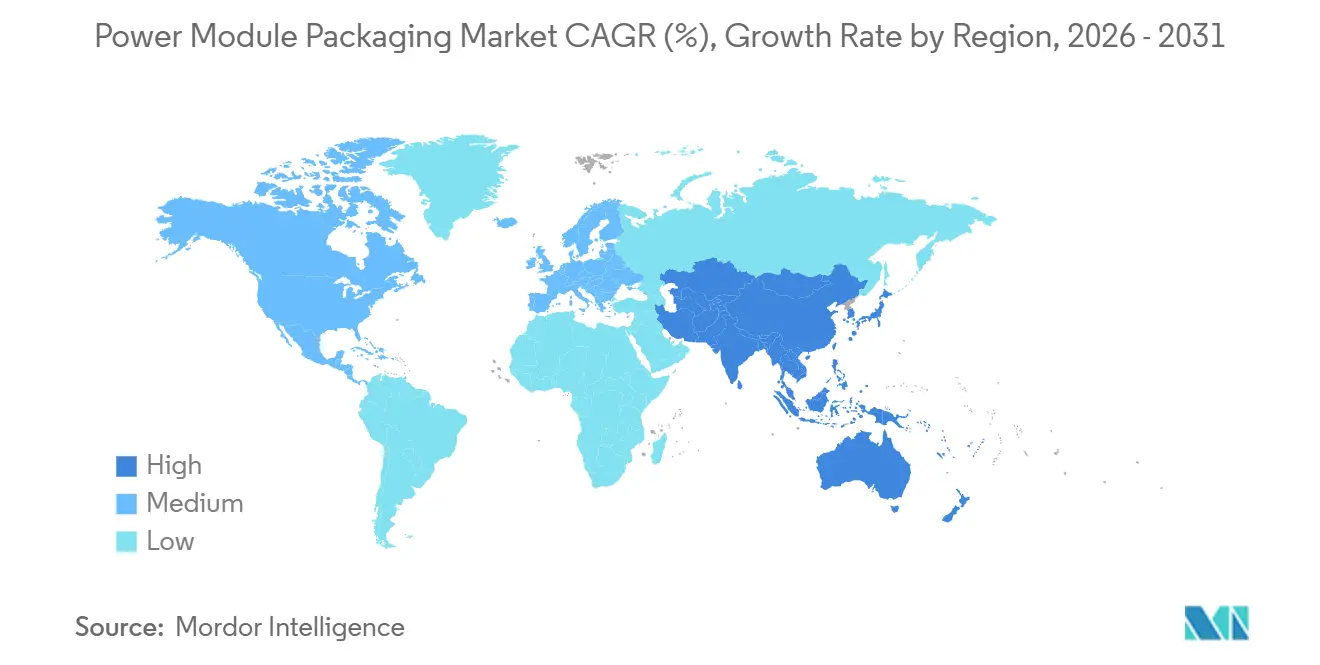

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

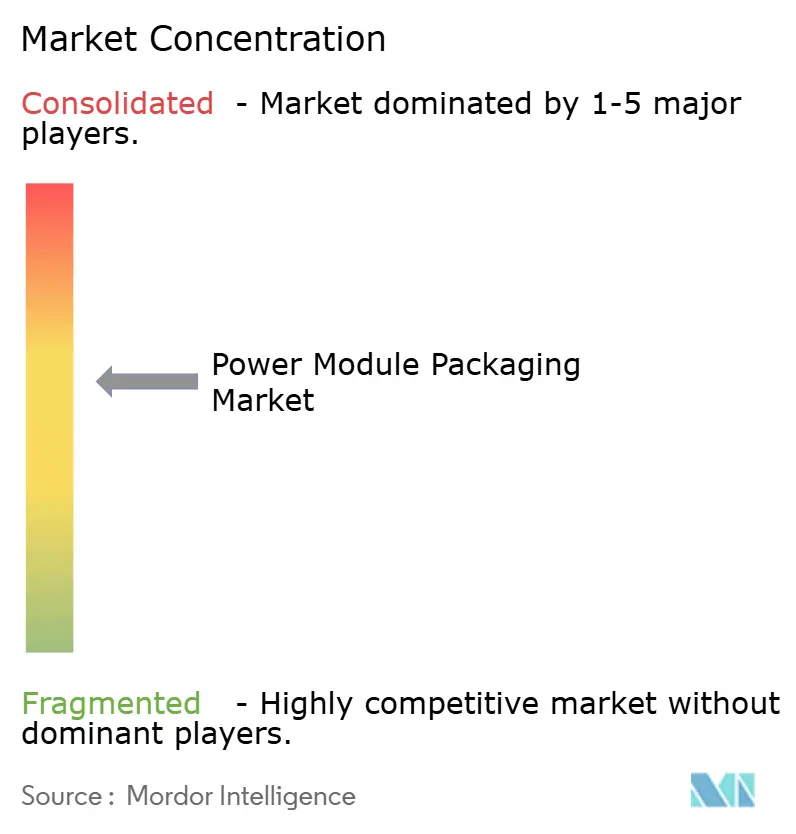

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Power Module Packaging Market Analysis by Mordor Intelligence

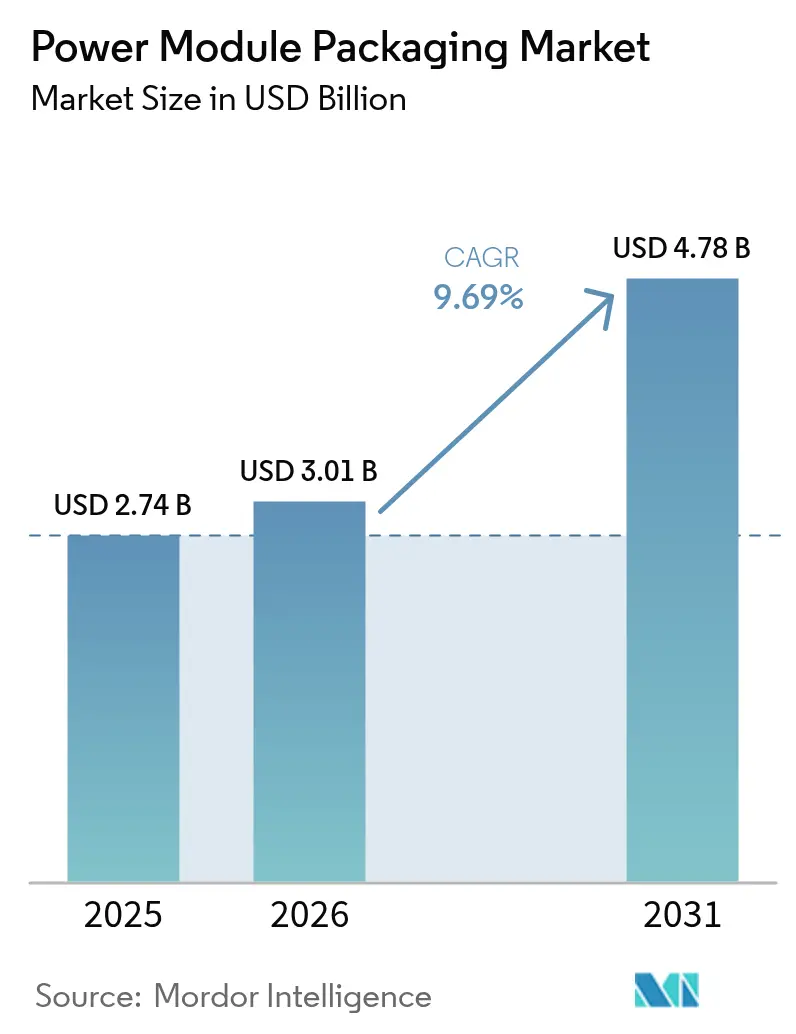

The power module packaging market size is projected to be USD 2.74 billion in 2025, USD 3.01 billion in 2026, and reach USD 4.78 billion by 2031, growing at a CAGR of 9.69% from 2026 to 2031. Momentum comes from electric-vehicle traction inverters that favor wide-bandgap devices, the fast build-out of multi-megawatt renewable-energy inverters, and industrial motor-drive upgrades that demand stringent thermal management. Suppliers are scaling double-sided-cooling substrates, adopting copper-sintering die attach, and localizing ceramic supply chains to cut lead times. The competitive focus has shifted toward reducing junction-to-case thermal resistance, automating X-ray inspection for ISO 26262 traceability, and securing aluminum nitride feedstock to avoid capacity bottlenecks.

Key Report Takeaways

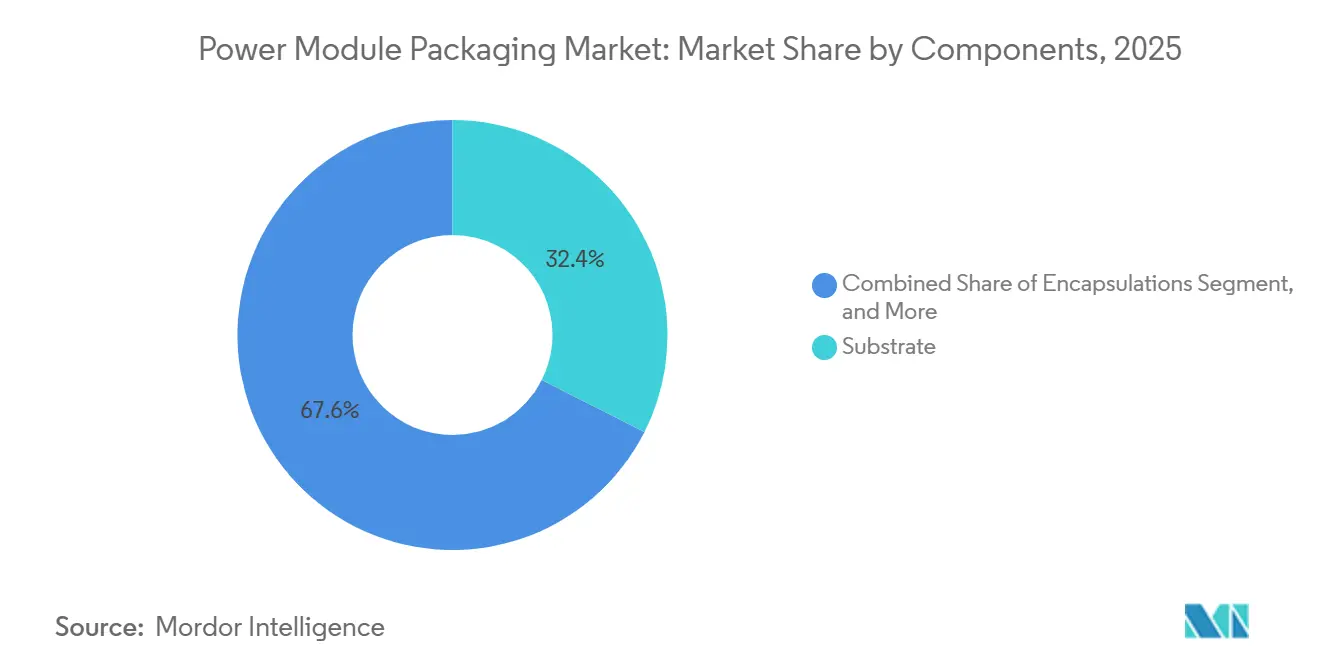

- By components, substrates led with 32.44% of 2025 revenue, while encapsulations are advancing at an 11.07% CAGR through 2031.

- By power device type, silicon-carbide modules accounted for 36.78% of the power module packaging market share in 2025; gallium-nitride modules are forecast to post a 10.66% CAGR through 2031.

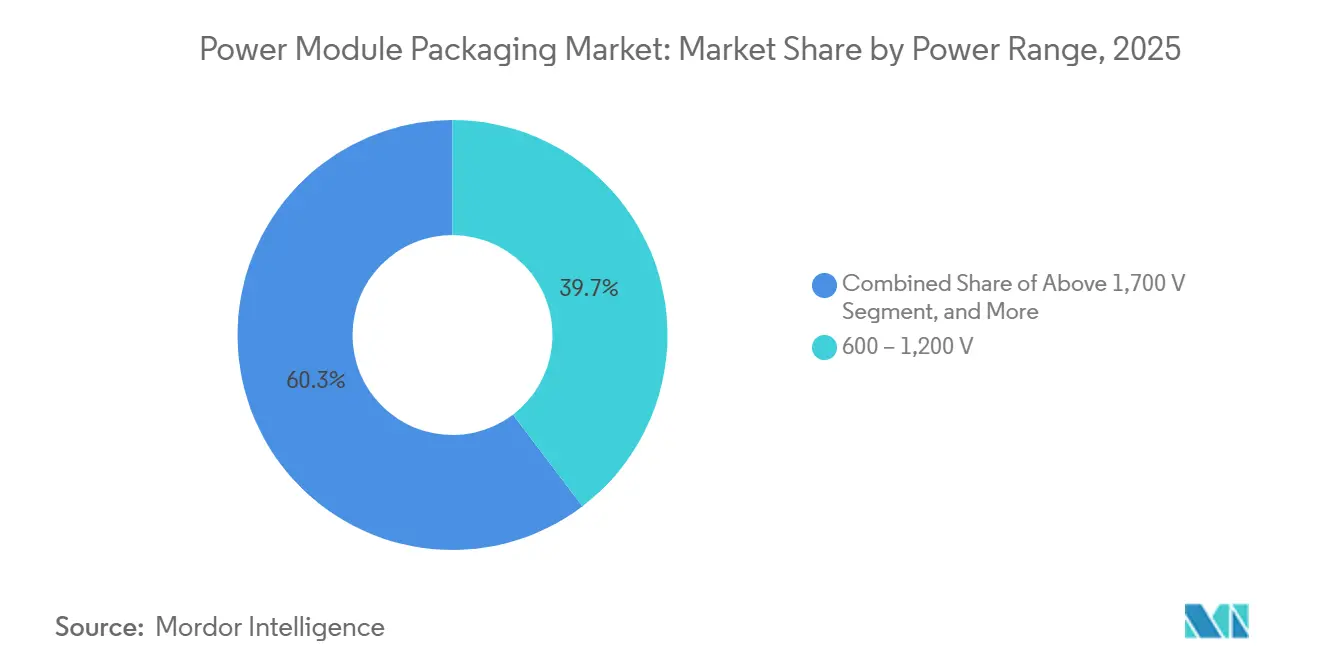

- By power range, the 600-to-1200-volt class captured 39.67% of the power module packaging market share in 2025, whereas modules above 1700 volts are expanding at a 10.47% CAGR through 2031.

- By end-user, automotive applications accounted for 48.36% of 2025 demand; renewable energy was the fastest-growing end-user, with a 11.29% CAGR through 2031.

- By geography, Asia-Pacific commanded 44.89% of global revenue in 2025 and is on track for a 10.62% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Power Module Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating adoption of SiC and GaN power devices in EV traction inverters | +2.8% | China, United States, Germany | Medium term (2-4 years) |

| Growing demand for energy-efficient industrial motor drives | +2.1% | Europe and Asia-Pacific manufacturing hubs | Long term (≥4 years) |

| Expansion of renewable-energy-linked high-power inverters | +1.9% | India, United States, Germany, offshore wind in Europe | Medium term (2-4 years) |

| Miniaturization mandate from on-board chargers in e-mobility fleets | +1.5% | North America, Europe, China | Short term (≤2 years) |

| Emergence of double-sided-cooling substrates lowering thermal resistance | +1.2% | Asia-Pacific core, spillover to North America and Europe | Medium term (2-4 years) |

| Localization policies in Asia boosting domestic packaging supply chains | +0.9% | China, India, Japan, South Korea | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Accelerating Adoption of SiC and GaN Power Devices in EV Traction Inverters

Electric-vehicle platforms built around 800-volt batteries now favor silicon-carbide and gallium-nitride modules because they shrink inverter losses and extend driving range by 5-7% per charge cycle.[1]Wolfspeed, “SiC Substrate Capacity Expansion,” wolfspeed.com Infineon reported a 65% year-over-year surge in CoolSiC automotive shipments during 2025 as European and Chinese original-equipment manufacturers ramped production. Packaging for these wide-bandgap devices must withstand 175 °C junction temperatures, so suppliers are moving to direct-bonded copper on aluminum-nitride substrates that deliver thermal conductivities above 200 W/m-K. Transient-liquid-phase sintering is displacing traditional solders because it forms high-strength intermetallics that endure 1,000 thermal cycles. ISO 26262 traceability rules now cap die-attach voids at 5%, forcing assemblers to invest in automated X-ray systems that cost over USD 500,000 per line.

Growing Demand for Energy-Efficient Industrial Motor Drives

Industrial motors draw about 45% of global electricity, and the IEC’s IE4 and IE5 classes mandate inverter topologies that limit switching losses. Parasitic inductance above 10 nH degrades efficiency, prompting modules to position the die within 2 mm of the baseplate terminals and replace wire bonds with copper clips.[2]International Electrotechnical Commission, “IE4 and IE5 Efficiency Classes,” iec.ch Mitsubishi’s J-series, released in 2025, embeds on-chip thermal sensors and exceeds 1 million power cycles per IEC 60747-9, easing downtime concerns for pump and compressor plants. Silicon-carbide MOSFET drives also fit legacy control cabinets, letting factories upgrade without rewiring mains feeds. As energy costs climb in Europe and Asia-Pacific, procurement teams specify packaging that can document lifetime reliability at switching frequencies above 20 kHz.

Expansion of Renewable-Energy-Linked High-Power Inverters

Utility-scale solar parks and offshore wind farms now deploy 5-8 MW central inverters that operate outdoors for 25 years, requiring power modules to withstand daily swings in ambient temperature from −40 °C to 85 °C. Double-sided cooling baseplates halve thermal resistance versus single-sided designs, enabling air-cooled operation in India’s desert projects. North Sea developers specify encapsulants with salt-fog resistance and moisture-ingress rates below 0.1%, driving silicone-gel innovation. To win tenders that emphasize levelized-cost reductions, module makers are extending warranties to 15 years and sharing field-failure data across the supply chain. The need to certify inverters under IEC 62109 further raises the bar for thermal-cycling and partial-discharge performance.

Miniaturization Mandate from On-Board Chargers in E-Mobility Fleets

Automakers shifting to 11 kW and 22 kW on-board chargers restrict enclosure volume to under 3 L and weight to below 5 kg to protect cabin space. Gallium-nitride HEMTs switching at 500 kHz enable power densities above 5 kW/L but demand low parasitic capacitance packaging to pass CISPR 25 electromagnetic-interference tests. ROHM’s 650 V GaN module, introduced in 2025, integrates gate drivers and current sensing in a 45 mm × 35 mm outline, reducing PCB area by 40%. Bidirectional vehicle-to-grid operation exposes modules to 1,200 V transients, so encapsulations now incorporate varistors and match PCB coefficients of thermal expansion within 5 ppm/°C. Fleet operators accept price premiums because a single charger failure can strand a vehicle and add USD 1,000 in towing costs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capex requirements for advanced packaging equipment | -1.4% | Global, acute for tier-2/3 assemblers | Short term (≤2 years) |

| Margin squeeze caused by market consolidation among tier-1 OSATs | -1.1% | Asia-Pacific outsourced assembly hubs | Medium term (2-4 years) |

| Reliability concerns over new lead-free die-attach materials above 200 °C | -0.8% | North America, Europe, Japan | Medium term (2-4 years) |

| Supply bottlenecks for high-thermal-conductivity ceramics AlN and Si₃N₄ | -0.7% | Global, dependent on Japan and Germany | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

High Capex Requirements for Advanced Packaging Equipment

Building a wide-bandgap module line requires vacuum reflow ovens, pressure-assisted sintering presses, and inline X-ray systems, pushing upfront investment above USD 5 million per line.[3]SEMI, “Advanced Packaging Equipment Market 2025,” semi.org Lead times stretched to 18 months in 2025 as Japanese motion-control suppliers fell behind on servo deliveries, delaying expansions in Malaysia and Thailand. Banks now demand ISO 9001 certification and customer letters of intent before releasing loans, a hurdle that sidelines tier-3 assemblers. Rapid technology shifts toward transient-liquid-phase bonding risk stranding today’s equipment within five years. Shared-line consortia exist, but concerns about intellectual property leakage limit uptake.

Margin Squeeze Caused by Market Consolidation among Tier-1 OSATs

Amkor’s 2024 European acquisition and ASE’s automotive push cut gross margins on standard silicon modules to 18% in 2025. The top five outsourced-assembly-and-test providers now control 60% of global capacity, letting them dictate payment terms and minimum order quantities. Consignment models, in which OEMs own the die, further erode OSAT's value capture and shift pricing power upstream. Niche players eye the aerospace and rail markets, but securing AS9100 and MIL-STD-883 certifications can take 2 years and cost millions of dollars. As vertical integration deepens, smaller houses struggle to access aluminum nitride substrates at competitive prices, further compounding the margin squeeze.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Components: Encapsulation Innovation Outpaces Substrate Maturity

Substrates accounted for 32.44% of the power module packaging market share in 2025, underscoring their role as the structural link that provides both electrical isolation and thermal conduction between the die and the baseplate. Baseplates are shifting from copper to aluminum-silicon-carbide composites, a move that trims weight by 35% while maintaining coefficients of thermal expansion compatible with ceramic layers. Encapsulations, however, are on track for an 11.07% CAGR through 2031 because new silicone gels resist partial-discharge stress above 10 kV/mm, meeting the rail and offshore-wind specifications that dominate recent tenders.

Sintered-silver and copper transient-liquid-phase die attach are replacing leaded solders, forming intermetallic bonds that survive 1,000 cycles between −40 °C and 200 °C. Substrate-attach layers now rely on nano-silver pastes that cure at 250 °C and eliminate voids larger than 50 µm, a critical safeguard for automotive modules qualified under ISO 26262. Copper-clip or ribbon interconnections cut loop inductance below 10 nH, enabling higher switching frequencies in the power module packaging market. Phase-change thermal-interface films that liquefy at 60 °C post 30% lower resistance than greases, and UV-curable potting compounds slash takt time to keep pace with just-in-time schedules. These advances position encapsulation and interconnection suppliers as prime beneficiaries of next-generation module designs.

By Power Device Type: GaN Modules Gain Ground as SiC Matures

Silicon-carbide modules held 36.78% of 2025 revenue, reaffirming their dominance in traction inverters and 50 kW-plus industrial drives. Gallium-nitride modules, meanwhile, are forecast to grow at a 10.66% CAGR through 2031 as automakers and cloud providers prioritize miniaturization and high-frequency operation. Traditional insulated-gate bipolar transistor modules still compete in legacy rail and heavy-industry systems, yet their share continues to erode as SiC offers 2-3 percentage-point gains in system efficiency.

ROHM’s 650 V GaN module achieves power densities above 6 kW/L, highlighting how integrated gate drivers and current sensors can reduce board area by 40% without compromising reliability. Trench-gate SiC architectures now trim on-resistance 20%, letting 1,200 V devices carry 400 A continuous current while staying below 150 °C junction limits. The power module packaging market size for silicon MOSFET modules is under price pressure as low-cost Chinese vendors crowd the sub-USD 5 segment. Suppliers counter by bundling drivers, sensors, and embedded diagnostics to retain value. Edge-field stress management in wide-bandgap die is pushing encapsulant makers toward materials with volume resistivities above 10¹⁴ Ω-cm, tightening collaboration across the value chain.

By Power Range: Ultra-High-Voltage Modules Serve Grid and Rail

The 600-to-1,200-V class captured 39.67% of 2025 revenue, reflecting its tight fit with 400 V and 800 V electric-vehicle architectures that enable 350 kW fast charging. Modules above 1,700 V are expanding at a 10.47% CAGR as China and Japan upgrade to 3,300 V silicon-carbide traction converters for high-speed rail. Sub-600 V modules remain core to 48 V data-center distribution even as consumer electronics commoditize.

Packaging ultra-high-voltage die introduces creepage and clearance challenges because IEC 60664 specifies at least 8 mm between 3,300 V live terminals, so designers stack substrates vertically to keep footprints compact. Mitsubishi’s X-series uses ceramic spacers rated at 20 kV/mm to house 3,300 V devices in a 140 mm × 190 mm outline, illustrating how material advances unlock higher system voltages. Standard 62 mm EconoDUAL packages dominate the mid-range, speeding design cycles and supply-chain logistics in the power module packaging market. Embedded-die board-in-package concepts cut assembly costs by 25% for sub-600 V applications and support the rising demand for compact smart chargers. Together, these trends widen the performance envelope without sacrificing manufacturability.

By End-User: Automotive Leads, Renewables Accelerate

Automotive customers absorbed 48.36% of 2025 demand, driven by a 40 million-unit electric-vehicle fleet and the widespread adoption of 800 V platforms that require modules capable of 200 kW continuous power. Renewable-energy developers are the fastest movers, with an 11.29% CAGR linked to India’s 15 GW-per-year solar pipeline and Europe’s offshore wind farms that specify double-sided-cooling designs for 25-year lifetimes. Industrial motor drives form a resilient foundation as factories replace aging variable-frequency drives with silicon-carbide models that meet the IE5 efficiency class.

Data centers and telecom operators now deploy 48 V bus converters demanding 3,000 A continuous current and fault-tolerant operation, creating white-space opportunities for high-density packaging. Rail and mass-transit buyers insist on 30-year modules certified under EN 50155, while aerospace customers pay premiums for radiation-hardened versions qualified to MIL-STD-883. Consumer electronics adopt GaN fast-charging modules that deliver 100 W in cubes under 50 cm³, validating high-volume potential despite tight margins. The diverse application mix shields the power module packaging market share from cyclical swings in any single vertical.

Geography Analysis

Asia-Pacific generated 44.89% of global revenue in 2025 and is projected to advance at a 10.62% CAGR through 2031, anchored by China’s target to source 70% of substrates and encapsulants domestically by 2027 and India’s USD 10 billion electronics production-linked incentive that subsidizes clean-room buildouts. Japan’s ceramic-substrate leadership and South Korea’s gallium-nitride epitaxy investments reinforce a self-sufficient supply chain, while Malaysia and Thailand attract tier-1 outsourced assemblers seeking proximity to regional electric-vehicle plants. These moves compress prototype lead times from 12 weeks to six, yet diverging national quality codes complicate cross-border IEC and UL compliance. The power module packaging market is therefore expanding fastest where localization policies and automotive demand overlap.

North America benefits from a 30% investment tax credit under the Inflation Reduction Act, prompting Wolfspeed to scale a North Carolina silicon-carbide module fab and ON Semiconductor to commit USD 2 billion to New Hampshire assembly lines. Mexico is becoming Detroit’s back-end shop as suppliers open lines in Monterrey to serve Ford and General Motors, and Canada leverages aluminum and copper reserves to supply baseplate feedstock. Public–private consortia funded by the CHIPS and Science Act are also prototyping heterogeneous integration of embedded gate drivers. Together, these incentives lift regional manufacturing content and help U.S. original-equipment manufacturers derisk Asian ceramic shortages.

Europe’s Green Deal ban on new internal-combustion cars after 2035 forces automakers to validate silicon-carbide traction modules with verified carbon footprints below 50 kg CO₂ per unit. Germany’s ISO 26262 ASIL-D traceability demands inline X-ray inspection of every die attach, and the United Kingdom’s 40 GW offshore-wind pipeline needs 6.6 kV salt-fog-proof modules. France’s nuclear-reactor modernization and Italy’s 25-year financing for solar projects round out demand for long-life devices, while the Middle East and Africa add niche growth, with solar-powered desalination plants specifying 55 °C-rated packages. These projects sustain the power module packaging market share in EMEA even as regional labor costs rise.

Competitive Landscape

The power module packaging market shows moderate concentration: the ten largest vendors hold about 55% of global revenue, yet no single firm exceeds 25%, keeping rivalry lively. Infineon and Mitsubishi integrate substrate fabrication, die attach, and final test under one roof, reducing thermal-resistance variability by 10% and securing a scarce supply of aluminum nitride. In response, Amkor and ASE bundle substrate build-up with wide-bandgap die assembly, leveraging their footprint in Malaysia, the Philippines, and Germany to win automotive programs that favor ISO 26262-certified multi-site capacity.

White-space opportunities arise in 48 V data-center converters, bidirectional vehicle-to-grid chargers, and aerospace modules that must pass MIL-STD-883, segments where the incumbent high-volume houses lack tailored qualifications. Smaller specialists pivot to these niches and charge >30% gross margins once AS9100 or EN 50155 certifications are complete. Patent trends from 2025 show a pivot toward embedded-die board-in-package and transient-liquid-phase sintering, which drops junction-to-case resistance below 0.1 K/W, with the strongest portfolios held by Infineon, Wolfspeed, and STMicroelectronics.

Market consolidation continues to squeeze tier-2 assemblers; the top five outsourced-assembly-and-test players now command 60% of automotive-qualified capacity and can impose 90-day payment terms. Consignment models shift die ownership to original-equipment manufacturers, eroding OSAT pricing power and compelling investment in automation to defend margins. Localization policies complicate strategy: China requires technology transfer for market entry, while India mandates majority local content, pushing multinationals to form joint ventures that dilute intellectual property yet unlock volume. As a result, the power module packaging market size is growing, but supplier profit pools hinge on mastering both regional compliance and next-generation thermal architectures.

Power Module Packaging Industry Leaders

-

Infineon Technologies AG

-

Mitsubishi Electric Corporation

-

Fuji Electric Co. Ltd

-

Hitachi Ltd

-

STMicroelectronics N.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Infineon Technologies began production at its USD 2.7 billion SiC module plant in Kulim, Malaysia, targeting 10 million automotive units annually by late 2027 and integrating double-sided-cooling substrates with <0.1 K/W resistance.

- January 2026: Wolfspeed and ZF Friedrichshafen agreed to co-design 800 V traction modules using fourth-generation SiC MOSFETs, with series qualification slated for 2027 model-year vehicles.

- December 2025: Mitsubishi Electric launched X-series 3 300 V SiC modules for high-speed rail, featuring 20 kV/mm dielectric ceramic spacers and 30-year lifetimes under EN 50155.

- November 2025: ON Semiconductor finished a USD 400 million SiC packaging expansion in Rožnov, Czech Republic, adding pressure-sintering and automated X-ray lines for European EV customers.

Global Power Module Packaging Market Report Scope

The Power Module Packaging Market Report is Segmented by Components (Substrate, Baseplate, Die Attach, Substrate Attach, Encapsulations, Interconnections, Other Components), Power Device Type (IGBT Modules, Si-MOSFET Modules, SiC Modules, GaN Modules, Other Power Device Types), Power Range (Below 600 V, 600-1200 V, 1,200-1,700 V, Above 1,700 V), End-User (Automotive, Industrial, Renewable Energy, Consumer Electronics, Data Centres and Telecom, Rail and Transportation, Aerospace and Defence, Other End-Users), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Substrate |

| Baseplate |

| Die Attach |

| Substrate Attach |

| Encapsulations |

| Interconnections |

| Other Components |

| IGBT Modules |

| Si-MOSFET Modules |

| SiC Modules |

| GaN Modules |

| Other Power Device Types |

| Below 600 V |

| 600 – 1,200 V |

| 1,200 – 1,700 V |

| Above 1,700 V |

| Automotive |

| Industrial |

| Renewable Energy |

| Consumer Electronics |

| Data Centres and Telecom |

| Rail and Transportation |

| Aerospace and Defence |

| Other End-Users |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Components | Substrate | ||

| Baseplate | |||

| Die Attach | |||

| Substrate Attach | |||

| Encapsulations | |||

| Interconnections | |||

| Other Components | |||

| By Power Device Type | IGBT Modules | ||

| Si-MOSFET Modules | |||

| SiC Modules | |||

| GaN Modules | |||

| Other Power Device Types | |||

| By Power Range | Below 600 V | ||

| 600 – 1,200 V | |||

| 1,200 – 1,700 V | |||

| Above 1,700 V | |||

| By End-User | Automotive | ||

| Industrial | |||

| Renewable Energy | |||

| Consumer Electronics | |||

| Data Centres and Telecom | |||

| Rail and Transportation | |||

| Aerospace and Defence | |||

| Other End-Users | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Rest of Europe | |||

| Asia Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the power module packaging market?

The power module packaging market size will reach USD 3.01 billion in 2026 and is projected to hit USD 4.78 billion by 2031.

Which component segment is growing the fastest?

Encapsulations are set to grow at an 11.07% CAGR through 2031 as silicone-gel formulations with high partial-discharge resistance gain traction.

Why are silicon-carbide modules important for electric vehicles?

Silicon-carbide modules cut inverter losses, allow 800-V architectures, and extend driving range, which is why they held 36.78% of 2025 revenue.

Which region leads demand for power module packaging?

Asia-Pacific accounted for 44.89% of 2025 revenue and is forecast to grow at a 10.62% CAGR thanks to strong EV production and localization incentives.

How is equipment cost affecting smaller assemblers?

Advanced packaging lines cost over USD 5 million, and long lead times plus tighter lending rules are squeezing tier-2 and tier-3 providers.

What trends influence renewable-energy inverter packaging?

Adoption of double-sided-cooling substrates and salt-fog-resistant encapsulations enables 5-8 MW solar and offshore wind inverters to meet 25-year life targets.

Page last updated on: