Intelligent Power Module (IPM) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

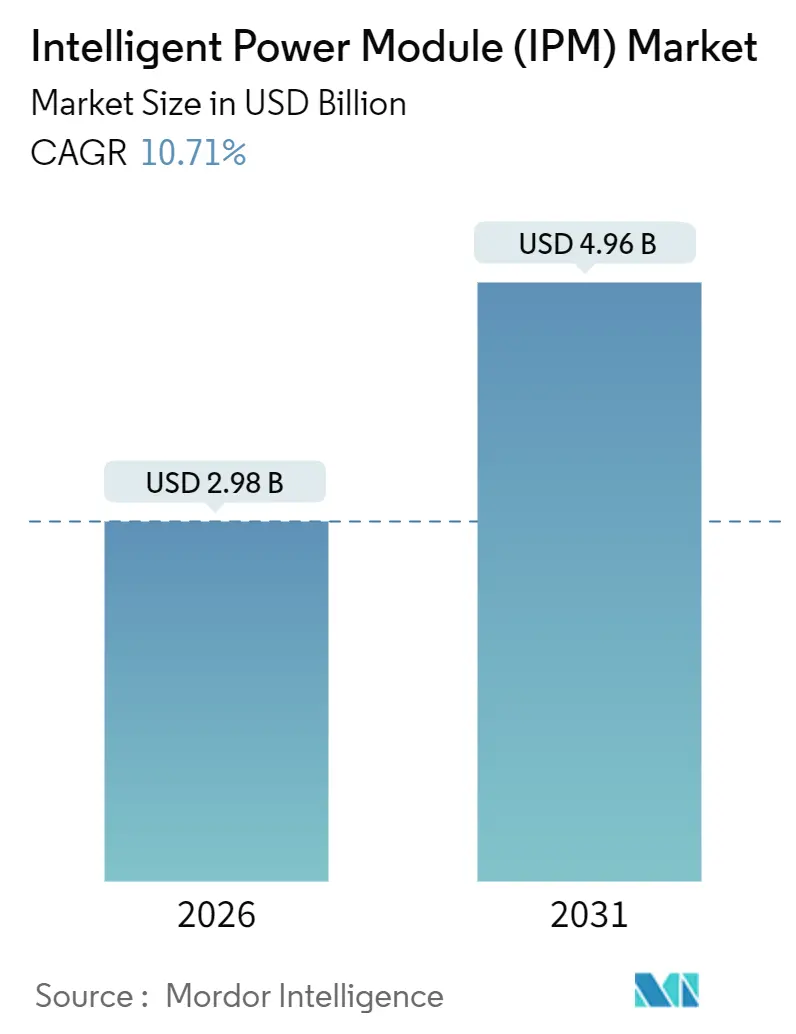

| Market Size (2026) | USD 2.98 Billion |

| Market Size (2031) | USD 4.96 Billion |

| Growth Rate (2026 - 2031) | 10.71% CAGR |

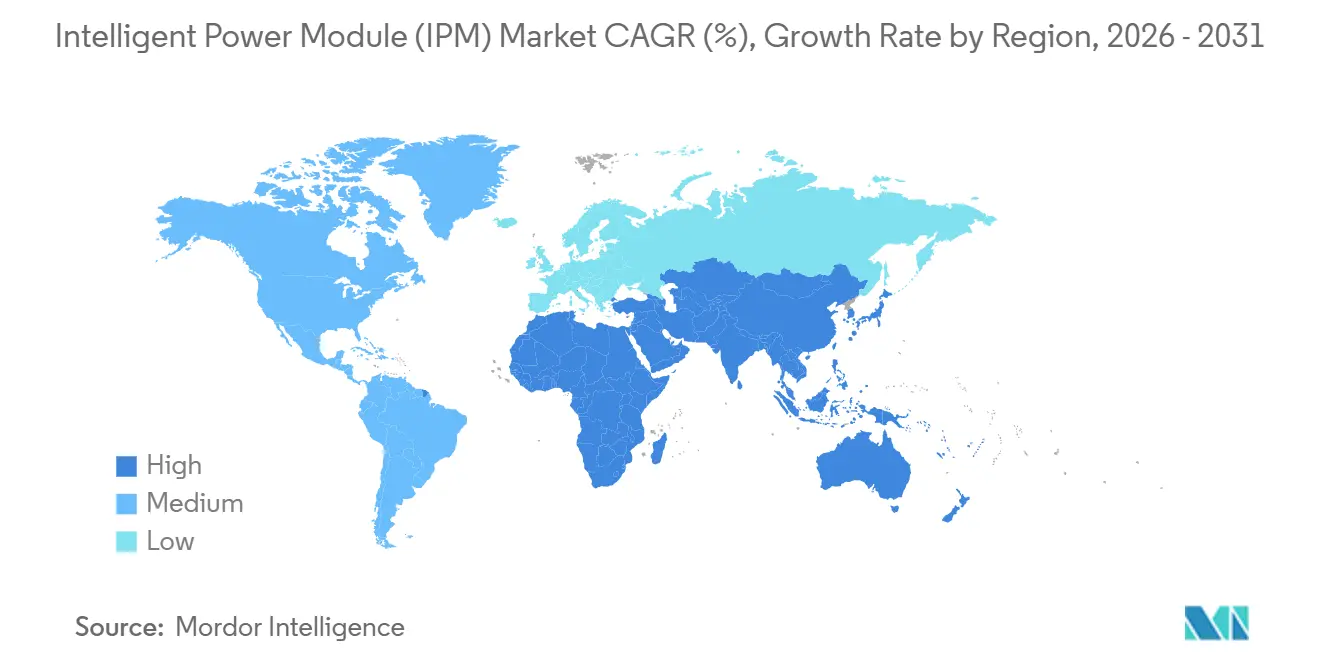

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

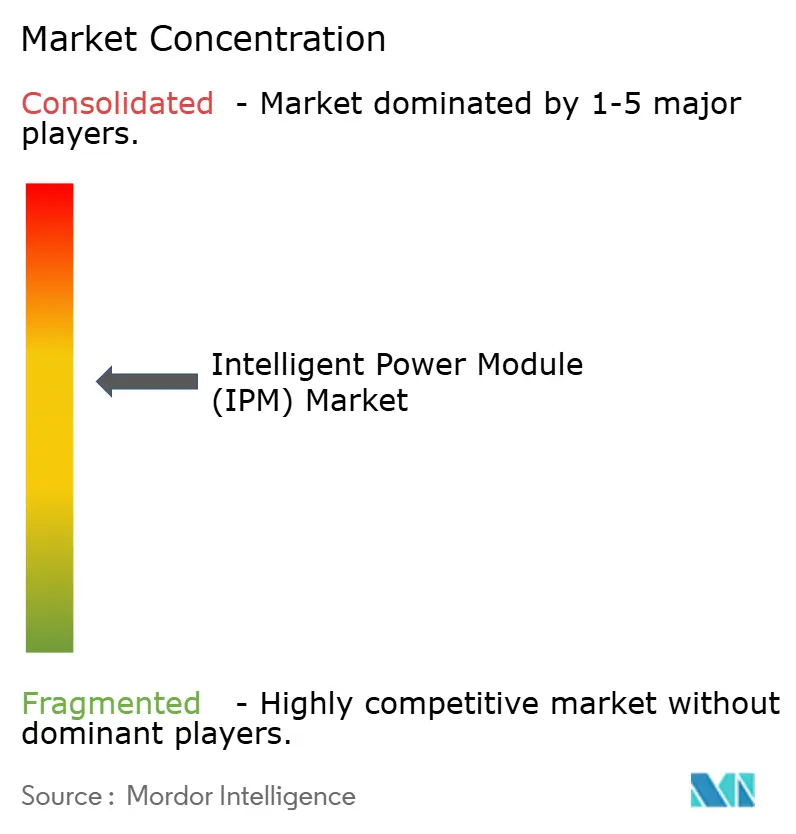

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Intelligent Power Module (IPM) Market Analysis by Mordor Intelligence

The intelligent power module market size reached USD 2.98 billion in 2026 and is projected to climb to USD 4.96 billion by 2031, advancing at a 10.71% CAGR. Continued conversion to silicon-carbide traction inverters, factory servo-drive retrofits, and tighter standby-power regulations across major economies keep demand robust. Automotive programs that standardize 800 V battery packs, European industrial retrofits prompted by energy-efficiency mandates, and Middle Eastern solar buildouts together underpin growth. Supply-side momentum is equally strong, as the leading vendors ramp 200-millimeter wafer lines and expand ceramic-substrate capacity to ease bottlenecks. Competition remains balanced: the top five suppliers controlled 55% of 2025 revenue, yet regional entrants still find room in low-current segments.

Key Report Takeaways

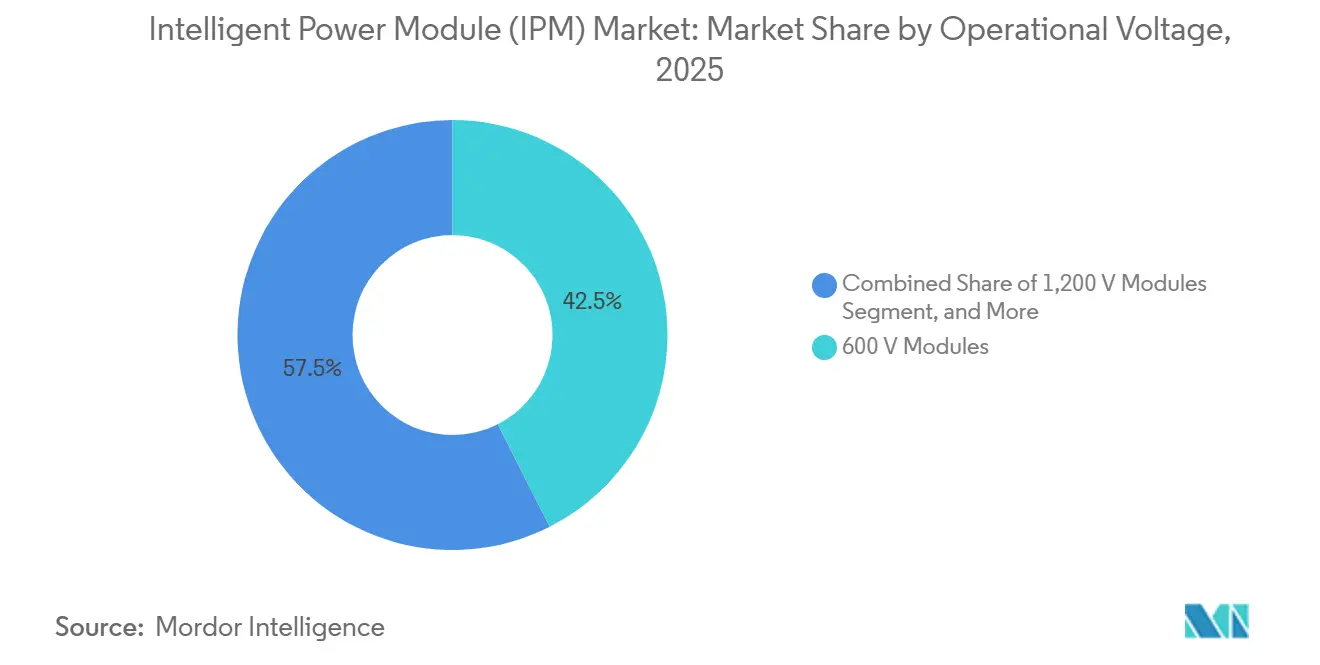

- By operational voltage, 600 V modules led with a 42.53% revenue share in 2025, while 1200 V variants are forecast to grow at an 11.26% CAGR through 2031.

- By power device, IGBT designs commanded 64.81% of 2025 revenue; silicon-carbide MOSFET modules are projected to expand at an 11.95% CAGR over the same period.

- By substrate material, direct-bonded-copper ceramic held the largest 2025 share at 38.19%, whereas silicon-nitride ceramic is set to post an 11.46% CAGR to 2031.

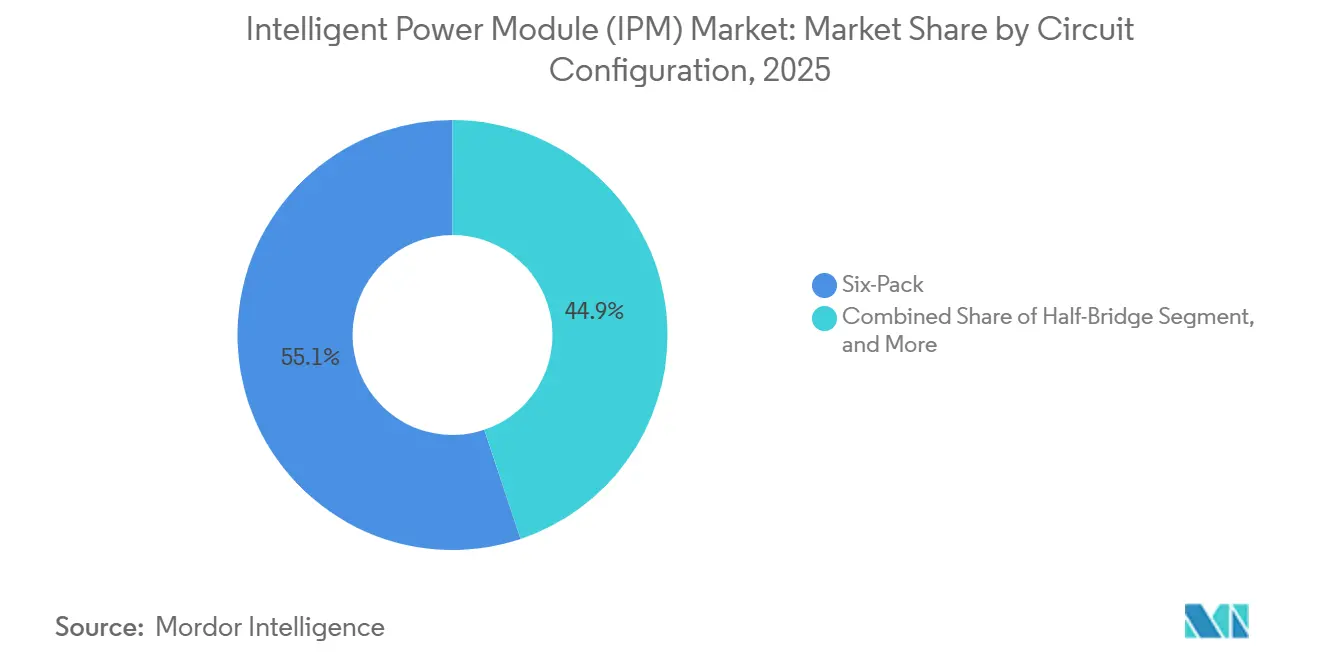

- By circuit configuration, six-pack modules captured 55.14% of revenue in 2025; seven-pack modules are the fastest expanding, at an 11.78% CAGR.

- By current rating, above-100 A modules represented the highest growth trajectory at a 12.04% CAGR, although the up-to-50 A bracket remained the largest in 2025.

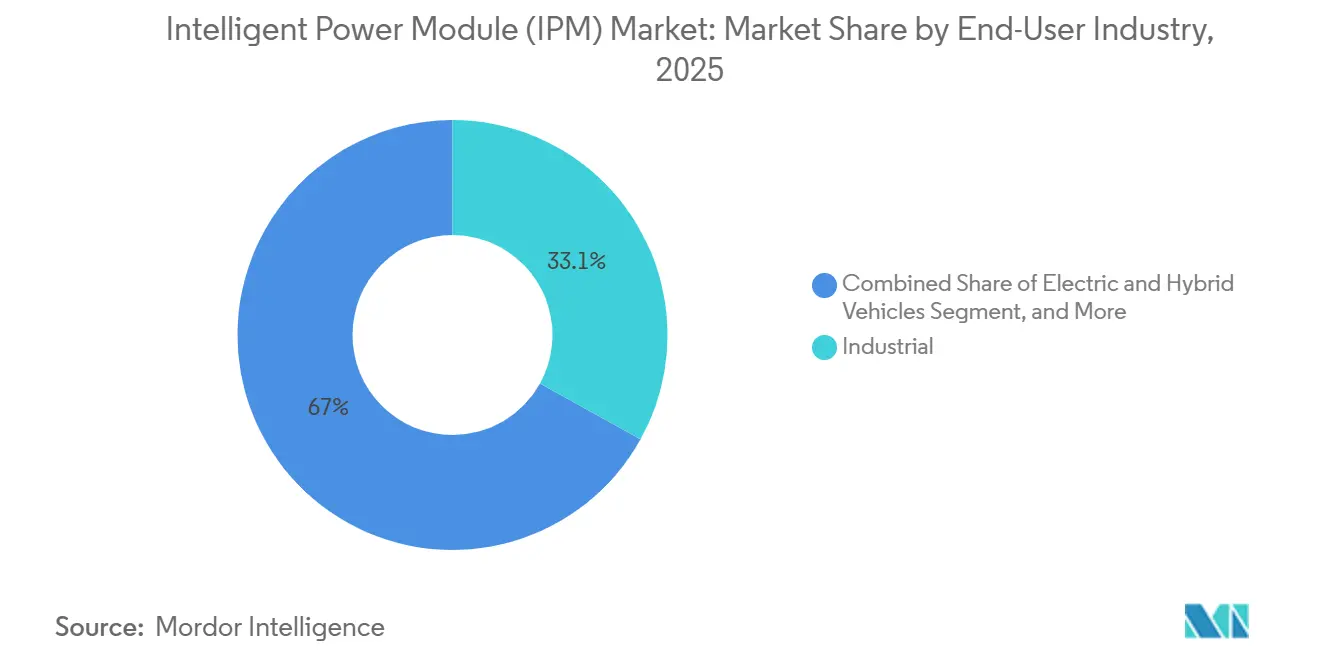

- By end-use industry, industrial automation and servo drives led with a 33.05% share in 2025, while electric and hybrid vehicles will register a 12.22% CAGR and overtake industrial after 2029.

- By sales channel, OEM shipments dominated at 78.82% in 2025; aftermarket and retrofit demand is poised for an 11.09% CAGR through 2031.

- By geography, Asia Pacific contributed 46.74% of 2025 revenue; the Middle East is projected to record the fastest regional CAGR at 12.45% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Market Trends and Insights

Drivers Impact Analysis of Intelligent Power Module (IPM) Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in SiC-based IPMs for high-efficiency EV inverters in China | +2.10% | China, APAC core with spill-over to Europe | Medium term (2-4 years) |

| Rapid adoption of IPM servo drives in European Industry 4.0 retrofits | +1.80% | Germany, France, Italy, Central Europe | Short term (≤ 2 years) |

| On-board charger integration trend among tier-1 automotive OEMs | +1.50% | Global, concentrated in North America, Europe, China | Medium term (2-4 years) |

| Regulatory push for ultra-low-standby home appliances in North America | +1.30% | United States, Canada | Short term (≤ 2 years) |

| Solar micro-/nano-inverter build-outs boosting 600 V IPM demand in the US | +1.20% | United States, with early adoption in California, Texas | Medium term (2-4 years) |

| Digital-twin-enabled predictive thermal management for high-power IPMs | +0.90% | Global, led by automotive and rail-traction segments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in SiC-Based IPMs for High-Efficiency EV Inverters in China

China produced 9.5 million battery-electric vehicles in 2025, and roughly 40% of new models adopted silicon-carbide modules to boost range beyond 500 kilometers. BYD reported a 32% inverter-loss reduction against silicon IGBT baselines, translating to another 25 kilometers of driving range. Subsidies introduced by the Chinese Ministry of Industry and Information Technology pay an extra CNY 3,000 per vehicle when traction inverters exceed 97% efficiency, a target currently feasible only with SiC modules.[1]Ministry of Industry and Information Technology, “New Energy Vehicle Subsidy Framework 2025,” Miit.gov.cn Tier-one suppliers doubled module capacity to chase the incentive, yet wafer shortages stretched lead times to 18 weeks, reinforcing SiC’s pull-through momentum.

Rapid Adoption of IPM Servo Drives in European Industry 4.0 Retrofits

European manufacturers upgraded about 180,000 machine tools with IPM servo drives in 2025, a 35% jump over 2024, as the average German industrial power price doubled versus 2020.[2]European Committee for Standardization, “Industrial Automation Technical Committee Report 2025,” Cencenelec.eu The EU Machinery Regulation 2023/1230 obliges IE4-level motor efficiency from 2026 onward, and IPM servo kits slash installation time from eight hours to 90 minutes. Siemens recorded a 42% year-on-year order spike for its SINAMICS retrofit packages in Q3 2025, with strongest traction among automotive suppliers and food processors.[3]Siemens AG, “Q3 2025 Earnings Call Transcript,” Siemens.com Quick commissioning and embedded protections make IPM kits attractive for small machine builders lacking in-house power-electronics expertise.

On-Board Charger Integration Trend Among Tier-1 Automotive OEMs

In 2025, 22% of fresh EV platforms embedded the on-board charger inside the battery pack, eliminating a separate housing. A Munro and Associates teardown found that the integrated charger saves 3.2 kilograms of wiring and 1.8 liters of underbody volume. Stellantis adopted Infineon’s 11 kW CoolSiC-based IPM charger on its STLA Medium platform to meet vehicle-to-grid needs at 95% round-trip efficiency. Tighter CISPR 25 Class 5 limits on conducted emissions favour the compact architecture, and suppliers such as Valeo co-design gate resistors for each OEM’s DC-link capacitance, cutting time-to-market by six months.

Regulatory Push for Ultra-Low-Standby Home Appliances in North America

The U.S. Department of Energy lowered standby-power caps to 0.5 W for core white-goods categories in March 2025. Whirlpool responded with a front-load washer that consumes 0.42 W while idle, using a 600 V IPM from STMicroelectronics. Variable-speed compressor drives in HVAC systems face similar limits under California Title 20, and industry data suggest North American appliance OEMs will consume 28 million IPM units in 2026. The shift benefits 15 A-30 A modules that integrate zero-current shutdown logic on-chip, satisfying the new ceiling without adding external components.

Restraints Impact Analysis of Intelligent Power Module (IPM) Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Wide-band-gap wafer supply constraints | -1.60% | Global, acute in automotive and renewable-energy segments | Short term (≤ 2 years) |

| Thermal-interface reliability beyond 1200 V ratings | -0.90% | Europe, Asia Pacific rail-traction and industrial high-power applications | Medium term (2-4 years) |

| High automotive AEC-Q101 validation costs for module makers | -0.70% | Global automotive supply chain | Medium term (2-4 years) |

| IP infringement and price erosion by low-end Asian vendors | -0.50% | Asia Pacific, spill-over to price-sensitive segments globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Wide-Band-Gap Wafer Supply Constraints

Automotive and renewable-energy customers required about 3.3 million 150 mm-equivalent SiC wafers in 2025, yet output reached only 2.8 million. Wolfspeed’s new 200 mm line hit 60% of nameplate capacity by year-end because of epitaxial yield challenges. ON Semiconductor still saw 26-week lead times for 1200 V dies, three times longer than silicon alternatives. The shortage forced OEMs to postpone platform launches by up to six months and pushed some industrial users back toward silicon IGBTs for sub-50 kW drives.

Thermal-Interface Reliability Beyond 1200 V Ratings

AEC-Q101 thermal-cycling tests reveal solder-based die attaches delaminate after 2,000 cycles at 175 °C, a threshold exceeded in many 1700 V rail applications. IEEE research shows sintered-silver attaches cut thermal resistance by 40% and survive 5,000 cycles, yet the 250 °C cure can warp thin ceramic substrates. Hitachi Energy now uses hybrid attach schemes but notes a 12% manufacturing-cost penalty. Until sintered silver reaches cost parity, module makers derate 1700 V units to 150 °C maximum junction temperature, trimming usable power density.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Intelligent Power Module (IPM) Market Segment Analysis

By Operational Voltage:

Automotive Platforms Accelerate 1200 V DemandModules rated up to 600 V maintained the highest 2025 share, at 42.53% of the intelligent power module market. Residential appliances, micro-inverters, and light industrial drives dominate this bracket, benefiting from simpler insulation needs. The 1200 V class is rising fastest, with an 11.26% CAGR, as 800 V battery packs in premium EVs call for higher DC-link voltage to cut copper mass. Porsche’s 2025 Taycan update relies on 1200 V SiC IPMs to shrink inverter volume from 11 L to 7.2 L, boosting power density to 48 kW/L. IEC 62477-1 revisions in 2024 increased creepage-distance costs above 1000 V, yet OEMs find the trade-off worthwhile for range and fast-charge performance. In regional terms, North American solar and European rooftop PV installations guide 600 V module volumes, while Chinese EV makers shift towards 1200 V benchmarks.

Grid standards and safety certifications accentuate the split. The National Electrical Code caps U.S. residential PV arrays at 600 V, aligning with lower-voltage IPMs, whereas European installers increasingly use 1000 V strings that entice 1200 V module adoption. Japanese rail-traction and Indian metro projects preserve a niche for 1700 V and 3300 V devices, though these remain volume-limited. In net effect, rising automotive production ensures that the 1200 V segment captures a growing fraction of the intelligent power module market size through 2031.

By Power Device:

SiC MOSFETs Win Premium ApplicationsIGBT-based IPMs supplied 64.81% of intelligent power module market share in 2025, anchored in industrial motion control, HVAC drives, and consumer appliances where cost remains pivotal. The class enjoys a mature, global supply chain and an approximate USD 0.08 per-ampere price edge over SiC. Yet SiC MOSFET modules will post an 11.95% CAGR, drawing on their lower switching and conduction losses in EV traction inverters, on-board chargers, and energy-storage converters. Wolfspeed’s automotive revenue mix reached 68% for SiC IPMs in 2025 as 200 mm wafer yields improved.

Below 200 V, silicon MOSFET IPMs dominate server power supplies and telecom rectifiers, prized for fast reverse-recovery behaviour. GaN FET modules, still niche, doubled shipments in 2025 on laptop adapters and 48 V mild-hybrid vehicles. Thermal headroom differentiates platforms: SiC sustains 200 °C junction temperatures with sintered-silver attaches, enabling 20% higher current in the same footprint, critical for under-hood EV inverters. The technology trajectory suggests silicon-carbide will carve out the premium and automotive middle-tier, while IGBT remains entrenched in cost-sensitive industrial drives.

By Substrate Material:

Silicon-Nitride Ceramic Gains TractionDirect-bonded-copper (DBC) ceramic commanded 38.19% of 2025 revenue, split between Al₂O₃ and AlN. Al₂O₃ serves cost-sensitive drives at USD 4.50 per sq in., whereas AlN’s 170 W/m-K thermal conductivity justifies its USD 12.00 price in automotive and rail modules. Silicon-nitride (Si₃N₄) ceramic is advancing at an 11.46% CAGR because its fracture toughness doubles that of AlN, cutting substrate crack risk during thermal cycling. A 2025 European Ceramic Society study proved Si₃N₄ survives 1,000 cycles from -40 °C to 150 °C without cracking.

Insulated-metal substrates serve modules below 100 A where weight matters, and active-metal-brazed copper targets 1700 V rail devices demanding 200 W/m-K conductivity. Kyocera’s 2025 Si₃N₄ substrate offers 90 W/m-K at 40% less cost than AlN, positioning it for volume automotive adoption. Lower parasitic capacitance on ceramic substrates trims common-mode noise by 8 dB, easing CISPR 25 compliance. Supply security is emerging as an issue because Japanese and German firms dominate advanced ceramics, prompting module makers to ink long-term offtake contracts.

By Circuit Configuration:

Seven-Pack Designs Enable Three-Level InvertersSix-pack modules remained the workhorse with 55.14% of 2025 revenue, supporting three-phase motors in appliances, HVAC, and industrial automation. Seven-pack IPMs are accelerating at an 11.78% CAGR as EV and elevator OEMs adopt three-level inverters that halve output-voltage steps and curb motor-bearing currents by 60%. ABB documented a 98.2% weighted efficiency for its ACS880 drive built around a Semikron seven-pack, versus 96.8% for an equivalent two-level unit.

Half-bridge modules power photovoltaic optimizers and auxiliary converters, while the “others” group covers H-bridges and custom topologies for aerospace. Mitsubishi Electric’s seventh-generation 1200 V, 150 A seven-pack launched in 2025 embeds a CAN-FD interface, offering plug-and-play upgrades from six-packs without PCB redesign. Functional-safety benefits further support seven-pack growth because integrating gate logic on the same substrate cuts layout-induced shoot-through risks.

By Current Rating:

Above-100 A Modules Rise with High-Power EVsModules up to 50 A dominated unit volume in 2025, powering household appliances, micro-inverters, and light-duty industrial drives. Yet modules above 100 A will show a 12.04% CAGR through 2031 as EV traction inverters demand currents from 400 A to 800 A. Tesla qualifies dual 450 A SiC IPMs for Model 3 and Model Y inverters, mitigating supply shocks through dual sourcing. Delhi, Riyadh, and Jakarta metros specified 1700 V, 600 A modules to replace series-connected 3300 V stacks, simplifying gate synchronization.

Thermally, >100 A modules rely on liquid cooling; ON Semiconductor simulations demonstrate a 150 A SiC IPM dissipates 320 W at 50 kHz, requiring a 0.15 °C/W heat sink. Regional differences persist: North America often parallelizes smaller modules for easier field replacement, whereas Europe and Asia prefer single high-current IPMs for density gains. As EV and rail volumes climb, the high-current class will seize an expanding slice of the intelligent power module market size.

By End-Use Industry:

Vehicles Near the Top SpotIndustrial automation held 33.05% of 2025 revenue, reflecting 30 years of IGBT deployment in variable-frequency drives and CNC tools. Electric and hybrid vehicles are advancing at a 12.22% CAGR and will overtake industrial by 2029 as global BEV output heads toward 25 million units. Ford’s next-generation electric truck will adopt a 1200 V, 500 A SiC IPM enabling 10-minute fast charging from 10% to 80% state-of-charge.

Consumer electronics and white goods remain steady, with inverter air conditioners and refrigerator compressors spearheading IPM penetration. Renewable-energy storage and grid-scale battery systems increasingly specify bidirectional inverters based on 1200 V IPMs to achieve 98% round-trip efficiency in California and Texas installations. Rail traction, though lower in volume, commands premium pricing because modules must endure 40 years of service and meet EN 50155 vibration limits. HVAC drives gain share as the EU Ecodesign Directive enforces seasonal efficiency minimums, while medical imaging and marine propulsion stay in the “others” niche for customized, low-volume designs.

By Sales Channel:

Retrofit Momentum BuildsOEM purchases represented 78.82% of 2025 shipments, but aftermarket and retrofit demand will expand at an 11.09% CAGR. Danfoss reports its VLT upgrade kits cut installation labour from six hours to 75 minutes, an attractive proposition for European plants chasing IE4 efficiency. The installed base of 2015-2020 residential inverters is aging, and installers opt for drop-in IPM replacements to avoid re-certification.

Automotive aftermarket applications stay limited because OEMs control powertrain components, yet industrial retrofit potential is large: 42% of German factories built before 2015 plan drive upgrades by 2027. Distribution channels differ: OEM sales go direct, while retrofit modules move through regional distributors and online platforms that bundle commissioning services. Regulatory pressure and electricity-price volatility underpin sustained retrofit adoption.

Geography Analysis

APAC Intelligent Power Module (IPM) Market

Asia Pacific generated 46.74% of 2025 revenue, buoyed by China’s 9.5 million-unit BEV output and India’s 18 GW solar additions. Chinese brands such as BYD and NIO rely on SiC IPMs to qualify for the MIIT efficiency subsidy, while Japan’s Mitsubishi Electric, Fuji Electric, and ROHM maintain technology leadership in high-voltage packaging. South Korea’s semiconductor fabs modernized cleanroom automation in 2025, generating demand for high-precision servo drives, and Southeast Asia’s appliance assembly plants integrated millions of 600 V modules.

North America Intelligent Power Module (IPM) Market

North America keeps a steady growth path on the back of Inflation Reduction Act credits and DOE standby-power limits. The United States installed 32 GW of utility-scale solar in 2025, 60% in Texas and California, using 1500 V string inverters built around 1700 V IPMs. Canadian BEV sales grew 48% year-on-year, aided by provincial mandates, and Mexico’s OEM powertrain localization is opening new supply-chain nodes. Retrofit demand in HVAC and industrial drives intensifies as electricity costs escalate.

Europe Intelligent Power Module (IPM) Market

Europe advances under the Machinery Regulation and the shift to 800 V EV platforms. Germany leads volume, with servo-drive upgrades in automotive and food processing sectors, while the United Kingdom’s offshore wind turbines employ 1700 V IPMs in 15 MW converters. France and Italy focus on rail-traction modernization, replacing legacy thyristor systems with IGBT IPMs that cut maintenance intervals. Spain’s favourable feed-in tariffs stimulate PV capacity additions that favour 1500 V inverters.

Middle East Intelligent Power Module (IPM) Market

The Middle East will log the quickest CAGR at 12.45% through 2031. Saudi Arabia commissioned 8 GW of solar in 2025, including the 2 GW Sudair plant that deploys central inverters based on 1700 V modules, and the UAE plans 1.2 GWh of storage at its flagship solar park to be supported by 1200 V SiC IPMs. Turkey’s appliance exports drive servo-drive demand, and Riyadh’s metro network will foster a lucrative replacement market starting in 2030.

South America and Africa Intelligent Power Module (IPM) Market

South America and Africa remain comparatively small but rising. Brazil’s automotive plants and food processors adopt IPM servo drives under modernization incentives, Argentina’s new renewable auctions will deploy 1500 V string inverters from 2027, and South Africa’s mines retrofit haul-truck drives to curb diesel usage. Nigeria’s hybrid solar-diesel commercial installations create a niche market for 600 V micro-inverters.

Regulatory Landscape

Standards and energy-efficiency requirements are tightening around high-voltage switching performance and safety verification, which directly feeds into IPM design and qualification. IEC 60747-15:2024 explicitly includes intelligent power semiconductor modules (IPMs) in Annex C, formalizing expectations for ratings, thermal resistance, and isolation testing, while European industrial motion applications are also shaped by the EU Machinery Regulation 2023/1230, which obliges IE4-level motor efficiency from 2026 and supports demand for integrated, protection-rich drive modules.

In 2026, compliance requirements are also extending into trade documentation and import controls. JEITA published JIS C 7012:2026 (May 2026), including requirements such as low stray inductance limits and Kelvin source stability checks for SiC module interconnect integrity. In the United States, USTR actions effective in December 2025 increased tariff scrutiny for semiconductors from China, and CBP enforcement of Section 232 duties (effective January 15, 2026) raises landed-cost risk for certain semiconductor imports, affecting sourcing decisions by module makers and OEMs.

Competitive Landscape

Competition in the intelligent power module market is moderate. Mitsubishi Electric, Infineon, Fuji Electric, ON Semiconductor, and Semikron Danfoss held 55% of 2025 revenue, but more than 20 regional suppliers divide the remainder. Technology leadership hinges on wide-bandgap devices: Wolfspeed and ROHM command premium pricing for SiC IPMs, while Navitas pushes GaN for 48 V and USB-PD niches. Manufacturing scale is equally vital; Infineon’s shift to 300 mm wafers lowers per-die costs, and Semikron Danfoss opened a new Indian line targeting two-wheeler EVs.

Strategic moves in 2025 underscore vertical integration. ON Semiconductor signed long-term SiC wafer deals to lock in supply, and Fuji Electric partnered with CRRC Times Electric for metro traction, transferring thermal-simulation know-how. Emerging Chinese foundries give price visibility in sub-50 A modules, pressuring incumbents. Embedded intelligence differentiates designs: STMicroelectronics patented on-chip machine-learning control that trims switching losses 12% without external microcontrollers.

Qualification costs still deter new entrants. AEC-Q101 testing can top USD 0.5 million per module family, but Chinese and Taiwanese test labs now offer services at one-third of European prices, eroding incumbents’ moat. White-space opportunities persist in standardized retrofit footprints and in above-1700 V rail applications where thermal-management challenges remain unresolved. Overall, expect heightened rivalry as automotive volumes attract dedicated engineering resources, potentially leaving gaps in industrial and consumer segments for niche specialists.

Intelligent Power Module (IPM) Industry Leaders

Mitsubishi Electric Corporation

Infineon Technologies AG

Fuji Electric Co., Ltd.

ON Semiconductor Corporation

Semikron Danfoss GmbH & Co. KG

- *Disclaimer: Major Players sorted in no particular order

Intelligent Power Module (IPM) Market Companies Covered in this Report

- Mitsubishi Electric Corporation

- Infineon Technologies AG

- Fuji Electric Co., Ltd.

- ON Semiconductor Corporation

- Semikron Danfoss GmbH & Co. KG

- ROHM Co., Ltd.

- Vincotech GmbH

- STMicroelectronics N.V.

- Powerex Inc.

- Toshiba Electronic Devices & Storage Corp.

- Wolfspeed, Inc.

- Microchip Technology Inc. (Microsemi)

- Renesas Electronics Corporation

- Littelfuse, Inc. (IXYS)

- Dynex Semiconductor Ltd.

- CRRC Times Electric Co., Ltd.

- StarPower Semiconductor Ltd.

- Hitachi Energy Ltd.

- Navitas Semiconductor Corp.

- Alpha & Omega Semiconductor Ltd.

- Sanken Electric Co., Ltd.

- BYD Semiconductor Co., Ltd.

- Nanjing SilverMicro Electronics Co., Ltd.

- Vishay Intertechnology Inc.

- Danfoss Silicon Power GmbH

Market Opportunities and Future Outlook

Manufacturing localization and scale-up are creating near-term whitespace in qualified IPM supply for automotive, industrial drives, and energy conversion, particularly as architectures move toward 800 V and above and wide-bandgap content expands. In April 2026, Alpha and Omega Semiconductor started commercial production of IPM5 modules at the new Kaynes Semicon OSAT facility in Sanand, Gujarat, widening the set of back-end options available to module vendors and OEM supply chains seeking redundancy beyond established East Asian packaging hubs. On the front-end, Infineon opened its Smart Power Fab in Dresden in July 2026 (EUR 5 billion investment) to increase output capacity for intelligent power semiconductors, signaling supplier funding for higher-volume production paths aligned with automotive and industrial demand.

Opportunities are also linked to cost-down and standardization, not only device performance. Industry efforts to scale 200 mm SiC manufacturing, including among Wolfspeed, Infineon, and Bosch, target lower per-die cost and higher throughput, while packaging standardization work (such as LV100-type concepts for three-level circuits in industrial and renewable applications) supports more interchangeable footprints and faster design-in across servo drives, PV/ESS converters, and retrofit markets. In parallel, Fuji Electric has communicated a roadmap targeting SiC modules for BEVs in FY2026 alongside new-generation IGBT modules for industrial use, reinforcing the split between premium SiC modules for high-voltage traction and cost-optimized IGBT IPMs for industrial automation and building systems.

Recent Industry Developments in Intelligent Power Module (IPM) Market

- June 2026: Mitsubishi Electric and Semikron Danfoss announced joint development of a new standard LV100-type package for power semiconductor modules with integrated three-level circuits aimed at industrial drives and renewable energy converters. The announcement extends packaging standardization in higher-performance topologies, supporting faster customer qualification and broader reuse of mechanical and electrical interfaces across platforms.

- October 2025: Infineon introduced the TDM22545T power module combining OptiMOS power stages with proprietary TLVR inductors for AI data center power delivery. The launch points to how higher-density power conversion loads are pushing module-style integration forward, which increases demand for compact, thermally optimized intelligent power modules in infrastructure power stages.

- July 2024: onsemi signed a multi-year agreement with Volkswagen Group to supply integrated power box modules featuring EliteSiC MOSFET technology for next-generation traction inverters. The agreement reinforces long-cycle automotive sourcing around SiC-enabled efficiency and provides volume visibility that can influence upstream wafer, substrate, and packaging allocations across the module ecosystem.

Intelligent Power Module (IPM) Market Report Scope and Research Methodology

Market Definition and Coverage

This market covers revenue from intelligent power modules sold as discrete, ready-to-mount power stages that integrate power switches with gate drive and protection, and are used to control motors, compressors, inverters, and power supplies across major end uses.

Scope exclusions: We exclude bare die, discrete power semiconductors sold outside a module, and chip-level integration that is only counted inside finished end equipment pricing.

Segments Covered in This Report

- By Operational Voltage

- 600 V Modules

- 650-900 V Modules

- 1,200 V Modules

- 1,700 V and Above Modules

- By Power Device

- IGBT-Based IPMs

- Si MOSFET-Based IPMs

- SiC MOSFET-Based IPMs

- GaN FET-Based IPMs

- By Substrate Material

- Insulated Metal Substrate (Al)

- DBC Ceramic (AlN / Al?O?)

- AMB Copper

- Si₃N₄ Ceramic

- By Circuit Configuration

- Half-Bridge

- Six-Pack

- Seven-Pack and Others

- By Current Rating

- Up to 50 A

- 51-100 A

- Above 100 A

- By End-Use Industry

- Consumer Electronics and Home Appliances

- Industrial Automation and Servo Drives

- Electric and Hybrid Vehicles

- Renewable Energy and ESS

- Rail Traction and Infrastructure

- HVAC and Building Systems

- Others End-User Industry

- By Sales Channel

- OEM

- Aftermarket / Retrofit

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-East Asia

- Rest of Asia Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started with building a clean view of how IPMs are shipped and priced in different applications, then mapping those patterns to demand drivers such as electrification and industrial automation. We leaned on public sources such as USITC and UN Comtrade trade tables, IEA energy and electrification indicators, IEA PVPS and IRENA renewable additions, and standards and efficiency references from groups such as IEC and IEEE to anchor the real-world usage backdrop.

To convert those signals into a usable sizing model, we also reviewed company filings, product catalogs, investor decks, and credible electronics press to understand typical module families, voltage classes, and packaging shifts. Select paid subscriptions for company financials and news helped us cross-check revenue splits and the timing of capacity or product launches, without relying on any single disclosure. The desk sources listed here are illustrative, since other public references were also used for collection, cross-checking, and clarification.

Primary Interviews and Surveys

Primary work focused on validating what portion of power-module demand is served by IPMs rather than discrete solutions, and how pricing changes as customers move from silicon to wide bandgap options. We spoke with a mix of module suppliers, distribution and channel participants, and engineering and procurement stakeholders across appliance, industrial drive, EV, and solar inverter ecosystems, and used that input to adjust assumptions by region and application.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 35% | CXOs: 14% | APAC: 46% |

| Mid tier: 47% | Functional/Unit leaders: 30% | EMEA: 35% |

| Smaller Players: 18% | Managers: 56% | Americas: 19% |

Market-Sizing & Forecasting

Sizing was built using a top-down demand-pool reconstruction, where end-use build rates and installed-base activity were translated into inverter and motor-drive power-stage needs, then filtered through realistic IPM adoption shares. For cross-checks, we also ran selective bottom-up approximations using sampled module families, typical average selling prices by voltage class, and shipment logic inferred from channel checks, and used those results to tune the totals.

Key inputs in the model included EV traction inverter production trends, industrial motor-drive retrofit activity, solar inverter shipment momentum, appliance compressor and HVAC motor demand, and the shift in voltage classes tied to faster switching and higher efficiency targets. Wide bandgap penetration assumptions were treated carefully because they can change the effective ASP path, so expert feedback was used to keep the price curve and mix changes consistent with what buyers are actually qualifying. For forecasting, scenario analysis was used around EV and renewables ramps, followed by an ARIMA-style time series check at the total-market level to keep the trajectory aligned with the historical growth pattern and the input indicators. Where bottom-up visibility was thin in smaller geographies, gaps were handled using regional proxy ratios based on electronics manufacturing intensity and validated with interview-based adoption ranges.

Data Validation & Update Cycle

Outputs were triangulated against multiple independent signals, including end-market shipment trends, regional electronics manufacturing indicators, and observed price and mix shifts discussed in interviews. Any sharp year-on-year changes were re-checked for unit consistency, currency timing, and mix effects, then reviewed through a multi-step analyst sign-off before finalizing.

The model is refreshed on an annual cycle, and interim checks are triggered when material events occur, such as major capacity moves, policy shifts affecting electrification, or a step change in EV or inverter shipments. Before delivery, a final pass is completed so the numbers reflect the latest available public data and the newest primary feedback.

Mordor Intelligence's Intelligent Power Module Ipm Market Size Compared With Other Published Estimates

Published IPM market values often vary because the counting rules are not the same, especially around what qualifies as an intelligent module versus a standard power module, and how the wide bandgap transition is priced into the curve. Differences also show up when one study anchors to end-use shipment demand while another leans more on supplier-side revenue disclosures that can include adjacent module categories.

The main gap comes from product-scope spillover, where Mordor Intelligence counts only factory-built IPMs with integrated drive and protection functions, and it keeps discrete power devices and non-intelligent module revenue out even if they sit in the same inverter bill of materials.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 2.98 B (2026) | |

| Industry Publisher A | USD 3.43 B (2025) | Uses an earlier base year and applies a faster growth path that can be influenced by aggressive wide bandgap mix and ASP uplift assumptions, which can inflate near-term value versus demand-linked adoption pacing. |

| Global Publisher B | USD 2.77 B (2024) | Anchors sizing to a different starting year and longer forecast window, and the revenue mapping by voltage and vertical can understate near-term value if EV and inverter ramps are treated conservatively. |

The spread in the table is mostly explained by when the sizing starts and how tightly the scope is restricted to true IPMs rather than adjacent power modules. By keeping the inputs traceable to end-use build indicators and then pressure-testing price and mix with interviews, the final number stays practical to replicate and easier to reconcile year to year.

Key Questions Answered in the Report

What is the current intelligent power module market size and expected growth?

The intelligent power module market size reached USD 2.98 billion in 2026 and is forecast to hit USD 4.96 billion by 2031, growing at a 10.71% CAGR.

Which voltage class is expanding fastest within intelligent power modules?

The 1200 V class is advancing at an 11.26% CAGR as 800 V electric-vehicle battery platforms become mainstream.

Why are silicon-carbide IPMs gaining share over IGBTs?

Silicon-carbide modules cut switching and conduction losses, enabling higher efficiency in EV traction, on-board chargers, and energy-storage converters despite higher unit costs.

How will aftermarket and retrofit channels evolve?

Retrofit demand will grow at an 11.09% CAGR as European factories and aging rooftop-solar inverters replace discrete designs with drop-in IPMs to meet new efficiency mandates.

Which region will post the fastest growth to 2031?

The Middle East is expected to lead regional growth with a 12.45% CAGR, thanks to large-scale solar and energy-storage investments.

Who are the top players in this space?

Mitsubishi Electric, Infineon, Fuji Electric, ON Semiconductor, and Semikron Danfoss together held about 55% of global revenue in 2025.

Page last updated on: