Automotive NVH Materials Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

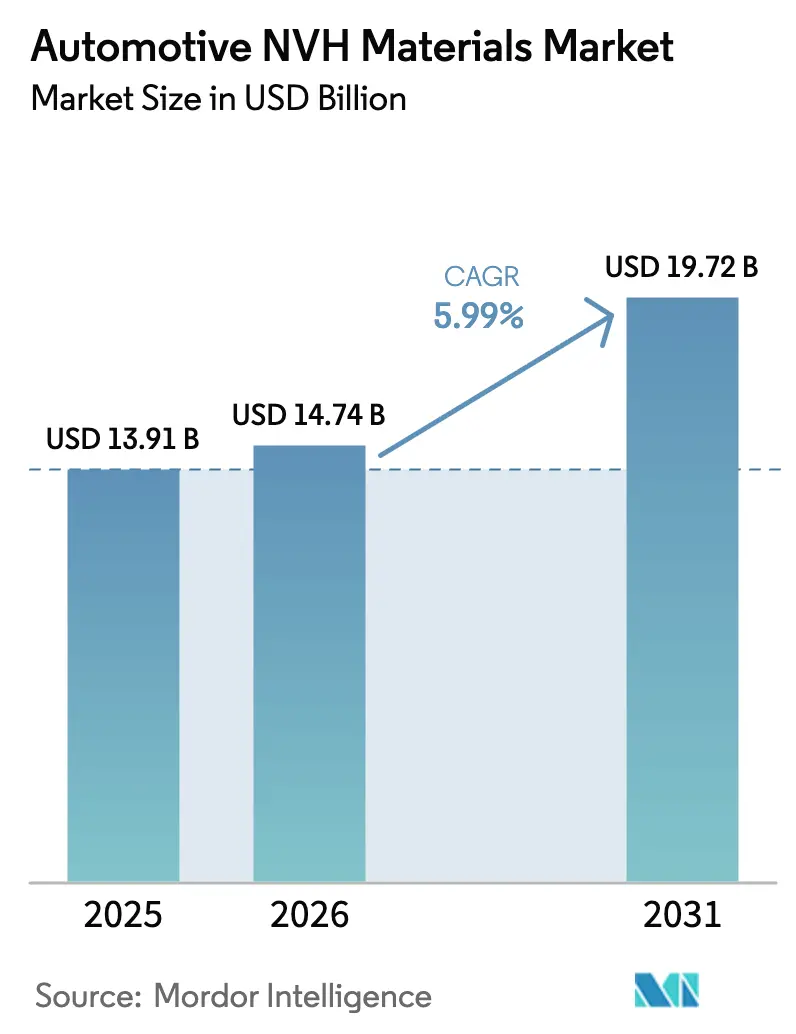

| Market Size (2026) | USD 14.74 Billion |

| Market Size (2031) | USD 19.72 Billion |

| Growth Rate (2026 - 2031) | 5.99% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive NVH Materials Market Analysis by Mordor Intelligence

The Automotive NVH Materials Market size is expected to grow from USD 13.91 billion in 2025 to USD 14.74 billion in 2026 and is forecast to reach USD 19.72 billion by 2031 at 5.99% CAGR over 2026-2031. Premium-grade acoustic comfort, stricter noise regulations, and the shift toward electrified drivetrains give sustained momentum to material suppliers across every vehicle class. Manufacturers are blending lightweight polymers with active noise control electronics to balance mass reduction and cabin serenity. Scale-driven acquisitions and regional manufacturing footprints continue to shape supplier strategies as automakers request integrated, system-level NVH packages. As a result, the Automotive NVH materials market is positioned for resilient growth even while propulsion technologies diversify.

Key Report Takeaways

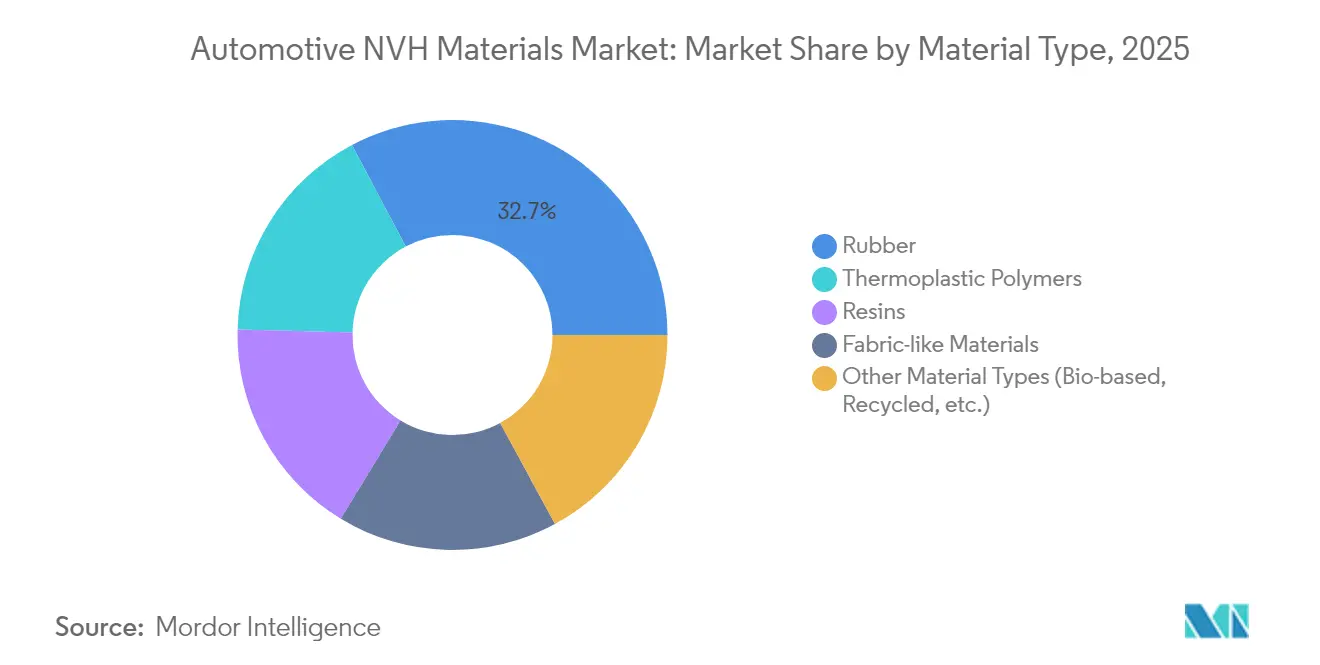

- By material type, rubber led with 32.74% of Automotive NVH materials market share in 2025, while other material types such as bio-based and recycled polymers are forecast to post the fastest 6.79% CAGR through 2031.

- By vehicle type, passenger cars accounted for 64.78% of the Automotive NVH materials market size in 2025 and are projected to expand at 7.57% CAGR between 2026-2031.

- By propulsion, internal combustion engine vehicles held 68.55% share in 2025; hybrid electric vehicles exhibit a 6.82% CAGR through 2031.

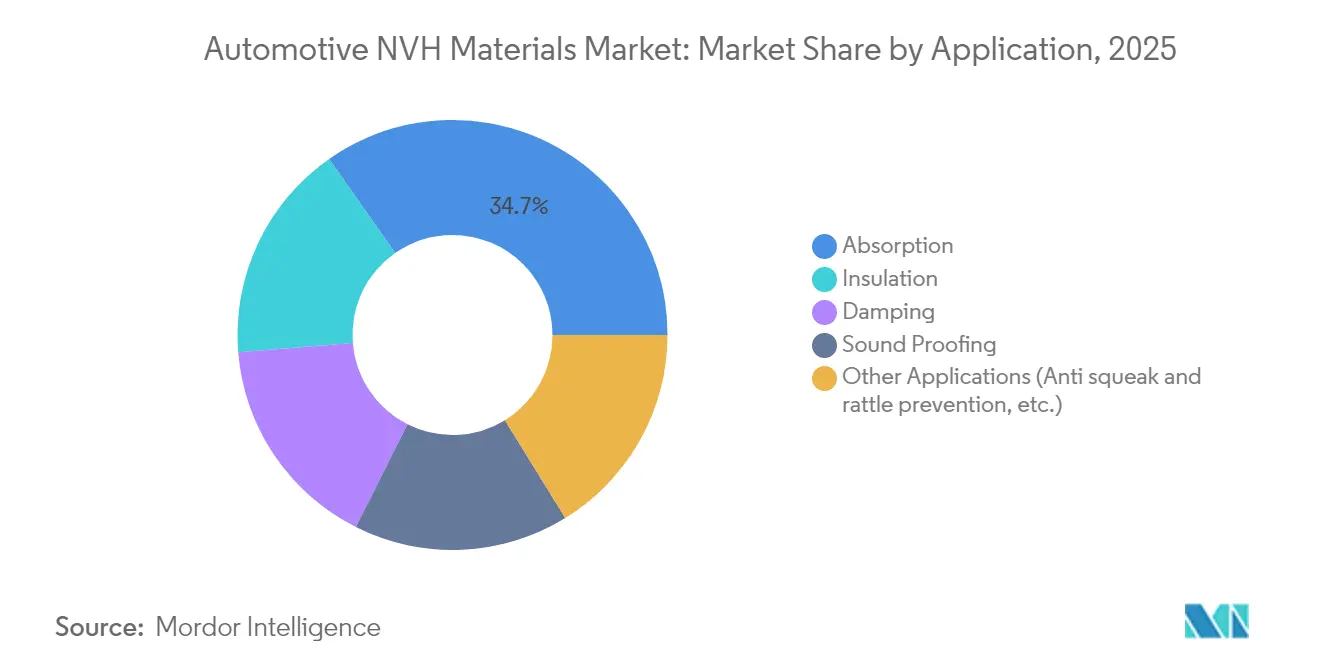

- By application, absorption captured 34.73% revenue share in 2025; insulation is set to advance at a 6.94% CAGR to 2031.

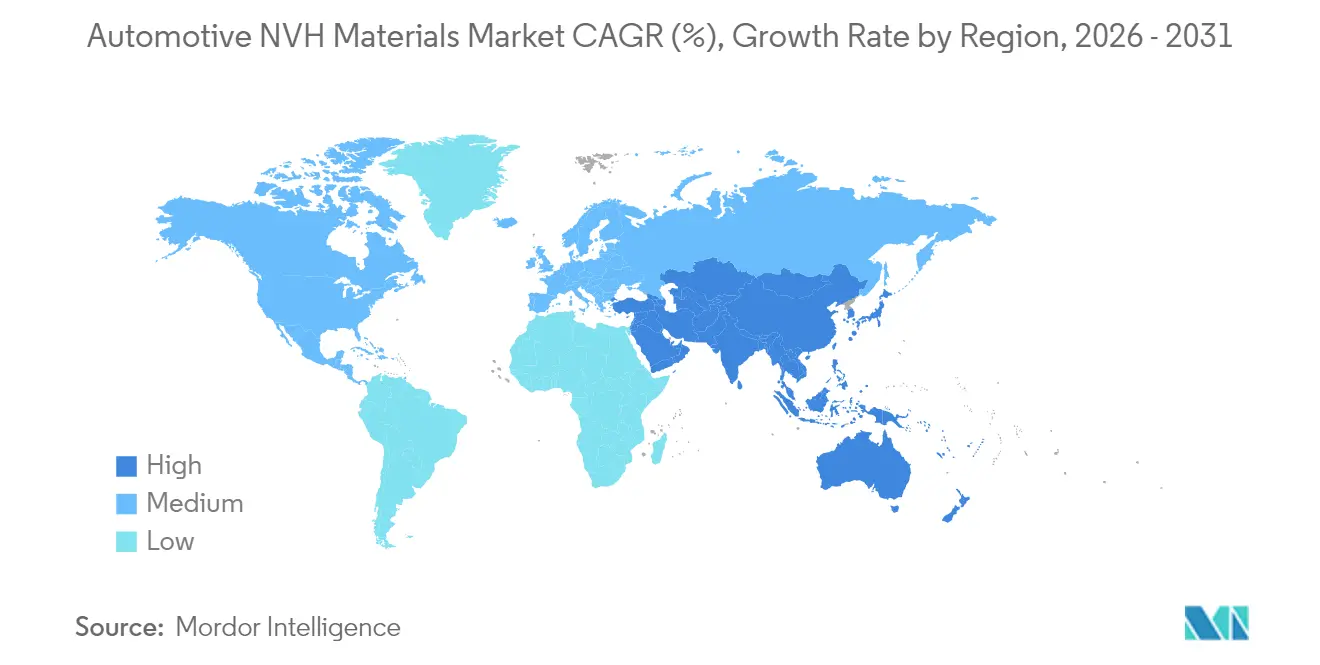

- By geography, Asia-Pacific dominated with 46.78% share in 2025 and remains the fastest-growing region at 6.66% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Automotive NVH Materials Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent cabin-noise legislation and rising comfort expectations | +1.8% | Global (EU & North America lead) | Medium term (2-4 years) |

| Booming EV and hybrid output exposing high-frequency NVH gaps | +0.7% | Global | Medium term (2–4 years) |

| Light-weighting strategies pivoting to polymer and composite NVH media | +1.2% | Global, accent on premium segments | Long term (≥ 4 years) |

| Premium and luxury vehicle proliferation demanding acoustic branding | +0.5% | North America & Europe | Medium term (2–4 years) |

| Increasing usage of automotive NVH materials in passenger vehicles | +0.4% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent Cabin-Noise Legislation and Rising Comfort Expectations

European Union Regulation 540/2014 tightened permissible exterior and interior noise limits, forcing OEMs to adopt higher-performance NVH materials that can pass compliance tests without adding unwanted mass[1].European Parliament, “Regulation ( EU ) No 540/2014 of the European Parliament and of the Council,” europarl.europa.eu Consumer awareness of quiet cabins also matured, encouraging mainstream brands to roll out features such as Honda’s Active Noise Control system across multiple model lines. Suppliers therefore observe non-discretionary demand that is insulated from macroeconomic cycles, since failing noise tests triggers financial penalties and brand damage. Automakers now frame interior sound quality as a branding device; BMW’s HypersonX program for Neue Klasse electric cars underscores the marketing weight attached to tailor-made acoustic signatures. The overlap of regulation and customer expectation cements a multi-year growth runway for advanced absorption, damping and insulation media.

Booming EV and Hybrid Output Exposing High-Frequency NVH Gaps

Electric motors reveal inverter whine and road-tire harmonics that traditional rubbers suppress poorly. Ascend Materials’ Vydyne Anti-Vibration Technology cuts cabin noise by up to 84%, proving that engineered polyamides can outperform legacy foams in the 3 kHz–4 kHz range. Hyundai’s Road-Noise Active Noise Control halves low-frequency disturbance through real-time phase inversion, letting carmakers mix lighter fabrics with electronic counterwaves for a refined ride. The urgency grows as Asia-Pacific factories accelerate battery-electric production, amplifying the need for composite mats and acoustic metamaterials tailored to high-frequency NVH profiles. As a result, the Automotive NVH materials market records its quickest contract wins in new EV platforms.

Light-Weighting Strategies Pivoting to Polymer and Composite NVH Media

Every kilogram shaved from a vehicle helps OEMs meet fleet CO₂ rules, so suppliers fuse acoustic and structural roles into multi-layer laminates. Material Sciences Corporation’s MSC Smart Steel trims panel mass by 35% while retaining comparable damping, supporting lower fuel use without cabin noise penalties. Thyssenkrupp’s bondal composite achieves up to 20 dB inverter noise reduction and adds electromagnetic shielding, illustrating the system benefits of hybrid laminates. Bio-infused alternatives, such as Toyoda Gosei’s cellulose-reinforced polypropylene, bring environmental credits while resisting impact in bumper beam trials. These developments show how weight cuts and acoustic targets converge, lifting demand for polymer-rich solutions across premium and mass segments.

Premium and Luxury Vehicle Proliferation Demanding Acoustic Branding

Sound design now anchors brand identity. BMW employs composer Hans Zimmer to create exclusive EV drive tones that communicate brand personality while masking high-frequency motor noise. Academic work at the Technical University of Munich confirms that a “solid” door-close sound raises perceived quality and purchase intent. As luxury attributes trickle into compact classes, suppliers must offer materials whose impedance characteristics enable fine tuning rather than blunt absorption. Mini’s four-mode sound worlds for its next EV series underline that acoustic branding extends beyond top-range sedans and into lifestyle models. The Automotive NVH materials market therefore benefits from higher content per vehicle as soundscapes become a differentiator.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Threat of substitutes from alternative technologies | −0.6% | Global | Medium term (2–4 years) |

| Feed-stock price volatility for petro-rubber and PU foams | −0.5% | Global | Short term (≤ 2 years) |

| Fire-safety hurdles for recycled foams | −0.4% | Europe & North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Feed-Stock Price Volatility for Petro-Rubber and PU Foams

Synthetic rubber prices swing with crude-derived butadiene supply. Spot Asian quotes surpassed USD 3,000 per ton in 2024, prompting Continental and Goodyear to lift tire prices and forcing NVH suppliers to pass on cost or lose margin. Budget segments are least able to absorb spikes, so some automakers scale back premium acoustic packs or delay launches. Supply disruptions such as rare-earth magnet shortages that idled a Ford plant in 2024 reveal the vulnerability of global feed-stock chains. The Automotive NVH materials market thus faces near-term expense pressure until hedging and localized sourcing strategies mature.

Fire-Safety Hurdles for Recycled Foams

United States FMVSS 302 caps burn rates at 102 mm per minute, and many recycled PU foams fail unless blended with halogenated flame retardants now under health scrutiny[2]National Highway Traffic Safety Administration, “FMVSS 302 Flammability of Interior Materials,” nhtsa.gov. Europe imposes parallel standards, while UL 94 V-0 ratings for electric-drive components create stricter hurdles. The regulatory friction slows commercial rollouts of sustainable acoustic pads. Scientific groups report catalyst systems that allow 30% recycled content to pass V-0, but mass-scale economics remain unproven. Until safer additives reach wide adoption, sustainability gains compete with fire-safety mandates and restrain segment expansion.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Bio-Innovation Drives Sustainability Transition

Rubber held the leading 32.74% share of the Automotive NVH materials market in 2025 because of its all-round vibration isolation performance and mature supply base. However, bio-based and recycled polymers clock a 6.79% CAGR as legislation and OEM carbon targets accelerate material substitution. The Automotive NVH materials market size for other types of polymer materials like bio-based and recycled polymers is projected to rise sharply once large-volume vehicle programs commit to lower-footprint interiors. Huntsman’s ACOUSTIFLEX HR BIO foam provides over 9% bio content while matching legacy PU resilience, demonstrating parity between green chemistry and ride refinement. LANXESS complements this shift with Tepex composites boasting more than 80% renewable feedstock for structural inserts.

Fabric-like non-woven sheets grow along lightweighting and recyclability goals. Milliken’s 50% lighter textile liner exceeds rivals in absorption and can reenter polymer streams at end of life. Mycelium-grown absorbers studied on ScienceDirect effectively damp 1 kHz cabin frequencies while biodegrading naturally. Over the forecast horizon, composite laminates that merge rubber skins with natural-fiber cores could unlock new cost-plus-sustainability value for Tier 1 suppliers. As those technologies scale, the Automotive NVH materials market will pivot from petro-heavy menus toward hybrid and renewable formulations. Acoustic metamaterials designed with periodic voids cancel 2.0–2.3 dB of low-frequency drone without mass, pointing to a future where geometry replaces heavier mass-law solutions. Such multifunctional approaches blur the historical lines between absorption, damping and insulation.

By Vehicle Type: Passenger Cars Drive Market Evolution

Passenger cars dominated the Automotive NVH materials market with 64.78% share in 2025 yet still deliver the highest 7.57% CAGR to 2031. The surge reflects rising per-unit content rather than sheer volume, as compact crossovers receive luxury-style acoustic packages to justify sticker prices. Light commercial vehicles benefit from parcel fleet electrification: Autoneum’s new Commercial Vehicle unit develops floor systems tuned to silent e-vans that amplify road roar. Heavy trucks adopt thicker dash mats to meet fatigue and safety guidelines for long-haul drivers. Two-wheelers and micro-mobility categories begin to integrate slimline damping strips as urban sound rules tighten. Consequently, the Automotive NVH materials market records wider application breadth, and suppliers must tailor acoustic, durability and cost attributes to vastly different duty cycles. Passenger car growth confirms that premium-feel acoustics are no longer confined to top-end sedans but span the mainstream showroom.

By Propulsion Type: Electrification Reshapes NVH Requirements

Internal combustion engine platforms still command 68.55% of revenue in 2025 because of the installed base. Hybrid electric vehicles, however, expand at 6.82% CAGR, presenting unique dual-frequency challenges that spur fresh material recipes. The Automotive NVH materials market share for battery electric vehicles is rising as pure EV lines multiply, demanding attenuation of high-pitch inverter tones without adding kilos that erode driving range.

Fuel-cell electric prototypes introduce hydrogen pump pulsation noise, creating a niche for low-mass diaphragms with broadband damping. Active noise cancellation complements lightweight foams: Hyundai’s RANC proves that control algorithms allow thinner floor sections while maintaining 50% interior noise cuts. Suppliers must therefore serve legacy ICE orders while pivoting R&D to electrified-specific solutions, enlarging the addressable Automotive NVH materials market size for smart composites and electronic hybrids.

By Application: Insulation Technologies Lead Growth Trajectory

Absorption pads accounted for 34.73% of revenue in 2025 because they are the default solution for airborne engine and road noise. Meanwhile, insulation products post the fastest 6.94% CAGR thanks to thermal management demands in battery electric platforms. Where battery packs raise cabin heat loads, suppliers combine aerogel particles with non-woven fibers to reduce both sound power by 40% and HVAC energy draw by 30%. Damping layers shift from asphalt sheets to BASF’s low-VOC LASD spray, trimming weight and installation time while maintaining frequency coverage. The Automotive NVH materials market size for insulation systems is projected to capture incremental gains each time an OEM launches a dedicated electric skateboard.

Geography Analysis

Asia-Pacific commanded 46.78% of the Automotive NVH materials market in 2025 and is forecast to grow at 6.66% CAGR, anchored by China, Japan and South Korea. Autoneum’s majority buyout of Jiangsu Huanyu strengthens local supply depth as Chinese OEMs demand quicker design-to-production cycles. Japanese conglomerates reorganize around EV parts, opening white space for NVH specialists who grasp battery-related acoustic profiles. South Korean material groups like Toray ramp capacity for sound-absorbing carbon-fiber sheets, signaling continued specialization. New assembly hubs in Thailand and Indonesia attract Japanese and Chinese Tier 1s that want tariff-free ASEAN access.

Europe maintains significant market presence driven by stringent regulatory frameworks and premium vehicle manufacturing concentration, with EU Regulation 540/2014 establishing comprehensive noise emission standards that directly influence NVH material specifications . German OEMs push suppliers toward acoustic branding, as BMW’s HypersonX project illustrates. Regulations further stimulate recycled polymer adoption, although FMVSS-equivalent fire standards slow mass uptake. Freudenberg’s EUR 42 million Punjab plants underscore European players’ strategy to serve global demand with localized output.

North America balances strict fire-safety code FMVSS 302 with a patchy supply base for specialty rubbers. Ford’s magnet shortage episode highlighted the urgency of regional resilience. AURELIUS Private Equity’s USD 1 billion acquisition of Teijin Automotive Technologies expands composite capabilities onshore, positioning the buyer for growth in EV acoustics. South America and the Middle East & Africa offer early-stage openings as local content mandates rise, yet economic swings and infrastructure gaps temper immediate volume.

Competitive Landscape

The Automotive NVH materials market is moderately fragmented, with top suppliers like Autoneum, 3M, and BASF leveraging proprietary chemistries, global tooling, and OEM collaborations to maintain their positions, while facing competition from agile entrants in smart materials. Innovation drives competition, with BASF’s low-density LASD sprays reducing weight and labor. Sustainability is critical, as seen in Dow’s bio-based NORDEL REN EPDM, which cuts CO₂ emissions by 90%. Regional expansions include Freudenberg’s new plants in India for localized NVH solutions and Chinese firms focusing on recycled thermoplastics, intensifying price competition. The market revolves around acoustic science, weight management, and sustainability, with consolidation offering scale advantages as automakers streamline supplier panels.

Automotive NVH Materials Industry Leaders

BASF

Dow

Autoneum

3M

Sumitomo Riko Company Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2024: Autoneum announced expansion in Asia with new plants in Changchun, China, and Pune, India, to meet growing demand for inner dashes, interior floor insulators and other NVH (noise, vibration, harshness) components for cars. The company aims to strengthen its market presence, and support sustainable mobility in key automotive hubs, with production starting in 2024.

- December 2023: Vibracoustic, subsidiary of Freudenberg SE, announced its new NVH technologies tailored for commercial vehicles transitioning to low- and zero-emission powertrains. Drawing on its extensive expertise, Vibracoustic has proactively adapted to industry shifts, crafting NVH-optimized mounting systems specifically for battery packs, electric motors, and fuel cells.

Global Automotive NVH Materials Market Report Scope

The Automotive NVH Materials Market report include

| Rubber |

| Thermoplastic Polymers |

| Resins |

| Fabric-like Materials |

| Other Material Types (Bio-based, Recycled, etc.) |

| Internal Combustion Engine (ICE) Vehicles |

| Hybrid Electric Vehicles (HEV/PHEV) |

| Battery Electric Vehicles (BEV) |

| Fuel-Cell Electric Vehicles (FCEV) |

| Passenger Cars |

| Light Commercial Vehicles |

| Heavy Commercial Vehicles |

| Two-Wheelers and Micro-Mobility |

| Absorption |

| Damping |

| Insulation |

| Sound Proofing |

| Other Applications (Anti squeak and rattle prevention, etc.) |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Material Type | Rubber | |

| Thermoplastic Polymers | ||

| Resins | ||

| Fabric-like Materials | ||

| Other Material Types (Bio-based, Recycled, etc.) | ||

| By Propulsion Type | Internal Combustion Engine (ICE) Vehicles | |

| Hybrid Electric Vehicles (HEV/PHEV) | ||

| Battery Electric Vehicles (BEV) | ||

| Fuel-Cell Electric Vehicles (FCEV) | ||

| By Vehicle Type | Passenger Cars | |

| Light Commercial Vehicles | ||

| Heavy Commercial Vehicles | ||

| Two-Wheelers and Micro-Mobility | ||

| By Application | Absorption | |

| Damping | ||

| Insulation | ||

| Sound Proofing | ||

| Other Applications (Anti squeak and rattle prevention, etc.) | ||

| Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the current size of the Automotive NVH materials market?

The market is valued at USD 14.74 billion in 2026 and is forecast to reach USD 19.72 billion by 2031.

How are electric vehicles affecting NVH material demand?

EV platforms expose high-frequency noise previously masked by engines, driving demand for lightweight composites and active noise technologies that meet new acoustic profiles.

Which region is the largest consumer of Automotive NVH materials?

Asia-Pacific leads with 46.78% market share in 2025 and also posts the fastest 6.66% CAGR.

What role do regulations play in material selection?

Standards like EU Regulation 540/2014 and US FMVSS 302 set strict limits on noise and flammability, making high-performance, compliant materials mandatory for OEM programs.

Page last updated on: