Automotive Engine And Engine Mounts Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

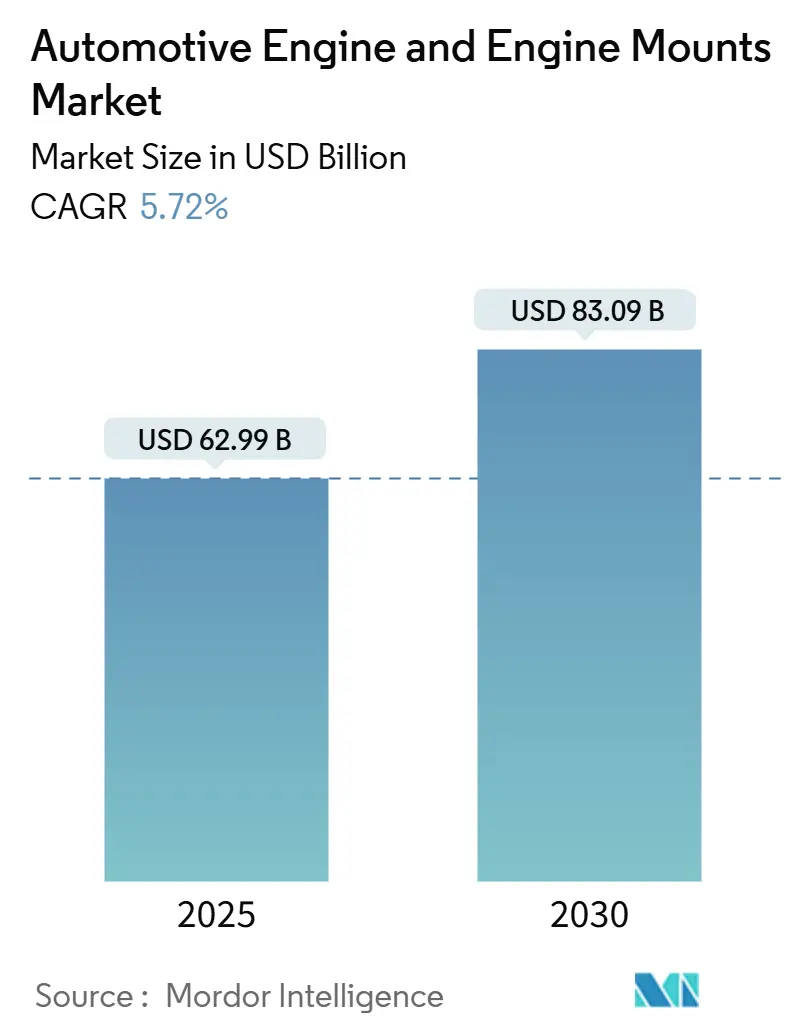

| Market Size (2025) | USD 62.99 Billion |

| Market Size (2030) | USD 83.09 Billion |

| Growth Rate (2025 - 2030) | 5.72% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Automotive Engine And Engine Mounts Market Analysis by Mordor Intelligence

The automotive engine and engine mounts market size stood at USD 62.99 billion in 2025 and is projected to reach USD 83.09 billion by 2030, registering a 5.72% CAGR over the forecast period. This trajectory reflects robust component demand in emerging economies, mounting complexity in hybrid platforms, and OEM prioritization of noise, vibration, and harshness (NVH) refinement despite electrification headwinds. Declining internal-combustion-engine (ICE) volumes in Europe and North America are offset by hybrid adoption and sustained production growth across Asia-Pacific, Latin America, and the Middle East. Suppliers that combine advanced elastomer chemistry, active damping electronics, and global manufacturing footprints continue to capture incremental share as OEMs accelerate platform standardization, shorten development cycles, and redesign mounts to meet stringent emission norms. Meanwhile, commodity-price volatility and tariff-driven regionalization compel manufacturers to pursue vertical integration and dual-sourcing strategies to protect margins and ensure supply continuity.

Key Report Takeaways

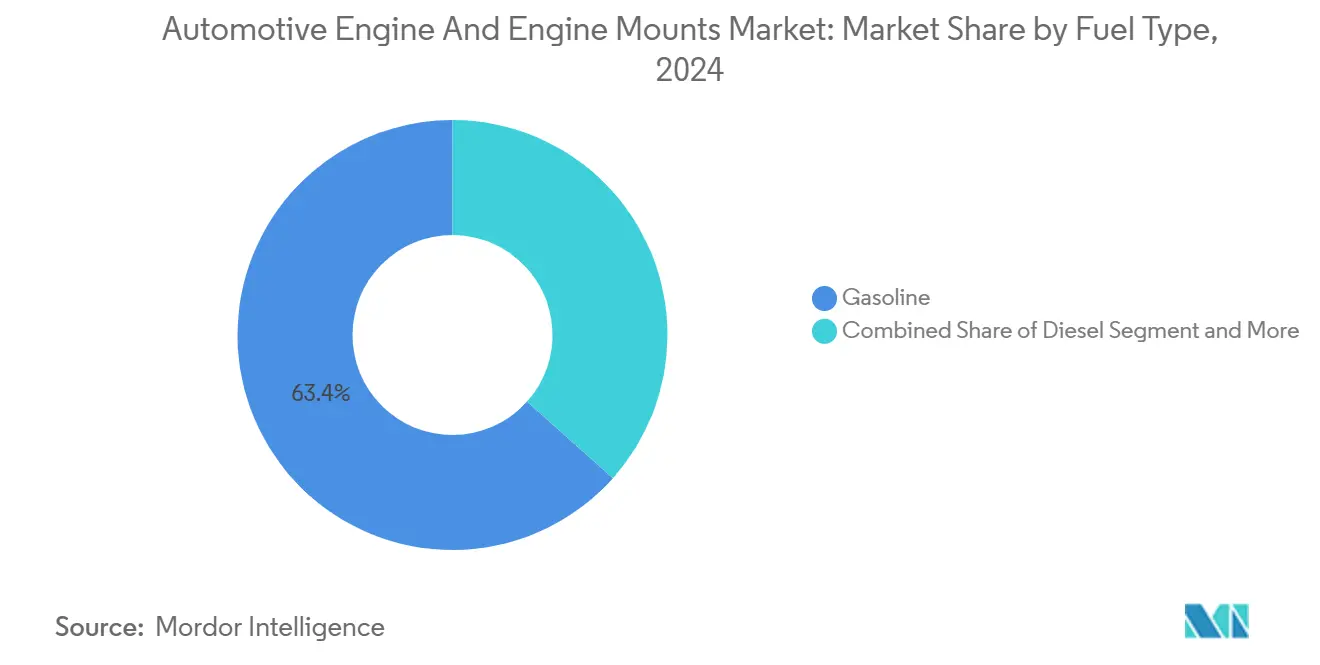

- By fuel type, gasoline engines held 63.42% of the automotive engine and engine mounts market share in 2024, while hybrid powertrains are advancing at a 12.67% CAGR through 2030.

- By vehicle type, buses and coaches accounted for the fastest expansion at a 7.35% CAGR, whereas passenger cars retained 49.58% revenue share in 2024.

- By engine mount technology, elastomer designs dominated with 71.83% share in 2024; electro-hydraulic/active systems are growing at 9.72% CAGR to 2030.

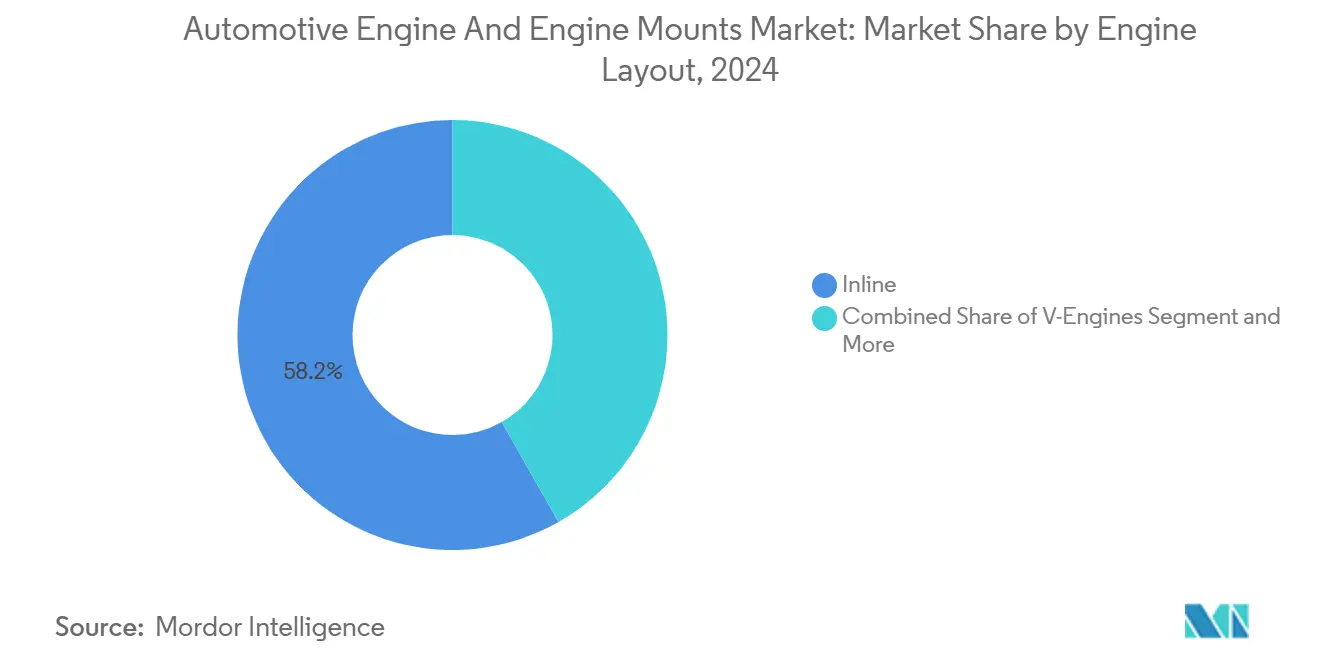

- By engine layout, inline engines captured 58.24% of the 2024 automotive engine and engine mounts market size, but W-layout units are forecast to grow at a 6.94% CAGR.

- By sales channel, OEM purchasing represented 78.31% of 2024 demand; the aftermarket is expanding at 5.47% CAGR, reflecting aging global vehicle fleets.

Global Automotive Engine And Engine Mounts Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding Vehicle Production in Emerging Economies | +1.5% | Asia-Pacific Core, Spill-over to Latin America and MEA | Short Term (≤ 2 Years) |

| Stringent Global Emission Norms Accelerating Engine Downsizing and Efficiency Upgrades | +1.2% | Global, with EU and China Leading Regulatory Implementation | Medium Term (2-4 Years) |

| Rising NVH-Comfort Expectations Boosting Demand for Advanced Engine Mounts | +0.9% | North America and EU Premium Segments, Asia-Pacific Luxury Expansion | Long Term (≥ 4 Years) |

| Hybrid-Powertrain Proliferation Creating Specialized Mount Requirements | +0.8% | Global, with Early Adoption in Japan, EU, and California | Medium Term (2-4 Years) |

| Tariff-Driven Reshoring of Mount Manufacturing Spurring Regional Investments | +0.6% | North America Primarily, with Secondary EU Effects | Short Term (≤ 2 Years) |

| AI-Driven Predictive Maintenance Shortening Elastomer-Mount Replacement Cycles | +0.4% | North America and EU Aftermarket, Gradual Asia-Pacific Penetration | Long Term (≥ 4 Years) |

| Source: Mordor Intelligence | |||

Stringent Global Emission Norms Accelerating Engine Downsizing and Efficiency Upgrades

Regulatory pressure from Euro 7 standards and China's National VI emissions regulations drives OEMs toward smaller, turbocharged engines that generate higher vibration frequencies and require sophisticated mounting solutions. Engine downsizing creates a technical paradox where reduced displacement increases specific power output, intensifying NVH challenges that traditional passive mounts struggle to address. Advanced hydraulic and electro-hydraulic mounts become essential for managing the complex vibration signatures of turbocharged 3-cylinder engines, which exhibit inherent imbalance compared to naturally aspirated 4-cylinder units. This regulatory-driven shift toward active mount technologies accelerates market premiumization, as OEMs prioritize customer comfort over cost optimization. The transition particularly affects European and Chinese markets, where stringent emissions compliance timelines compress development cycles and favor suppliers with proven active mount capabilities.

Rising NVH-Comfort Expectations Boosting Demand for Advanced Engine Mounts

Consumer expectations for luxury-grade refinement across mainstream vehicle segments drive demand for advanced mount technologies that deliver superior vibration isolation. The proliferation of quiet electric powertrains in the market creates a reference point for NVH performance that ICE and hybrid vehicles must match, pushing traditional rubber mounts toward their technical limits. Magnetorheological and semi-active mount systems emerge as solutions for real-time vibration tuning, adapting damping characteristics based on engine operating conditions and road inputs. Premium automakers increasingly specify active mounts as standard equipment rather than optional features, creating volume scale that reduces per-unit costs and accelerates mainstream adoption. This trend particularly benefits suppliers like Vibracoustic and Continental, whose advanced mount portfolios align with OEM strategies to differentiate through refined driving experiences rather than purely performance metrics.

Expanding Vehicle Production in Emerging Economies

Vehicle production growth in India, Southeast Asia, and Latin America creates substantial demand for cost-effective engine mount solutions that balance performance with price sensitivity. India's automotive manufacturing expansion, supported by production-linked incentive schemes, positions the country as a global sourcing hub for engine components, including mounts designed for local and export markets. Chinese OEMs' aggressive export strategy, targeting 6 million vehicle exports in 2024, requires scalable manufacturing supply chains that can support rapid volume ramp-up while maintaining quality standards[1]Michael Dunne, "The Great China Car Blitzkrieg," Dunne Insights, dunneinsights.com. . The emerging market focus on affordable mobility solutions favors elastomer mount technologies that offer proven reliability at competitive costs, though hybrid adoption in these regions will gradually introduce demand for more sophisticated mounting systems. Regional manufacturing investments, including Saudi Arabia's USD 1.3 billion Ceer EV complex and Morocco's EUR 180 million CITIC Dicastal aluminum casting plant, establish local supply chains that reduce logistics costs and improve responsiveness to regional OEM requirements[2]"Autos Investment Round-Up: Saudi Arabia Tops Our Q124 Round-Up And Collaboration Starts Paying Off," BMI, fitchsolutions.com..

Hybrid-Powertrain Proliferation Creating Specialized Mount Requirements

Hybrid powertrains introduce unique mounting challenges through P2 and P3 configurations that combine internal combustion engines with electric motors, creating complex vibration patterns that traditional mounts cannot adequately isolate. The integration of electric motors directly into the powertrain requires specialized mounting solutions that accommodate both engine vibration and electric motor torque characteristics, particularly during engine start-stop transitions. Hybrid systems' frequent engine cycling creates thermal stress patterns that accelerate elastomer degradation, driving demand for advanced rubber compounds and temperature-resistant mounting designs. Active mount systems become particularly valuable in hybrid applications, where real-time vibration control can mask the NVH compromises inherent in engine start-stop operation and electric-ICE power transitions. This technical complexity creates opportunities for suppliers with advanced materials expertise and active mount capabilities, while challenging traditional mount manufacturers to develop hybrid-specific solutions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fast-Growing Electrification Shrinking ICE Addressable Market | -1.2% | EU and China Leading, North America Following | Medium Term (2-4 Years) |

| Raw-Material Price Volatility (Steel, Elastomers) | -0.8% | Global, with Acute Impact in Import-Dependent Regions | Short Term (≤ 2 Years) |

| Cyber-Security-Gated OEM Data Curbing Independent Aftermarket Fitment | -0.6% | Global, with Strongest Impact in EU and North America | Long Term (≥ 4 Years) |

| High-Temperature Rubber Degradation in Urban Start-Stop Traffic | -0.5% | Global Urban Centers, Stronger Impact in Asia-Pacific and EU | Short Term (≤ 2 Years) |

| Source: Mordor Intelligence | |||

Raw-Material Price Volatility (Steel, Elastomers)

Steel and elastomer price volatility creates significant margin pressure for mount manufacturers. Natural rubber supply constraints, particularly from Southeast Asian producing regions, create procurement challenges for mount manufacturers who rely on specific rubber compounds for durability and performance characteristics. The volatility particularly affects smaller tier-2 suppliers with limited hedging capabilities, potentially accelerating industry consolidation as larger players leverage purchasing scale and financial resources to weather commodity cycles. Long-term supply agreements and vertical integration strategies become critical competitive advantages in managing raw material exposure.

Fast-Growing Electrification Shrinking ICE Addressable Market

Battery electric vehicle adoption accelerates the decline of traditional engine mount demand, particularly in European and Chinese markets, where regulatory support and consumer acceptance drive rapid EV penetration. The transition creates a structural headwind for mount suppliers whose core competencies center on ICE vibration isolation, requiring strategic pivots toward EV-specific mounting solutions for battery packs, electric motors, and power electronics. Chinese EV manufacturers' export ambitions, targeting global markets with competitively priced electric vehicles, intensify pressure on traditional automotive supply chains and create overcapacity in ICE-focused manufacturing assets. The electrification timeline varies significantly by region, with Europe and China leading adoption while emerging markets maintain ICE preference due to infrastructure and affordability constraints, creating geographic demand imbalances that challenge global supply chain optimization. Mount suppliers must balance investments in declining ICE technologies with emerging EV opportunities, requiring careful portfolio management and strategic partnerships to navigate the transition successfully.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Fuel Type: Gasoline Dominance Faces Hybrid Disruption

Gasoline engines maintain the largest 2024 market share at 63.42%, while advanced hybrid powertrains emerge as the most dynamic fuel-type segment, recording a 12.67% CAGR through 2030. Hybrid systems require specialized mounting solutions that accommodate dual-power sources and frequent engine start-stop cycles, creating technical complexity that favors suppliers with advanced materials and active mount capabilities. Diesel applications continue declining in passenger vehicles due to emissions regulations, though commercial vehicle demand remains stable in emerging markets where fuel efficiency outweighs environmental concerns. Alternative fuel engines, including CNG and biofuel applications, represent niche opportunities primarily in fleet applications and regions with supportive infrastructure policies.

The shift toward hybrid architectures fundamentally alters mount design requirements, as P2 hybrid configurations integrate electric motors directly into the powertrain, creating vibration patterns that traditional elastomer mounts cannot adequately isolate. Research demonstrates that hybrid powertrains require specialized mount tuning to manage the NVH challenges of engine start-stop transitions and electric-ICE power blending. Gasoline engines benefit from continued refinement in turbocharged configurations, where downsizing strategies increase specific power output but intensify vibration control requirements, supporting demand for hydraulic and active mount technologies.

By Vehicle Type: Commercial Segments Drive Growth

Passenger cars command 49.58% market share in 2024, benefiting from volume scale but facing margin pressure as OEMs prioritize cost optimization over premium mount technologies in mainstream segments. Buses and coaches lead vehicle-type growth at 7.35% CAGR, reflecting commercial fleet electrification and hybrid adoption that requires sophisticated mounting solutions for heavy-duty applications. Light commercial vehicles experience steady demand growth, supported by e-commerce logistics expansion and last-mile delivery requirements that favor reliable, cost-effective mounting solutions. Medium and heavy commercial vehicles maintain stable demand, though regulatory pressure for emissions compliance drives gradual adoption of advanced mount technologies in premium truck segments.

Two-wheeler applications represent a specialized segment where weight and cost constraints limit advanced mount adoption, though premium motorcycle manufacturers increasingly specify hydraulic mounts for enhanced rider comfort. The commercial vehicle focuses on the total cost of ownership, creating opportunities for predictive maintenance solutions that extend the mount service life and reduce unplanned downtime. Fleet operators' data-driven approach to maintenance scheduling supports adoption of AI-driven monitoring systems that optimize replacement intervals based on actual operating conditions rather than fixed service schedules.

By Engine Mount: Elastomer Leadership Challenged by Active Systems

Elastomer mounts retain 71.83% market share in 2024, supported by cost advantages and proven reliability in mainstream applications, though technical limitations become apparent in turbocharged and hybrid powertrains. Hydraulic mounts occupy a middle ground, offering superior vibration isolation compared to passive elastomer systems while maintaining cost competitiveness versus fully active solutions. The technology progression reflects automotive industry premiumization, where features once reserved for luxury vehicles migrate to mainstream segments as production scale reduces per-unit costs. Electro-hydraulic and active mount systems achieve 9.72% CAGR through 2030, driven by OEM demand for real-time vibration control that adapts to varying engine operating conditions.

Active mount adoption accelerates in hybrid applications, where frequent engine start-stop cycles create NVH challenges that passive systems cannot adequately address. Continental's development of magnetorheological mount systems demonstrates the industry's technical evolution toward real-time vibration control that adjusts damping characteristics based on vehicle operating conditions. The transition toward active systems creates competitive advantages for suppliers with advanced materials expertise and electronic control capabilities, while challenging traditional rubber manufacturers to develop next-generation solutions or risk market share erosion.

By Engine Layout: Inline Engines Maintain Dominance

Inline engines command 58.24% market share in 2024, benefiting from manufacturing simplicity and cost advantages that align with mainstream vehicle requirements. V-engines maintain steady demand in performance and luxury applications, where power density and refinement justify specialized mounting systems' additional complexity and cost. Flat and boxer engine configurations represent niche applications primarily in specific OEM portfolios, requiring customized mounting solutions that limit supplier scale economies. W-Layout engines achieve 6.94% CAGR growth through 2030, reflecting premium automaker adoption of compact, high-performance configurations that require sophisticated mounting solutions.

The engine layout segmentation reflects broader automotive industry trends toward downsizing and electrification, where traditional displacement-based power delivery gives way to turbocharged efficiency and hybrid integration. W-Layout engines' compact packaging advantages become particularly valuable in hybrid applications, where space constraints require innovative mounting solutions that accommodate both ICE and electric power sources within limited engine bay dimensions. Inline engine dominance supports supplier standardization strategies, where common mounting interfaces reduce development costs and improve manufacturing efficiency across multiple vehicle platforms.

By Sales Channel: OEM Dominance with Aftermarket Acceleration

OEM channels maintain 78.31% market share in 2024, reflecting the critical role of engine mounts in vehicle NVH performance and safety, where OEM specifications ensure compatibility and performance standards. Aftermarket growth benefits from independent repair shop consolidation and digital catalog systems that improve parts availability and fitment accuracy. The channel dynamics reflect broader automotive aftermarket trends toward professional service providers and away from do-it-yourself maintenance for complex components like engine mounts. The aftermarket channel demonstrates robust 5.47% CAGR growth through 2030, driven by aging vehicle fleets and predictive maintenance adoption that optimizes replacement timing.

Genuine Parts Company's acquisition of Motor Parts & Equipment Corporation for 181 NAPA locations demonstrates aftermarket consolidation that improves distribution reach and inventory management. Predictive maintenance technologies enable aftermarket suppliers to optimize inventory positioning and reduce obsolete stock, while AI-driven diagnostic systems help technicians identify mounting failure patterns before a complete system breakdown. The OEM channel benefits from long-term supply agreements and platform standardization, though margin pressure from cost-conscious automakers drives continuous efficiency improvements and value engineering initiatives.

Geography Analysis

Asia-Pacific leads global market dynamics with 44.29% share in 2024 and 6.68% CAGR through 2030, driven by China's automotive manufacturing scale and India's expanding production base. Chinese OEMs' export ambitions, targeting 6 million vehicle exports in 2024, create substantial component demand that benefits regional mount suppliers with cost-competitive manufacturing capabilities. India's production-linked incentive schemes support automotive manufacturing expansion, positioning the country as a global sourcing hub for engine components designed for both domestic consumption and export markets.

North America experiences mature market conditions with steady demand supported by vehicle fleet renewal and commercial vehicle growth. The region benefits from reshoring initiatives, including Hyundai's USD 5.8 billion Louisiana steel facility targeting automotive applications and General Motors' USD 4 billion investment to relocate production from Mexico. U.S. tariffs on steel and aluminum imports create cost pressures for mount manufacturers, though domestic sourcing initiatives partially offset raw material price increases through reduced logistics costs and supply chain resilience. Canada's automotive manufacturing base supports regional mount production, while Mexico's cost advantages attract continued investment despite trade policy uncertainties. The USMCA trade agreement provides framework stability for cross-border supply chains, though political tensions over automotive content requirements create ongoing compliance challenges.

Europe faces declining ICE demand offset by hybrid adoption and premium vehicle production that requires advanced mounting technologies. The region's stringent emissions regulations drive OEM demand for sophisticated mount systems that support engine downsizing and electrification strategies. Germany's automotive engineering leadership creates demand for high-performance mount solutions, while Eastern European manufacturing provides cost-competitive production capabilities for volume applications. Brexit continues affecting UK automotive supply chains, though established relationships and specialized capabilities maintain market position for British mount suppliers.

Competitive Landscape

The automotive engine and engine mounts market exhibits moderate concentration with established tier-1 suppliers leveraging technological differentiation and long-term OEM partnerships to maintain competitive positions. Continental, Vibracoustic, and Sumitomo Riko dominate through advanced mount technologies and global manufacturing footprints that align with OEM platform strategies and regional sourcing requirements. Competition intensifies around active mount technologies, where suppliers with electronic control capabilities and advanced materials expertise gain advantages in hybrid and premium vehicle applications.

The market structure reflects broader automotive supplier consolidation trends, where scale economies and R&D investments create barriers to entry for smaller players lacking global reach and technological depth. Strategic patterns emphasize technology development over price competition, as OEMs prioritize NVH performance and reliability over cost optimization in critical safety components. Continental's automotive spin-off into Aumovio ahead of a September 2025 IPO demonstrates strategic repositioning toward software-defined vehicles and Asian market expansion.

White-space opportunities emerge in EV-specific mounting solutions for battery packs and electric motors, where traditional ICE mount expertise requires adaptation to different vibration characteristics and packaging constraints. Emerging disruptors include materials technology companies developing advanced elastomer compounds and smart mount systems with integrated sensors for predictive maintenance applications. Technology adoption focuses on active damping systems and AI-driven diagnostic capabilities that enable real-time performance optimization and predictive failure detection.

Automotive Engine And Engine Mounts Industry Leaders

-

Continental AG

-

Vibracoustic

-

Sumitomo Riko

-

Tenneco Inc.

-

Hutchinson SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Continental announced the spin-off of its Automotive Group into a new independent company branded Aumovio, ahead of a planned IPO in September 2025. The strategic restructuring emphasizes software-defined vehicles and positions the company for enhanced focus on Asian growth markets and advanced mobility solutions.

- March 2025: Hyundai Motor Group committed USD 5.8 billion to build an ultra-low carbon steel production facility in Louisiana, targeting 2.7 million metric tons of annual automotive steel output. The investment strengthens North American automotive supply chains and reduces dependence on imported steel for engine mount and structural component manufacturing.

Global Automotive Engine And Engine Mounts Market Report Scope

| Gasoline |

| Diesel |

| Hybrid |

| Others (CNG, Bio-fuel etc.) |

| Two-Wheeler |

| Passenger Cars |

| Light Commercial Vehicles |

| Medium and Heavy Commercial Vehicles |

| Buses and Coaches |

| Elastomer (Passive Rubber) |

| Hydraulic |

| Electro-Hydraulic/Active |

| Inline |

| V-Engines |

| Flat/Boxer |

| W-Layout |

| OEM |

| Aftermarket |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle-East and Africa |

| By Fuel Type | Gasoline | |

| Diesel | ||

| Hybrid | ||

| Others (CNG, Bio-fuel etc.) | ||

| By Vehicle Type | Two-Wheeler | |

| Passenger Cars | ||

| Light Commercial Vehicles | ||

| Medium and Heavy Commercial Vehicles | ||

| Buses and Coaches | ||

| By Engine Mount | Elastomer (Passive Rubber) | |

| Hydraulic | ||

| Electro-Hydraulic/Active | ||

| By Engine Layout | Inline | |

| V-Engines | ||

| Flat/Boxer | ||

| W-Layout | ||

| By Sales Channel | OEM | |

| Aftermarket | ||

| By Region | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

How large is the automotive engine and engine mounts market in 2025?

The automotive engine and engine mounts market size reached USD 62.99 billion in 2025 and is expected to hit USD 83.09 billion by 2030.

Which fuel type will grow the fastest through 2030?

Hybrid powertrains lead with a projected 12.67% CAGR as OEMs expand electrified lineups requiring specialized mount solutions.

What share do elastomer mounts hold today?

Elastomer designs captured 71.83% of 2024 demand, reflecting cost advantages despite rapid growth of electro-hydraulic and active systems.

Why are active engine mounts gaining traction?

Active mounts provide real-time damping adjustment that meets stricter NVH targets for downsized turbo and hybrid engines, supporting 9.72% CAGR for the technology.

Which region dominates future demand?

Asia-Pacific leads with 44.29% share in 2024 and a 6.68% CAGR, supported by high vehicle production in China, India, Japan, and South Korea.

Page last updated on: