Automotive Leaf Spring Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 14.09 Billion |

| Market Size (2031) | USD 20.96 Billion |

| Growth Rate (2026 - 2031) | 8.28% CAGR |

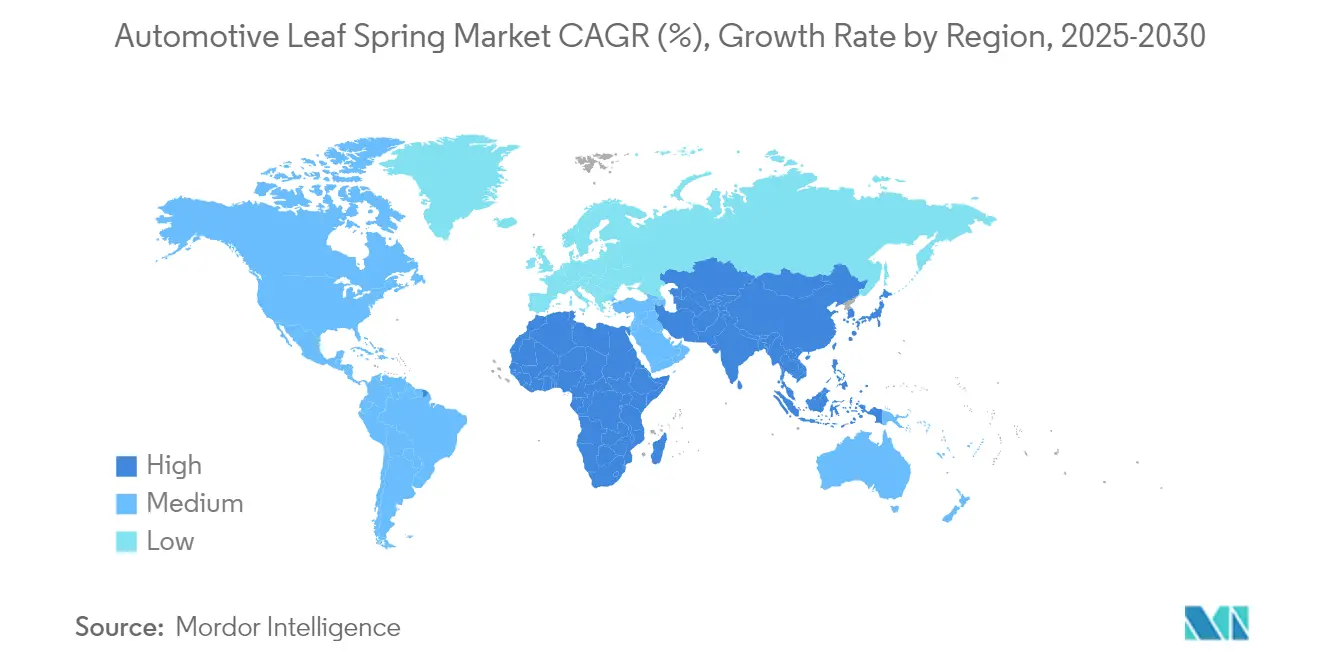

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive Leaf Spring Market Analysis by Mordor Intelligence

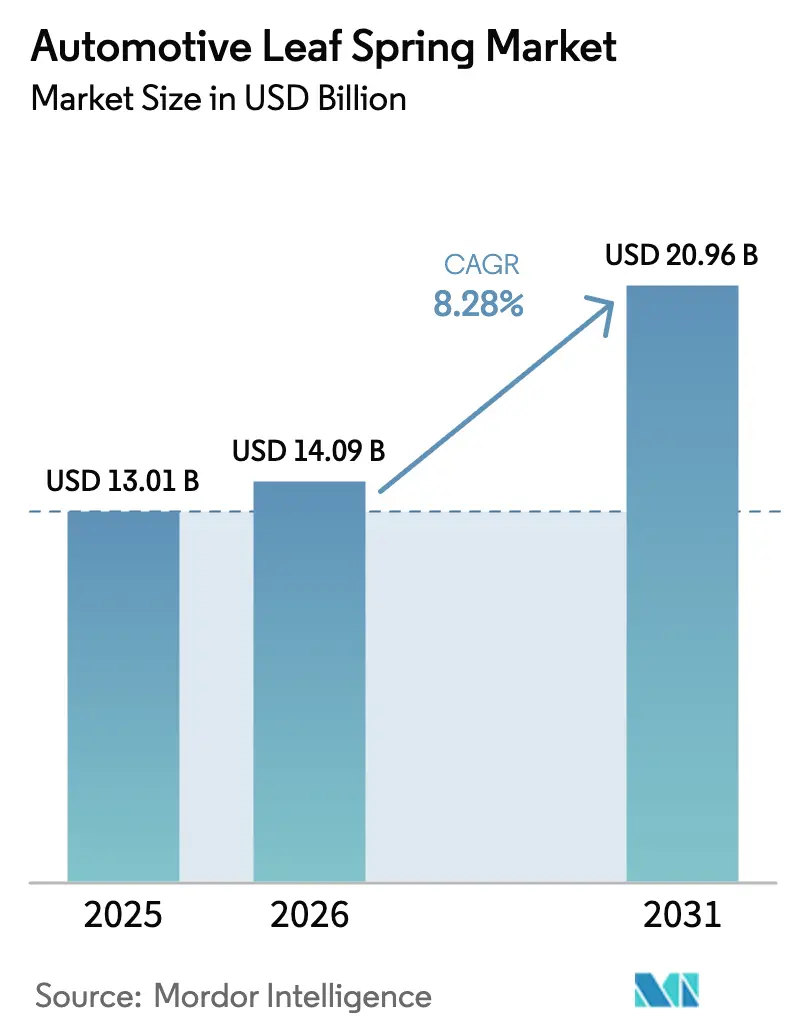

The automotive leaf spring market size in 2026 is estimated at USD 14.09 billion, growing from 2025 value of USD 13.01 billion with 2031 projections showing USD 20.96 billion, growing at 8.28% CAGR over 2026-2031. Demand gains mirror sustained growth in global commercial‐vehicle production, rapid electrification of trucks and vans, and a steady shift toward lightweight materials that enhance payload capacity without compromising durability.[1]International Energy Agency, “Global EV Outlook 2025”, iea.org OEMs specify lighter spring assemblies to offset battery mass, and fleet operators prioritize components that minimize downtime. Supply–chain realignment in North America and Asia’s strong output momentum further widens addressable volumes. Meanwhile, heightened volatility in steel pricing is nudging manufacturers toward composite and hybrid steel-composite designs that deliver double-digit weight savings per vehicle.

Key Takeaways

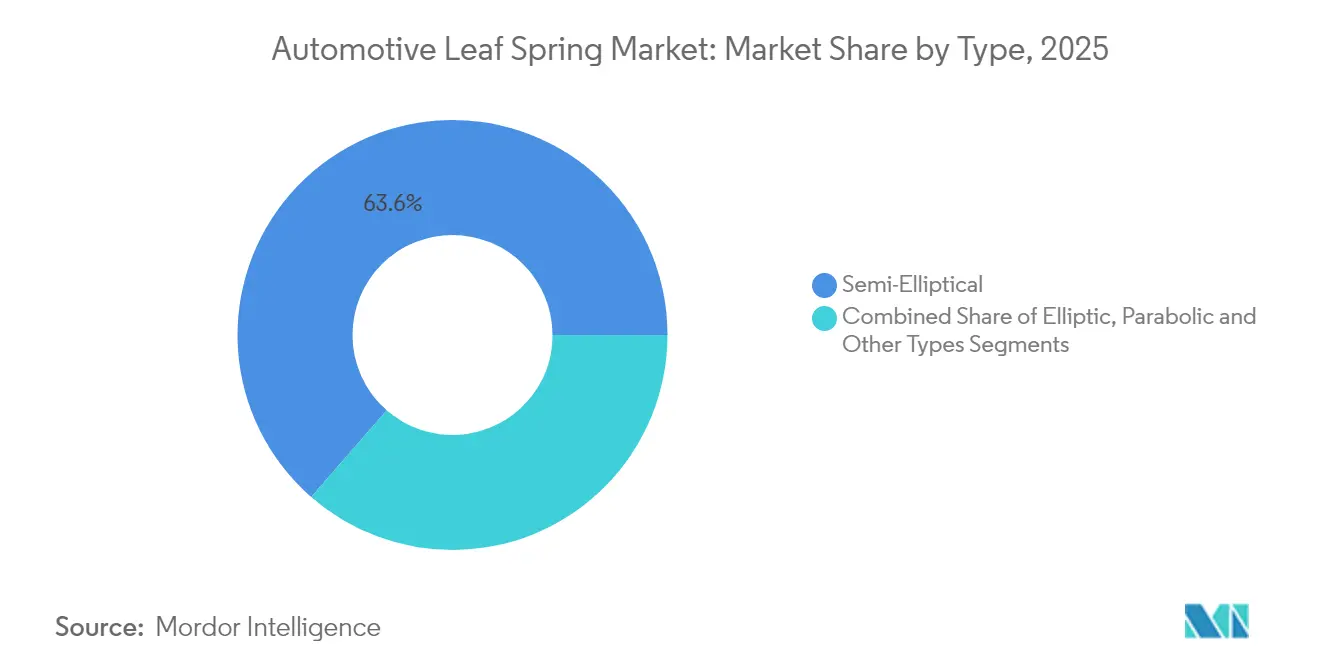

- By spring type, semi-elliptical configurations held 63.58% of the leaf springs market share in 2025, while parabolic designs will post the fastest 7.05% CAGR to 2031.

- By material, steel commanded a 74.68% share of the leaf springs market size in 2025, whereas composites are on track for an 8.19% CAGR.

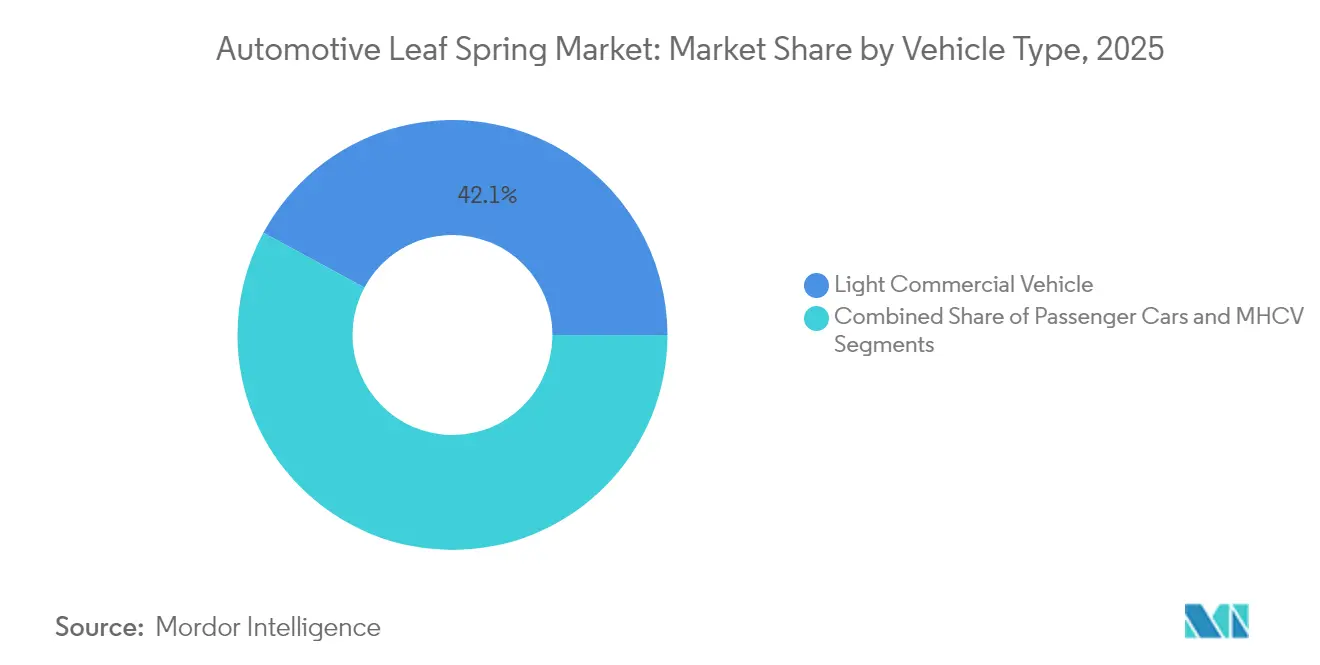

- By vehicle type, light commercial vehicles led with 42.12% revenue share in 2025; the segment is projected to expand at a 9.32% CAGR through 2031.

- By sales channel, OEM installations captured 69.74% share of the global leaf springs market size in 2025; aftermarket revenues are slated for a 6.41% CAGR.

- By region, Asia-Pacific accounted for 44.83% of 2025 revenue and is advancing at a 6.18% CAGR to 2031

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Automotive Leaf Spring Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth in global commercial vehicle production and sales | +2.1% | Global, with APAC core leadership | Medium term (2-4 years) |

| Rising demand for lightweight suspension components for fuel economy | +1.8% | North America & EU, spill-over to APAC | Long term (≥ 4 years) |

| Cost advantage & durability of leaf springs vs. air suspension | +1.4% | Global, particularly emerging markets | Short term (≤ 2 years) |

| Retrofit programs for last-mile electric delivery vans (parabolic packages) | +1.2% | North America & EU urban centers | Medium term (2-4 years) |

| Near-shoring of chassis component supply chains in North America | +0.9% | North America, with Mexico-US corridor focus | Long term (≥ 4 years) |

| Smart leaf springs with embedded load sensors for predictive maintenance | +0.6% | Global, early adoption in premium segments | Long term (≥ 4 years |

| Source: Mordor Intelligence | |||

Growth in Global Commercial-Vehicle Production and Sales

Global commercial-vehicle sales are rising despite macro headwinds, delivering a wider installed base that sustains the leaf springs market. Electric medium- and heavy-duty truck registrations surpassed 90,000 units in 2024, an 80% jump that tilts specification sheets toward custom spring geometries suited for heavy battery packs. Daimler Truck shipped 460,409 vehicles in 2024, underscoring a resilient production pipeline. As total-cost-of-ownership parity between diesel and electric drivelines approaches, fleets accelerate replacement intervals, lifting new-build demand for durable yet lightweight suspension components. The net effect is a sustained pull on leaf-spring orders through 2030

Rising Demand for Lightweight Suspension Components for Fuel Economy

Regulators in North America and Europe continue to tighten fuel-economy norms, prompting OEM engineers to remove every non-essential kilogram from chassis architectures. Composite leaf springs cut up to 92% mass compared with steel, yet retain equivalent stiffness. Ford’s F-150 hybrid steel-composite rear spring trims 16 kg per vehicle, illustrating a viable pathway to aggressive lightweight targets. Advanced high-pressure resin-transfer molding now yields volumes of 900,000 units annually, providing the scale needed for mainstream adoption. Longer fatigue life and inherent corrosion resistance improve lifecycle economics, positioning composites as a core enabler of electrified last-mile fleets.

Cost Advantage & Durability of Leaf Springs vs. Air Suspension

While air suspension penetration in heavy trucks has soared, leaf springs remain the default solution for applications where ruggedness, low acquisition cost, and ease of field repair outweigh ride-comfort gains. Steel-spring sets have 35–50% lower upfront cost than an equivalent air system and can be retrofitted without auxiliary plumbing. The OECD forecasts a 6.7% rise in global steel overcapacity by 2027, likely tempering raw-material prices and preserving the spring’s cost edge [2]Hendrickson International, “Air Suspension Adoption Trends”, hendrickson-intl.com. Fleets operating in harsh terrain value the inherent durability, and electric vehicles appreciate the lower service complexity compared with compressor-based systems.

Retrofit Programs for Last-Mile Electric Delivery Vans (Parabolic Packages)

Urban delivery fleets are adopting parabolic leaf springs that deliver progressive rates, lower NVH, and reduced inter-leaf friction, key for electric vans that carry variable payloads and operate in low-noise zones. Retrofit kit suppliers report premium pricing for these tailored assemblies, offset by improved driver comfort and payload efficiency. Because battery packs shift center-of-gravity profiles, parabolic systems allow chassis tuners to fine-tune ride height without sacrificing cargo volume. European metropolitan clean-air rules catalyze these conversions and reinforce demand visibility through the decade.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift toward air & multi-link suspensions in premium segments | -2.1% | North America & EU premium vehicle segments | Medium term (2-4 years) |

| EU Phase-2 GSR push for active suspension systems | -1.6% | Europe, with potential global spillover | Long term (≥ 4 years) |

| Structural sagging & fatigue over service life | -1.3% | Global, particularly high-usage commercial applications | Short term (≤ 2 years) |

| Volatility in spring-steel alloy prices | -1.0% | Global, with emerging market sensitivity | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Shift Toward Air & Multi-Link Suspensions in Premium Segments

Premium pickups, SUVs, and certain medium trucks increasingly prefer multi-link and electronically controlled air systems that yield superior ride-handling balance. EU safety mandates for active suspension under the General Safety Regulation amplify this tilt by linking compliance to dynamic-ride interventions[3] European Commission, “General Safety Regulation Phase 2 Overview”, ec.europa.eu. The migration diverts a slice of high-margin unit demand away from conventional springs, challenging manufacturers to defend their share by adding smart capabilities or hybridizing designs.

Structural Sagging & Fatigue Over Service Life

Heavy freight cycles expose steel springs to micro-crack propagation and plastic deformation that culminate in ride-height sagging. The outcome elevates tire wear and fuel consumption while eroding driver confidence. Although composites offer higher fatigue thresholds, their premium cost can deter adoption among small fleet operators. High-cycle routes in South and Southeast Asia exemplify this tension, fueling a lively aftermarket for replacement assemblies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Parabolic Designs Gain Electric Vehicle Traction

Semi-elliptical configurations captured 63.58% of the leaf springs market share in 2025, due to decades of proven reliability across heavy trucks, trailers, and off-highway equipment. They anchor the leaf springs market size at USD 13.01 billion in 2025 and continue to defend applications needing maximum load density. The design’s layered architecture distributes stress effectively, supports straightforward maintenance, and benefits from well-amortized tooling.

Although only 23% of 2025 sales are in parabolic springs, they are expanding at a 7.05% CAGR, the fastest within the leaf springs market. The single-leaf, tapered profile eliminates inter-leaf friction and lowers unsprung mass, a desirable trait for battery-electric vans seeking extra range. OEM endorsements from Ford and Daimler signal mainstream acceptance. Variable-rate and progressive-thickness subtypes occupy niche roles in performance pickups and military transports, illustrating design diversity poised to capture specialized use cases through the forecast window.

By Material: Composite Innovation Accelerates Despite Steel Dominance

Steel held 74.68% of global demand in 2025, undergirding the baseline leaf springs market with cost advantages and robust global supply chains. Mature metallurgical grades deliver predictable modulus values and straightforward recyclability, which are key for fleet operators wedded to standardized maintenance practices. Current overcapacity projections from the OECD indicate a mild downtrend in steel pricing, potentially shoring up the material’s cost competitiveness.

Composite alternatives, chiefly glass-fiber-reinforced polymer, are surging at an 8.19% CAGR and could command a double-digit slice of the leaf springs market size by 2031. Rassini’s 900,000-unit capacity line for Ford F-150 rear springs showcases process repeatability at scale. Inherent corrosion immunity, 75–92% mass savings, and longer fatigue life reinforce the value proposition for electric and light-payload vehicles. Hybrid steel-composite packages further blur the line, balancing cost and performance while opening room for embedded sensor arrays that convert passive springs into smart structural members.

By Vehicle Type: Light Commercial Vehicles Drive Market Leadership

Light commercial vehicles (LCVs) delivered 42.12% of 2025 unit revenues, anchoring the leaf springs market through bulk van and pickup volumes. E-commerce acceleration and last-mile delivery focus give LCVs a 9.32% CAGR, the highest among vehicle classes. The frequent stop-start cycles, payload variability, and urban noise limit spotlights parabolic and composite configurations, improving NVH and cut mass.

Medium and heavy trucks account for the lion’s share of steel spring tonnage because of their higher per-vehicle spring count. Heavy truck electrification, evidenced by more than 90,000 global sales in 2024, prompts spec revisions to accommodate extra axle loads. Passenger cars represent a smaller slice yet remain steady in certain pickup and SUV niches where solid-rear-axle layouts persist.

By Sales Channel: OEM Dominance Faces Aftermarket Growth

The OEM channel captured 69.74% of 2025 revenue, reflecting its lock on initial vehicle assembly, where specifications are frozen years in advance. Collaborative design programs between spring makers and chassis engineers ensure fit-for-purpose geometry, weight alignment, and durability targets. As OEMs roll out new electric platforms, they prefer partnering with spring suppliers versed in composite and sensor integration, reinforcing incumbent advantages.

Aftermarket sales generate a 6.41% CAGR, fueled by aging vehicle fleets and higher mileages. Private-equity interest, as seen in MidOcean Partners’ Arnott acquisition, signals accelerating consolidation potential. Retrofit kits tailored for electric van conversions add a fresh layer of demand diversity.

Geography Analysis

Asia-Pacific anchors the leaf springs market at 44.83% in 2025 revenue and is forecast to grow 6.18% through 2031. China’s status as the world’s largest producer of electric heavy-duty trucks, with 80% of 2024 global volume, aligns perfectly with parabolic and composite spring adoption trajectories. Government Production-Linked Incentive schemes and Make-in-India programs spur domestic forging and composite lay-up capacity, enhancing regional self-sufficiency across the leaf springs market.

North America forms the second-largest cluster, energized by a near-shoring push that channels USD 81.2 billion of Mexican auto-parts exports into U.S. assembly plants. Ten manufacturing megaprojects announced since 2019 in Tennessee alone promise localized demand streams. Electrified-fleet adoption by parcel and grocery chains fuels specialized retrofit programs featuring parabolic glass-fiber assemblies that cut downtime relative to air conversions. U.S. tariffs on aluminum and selected steel grades raise near-term uncertainty but concurrently accelerate composite substitution trends.

Europe shows a mixed landscape. Light-vehicle sales rose to 74.6 million units in 2024, yet EU production slipped 6.2% as manufacturers repositioned their footprints. GSR legislation intensifies the pivot toward active chassis technologies, challenging traditional spring makers to embed sensors or collaborate on smart systems. Suppliers such as ZF, are investing in Asia-Pacific and North America to offset regional softness. OEM consolidation and platform rationalization may restrain volume upside but elevate the value per unit by favoring advanced composite designs

Competitive Landscape

Competition is moderate, with the top five suppliers holding significant share, leaving ample space for regional specialists. Hendrickson, Jamna Auto Industries, Rassini, and NHK Spring exploit legacy customer relationships, diverse manufacturing footprints, and expanding composite portfolios to protect their share. Hendrickson parlayed its deep air-suspension knowledge into hybrid leaf packages, proving the capability to straddle both technologies.

Rassini’s joint development with Hexion on epoxy-based composites cut 16 kg from each Ford F-150, highlighting how partnerships can secure flagship contracts. Jamna Auto leverages low-cost Indian forging capacity and an emerging composites line for export pickups. NHK Spring focuses on Japan’s stringent quality environment, preparing smart spring prototypes with embedded load sensors that dovetail with autonomous-driving test beds.

Private-equity investments in aftermarket champions such as Arnott point to profitable roll-up potential in replacement parts. Strategically, suppliers hedge raw-material exposure by dual-sourcing composite feedstocks and adopting scrap-based electric-arc-furnace steel to lower carbon footprints. OEMs reward such moves with sourcing preference as they chase ESG targets.

Automotive Leaf Spring Industry Leaders

Hendrickson USA LLC

Jamna Auto Industries Ltd.

Rassini

Sogefi S.p.A.

NHK Spring Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2024: MidOcean Partners acquired Arnott Industries, adding 800 air-suspension SKUs that cover 90% of factory-equipped vehicles.

- March 2024: DexKo Global Inc. acquired City Spring & Axle Ltd., a key spring manufacturing and distribution player in Western Canada. This strategic acquisition enhances DexKo's presence in the Canadian market, supporting trailer and truck industries with high-quality spring and suspension parts.

- April 2024: Mitsubishi Steel Manufacturing Group strengthened its Springs business in India, doubling production capacity at its joint venture Stumpp Schuele & Somappa Auto Suspension Systems Pvt. Ltd.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

According to Mordor Intelligence, the automotive leaf spring market comprises factory-built steel or composite springs that attach the axle to a vehicle's frame, control ride height, and bear dynamic loads in light, medium, and heavy on-road vehicles, as well as purpose-built off-road trucks. Our study tracks only new springs sold to original-equipment manufacturers and through branded or independent aftermarket channels; refurbishments and air-spring retrofits fall outside the scope.

Scope Exclusions: re-arched or reconditioned springs and air-suspension conversion kits are not covered.

Segmentation Overview

- By Type

- Semi-Elliptic

- Elliptic

- Parabolic

- Other Types

- By Material

- Steel

- Composite

- By Vehicle Type

- Passenger Cars

- Light Commercial Vehicles (LCV)

- Medium & Heavy Commercial Vehicles (MHCV)

- By Sales Channel

- OEMs

- Aftermarket

- By Geography

- North America

- United States

- Canada

- Rest of North America

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- UAE

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed spring manufacturers, chassis engineers at commercial-vehicle OEMs, regional distributors, and fleet maintenance heads across Asia-Pacific, North America, and Europe. These conversations validated service-life assumptions, composite price premiums, and emerging demand from electric delivery vans, closing gaps left by desk research.

Desk Research

We first map the universe using freely available tier-1 data sets, such as OICA light and heavy vehicle production tallies, UN Comtrade HS 7320 trade codes for spring steel, the U.S. Bureau of Transportation Statistics fleet mileage survey, and the European Automobile Manufacturers' Association quarterly registration files. Company 10-Ks, supplier presentations, and patent filings on Questel help us benchmark average spring counts per platform. Dow Jones Factiva keeps our analysts abreast of pricing swings for 55Si7 spring steel and composite laminates. The sources listed are illustrative; many additional public and paid references underpin our evidence base.

Market-Sizing & Forecasting

A blended top-down build, starting with global vehicle output, repair-rate pools, and regional leaf-spring fitment percentages, is cross-checked by selective bottom-up roll-ups of supplier shipments and sampled average selling prices. Key variables include light-commercial-vehicle build rates, parabolic-spring penetration, aftermarket replacement interval, spring-steel input costs, regional freight-ton-kilometer growth, and composite material discount trajectories. Multivariate regression coupled with scenario analysis projects 2025-2030 demand; where unit data are partial, interpolation guided by expert consensus bridges gaps.

Data Validation & Update Cycle

Outputs pass a three-step review: automated variance scans, peer analyst scrutiny, and supervisory sign-off. Reports refresh annually, with interim updates triggered by regulatory shifts or greater than 5% variance in quarterly production or price indices, ensuring clients receive the latest vetted view.

Why Mordor's Automotive Leaf Spring Baseline Commands Reliability

Estimates from different publishers rarely align because each firm frames the market, chooses cost assumptions, and times its refreshes differently. We acknowledge those disparities up front so users grasp the moving pieces.

Key gap drivers include narrower vehicle scopes, omission of aftermarket volumes, static average-selling-price ladders, and infrequent currency realignments adopted by other studies, whereas Mordor applies live exchange rates, yearly ASP recalibration, and a bottom-up sense-check before publishing.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 13.01 Bn (2025) | Mordor Intelligence | - |

| USD 6.24 Bn (2024) | Global Consultancy A | Excludes composite springs and relies on 2021 ASPs |

| USD 5.80 Bn (2024) | Industry Research B | Omits independent aftermarket; limited to MHCV segment |

| USD 7.51 Bn (2024) | Research Firm C | Applies constant 5% annual price uplift without regional mix adjustment |

Taken together, the comparison shows how Mordor's disciplined scope, live pricing inputs, and yearly refresh cadence deliver a balanced, transparent baseline that decision-makers can trace to clear variables and repeat with confidence.

Key Questions Answered in the Report

What is the current size of the leaf springs market?

The leaf springs market size stood at USD 14.09 billion in 2026 and is projected to reach USD 20.96 billion by 2031 at an 8.28% CAGR

Which segment holds the largest leaf springs market share?

Semi-elliptical springs accounted for 63.58% of 2025 revenue, making them the dominant spring type in the global market.

Why are composites gaining traction in the leaf springs industry?

Composite designs deliver up to 92% weight savings, longer fatigue life, and corrosion resistance, helping OEMs meet fuel-economy and electric-vehicle range targets.

Which region is expected to grow the quickest?

Asia-Pacific leads with a 6.18% CAGR thanks to China’s electric-truck boom and India’s expanding component manufacturing base.

What impact do tariffs have on leaf spring costs?

The March 2025 U.S. tariff hike on aluminum and selected steel grades elevates material costs, pushing suppliers to explore composite substitution and localized sourcing.

Page last updated on: