Automotive Fuel Cell Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 9.66 Billion |

| Market Size (2031) | USD 50.21 Billion |

| Growth Rate (2026 - 2031) | 39.02% CAGR |

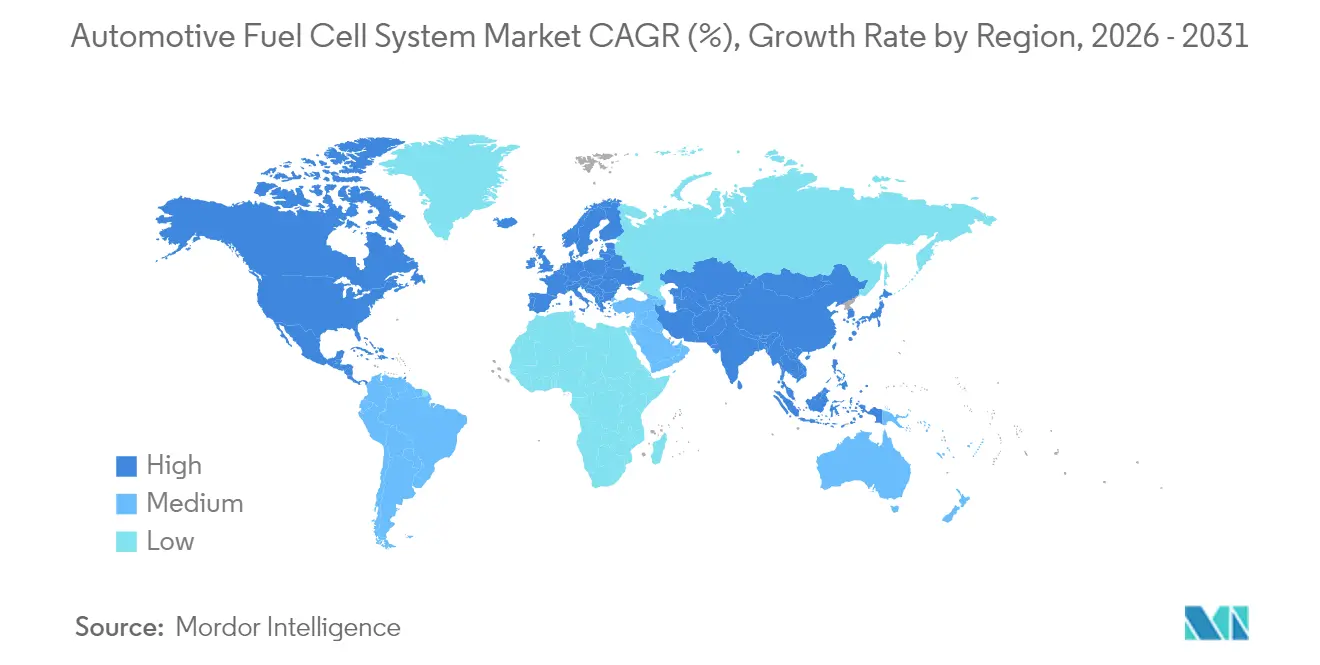

| Fastest Growing Market | Europe |

| Largest Market | Asia-Pacific |

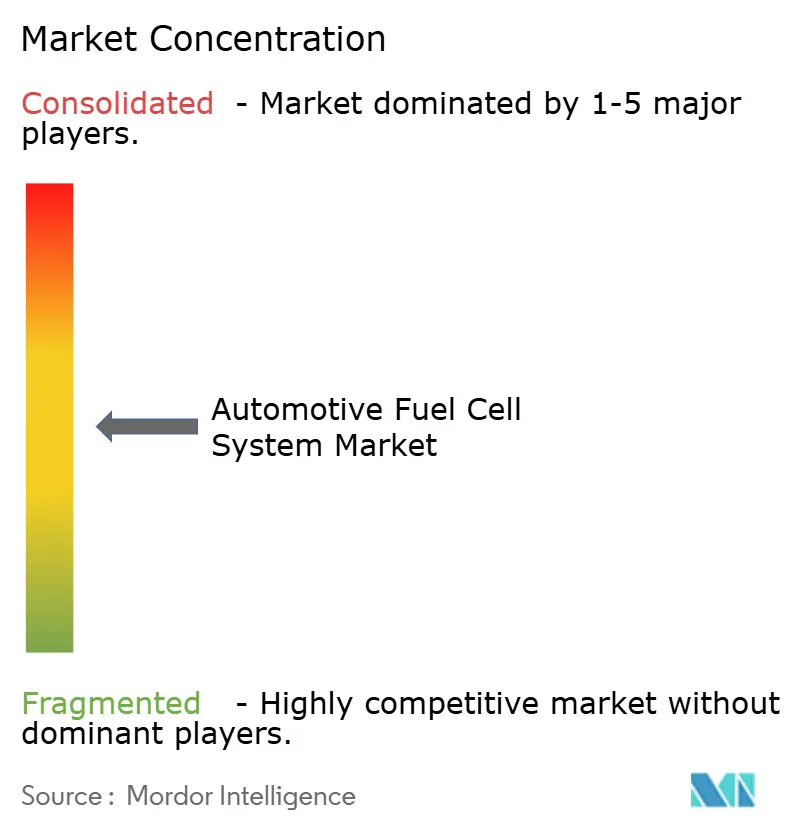

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Automotive Fuel Cell Market Analysis by Mordor Intelligence

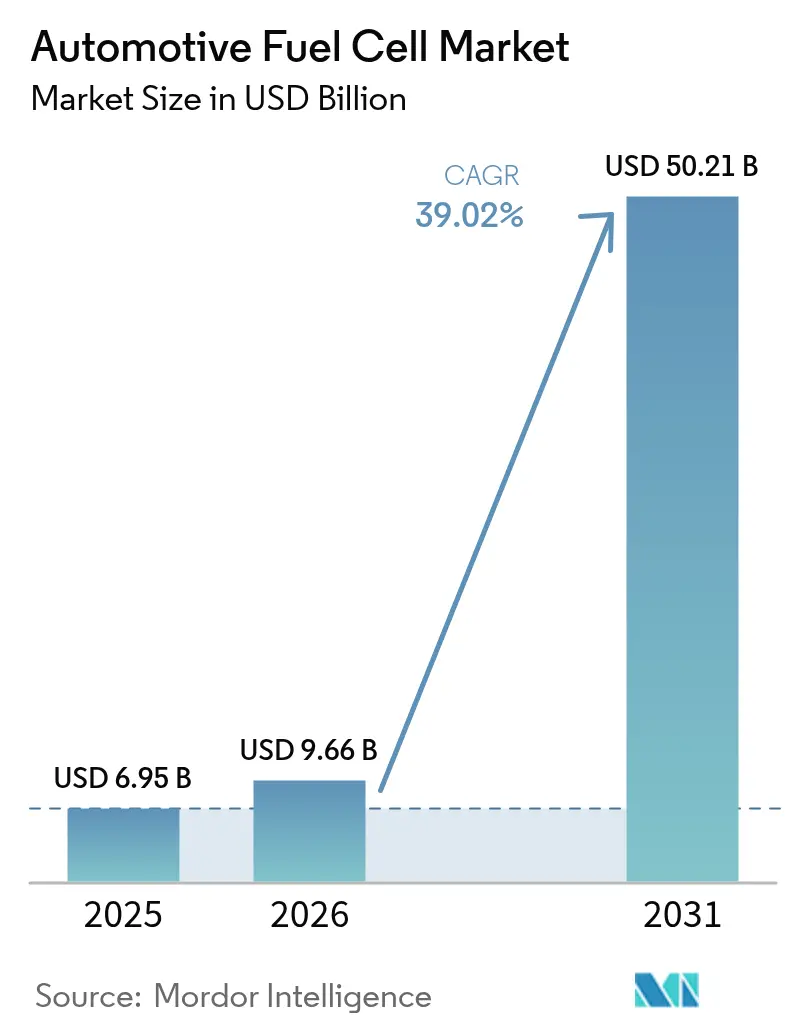

The automotive fuel cell market size was valued at USD 6.95 billion in 2025 and estimated to grow from USD 9.66 billion in 2026 to reach USD 50.21 billion by 2031, at a CAGR of 39.02% during the forecast period (2026-2031). Rising zero-emission vehicle mandates, falling fuel-cell stack costs, and expanding hydrogen corridors are pushing the automotive fuel cell market toward large-scale commercialization. Commercial fleet operators are prioritizing fuel cell trucks and buses to avoid battery weight penalties, while passenger-car programs benefit from technology spillovers. Asia-Pacific leads early adoption thanks to Chinese infrastructure subsidies and Japanese technology leadership, and Europe is accelerating on the back of stringent CO₂ standards. Competitive intensity is increasing as traditional OEMs partner with specialist stack suppliers to de-risk scale-up and secure platinum-group metals.

Key Report Takeaways

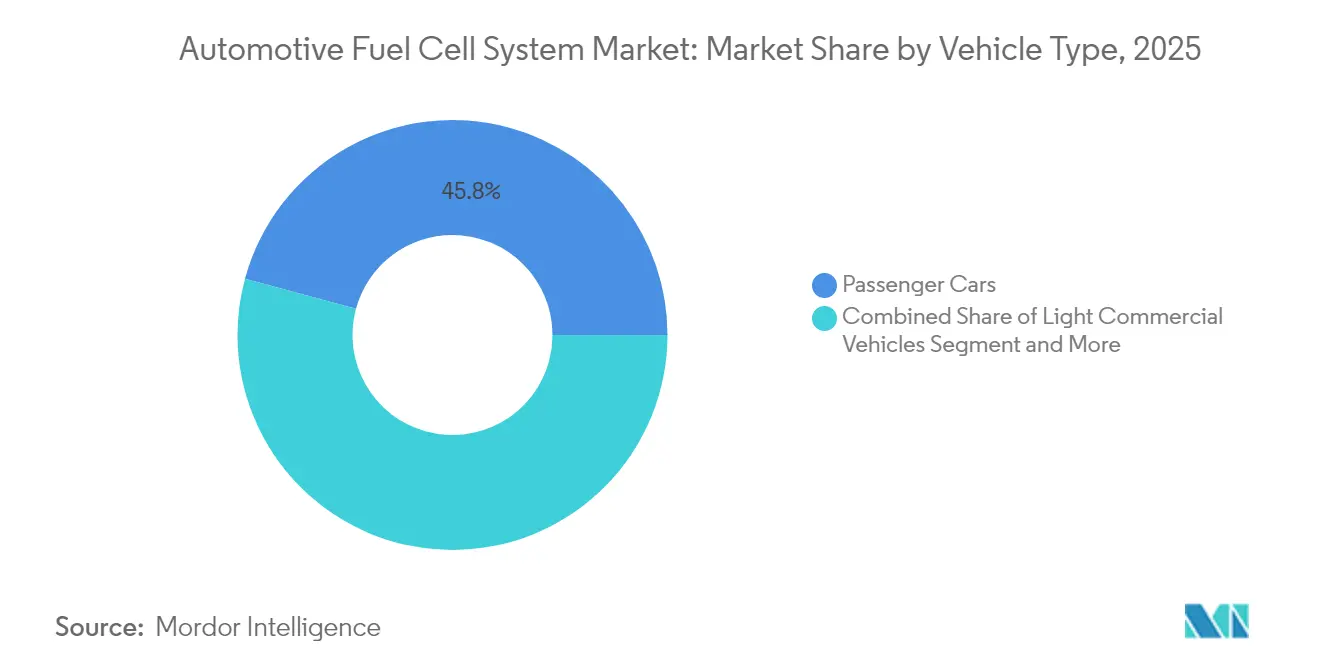

- By vehicle type, passenger cars held 45.78% of the automotive fuel cell market share in 2025, whereas medium- and heavy-commercial vehicles are advancing at a 39.60% CAGR through 2031.

- By drive type, front-wheel-drive configurations commanded 56.30% share of the automotive fuel cell market size in 2025, while all-wheel-drive systems are projected to expand at 26.40% CAGR to 2031.

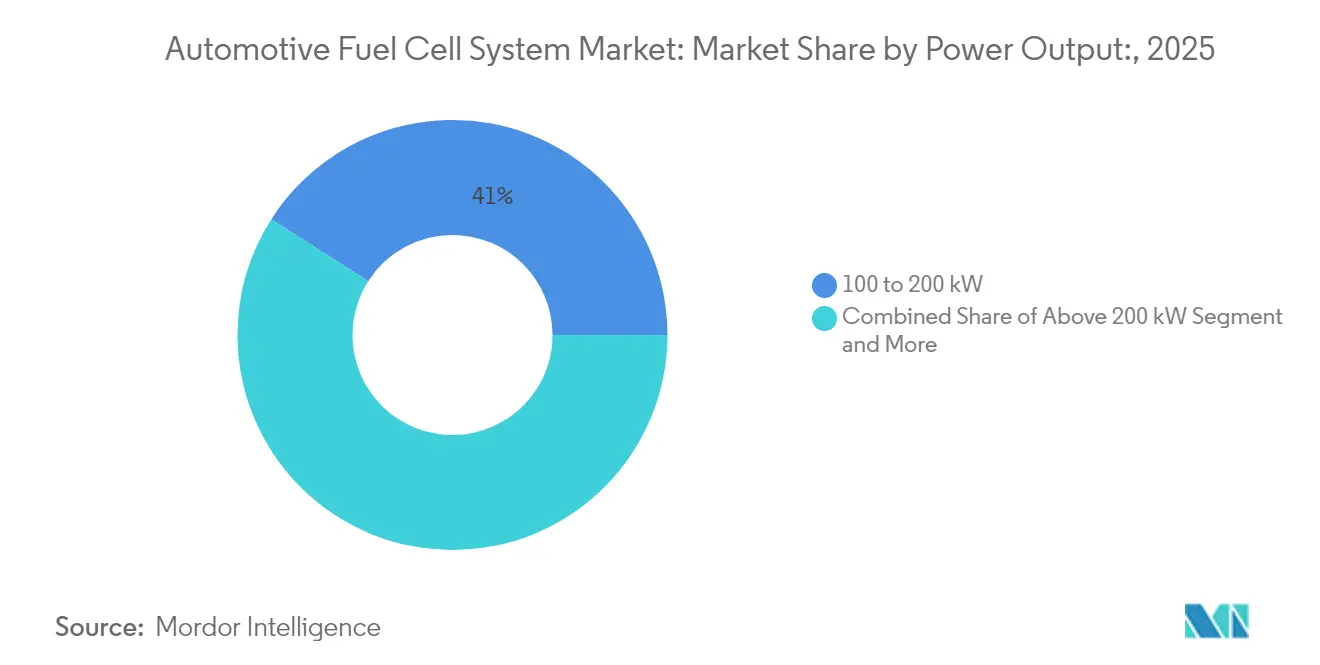

- By power output, 100 to 200 kW systems accounted for a 40.95% share of the automotive fuel cell market size in 2025, and systems above 200 kW are rising at a 30.10% CAGR over the same horizon.

- By propulsion, FCEVs dominated with 91.10% share in 2025, whereas hybrid fuel-cell configurations are expected to register a 32.80% CAGR to 2031.

- By geography, Asia-Pacific led with 53.70% revenue share in 2025; Europe is forecast to grow at a 28.10% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Automotive Fuel Cell Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter CO₂ and ZEV Mandates in Key Auto Markets | +8.2% | Global, with emphasis on EU, California, China | Medium term (2–4 years) |

| Falling USD/kW Stack Costs Due to Scale and Catalyst Thrifting | +7.8% | Global manufacturing hubs: Japan, South Korea, Germany | Short term (≤ 2 years) |

| Rapid Build-Out of Public H₂ Refuelling Corridors | +6.5% | Asia-Pacific core, spill-over to North America and EU | Medium term (2–4 years) |

| Purchase and Tax Incentives for FCEV Fleets | +5.1% | North America, EU, select Asia-Pacific markets | Short term (≤ 2 years) |

| Zero-Emission Long-Haul Fleet MoUs | +4.7% | Global logistics corridors, port cities | Long term (≥ 4 years) |

| Corporate Renewable-H₂ Offtake Contracts Tied to FCEV Uptake | +3.9% | Industrial clusters in developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stricter CO₂ and ZEV Mandates Drive Commercial Fleet Adoption

California’s Advanced Clean Fleets rule and the EU’s heavy-duty CO₂ standards oblige manufacturers and fleets to shift toward zero-emission trucks by the mid-2030s[1]Eamonn Mulholland, "The revised CO2 standards for heavy-duty vehicles in the European Union," ICCT, theicct.org., anchoring demand for fuel-cell drivetrains. Fleet managers value hydrogen’s energy density because every kilogram of battery mass erodes payload revenue. Regulatory certainty accelerates procurement cycles, especially in port drayage and long-haul corridors. OEMs now treat compliance volumes as base demand, unlocking multi-year supply agreements with fuel-cell suppliers. Follow-on infrastructure grants further narrow the total-cost-of-ownership gap versus diesel.

Fuel-Cell Stack Cost Reduction Accelerates Commercial Viability

Toyota’s latest Gen 2 stack lands at USD 45 per kW after a 65% cost slide since 2020, thanks to lower platinum loading and automated membrane-electrode assembly. Volumes above 50,000 units per year support learning-curve effects that target USD 30 per kW by 2027. Durability now exceeds 25,000 hours, easing residual-value concerns for leasing companies. As cost parity approaches, the automotive fuel cell market gains a clearer path to double-digit adoption in heavy-duty segments.

Hydrogen Infrastructure Deployment Creates Network Effects

In 2024, around 125 new hydrogen refuelling stations were opened worldwide: 42 in Europe, around 30 in China, 25 in South Korea, 8 in Japan, and 13 in North America,[2]"Milestone reached: over 1,000 hydrogen refueling stations in operation worldwide in 2024," TUV SUD, tuvsud.com. and is adding one new site every three days under its National Hydrogen Plan. Europe follows with binding targets for 1,000 stations along the TEN-T core network by 2030. Station density along freight corridors reduces range anxiety, boosting fleet asset utilization. Private investors see rising throughput, lifting utilization above the 30% cash-break-even threshold in mature clusters. Each new corridor amplifies demand, reinforcing a positive feedback cycle for the automotive fuel cell market.

Fleet Purchase Incentives Offset Initial Cost Premiums

The U.S. Inflation Reduction Act provides up to USD 40,000[3]"Commercial Clean Vehicle Credit," IRS, irs.gov. per fuel-cell truck and an extra 30% investment tax credit for hydrogen refueling equipment. Germany, France, and South Korea extend similar purchase rebates, compressing payback periods to under four years in many duty cycles. Fleet operators roll incentives into life-cycle cost models that favor fuel-cell adopters over diesel retrofits. Policy makers intentionally concentrate subsidies on heavier classes to prioritize segments where hydrogen is most competitive.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Delivered Cost of Green and Blue Hydrogen | -4.8% | Global, particularly regions without industrial H₂ clusters | Medium term (2–4 years) |

| Sparse Refuelling Infrastructure Outside Pilot Corridors | -3.2% | Rural and secondary markets globally | Short term (≤ 2 years) |

| Platinum-Group Metal Supply-Chain Vulnerability | -2.7% | Global supply chains, concentrated in South Africa | Long term (≥ 4 years) |

| Lengthy Certification of 700-Bar Composite Tanks | -1.9% | Markets with stringent safety regulations | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

High Hydrogen Production Costs Constrain Market Expansion

Green hydrogen averages USD 4–6 per kg, double the cost target for diesel parity in long-haul trucking. Blue hydrogen’s economics hinge on carbon-capture capacity that remains geographically limited. Transportation adds USD 1–2 per kg for delivered hydrogen in markets without pipeline access. Competing industrial offtakers raise price volatility, complicating fleet budgeting. Until renewable electricity prices fall or electrolysis scale improves, the automotive fuel cell market must rely on policy instruments to bridge the gap.

Infrastructure Gaps Limit Geographic Development

Hydrogen refueling remains concentrated in pilot clusters; many rural freight routes still lack a single 700-bar station. Utilization in early-stage markets often sits below 25%, deterring private investors. Station capex near USD 3 million strains ROI when vehicle density is low. Safety approvals for 700-bar composite tanks add further lead time. The resulting chicken-and-egg constraint slows passenger-car rollout and pushes OEMs to focus on captive depot refueling for trucks and buses.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: Commercial Fleets Propel Scale

Passenger cars held a 45.78% 2025 market share, while medium-and heavy-commercial vehicles are pacing at a 39.60% CAGR. Commercial operators prize the quick refueling and long range that hydrogen offers on fixed routes. Total-cost-of-ownership modeling shows break-even against diesel as early as 2027 in California drayage, assuming a delivered hydrogen price of USD 3 per kg. Depot refueling avoids retail infrastructure voids and maximizes truck uptime. Global logistics firms like Amazon, DHL, and UPS have ordered hundreds of fuel-cell box trucks, creating visible scale signals for suppliers.

Passenger-car adoption remains strategic for brand positioning but secondary in volume. Toyota and Hyundai use limited-production sedans to validate durability and familiarize technicians, yet investment focus now tilts to commercial platforms. Municipal transit agencies are rolling out fuel-cell buses on densely trafficked routes, further growing the automotive fuel cell market. Over the forecast window, commercial fleets are set to anchor stack volumes, driving supply-chain maturity that eventually benefits passenger models.

By Drive Type: Performance-Oriented AWD Gains Share

Front-wheel-drive models captured 56.30% share in 2025 because packaging simplicity keeps costs low. Automakers mount stacks under the hood and gas tanks aft, leveraging legacy platforms. All-wheel-drive, however, should grow 26.40% annually as premium brands unveil dual-motor SUVs that promise sports-utility dynamics. BMW’s hydrogen X5 prototype demonstrates superior low-temperature performance versus battery peers, underpinning AWD interest. Rear-wheel-drive trucks exploit under-frame space to house larger hydrogen cylinders without compromising payload.

Drive-type diversity signals maturity: early adopters targeted compliance niches while next-generation line-ups position hydrogen as a performance proposition. Multi-motor torque vectoring enables marketing messages around mountain towing and off-road agility that battery packs struggle to match under high loads. As OEMs migrate fuel-cell modules into skateboard EV architectures, drivetrain flexibility will become a non-issue, further expanding the automotive fuel cell market.

By Power Output: High-Power Modules Meet Heavy-Duty Needs

Systems rated 100–200 kW held 40.95% market share in 2025, aligning with long-range SUVs and regional-haul trucks. Above-200 kW modules, however, are rising at 30.10% CAGR as long-haul tractor units demand diesel-like hill-climb performance. Cummins and Daimler’s joint 300 kW demonstrator has logged 1 million test miles, validating high-thermal-load management. In urban logistics, sub-100 kW stacks suit last-mile vans that cycle continuously between depot and city center.

Hardware modularity lets OEMs stack 30 kW plates into higher-power arrays or mix fuel-cell and battery packs for hybrid load-sharing. Cooling system upgrades, advanced bipolar plates, and boosted air compressors sustain output on steep grades without derating. Capex per kilowatt is falling quicker in the large-module class, narrowing the upfront premium on heavy trucks. Continued power scaling broadens hydrogen’s addressable vehicle classes and cements a diverse supply base in the automotive fuel cell market.

By Propulsion: Hybrids Bridge the Cost Gap

FCEVs controlled 91.10% share of 2025 registrations, yet hybrid fuel-cell setups are forecast at 32.80% CAGR as automakers downsize stacks and buffer power with batteries. Hyundai’s XCIENT concept trims stack size by 20% and taps a 60 kWh lithium-ion pack for acceleration boosts, cutting hydrogen use in urban stop-and-go. The approach lowers per-vehicle platinum demand, easing material-supply risk.

Energy-management algorithms decide whether to pull from the pack or operate the stack at its efficiency sweet spot. This hybridization improves well-to-wheel efficiency in congested traffic while preserving long-range capability for inter-city drives. For cost-sensitive passenger segments, hybrids offer a price bridge until stack costs hit mass-market targets, accelerating consumer acceptance within the automotive fuel cell market.

Geography Analysis

Asia-Pacific generated 53.70% of global revenues in 2025 on the back of China’s National Hydrogen Plan that targets 1 million fuel-cell vehicles by 2030. Provincial subsidies covering 40% of vehicle cost have pulled in OEM joint ventures, while state-owned energy firms fast-tracked 1,200 public stations. Japan’s Green Growth Strategy keeps Mirai sedans in taxi fleets and aims for 900 stations by 2030, sustaining domestic stack demand. South Korea couples a hydrogen production roadmap with Hyundai’s supply-chain cluster, positioning the country as an export hub for 10,000-psi tanks.

Europe is poised for a 28.10% CAGR as Brussels’ Alternative Fuels Infrastructure Regulation obliges member states to build hydrogen stations every 200 km along the TEN-T core network. Germany’s National Innovation Program funds both buses and long-haul trucks, while France links hydrogen refueling sites with renewable electrolysis capacity. Nordic countries pilot hydrogen ferries and heavy trucks that integrate freight, marine, and energy decarbonization. Commercial-vehicle uptake outruns passenger-car rollouts because corporate ESG targets align with ambitious CO₂ reduction pathways.

North America lags in station density but gains momentum from synchronized federal and state incentives. California alone hosts 60% of U.S. public stations and uses the Low Carbon Fuel Standard to subsidize renewable hydrogen at the pump. The Inflation Reduction Act’s USD 3 per kg hydrogen production credit is catalyzing new electrolysis projects in Texas and the Midwest. Canada leverages abundant hydropower to plan export corridors into the U.S. Pacific Northwest, targeting trucking lanes that stretch from Vancouver to Los Angeles. Collectively, these developments indicate converging policy frameworks that underwrite long-term growth for the automotive fuel cell market.

Competitive Landscape

The market remains moderately fragmented, with the top five vehicle-integrating OEMs and the top five independent stack suppliers jointly controlling roughly 55% of shipped capacity in 2024. Toyota and Hyundai anchor passenger platforms, whereas Ballard, Plug Power, and Cummins lead in heavy-duty modules. This dual-track structure forces OEMs without in-house stacks to secure long-term supply deals, such as Volvo’s binding agreement with Cellcentric for 2027 truck volumes. Specialist suppliers differentiate through power density and total-cost-of-ownership guarantees, often bundling hydrogen offtake contracts.

Strategic alliances are multiplying. The Honda–GM Fuel Cell System Manufacturing LLC began serial production in Ohio, sharing plant overheads to halve per-stack costs. BMW sources high-pressure tanks from Faurecia-Michelin joint venture Symbio, underscoring the need for scale in composite cylinder fabrication. Meanwhile, Tier-1 suppliers like Bosch are vertically integrating membrane coating and balance-of-plant electronics, seeking margin capture across the stack subsystem.

New entrants chase white-space applications. Nikola targets sleeper-cab tractors for cross-country routes; Quantron sells fuel-cell conversion kits for diesel truck repowers. Chinese startups such as H-Energy capitalize on domestic subsidies to iterate stack chemistries at high volumes. As M&A intensifies, scale economies are likely to tilt in favor of vertically integrated players, yet niche innovators retain scope in specialty fleets. Sustained cost declines and supply-chain localization will determine long-run positions in the automotive fuel cell market.

Automotive Fuel Cell Industry Leaders

-

Ballard Power Systems Inc.

-

Doosan Fuel Cell Co Ltd

-

Plug Power

-

Nuvera Fuel Cells LLC

-

Cummins Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Toyota Motor Corporation launched commercial production of its next-generation fuel cell system, achieving 65% cost reduction through platinum catalyst optimization and manufacturing process improvements. The system targets integration in heavy-duty commercial vehicles with enhanced durability specifications.

- January 2025: Nikola Corporation announced successful completion of 1 million mile durability testing for its fuel cell powertrain, demonstrating commercial vehicle reliability requirements.

Global Automotive Fuel Cell Market Report Scope

An automotive fuel cell system generates electricity by combining hydrogen and oxygen through an electrochemical process. It powers electric vehicles, emitting only water vapor, making it a promising clean and sustainable transportation technology. Challenges include hydrogen infrastructure, cost, and durability, which are being addressed for wider adoption.

The automotive fuel cell system market is segmented by electrolyte type (polymer electronic membrane fuel cell, direct methanol fuel cell, alkaline fuel cell, and phosphoric acid fuel cell), vehicle type (passenger cars and commercial vehicles), fuel type (hydrogen and methanol), power output (below 100 KW, 100-200 KW, and above 200 KW), and geography (North America, Europe, Asia-Pacific, South America, and Middle-East and Africa).

The report offers the market size and forecasts for automotive fuel cell systems in value (USD) for all the above segments.

| Polymer Electronic Membrane Fuel Cell |

| Direct Methanol Fuel Cell |

| Alkaline Fuel Cell |

| Phosphoric Acid Fuel Cell |

| Passenger Cars |

| Commercial Vehicles |

| Hydrogen |

| Methanol |

| Below 100 KW |

| 100 to 200 KW |

| Above 200 KW |

| North America | United States |

| Canada | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Russia | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Rest of Middle-East and Africa |

| Electrolyte Type | Polymer Electronic Membrane Fuel Cell | |

| Direct Methanol Fuel Cell | ||

| Alkaline Fuel Cell | ||

| Phosphoric Acid Fuel Cell | ||

| Vehicle Type | Passenger Cars | |

| Commercial Vehicles | ||

| Fuel Type | Hydrogen | |

| Methanol | ||

| Power Output | Below 100 KW | |

| 100 to 200 KW | ||

| Above 200 KW | ||

| Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

How large is the automotive fuel cell market in 2026?

The automotive fuel cell market size is USD 9.66 billion in 2026.

What is the forecast CAGR for automotive fuel-cell vehicles to 2031?

The market is projected to grow at a 39.02% CAGR between 2026 and 2031.

Which region leads current fuel-cell vehicle adoption?

Asia-Pacific holds 53.70% of global revenue thanks to Chinese and Japanese programs.

Which vehicle segment is growing fastest?

Medium- and heavy-commercial vehicles are advancing at a 39.60% CAGR through 2031.

What is the biggest barrier to broader FCEV rollout?

High delivered costs of green and blue hydrogen remain the primary constraint on near-term expansion.

Page last updated on: