Gigabit Ethernet Test Equipment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.48 Billion |

| Market Size (2031) | USD 2.01 Billion |

| Growth Rate (2026 - 2031) | 6.38% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Gigabit Ethernet Test Equipment Market Analysis by Mordor Intelligence

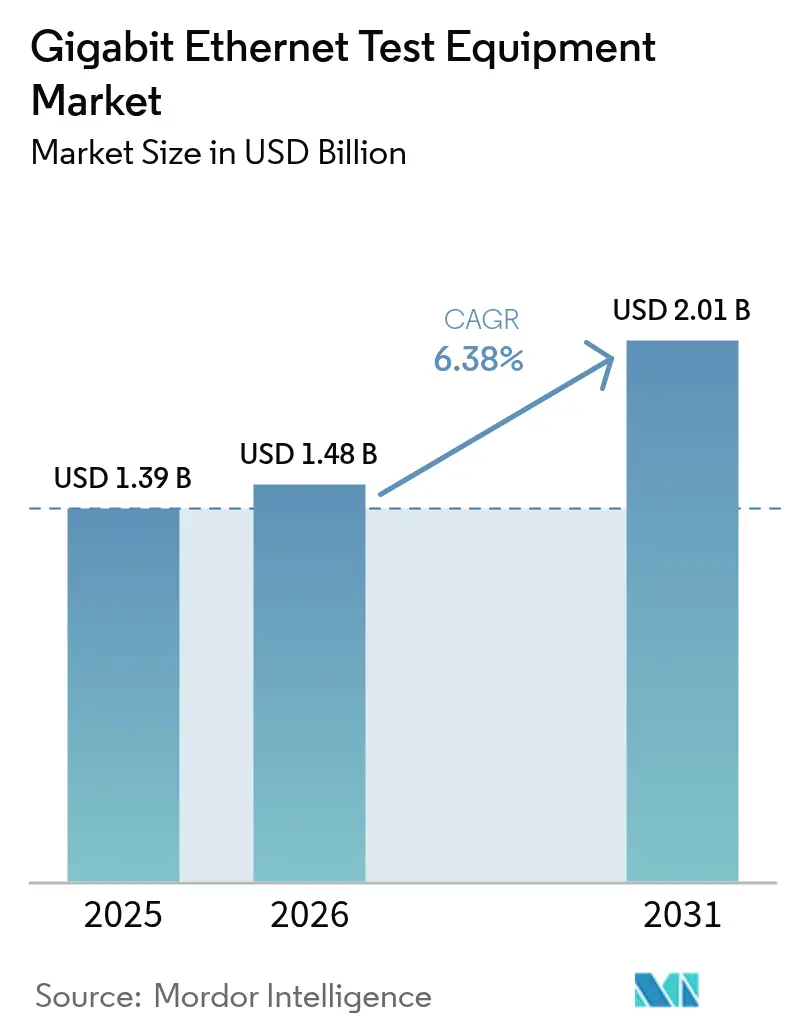

The Gigabit Ethernet test equipment market size is expected to grow from USD 1.39 billion in 2025 to USD 1.48 billion in 2026 and is forecast to reach USD 2.01 billion by 2031 at 6.38% CAGR over 2026-2031.[1]Spirent Communications, “2024–2026 High-Speed Ethernet Outlook,” spirent.com Rising adoption of artificial intelligence workloads is redefining bandwidth expectations, forcing validation teams to move beyond 400G and embrace emerging 800G and 1.6T standards. Data center operators are reallocating budgets from legacy bit error rate tools to high-precision solutions that evaluate packet spray, forward error correction, and RoCEv2 latency under real-world congestion. Hyperscalers now request fully automated test beds that blend traffic generation, network emulation, and machine-learning-driven analytics to shorten development cycles. Supply bottlenecks for PAM4 optics and a shortage of 224 Gbps channel-design experts keep delivery lead times long and price points high, yet vendors that can guarantee early access to 1.6T capability are commanding premium contracts.

Key Report Takeaways

- By test type, performance and stress testing held 37.40% of the Gigabit Ethernet test equipment market share in 2025, while network emulation is projected to expand at 16.45% CAGR through 2031.[2].

- By end-user industry, telecommunications led with 36.05% revenue share in 2025, whereas data centers and cloud providers are advancing at an 17.25% CAGR to 2031.[3].

- By application, field service accounted for 39.20% of the Gigabit Ethernet test equipment market size in 2025, and R&D labs are growing at a 15.95% CAGR through 2031.

- By geography, North America commanded 32.70% revenue in 2025; Asia Pacific is the fastest growing region at a 10.05% CAGR to 2031.

- Keysight, VIAVI, and Anritsu together controlled about 44.60% of global sales in 2025, reflecting intensifying consolidation across ultra-high-speed validation niches.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Gigabit Ethernet Test Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| AI cluster demand for 800G / 1.6T testing | +2.1% | Global, concentrated in North America and China | Medium term (2-4 years) |

| Adoption of cloud services and big data | +1.8% | Global, led by North America and Europe | Long term (≥ 4 years) |

| Growth in mobile backhaul | +1.2% | APAC core, spill-over to MEA | Medium term (2-4 years) |

| Increased Ethernet use in manufacturing | +0.9% | Europe and North America, expanding to APAC | Long term (≥ 4 years) |

| 2.5 / 5 GbE upgrades on legacy cabling | +0.3% | Global, enterprise-focused | Short term (≤ 2 years) |

| RoCEv2-driven ultra-low-latency validation | +0.2% | North America and Europe data centers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

AI Cluster Infrastructure Drives 800G Testing Demand

- Artificial intelligence training pushes bandwidth requirements beyond conventional 400G, compelling operators to adopt 800G and 1.6T links that demand fresh validation strategies. Current clusters need 1 Tbps per xPU, stressing SerDes designs that shift from NRZ to PAM4 modulation, which in turn mandates eye-opening precision for signal-to-noise ratio analysis. Vendors now bundle high-speed oscilloscopes with automated de-embedding software so engineers can characterize sub-10-ps unit intervals in minutes rather than days. The Ultra Ethernet Consortium is finalizing v1.0 specifications that extend beyond IEEE 802.3, adding congestion management tests never seen in legacy Ethernet. Early movers that deliver 1.6T capability are winning multi-year framework deals with hyperscalers eager to future-proof AI fabrics. These projects accelerate revenue for companies able to link optics, traffic generation, and analytics into a single orchestration layer.

Cloud Services Expansion Accelerates Multi-Speed Testing

Cloud providers deploy mixed 100G, 400G, and 800G topologies to balance performance and cost across variable workloads, creating a need for test rigs that validate several speeds concurrently. Forward error correction, particularly RS-FEC, is essential at those rates, so solutions must monitor real-time parity blocks without masking latent defects. Emulation engines now replay days of traffic logs to reproduce microburst congestion while maintaining sub-microsecond latency metrics. Operators request programmable APIs that integrate with CI/CD toolchains, enabling daily regression of network upgrades. The result is rising demand for virtualized test labs that cut hardware capex yet still provide deterministic performance baselines.

Manufacturing Ethernet Adoption Creates Industrial Testing Opportunities

Process industries are migrating to Ethernet-APL at 10 Mbps on two-wire infrastructure, stimulating fresh demand for intrinsically safe compliance testing that merges power and data validation. Time-sensitive networking features such as IEEE 802.1AS and 802.1Qbv require deterministic latency verification, elevating the role of precision timestamp generators. Automotive OEMs continue to extend 100BASE-T1 and 1000BASE-T1 designs toward 10GBASE-T1, and specialized oscilloscopes with automated fixture compensation now dominate lab benches. The industrial wave diversifies revenue away from hyperscale data centers, rewarding vendors with modular platforms able to swap between harsh-environment Ethernet, Industrial Ethernet, and automotive compliance suites. Service labs responding to this shift report double-digit order growth for ruggedized adaptors and field-portable analyzers.

Legacy Infrastructure Upgrades Drive Multi-Gigabit Testing

Enterprises upgrading from 1 GbE to 2.5 G and 5 G on existing Cat 5e / 6 cabling avoid forklift rewires yet still require assurance that NBASE-T links negotiate flawlessly. Multi-rate hand-shakes create new corner cases for auto-negotiation, flow control, and PoE load balancing. The Ethernet Alliance certification program is expanding to validate both data throughput and power delivery at higher wattage budgets, pushing meter probes and thermal sensors into common site acceptance test kits. Portable testers now include integrated cable certification and traffic generation, allowing technicians to replicate R&D grade diagnostics in the field. This upgrade cycle boosts near-term revenue for handheld equipment specialists and drives recurring software license sales for ongoing health monitoring.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lack of technical expertise | -1.4% | Global, acute in emerging markets | Long term (≥ 4 years) |

| Complex measurement accuracy limits | -0.8% | Global, concentrated in high-speed applications | Medium term (2-4 years) |

| Energy and thermal constraints in 800G rigs | -0.6% | North America and Europe data centers | Short term (≤ 2 years) |

| Supply-chain bottlenecks for PAM-4 optics | -0.5% | Global, semiconductor-dependent regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Technical Expertise Shortage Constrains Market Expansion

Moving from NRZ to PAM4 demands engineers competent in de-skewing, symbol error plotting, and 224 Gbps channel modeling, skills still rare across global labor pools.[4]Keysight Technologies, “224 Gbps Channel Characterization Guide,” keysight.com Many service providers rely on automated algorithms to interpret eye height and jitter budgets, yet complex failures still need human insight. Fiber inspection campaigns such as “Inspect Before You Connect” show how deficit skills inflate installation error rates. Training pipelines lag behind technology roadmaps, compelling vendors to embed AI-driven wizards that configure instruments based on minimal user input. Nevertheless, advanced troubleshooting of PAM4 crosstalk, skew, and FEC margin remains a manual discipline, keeping project timelines vulnerable to talent shortages.

Measurement Accuracy Limitations Impede High-Speed Validation

PAM4’s four-level signaling shrinks voltage margins, increasing sensitivity to noise and crosstalk at 800G and beyond. Test platforms must deliver sub-90 fs intrinsic jitter and sustain less than 15 µW optical noise to meet 1.6T requirements, stretching current hardware to physical limits. Optical bandwidth rules shift too, with the IEEE defining a -3 dB e point at half the baud rate for PAM4 rather than three-quarters of the bit rate for NRZ. Achieving consistent results demands temperature-controlled fixtures and advanced DSP filtering that smaller labs often cannot afford. These precision barriers slow equipment adoption in price-sensitive segments and leave some early deployments under-instrumented.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: 800G Platforms Challenge 10 GbE Dominance

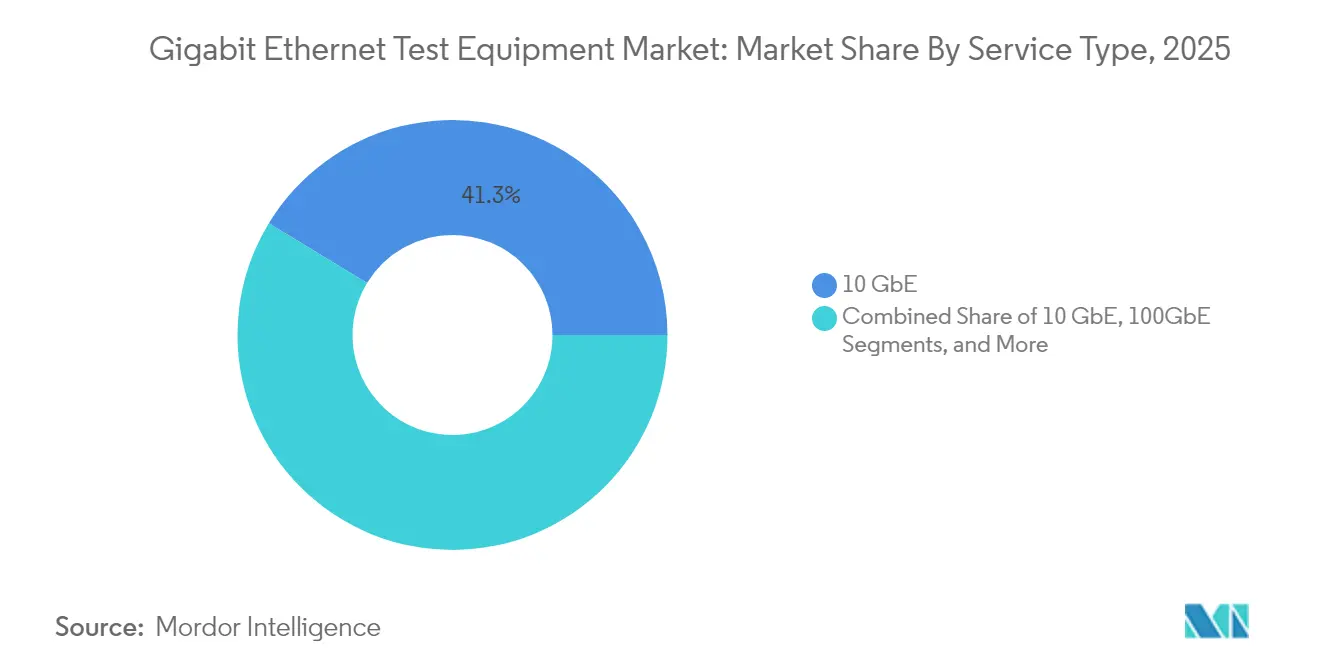

The 10 GbE category retained 41.30% of the Gigabit Ethernet test equipment market share in 2025, underscoring its entrenched presence in enterprise switching backbones. Yet 800 GbE and 1.6 TbE rigs are set to grow at 20.10% CAGR to 2031, the fastest pace of any speed grade, fueled by AI cluster architectures that need line-rate validation at 224 Gbps per lane. Keysight’s AresONE platform streams 6.4 Tbps of test traffic, marking a leap that positions the Gigabit Ethernet test equipment market size for ultra-high-speed gear at USD 548.3 million by 2031, according to Keysight. Meanwhile 25/40/50 GbE and 100 GbE serve as cost-efficient stepping-stones, especially where legacy optics ecosystems lower migration risk. Semiconductor vendors such as Marvell accelerate the shift by sampling 3 nm PAM4 DSPs that drop module power by 20%, extending cooling envelopes inside dense chassis.

Buyers weigh upgrade timing against standards maturity. 400 GbE enjoys mature RS-FEC profiles, so projects chasing rapid returns still favor it. Conversely, engineering labs evaluating 1.6 T are ordering mixed-speed chassis that combine 800 G blades for immediate needs and empty cages ready for future 1.6 T pluggables. This flexibility stabilizes capital planning while protecting early adopters from obsolescence. As hyperscalers roll out fabric upgrades in six-month sprints, vendors that ship field-upgradeable hardware and perpetual software licenses gain recurring revenue streams. The transition compresses product lifecycles, shifting competitive focus from hardware bill-of-materials to programmable feature velocity.

By End-user Industry: Data Centers Accelerate Past Telecommunications

Telecommunications captured 36.05% of 2025 revenue due to 5G backhaul rollouts, yet data centers and cloud providers are expanding at an 17.25% CAGR to 2031, overtaking telcos in absolute spending by 2027. AI workload density drives data centers to validate lossless packet spraying, sub-microsecond jitter, and RoCEv2 congestion control concurrently, all of which exceed traditional telco metrics. Automotive and transport OEMs ramp Ethernet compliance to support driver assistance and autonomous stacks, creating demand for rugged oscilloscopes and EMI chambers capable of 10GBASE-T1 characterization.

Meanwhile, manufacturing outfits accelerate Ethernet-APL pilots within hazardous zones, requiring intrinsically safe testers that double as power loop analyzers. A&D integrators need equipment that withstands vibration, temperature extremes, and electromagnetic pulse, compelling suppliers to adapt military-grade enclosures. Utilities and healthcare specify deterministic fail-safe protocols, pushing test plans to verify zero-loss protection switching and cyber-hardened firmware. These cross-sector nuances pressure vendors to offer modular platforms that slot vertical-specific compliance packages on demand, a strategy that tempers R&D overhead while addressing divergent regulatory frameworks.

By Application: R&D Labs Drive Innovation Testing

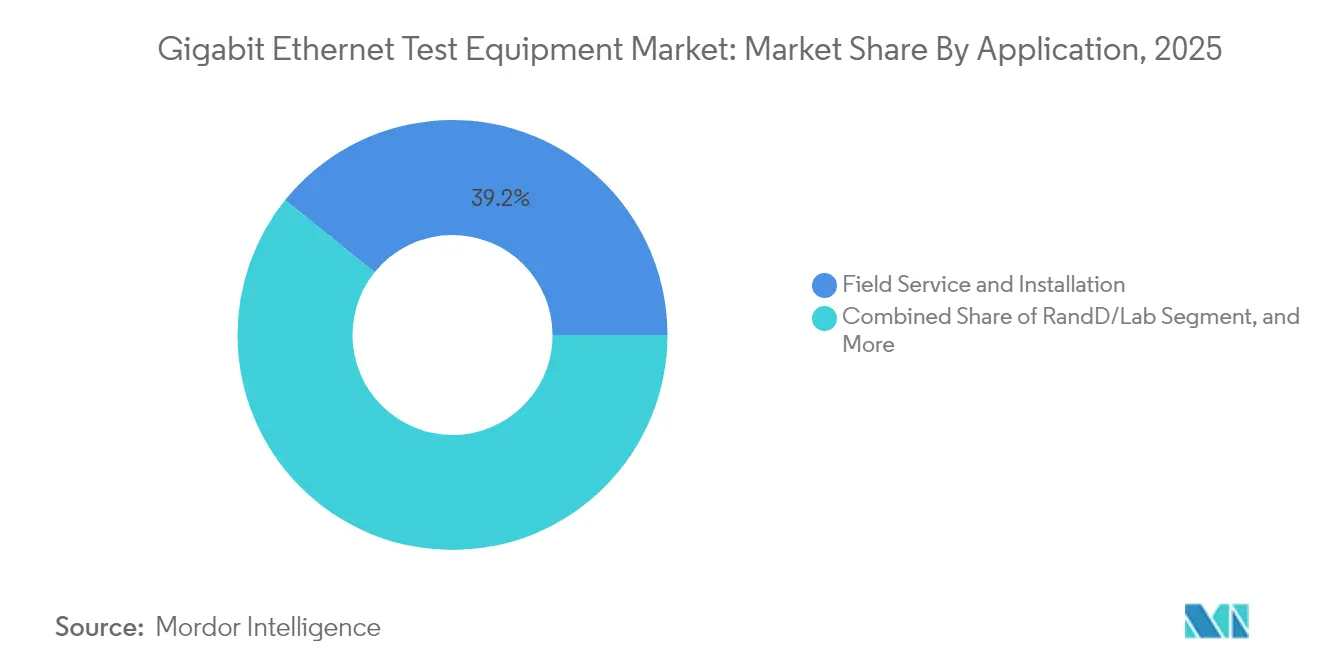

Field service dominated with 39.20% revenue in 2025 as crews troubleshoot multi-vendor networks, yet R&D and lab deployments are rising at 15.95% CAGR, reaching a projected 36.50% revenue share by 2031. Labs now stage full-fabric replicas to validate AI topologies before field rollout, blending traffic generators, optical T&M, and power analytics under a single orchestration dashboard. Handheld testers are mirroring this complexity, integrating packet replay, cable certification, and PoE load-testing to shorten mean-time-to-repair during service calls.

Manufacturing and production sites rely on all-in-one BERTs to certify optical transceiver quality at scale, and the Gigabit Ethernet test equipment market size for production-grade units is forecast at USD 356.4 million by 2031, translating to a 5.08% CAGR. Certification labs expand concurrently, driven by new IEEE sub-clauses for automotive, industrial, and 1.6 T interfaces. Vendors that embed automated standards libraries help users keep pace without manual script updates, reducing compliance cycles from weeks to days.

By Test Type: Network Emulation Emerges as Growth Leader

Performance and stress testing instruments still deliver 37.40% of total sales thanks to their central role in capacity planning, but network emulation is growing at 16.45% CAGR due to its ability to recreate latency, jitter, and packet loss under deterministic control. Organizations running RoCEv2 on AI fabrics need to model congestion tree collapse at microburst scales, scenarios that static BERTs cannot reproduce. Functional and traffic generation suites remain essential for baseline interoperability, while compliance testing rides rising standardization in automotive and industrial IoT.

The Gigabit Ethernet test equipment market benefits from open API frameworks that let DevOps teams spin up virtual ports inside CI/CD pipelines, shrinking test windows from hours to minutes. Meanwhile, university labs such as UNH-IOL define new interoperability plans, offering reference scripts that ship pre-loaded on commercial equipment. These contributions standardize edge-case coverage and mitigate vendor lock-in, although proprietary extensions for congestion telemetry and FEC visibility keep premium licensing models intact.

Geography Analysis

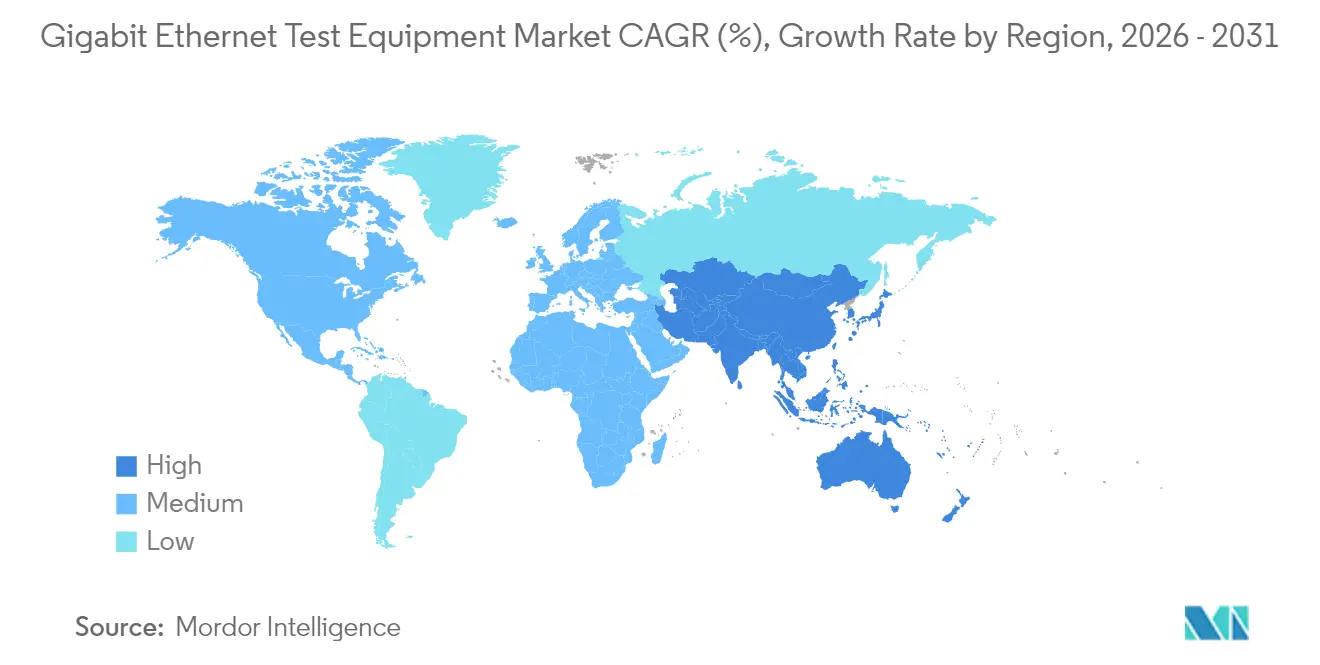

North America holds 32.70% revenue thanks to concentrated semiconductor R&D and aggressive AI cluster deployments that mandate 800G qualification in record time. United States cloud providers anchor most orders, but Canada gains traction through broadband revitalization and industrial Ethernet upgrades. Mexico leverages nearshoring trends to expand automotive harness manufacturing, raising demand for T1 compliance kits. Low energy costs in some states attract additional data center builds, yet the high power draw of 800G rigs prompts sustainability audits that may influence procurement cycles.

Asia Pacific leads growth at 10.05% CAGR on the back of China’s hyperscale expansion and localized 1.6 T optics supply chains. Japan’s auto sector champions deterministic Ethernet stacks that require stringent EMC validation, while Korea pushes semiconductor fabs into 3 nm class, needing ultra-fast jitter and crosstalk probes. ASEAN states deploy 5G backhaul and smart factory pilots, generating orders for multi-rate handheld analyzers. India’s policy incentives spur telco equipment manufacturing and software defined network labs, though patchy infrastructure and a talent shortfall temper near-term adoption.

Europe charts steady gains with German OEMs formalizing in-vehicle Ethernet test plans and industrial operators embracing Ethernet-APL inside process plants. The United Kingdom modernizes fiber backbone networks, fueling demand for portable OTDRs and BERTs. France and Spain invest in renewable energy grid upgrades that require deterministic sub-station Ethernet testing. The Middle East channels oil revenues into greenfield data centers in the Gulf, while African miners commission ruggedized PoE testers for harsh environments. South America remains modest but stable, driven by Brazilian telco upgrades and Argentine automotive wire harness exports.

Regulatory Landscape

Compliance requirements for gigabit and terabit Ethernet testing are shaped by evolving standards and national conformity assessment programs. On the standards side, ITU-T approvals such as Recommendation G.8020.3 (Ethernet, November 2025) and G.8052.1 (management aspects of Ethernet transport, June 2025) reinforce interoperability and manageability expectations that feed into carrier-grade test plans and automation interfaces. For equipment robustness, ITU-T K.147 (July 2023) defines resistibility testing against surge and power fault conditions for information technology equipment interfaces, including Ethernet ports, which in turn informs lab validation and certification workflows.

On the policy and program side, national regulators increasingly link deployment funding and market access to measurable network performance and conformity assessment outcomes. In the United States, FCC and USAC performance measures testing requirements for high-cost broadband programs (including thresholds for speed and latency compliance) raise the value of field and lab instruments that can report throughput and latency metrics in auditable formats. In India, the Telecommunication Engineering Centre (TEC) framework for mandatory testing and certification (MTCTE) and Gazette-notified standards, including revisions published in May 2026 under the Telecommunications (Framework to Notify Standards, Conformity Assessment and Certification) Rules, 2025 (covering items such as LAN switches and firewall test guidance), increase demand for conformance-capable Ethernet test platforms and standardized reporting.

Value Chain Analysis

The value chain starts with standards bodies and interoperability forums that define the test requirements vendors need to implement, then moves into the component and subsystem ecosystem behind high-speed instrumentation. IEEE 802.3 standards activity is a primary upstream driver. IEEE Std 802.3df-2024 defines MAC and PHY parameters for 400 Gb/s and 800 Gb/s operation, while the IEEE P802.3dj project advances 1.6 Tb/s Ethernet definitions that raise performance and signal integrity requirements for test instruments. These roadmaps translate into demand for high-bandwidth analog front-ends, precision timing and clocking, high-speed ADC/DSP, optical interfaces (including PAM4-capable optics), and the software stacks needed for automation, analytics, and API-driven orchestration.

Midstream, test equipment OEMs (such as Keysight Technologies, VIAVI Solutions, Teledyne LeCroy (Xena), Rohde and Schwarz, EXFO, Sifos Technologies, and Aukua Systems) integrate these components into modular chassis, handheld field units, and lab-grade platforms. They also package compliance libraries and automation suites for R&D, manufacturing/production, and certification labs. Downstream, distribution and adoption depend on direct enterprise and hyperscaler sales, partner-led system integration, and test labs that validate interoperability across multi-vendor ecosystems. Plugfests and lab programs are a commercialization bridge, as reflected in the IEEE/Ethernet Alliance interoperability activity hosted at Keysight facilities in Cupertino, California (December 2025), which focused on 224G SerDes conformance and interoperability. PAM4 optics bottlenecks and scarce 224 Gbps channel expertise, highlighted in the market context, act as cross-chain friction points by extending lead times and increasing the value of turnkey, automated test workflows.

Competitive Landscape

Consolidation is reshaping the Gigabit Ethernet test equipment market. Keysight acquired Spirent for USD 1.46 billion, then divested the high-speed Ethernet portfolio to VIAVI for USD 410 million to address antitrust concerns and focus on 1.6 T research. VIAVI now integrates that business with its ONE LabPro platform, enabling 64 × 1.6 T ports per chassis that target AI cluster deployments. Anritsu emphasizes optical transceiver verification and recently added fixed broadband assurance analytics that pivot toward proactive quality-of-experience monitoring.

Technology differentiation hinges on PAM4 fidelity and software-defined test orchestration. Keysight’s new DCA-M sampling scopes deliver sub-90 fs jitter, capturing lane integrity at 120 GBaud without external clock recovery. Lumentum introduces 400 Gbps-per-lane InP chips and efficient 200 Gbps PAM4 lasers aimed at lowering optical power budgets inside AI fabrics. Marvell’s Ara platform moves the silicon node to 3 nm, slicing optical module power by one-fifth and enabling denser switch cards. Emerging players such as Candela Technologies and EXFO compete on flexible software stacks that spin virtual ports in public clouds, a model appealing to mid-tier operators that want subscription billing rather than capex.

Standardization forums have become a strategic arena. The Ultra Ethernet Consortium now counts more than 100 companies, including optics suppliers, silicon houses, and test vendors, all vying to shape congestion management rules that dictate future instrument features. Early participation helps vendors pre-align hardware roadmaps, cutting time to revenue when final specs release. However, the specialized skills and capital required for sub-pico-second measurement still create high barriers to entry, anchoring incumbent leadership even as smaller firms aim to carve software niches.

Gigabit Ethernet Test Equipment Industry Leaders

Anritsu Corp.

Spirent Communications PLC

Keysight Technologies Inc. (Ixia)

Viavi Solutions Inc.

Exfo Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A key whitespace sits at the intersection of terabit Ethernet standardization and practical multi-vendor interoperability, where buyers want repeatable validation across optics, switches, and link management. Current ecosystem signals include the Ethernet Alliance publishing its 2026 Ethernet Roadmap (December 2025), covering 100G to 800G interconnects and emerging 1.6 Tb/s Ethernet, alongside multi-vendor demonstrations at OFC 2026 that highlighted high-speed Ethernet technologies including 1.6T solutions. Together, they support opportunities for test platforms that package end-to-end workflows, electrical and optical characterization, and network emulation for congestion and RoCEv2-style behavior into CI/CD-friendly, API-driven environments.

Opportunities extend beyond hyperscale data centers into regulated and compliance-heavy deployments where test documentation and conformance drive purchasing decisions. In automotive and industrial domains, newly approved IEEE standards expand the addressable set of conformance and validation needs, including IEEE 802.3dk-2026 (April 2026) for multi-gigabit optical automotive Ethernet and IEEE 802.3dg-2026 for single-pair Ethernet with management parameters and power delivery considerations. For telecom infrastructure validation, ETSI TS 138 176-1 V19.2.0 (February 2026) for 5G NR Integrated Access and Backhaul, conducted via conformance testing, reinforces demand for setups that pair Ethernet transport validation with telecom conformance processes, benefiting vendors that can combine packet performance testing, timing/latency measurement, and automated compliance reporting in one workflow.

Recent Industry Developments

- June 2026: Keysight Technologies completed the acquisition of VPIphotonics to expand its photonic design automation portfolio with system-level simulation capabilities. The acquisition strengthens Keysight's ability to support end-to-end optical link design and validation workflows that underpin high-speed Ethernet transceiver and interconnect development. It connects instrument-based test with pre-silicon and pre-build photonic modeling, helping customers correlate simulated and measured performance at advanced data center link speeds.

- October 2025: VIAVI Solutions closed its acquisition of Spirent Communications plc's High-Speed Ethernet, Network Security, and Channel Emulation testing business from Keysight for USD 425 million. Folding these assets into VIAVI's network test portfolio expands its position in high-speed Ethernet validation and channel emulation, which are central to lab qualification and data center ecosystem interoperability testing. The deal also increases competitive intensity for incumbent high-speed Ethernet test vendors by broadening VIAVI's depth in both hardware and software-led test capabilities.

- March 2025: Keysight Technologies completed the acquisition of Spirent Communications plc. The transaction added Spirent's test and assurance capabilities to Keysight's portfolio, strengthening coverage across traffic generation, network emulation, and security testing workflows used by telecom and data center customers. This consolidation step also set the stage for subsequent portfolio actions tied to regulatory review and strategic focus in ultra-high-speed Ethernet validation.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers purpose-built Gigabit Ethernet test equipment used to generate, impair, capture, and analyze Ethernet traffic over copper or optical media, mainly for lab validation, manufacturing tests, data center turn-up, and in-service network checks.

Scope exclusions: We exclude purely software analyzers that run on a host NIC without dedicated physical-layer test interfaces.

Segmentation Overview

- By Type

- 1 GbE

- 10 GbE

- 25/40/50 GbE

- 100 GbE

- 400 GbE

- 800 GbE and 1.6 TbE

- By End-user Industry

- Telecommunications

- Data Centers and Cloud

- Manufacturing

- Automotive and Transport

- Aerospace and Defense

- Others (Utilities, Healthcare)

- By Application

- RandD/Lab

- Manufacturing/Production

- Field Service and Installation

- Certification and Compliance

- By Test Type

- Functional / Traffic Generation

- Performance / Stress

- Compliance / Conformance

- Network Emulation

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- South Korea

- ASEAN

- Rest of Asia Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- UAE

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research is used to set the boundaries of what counts as test equipment and to build the first set of demand indicators that the model must match. We mainly rely on public, non-paywalled sources such as FCC equipment authorization databases, IEEE Ethernet standards releases, ITU and ISO publications, and trade and customs statistics (where relevant for instruments and components). We also use peer-reviewed journals and conference proceedings to understand how test needs change as speeds, modulation, and optics move forward.

To translate the technology picture into market math, we review company filings, annual reports, investor decks, product documentation, and reputable press coverage of lab expansions and network rollouts. A limited set of paid subscriptions is used only for company financials, patent lookups, and shipment-level import-export checks when public detail is not specific enough. These desk sources are illustrative, and many other public documents and datasets were also reviewed to fill gaps and validate assumptions.

Primary Interviews and Surveys

Primary work is used to pressure-test the desk assumptions, especially around what customers actually buy, replacement cycles, and how pricing changes when higher port density and higher speeds are adopted. We speak with a mix of instrument suppliers, channel partners, labs, data center operators, and telecom teams across APAC, EMEA, and the Americas, then align the findings back to the model inputs so the final view stays consistent.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 28% | CXOs: 15% | APAC: 52% |

| Mid tier: 54% | Functional/Unit leaders: 42% | EMEA: 29% |

| Smaller Players: 18% | Managers: 43% | Americas: 19% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where equipment demand is reconstructed from the installed base of Ethernet networks and test points that must be verified across lab, production, and field use. In practice, the model is anchored on measurable signals such as data center build-outs and upgrades, the pace of enterprise switching refresh, carrier transport and access investments, and the rollout of higher-speed Ethernet links that increase testing intensity.

Those demand signals are then converted into revenue using pricing logic, where average selling prices are adjusted by form factor and port density and checked against observed discounting and mix shifts from interviews. To keep totals realistic, selective bottom-up approximations are also used, including sampled unit volumes by equipment class and channel checks on typical order sizes, and gaps are handled by applying conservative penetration ranges that are rechecked with experts. For the forecast, scenario analysis is applied around capex cycles and speed-transition timing, and assumptions are reviewed with primary respondents so growth does not overshoot what supply capacity and customer budgets can support.

Data Validation & Update Cycle

Model outputs are cross-checked against independent signals such as equipment shipment direction, publicly discussed lab capacity additions, and the pace of Ethernet standard adoption, which helps flag step changes that look too sharp. When variances show up, the driver is traced back to the specific input (for example, speed mix, pricing, or replacement timing) and then corrected through a second review before sign-off.

Reports are refreshed annually, and interim updates are triggered when material events occur, such as major product launches, large network upgrade announcements, or sudden currency movements that change reported revenues. Before delivery, a final analyst pass is completed so clients receive an updated and internally consistent view of the market.

Mordor Intelligence's Gigabit Ethernet Test Equipment Market Size Compared With Other Published Estimates

Published market sizes for Gigabit Ethernet test equipment often vary even when the topic label looks the same, since each publisher may draw the line differently on what counts as dedicated hardware versus adjacent software tools. Timing also matters because this market has meaningful price mix shifts, and a single year can move based on when higher-speed modules and dense port platforms get adopted.

The spread usually comes from refresh cadence and how pricing is carried forward, since discounts, bundle structures, and currency conversion timing can change the reported value even if unit demand is similar. Another common gap is scope, where some figures may mix in nearby Ethernet speeds or broader network test categories, and then the total is not fully revalidated against real-world procurement behavior.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.39 B (2025) | |

| Global Consultancy A | USD 1.50 B (2025) | Often carries forward pricing with broad inflation factors and wider test-instrument scope, which can lift totals when higher-speed modules and adjacent network test tools are blended into one revenue pool. |

| Industry Publisher B | USD 1.30 B (2024) | Uses an earlier-year snapshot and may rely on limited validation for discounting and product mix, which can understate the step-up from newer high-density platforms and updated currency conversion timing. |

Looking at the table, the difference is mainly explained by timing and boundary choices, followed by how pricing and mix are updated into the current year. By updating currency timing and average selling price assumptions during the review cycle and rechecking them through interview validation, Mordor Intelligence keeps the estimate tied to what buyers are actually paying for dedicated GbE test instruments.

Key Questions Answered in the Report

What is the current value of the Gigabit Ethernet test equipment market?

The market is valued at USD 1.48 billion in 2026 and is projected to reach USD 2.01 billion by 2031, reflecting a 6.38% CAGR over 2026-2031.

Which test type is growing the fastest?

Network emulation leads with a 16.45% CAGR because it replicates real-world congestion and latency scenarios required for AI clusters.

Which region is expanding most quickly?

Asia Pacific shows the highest growth at a 10.05% CAGR, fueled by large-scale data center builds in China and advanced automotive Ethernet testing in Japan.

Why are 800G and 1.6T standards important?

AI workloads demand up to 1 Tbps per accelerator, so data centers are migrating from 400G to 800G and 1.6T links that need new validation methodologies.

How is consolidation shaping the competitive landscape?

Keysight’s acquisition of Spirent and subsequent divestiture to VIAVI signal intensified M&A activity as vendors seek specialization in ultra-high-speed testing niches.

What are the main challenges facing the market?

Talent shortages in PAM4 signal integrity, supply constraints for PAM4 optics, and measurement accuracy limits at 224 Gbps channels are key restraints hindering rapid deployment.

Page last updated on: