Automotive Engine Encapsulation Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

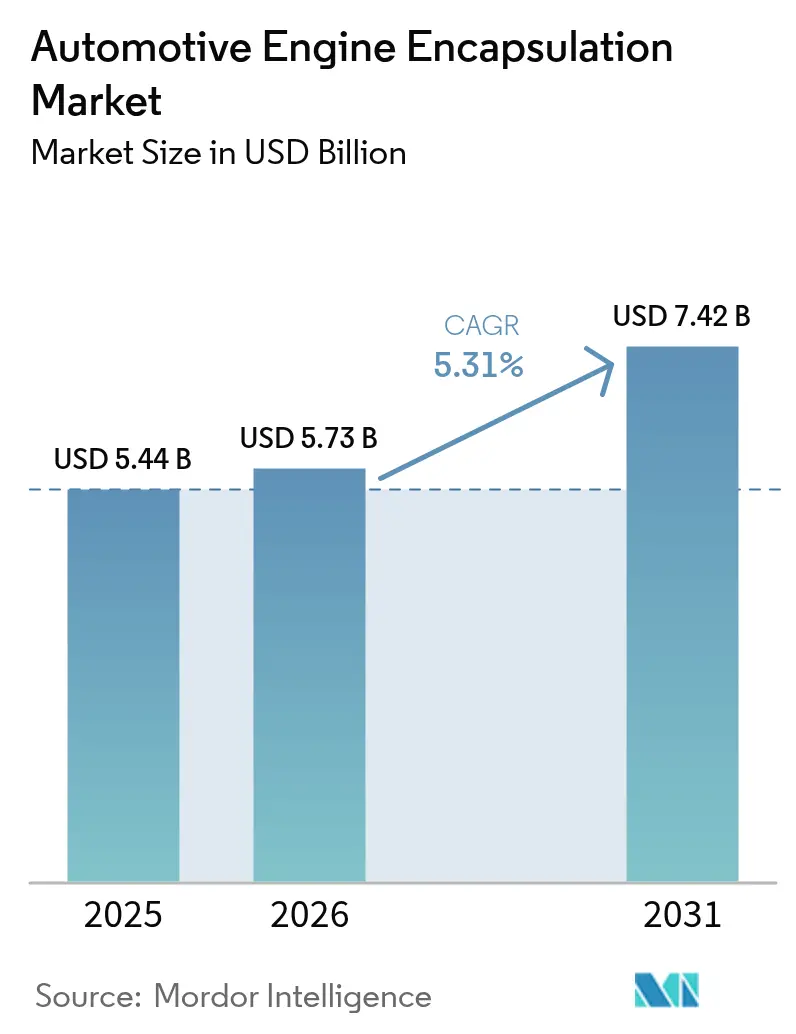

| Market Size (2026) | USD 5.73 Billion |

| Market Size (2031) | USD 7.42 Billion |

| Growth Rate (2026 - 2031) | 5.31% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive Engine Encapsulation Market Analysis by Mordor Intelligence

The automotive engine encapsulation market size is expected to grow from USD 5.44 billion in 2025 to USD 5.73 billion in 2026 and is forecast to reach USD 7.42 billion by 2031 at 5.31% CAGR over 2026-2031. Demand accelerates as Euro 7 regulations tighten cold-start CO₂ limits, premium brands chase library-quiet cabins, and hybrid powertrains require sophisticated under-hood thermal control. Automakers adopt gigacasting and digital-twin design loops that merge structural, thermal, and acoustic functions, cutting component counts while boosting thermal efficiency. Material strategies pivot toward recyclable thermoplastics to meet circular-economy mandates, and carbon-fiber cost declines open lightweight options for mid-volume models. Suppliers form alliances with battery-thermal specialists to bridge ICE and EV requirements as the automotive engine encapsulation market navigates the combustion-to-electric transition.

Key Report Takeaways

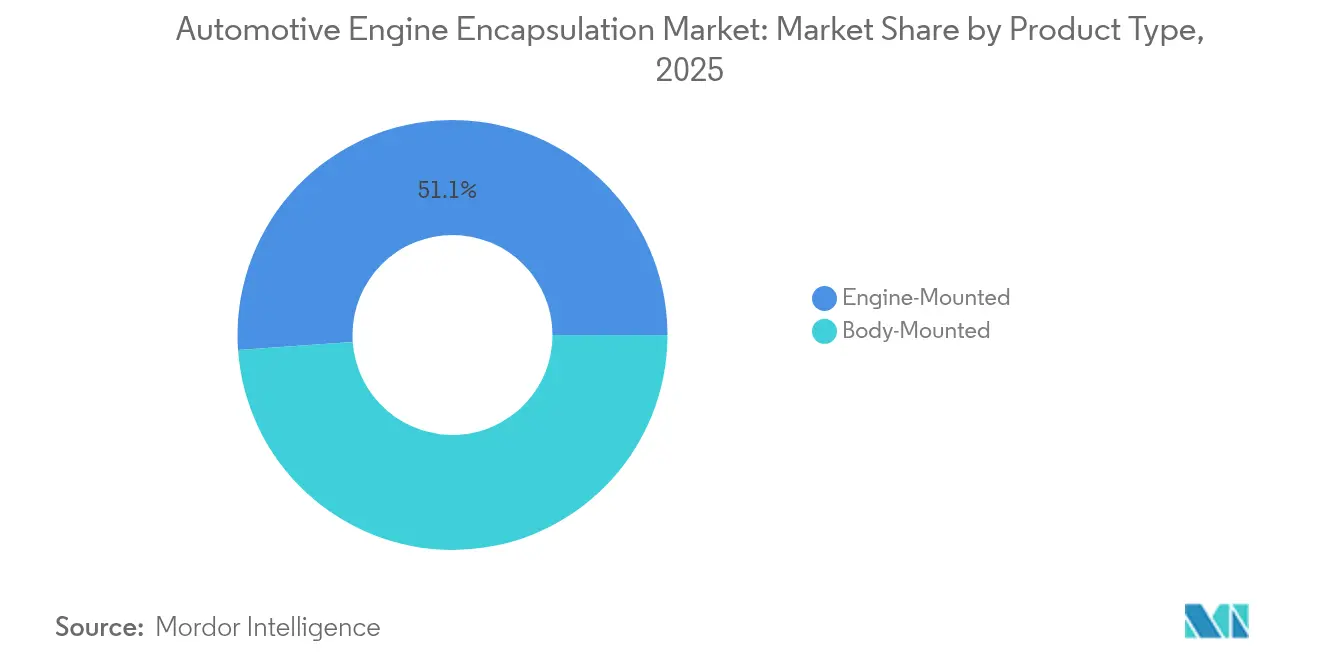

- By product type, engine-mounted solutions led with 51.12% of the automotive engine encapsulation market share in 2025, while body-mounted designs are expanding at a 7.26% CAGR to 2031.

- By fuel type, gasoline engines held a 65.20% share of the automotive engine encapsulation market size in 2025, while electric powertrains are moving at a 7.61% CAGR.

- By material type, carbon fiber captured 33.85% share of the automotive engine encapsulation market size in 2025, and polypropylene is advancing at an 7.78% CAGR through 2031.

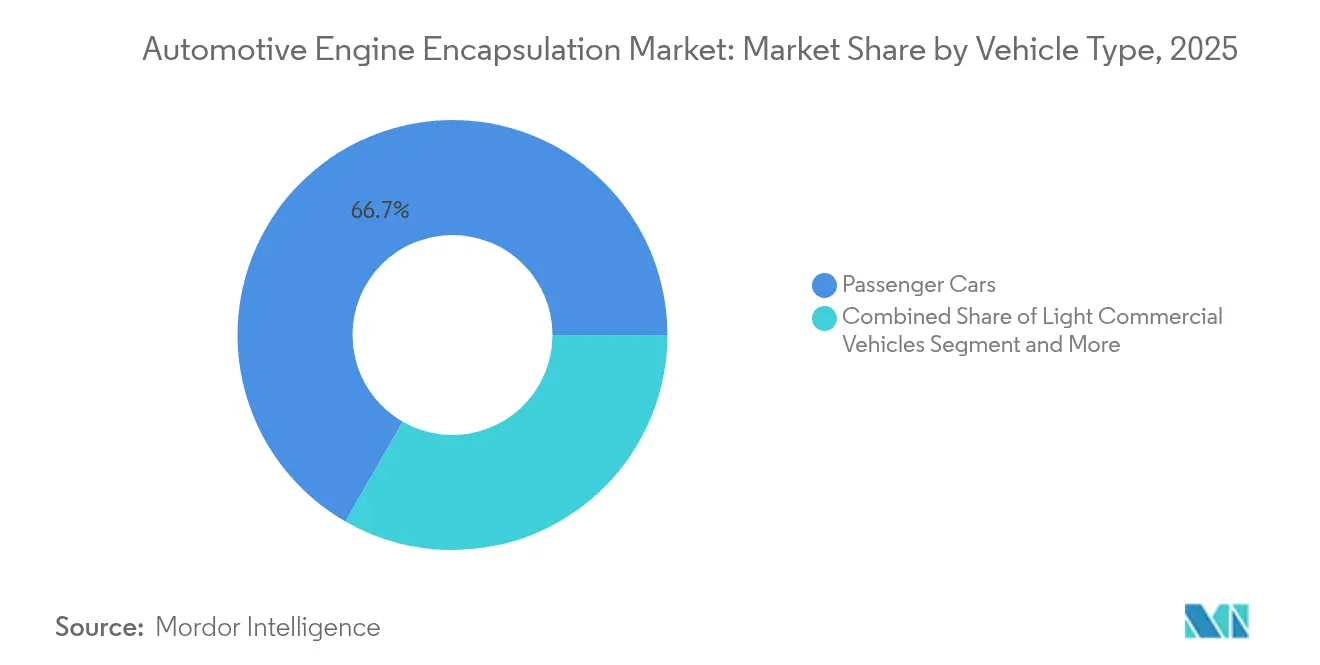

- By vehicle type, passenger cars accounted for 66.70% of the automotive engine encapsulation market size in 2025 and are growing at a 6.57% CAGR.

- By sales channel, OEM-fitted systems commanded 85.60% share of the automotive engine encapsulation market size in 2025 and are rising at a 6.85% CAGR.

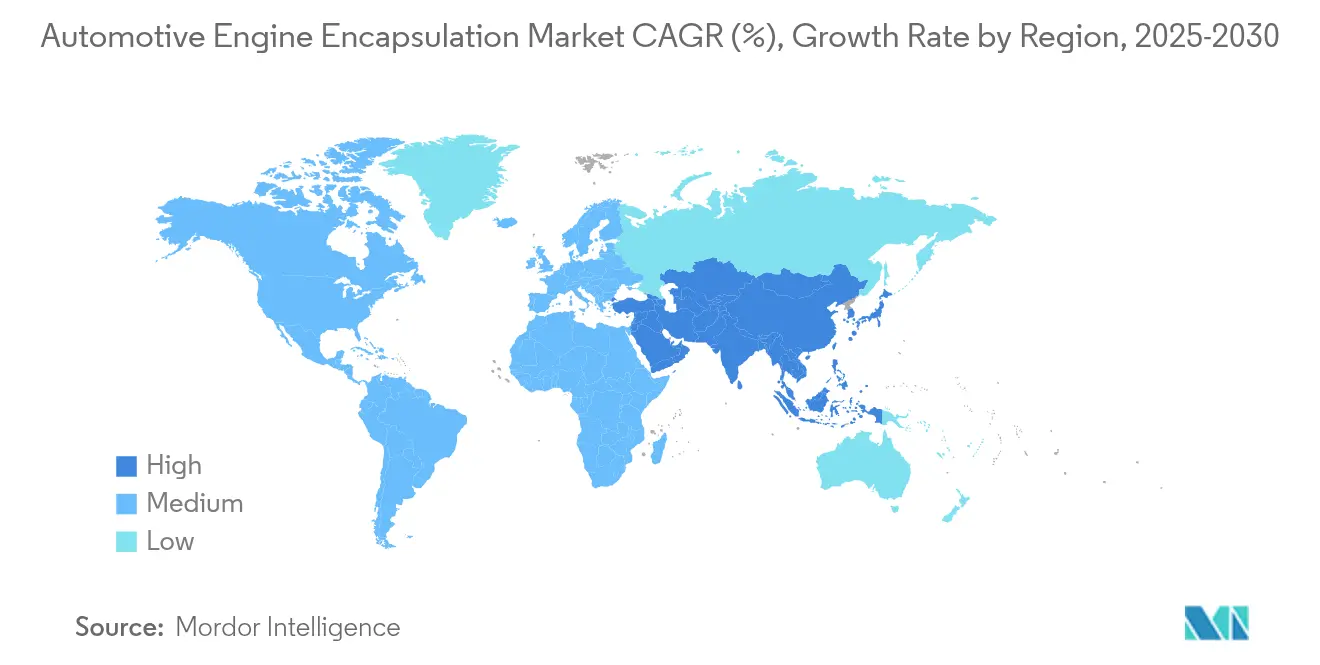

- By geography, Asia-Pacific dominated with 48.10% automotive engine encapsulation market share in 2025; it also posts the fastest 8.18% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Automotive Engine Encapsulation Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter post-Euro 7 Cold-start CO₂ Targets | +1.2% | Europe with spillover to APAC and North America | Medium term (2-4 years) |

| Premium-brand Shift to Library-quiet Cabins | +0.8% | Global luxury segments | Short term (≤ 2 years) |

| Battery Pre-conditioning Needs in PHEVs | +0.7% | APAC core, expanding to Europe and North America | Medium term (2-4 years) |

| Lightweight Carbon-fiber Cost Inflection | +0.6% | North America and Europe, selective APAC adoption | Long term (≥ 4 years) |

| Gigacasting Enables Larger Body Solutions | +0.9% | Global, led by premium EV OEMs | Short term (≤ 2 years) |

| OEM Digital Twins Optimize Thermal Maps | +0.4% | North America and Europe, gradual APAC adoption | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stricter Post-Euro 7 Cold-Start CO₂ Targets

Euro 7 takes effect for new vehicle types in November 2026 and extends compliance to 200,000 km, putting cold-start emissions under unprecedented scrutiny.[1]Applus IDIADA, “Euro 7 Regulatory Impact Assessment,” idiada.com Automakers now need encapsulation that accelerates warm-up times and dampens engine noise across ambient ranges from -7°C to 35°C. The requirement pushes hybrid material stacks that blend carbon-fiber structures with phase-change layers, securing emission compliance without sacrificing acoustics.

Premium-Brand Shift to Library-Quiet ICE Cabins

Luxury marques target idle cabin noise below 40 dB, mirroring silent EV experiences. Multi-layer encapsulation with aerogel barriers achieves noise reduction coefficients above 0.9 while sustaining thermal insulation. Programs now extend beyond engines to transmission tunnels, treating the full powertrain as one acoustic source for a unified solution.

Battery Pre-Conditioning Needs in PHEVs

PHEVs must keep batteries within 20-30°C and isolate them from adjacent ICE heat. Encapsulation systems integrate phase-change materials that store excess heat during combustion peaks, then release it in EV mode, optimizing range and cell longevity. Digital-twin simulations accelerate these designs by mapping thermal cross-talk before hardware builds.

Lightweight Carbon-Fiber Cost Curve Inflection

Recycled carbon fiber now delivers 80% of virgin strength at half the cost, lowering the entry point for mass-market encapsulation.[2]MDPI Journals, “Advances in Carbon-Fiber Recycling,” mdpi.com Automated fiber placement boosts throughput and supports complex geometries, mirroring Tesla’s carbon-wrapped motor scale-up.

Restraints Impact Analysis of Automotive Engine Encapsulation Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid BEV Power-train Mix Diluting ICE Volume | -1.8% | Global, faster in Europe, and China | Short term (≤ 2 years) |

| Petro-chemical Price Volatility for Foams | -0.9% | Global, hitting cost-sensitive segments | Medium term (2-4 years) |

| Limited Recyclability of Multi-layer NVH | -0.6% | Europe and North America | Long term (≥ 4 years) |

| Engine-bay Packaging Conflicts in Downsized ICEs | -0.4% | Global, focused on compact cars | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid BEV Power-Train Mix Diluting ICE Volume

BEV penetration in new car registration across Europe hit 15.40% in 2024 and is forecast to be above 50% by 2030, shrinking demand for ICE-specific encapsulation. Suppliers must reinvest profits from declining ICE programs into EV-thermal products or face margin erosion.

Petro-Chemical Price Volatility for Polymer Foams

Polypropylene and polyurethane feedstocks swing 25-40% in price, yet materials form 60-70% of encapsulation cost. BASF’s bio-based polyurethane trials ease petroleum exposure but currently carry 15-20% premiums that mainstream models cannot absorb.[3]BASF SE, “Bio-Based Polyurethane Solutions,” basf.com

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Automotive Engine Encapsulation Market Segment Analysis

By Product Type:

Body-Mounted Solutions Drive Integration InnovationEngine-mounted encapsulations led the automotive engine encapsulation market with a 51.12% share in 2025. These modules excel at vibration isolation because they sit directly on the power unit, enabling rapid warm-up and line-side installation. Body-mounted designs are accelerating at 7.26% CAGR and increasingly cast into large underbody sections, supporting platform consolidation and lowering assembly time.

Body-mounted encapsulation integrates acoustic barriers with structural members, improving stiffness while sealing the engine bay. This format dovetails with gigacast underbodies that eliminate multiple brackets and fasteners. Suppliers must formulate materials that tolerate die-casting thermal cycles without delamination. Consequently, the automotive engine encapsulation market size for body-mounted solutions is projected to expand steadily through 2031.

By Fuel Type:

Electric Powertrains Drive Innovation Despite Gasoline DominanceGasoline engines accounted for 65.20% automotive engine encapsulation market size in 2025, supported by their prevalence in global passenger fleets. Encapsulation for gasoline units emphasizes rapid warm-up and idle noise suppression.

Electric powertrains exhibit the briskest 7.61% CAGR because hybrids and range-extended models blend battery cooling with combustion insulation. Suppliers engineer dual-purpose barriers that protect cells from engine heat spikes while muting inverter whine. Diesel remains for torque-intensive use cases but faces cost headwinds due to after-treatment complexity.

By Material Type:

Polypropylene Gains Ground Through Recyclability AdvantagesCarbon fiber retained 33.85% automotive engine encapsulation market share in 2025, favored in premium and performance cars for its stiffness-to-mass ratio. Recycled carbon fiber feedstock and automated layup reduce cost barriers, positioning the material for mid-segment adoption.

Polypropylene is scaling fastest at 7.78% CAGR thanks to its closed-loop recyclability and compliance with the EU End-of-Life Vehicles Directive. The automotive engine encapsulation market size for polypropylene composites is tied to OEM sustainability targets, while polyurethane remains entrenched in foam liners that balance weight and damping. Polyamide and glass wool maintain niche roles for high-heat and low-cost applications, respectively.

By Vehicle Type:

Passenger Cars Maintain Dominance Through Volume ScalePassenger cars held 66.70% of the automotive engine encapsulation market share in 2025 and are growing 6.57% through 2031. High global production volume and uniform acoustic targets drive standardized encapsulation specifications that lower per-unit costs.

Light commercial vehicles adopt similar NVH solutions to meet urban noise ordinances, while medium and heavy trucks focus on thermal durability rather than decibel performance. The automotive engine encapsulation market size for passenger cars benefits from emerging-market assembly growth that offsets BEV migration in developed regions.

By Sales Channel:

OEM Integration Dominates Through Manufacturing EfficiencyOEM-fitted systems held 85.60% of the automotive engine encapsulation market share in 2025 and are set to expand with a 6.85% CAGR through 2031. Factory installation assures tight tolerances, simplifies warranty accountability, and lets engineers tune NVH during platform development.

Aftermarket demand focuses on fleet retrofits and replacement parts where extended service life warrants NVH upgrades. Still, high installation labor and acoustics validation limit aftermarket penetration. Consequently, the automotive engine encapsulation market size continues to tilt toward OEM channels as assembly plants integrate encapsulation steps into automated body lines.

Geography Analysis

APAC Automotive Engine Encapsulation Market

Asia-Pacific led the automotive engine encapsulation market with 48.10% share in 2025 and is advancing at 8.18% CAGR. China’s dominance derives from vast vehicle output and policy-driven hybrid growth that prolongs ICE encapsulation demand even in an EV-centric roadmap. India’s production-linked incentives lure suppliers to localize encapsulation, combining cost competitiveness with duty advantages.

Europe and North America Automotive Engine Encapsulation Market

Europe is leveraging Euro 7 regulations to drive advanced solutions for cold-start emissions. This, coupled with the widespread adoption of hybrids, underscores the continued relevance of internal combustion engines (ICE). Carbon-fiber and digital-twin tools mature here first, then migrate globally, reinforcing the region’s thought leadership. North America grows steadily on the back of SUV and pickup sales that use larger powertrains, which need robust thermal-acoustic barriers.

MEA and South America Automotive Engine Encapsulation Market

The Middle East and Africa, and South America, remain emerging pockets. They rely on imported NVH kits or CKD assembly, yet rising local output attracts suppliers establishing greenfield plants. Altogether, the automotive engine encapsulation market continues regional consolidation around APAC capacity while Europe drives specification trends embraced worldwide.

Competitive Landscape

The automotive engine encapsulation market shows moderate concentration. Tier-one NVH specialists, diversified chemical conglomerates, and composite technology start-ups vie for a share. Market leaders leverage global footprints and integrated material supply to satisfy OEM just-in-time schedules. Mid-sized players differentiate with proprietary acoustic foams or fiber formulations targeted at premium segments.

Strategic focus shifts to systems that fuse thermal shielding, acoustic damping, and crash protection, reducing part count. Partnerships between composite material producers and die-casters speed up the entry into giga-cast architecture. ElringKlinger doubled its E-Mobility revenue in 2024 while maintaining ICE product cost leadership, illustrating a dual-lane strategy.

Capital expenditure trends favor automation and closed-loop recycling lines that cut scrap and carbon intensity. Suppliers that secure raw material backward integration in polypropylene and recycled carbon channels gain margin insulation when petrochemical prices spike. Competitive success will depend on scaling next-gen encapsulation before ICE decline outpaces revenue pivot capacity.

Automotive Engine Encapsulation Industry Leaders

Autoneum Holding AG

BASF SE

Continental AG

ElringKlinger AG

Adler Pelzer Group

- *Disclaimer: Major Players sorted in no particular order

Automotive Engine Encapsulation Market Companies Covered in this Report

- Autoneum Holding AG

- Continental AG

- ElringKlinger AG

- BASF SE

- 3M Company

- Rochling Group

- Adler Pelzer Group

- Trocellen Automotive

- Woco Group

- SA Automotive

- Charlotte Baur Formschaumtechnik GmbH

- Sumitomo Riko Co. Ltd

- Sika Automotive

- Pritex Ltd

- UGN Inc.

- Langfang Sound (China)

Recent Industry Developments in Automotive Engine Encapsulation Market

- May 2025: Autoneum launched a thermoplastic impact-protection plate that shields EV batteries while providing thermal insulation to extend range.

- August 2024: Autoneum opened a fully owned Pune plant producing carpet systems, wheelhouse liners, and e-motor encapsulations for Indian and export OEMs.

- July 2024: Hutchinson debuted an NVH encapsulation product that attenuates high-frequency e-compressor and motor noise for upcoming electric and hybrid models.

Global Automotive Engine Encapsulation Market Report Scope

Segmentation Overview

| Engine-Mounted |

| Body-Mounted |

| Gasoline |

| Diesel |

| Electric |

| Carbon Fiber |

| Polyurethane |

| Polypropylene |

| Polyamide |

| Glasswool |

| Passenger Cars |

| Light Commercial Vehicles |

| Medium and Heavy Commercial Vehicles |

| OEM-Fitted |

| Aftermarket |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| New Zealand | |

| Rest of Asia-Pacific | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Egypt | |

| Turkey | |

| South Africa | |

| Rest of Middle East and Africa |

| By Product Type | Engine-Mounted | |

| Body-Mounted | ||

| By Fuel Type | Gasoline | |

| Diesel | ||

| Electric | ||

| By Material Type | Carbon Fiber | |

| Polyurethane | ||

| Polypropylene | ||

| Polyamide | ||

| Glasswool | ||

| By Vehicle Type | Passenger Cars | |

| Light Commercial Vehicles | ||

| Medium and Heavy Commercial Vehicles | ||

| By Sales Channel | OEM-Fitted | |

| Aftermarket | ||

| Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Egypt | ||

| Turkey | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the automotive engine encapsulation market?

The automotive engine encapsulation market size stands at USD 5.73 billion in 2026 and is projected to grow to USD 7.42 billion by 2031, representing a 5.31% CAGR.

Which region leads the automotive engine encapsulation market?

Asia Pacific commands 48.10% market share and shows the fastest 8.18% CAGR thanks to China’s scale and India’s rapid capacity additions.

Why are body-mounted encapsulations gaining traction?

Gigacasting underbodies allow larger single-piece aluminum sections that integrate acoustic and thermal barriers, prompting a 7.26% CAGR for body-mounted solutions through 2031.

Which material segment is growing fastest?

Polypropylene encapsulations expand to an 7.78% CAGR as automakers prioritize recyclable thermoplastics to comply with circular-economy directives.

Page last updated on: