Automotive Display Panel Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

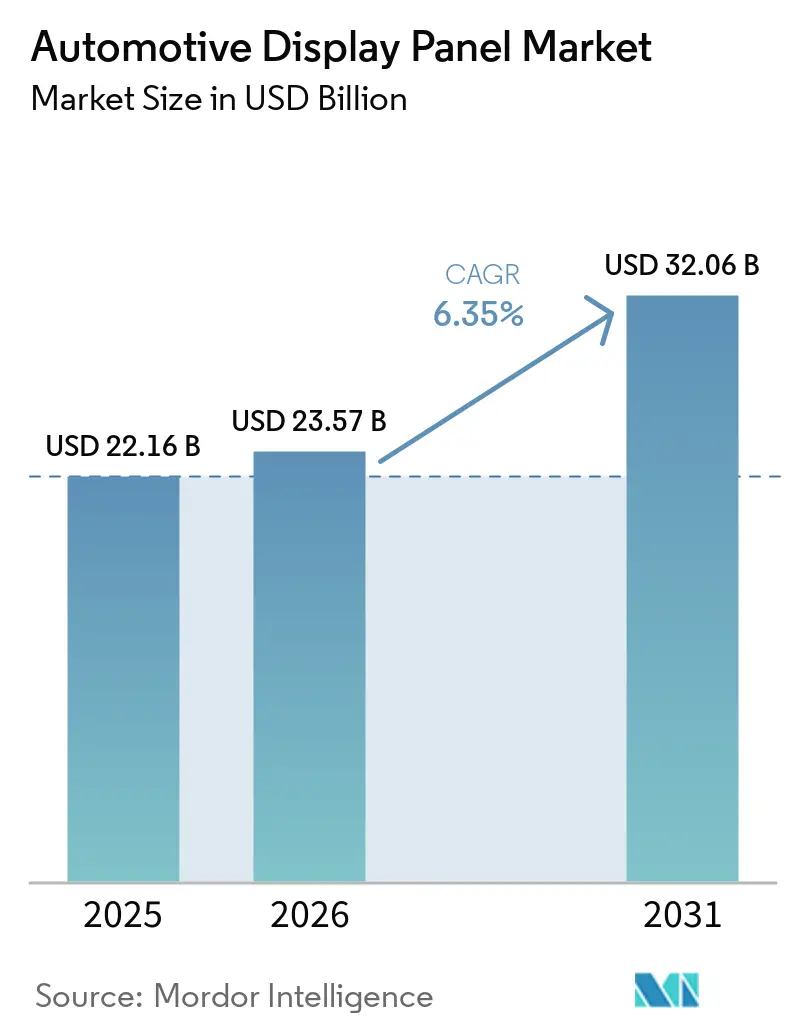

| Market Size (2026) | USD 23.57 Billion |

| Market Size (2031) | USD 32.06 Billion |

| Growth Rate (2026 - 2031) | 6.35% CAGR |

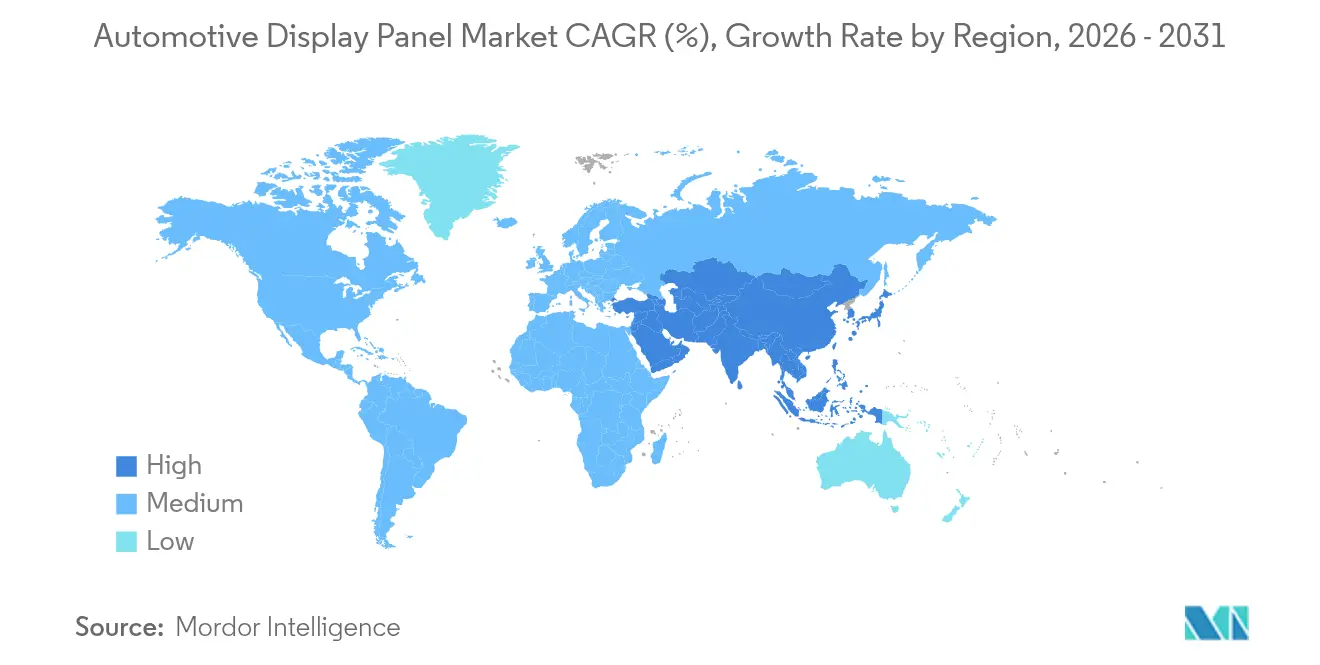

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

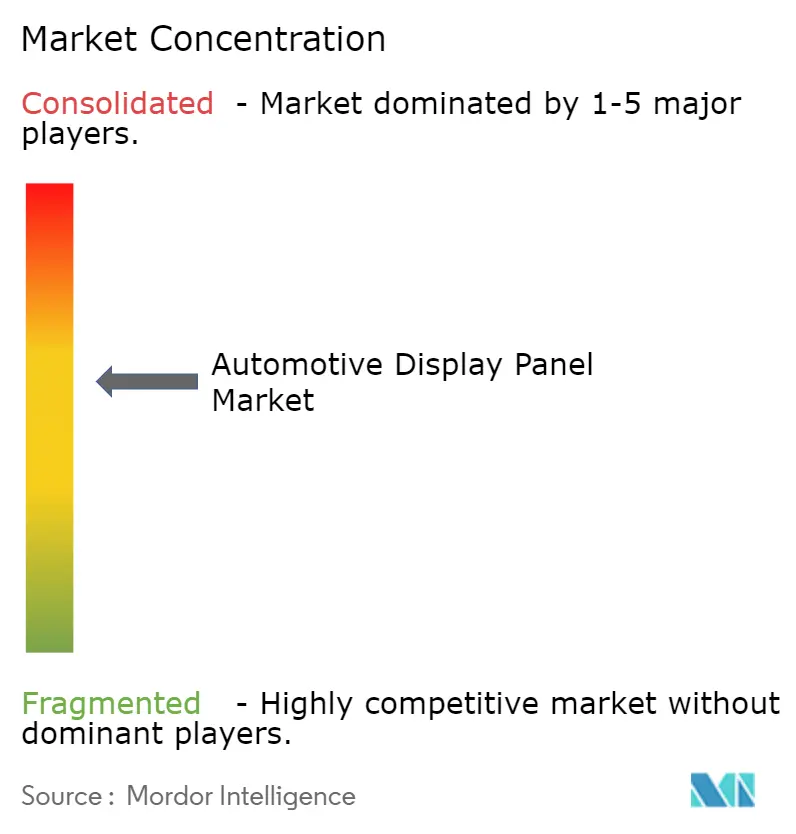

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive Display Panel Market Analysis by Mordor Intelligence

The automotive display panel market size is expected to grow from USD 22.16 billion in 2025 to USD 23.57 billion in 2026 and is forecast to reach USD 32.06 billion by 2031 at 6.35% CAGR over 2026-2031. Rising adoption of software-defined vehicles elevates display panels from accessory to core human–machine interface. Tighter safety regulations that oblige larger, higher-resolution clusters, falling OLED prices, and regional mandates for camera-based mirrors strengthen demand. Automakers also pursue pillar-to-pillar layouts to unlock subscription revenue, while Mini-LED backlighting solves visibility issues in hot climates. Supply-chain localization in North America and India seeks to limit geopolitical risk and shorten lead times, yet limited IGZO capacity and cybersecurity compliance still restrict output. Overall, the automotive display panel market continues to pivot from cost-centric supply to experience-centric differentiation, creating room for both incumbent panel makers and Tier-1 integrators.

Key Report Takeaways

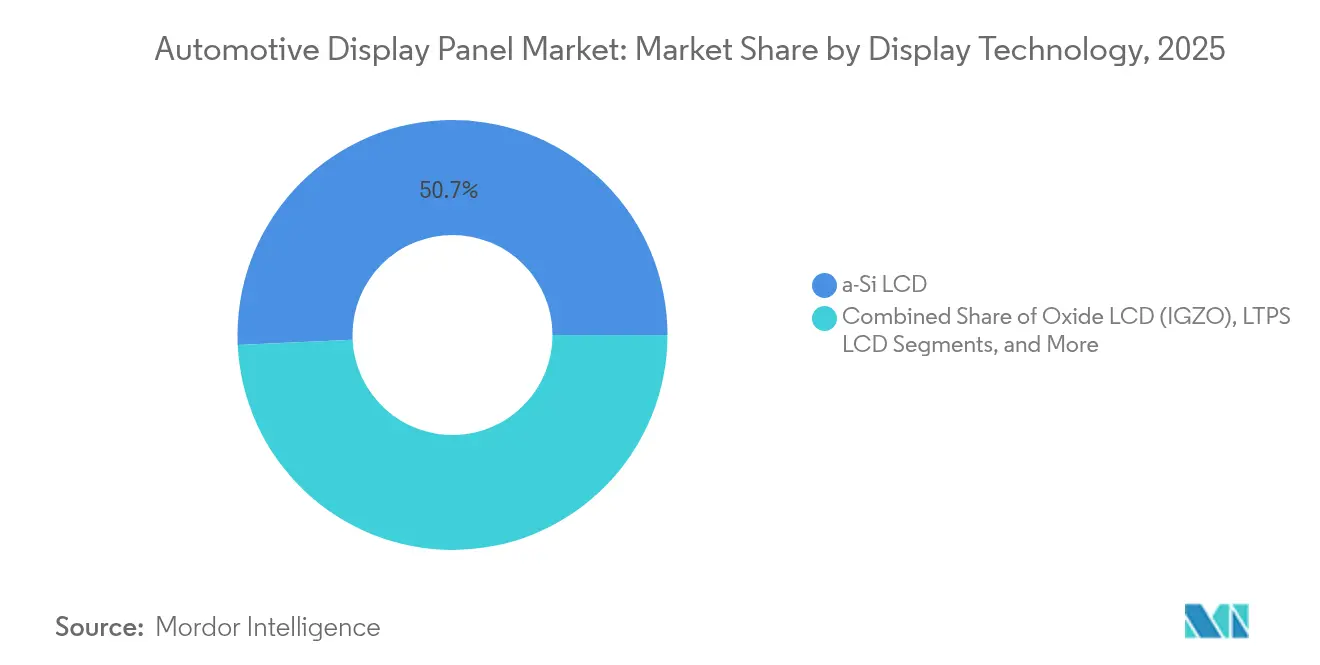

- By display technology, a-Si LCD held 50.74% of the automotive display panel market share in 2025, whereas MicroLED segment is poised for an 10.85% CAGR to 2031.

- By screen size, 5.1-8 inch panels led with 37.12% revenue share in 2025; displays above 12 inches are projected to expand at a 10.12% CAGR through 2031.

- By vehicle type, passenger cars captured 83.58% share of the automotive display panel market size in 2025, while heavy commercial vehicles will accelerate at a 13.55% CAGR by 2031.

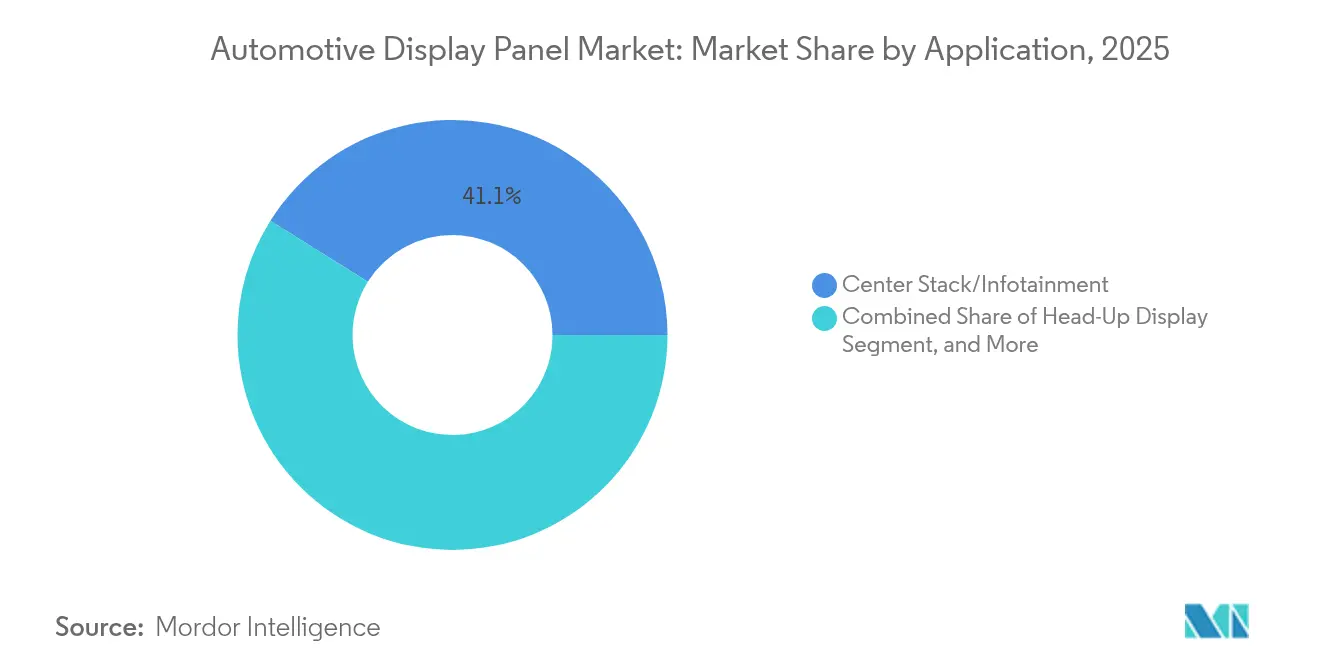

- By application, center stack / infotainment controlled 41.08% revenue in 2025; digital side / smart mirrors will rise the fastest at 9.31% CAGR.

- By integration level, stand-alone displays dominated with 73.12% revenue in 2025, whereas integrated cockpit / pillar-to-pillar solutions are set for an 8.22% CAGR to 2031.

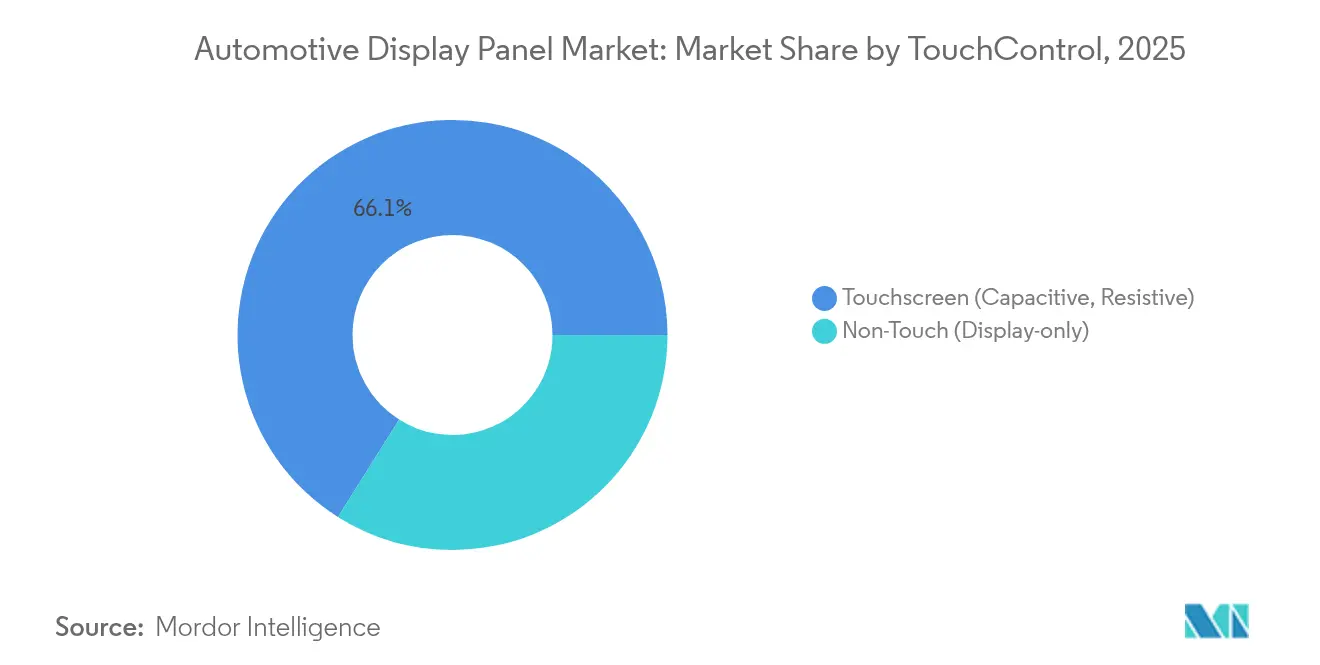

- By touch / control, capacitive touchscreens commanded 66.05% revenue in 2025; haptic-enabled touchscreens will register the quickest 11.74% CAGR.

- By sales channel, OEM-fitted units accounted for 90.25% of 2025 revenue, while aftermarket retrofit displays are forecast to grow at a 6.74% CAGR.

- By geography, Asia-Pacific commanded 48.12% of 2025 revenue; Middle East and Africa is the quickest-growing region at 8.17% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Automotive Display Panel Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Automaker race to deliver pillar-to-pillar cockpits | +1.2% | China, North America premium | Medium term (2-4 years) |

| EU mandate for advanced driver distraction warning | +0.9% | Europe, global spillover | Short term (≤2 years) |

| Declining OLED ASPs broaden mid-range adoption | +0.8% | Global, Asia-Pacific focus | Medium term (2-4 years) |

| Mini-LED backlighting for high-temp EV markets | +0.6% | Middle East, North Africa | Long term (≥4 years) |

| In-vehicle streaming and gaming preferences | +0.7% | North America, China | Medium term (2-4 years) |

| Rollout of digital side mirrors | +0.4% | Japan, South Korea, EU | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Automaker race to deliver pillar-to-pillar cockpit displays in China and US premium segments

Mass-production of LG Display’s 40-inch unit since February 2025 signals a paradigm shift whereby displays act as brand signatures instead of functional upgrades.[1]European Parliament, “Regulation (EU) 2019/2144 on Type-Approval Requirements for Motor Vehicles,” eur-lex.europa.eu Switchable Privacy Mode permits front-seat streaming without distracting the driver, alleviating regulatory risk while enabling subscription revenue. Sony-Honda’s AFEELA sedan will debut the module, and more than 100 Chinese EV launches in 2024 already prioritized similar configurations. This reinforces a display-centric cockpit model that supports over-the-air feature unlocks, making the automotive display panel market a software monetization anchor

Regulatory push for advanced driver assistance requiring larger digital instrument clusters in EU

Regulation (EU) 2019/2144 forces new type approvals from July 2024 to integrate driver-distraction warning functions that rely on gaze tracking.[2]LG Display, “LG Display Begins Mass Production of Ultra-Large Automotive Display Solutions,” bastillepost.com Meeting the technical files persuades OEMs to standardize larger, sensor-rich clusters across model lines rather than limit such panels to premium trims. The rule also propagates globally through UNECE channels, effectively lifting the baseline specification for forthcoming instrument clusters.

Falling OLED panel ASPs triggering OEM adoption in mid-range passenger cars

Samsung Display’s collaboration with Dolby for HDR certification shows how cost erosion and maturing durability invite OLED into mid-segment trims.[3]Samsung Display, “Samsung Display Partners with Dolby to Enhance Automotive HDR,” samsungdisplay.com Chinese capacity expansions by BOE and TCL CSOT deepen price competition. Automakers first position OLEDs in center stacks to balance bill-of-materials before scaling to full cockpits, exploiting improved 1,500-hour lifetimes at 85 °C that temper former burn-in worries.

Mini-LED backlighting enhancing brightness for EVs in high-temperature Middle-East markets

TCL CSOT’s 45,000-nit prototypes showcased in 2025 resolve glare and thermal fade seen in desert environments where dashboards surpass 85 °C. Energy efficiency improvements matter because displays can draw up to 3% of EV pack capacity under harsh sunlight. Local dimming also lowers heat generation by 40%, fitting the Middle-East as a proving ground before global releas

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| OLED burn-in reliability concerns in fleet vehicles | -0.6% | Global fleet hubs | Short term (≤2 years) |

| IGZO backplane capacity scarcity | -0.8% | Asia-Pacific acute | Short term (≤2 years) |

| High BOM cost of curved displays in price-sensitive markets | -0.4% | India, Brazil | Medium term (2-4 years) |

| Cybersecurity compliance costs on retrofits | -0.3% | EU, developed markets | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

OLED burn-in reliability concerns limiting deployment in taxis/fleets

Continuous static images such as fare data create uneven pixel aging. Pixel-shift algorithms raise uniformity to 94.5%, yet operators demand multi-year proof before large rollouts. Replacement cycles of 5-7 years amplify the hesitancy, stalling OLED penetration into high-utilization fleets that otherwise would contribute sizable volumes to the automotive display panel market.

Scarcity of IGZO backplane capacity causing 2025 model-year delays

High pixel density and low leakage make IGZO essential for premium clusters, but production remains confined to a handful of Gen-8 fabs. Qualification cycles exceed 18 months, thus new EV launches are forced to stagger high-resolution trims or pivot to LTPS alternatives until capacity ramps. The bottleneck weighs on forecast output during 2025-2026, curbing near-term automotive display panel market growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Display Technology: MicroLED Drives Premium Differentiation

MicroLED is set to grow at 10.85% CAGR as carmakers target unmatched brightness and efficiency for flagship models. AUO’s transparent roof panels and morphing controls presented in 2025 validate design freedom that standard LCD cannot match. While a-Si LCD still commanded 50.74% revenue, its cost advantage wanes in upper trims where user-experience metrics trump unit price. Oxide LCD (IGZO) powers high-resolution instrument clusters that need minimal standby draw, and Mini-LED backlit LCD bridges the gap with quasi-OLED contrast. OLED breakthroughs in burn-in algorithms lengthen usable life, yet fleet buyers stay wary. These parallel tracks confirm that the automotive display panel market accommodates coexistence rather than outright substitution, enabling tiered feature packaging across vehicle lines.

Large automakers now hedge sourcing risk by approving both MicroLED and OLED for future cockpits; Samsung Display already samples 12-inch MicroLED clusters for 2028 production. Meanwhile, Tier-1 suppliers embed common graphics stacks so dashboards can interchange panel types with minor software changes, supporting software-defined vehicles goals. This flexibility sustains volume for incumbent LCD fabs even as next-gen formats expand, keeping the automotive display panel industry diversified.

By Screen Size: Large Formats Enable New Applications

Displays above 12 inches, though niche in 2024, unlock new cockpit architectures such as pillar-to-pillar dashboards and roof installations. LG Display’s 40-inch module supports multi-zone dimming, allowing simultaneous cluster, infotainment, and passenger cinema in one surface. Mid-sized 5.1-8 inch panels remain primary for mainstream infotainment and secure 37.12% 2025 revenue, but growth momentum shifts upward. Conversely, up-to-5-inch screens gain traction in mirror replacements and HVAC touch bars, keeping unit volumes high. The bifurcation is clear: premium vehicles order expansive canvases; mass models opt for distributed clusters of small panels. As software layers decouple function from location, size selection hinges on aesthetics and bill-of-materials rather than fixed gauge placement, reinforcing flexible design in the automotive display panel market.

Market leaders deploy adaptive UI frameworks that reconfigure layout based on driving mode, from high-contrast ADAS overlays during motion to cinematic widescreen when parked. Such adaptability steers future strategy, where automotive display panel market size for large formats benefits from time-of-use monetization, for instance, streaming subscriptions activated in autonomous mode.

By Vehicle Type: Commercial Vehicles Accelerate Adoption

Passenger cars keep 83.58% of 2025 shipments, yet heavy commercial vehicles grow faster at 13.55% CAGR as safety mandates and telematics converge. Fleet operators justify high-resolution clusters that synthesize tire pressure, route analytics, and driver coaching on a single interface, cutting downtime. Light commercial vans follow, blending passenger-car UX expectations with cargo optimization tools. The automotive display panel market size for commercial classes is projected to cross 15.24% revenue share by 2031, underscoring a shift from optional extras to operational necessities.

Panel suppliers respond with shock-and-vibration-rated assemblies exceeding 70 Gs and anti-glare cover glass that withstands daily cleanings. Over-the-air upgrades permit freight companies to unlock advanced telematics on existing dashboards, converting hardware into recurrent service income. This business model cements displays as revenue generators rather than depreciating assets, amplifying value capture across the automotive display panel industry.

By Application: Digital Mirrors Emerge as Growth Driver

Center stack / infotainment dominated 41.08% of 2025 value, but camera-based mirror systems command the fastest 9.31% CAGR thanks to aerodynamic fuel-savings and widening regulatory acceptance. Japan and South Korea validated homologation paths, and US evaluations signal expanded addressable volume. Head-up displays evolve with AR overlays; Hyundai Mobis’ holographic windshield aims for 2027 mass adoption, projecting navigation cues directly on glass. For rear-seat entertainment, transparent MicroLED roof displays convert cabins into planetariums, echoing younger buyers’ streaming habits. Such variety ensures the automotive display panel market retains multi-vector expansion where a single vehicle can host six or more specialized screens.

Digital mirror adoption further spurs semiconductor demand for low-latency cameras and image processors. Suppliers that master optical calibration and weather-proof housings gain early advantage, as legislated field-of-view and brightness metrics tighten. By 2030, shipments of display-based mirror units may surpass traditional glass for luxury segments, feeding sustained growth in the automotive display panel market.

By Integration Level: Stand-Alone Displays Dominate Current Market

Stand-alone panels remain 73.12% of 2025 shipments because legacy E/E architectures allocate discrete ECUs. Integrated cockpits, however, expand at 8.22% CAGR, bolstered by Snapdragon-based domain controllers that unify graphics rendering. Consolidation reduces wiring weight by 30% and simplifies OTA update cadence, appealing to automakers chasing cost savings and feature agility. Transition hurdles include thermal management, EMC compliance, and supplier hand-offs, yet multi-function panels align closely with software-defined roadmaps. As volume scales, integrated cockpits will seize higher value per vehicle, deepening the automotive display panel market opportunity for Tier-1s offering turnkey platforms.

OEM strategies now pair large, bonded glass with zonal computing, allowing partitioned safety domains. This approach supports gradual migration: vehicles can start with cluster + infotainment fusion and later enable passenger gaming with a software key. Such pathways cushion capital outlay while preserving future revenue options.

By Touch/Control: Haptic Technology Enhances Interface

Capacitive touch retained 66.05% share in 2025 for its familiar smartphone-like interaction. Yet regulators urge tactile feedback to cut glance time; thus, haptic-enabled touch surges at 11.74% CAGR. Surface-actuated vibrations confirm inputs so drivers keep eyes forward, aligning with driver distraction guidelines. Non-touch displays for clusters and HUDs grow steadily as vehicles embrace voice and gesture controls that circumvent physical contact. Resistive panels persist only in glove-friendly or rugged vocational trucks.

Haptic suppliers embed localized piezo actuators beneath thin glass, granting button-like feedback without mechanical parts. Early adopters report 15% shorter driver glance durations, assisting safety ratings. This performance edge makes haptics a default spec in next-gen center stacks, reinforcing premium positioning within the automotive display panel market.

By Sales Channel: OEM Integration Dominates Market

Factory-fitted screens captured 90.25% of 2025 volume because compliance, warranty, and cybersecurity responsibilities rest with automakers. Retrofit demand increases 6.74% CAGR as owners modernize vehicles lacking native displays, but UN R155 cybersecurity requirements raise entry barriers. Established Tier-1s, able to fund penetration testing and documentation, extend sensor portfolios to aftermarket lines, while smaller brands retreat to niche segments. Long homologation cycles for critical systems like clusters further tilt share to OEM fitment, safeguarding reliability standards.

Still, the retrofit niche stays relevant for fleets prolonging asset life or for enthusiasts seeking CarPlay upgrades. Supply-chain players that harness modular interfaces and open-source Linux stacks could ease certification costs, unlocking latent expansion. However, OEM dominance will continue to characterize the automotive display panel market through the decade.

Geography Analysis

Asia-Pacific led with 48.12% revenue in 2025 owing to China’s prolific EV pipelines and Japan’s early legalization of camera mirrors. Regional automakers tout 32-inch passenger screens and AR HUDs as baseline features, forcing global competitors to match specs. Indigenous panel makers like BOE ship 9K oxide TFT prototypes, proving domestic ecosystem depth. Meanwhile, joint ventures in India localize LCD module assembly, fulfilling cost-sensitive markets and insulating supply from external shocks.

North America benefits from luxury SUV appetite and regulatory momentum toward mirrorless approvals. Pillar-to-pillar dashboards differentiate premium trims, while truck cabins embrace wide displays for towing visualization. Massive semiconductor investments, such as USD 60 billion in new US wafer fabs, strengthen upstream resilience, smoothing panel controller availability. These factors cement North America as the second-largest region by 2025 for the automotive display panel market.

Europe centers on safety-oriented adoption driven by Regulation 2019/2144. Automakers integrate gaze-tracking clusters and cross-domain displays that meet Euro NCAP roadmap targets. Panoramic Vision concepts slated for 2025 production reveal how German OEMs merge ADAS feeds with expansive glass surfaces. Supplier clusters in Germany and Czechia specialize in optical bonding and auto-grade coatings, anchoring European content despite cost pressures.

Middle East and Africa posts the highest 8.17% CAGR. Extreme heat calls for 45,000-nit Mini-LED panels that maintain chroma at 85 °C. Luxury imports equip rear entertainment suites as ride-hailing fleets upgrade passenger amenities. Government electrification targets in Gulf Cooperation Council nations further accelerate demand for efficient, high-brightness displays. South America lags in premium penetration but seeds growth through local glass finishing plants in Brazil and Vietnam-to-Mercosur supply chains, positioning the region for gradual uptake in the automotive display panel industry.

Competitive Landscape

Market structure remains moderately concentrated: the top six suppliers control roughly 45% revenue, blending panel fabrication giants with Tier-1 integrators. LG Display grew automotive share to 9% of group sales in Q1 2025 by launching ultra-wide OLED clusters, while Samsung Display ramps MicroLED sampling to hedge against OLED aging risk. BOE leverages Chinese OEM proximity and cost leadership to win domestic EV dashboards.

On the system side, Continental secured production awards for frameless curved OLEDs using film-insert molding, whereas Visteon booked USD 1.9 billion new orders by bundling cockpit domain controllers with its Phoenix graphics engine. Denso partners with Qualcomm to co-develop zonal compute modules that shorten software cycles. Cooperation between panel makers and Tier-1s intensifies because integrated cockpits demand synchronized hardware-software roadmaps.

Emerging entrants such as Mojo Vision and VueReal target micro-display niches for HUDs, often licensing IP to incumbents rather than competing head-on. Cybersecurity and functional-safety certifications present high barriers, favoring players with legacy automotive track records. Nevertheless, patent cross-licensing and regional production pivots create openings for alliances that can collectively address the diverse requirements of the automotive display panel market.

Automotive Display Panel Industry Leaders

LG Display

Samsung Display

BOE

Innolux Corporation

AUO

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: CarUX, Innolux subsidiary, acquires Pioneer for NT$37.7 billion to deepen smart-cockpit portfolio.

- May 2025: AUO debuts transparent MicroLED roof and foldable center-stack prototypes with AI integration.

- April 2025: Infineon and Marelli unveil MEMS laser beam scanning system for display-free cockpit projections.

- April 2025: EDT and Nippon Seiki establish EDT-India Pvt Ltd to localize TFT-LCD modules.

- March 2025: Hyundai Motor Group pledges USD 21 billion US investment, including USD 6 billion for components relevant to display systems.

- March 2025: Hyundai Motor Group pledges USD 21 billion US investment, including USD 6 billion for components relevant to display systems.

- February 2025: LG Display starts mass production of 40-inch pillar-to-pillar panel with privacy filtering.

Global Automotive Display Panel Market Report Scope

Automotive display panels are electronic screens used in vehicles to provide visual information to drivers and passengers. These panels can be found in various vehicle locations, such as the instrument cluster, center console, dashboard, rear mirror, and steering wheel. They are designed to display a wide range of information, including vehicle speed, fuel level, engine temperature, navigation directions, and entertainment system controls.

The automotive display panel market is segmented by display panel (technology [a-Si LCD, Oxide LCD, LTPS LCD, and AMOLED]), display console/cluster (application [instrument cluster, center stack, heads-up display, and other applications]), and geography (North America, Europe, Asia-Pacific, Middle East and Africa, and Latin America). The market sizes and forecasts are provided in terms of value in USD for all the above segments.

| a-Si LCD |

| Oxide LCD (IGZO) |

| LTPS LCD |

| OLED (AMOLED, PMOLED) |

| MicroLED |

| Others (E-paper, Mini-LED Backlit) |

| Upto 5 inch |

| 5.1-8 inch |

| 8.1-12 inch |

| Above 12 inch |

| Passenger Cars |

| Light Commercial Vehicles |

| Heavy Commercial Vehicles |

| Instrument Cluster |

| Center Stack/Infotainment |

| Head-Up Display |

| Rear Seat Entertainment |

| Digital Side/Smart Mirror |

| Others (Roof, HVAC) |

| Stand-alone Displays |

| Integrated Cockpit/Pillar-to-Pillar |

| Touchscreen (capacitive, Resistive) |

| Non-Touch (Display-only) |

| OEM-fitted |

| Aftermarket Retrofit |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Nordics | ||

| Rest of Europe | ||

| South America | Brazil | |

| Rest of South America | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South-East Asia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Gulf Cooperation Council Countries |

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Display Technology | a-Si LCD | ||

| Oxide LCD (IGZO) | |||

| LTPS LCD | |||

| OLED (AMOLED, PMOLED) | |||

| MicroLED | |||

| Others (E-paper, Mini-LED Backlit) | |||

| By Screen Size | Upto 5 inch | ||

| 5.1-8 inch | |||

| 8.1-12 inch | |||

| Above 12 inch | |||

| By Vehicle Type | Passenger Cars | ||

| Light Commercial Vehicles | |||

| Heavy Commercial Vehicles | |||

| By Application | Instrument Cluster | ||

| Center Stack/Infotainment | |||

| Head-Up Display | |||

| Rear Seat Entertainment | |||

| Digital Side/Smart Mirror | |||

| Others (Roof, HVAC) | |||

| By Integration Level | Stand-alone Displays | ||

| Integrated Cockpit/Pillar-to-Pillar | |||

| By Touch/Control | Touchscreen (capacitive, Resistive) | ||

| Non-Touch (Display-only) | |||

| By Sales Channel | OEM-fitted | ||

| Aftermarket Retrofit | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Nordics | |||

| Rest of Europe | |||

| South America | Brazil | ||

| Rest of South America | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South-East Asia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Gulf Cooperation Council Countries | |

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the automotive display panel market?

The automotive display panel market stands at USD 23.57 billion in 2026 and is projected to reach USD 32.06 billion by 2031.

Which region leads the automotive display panel market?

Asia-Pacific accounts for 48.12% of 2025 revenue, propelled by China’s aggressive EV rollout and Japan’s regulatory head start on digital mirrors.

Which display technology is growing the fastest?

MicroLED panels register the highest 10.85% CAGR through 2031 as OEMs pursue superior brightness and energy savings.

Why are digital side mirrors important for market growth?

Camera-based mirrors improve aerodynamics by 1.5-2 mpg and meet new safety regulations, driving a 9.31% CAGR in this application segment.

How will cybersecurity rules affect aftermarket display upgrades?

UN R155 requires retrofit suppliers to certify robust cyber-defense processes, raising development costs and slowing aftermarket penetration.

What factors limit OLED usage in fleet vehicles?

Burn-in risks from static images and long fleet replacement cycles make operators cautious despite recent advances in compensation algorithms.

Page last updated on: