Market Overview

| Study Period | 2020 - 2031 |

|---|---|

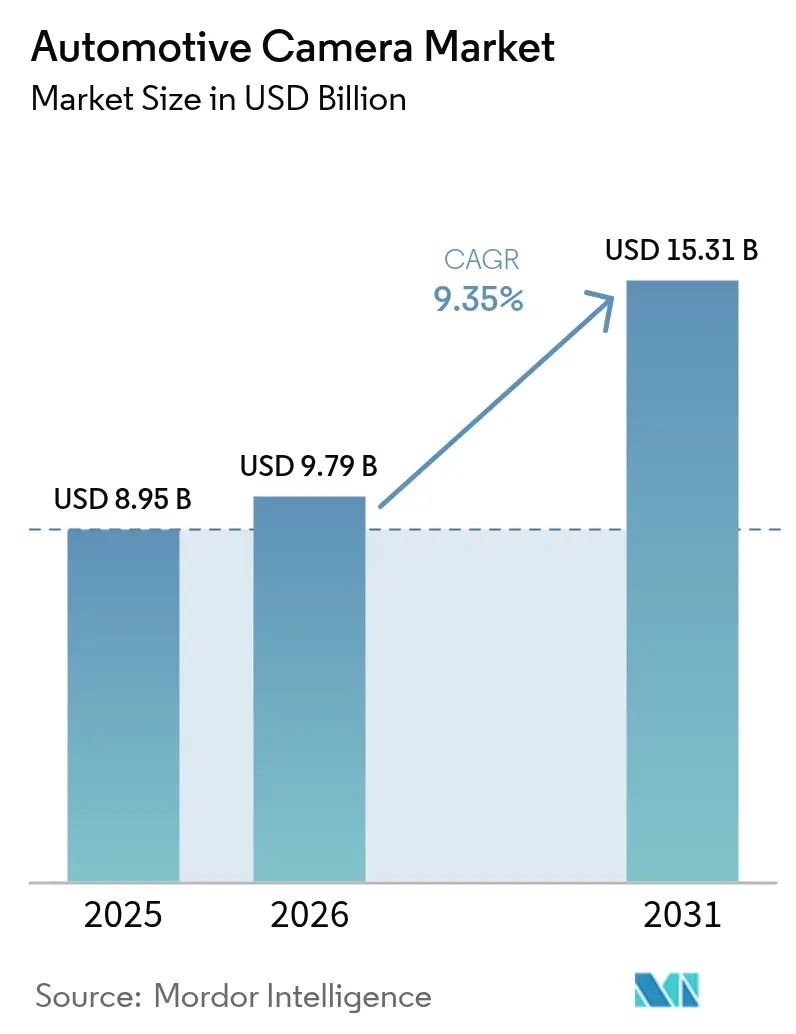

| Market Size (2026) | USD 9.79 Billion |

| Market Size (2031) | USD 15.31 Billion |

| Growth Rate (2026 - 2031) | 9.35% CAGR |

| Fastest Growing Market | North America |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Automotive Camera Market Analysis by Mordor Intelligence

The automotive camera market size was valued at USD 8.95 billion in 2025 and estimated to grow from USD 9.79 billion in 2026 to reach USD 15.31 billion by 2031, at a CAGR of 9.35% during the forecast period (2026-2031). A synchronized wave of regulatory mandates, rising vehicle automation, and falling CMOS sensor costs is lifting both unit volumes and ASPs, pushing the automotive camera market size toward double-digit growth. Tightened safety rules in the European Union, the United States, and China now require camera-enabled functions such as automated emergency braking, intelligent speed assistance, and driver monitoring, making cameras a non-negotiable core of modern vehicle design. Automakers also view multi-camera arrays as the lowest-cost path to Level 2+ autonomy, which is accelerating platform-wide adoption across mid-priced models. At the same time, thermal and near-infrared technologies are broadening the performance envelope into night and bad-weather scenarios, opening premium upgrade opportunities. Finally, wafer cost deflation throughout 2024 and expected through 2025 is shrinking the bill-of-materials, letting OEMs fit more cameras per vehicle without inflating sticker prices.[1]"Federal Motor Vehicle Safety Standards; Automatic Emergency Braking Systems for Light Vehicles", National Highway Traffic Safety Administration (NHTSA), www.nhtsa.gov.

Key Report Takeaways

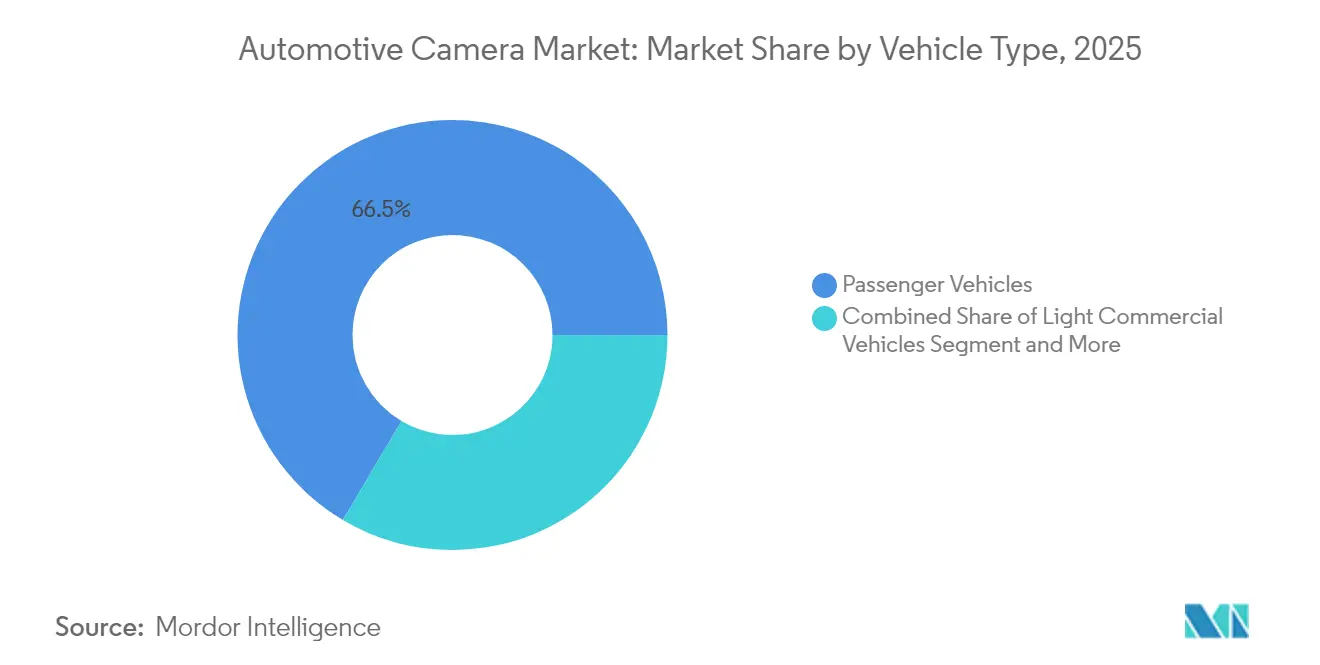

- By vehicle type, passenger vehicles led with 66.48% revenue share in 2025, while light commercial vehicles are projected to expand at an 11.02% CAGR through 2031.

- By camera technology, digital CMOS held 45.05% of the automotive camera market share in 2025; thermal LWIR is forecast to grow at a 14.12% CAGR to 2031.

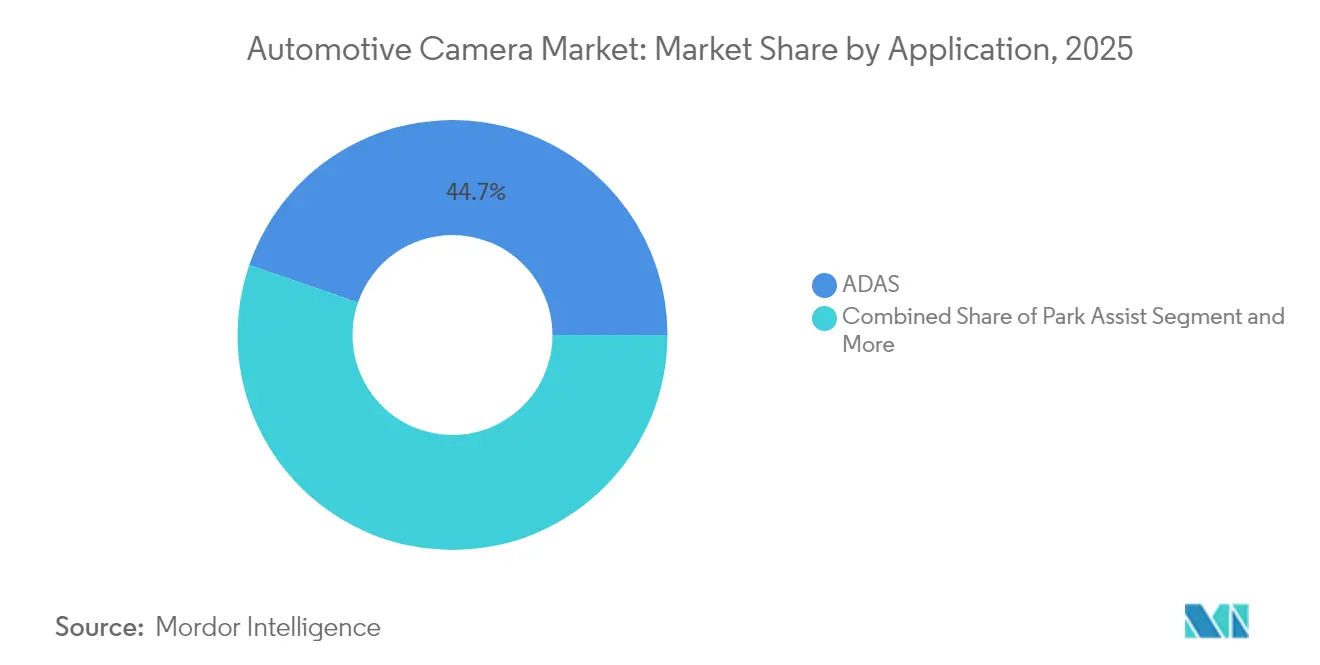

- By application, ADAS accounted for a 44.72% share of the automotive camera market size in 2025, whereas driver monitoring systems are advancing at a 15.62% CAGR.

- By sales channel, OEM installations captured 86.90% of 2025 revenue, but the aftermarket is expanding fastest at 14.95% CAGR.

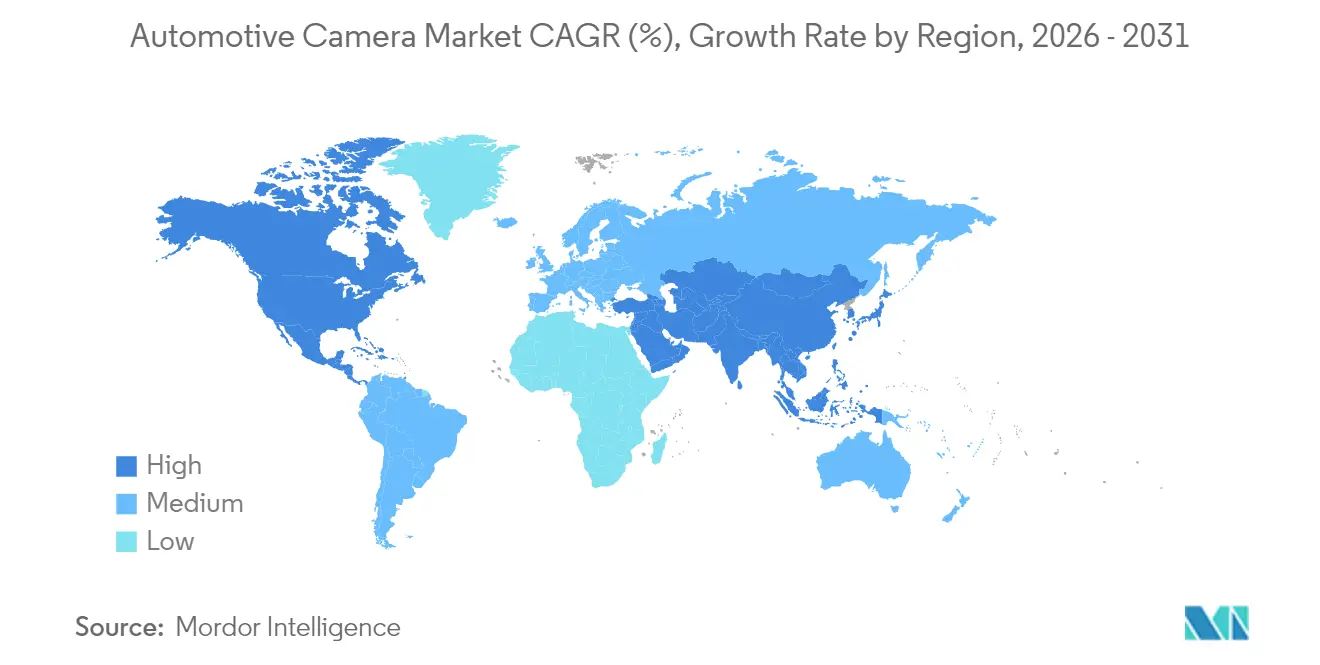

- By geography, Asia-Pacific led with 40.10% of global revenue in 2025; the North America region is growing at a 12.31% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Automotive Camera Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Point Impact on Market CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Safety-camera mandates in US, EU & China | +2.8% | Global, with early implementation in Europe and United States | Short term (≤ 2 years) |

| ADAS & autonomy penetration | +2.1% | Global, led by North America and Europe | Medium term (2-4 years) |

| Parking/360-view consumer pull | +1.4% | Asia-Pacific core, spill-over to North America | Medium term (2-4 years) |

| CMOS-AI cost deflation | +1.2% | Global | Long term (≥ 4 years) |

| Driver-monitoring regulation momentum | +1.1% | EU and China, pending United States adoption | Short term (≤ 2 years) |

| EV drag-reduction via e-mirrors | +0.9% | Europe and China, expanding to North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Safety-camera mandates in US, EU & China

A convergence of safety regulations is forcing OEMs to integrate multi-camera suites in every new vehicle platform. The European Union’s General Safety Regulation II, effective July 2024, compels forward-facing cameras for lane keeping, intelligent speed assistance, and emergency braking. China’s 2024 NCAP now scores driver-monitoring accuracy, effectively requiring infrared cabin cameras. In the United States, the NHTSA rule finalized in 2024 obliges automatic emergency braking with pedestrian detection up to 90 mph, creating a clear pull for thermal sensors that can see in darkness. Automakers, therefore, seek camera architectures that meet all three regimes simultaneously, accelerating global design cycles. Suppliers equipped with scalable reference designs are winning new RFQs from volume platforms. Regulatory alignment is thus turning safety cameras into a baseline commodity rather than a differentiator, lifting overall shipment volumes across the automotive camera market.[2]TÜV SÜD, “EU General Safety Regulation II: What Vehicle Manufacturers Need to Know,” tuvsud.com.

ADAS & autonomy penetration

Level 2+ driving functions are shifting from premium nameplates to mass-market C-segment vehicles. Mobileye’s SuperVision platform now powers Volkswagen’s MQB models, using up to 11 cameras for surround sensing and high-definition road referencing. Sony forecasts each vehicle will embed 12 cameras by fiscal 2027, up from 8 today. AI-on-sensor capabilities let real-time vision algorithms run on edge silicon, trimming system latency and wiring complexity. In turn, higher automation creates a payback for more cameras, closing the cost-benefit loop. The net effect is an upward shift in camera ASPs alongside ballooning unit counts, underpinning an incremental 2.1-percentage-point lift in the automotive camera market CAGR through 2030.

Parking/360-view consumer pull

Urban density is nudging buyers to choose packages that simplify tight-space maneuvering. Surround-view systems that fuse four or more cameras have moved from luxury SUVs into mid-range sedans, with Samsung Electro-Mechanics chasing a 24% share of this sub-segment by 2025. Weather-proof housings sustain clarity in rain and snow, while embedded AI dynamically classifies obstacles that ultrasonic sensors miss. Consumers perceive tangible convenience, which supports subscription-based upgrades and helps OEMs upsell mid-trim variants. Demand is particularly intense in Asia-Pacific megacities such as Shanghai and Seoul, turbocharging volume growth in the region’s automotive camera market.

Driver-monitoring regulation momentum

From July 2024, every new EU passenger car must warn of driver fatigue, anchoring two infrared cameras in the cockpit. China will impose parallel rules in 2026. Anticipating U.S. adoption, Tier 1 suppliers are releasing single-box solutions that monitor eye closure, head pose, and vital signs. OEMs are bundling these features with occupant-sensing airbags, forging a unified safety narrative that boosts take-rates even in markets where regulation lags.

Restraints Impact Analysis*

| Restraint | (~) % Point Impact on Market CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| CMS rule-making uncertainty | -0.7% | North America and Europe | Medium term (2-4 years) |

| IR-glass supply crunch | -0.9% | Global, affecting thermal camera adoption | Short term (≤ 2 years) |

| Cyber-security & privacy risks | -1.2% | Global, with stricter enforcement in EU | Long term (≥ 4 years) |

| Multi-camera BOM cost | -1.8% | Global, particularly price-sensitive segments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Multi-camera BOM cost

Comprehensive ADAS stacks now need 8-12 cameras, yet unit prices range from USD 20 to USD 500, depending on resolution. For value-oriented nameplates, cameras can consume up to 3% of vehicle material cost, squeezing margins. Ford’s 2025 recall of 1.075 million vehicles over rear camera software faults underscores the warranty exposure linked with added complexity. Tier 1 suppliers are responding with consolidated vision ECUs and single-cable architectures, but near-term cost headwinds still trim 1.8 percentage points from the automotive camera market CAGR.

Cyber-security & privacy risks

Camera data flows travel across in-vehicle, edge, and cloud domains, creating attack surfaces. In early 2025, a series of ransomware incidents hit global automakers, exposing component drawings and customer data. The U.S. ban on connected-vehicle tech from China and Russia has forced supply-chain reshuffles that add compliance costs. ISO/SAE 21434 mandates security by design, embedding extra silicon and software validation steps. EU GDPR rules also cap the collection of biometric data from cabin cameras, potentially curbing advanced analytics. These factors collectively shave 1.2 percentage points off the market growth rate.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: Commercial Fleets Drive Camera Adoption

The automotive camera market size for passenger vehicles stood at USD 5.95 billion in 2025, equal to 66.48% of global revenue. Light commercial vehicles, while smaller today, are expanding at an 11.02% CAGR through 2031, outpacing overall growth. Fleet owners embrace cameras to trim insurance costs, curb collisions, and support telematics-based driver scoring. Volvo Trucks reports fuel savings of 2% when camera monitor systems replace traditional mirrors. The automotive camera market, therefore, sees rising procurement from logistics firms that can quantify ROI.

Passenger cars keep leadership because of scale production and consumer willingness to pay for safety packs. ADAS penetration exceeded 90% in new light-duty vehicles in 2025, ensuring a stable installed base. In heavy trucks, camera adoption aligns with regulatory milestones such as the EU’s GSR II blind-spot detection rule. Stoneridge’s MirrorEye system on Freightliner Cascadia heavy trucks has demonstrated 8-camera redundancy that may later cascade to consumer SUVs. The blend of cost-down modules and proven fleet savings sustains a double-digit rise in the automotive camera market across commercial segments.

By Camera Type: Sensing Systems Gain Intelligence Edge

Viewing cameras retained a 56.80% revenue share in 2025, anchoring the automotive camera market share around reversing, surround, and mirror replacement functions. Yet, sensing and stereo units are scaling at 12.95% CAGR as OEMs prioritize perception over display. Subaru’s next-gen EyeSight leverages onsemi Hyperlux AR0823AT sensors to offer lane-centering precision previously limited to lidar setups. Depth-perception stereo rigs are now validated to Automated Driving Systems (ADS) Level 3 in Japan, driving broader uptake. As sensing cameras migrate into affordable trims, the automotive camera market size within perception sub-segments will narrow the gap against legacy viewing categories.

Traditional viewing systems evolve too, with higher HDR and de-spray coatings that maintain clarity in road grime. Automakers are integrating bird-eye computational mosaics that require frame-accurate synchronization across four cameras, pushing suppliers to deliver low-skew imagers. Foresight’s stereo algorithm bundles deliver object detection at sub-0.05 lux, positioning sensing cameras as a cost-effective alternative to lidar. Overall, image-based perception advantages and falling BOMs are pivoting growth toward the intelligence end of the automotive camera market.

By Technology: Thermal Cameras Emerge from Niche Applications

Digital CMOS technology commanded 45.05% of the automotive camera market share in 2025, but long-wave infrared (LWIR) cameras grew 14.12% CAGR, the steepest among all modalities. Thermal sensors sidestep the visibility limitations of rain, fog, and darkness. Magna has shipped more than 1.2 million thermal units, especially to premium brands seeking 5-Star Euro NCAP ratings. Infrared NIR, at 44.35% share, anchors driver monitoring systems where invisible illumination avoids distraction. Metalens breakthroughs promise thinner optics that could collapse separate thermal and visible channels into a single stack.

Supply chain volatility tempers expansion. A 38% jump in germanium prices since August 2023 lifted lens costs. Manufacturers hedge by validating chalcogenide glass and expanding recycling loops. Concurrently, CMOS vendors integrate RGB-IR pixels, cutting lens counts and wiring. The technology mix will thus stay fluid, but thermal imaging’s proven night-time safety gains secure its trajectory within the automotive camera market.

By Application: Driver Monitoring Gains Regulatory Momentum

ADAS ruled 44.72% of deployments in 2025, but driver monitoring systems (DMS) are sprinting ahead with 15.62% CAGR, closing the gap quickly. EU mandates require drowsiness alerts, transforming DMS into a legal minimum. Hyundai Mobis’s In-Cabin Monitoring reads heart rate and breathing, broadening safety into wellness assessment. Park-assist retains a 38% slice of revenue by adding AI-based slot detection and smartphone valet modes. OMNIVISION and Philips are co-developing sensors that check occupant vitals, pointing to health-oriented upsell paths. The application mix shows an automotive camera market swinging from purely external sensing toward holistic in-cabin awareness.

By Sales Channel: Aftermarket Accelerates Despite OEM Dominance

OEM factory installs represented 86.90% of 2025 shipments, anchored by scale and integrated electronics. Valeo alone delivered over 20 million front cameras with Mobileye EyeQ processors. Yet the aftermarket grows at 14.95% CAGR as owners retrofit older vehicles. The dash-cam segment could exceed USD 12 billion by 2033, propelled by insurance discounts. Vueroid’s S1 Infinite 4K dash-cam uses edge AI to warn of lane drifts and potential forward collisions. Drops in sensor cost and easy OBD-II power taps make self-installation mainstream, carving a sustainable niche inside the automotive camera market.

Geography Analysis

Asia-Pacific dominated the automotive camera market with a 40.10% share in 2025, buoyed by China’s production scale and Japan’s semiconductor leadership. Sony targets a significant global share in automotive imagers by fiscal 2026, reinforcing regional supply-chain competitiveness. Beijing’s smart-vehicle roadmap subsidizes Level 2+ systems, making multi-camera packages standard even in economy EVs. South Korea’s OEMs embed advanced surround-view on every new SUV, underpinned by local sensor and lens fabrication. Such a policy and industrial depth secure APAC’s anchor position in the automotive camera market.

North America held a 26.05% share in 2025 as consumer demand for high-end safety features dovetailed with NHTSA mandates. The U.S. rule obliging automatic emergency braking by 2029 incentivizes early camera adoption to spread validation costs over longer cycles. Canadian provinces offer fleet insurance rebates for dash-cams, expanding the retrofit pool. Silicon Valley chip firms provide edge-AI reference designs that reduce time-to-market for domestic OEMs. These factors keep the region’s automotive camera market on a firm expansion track.

Europe captured 23.15% share, driven by being first to legislate comprehensive camera-based safety under GSR II. German luxury brands equip vehicles with up to 10 cameras to secure 5-Star Euro NCAP scores. The bloc’s e-mirror approval delivers a fresh windfall as EV makers adopt drag-cutting virtual mirrors. However, GDPR imposes strict data processing rules that limit broader analytics, slightly moderating growth relative to APAC.

The Middle East and Africa region accounted for 6.70% of 2025 revenue, thanks to safety-equipment mandates in Gulf Cooperation Council states and expanding urbanization. Saudi Arabia’s emerging automotive split-view camera ecosystem underpins domestic assembly ambitions. South America remained at 4.00% share, yet Brazil’s 2026 plan to align with UN ECE rearview camera standards sets a multi-year upgrade cycle. Overall, differential regulation timing drives geographic dispersion within the automotive camera market.

Competitive Landscape

The automotive camera market features a moderately fragmented structure where no single vendor tops a significant revenue share. Tier 1 majors such as Bosch, Continental, and Valeo leverage deep OEM integrations, while semiconductor specialists like onsemi and OMNIVISION climb the value ladder through differentiated sensor offerings. Mobileye’s camera-centric perception stacks blur lines between hardware and software, prompting incumbents to form alliances: Volkswagen partnered with Valeo and Mobileye in 2025 to enhance Level 2+ automation.

Strategic moves show increasing vertical integration. Infineon’s USD 2.5 billion purchase of Marvell’s automotive Ethernet business prepares the firm to ship complete “sensor-to-cloud” data pipelines. Gentex’s planned acquisition of VOXX extends its mirror and camera modules into consumer electronics for aftermarket leverage. Cost pressures drove suppliers to standardize reference designs that scale from entry to luxury trim, reusing optics and PCB layouts.

Emerging disruptors exploit AI differentiation. Helm.ai demonstrated a generative-AI-based simulation that slashes validation time, appealing to OEMs pursuing software-defined vehicles. Universities and startups investigate neuromorphic vision sensors, promising order-of-magnitude lower power draw, key for all-electric architectures. As traditional hardware commoditizes, value creation shifts to perception software and data services, redefining rivalry lines in the automotive camera market.

Automotive Camera Industry Leaders

-

Garmin Ltd

-

Continental AG

-

Panasonic Corporation

-

Magna International Inc.

-

Bosch Mobility Solutions

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Visteon Corporation began manufacturing high-resolution camera systems and display backlight units at its Chennai facility in India. The company invested USD 10 million in this expansion, which marked its entry into in-house production of automotive components as part of its vertical integration strategy.

- January 2025: UVeye raised USD 191 million to scale AI-based vehicle inspection cameras.

- January 2025: HARMAN disclosed collaborations with HL Klemove on central compute units combining cockpit and ADAS features.

- December 2025: Gentex signed a deal to acquire VOXX International, expanding OEM and aftermarket reach.

Global Automotive Camera Market Report Scope

An automotive camera is installed on the front side, rear side, or inside a vehicle for safety purposes. Camera modules contain image sensors that are coupled with electronic components in vehicles. The automotive camera market report covers the latest trends, COVID-19 impact, and technological developments in the market.

The scope of the report covers segmentation based on vehicle type, type, technology, applications, and geography. By vehicle type, the market is segmented into passenger vehicles and commercial vehicles. By type, the market is segmented into viewing cameras and sensing cameras. By technology, the market is segmented into digital cameras, infrared, and thermal.

By application, the market is segmented into ADAS, parking assist, and other applications. By geography, the market is segmented into North America, Europe, Asia-Pacific, and the Rest of the world. For each segment, the market sizing and forecast are based on value (USD billion).

By Vehicle Type

| Passenger Vehicles |

| Light Commercial Vehicles |

| Medium and Heavy Commercial Vehicles |

By Camera Type

| Viewing (Surround/Rear/Front/Interior) |

| Sensing / Stereo Cameras |

By Technology

| Digital (CMOS) |

| Infra-red (NIR) |

| Thermal (LWIR) |

By Application

| Park Assist |

| Advanced Driver Assistance Systems (ADAS) |

| Driver Monitoring & Cabin Safety |

By Sales Channel

| OEM-Installed |

| Aftermarket |

By Geography

| North America | United States |

| Canada | |

| Rest of North America | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Vehicle Type | Passenger Vehicles | |

| Light Commercial Vehicles | ||

| Medium and Heavy Commercial Vehicles | ||

| By Camera Type | Viewing (Surround/Rear/Front/Interior) | |

| Sensing / Stereo Cameras | ||

| By Technology | Digital (CMOS) | |

| Infra-red (NIR) | ||

| Thermal (LWIR) | ||

| By Application | Park Assist | |

| Advanced Driver Assistance Systems (ADAS) | ||

| Driver Monitoring & Cabin Safety | ||

| By Sales Channel | OEM-Installed | |

| Aftermarket | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the automotive camera market?

The automotive camera market size stands at USD 9.79 billion in 2026 and is projected to hit USD 15.31 billion by 2031.

Which segment is growing fastest?

Driver monitoring and in-cabin safety systems are the fastest-growing application, expanding at a 15.62% CAGR during 2026-2031.

How many cameras will an average vehicle carry by 2031?

Industry forecasts from Sony suggest the average will rise to about 12 cameras per vehicle by fiscal 2027-2028, up from 8 in 2025.

What regulations are most influential?

The EU General Safety Regulation II, U.S. AEB mandate, and China’s 2024 NCAP revisions together drive the bulk of new camera fitment requirements.

Why are thermal cameras gaining traction?

Thermal LWIR units can detect pedestrians in darkness and adverse weather, helping OEMs meet stringent AEB performance targets at night.

Is the aftermarket a meaningful opportunity?

Yes. Although it holds just 13.10% of sales today, the aftermarket channel is growing at 14.95% CAGR as older vehicles are retrofitted with dash-cams and 360-view kits.

Page last updated on: