Automotive Airbags Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 31.14 Billion |

| Market Size (2031) | USD 53.13 Billion |

| Growth Rate (2026 - 2031) | 11.30% CAGR |

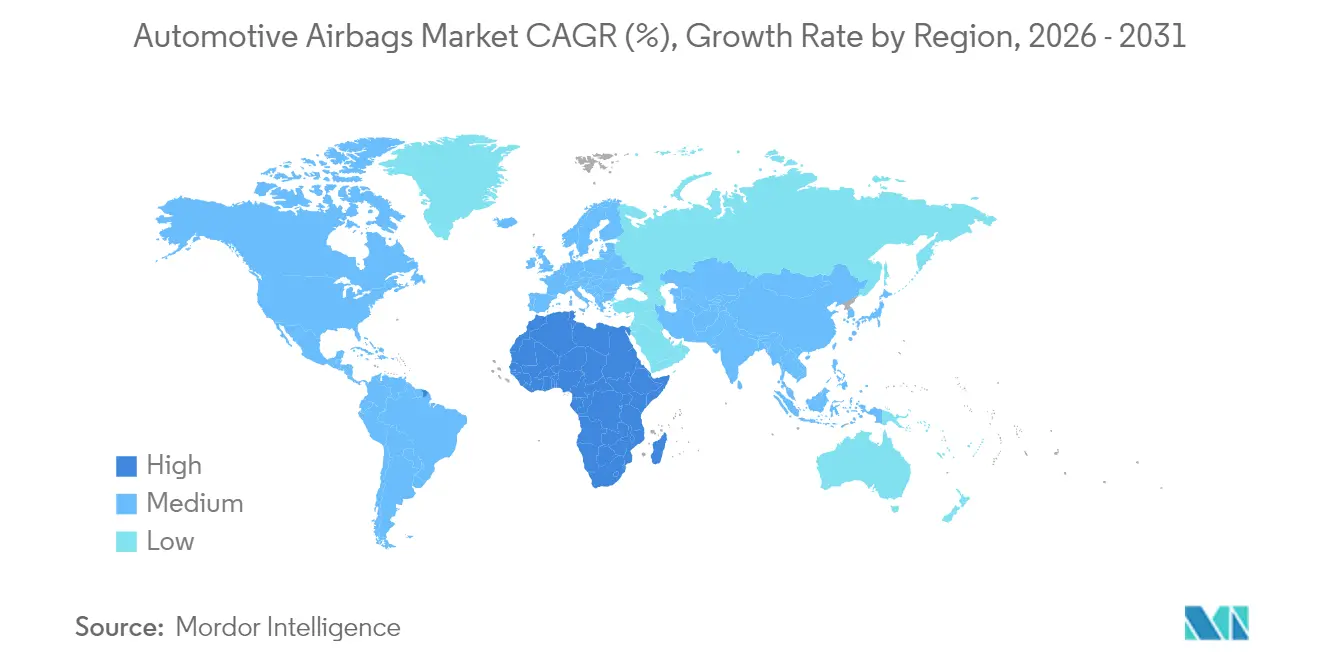

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Automotive Airbags Market Analysis by Mordor Intelligence

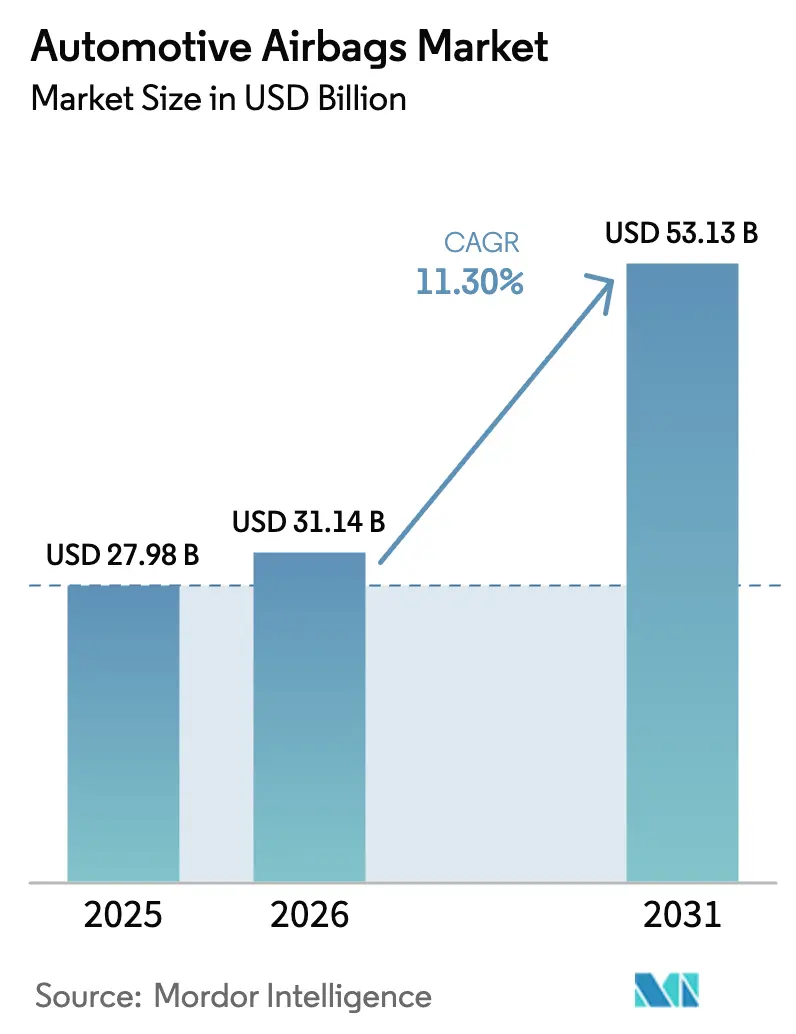

The automotive airbags market size is expected to grow from USD 27.98 billion in 2025 to USD 31.14 billion in 2026 and is forecast to reach USD 53.13 billion by 2031 at 11.30% CAGR over 2026-2031. Tighter frontal and side-impact regulations in emerging economies, the accelerating shift to electric vehicles, and sustained SUV demand provide the strongest tailwinds. Automakers are integrating more sensors and smarter electronic control units to fine-tune deployment, while suppliers invest in lighter fabrics that meet both sustainability and weight-reduction goals. The semiconductor shortage remains the chief near-term bottleneck, yet proactive inventory strategies and long-term supply agreements are mitigating its sting. Heightened retrofit activity—spurred by insurance incentives and rising safety awareness—adds another layer of momentum for the automotive airbags market.

Key Report Takeaways

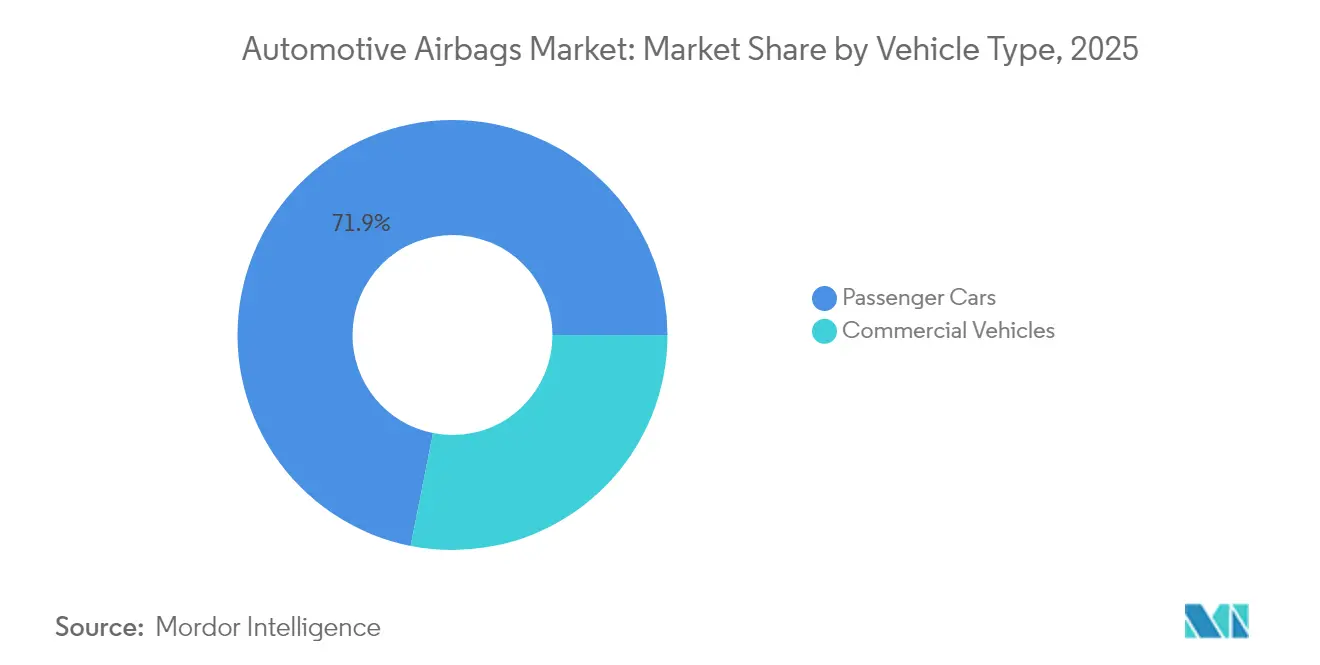

- By vehicle type, passenger cars led the automotive airbags market with a 71.88% revenue share in 2025, while commercial vehicles are projected to expand at an 8.12% CAGR through 2031 as safety mandates extend to trucks and buses.

- By propulsion type, battery electric vehicles (BEVs) are emerging as the fastest-growing sub-segment, expected to grow at a 14.85% CAGR, even though ICE vehicles still dominate with an 86.65% share.

- By component, airbag modules held a 52.10% share in 2025, but crash sensors and ECUs are growing fastest at a 11.95% CAGR, driven by rising demand for algorithm-optimized deployment precision.

- By material, nylon 66 remained the dominant choice with a 65.95% share in 2025, while polyester is expected to grow at a 13.05% CAGR owing to its cost-effectiveness and recyclability.

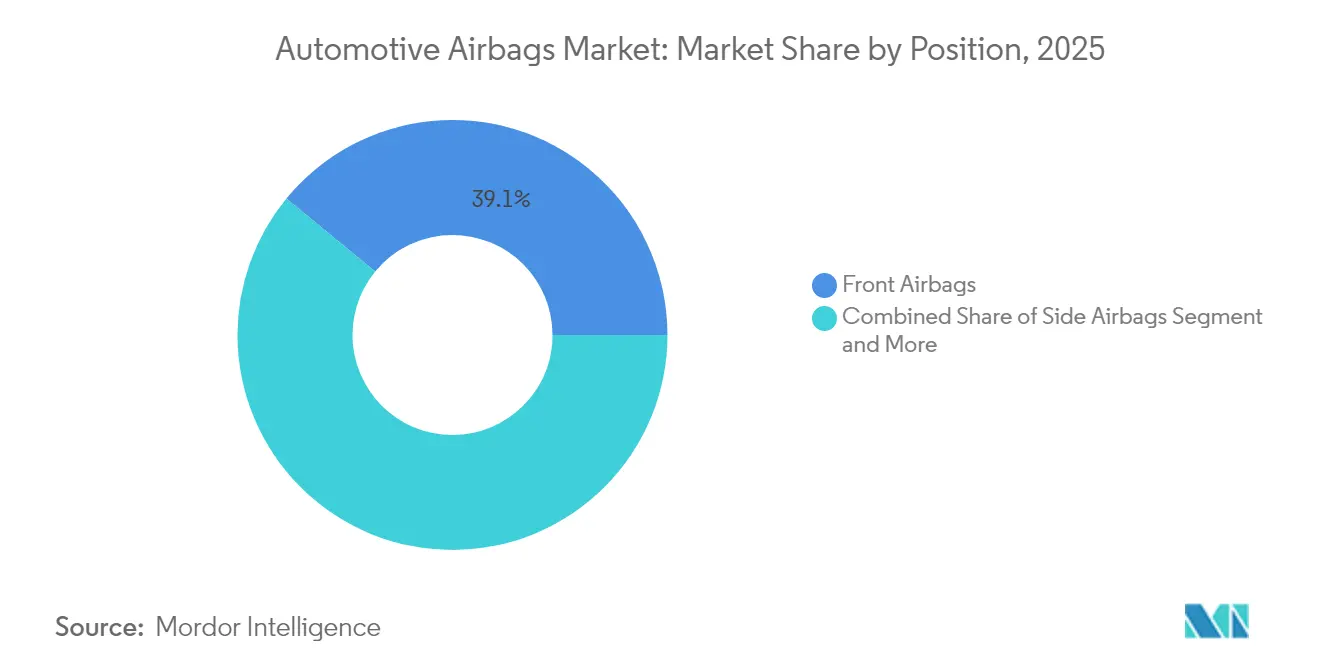

- By airbag position, front airbags accounted for 39.05% of the market in 2025, whereas curtain airbags are projected to grow at a 13.85% CAGR, supported by heightened side-impact safety focus.

- By sales channel, OEMs contributed 90.75% of the market in 2025, but the aftermarket is gaining momentum with a 13.45% CAGR, fueled by growing retrofit demand and safety regulation compliance.

- By geography, Asia-Pacific dominated with a 42.10% market share in 2025, while the Middle East and Africa is set to be the fastest-growing region with a 14.90% CAGR through 2031, aided by rising new vehicle production and import-based airbag integration.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Automotive Airbags Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Dual-Airbag Rules in Developing Market | +2.3% | India, Southeast Asia, Latin America | Short term (≤ 2 years) |

| Frontal and Side-Impact Mandates in Emerging Market | +2.1% | India, Brazil, ASEAN | Medium term (2-4 years) |

| EV Packaging Driving Module Integration | +1.8% | Europe, China | Medium term (2-4 years) |

| SUV Mix Driving Curtain-Airbag Demand | +1.7% | North America, spillover in Europe | Short term (≤ 2 years) |

| Chinese OEM Push for Euro NCAP Airbags | +1.5% | Global, with primary impact in China and export markets | Medium term (2-4 years) |

| Insurance-Linked Incentives for Fleet Upgrades | +1.2% | North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Frontal and Side-Impact Safety Mandates in Emerging Economies

Rapid regulatory rollouts have amplified unit volumes for the automotive airbags market. India’s rule requiring dual front airbags on all passenger vehicles from January 2025 alone adds nearly 10 million annual units. Brazil’s comparable mandate pushed national airbag penetration close to full coverage. These rules dovetail with consumer awareness campaigns and favorable insurance terms, accelerating factory install rates. Suppliers are ramping localized production to meet lead-time targets while maintaining global quality standards, ensuring cost parity for price-sensitive segments.

EV-Platform Packaging Needs Driving Multi-Module Integration

Battery placement and flat-floor cabins in EVs reshape crash dynamics, compelling designers to adopt specialized airbags. Autoliv’s Bernoulli Airbag™ accommodates wide cabin geometries and reduces inflator heat by 30%. Center airbags like Hyundai Mobis’ 2025 unit prevent driver-passenger contact in side impacts. These bespoke modules increase average airbags per EV, widening the automotive airbags market opportunity while pushing R&D toward lighter gas generators that minimize thermal stress around high-voltage packs.

Rising SUV Mix Spurring Demand for Side-Curtain Airbags in North America

SUVs account for more than 70% of U.S. light-vehicle sales, elevating rollover risk. Side-curtain airbags, which remain inflated during roll events, have become a persuasive feature in dealership showrooms. The Insurance Institute for Highway Safety notes a 37% reduction in driver deaths when head-protection curtains are present [1]."Airbags," Insurance Institute for Highway Safety, iihs.org Automakers are broadening coverage to third-row seats and integrating far-side units that protect against occupant-to-occupant injury. The result is a deepening penetration of curtain modules within the automotive airbags market.

Mandatory Dual-Airbag Rules in India and Similar Developing Markets

Regulators in India, Southeast Asia, and South America see dual airbags as the minimum viable safety standard. These low-cost compliance upgrades yield outsized life-saving benefits, as U.S. Department of Transportation data show frontal airbags cut driver fatalities by 29% [2]."Safer Vehicles," US Department of Transportation, transportation.gov Domestic assemblers in India, for instance, have re-engineered dashboards to house passenger bags without sacrificing cabin space. With local OEMs targeting cost-conscious consumers, this mandate delivers consistent volume gains for Tier-1 suppliers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Semiconductor and Inflator Propellant Shortages | -1.8% | North America, Europe | Short term (≤ 2 years) |

| Rising Zero-Defect R&D Costs Squeezing Tier-2 Margins | -1.2% | Global, with concentrated impact on smaller suppliers | Medium term (2-4 years) |

| Counterfeit Aftermarket Airbags | -0.9% | Asia, Africa, Latin America | Medium term (2-4 years) |

| EV Lightweighting Driving Alternative Restraint Exploration | -0.7% | Global, with early effects in the premium EV segment | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Semiconductor Shortages Disrupting Output

Airbag ECUs rely on 32-bit microcontrollers, and allocation shortfalls cut 2024 global vehicle output by 2.3 million units. Suppliers reported order backlogs stretching 28 weeks, prompting automakers to favor high-margin models. Component costs climbed 12-15% against 2023 benchmarks, squeezing Tier-2 margins. Strategic buffering and foundry-level agreements are stabilizing supply, yet the situation continues to cap near-term expansion for the automotive airbags market.

Counterfeit Aftermarket Airbags Erode Consumer Confidence

NHTSA estimates 250,000 counterfeit bags entered North American vehicles in 2024, with more than 80% failing safety tests. Illicit units, often sold online, undercut legitimate offerings and jeopardize occupants. OEMs and suppliers now embed QR codes and RFID tags for verification, but this raises unit costs by USD 3–5. Persistent policing and consumer education remain critical to safeguard the aftermarket’s credibility and, by extension, sustained growth of the automotive airbags market. [3]"Vehicle Air Bags and Injury Prevention," National Highway Traffic Safety Administration, nhtsa.gov

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: Passenger Cars Anchor Volume, Commercial Vehicles Accelerate

Passenger cars accounted for 71.88% of the automotive airbags market in 2025, buoyed by larger build counts and rising airbags per car. Commercial vehicles, however, are pacing faster with an 8.12% CAGR through 2031, as Europe’s General Safety Regulation mandates advanced restraint systems for new heavy-duty models starting in 2025. Fleet managers value the documented 42% reduction in injury-related downtime delivered by full airbag suites, a payoff that offsets upfront costs. The automotive airbags market size for commercial vehicles is projected to climb steadily, leveraging telematics-driven insurance discounts that reward safety-equipped trucks.

Surging e-commerce has intensified long-haul freight activity, calling for better driver protection in congested corridors. North American fleets are specifying side-curtain and knee airbags in Class 8 tractors, elevating average airbag content from two units in 2020 to five units in 2025. With regulators eyeing further occupant-safety enhancements, commercial platforms present a robust incremental opportunity for the automotive airbags market.

By Propulsion Type: BEVs Redefine Integration Complexity

ICE vehicles still dominate volume with an 86.65% share in 2025, yet BEVs exhibit the fastest growth in the automotive airbags market with a 14.85% CAGR through 2031. Battery packs curb traditional crumple zones, prompting the adoption of external pre-crash airbags and lower-temperature inflators. Autoliv’s low-heat gas generator addresses fire-safety constraints near high-voltage systems, widening design flexibility. The automotive airbags market size for BEVs is set to compound as global electric-vehicle sales exceed 17 million units in 2024, each requiring supplementary restraint modules.

Hybrid and plug-in hybrid models are growing at a 8.85% CAGR, driving demand for dual-mode deployment algorithms that accommodate both combustion and electric components. Suppliers integrate machine-learning logic into ECUs, parsing 400 data points per second to adjust inflation force. Such complexity lifts ECU revenue share and consolidates the automotive airbags market around players with software-heavy portfolios.

By Component: Sensors and ECUs Outpace Modules

Airbag modules commanded 52.10% of automotive airbag market revenue in 2025, yet sensors and ECUs are the fastest-growing segment, advancing at a 11.95% CAGR through 2031. Vehicles now host 6-12 accelerometers, pressure sensors, and gyroscopes feeding central processors that make release decisions within 30 milliseconds. Bosch’s 2025 AI-enabled ECU improves deployment accuracy by 10%, cutting false-trigger rates and helping automakers meet zero-defect goals. Advanced logic also underpins occupant-adaptive bags that modulate inflation to body size and seating position, a differentiator inside the automotive airbags market.

Inflators, growing at 7.55% CAGR, are trending toward cleaner propellants that trim carbon footprints. Development efforts center on replacing sodium azide with gas-generant mixes that produce fewer particulates without compromising open-time consistency.

By Material: Polyester Surges on Sustainability Edge

Nylon 66 held a 65.95% share of the automotive airbags market in 2025, driven by its superior tensile strength and heat resistance properties. Supply volatility and higher input costs, however, spur OEMs to trial polyester fabrics, which are 15-20% less expensive and nearly performance-parity. Autoliv’s 100% recycled-polyester cushion, launched in 2025, halves greenhouse-gas emissions relative to virgin polyester. SK Chemicals’ closed-loop recycling converts spent airbags to BHET monomer, showcasing circularity that may become regulatory necessity under the EU End-of-Life Vehicle Directive. Polyester’s 13.05% CAGR signals a gradual re-balancing of material shares within the automotive airbags market.

By Position: Curtain Airbags Extend Three-Row Coverage

Front airbags remain ubiquitous, representing 39.05% of units in 2025. Curtain airbags are registering the fastest growth, with a 13.85% CAGR, as they help mitigate rollover fatalities, particularly in high-center-of-gravity vehicles like SUVs and vans. Third-row curtains debuted in premium SUVs such as the 2025 Kia EV9, expanding protection to family haulers. Knee airbags clock an 8.65% CAGR and are now standard in several volume models across the Middle East, nurturing wider consumer expectations for leg-injury mitigation. External airbags, though nascent, exemplify frontier innovation, pre-tensing bumper zones to absorb side-impact energy before it reaches occupants—a development likely to broaden the automotive airbags market share for advanced positions.

By Sales Channel: Aftermarket Gains Relevance Through Retrofit

OEM fitments accounted for 90.75% of the automotive airbags market size in 2025. Retrofit demand, however, is driving the aftermarket segment to grow at a 13.45% CAGR through 2031. Insurance carriers in North America and Europe offer 5–15% premium breaks for vehicles upgraded with additional airbags, driving workshops to stock certified kits. Authentication technologies fight counterfeit infiltration, preserving trust and unlocking repeat business. Emerging economies adopt similar incentives as regulators observe safety outcomes, ensuring the aftermarket remains a sturdy complement to new-vehicle installations within the automotive airbags market.

Geography Analysis

Asia-Pacific controlled 42.10% of the automotive airbags market in 2025, anchored by China’s production of over 220 million airbag units and India’s dual-airbag mandate. Average airbag count per vehicle in China rose from 2.3 in 2020 to 4.8 in 2025, underpinned by domestic brands chasing Euro NCAP compliance for export models. Japan and South Korea contribute engineering depth and manufacturing scale, supplying modules to global OEM platforms. Regional suppliers such as Joyson leverage proximity to major assemblers, shortening lead times and deepening integration in next-generation EV programs.

The Middle East is the fastest-growing sub-region, projected to grow at a 14.90% CAGR through 2031. Gulf Cooperation Council countries tighten safety regulations and favor large SUVs, boosting airbags per vehicle beyond global averages. Local assembly ventures in Saudi Arabia and the United Arab Emirates lure Tier-1s to establish inflator and cushion facilities, positioning the region as an export hub into Africa and parts of Europe. The 2025 Nissan Patrol, fitted with seven airbags including knee units, exemplifies rising consumer expectations.

North America and Europe collectively make up nearly half of global revenue. North American growth rides on SUV popularity and stringent FMVSS side-impact updates, while Europe’s General Safety Regulation layers new obligations for far-side and pedestrian airbags starting 2026. Both regions spearhead AI-enabled ECUs and greener propellants, innovations that later cascade to emerging markets, reinforcing global homogeneity in safety standards across the automotive airbags market.

Competitive Landscape

The automotive airbags market is moderately concentrated. Autoliv leads the segment, supported by 66 plants worldwide and an innovation pipeline that introduced the Bernoulli Airbag Module in 2025. ZF Friedrichshafen follows, leveraging its system-level expertise post-TRW integration to offer combined sensor-to-actuator packages. Joyson Safety Systems rounds out the top trio, focusing on value-oriented solutions for mass-market models and maintaining strong positions with Chinese OEMs.

Consolidation persists as suppliers seek scale to absorb soaring R&D costs tied to zero-defect quality targets. Chinese players such as Jinzhou Jinheng advance aggressively, using domestic demand to refine manufacturing and win export contracts. Partnerships between airbag manufacturers and semiconductor firms are common: Bosch collaborates with Autoliv on AI-infused control units, while Continental secures microcontroller supply through long-term agreements with Taiwan-based foundries. These alliances underscore the strategic importance of chip security and software prowess in sustaining leadership within the automotive airbags market.

Sustainability is another competitive axis. Autoliv’s recycled-polyester cushion and ZF’s Active Heel Airbag reveal a turn toward resource-light products that also address new injury patterns, such as foot trauma in front-seat occupants. Suppliers that demonstrate both environmental stewardship and advanced occupant-protection capabilities are winning extended sourcing contracts as OEMs align procurement metrics with ESG targets.

Automotive Airbags Industry Leaders

-

ZF Friedrichshafen AG

-

Autoliv Inc.

-

Toyoda Gosei Co. Ltd

-

Joyson Safety Systems

-

Hyundai Mobis Co. Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Hyundai Mobis unveiled a center-mounted airbag for EVs that deploys between front occupants, preventing mutual collision during side impacts.

- February 2025: ZF Lifetec introduced the Active Heel Airbag, inflating beneath the floor carpet to limit foot injuries without demanding additional cabin space.

- February 2025: Autoliv launched airbag cushions made from 100% recycled polyester, reducing greenhouse-gas emissions by 50% while retaining safety performance.

- December 2024: Nissan debuted the all-new Patrol, integrating seven airbags—including knee units—to meet rising safety expectations in the Middle East.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study treats the automotive airbags market as the value generated by factory-installed and replacement airbag modules, driver, passenger, side, curtain, knee, and emerging center units, in all on-road passenger cars and commercial vehicles. Sensors, ECUs, and inflators are counted only when shipped as part of a complete module.

Scope exclusion: Seatbelts, airbag fabrics sold separately, two-wheeler airbags, and other passive-safety devices fall outside this sizing.

Segmentation Overview

-

By Vehicle Type

- Passenger Cars

- Commercial Vehicles

-

By Propulsion Type

- Internal Combustion Engine Vehicles (ICE)

- Battery Electric Vehicles (BEV)

- Hybrid & Plug-in Hybrid Vehicles (HEV/PHEV)

- Fuel-Cell Electric Vehicles (FCEV)

-

By Component

- Airbag Module

- Inflator

- Crash Sensor & ECU

- Airbag Fabric

-

By Material

- Nylon 66

- Nylon 6

- Polyester

-

By Position/Airbag Type

- Front Airbags

- Side Airbags

- Curtain Airbags

- Knee Airbags

- Inflatable Seat-Belts

-

By Sales Channel

- Original Equipment Manufacturer (OEM)

- Aftermarket/Replacement

-

By Geography

-

North America

- United States

- Canada

- Rest of North America

-

South America

- Brazil

- Argentina

- Rest of South America

-

Europe

- Germany

- United Kingdom

- France

- Spain

- Italy

- Rest of Europe

-

Asia-Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia-Pacific

-

Middle East and Africa

- Saudi Arabia

- United Arab Emirates

- Turkey

- South Africa

- Egypt

- Rest of Middle East and Africa

-

North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed procurement heads at OEMs, module engineers, propellant suppliers, and regional road-safety officials across Asia-Pacific, Europe, and the Americas. These interactions clarified discount structures, replacement rates after collisions, and likely timelines for six-airbag mandates, allowing us to challenge desk-based assumptions and tune price-volume curves.

Desk Research

We began by mapping publicly available datasets such as UNECE and NHTSA crash files, OICA production tallies, UN Comtrade HS-code trade flows, and Euro NCAP fitment guides, which help establish baseline vehicle pools and mandated airbag counts. Additional context was gathered from tier-1 supplier filings, investor decks, industry journals like SAE International, and regulatory dockets on upcoming mandates in India and Brazil. Paid tools, including D&B Hoovers for company revenues and Dow Jones Factiva for recall news, filled financial and event gaps. The sources cited illustrate key inputs; many other publications and databases were also reviewed.

Market-Sizing & Forecasting

A top-down model converts country-level light-vehicle production and parc data into potential airbag "positions," adjusts for regulatory fitment ratios, then multiplies by weighted average selling prices. Select bottom-up checks, supplier shipment roll-ups, and sampled OEM bill-of-materials are used to reconcile totals. Key variables tracked include new-vehicle output, mandated airbags per vehicle, module ASP trends, recall-driven replacement volumes, and scrappage rates. Multivariate regression, supported by ARIMA time-series smoothing, projects each driver to 2030; scenario analysis captures mandate slippage or faster EV uptake. Data gaps in smaller markets are bridged using regional proxy ratios vetted with experts.

Data Validation & Update Cycle

Outputs pass three layers of analyst review, variance tests against external indicators, and anomaly flags exceeding ±5%. Reports refresh annually; material events such as large recalls trigger interim updates. A final pre-publication sweep ensures clients receive the latest numbers.

Why Mordor's Automotive Airbags Baseline Commands Reliability

Published estimates differ because firms adopt varied scopes, base years, and price assumptions.

By isolating pure airbag modules and refreshing inputs yearly, Mordor's view offers decision-makers a consistent yardstick.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 27.98 bn | Mordor Intelligence | - |

| USD 40.40 bn | Global Consultancy A | Combines seatbelts with airbags and assumes uniform six-airbag fitment from 2023 |

| USD 17.11 bn | Regional Consultancy A | Uses ex-factory prices only, omits aftermarket replacements |

| USD 56.25 bn | Trade Journal B | Aggregates airbags plus seatbelts; limited reconciliation with production data |

These comparisons show that scope creep, pricing bases, and refresh cadence drive wide spreads.

Grounded in clearly defined modules, verified variables, and regular updates, Mordor's baseline remains the most traceable and repeatable reference for stakeholders.

Key Questions Answered in the Report

What is the current value of the automotive airbags market and its expected growth?

The automotive airbags market is valued at USD 31.14 billion in 2026 and is projected to reach USD 53.13 billion by 2031, reflecting an 11.30% CAGR over 2026-2031.

Which vehicle type contributes most to automotive airbags demand?

Passenger cars account for 71.88% of the automotive airbags market, although commercial vehicles are gaining ground with an 8.12% CAGR through 2031.

Why are curtain airbags growing faster than other types?

The popularity of SUVs and stricter side-impact standards are elevating demand for curtain airbags, which are expanding at a 13.85% CAGR.

What materials are suppliers adopting for sustainability?

While nylon 66 still dominates with 65.95% share, recycled polyester fabrics are advancing at a 13.05% CAGR, cutting greenhouse-gas emissions by about 50%.

Page last updated on: