Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

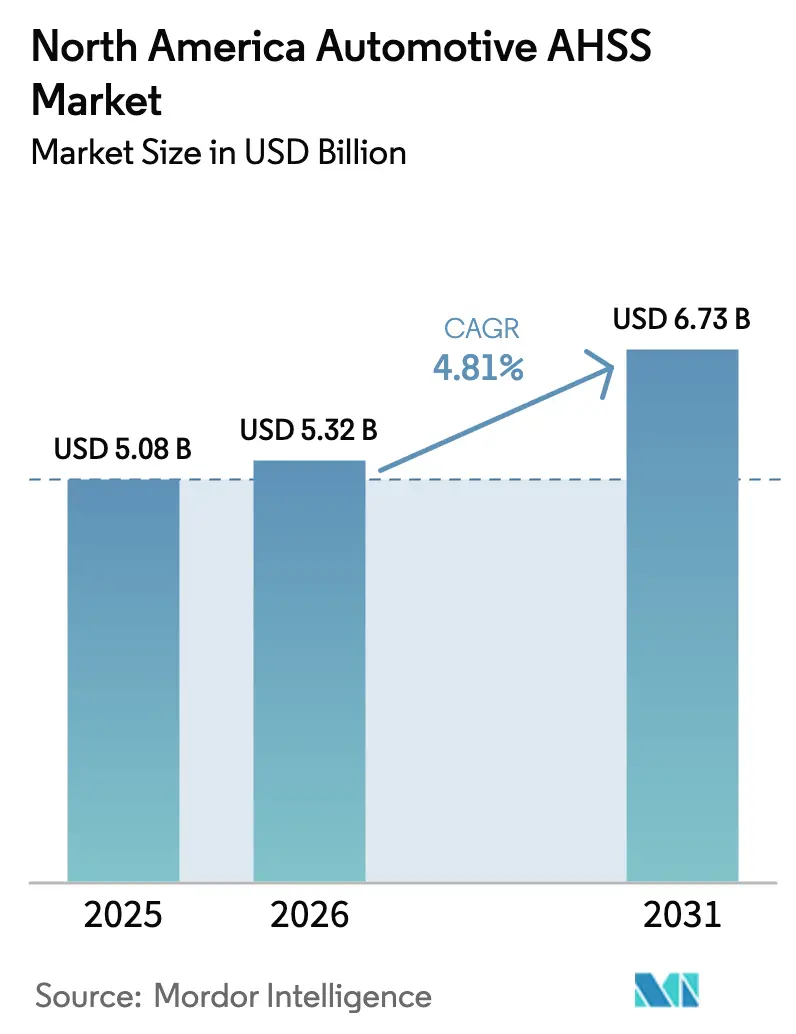

| Base Year Market Size (2025) | USD 5.08 Billion |

| Market Size (2026) | USD 5.32 Billion |

| Market Size (2031) | USD 6.73 Billion |

| Growth Rate (2026 - 2031) | 4.81% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Automotive AHSS Market Analysis by Mordor Intelligence

The North American automotive AHSS (Advanced High-Strength Steel) market size is projected to grow from USD 5.08 billion in 2025 to USD 5.32 billion in 2026, and is forecast to reach USD 6.73 billion by 2031, growing at a CAGR of 4.81% during the forecast period (2026-2031). Corporate Average Fuel Economy targets, stricter crash protocols, and the push for electric vehicles keep lightweighting at the forefront of design priorities. Advanced High-Strength Steels (AHSS) grades with higher strength levels offer a cost-effective way to reduce vehicle weight while maintaining crash energy absorption. The surge in battery-electric vehicles drives consistent demand, as every enclosure must protect high-voltage packs from potential intrusions. High-strength steels efficiently handle this task with minimal packaging penalties. On the supply front, new electric-arc-furnace capacity is expected to come online soon. This development not only reduces lead times from mills to Original Equipment Manufacturers (OEMs) but also boosts the local share of qualifying steel in line with USMCA regulations. Furthermore, producers are setting themselves apart by offering guaranteed hole-expansion ratios. This innovation allows stampers to utilize thinner gauges without the risk of edge-crack scrap, thereby reducing material waste per vehicle and speeding up program launches.

Key Report Takeaways

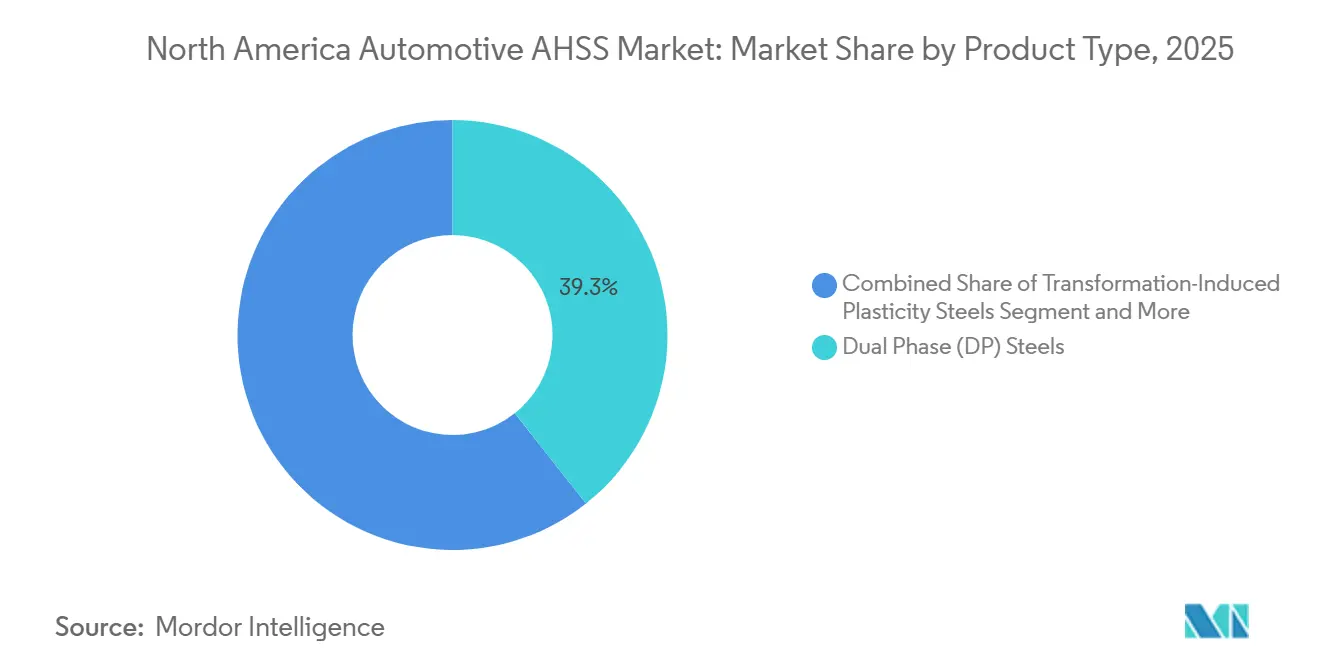

- By product type, dual-phase steels led with 39.33% of the North America automotive AHSS market share in 2025, while TRIP grades are advancing at a 7.78% CAGR through 2031.

- By vehicle type, passenger cars accounted for 62.29% of the North America automotive AHSS market share in 2025; light commercial vehicles are projected to expand at a 7.54% CAGR between 2026 and 2031.

- By application, body-in-white accounted for 43.86% of the North America automotive AHSS market share in 2025, and closures are forecast to grow at a 7.51% CAGR through 2031.

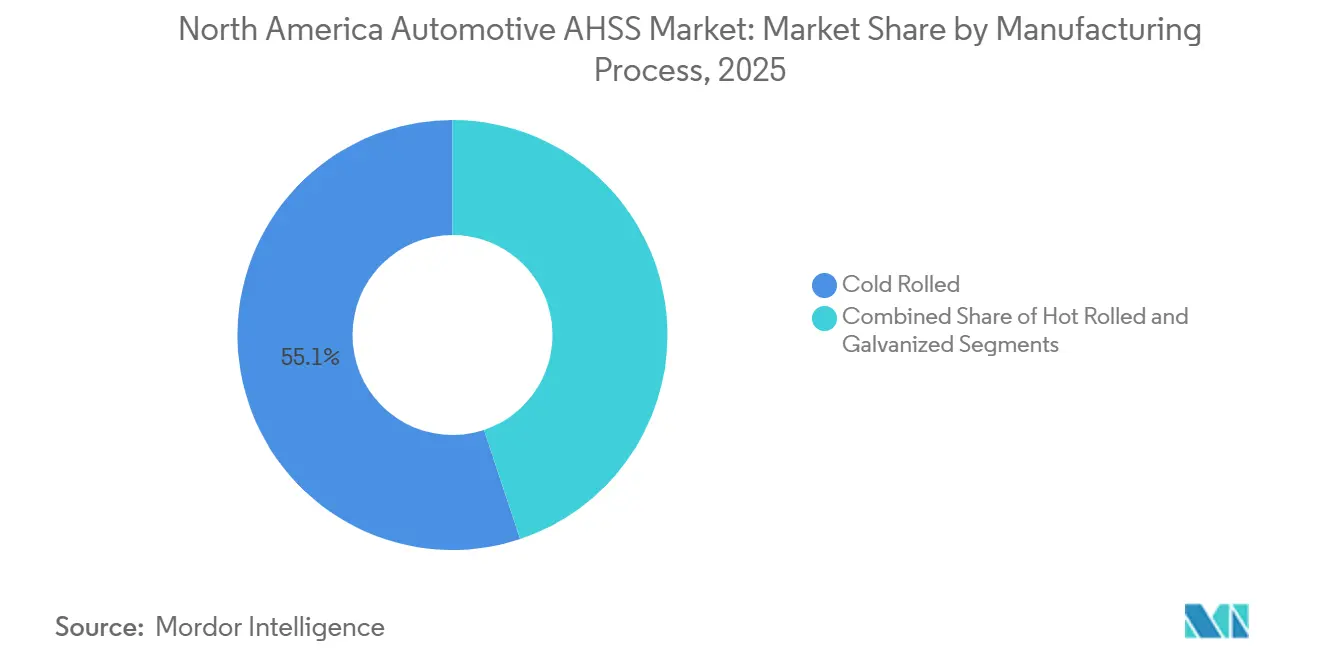

- By manufacturing process, cold-rolled product commanded 55.11% of the North America automotive AHSS market share in 2025, while hot-rolled output is set to post a 7.21% CAGR over 2026-2031.

- By end user, OEMs captured 82.29% of the North America automotive AHSS market share in 2025, but the aftermarket is on track for a 7.61% CAGR through 2031.

- By country, the United States accounted for 75.16% of the North American automotive AHSS market share in 2025; Canada is projected to grow at a 7.13% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

North America Automotive AHSS Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| U.S. and Canadian Fuel Economy and GHG Mandates Drive Lightweighting | +1.3% | United States, Canada | Medium term (2-4 years) |

| Higher IIHS and NCAP Crash-Rating Targets Boost Stronger Body Structures | +1.2% | United States, Canada | Short term (≤ 2 years) |

| North American EV Production Growth Increases AHSS Demand for Battery Protection | +1.0% | United States, Canada, Mexico | Medium term (2-4 years) |

| New U.S. EAF Installations Expand Advanced Steel Supply | +0.8% | United States, Canada | Long term (≥ 4 years) |

| USMCA Rules Prompt Tier-1 Hot-Stamping Near-Shoring | +0.6% | United States, Canada, Mexico | Short term (≤ 2 years) |

| Commercial HER Grade Roll-Out Ends Edge-Crack Scrap | +0.4% | United States, Canada | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Strict U.S./Canada Fuel-Economy and GHG Mandates Accelerate Light Weighting

The Environmental Protection Agency and the National Highway Traffic Safety Administration finalized 8% annual fuel-economy gains for model years 2024-2025 and a 10% step-up for 2026, pushing fleet averages toward 58 mpg-equivalent by 2032 [1]“Corporate Average Fuel Economy Standards,” U.S. Department of Transportation, transportation.gov. For every reduction in curb weight, fuel savings increase significantly. As a result, Body-in-White (BIW) manufacturers are transitioning from mild steel to dual-phase or complex-phase grades. These advanced materials enable a reduction in gauge without compromising torsional rigidity. Canada is adopting similar measures, introducing a zero-emission vehicle sales quota that aims to achieve full adoption. This move underscores the need for structural stiffness, especially as battery additions increase vehicle mass. A Federal Reserve study pegged the compliance cost as a percentage of a vehicle's price. This insight has led Original Equipment Manufacturers (OEMs) to prioritize material changes over more expensive propulsion modifications. Thyssenkrupp’s HCT980XG dual-phase steel offers significant weight reduction compared to mild steel, all while maintaining a torsional stiffness critical for Noise, Vibration, and Harshness (NVH)[2]“Multiphase Steel for Automotive,” Thyssenkrupp AG, thyssenkrupp.com.

Rising IIHS and NCAP Crash-Rating Targets Spur Stronger Body Structures

The Insurance Institute for Highway Safety tightened side-impact standards, setting a limit on B-pillar intrusion for a "Good" rating. To meet this benchmark, manufacturers often turn to press-hardened martensitic steel in cage structures. This marks a shift from the previously adequate components. Looking ahead, the NHTSA plans to introduce frontal-oblique and far-side tests, necessitating higher tensile targets in rocker and roof rails. In a bid for a Top Safety Pick+ rating, Nissan boosted AHSS content in its Rogue and incorporated tailor-welded pillars. Meanwhile, Chevrolet's Blazer EV, with its AHSS and UHSS integration, underscores the industry's stance: even mainstream EVs prioritize crashworthiness over cost.

Surge in North American EV Output Lifts AHSS Demand for Battery Protection

Regional production of battery-electric vehicles has surpassed significant volumes. Each vehicle's pack enclosure is fortified with ultra-high-strength steel, ensuring compliance with FMVSS 305 isolation standards. SSAB’s Docol CR1700M, boasting exceptional tensile strength, is roll-formable and ideal for tray frames. Cleveland-Cliffs unveiled its C-STAR™ steel, showcasing a fully steel battery box. This innovation not only reduces costs per vehicle compared to mixed-material designs but also enhances pole-side crash performance. Additionally, Martinrea secured substantial contract wins focusing on hot-stamped battery structures, underscoring supplier confidence in this burgeoning sector.

Domestic EAF Buildouts Widen Local Supply of Advanced Grades

ArcelorMittal's Calvert EAF will boost production, utilizing near-net-shape casting to directly feed galvanizing lines, eliminating the need for slab reheating. Nucor's Apple Grove sheet mill produces sheets, with a dedicated galvanizer focusing on DP 780 and TRIP 690 grades. Cleveland-Cliffs plans to launch a hydrogen-ready DRI facility in Middletown, aiming for a low-carbon AHSS feedstock. These initiatives promise to significantly cut OEM lead times while also reducing dependence on imports from Asia.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Conventional Steels and Aluminum Face a Cost Premium | -0.9% | United States, Canada, Mexico | Medium term (2-4 years) |

| Smaller Tier-2 Companies Delay Adoption Due to Costly Forming and Welding Upgrades. | -0.6% | United States, Canada | Long term (≥ 4 years) |

| Geopolitical Tensions Risk Supply of Alloying Elements Like Nickel (Ni) and Molybdenum (Mo). | -0.5% | Global, with acute impact on United States and Canada | Medium term (2-4 years) |

| Limited Galvanizing Line Capacity for UHSS Coatings Delays Programs. | -0.4% | United States, Canada | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Persistent Cost Premium Versus Conventional Steels and Aluminum

AHSS grades above certain strength levels command a price premium over lower-strength grades. Meanwhile, martensitic press-hardened stock can fetch an even heftier premium. Thanks to aluminum's low density, manufacturers can achieve significant weight reduction in non-structural lids. This limitation confines AHSS usage primarily to structures where stiffness is prioritized over weight. While tariffs have diminished the cost advantage of imported aluminum, manufacturers of hoods and liftgates continue to adopt a mixed-material approach. However, for smaller, price-sensitive battery electric vehicles (BEVs), the scales tip back in favor of steel. This is because AHSS provides most of the desired weight reduction at a significantly lower cost per unit of raw material. In a notable move, Cleveland-Cliffs demonstrated that, with only minor adjustments to the dies, AHSS blanks can be processed on aluminum press lines. This development simplifies the transition between materials for original equipment manufacturers (OEMs).

Capital-Intensive Forming / Welding Upgrades Slow Adoption at Smaller Tier-2s

Servo presses, boasting ratings above those of their conventional counterparts, and MFDC weld guns equipped with adaptive control add to per-line costs. Meanwhile, laser-welded tailored blank stations can add significant expenses. However, smaller Tier-2s, operating on thin margins, find it challenging to finance such tooling. This financial strain has created a landscape in which the top stampers account for the majority of turnover in structural components. Absent pooled purchasing or sustained OEM tooling backing, the penetration of AHSS beyond the primary supply tier is likely to remain subdued.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: TRIP Steels Lift Crash Energy Absorption

Dual-phase steels maintained a 39.33% of the North America automotive AHSS market share in 2025, owing to their formability-versus-strength sweet spot. TRIP grades are forecast to post a 7.78% CAGR over 2026-2031, the fastest among the product slate. In crumple zones, the ability to harden on the fly and distribute deformation is crucial. Complex-phase steels occupy specialized roles in suspension links, while martensitic grades take precedence in high-strength pillars, especially where IIHS thresholds leave no room for error. Although twinning-induced plasticity and warm-formed steels are niche players, they are drawing significant R&D attention, as evidenced by METAKUS’s award-winning SIBORA.

A specific type of steel offers high tensile strength and notable elongation, enabling significant draw ratios in crush cans. Adjustments to punching clearance have shown potential to boost HER, impacting die standards across a broad region. A particular concept, utilizing this steel in hydro-formed pillars, achieved cost savings compared to press-hardened alternatives while delivering performance aligned with top safety standards. Despite these advancements, certain high-strength steels are expected to grow steadily, driven by the continued need for durable components in side-impact load paths.

By Vehicle Type: LCV Electrification Accelerates Lightweighting

Passenger cars remain the tonnage leader at 62.29% of the North America automotive AHSS market share in 2025, but growth is slow as platforms migrate to cost-conscious BEV architectures. Light commercial vehicles are set for a 7.54% CAGR as parcel and service fleets electrify and increase payload. Medium- and heavy-duty trucks selectively incorporate Advanced High-Strength Steel (AHSS) in their cabs and chassis rails, limiting its use to a small percentage of the vehicle's total mass.

GM’s BrightDrop Zevo uses a higher proportion of AHSS to counterbalance a heavy battery, while maintaining a spacious cargo bay. Ford’s updated E-Transit increased its AHSS content to accommodate a larger battery pack without reducing payload capacity. Rivian’s EDV utilizes hot-stamped door beams to enhance range efficiency. In the passenger car segment, Honda’s Civic incorporates a significant amount of AHSS within its ACE cage, while more affordable models limit the use of premium materials to keep costs competitive.

By Application: Closures Gain on Tailor-Welded Blank Use

The BIW still commands 43.86% of the North America automotive AHSS market share in 2025 as the primary crash-energy sink. Closures will grow at a 7.51% CAGR because tailor-welded blanks pair thin DP 590 skins with martensitic 1,180 MPa inserts to meet pedestrian-impact requirements without a mass penalty. Chassis and suspension parts selectively incorporate AHSS, balancing considerations of weight, cost, and form complexity. Meanwhile, bumpers opt for UHSS, especially when regulatory load cases necessitate a more compact design.

Nissan's latest Rogue utilized a cold-stamped B-pillar blank, achieving a significant weight reduction and securing a top safety accolade. Chevrolet's Blazer EV chose third-generation AHSS over PHS for its pillars, resulting in notable cost savings per unit. ArcelorMittal's investment in laser blanking is set to bolster door outers, featuring thinner skins seamlessly welded to thicker reinforcements. While suspension links remain a niche, Audi's planned refresh aims to integrate hot-stamped steel links, targeting substantial weight reduction over aluminum forgings while maintaining a similar cost.

By Manufacturing Process: Hot-Rolled Output Expands with EAF Startups

Hot-rolled AHSS is on track for a 7.21% CAGR, lifted by new EAF mills that specialize in automotive chemistries and feed directly to galvanizers. Cold-rolled tonnage accounted for 55.11% of the North America automotive AHSS market share in 2025, owing to strong outer-panel finish demand. With the introduction of new coating lines, the bottleneck on substrates exceeding certain strength levels is starting to ease.

Nucor’s Apple Grove mill is now shipping hot-rolled DP 780 directly to galvanizing, maintaining tight chemistry controls. ArcelorMittal’s near-net-shape caster is producing hot bands with low carbon equivalents, resulting in lower costs than slab routes. SSAB’s HR1500M, backed by HER guarantees, is now targeting battery frames, prioritizing functionality over cosmetic finish. While legacy galvanizers struggled with adhesion loss on high-strength substrates, Nucor and Ternium's new lines, equipped with integrated pre-treatments, are now successfully processing UHSS throughput.

By End User: Aftermarket Rises on Collision-Repair Complexity

Aftermarket tonnage is forecast to rise at 7.61% CAGR as repair networks invest in MFDC welders and certified blanks. OEM channels captured 82.29% of the North America automotive AHSS market share in 2025, but slowed as vehicle build levels approached high annual levels and per-car AHSS share matured.

A significant portion of independent shops lack MFDC guns, leading them to rely on dealer networks for repairs, often at a price premium. The IIHS mandates that repaired structures adhere to original crash metrics, making certified replacement parts with traceable heat numbers essential. Tesla's in-house hot-stamping of door rings effectively binds repairers to pricier service-center components. Cleveland-Cliffs introduced pre-cut blank kits targeting independent shops, aiming to generate substantial aftermarket revenue.

Geography Analysis

The United States delivered 75.16% of the North American automotive AHSS market share in 2025. In the Midwest and Southeast, the Detroit Three and various transplant plants collectively assemble a significant volume of light vehicles, solidifying the demand. As CAFE and IIHS regulations tighten, they continue to push tensile targets higher. New EAF capacities are expected to introduce additional AHSS-capable steel in the coming years. Meanwhile, Section 232 tariffs have reduced aluminum's cost advantage, enabling designers to achieve weight targets using steel. This steel meets a substantial portion of the performance delta while maintaining a lower material cost.

Canada is projected to post the fastest CAGR at 7.13% through 2031. USMCA melt-and-pour verification from July 2027 channels hot-stamping investment into Ontario and Quebec, close to assembly lines. Transport Canada’s ZEV mandate is driving increased use of steel for pack protection in BEVs. Meanwhile, Algoma Steel leverages its cost advantage from affordable hydroelectric power, strengthening its hot-rolled steel supply to stampers in Ontario.

North America, led by Mexico, has become a key hub for coating and hot stamping. Nucor-JFE’s galvanizer and Ternium’s Pesqueria line play a significant role in supplying GM, Ford, and Stellantis plants. Mexico’s strategic location, competitive labor costs, and treaty compliance make it a natural extension of the supply corridor from the Great Lakes to the Southeast.

Competitive Landscape

Top mills—ArcelorMittal, Nucor, Cleveland-Cliffs, U.S. Steel, and SSAB—control a significant portion of the market capacity, creating opportunities for specialized entrants. Incumbent mills are expanding downstream: Cleveland-Cliffs, in a strategic move, acquired POSCO's coating expertise through an equity swap; Nucor is heavily investing in galvanizers, aiming to reclaim margins previously lost to toll coaters. SSAB is capitalizing on guaranteed HER products, while METAKUS is exploring opportunities in warm-forming niches[3]“SSAB Zero™ Fossil-Free Steel,” SSAB AB, ssab.com.

NanoSteel is promoting a lower-density AHSS, highlighting its potential to enhance EV ranges. Martinrea has adopted machine-learning weld controls, achieving a notable reduction in scrap for hot-stamped enclosures. U.S. Steel, utilizing Nippon's technology, is achieving precise gauge tolerances, crucial for ultra-thin, high-strength skins. Mills without Electric Arc Furnaces (EAF) or low-carbon strategies are increasingly at a disadvantage as OEMs tighten their Scope 3 emissions criteria.

North America Automotive AHSS Industry Leaders

ArcelorMittal NA

United States Steel Corporation

Nucor Corporation

Cleveland-Cliffs Inc.

SSAB AB

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: ArcelorMittal Tailored Blanks North America (AMTB) announced plans to establish a new plant in Ingersoll, Ontario. Construction of the facility is currently in progress, with production equipment expected to arrive at a later stage. Installation and commissioning activities will follow, and the company aims to begin ramping up production at the plant after these processes are completed.

- June 2025: ArcelorMittal has acquired Nippon Steel Corporation’s stake in AM/NS Calvert, now renamed ArcelorMittal Calvert. This facility, one of North America's top steel finishing plants, features a hot strip mill (HSM) for advanced high-strength steels (AHSS), a Continuous Pickling Line (CPL) for Line Pipe & Stainless products, and a Pickle Line-Tandem Cold Mill (PLTCM) for automotive production. It also includes Coating and Continuous Annealing Lines that produce galvanized, galvanneal, aluminized, and cold-rolled products, including Gen3 AHSS and Press Hardened Steel (PHS).

North America Automotive AHSS Market Report Scope

The North America automotive AHSS market report is segmented by product type (dual phase, trip, complex phase, martensitic, and others), vehicle type (passenger cars, and more), application (BIW, chassis, suspension, closures, and more), manufacturing process (cold rolled, hot rolled, and galvanized), end user (Original Equipment Manufacturer (OEM) and aftermarket), and country. The market forecasts are provided in value (USD).

By Product Type

| Dual Phase (DP) Steels |

| Transformation-Induced Plasticity (TRIP) Steels |

| Complex Phase (CP) Steels |

| Martensitic Steels |

| Others (including TWIP, Hot-Formed Steels) |

By Vehicle Type

| Passenger Cars |

| Light Commercial Vehicles (LCVs) |

| Medium and Heavy Commercial Vehicles (MHCVs) |

By Application

| Body Structure (BIW) |

| Chassis |

| Suspension |

| Closures (Doors, Hoods, Trunk Lids) |

| Bumpers |

| Other Components |

By Manufacturing Process

| Cold Rolled |

| Hot Rolled |

| Galvanized |

By End User

| Original Equipment Manufacturer (OEM) |

| Aftermarket |

By Country

| United States |

| Canada |

| Rest of North America |

| By Product Type | Dual Phase (DP) Steels |

| Transformation-Induced Plasticity (TRIP) Steels | |

| Complex Phase (CP) Steels | |

| Martensitic Steels | |

| Others (including TWIP, Hot-Formed Steels) | |

| By Vehicle Type | Passenger Cars |

| Light Commercial Vehicles (LCVs) | |

| Medium and Heavy Commercial Vehicles (MHCVs) | |

| By Application | Body Structure (BIW) |

| Chassis | |

| Suspension | |

| Closures (Doors, Hoods, Trunk Lids) | |

| Bumpers | |

| Other Components | |

| By Manufacturing Process | Cold Rolled |

| Hot Rolled | |

| Galvanized | |

| By End User | Original Equipment Manufacturer (OEM) |

| Aftermarket | |

| By Country | United States |

| Canada | |

| Rest of North America |

Key Questions Answered in the Report

How large is the North America advanced high-strength steel market in 2026?

The market is valued at USD 5.32 billion in 2026, on track to reach USD 6.73 billion by 2031 at a 4.81% CAGR through 2031.

Which product type grows fastest through 2031?

TRIP grades post the fastest expansion at a 7.78% CAGR due to superior crash energy absorption.

Why is AHSS demand rising in electric vans?

Battery packs increase curb weight, and fleets use AHSS to protect cells while keeping payloads high.

What limits AHSS uptake among small stampers?

High capital outlays for servo presses, MFDC welders, and laser cells make upgrades hard to finance.

Which country shows the fastest market growth ahead?

Canada leads with a 7.13% CAGR, aided by ZEV mandates and new hot-stamping lines near Ontario plants.

Page last updated on: