Bulgaria Container Glass Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

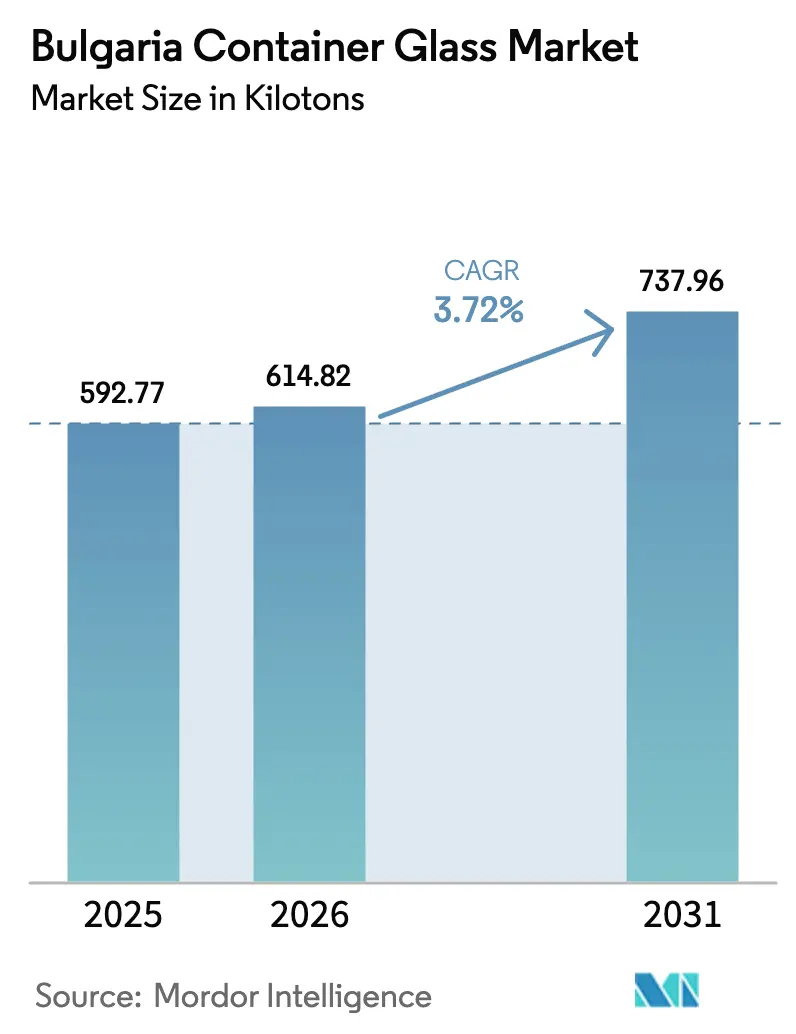

| Base Year Market Size (2025) | 592.77 kilotons |

| Market Volume (2026) | 614.82 kilotons |

| Market Volume (2031) | 737.96 kilotons |

| Growth Rate (2026 - 2031) | 3.72% CAGR |

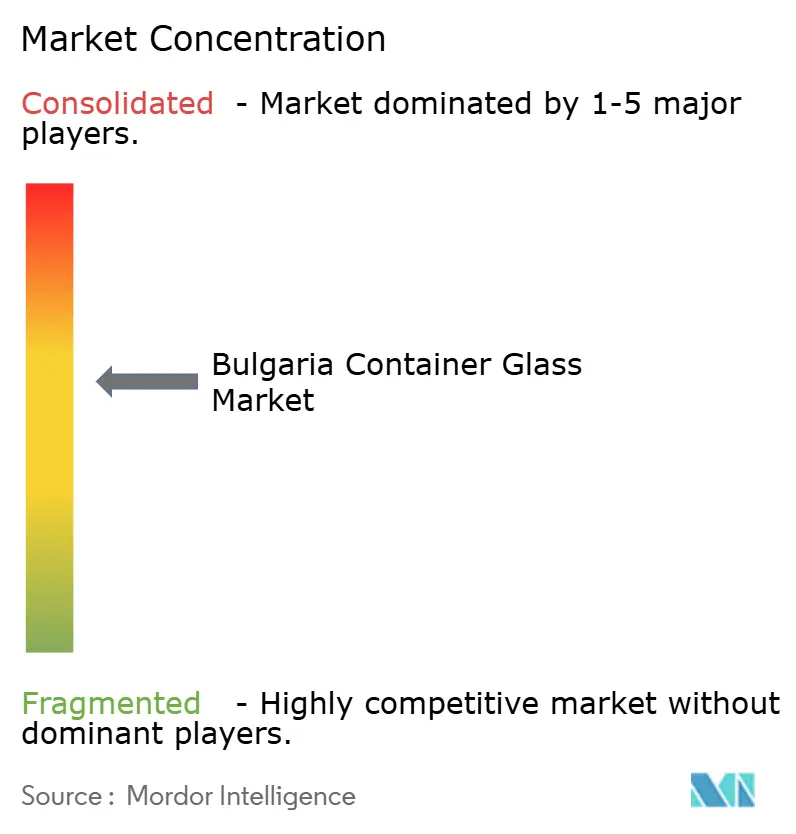

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Bulgaria Container Glass Market Analysis by Mordor Intelligence

The Bulgaria container glass market size was valued at 592.77 kilotons in 2025 and estimated to grow from 614.82 kilotons in 2026 to reach 737.96 kilotons by 2031, at a CAGR of 3.72% during the forecast period (2026-2031). This trajectory rests on Bulgaria’s alignment with the European Union circular-economy agenda, the country’s cost-competitive manufacturing profile inside the single market, and a deepening commitment by beverage, food, and pharmaceutical brand owners to embed returnable or refillable glass in their packaging portfolios. Demand strength is further amplified by premiumization trends across craft alcohol, beauty, and OTC healthcare, each of which favors the material’s chemical inertness and elevated shelf-presence. At the same time, sustained foreign direct investment in furnace upgrades and cold-end automation disseminates best-in-class energy efficiency expertise throughout the local value chain, thereby cushioning margins as electricity prices rose 9% and natural-gas tariffs increased by almost 10% in January 2025.[1]BNR, “Spikes in Bulgarian Electricity and Natural-Gas Tariffs,” bnr.bg Strategic risks do exist, chiefly the sector’s reliance on imported silica sand blends and the ongoing shortage of certified furnace technicians, but most operators continue to report utilization rates above 80%, reflecting a fundamentally favorable supply-demand balance.

Key Report Takeaways

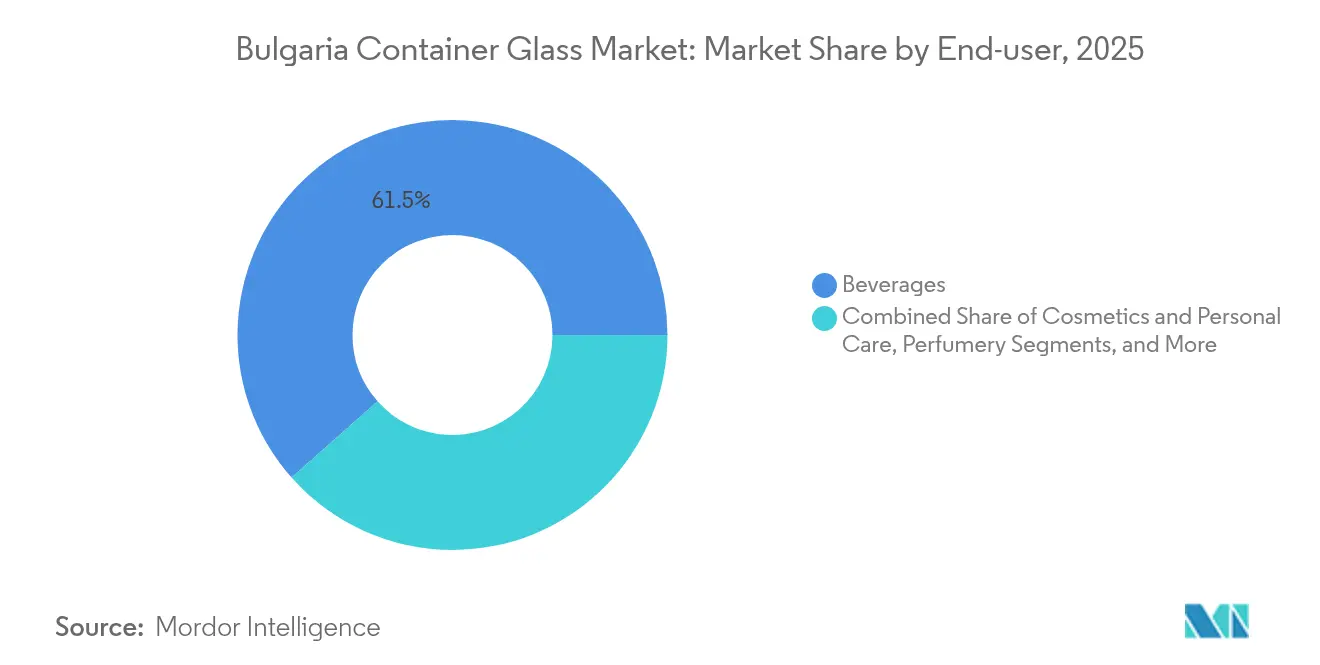

- By end-user, beverages captured 61.54% of the container glass market share in 2025.

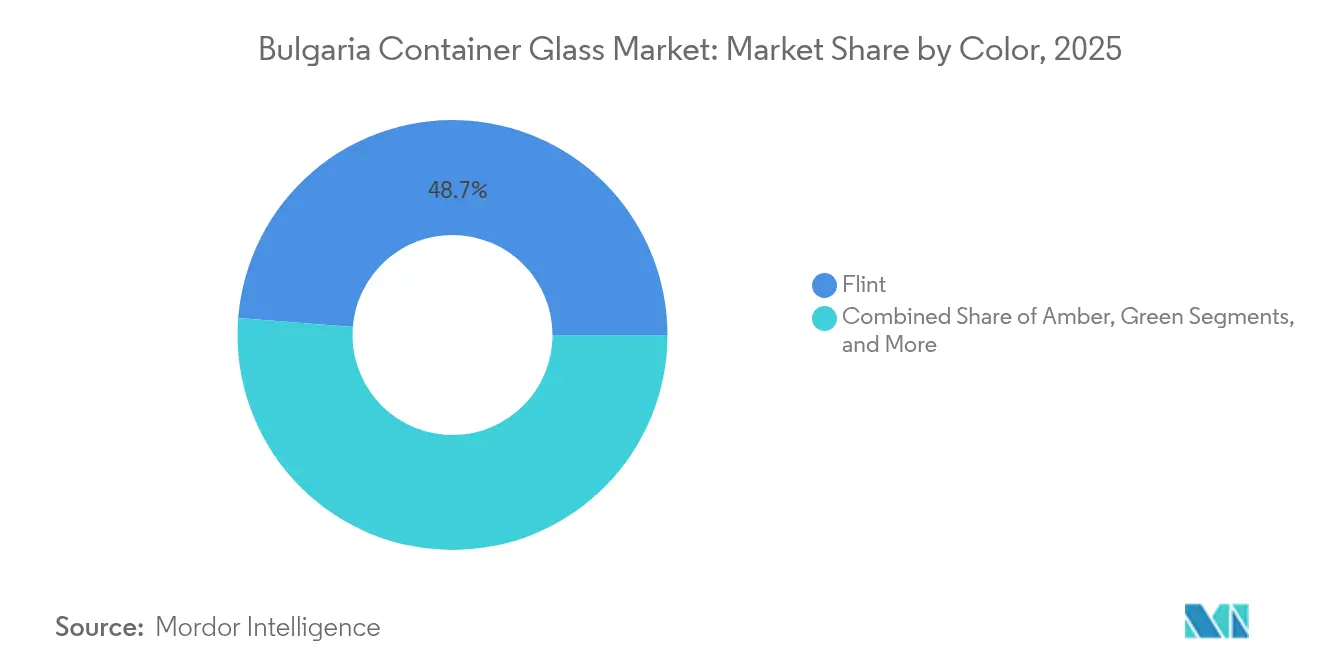

- By color, the container glass market size for the amber glass segment is projected to grow at a 5.61% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Bulgaria Container Glass Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for sustainable packaging in beverages | +1.2% | Bulgaria, with spillover to Balkans | Medium term (2-4 years) |

| Pharmaceutical demand for high-purity containers | +0.8% | National, with early gains in Sofia, Plovdiv | Long term (≥ 4 years) |

| Government incentives for recycling infrastructure | +0.6% | National | Medium term (2-4 years) |

| EU circular-economy targets accelerating glass reuse | +0.9% | EU-wide, concentrated in Bulgaria | Long term (≥ 4 years) |

| Premiumisation trend in craft alcohol boosting flint glass | +0.4% | National, with concentration in urban centers | Short term (≤ 2 years) |

| Breweries' shift from cans to returnable glass | +0.3% | Regional, with focus on major brewing centers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Sustainable Packaging in Beverages

Multinational bottlers and leading domestic breweries are redesigning their procurement strategies to prioritize closed-loop glass, bolstered by the EU mandate that 90% of beverage containers be separately collected by 2029. In 2024, Coca-Cola HBC deployed 193,285 tonnes of returnable glass across its regional network, a shift that reduces lifecycle emissions per liter filled by up to 40%.[2]Coca-Cola HBC, “Glass Packaging Usage Report 2024,” coca-colahellenic.com Bulgarian plants are logical beneficiaries because road freight from Sofia or Plovdiv to Balkan capitals stays within a 500 km radius, keeping transport emissions competitive with local PET. Bulk buyers also negotiate multi-year contracts that include cullet quality clauses, encouraging suppliers to increase the recovered-glass content, thereby reducing energy use by roughly 3% for every 10% of cullet blended. Over the medium term, beverage-sector ESG scorecards will hard-wire these gains, supporting continuous order flow for Bulgarian furnaces.

Pharmaceutical Demand for High-Purity Containers

European Medicines Agency guidelines stipulate borosilicate or Type I neutral glass for parenteral drugs, a specification that has pushed regional capacity expansions by SCHOTT Pharma and other specialty converters. Bulgaria sits inside a cross-border pharma belt stretching from Hungary to Serbia, meaning GMP-certified Bulgarian vials can be trucked to CMO fill-finish sites within one day. Lower cost bases versus Western Europe and reduced cold-chain risk give domestic converters a competitive edge. Moreover, ISO 15378 and EU GMP audits deter opportunistic entrants, preserving pricing discipline and underpinning a 0.8% positive swing in forecast CAGR. Longer-term, injectable biologics and vaccine booster platforms will sustain this demand, keeping high-clarity flint and amber outputs in tight balance.

Government Incentives for Recycling Infrastructure

Bulgaria’s Extended Producer Responsibility regulation channels brand-owner levies into collection and color-sorting hubs, a mechanism that provided USD 8.4 million in earmarked funds during 2024. Municipal tenders across Varna, Burgas, and Stara Zagora co-finance upgrades to bottle banks and optical sorters, resulting in a doubling of recovery volumes at double-digit rates. Higher cullet availability yields direct cost relief because every 10% increase in recycled input reduces furnace energy demand by approximately 2%, a particularly valuable offset following the January 2025 tariff hike. In parallel, several operators have negotiated green-electricity PPAs with solar farms under Bulgaria’s Renewable Energy Act, ensuring that the recycling flywheel reinforces both profitability and carbon-intensity benchmarks.

EU Circular-Economy Targets Accelerating Glass Reuse

The 2025 Packaging and Packaging Waste Regulation requires member states to implement nationwide deposit-return schemes by 2029, thereby propelling glass into a favored position for reuse loops. Bulgarian converters are therefore locking in long-term supply agreements with brand owners who wish to avoid more costly compliance penalties associated with single-use plastics. Because flint bottles often complete 15-25 refill cycles before retirement, breweries and soft-drink fillers realize considerable amortization benefits, channeling part of those savings into premium container design and brand-enhancing embossments. The regulatory deadline further stimulates furnace refurbishments that boost pull capacities in the 180-220 tonnes-per-day range, cementing Bulgaria’s role as a strategic hub for returnable-glass servicing within Southeastern Europe.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Labour shortages in furnace operations | -0.7% | National, concentrated in industrial regions | Short term (≤ 2 years) |

| High energy costs versus PET alternatives | -0.9% | National | Medium term (2-4 years) |

| Limited domestic silica sand quality | -0.5% | National, with regional sourcing challenges | Long term (≥ 4 years) |

| Slower GDP growth dampening discretionary spend | -0.3% | National, with urban concentration | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Labour Shortages in Furnace Operations

Specialist glassblowing and hot-end maintenance skills are in short supply as Bulgaria’s working-age population continues to shrink. Attrition rates in larger plants surpassed 15% during 2024, forcing operators to run shifts with under-staffed forehearth crews and to trade spare capacity on short notice. Training a furnace technician to full competency requires 18-24 months, and poaching by Western European sites offering 20-30% higher wages remains a persistent drain. Although automation is progressing, the complexity of live glass flow makes full substitution impractical in the near term, subtracting roughly 0.7% from the market’s annual growth outlook.

High Energy Costs Versus PET Alternatives

Container glass production consumes roughly 2.5 MWh per tonne, so the 2025 jumps in Bulgaria’s electricity and natural-gas tariffs place upward pressure on ex-works prices. PET, by comparison, relies on lower-temperature polymerization and benefits from a strong regional PTA supply, narrowing the unit-cost gap in mass-market mineral water and edible oil applications. While sustainability premiums still favor glass in hospitality and upscale retail, price-sensitive categories such as private-label foodstuffs may delay migration from plastic. The resulting headwind subtracts an estimated 0.9% from the compound growth curve, underscoring the need for on-site cogeneration, waste heat recovery, and photovoltaic installations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End-User: Beverages Retain Scale as Specialty Segments Accelerate

The beverages channel contributed 61.54% of Bulgaria's container glass market share in 2025, underscoring the sector’s dependence on returnable orders for beer, spirits, and soft drinks. This leadership is based on multi-plant bottling agreements that specify minimum glass allocations to ensure filler line efficiency. Although beverage volumes dominate, absolute margins are tighter because of high SKU churn and stringent filling-line tolerances that favor standardized bottle footprints. The cosmetics and personal care categories, although smaller, are registering the fastest growth, expanding at a 4.18% CAGR through 2031. Luxury skincare lines have adopted flint jars with micro-thin aluminum caps, and several dermo-cosmetic players require USP Type III glass to maintain minimal preservative loads, supporting price points that exceed those of beverage-grade flint by nearly 55 EUR per tonne (USD 61 per tonne). Food packaging applications such as condiments and fruit preserves provide a predictable baseline, but modest promotions in modern trade keep their growth curve aligned with GDP progression rather than outpacing it.

BA Glass Bulgaria’s EUR 30 million (USD 33 million) solar and waste-heat projects reflect the sector’s broader energy-mitigation logic, especially for plants running varied batch sizes for cosmetics and OTC healthcare. Suppliers that can validate ISO 15378 lines for pharmaceutical sub-contractors find themselves in a sweet spot, balancing steady OTIF metrics demanded by global generic-drug firms with higher netback prices. Perfumery glass, niche in tonnage terms, nevertheless adds an outsized contribution to operating margin because decorative hot stamping, acid-etching, and color-spray finishes are performed in-house, capturing value that would otherwise sit with external decorators. Overall, the mix shift toward specialty-grade orders supports rational capacity additions, mitigating the risk of oversupply that often plagues monolithic beverage-oriented furnaces.

By Color: Flint Keeps Leadership While Amber Captures Momentum

Flint glass delivered 48.74% of the 2025 volume, evidence of its entrenchment in spirits, cocktail mixers, and pharmaceutical vials, where visual purity is a stringent requirement. Bulgaria's container glass market size for flint outputs is expected to remain steady, given the concurrent rise of premium white spirits brands targeting duty-free channels. Amber is the standout gainer, growing at 5.61% CAGR, thanks to craft brewers who value amber’s 95% UV-blocking profile that mitigates lightstruck off-flavors. National health authority procurement for amber ampoules and insulin bottles adds another dependable demand pocket. Green glass holds its own because legacy European wine SKUs continue to standardize on 750 ml containers that mask sediment and reduce light exposure. Specialty blues and pinks sit below 3% of total tonnage yet command premiums exceeding 120 EUR per tonne (USD 135 per tonne), creating margin buffers that compensate for low run lengths.

Verallia’s H1 2024 performance, featuring a 25.8% revenue decline in Northern and Eastern Europe, illustrates how exchange-rate volatility and sluggish beer markets can impact traditional green-glass tonnage. In response, several Bulgarian operators have installed dual-firing furnaces that enable quick color changeovers, reducing downtime to six hours compared to the standard 12 hours. The flexibility unlocks small-batch amber or blue campaigns without derating capacity, ensuring operators can address emerging craft segments without large CAPEX outlays. Over the forecast horizon, sustained diversification of color portfolios will be pivotal for Bulgaria container glass market resilience as shipment schedules become increasingly SKU-fragmented.

Geography Analysis

Bulgaria container glass market operates in symbiosis with the wider European supply chain that prizes cost-effective capacity located within tariff-free borders. The Sofia-Plovdiv industrial axis, home to nearly three-quarters of total melting capacity, leverages two intersecting trans-European rail corridors and proximity to Thessaloniki port, allowing finished pallets to reach Central European depots inside 48 hours. Northern districts such as Pleven and Ruse have begun to attract brownfield upgrades, encouraged by local tax incentives and available labor pools freed by agricultural mechanization. The newly announced Ruse eco-industrial park earmarks 60 hectares for glass upstream suppliers, signaling a drive to regionalize silica-mix stockpiles and reduce reliance on imports from Türkiye.

Cross-border trade flows validate Bulgaria’s strategic placement. Roughly 38% of domestic output left the country in 2024, primarily headed to Greece, Romania, and Croatia. Meanwhile, 12% of Bulgarian consumption relied on specialized imports, mainly coated-flint spirit bottles and extra-flint pharmaceutical vials from Czechia. Such two-way trade underscores that the Bulgarian container glass market is embedded in a complex lattice of European sourcing decisions that weigh currency swings, haulage tariffs, and carbon footprint metrics. High energy prices remain the Achilles’ heel for local producers, yet renewable PPAs and cullet-rich batch recipes are eroding that disadvantage, especially against Ukrainian float-glass projects still navigating war-time logistics. The EU’s deposit-return timetable is expected to level regulatory playing fields across Southeastern Europe, compelling neighboring countries to harmonize bottle-design standards. That shift presents Bulgarian lines with an export opportunity, as standardized neck finishes and thread profiles reduce supply-chain friction for converters servicing multiple jurisdictions. However, new capacity announcements, such as NovaSklo’s EUR 240 million (USD 265 million) float-glass plant in Ukraine, inject future competitive pressure that could moderate price-realization in commodity flint after 2028.

Competitive Landscape

The Bulgaria container glass market exhibits moderate concentration, with the top five players holding roughly 65% of installed capacity. BA Glass Bulgaria, Vetropack, and Verallia anchor the leadership tier, each operating high-pull IS machines complemented by on-site decoration. Domestic independents occupy the mid-tier, typically running single-furnace set-ups optimized for niche products or private-label volumes. Rising energy costs and looming EU eco-modulation fees have prompted all operators to pursue thermal efficiency milestones. BA Glass Bulgaria’s photovoltaic investment represents an archetype: it hedges power volatility while generating green-certificate income streams. Vetropack, in contrast, focuses on oxyfuel furnace retrofits that promise up to 20% fuel savings and a 50% reduction in NOₓ emissions.

Technology collaboration is accelerating. In October 2024 Schneider Electric and Saint-Gobain presented a software-defined control stack at Glasstec that marries PLC virtualization with real-time predictive maintenance for lehr conveyors. Bulgarian mid-caps are early adopters because capex is amortized over smaller baseline costs, letting them leapfrog legacy competitors without major greenfield builds. Meanwhile, distribution networks are consolidating: TricorBraun’s acquisition spree in Germany and Austria foreshadows deeper integration of Eastern European warehouses into multi-country just-in-time loops, potentially reshuffling bargaining power between converters and merchants.

Strategic white-space resides in pharmaceutical and premium-spirits sub-sectors where audit barriers and brand equity insulate price points. Operators that secure Type I vial accreditation or invest in frosted-glass decorators can lock in contracts exceeding five years, a rarity in the price-volatile beverage segment. Nonetheless, labor shortages persist and may intensify as Western European wage offers climb. Companies are therefore experimenting with robotics for hot-end gob monitoring and with remote expert-support systems that let senior technicians oversee multiple sites simultaneously, mitigating human-capital risk.

Bulgaria Container Glass Industry Leaders

BA Glass Bulgaria SA

Rubin Trading JSC

Vials.Bg – Melampous Ltd

Glassy Bulgaria

Ecoprint Glass, Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Nikolaus Wiegand assumed full ownership of Wiegand-Glas, signaling succession planning and potential refocus of Central European capacity.

- February 2025: The EU Packaging and Packaging Waste Regulation entered into force, triggering nationwide alignment with recyclability and deposit-return protocols.

- January 2025: Bulgaria’s utility regulator approved a 9% rise in electricity tariffs and nearly 10% in natural-gas prices, prompting glassmakers to accelerate energy-efficiency projects.

- January 2025: TricorBraun announced agreements to acquire Euroglas and Glaspack, extending its reach in Central Europe and creating a denser distribution web that could redirect order flow toward Bulgarian plants.

Bulgaria Container Glass Market Report Scope

Glass Containers refer to clean bottles and jars made from glass. The scope excludes windows and other non-container glass products. Container glass is used in the alcoholic and non-alcoholic beverage industries due to its ability to maintain chemical inertness, sterility, and non-permeability. Glass packaging is valued for its unique properties, including its transparency, inertness, and ability to preserve the quality and integrity of its contents. The Bulgaria glass containers market tracks the shipment volume of different types of glass containers across end-user industries in the market.

Bulgaria Container Glass Market is segmented by end-user vertical (beverages [alcoholic beverages (beer, wine, spirits, and other alcoholic beverages {cider and other fermented drinks}), non-alcoholic beverages (juices, carbonated drinks (CSDs), dairy product-based drinks, other non-alcoholic beverages)], food [jam, jelly, marmalades, honey, sausages and condiments, oil, pickles], cosmetics and personal care, pharmaceuticals (excluding vials and ampoules), and perfumery, and by color (green, amber, flint and other colors). The report offers market forecasts and size in volume (kilotons) for all the above segments.

| Beverages | Alcoholic | Beer |

| Wine | ||

| Spirits | ||

| Other Alcoholic Beverages (Cider and Other Fermented Drinks) | ||

| Non-Alcoholic | Juices | |

| Carbonated Drinks (CSDs) | ||

| Dairy Product Based Drinks | ||

| Other Non-Alcoholic Beverages | ||

| Food (Jam, Jelly, Marmalades, Honey, Sausages and Condiments, Oil, Pickles) | ||

| Cosmetics and Personal Care | ||

| Pharmaceuticals (excluding Vials and Ampoules) | ||

| Perfumery | ||

| Green |

| Amber |

| Flint |

| Other Colors |

| By End-user | Beverages | Alcoholic | Beer |

| Wine | |||

| Spirits | |||

| Other Alcoholic Beverages (Cider and Other Fermented Drinks) | |||

| Non-Alcoholic | Juices | ||

| Carbonated Drinks (CSDs) | |||

| Dairy Product Based Drinks | |||

| Other Non-Alcoholic Beverages | |||

| Food (Jam, Jelly, Marmalades, Honey, Sausages and Condiments, Oil, Pickles) | |||

| Cosmetics and Personal Care | |||

| Pharmaceuticals (excluding Vials and Ampoules) | |||

| Perfumery | |||

| By Color | Green | ||

| Amber | |||

| Flint | |||

| Other Colors | |||

Key Questions Answered in the Report

How large is Bulgaria container glass market demand in 2026?

The Bulgaria container glass market size stands at 614.82 kilotons in 2026 and is projected to grow at a 3.72% CAGR to 2031.

Which end-user segment is growing fastest?

Cosmetics and personal care containers show the quickest climb, advancing at a 4.18% CAGR through 2031.

Why is amber glass gaining popularity among Bulgarian brewers?

Amber blocks about 95% of ultraviolet light, protecting beers from lightstruck off-flavors and aligning with craft breweries’ quality priorities.

How are energy price hikes affecting Bulgarian glassmakers?

A 9% electricity and nearly 10% natural-gas increase in 2025 is pushing manufacturers to invest in photovoltaic, oxyfuel, and waste-heat projects to safeguard margins.

What role do EU deposit-return schemes play in future demand?

Mandatory deposit-return systems by 2029 favor reusable glass, giving Bulgarian plants a structural demand uplift from beverage fillers seeking compliant packaging.

Which companies hold the largest share of Bulgarian output?

BA Glass Bulgaria, Vetropack, and Verallia together account for roughly 55% of fully-finished container glass shipped from Bulgaria.

Page last updated on: