Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

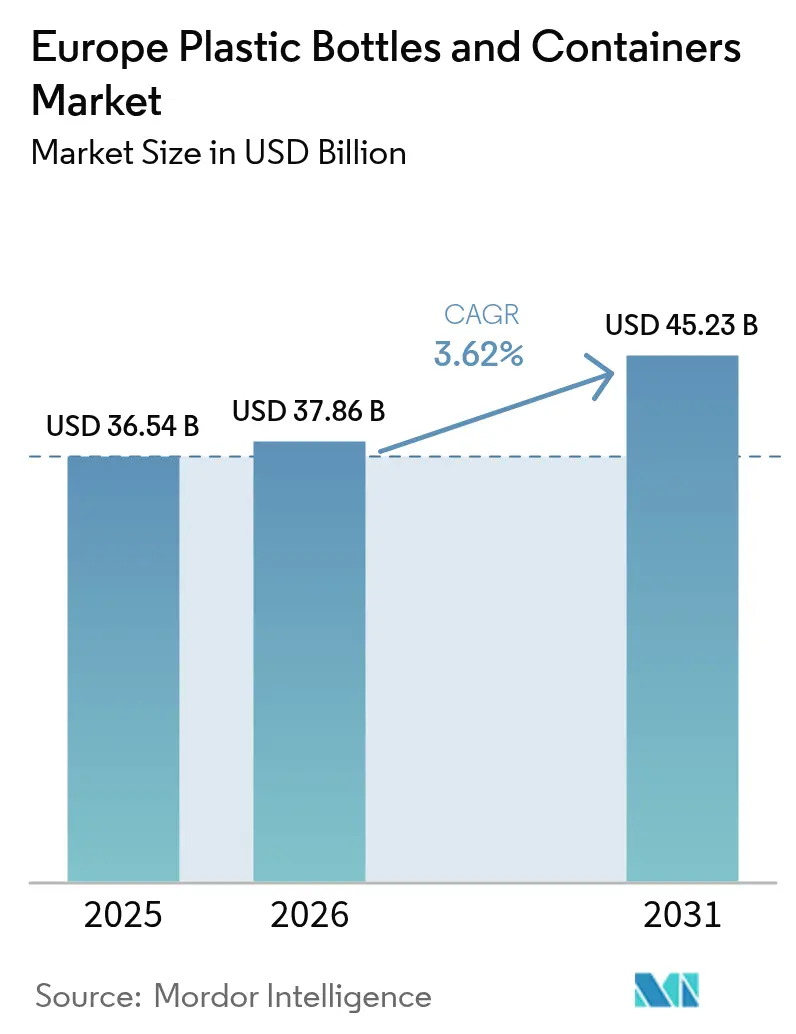

| Base Year Market Size (2025) | USD 36.54 Billion |

| Market Size (2026) | USD 37.86 Billion |

| Market Size (2031) | USD 45.23 Billion |

| Growth Rate (2026 - 2031) | 3.62% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Plastic Bottles And Containers Market Analysis by Mordor Intelligence

The Europe plastic bottles and containers market size is expected to grow from USD 36.54 billion in 2025 to USD 37.86 billion in 2026 and is forecast to reach USD 45.23 billion by 2031 at 3.62% CAGR over 2026-2031. Growth stems less from pure volume expansion and more from regulatory alignment, recycled-content adoption, and pharmaceutical fill-finish capacity additions.[1] European Commission, “Single-Use Plastics,” environment.ec.europa.eu Tightening rules under the Packaging and Packaging Waste Regulation (PPWR) and the Single-Use Plastics Directive are accelerating design for recycling, mono-material conversion, and blended-PCR procurement strategies. On the supply side, integrated resin-to-recycling chains mitigate feedstock volatility, while lightweighting and digital watermarking programs lower logistics outlays and improve downstream sortation yields. M&A momentum, highlighted by Amcor’s 2024 takeover of Berry’s rigid unit, confirms that scale is becoming critical to finance chemical-recycling build-outs and meet recycled-content mandates.

Key Report Takeaways

- By material, PET held 51.04% of the Europe plastic bottles and containers market share in 2025, and bioplastics are forecast to grow at a 4.78% CAGR between 2026-2031.

- By packaging type, bottles accounted for 48.26% of the Europe plastic bottles and containers market size in 2025, and ampoules and vials are projected to register a 4.63% CAGR through 2031.

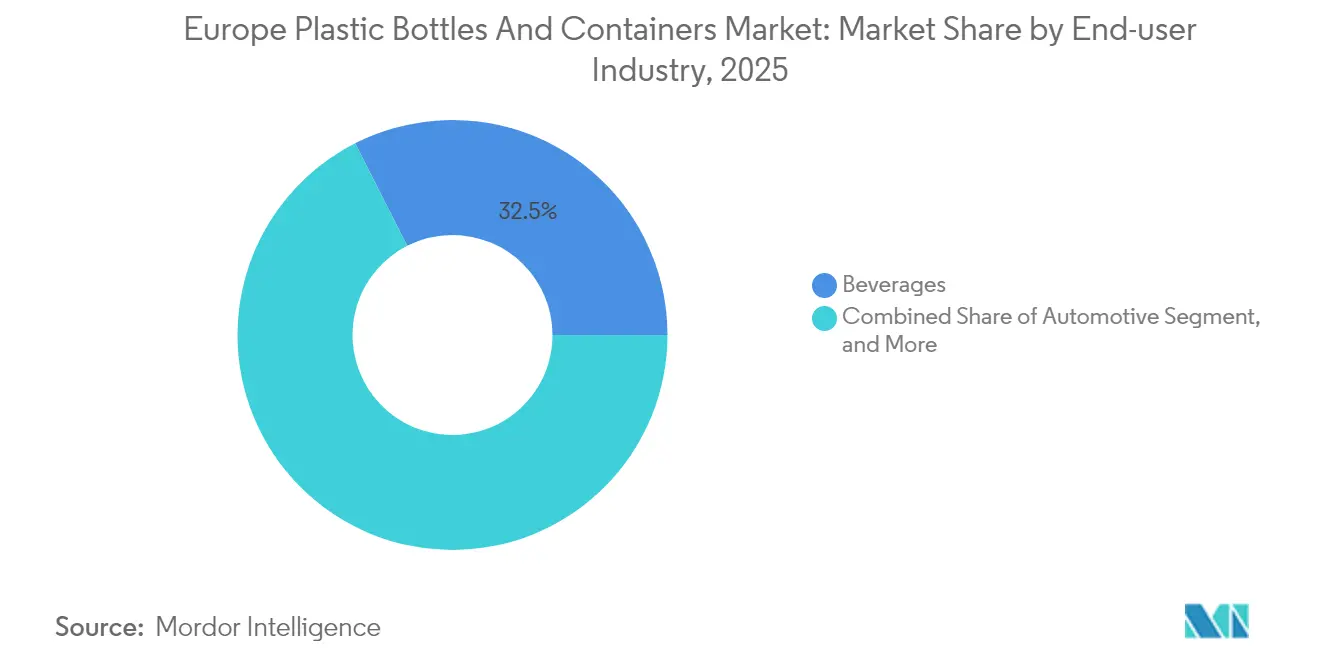

- By end user, beverages controlled 32.48% revenue share in 2025; pharmaceuticals are advancing at a 4.45% CAGR to 2031.

- By manufacturing technology, injection stretch blow molding led with 29.54% share in 2025; injection blow molding shows the fastest 5.05% CAGR outlook.

- By country, the United Kingdom represented 22.46% share in 2025, while Poland is set to expand at a 5.87% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Plastic Bottles And Containers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for bottled water and on-the-go beverages | +0.8% | Global, strongest in Southern Europe | Medium term (2-4 years) |

| E-commerce boosting durable leak-proof packs | +0.6% | Pan-European, urban centers | Short term (≤ 2 years) |

| Lightweighting initiatives to cut logistics cost | +0.4% | EU-wide, logistics hubs | Medium term (2-4 years) |

| Brand shift to mono-material packs for easier recycling | +0.7% | Core EU markets | Long term (≥ 4 years) |

| Surge in chemical-recycling off-take contracts for food-grade PCR | +0.5% | Germany, Netherlands, Belgium | Long term (≥ 4 years) |

| Early adoption of digital watermarking enabling high-speed sorting | +0.3% | Northern Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Bottled Water and On-the-Go Beverages

Southern Europe’s tourism rebound, combined with heightened health awareness, is lifting per-capita bottled-water and functional-drink consumption. Brand owners are responding with barrier-enhanced PET and lightweight closures that preserve carbonation and taste. Nestlé reduced resin use while keeping top-load strength intact, showing that volume growth can coexist with sustainability targets.[2]Nestlé, “Packaging,” nestle.com Sports-nutrition brands are also shifting to ergonomic bottle profiles that support single-hand use during activity, elevating value per pack. As premium waters migrate to recycled-PET, converters with food-grade r-PET lines gain a margin edge, reinforcing material-loop investments across the Europe plastic bottles and containers market.

E-commerce Boosting Durable Leak-proof Packs

Parcel growth is redefining performance thresholds for rigid containers. InPost’s EUR 600 million out-of-home locker rollout triggers packaging demand for formats that can withstand conveyor impacts and temperature swings. Beauty and personal-care players now specify drop-tested, child-resistant closures for direct-to-consumer shipments. Subscription models stimulate refill-ready bottle architectures that balance durability with material minimization. Automated fulfillment favors dimensional standardization, prompting converters to harmonize neck finishes across SKUs. These needs reinforce the pivot of the Europe plastic bottles and containers market toward higher-specification, e-commerce-optimized designs.

Lightweighting Initiatives to Cut Logistics Cost

Resin cost inflation and climate-levy exposure encourage brand owners to slash gram weights. Coca-Cola’s European operations avoided 6,800 tonnes of polymer use annually by refining preform geometry. Graham Packaging’s rib-reinforced gallon jug cut weight by 11% while passing drop-test norms. Process-control upgrades in injection stretch blow molding allow thinner walls without compromising barrier integrity. The cumulative savings flow through lower freight emissions and carbon-tax liabilities, consolidating lightweighting as a structural lever within the Europe plastic bottles and containers market.

Brand Shift to Mono-material Packs for Easier Recycling

EU-mandated recycled-content thresholds push brands to purge multi-layer laminates. L’Oréal is replacing adhesive labels with direct inkjet decoration to keep entire packs in one polymer family. Switchovers demand alternative oxygen-barrier chemistries and UV inks that do not impair food-grade recyclate. Certification to EN 13432 or ISO 14855 guides compostable polymer adoption for select applications. The transition rewards firms owning extrusion-coating or mono-material lidding patents, reinforcing technology investment across the Europe plastic bottles and containers market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating anti-single-use-plastic regulations | -0.9% | EU-wide, strictest in Northern Europe | Short term (≤ 2 years) |

| Feedstock volatility inflating virgin-resin prices | -0.6% | Global, EU manufacturing centers | Medium term (2-4 years) |

| Mandatory recycled-content targets inflating compliance cost | -0.4% | Core EU markets | Medium term (2-4 years) |

| Retailer refill-station pilots cannibalizing single-use volumes | -0.3% | Urban centers, progressive chains | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Escalating Anti-Single-Use-Plastic Regulations

Member-state transposition of the Single-Use Plastics Directive drives rapid design overhauls. Poland set 25% r-PET requirements by 2025 with fines up to PLN 500,000 for non-compliance, pushing converters to certify supply chains quickly. Attached-cap rules effective July 2024 force neck-finish redesigns and new hinge tooling. Extended Producer Responsibility fees, indexed to recyclability scores, alter SKU profitability and favor companies with closed-loop systems. PFAS phase-outs require fresh barrier technologies, lifting R&D spend across the Europe plastic bottles and containers market.

Feedstock Volatility Inflating Virgin-Resin Prices

Disruptions in shipping lanes and petrochemical outages lifted European PET prices above EUR 900 per tonne in 2025. Smaller converters lacking hedging struggle to pass spikes through to customers. Recycled-PET premiums also fluctuate based on collection yields, adding budgeting uncertainty. Energy-intensive operations face exposure to gas-price swings, though some plants receive state aid under energy-cost relief programs, as seen with KGL S.A. in 2024. Volatility steers procurement toward long-term offtake contracts and integrated recycling, shaping risk-management strategies in the Europe plastic bottles and containers market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: PET Retains an Edge as Bioplastics Accelerate

PET captured 51.04% of the Europe plastic bottles and containers market share in 2025 thanks to clarity, gas-barrier performance, and established bottle-to-bottle collection loops. Brand owners continue to specify food-grade r-PET for beverages and oral pharmaceuticals as it enables compliant PCR incorporation at lower risk. High-Density Polyethylene supports agrochemical and personal-care streams that prioritize chemical resistance, while Polypropylene serves hot-fill sauces and sterilized drug-contact formats. Low-Density Polyethylene’s flexible-squeeze properties carve a niche in cosmetic tubes, although low recycling rates restrain its scope.

Bioplastics, while only a single-digit slice of the Europe plastic bottles and containers market, are expanding at a 4.78% CAGR through 2031. Producers such as Greiner Packaging have initiated bio-based PET trials that promise carbon-footprint cuts without compromising supply-chain compatibility. Capacity additions remain modest, keeping price points above petroleum-based resins. Nevertheless, premium cosmetics and functional-beverage lines accept the premium to signal environmental leadership, ensuring that the Europe plastic bottles and containers industry begins accommodating blended bio-content volumes in mainstream production flows.

By Packaging Type: Bottles Dominate while Ampoules Surge

Bottles commanded 48.26% of the Europe plastic bottles and containers market size in 2025, covering everything from 250 milliliter water units to five-liter edible-oil packs. Format standardization allows converters to switch between neck finishes rapidly, supporting cost-effective changeovers. Wall-thickness optimizations and tethered-cap rollouts align bottles with PPWR thresholds, reinforcing their primacy. Jars, canisters, and jerrycans serve viscous foods, powders, and industrial fluids that benefit from wide-mouth or handle-integrated designs, keeping their shares stable.

Ampoules and vials are the fastest-growing packaging type at 4.63% CAGR, riding Europe’s biologics pipeline and aseptic-fill investment wave. SCHOTT Pharma’s snap-on vial platform simplifies closure compatibility, cutting line-setup time for nasal vaccines. Tamper-evidence and data-matrix serialization turn these tiny containers into high-value units demanding precise injection blow molding. This dynamic attracts specialist converters seeking premium margins, sustaining innovation flow in the Europe plastic bottles and containers market.

By End User: Beverages Lead as Pharmaceuticals Outpace

The beverage sector generated 32.48% of 2025 revenue, benefiting from mass-scale production and formidable brand marketing. Deposit-return schemes lift collection rates, enabling closed-loop r-PET usage that satisfies recycled-content quotas economically. Carbonated-soft-drink players pilot attached-cap solutions well ahead of legal deadlines, using early adoption to polish environmental branding.

Pharmaceutical fillers, although smaller in value today, advance at a 4.45% CAGR to 2031. Aging demographics, biologic therapies, and personalized medicines require sterile, traceable, and often small-batch containers. Prefillable syringes and specialty vials generate per-unit values several times higher than beverage bottles, prompting targeted capacity investments across the Europe plastic bottles and containers industry. Food, cosmetics, and household chemicals round out demand with use-case-specific performance criteria that safeguard a broad format portfolio for converters.

By Manufacturing Technology: Injection Stretch Blow Molding Holds the Lead

Injection stretch blow molding (ISBM) generated 29.54% revenue in 2025. Two-stage ISBM lines deliver tight wall-thickness tolerances, essential for lightweighting. In-mold labeling upgrades add brand impact without secondary labeling steps. Extrusion blow molding remains favored for large volumes and handleware where pinch-off strength matters more than optical clarity. Compression blow molding services oval-shaped cosmetics and pharma packs requiring a superior surface finish.

Injection blow molding (IBM) posts the highest 5.05% CAGR, pushed by pharmaceutical orders for dimensionally precise vials. Kautex Maschinenbau’s latest KCC series embraces servo-hydraulics for faster cycle times and energy cuts. Digital twin modeling from IANUS Simulation optimizes parison formation, trimming resin use while hitting rigorous burst-pressure specs. The technology race reinforces capital-intensive barriers to entry, shaping competitive positioning within the Europe plastic bottles and containers market.

Geography Analysis

The United Kingdom leads the Europe plastic bottles and containers market with 22.46% 2025 share, driven by high per-capita beverage consumption, a top-tier pharmaceutical cluster, and dense e-commerce logistics that favor sturdy, parcel-ready formats. Deposit-return incentives elevate r-PET availability, lowering compliance costs for domestic fillers. Meanwhile, e-commerce parcel volumes linked to InPost’s locker expansion create sustained demand for leak-proof bottles and refill pods designed for automated handling.

Germany anchors regional supply chains with world-class resin conversion capacity and engineering firms that pioneer advanced blow-molding lines. Chemical-recycling pilot plants and deposit-system efficiencies raise recycled-content supply, enabling converters to satisfy upcoming PPWR thresholds earlier than peers. Automotive and chemical exporters also demand industrial jerrycans produced to UN hazard-goods specifications, firming baseline volumes.

Emerging Eastern European markets, headed by Poland, absorb manufacturing investments that chase lower labor costs and proximity to growth corridors. Poland’s incentives for energy-intensive industries cushion gas-price shocks, promoting polymer-processing uptime. EU funds finance collection-sorting upgrades that feed local r-PET plants, closing loops within national borders. Italy, France, and Spain rely on agri-food exports, premium wines, and beauty brands to stabilize demand for tailored rigid containers, reinforcing the pan-regional diversity that underpins resilience in the Europe plastic bottles and containers market.

Regulatory Landscape

The EU regulatory framework is tightening around recyclability, recycled content, and reuse for plastic bottles and containers. Regulation (EU) 2025/40, the Packaging and Packaging Waste Regulation (PPWR), entered into force on 11 February 2025 and applies from 12 August 2026, replacing the prior directive-led approach with directly applicable, harmonized requirements across Member States. Under the broader EU plastics regime, Directive (EU) 2019/904 (Single-Use Plastics Directive) sets a 90% separate collection target for single-use plastic beverage bottles by 2029 and establishes minimum recycled-content thresholds for beverage bottles, including 25% recycled PET in PET bottles by 2025 and 30% for all plastic beverage bottles by 2030. This reinforces bottle-to-bottle loop economics.

Implementation is increasingly defined through delegated and implementing acts. In June 2026, the European Commission adopted an implementing decision establishing harmonized rules for calculating, verifying, and reporting recycled plastic content in single-use PET beverage bottles. In May 2026, the Commission adopted a delegated decision exempting certain transport-related items, such as pallet wrappings and straps, from PPWR reuse targets under Article 29, indicating where reuse obligations are being narrowed while recyclability and recycled-content compliance continues to expand for consumer-facing rigid packaging.

Value Chain Analysis

The value chain for plastic bottles and containers in Europe spans petrochemical and bio-based resin producers (PET, HDPE, PP, LDPE, and emerging bioplastics), additive and masterbatch suppliers, preform makers, converters using ISBM/EBM/IBM technologies, and brand owners in beverages, food, pharmaceuticals, personal care, and industrial chemicals. Downstream, distribution runs through retailers and e-commerce platforms, while end-of-life outcomes depend on collection systems, including deposit-return schemes for beverage bottles, sorting facilities, mechanical recyclers producing food-grade r-PET, and a growing chemical recycling ecosystem that supplies circular polymers under mass balance accounting. Compliance documentation and third-party certifications increasingly track with physical material flows to substantiate recycled-content and recyclability claims.

In 2026, supply chain resilience and traceability are central operational levers. Geopolitical disruptions and raw-material availability constraints heightened resin and film price volatility in early 2026, strengthening the case for integrated resin-to-recycling chains and long-term offtake contracts for food-grade PCR. On the regulatory interface, the European Commission adopted Implementing Decision (EU) 2026/1425 in June 2026, establishing harmonized rules for calculating and verifying recycled plastic content for single-use beverage bottles and formalizing reporting approaches, including mass balance provisions relevant to chemical recycling. This accelerates data-sharing requirements between waste management operators, recyclers, and converters, and increases the need for standardized quality, auditing, and chain-of-custody controls across the Europe plastic bottles and containers value chain.

Competitive Landscape

Consolidation advanced markedly when Amcor integrated Berry’s rigid assets, forming the largest global player and capturing broad shelf presence across beverages, pharma, and personal care.[4]Amcor, “Amcor Completes Acquisition of Berry Global’s Global Rigid Packaging Business,” amcor.com Scale enables higher PCR procurement power and financing clout for chemical-recycling plants. ALPLA’s pledge to run 700,000 tonnes of recycling capacity by 2030 signals vertical integration aimed at insulating operations from virgin-resin volatility.

Technology differentiation remains central. Early adopters of HolyGrail 2.0 digital watermarking gain Extended Producer Responsibility fee rebates through demonstrable recyclability, turning what was once a compliance task into a margin lever. ISBM line retrofits with real-time cavity pressure sensors cut scrap rates below 1%, supporting thin-wall conversion economics. Patent filings around parison lubrication and servo-controlled injection sequences amplify barriers to late entrants and keep R&D spend elevated across the Europe plastic bottles and containers market.

Sustainability credentials shape buying decisions. Greiner’s EcoVadis platinum ranking places it in the top 1% of audited suppliers, earning preferential sourcing status among multinationals that scorepack vendors on ESG metrics. SCHOTT Pharma scales prefillable-syringe capacity to ride biologics growth and leverages its glass-polymer hybrid know-how for barrier-critical drug containers. Disruptive entrants are targeting bio-based PET and refill-as-a-service models, but incumbent converters counter through venture capital arms and joint pilot projects, ensuring dynamic yet disciplined competition within the Europe plastic bottles and containers market.

Europe Plastic Bottles And Containers Industry Leaders

Amcor plc

ALPLA Werke Alwin Lehner GmbH & Co KG

Gerresheimer AG

Plastipak Holdings, Inc.

Alpha Packaging, Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

PPWR implementation from 12 August 2026 creates near-term whitespace for packaging formats and materials that can be documented as recyclable, support higher recycled-content inclusion, and meet substance-of-concern constraints with verifiable technical files and EU Declarations of Conformity. The resulting demand is showing up in mono-material bottle-and-closure systems, label and ink choices that preserve recyclate quality, and converter capabilities that maintain performance while increasing PCR use. This is particularly relevant for PET beverage bottles and oral pharmaceutical packs, where compliance risk is higher. The June 2026 European Commission implementing decision on harmonized calculation and reporting of recycled plastic content in single-use PET beverage bottles strengthens the business case for certified, auditable PCR supply and for converters that can offer compliant chain-of-custody documentation end-to-end.

Investment and capability upgrades underpin opportunities across regional capacity additions, compliant r-PET integration, and high-value pharma-grade containers. Amcor announced in January 2026 an EUR 120 million investment to expand PET bottle production capacity in Wroclaw, Poland, adding reported annual output capacity of 40,000 tonnes. This highlights Eastern Europe as a build-and-serve base for pan-European brand owners while aligning production footprints with recycled-content and design-for-recycling needs. In parallel, barrier and protection innovations for sensitive pharmaceutical contents, including upgraded moisture-barrier HDPE systems enabled through partnerships like Gerresheimer and Milliken (LeneX UltraGuard), support a shift toward higher-specification containers where regulatory, stability, and traceability requirements justify premiumization relative to commodity beverage packs.

Recent Industry Developments

- July 2026: Amcor published guidance for beverage producers on closure and packaging considerations tied to EU reuse and PPWR-driven compliance, focusing on design choices that support reusable PET and glass bottle systems. The update reinforces how suppliers are repositioning from single-format packaging toward portfolios that accommodate reuse, refill, and harmonized compliance across European markets.

- June 2026: Gerresheimer reported operational execution challenges and project delays and adjusted its 2026 outlook, according to Reuters. The update pointed to near-term constraints in scaling specialized packaging and device programs, affecting lead times and capacity planning for pharmaceutical customers relying on high-specification container supply.

- April 2026: Gerresheimer announced a partnership with Milliken & Company to integrate LeneX UltraGuard technology into HDPE pharmaceutical packaging, citing up to a 40% improvement in moisture barrier performance. This strengthens the focus on functional additives and barrier technologies that protect sensitive drug products while supporting downgauging and material optimization.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the value of plastic bottles and plastic containers sold in Europe for packaging and storage uses across consumer and industrial applications, reported in USD.

Scope exclusions: Excludes non-plastic packaging formats and excludes caps, closures, labels, and secondary packs when they are sold separately from the bottle or container.

Segmentation Overview

- By Material

- Polyethylene Terephthalate (PET)

- High-Density Polyethylene (HDPE)

- Polypropylene (PP)

- Low-Density Polyethylene (LDPE)

- Bioplastics

- Other Plastics

- By Packaging Type

- Bottles

- Jars and Canisters

- Jerrycans

- Ampoules and Vials

- Other Packaging Types

- By End-user Industry

- Beverages

- Non-Alcoholic Beverages

- Bottled Water

- Carbonated Soft Drinks

- Dairy and Functional Drinks

- Other Non-Alcoholic Beverages

- Alcoholic Beverages

- Non-Alcoholic Beverages

- Food

- Pharmaceuticals

- Cosmetics and Personal Care

- Industrial Chemicals

- Other End-user Industries

- Beverages

- By Manufacturing Technology

- Extrusion Blow Moulding

- Injection Stretch Blow Moulding

- Injection Blow Moulding

- Compression Blow Moulding

- Other Manufacturing Technologies

- By Country

- United Kingdom

- Germany

- Italy

- France

- Spain

- Poland

- Rest of Europe

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started with public packaging and plastics data to set the demand context and the rulebook for what should be counted. We leaned on sources such as Eurostat (production and trade series), the European Commission policy pages on packaging waste and recycled-content targets, national statistical offices in key European economies, and patent databases for packaging material and recycling-related filings.

After that, sizing inputs were shaped using company annual reports and investor decks for packaging suppliers and resin producers, alongside trade association publications and reputable press that track packaging format shifts. In a few cases, paid subscriptions for company financials and news intelligence were used to cross-check revenue direction and expansion timelines. These desk sources are illustrative, and we also used other public references for data collection, validation, and research clarification.

Primary Interviews and Surveys

Primary interviews and surveys were used to pressure-test what we saw in desk research, especially around pricing pass-through, recycled-content adoption, and substitution between bottles, jars, canisters, and other rigid formats. We spoke with a mix of packaging producers, resin and recycled resin participants, converters, and large end users in food, beverage, pharma, and home care across Europe, so assumptions could be corrected where buying behavior diverged from public indicators.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 31% | CXOs: 12% | |

| Mid tier: 53% | Functional/Unit leaders: 37% | |

| Smaller Players: 16% | Managers: 51% |

Market-Sizing & Forecasting

The core model uses a top-down approach where packaging demand is reconstructed from end-use output and packaging intensity, then translated into value using observed price levels by resin and format. To avoid relying on a single data series, we corroborate results with selective bottom-up approximations, such as sampled supplier revenue splits, capacity signals from expansion announcements, and spot checks of volume times average selling price for common bottle and container types.

Inputs tracked (illustrative) include resin price trends for PET, PE, and PP, recycled-content targets and collection progress, beverage and packaged food production indicators, pharma packaging demand signals, and country-level trade flows for plastic packaging articles. Forecasts were built using scenario analysis, where regulatory timing, recycled resin availability, and price pass-through were flexed, then aligned to what interviewees expect by country group. Where bottom-up checks had missing coverage for smaller formats, we used ratio-based scaling based on end-use mix and consistent price bands, before normalizing totals back to the demand pool.

Data Validation & Update Cycle

Outputs are checked against independent signals like resin spreads, conversion margins, and trade balances, so the growth path stays realistic by country group and by format. If a variance looks too high, we revisit the driver inputs, re-check unit economics, and re-contact experts when the mismatch cannot be explained by seasonality or one-off inventory moves.

A multi-step analyst review is followed before sign-off, including consistency checks on units, currency timing, and implied volumes. Reports are refreshed annually, and interim updates are done when material events occur, such as major regulation changes or sharp resin price swings. Right before delivery, we complete a final review pass so the latest updated view is reflected in the output.

Mordor Intelligence's Europe Plastic Bottles Containers Market Estimate Compared With Other Published Estimates

Published estimates for this market often differ because the product set is not uniform, and because pricing is treated differently across bottles, jars, and other rigid packs. Timing can also shift results since resin-linked pricing moves quickly, and some studies lock currency conversion to a different month or year.

Key gaps usually come from what gets counted as a bottle or container, whether packaging used in pharma and personal care is included at the same value point as food and beverage, and how recycled-content related costs are assumed to flow into average selling prices.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 36.54 B (2025) | |

| Trade Journal B | USD 19.80 B (2024) | Uses a plastic container definition aligned to a specific statistical product code and reports nominal wholesale prices, which can exclude several bottle-led and higher specification applications that are captured when conversion value across end uses is counted. |

| Regional Consultancy A | USD 35.18 B (2024) | Often anchors the starting year differently and may apply blended average prices without separating resin-linked price movement by format and end use, which can shift the reported level even if the direction is similar. |

The table highlights scope and value-point differences as the main drivers of the spread. In Mordor Intelligence's model, the market includes plastic bottles plus a wider set of rigid container forms across food, beverage, pharma, and home care, and resin-specific pricing pass-through is refreshed as conditions change. With these rules stated clearly, the final number is easier to trace back to demand indicators and repeatable checks rather than a single headline assumption.

Key Questions Answered in the Report

How large is the Europe plastic bottles and containers market in 2026?

The market stands at USD 37.86 billion in 2026 and is projected to rise to USD 45.23 billion by 2031.

Which material leads rigid-pack demand across Europe?

PET dominates with 51.04% 2025 share due to clarity, barrier performance, and mature bottle-to-bottle loops.

Which segment is growing fastest within rigid containers?

Pharmaceutical ampoules and vials are expanding at a 4.63% CAGR through 2031, fueled by biologics and personalized medicine.

How are EU regulations affecting packaging design?

The PPWR and Single-Use Plastics Directive push brands toward mono-material packs with 25-30% PCR, driving redesign and recycled-feedstock investments.

What role does Poland play in regional growth?

Poland is the fastest-expanding national market with a 5.87% CAGR, buoyed by EU funding, manufacturing grants, and rising domestic consumption.

Page last updated on: