Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

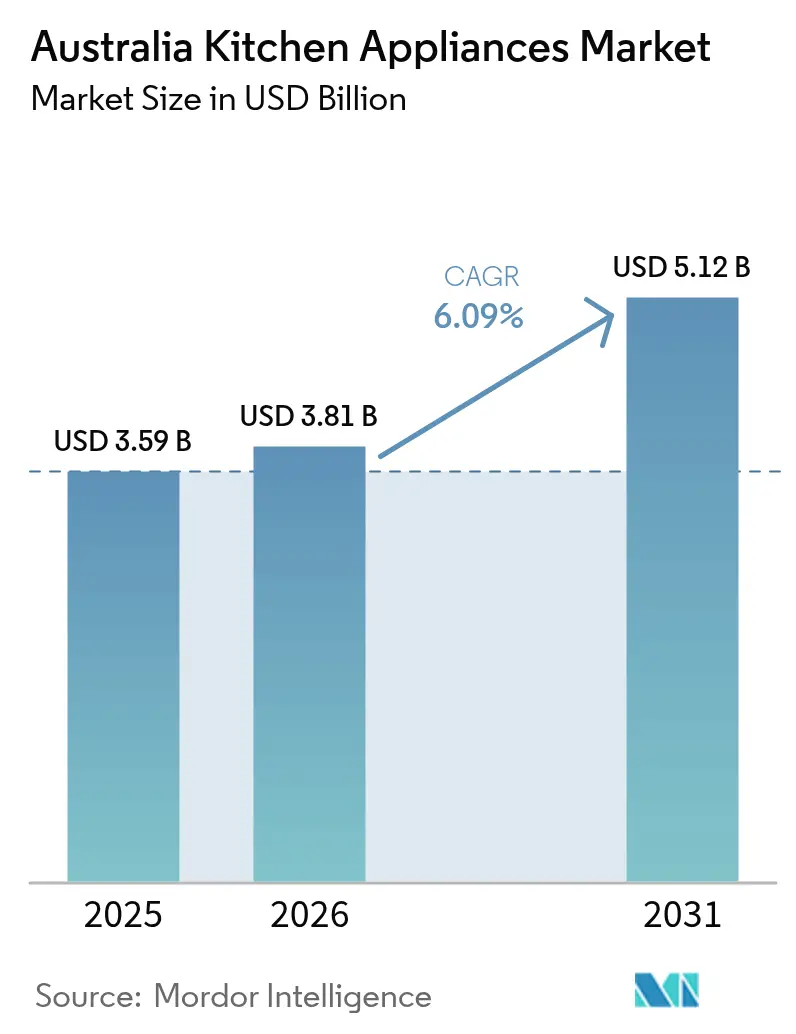

| Base Year Market Size (2025) | USD 3.59 Billion |

| Market Size (2026) | USD 3.81 Billion |

| Market Size (2031) | USD 5.12 Billion |

| Growth Rate (2026 - 2031) | 6.09% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Australia Kitchen Appliances Market Analysis by Mordor Intelligence

The Australia Kitchen Appliances market size is expected to grow from USD 3.59 billion in 2025 to USD 3.81 billion in 2026 and is forecast to reach USD 5.12 billion by 2031 at 6.09% CAGR over 2026-2031. Growth momentum stems from electrification mandates, renovation-driven replacement cycles, and wider uptake of smart-home ecosystems that encourage premium appliance upgrades. State rebate schemes create immediate price parity between standard and energy-efficient models, while Buy Now Pay Later (BNPL) services lift ticket sizes and reduce friction for large online purchases. Logistics bottlenecks and higher compliance costs under Australia’s Circular Economy Framework pressure margins yet nudge brands toward local assembly and design-for-recycling programs that resonate with sustainability-focused consumers. Manufacturers able to integrate AI, energy management, and open-standards connectivity capture disproportionate value as households and hospitality venues future-proof kitchens for cost-of-living and climate resilience.

Key Report Takeaways

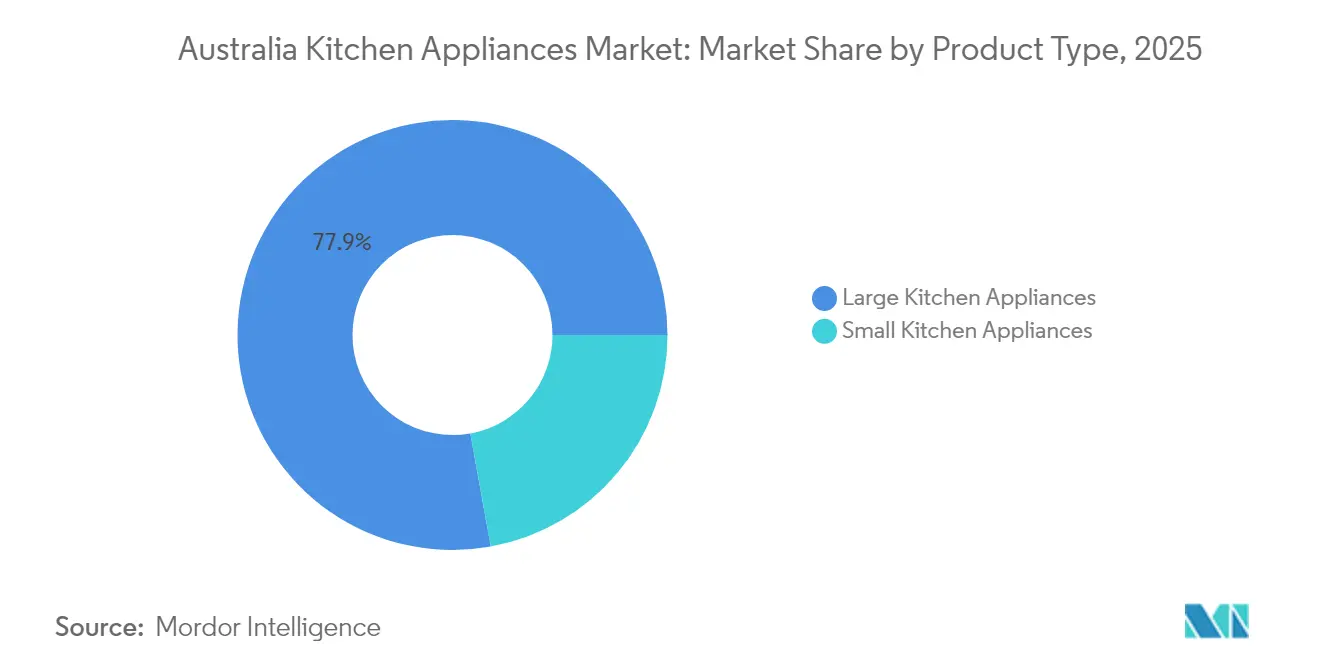

- By product type, large kitchen appliances led with 77.85% revenue share in 2025; small appliances are projected to expand at a 6.61% CAGR through 2031.

- By end user, the residential segment held 72.75% of the Australia Kitchen Appliances market share in 2025, while the commercial segment is advancing at a 5.28% CAGR to 2031.

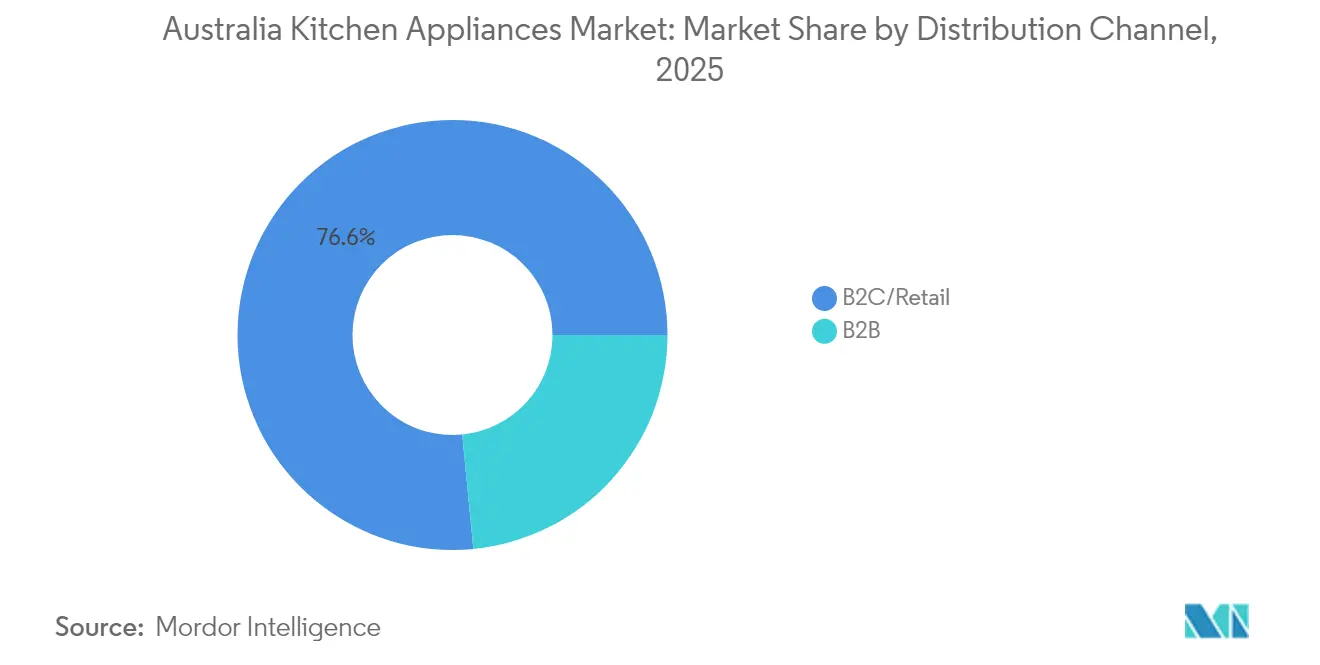

- By distribution channel, B2C/retail controlled 76.55% revenue share in 2025, and the online sub-channel is expected to post a 7.42% CAGR during 2026-2031.

- By geography, New South Wales accounted for 31.05% of 2025 sales; Queensland is forecast to grow the fastest at 6.88% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Australia Kitchen Appliances Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Energy-efficient appliance rebates & minimum-star upgrades | +1.2% | National, with strongest uptake in Victoria, Queensland, South Australia | Short term (≤ 2 years) |

| Rapid post-pandemic renovation boom in detached housing | +1.8% | National, concentrated in NSW coastal areas, Victoria inner-city regions | Medium term (2-4 years) |

| Hospitality sector's premiumisation of back-of-house kitchens | +0.7% | National, with premium growth in Sydney, Melbourne, Brisbane CBDs | Medium term (2-4 years) |

| Surge in BNPL adoption lifting ticket sizes for big-ticket whitegoods | +1.1% | National, with higher penetration in urban centers | Short term (≤ 2 years) |

| Electrification incentives replacing gas cooktops in new builds | +0.9% | Victoria, with spillover to ACT and Tasmania | Long term (≥ 4 years) |

| Edge-AI food-recognition modules enabling automated cooking | +0.5% | National, early adoption in high-income metropolitan areas | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Energy-Efficient Appliance Rebates Drive Premium Segment Adoption

Government support programs such as Queensland’s Climate Smart Energy Savers and Victoria’s Energy Upgrades lower upfront costs and encourage households to select higher-star models that deliver ongoing energy savings[1]Source: Queensland Government, “Climate Smart Energy Savers Scheme Update 2025,” qld.gov.au. Minimum performance thresholds under the Greenhouse and Energy Minimum Standards Act filter out inefficient stock, pushing brands toward smart induction cooktops, inverter refrigerators, and connected dishwashers that qualify for rebates[2]Source: Victorian Energy Upgrades, “Household Rebate Schedule 2025,” energysaver.vic.gov.au. Retailers report rising attachment rates for Wi-Fi-enabled models because connected dashboards help consumers monitor usage and validate rebate applications. Manufacturers with in-house R&D and local compliance teams gain a head start in certifying new SKUs, capturing an outsized share of the Australian kitchen Appliances market. Rapid rebate uptake compresses payback periods to less than two years for many high-efficiency products, reinforcing the premiumization flywheel.

Post-Pandemic Renovation Boom Sustains Appliance Replacement Cycles

Renovation spending rose to 40% of residential construction value in 2023-24, shifting capital from new builds to kitchen refresh projects that normally involve a full appliance suite upgrade. Homeowners leverage prolonged work-from-home periods and equity gains to finance upscale cooktops, ovens, and French-door refrigerators. Victoria’s one-for-one replacement rate of 12.6% of new-build spend underscores how legacy housing stock spurs structural demand for electrified appliances compatible with induction-ready cabinetry. Renovation projects often bundle flooring, benchtops, and appliances, raising average transaction values at specialty retailers. The surge in detached-home makeovers also supports the growth of installation and haul-away services, cementing sticky relationships between brands, trade contractors, and end users.

Hospitality Premiumisation Elevates Commercial Kitchen Standards

Restaurants aim to cut labor costs up to 25% by 2026 through robotics, AI scheduling, and sensor-equipped combi ovens that auto-calibrate recipes. Consumer preference for locally sourced menus (78%) drives demand for precision storage and preparation equipment that preserves provenance and reduces spoilage. Plant-based experimentation nearing USD 9 billion by 2030 requires multi-mode cookers able to handle alternative proteins. QR-code ordering adopted by two-thirds of casual venues pushes kitchens to integrate software-defined appliances for real-time inventory sync. Food-waste reduction goals influence purchasing toward vacuum sealers and blast chillers that extend shelf life. Suppliers delivering modular, energy-efficient, and IoT-ready gear secure premium contracts and long-term maintenance revenue across major CBDs.

BNPL Integration Transforms Large-Appliance Purchase Behavior

BNPL accounted for 40% of consumer payments by value in 2024, turning deferred payments into a mainstream financing method for USD 1,000-plus refrigerators, ranges, and dishwashers. No-surcharge rules mean retailers absorb fees but recoup value through higher cart sizes and lower abandonment rates. Online appliance turnover reached USD 4.52 billion in March 2025—11.6% of total retail—highlighting BNPL’s direct link to e-commerce gains[3]Source: Australian Bureau of Statistics, “Online Retail Sales March 2025,” abs.gov.au. As PayTo rails mature, merchants anticipate lower transaction costs that further widen BNPL’s appeal. Brands run exclusive web promotions featuring six- or twelve-month interest-free plans, steering price-sensitive households toward mid and premium tiers of the Australia Kitchen Appliances market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mortgage stress squeezing discretionary household spend | -1.4% | National, with acute pressure in Sydney, Melbourne high-mortgage areas | Short term (≤ 2 years) |

| Persistent logistics bottlenecks at Port Botany/Port of Melbourne | -0.8% | National, with direct impact on NSW, Victoria distribution networks | Medium term (2-4 years) |

| Fragmented smart-home standards delaying connected upgrades | -0.6% | National, with higher impact in tech-savvy urban centers | Medium term (2-4 years) |

| Rising e-waste regulation costs for OEM product stewardship | -0.4% | National, with compliance costs affecting all manufacturers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Mortgage Stress Constrains Premium Appliance Adoption

Real disposable income fell 5.5% since early 2022, forcing many borrowers to divert cash toward mortgage payments and away from non-essential kitchen upgrades. Credit-card balances climb while savings buffers thin, prompting middle-income families to down-trade or delay replacements. Retailers adapt by stocking entry-series ranges and coupling BNPL deals with extended warranties to preserve volume. High-income segments remain resilient, but reliance on affluent pockets elevates competitive intensity among premium brands. Commercial buyers also show caution as hospitality foot traffic normalizes slower than projected, trimming capital budgets for back-of-house tech.

Supply Chain Bottlenecks Increase Operational Costs

Industrial action at major ports disrupted roughly 20% of scheduled appliance imports during 2024, leading to container dwell times that topped nine days and spot-rate surcharges near 20%[4]Source: APPLiA, “European Competitiveness Fund Position Paper,” applia-home.org. Harvey Norman and other retailers reported stock-outs on refrigerators and dishwashers, prompting emergency airfreight at triple the cost per unit. Brands raised safety stock and sourced alternate regional warehouses, inflating working capital requirements. Ocean relapse risks remain as Houthi-related shipping diversions and Panama Canal drought constraints converge with domestic labor disputes. Higher landed costs may flow through to shelf prices, potentially tempering volumes in the Australia Kitchen Appliances market during peak promotional windows.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Electrification Lifts Large-Appliance Outlays

Large kitchen appliances contributed 77.85% of 2025 sales, underscoring their primacy in meeting Victoria’s all-electric new-home mandate and rebate-fueled replacement cycles. Refrigerators and freezers top the list thanks to energy-label updates that encourage inverter compressors and adaptive defrost. Induction cooktops post double-digit unit growth as households remove gas lines and pocket annual savings of USD 350-400 on connection charges. Smart ovens add steam-assist and camera guidance, expanding average selling prices and aligning with demand-response programs. Dishwashers benefit from water-rating thresholds, and range hoods gain relevance by optimizing ventilation in sealed all-electric builds.

Small kitchen appliances, while holding only 22.15% share, are forecast to expand at 6.61% CAGR as urban consumers embrace air fryers, barista-grade coffee machines, and multifunctional food processors. Countertop ovens address compact living trends and supplement larger ranges in high-value homes. AI-enabled blenders and juicers pivot toward plant-based dieting, while connected kettles sync with energy-tariff apps to time boils during off-peak windows. Low-price elasticity and gift-season spikes underpin consistent sell-through for toasters and rice cookers, rounding out basket size and frequency for retailers.

By End User: Residential Spend Dominates, Commercial Uptick Accelerates

Residential buyers accounted for 72.75% of the Australia Kitchen Appliances market in 2025, propelled by renovation-intensive suburbs and rebate-linked electrification. BNPL removes friction for middle-tier households aiming for premium refrigerator French doors or double-drawer dishwashers, while loyalty apps boost repeat purchases of small appliances. Connectivity features carry weight as families seek centralized dashboards that track energy budgets and grocery inventories. Aging housing stock guarantees a steady pipeline of replacements, cushioning sales against the volatility of new-build activity.

Commercial kitchens, though smaller in absolute value, will log a 5.28% CAGR through 2031 as restaurants deploy smart combi ovens, blast chillers, and AI fryers to offset wage pressures. Demand centers on Sydney, Melbourne, and Brisbane CBD precincts, where footfall recovers and menu innovation intensifies competition. Compliance imperatives—from food-waste cuts to volatile energy tariffs—prompt operators to specify equipment with IoT analytics and remote diagnostics. Vendors offering lifecycle maintenance bundles and financing gain share, ensuring penetration across independent cafés as well as multi-site chains.

By Distribution Channel: Digital Gains Within Omnichannel Portfolios

B2C/retail outlets claimed 76.55% sales in 2025, with store formats ranging from destination big-box to boutique showrooms offering design consults. The online slice, currently at 11.6% of retail appliance turnover, is projected to rise fastest at 7.42% CAGR, driven by mobile-first comparison shopping and home delivery convenience. BNPL check-outs spike during Black Friday and EOFY events, pushing average order values beyond USD 1,500 without traditional credit. Brick-and-click models flourish as consumers research online and finalize in-store, where installation and haul-away services are bundled. Exclusive brand outlets lean into immersive experiences—such as live cooking demos—to upsell connected ecosystems.

B2B direct-from-manufacturer sales serve hospitality, property developers, and institutional buyers demanding volume pricing and spec customization. Integrated financing, extended warranty, and software-as-a-service dashboards sway purchasing committees, especially for energy-intensive refrigeration and combi-ovens. Channel partners that offer predictive-maintenance APIs tie equipment lifecycles to cloud analytics, locking in multiyear service revenue and enhancing brand stickiness across the Australia Kitchen Appliances market.

Geography Analysis

New South Wales retained 31.05% share in 2025 on the back of high disposable incomes, dense hospitality clusters, and a mature housing base that cycles through replacements every seven to nine years. Sydney’s renovation surge in coastal suburbs sustains premium cooker and range-hood demand, while the Energy Savings Scheme nudges households toward high-star refrigerators. Mortgage stress, however, tempers mid-market growth, compelling retailers to tailor assortments for entry segments. Port Botany congestion introduces supply risk; brands offset by pooling inventory in western Sydney logistics hubs.

Victoria anchors demand for induction cooktops, heat-pump dryers, and inverter fridges as electrification deadlines loom for new dwellings. The state’s rebate of up to USD 140 on eligible cooktops accelerates switch-outs, promoting price parity with gas alternatives. Melbourne’s café culture fuels commercial coffee-machine upgrades, and local manufacturing incentives under the Industry Diversification Program spark capacity investments that may cut lead times and landing costs for the Australia Kitchen Appliances market. One-for-one renovation replacement intensity creates visibility for appliance pipeline orders beyond 2027.

Queensland is set to log the fastest 6.88% CAGR through 2031, supported by population inflows and green-energy rebates that have already funded 72,700 household upgrades. Tourism rebound bolsters kitchen retrofits across resorts and restaurants, driving demand for marine-grade refrigerators and high-capacity dishwashers. PeakSmart incentives illustrate how broader home-energy programs pull through kitchen appliance categories, especially when paired with smart-meter tariffs. Regional dispersion challenges logistics, prompting drop-ship partnerships with third-party carriers. Western Australia, South Australia, Tasmania, and the ACT-NT cluster collectively form a steady but smaller revenue pool. Mining communities and remote catering sites specify ruggedized cold-chain units, while South Australia’s wine industry leverages temperature-controlled storage. Tasmania’s no-interest loan scheme expands access to high-efficiency models for lower-income households, widening the funnel for brands mastering service coverage beyond mainland metros.

Competitive Landscape

The Australia Kitchen Appliances industry features a moderately fragmented structure where the top brands account for an estimated majority of the combined revenue, leaving room for challenger entries and niche specialists. Samsung spearheads AI-driven launches such as the 2025 Bespoke line, embedding food-recognition cameras and adaptive defrost to synchronize with SmartThings energy dashboards. LG and Electrolux cooperate within the Home Connectivity Alliance to align on Energy Management Interface protocols that adjust appliance loads during peak pricing windows. Haier leverages Fisher & Paykel’s design equity to court premium renovators through integrated refrigeration walls.

Local assembly gains currency as Electrolux breaks ground at Port of Brisbane, aiming to cut shipping lead times and buffer against port disruption risk. Breville’s expansion into Asia underlines a diversification play that frees capacity for domestic coffee-machine innovation. Mid-tier brands uplift value via extended warranties and cashback bundles aligned with state rebates. Edge-AI module suppliers partner with OEMs to incorporate image classification chips at incremental bill-of-materials cost yet meaningful ASP uplift.

Emergent direct-to-consumer labels court Gen-Z buyers online with transparent pricing, carbon-neutral shipping, and modular repair kits. However, scale economics and after-sales requirements erect barriers to rapid share capture. The Australia Kitchen Appliances market thus rewards incumbents skilled at blending omnichannel reach with iterative software updates that enhance existing hardware, prolonging product relevance and customer lifetime value.

Australia Kitchen Appliances Industry Leaders

Samsung Electronics

Electrolux

LG Electronics

Haier Group

Breville Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Samsung unveiled the Bespoke AI Home Appliances range in Australia, featuring 400 W cordless vacuums and smart-screen refrigerators linked to Knox-secured SmartThings hubs.

- March 2025: Electrolux commenced construction of a manufacturing facility at Port of Brisbane to boost local production capacity.

- February 2025: Breville announced plans to scale its Oracle coffee-machine franchise across Asia and the Middle East after doubling global sales in five years.

- September 2024: Electrolux launched a connected laundry series at IFA 2024, extending its IoT ecosystem beyond the kitchen.

Australia Kitchen Appliances Market Report Scope

Kitchen appliances, such as refrigerators, stoves, dishwashers, washing machines, tumble dryers, and microwave ovens, are generally found in consumers' kitchens. A complete background analysis of the Australian kitchen appliances market, which includes an assessment of the economy, market overview, market size estimation for key segments, emerging trends in the market, market dynamics, vital competitive profiles, and the impact of COVID-19, are covered in the report. Large kitchen appliances, small kitchen appliances, end users, and distribution channels segment the market. By large kitchen appliances, the market is segmented into refrigerators and freezers, ovens, dishwashers, and other large kitchen appliances. By small kitchen appliances, the market is segmented into food processors, mixers and grinders, grills and toasters, coffee/tea makers, cookers, and other small kitchen appliances (bread makers, air fryers, etc.). By end user, the market is segmented into residential and commercial. By distribution channel, the market is segmented into multi-brand stores, exclusive stores, online channels, and other distribution channels. The market size is provided in terms of value (USD) during the forecast period for all the above segments.

By Product

| Large Kitchen Appliances | Refrigerators & Freezers |

| Dishwashers | |

| Range Hoods | |

| Cooktops | |

| Ovens | |

| Other Large Kitchen Appliances | |

| Small Kitchen Appliances | Food Processors |

| Juicers and Blenders | |

| Grills and Roasters | |

| Air Fryers | |

| Coffee Makers | |

| Electric Cookers | |

| Toasters | |

| Electric Kettles | |

| Countertop Ovens | |

| Other Small Kitchen Appliances |

By End User

| Residential |

| Commercial |

By Distribution Channel

| B2C/Retail | Multi-brand Stores |

| Exclusive Brand Outlets | |

| Online | |

| Other Distribution Channels | |

| B2B (directly from the manufacturers) |

By Geography

| New South Wales |

| Victoria |

| Queensland |

| Western Australia |

| South Australia |

| Tasmania |

| Australian Capital Territory & Northern Territory |

| By Product | Large Kitchen Appliances | Refrigerators & Freezers |

| Dishwashers | ||

| Range Hoods | ||

| Cooktops | ||

| Ovens | ||

| Other Large Kitchen Appliances | ||

| Small Kitchen Appliances | Food Processors | |

| Juicers and Blenders | ||

| Grills and Roasters | ||

| Air Fryers | ||

| Coffee Makers | ||

| Electric Cookers | ||

| Toasters | ||

| Electric Kettles | ||

| Countertop Ovens | ||

| Other Small Kitchen Appliances | ||

| By End User | Residential | |

| Commercial | ||

| By Distribution Channel | B2C/Retail | Multi-brand Stores |

| Exclusive Brand Outlets | ||

| Online | ||

| Other Distribution Channels | ||

| B2B (directly from the manufacturers) | ||

| By Geography | New South Wales | |

| Victoria | ||

| Queensland | ||

| Western Australia | ||

| South Australia | ||

| Tasmania | ||

| Australian Capital Territory & Northern Territory | ||

Key Questions Answered in the Report

What is the current value of the Australia Kitchen Appliances market?

It was valued at USD 3.81 billion in 2026 and is projected to reach USD 5.12 billion by 2031 at a 6.09% CAGR.

Which product category generates the most revenue?

Large kitchen appliances contributed 77.85% of 2025 sales, reflecting electrification mandates and rebate incentives.

Which state shows the fastest growth?

Queensland is forecast to grow at a 6.88% CAGR through 2031 due to population gains and household rebate programs.

How important are online channels?

Online sales represented 11.6% of appliance turnover in March 2025 and are expected to rise fastest at 7.42% CAGR.

What role does BNPL play in appliance purchases?

BNPL accounted for 40% of consumer payment value in 2024, lifting average order sizes for high-ticket refrigerators, ovens, and dishwashers.

Page last updated on: