Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

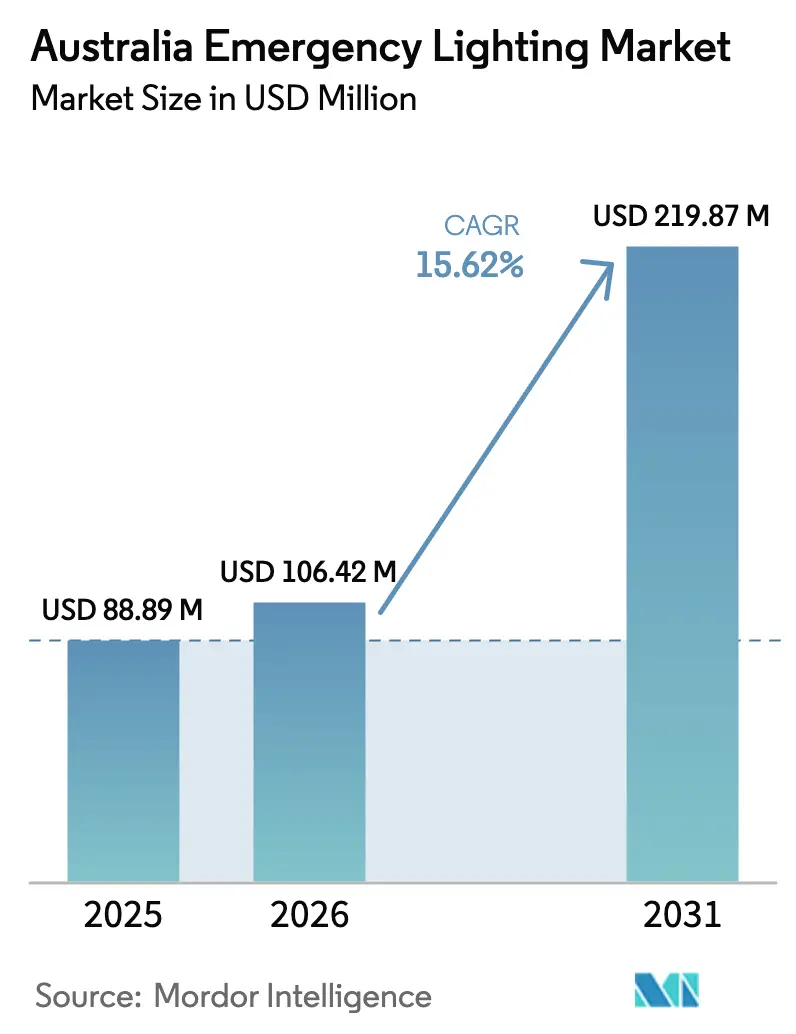

| Base Year Market Size (2025) | USD 88.89 Million |

| Market Size (2026) | USD 106.42 Million |

| Market Size (2031) | USD 219.87 Million |

| Growth Rate (2026 - 2031) | 15.62% CAGR |

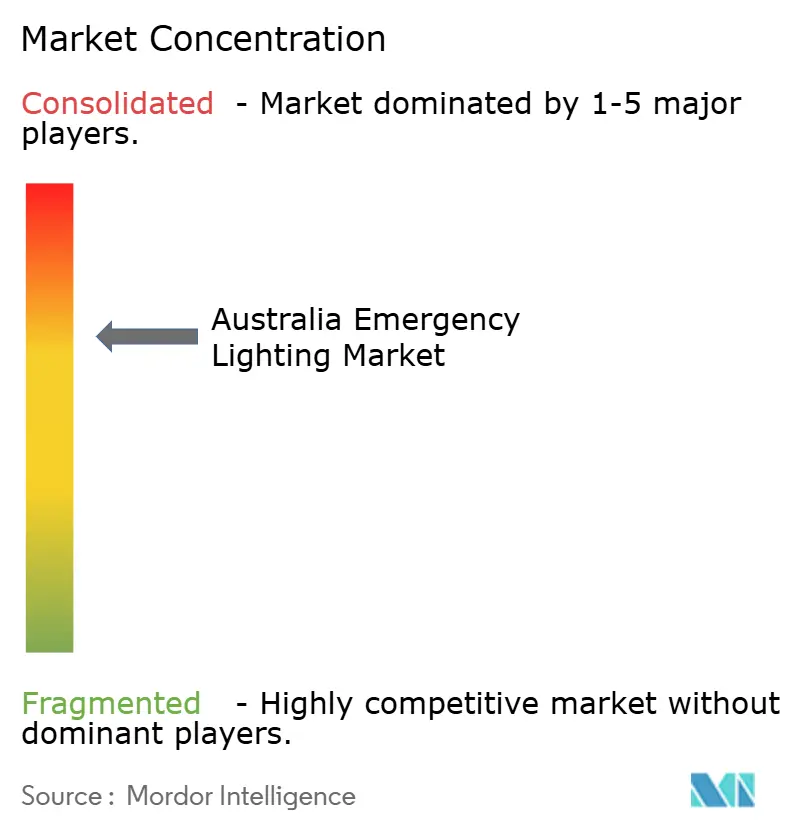

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Australia Emergency Lighting Market Analysis by Mordor Intelligence

The Australia emergency lighting market size is projected to be USD 88.89 million in 2025, USD 106.42 million in 2026, and reach USD 219.87 million by 2031, growing at a CAGR of 15.62% from 2026 to 2031. A construction pipeline topping USD 77 billion, sweeping changes to AS/NZS 2293 and National Construction Code Part E4, and the 2025 phase-out of legacy lamps together underpin robust demand for compliant, energy-efficient systems. The Australia emergency lighting market is also benefiting from sustained retrofits in hospitals and build-to-rent towers, where operators view modern luminaires as low-risk ways to lift sustainability ratings and lower power bills. Competitive intensity has increased as global brands embed cloud dashboards and mesh networks into hardware, allowing them to defend share against price-driven importers. Meanwhile, lithium-iron phosphate batteries and IoT-enabled self-testing are becoming the default specifications in new tenders, reducing lifecycle costs and supporting the momentum of the Australian emergency lighting market.

Key Report Takeaways

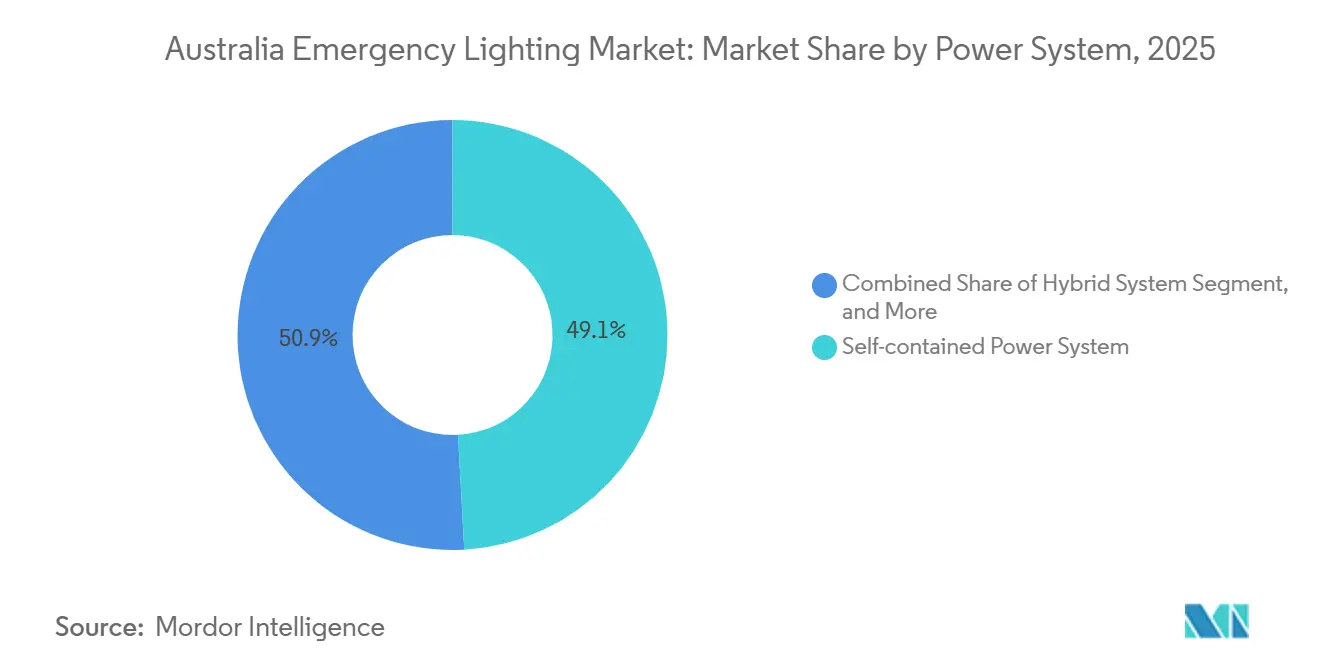

- By power system, self-contained luminaires led with 49.13% revenue share in 2025, while hybrid systems are projected to expand at a 16.22% CAGR through 2031.

- By 2025, LED products captured 79.26% of the Australia emergency lighting market share and are predicted to grow at a 16.29% CAGR through 2031.

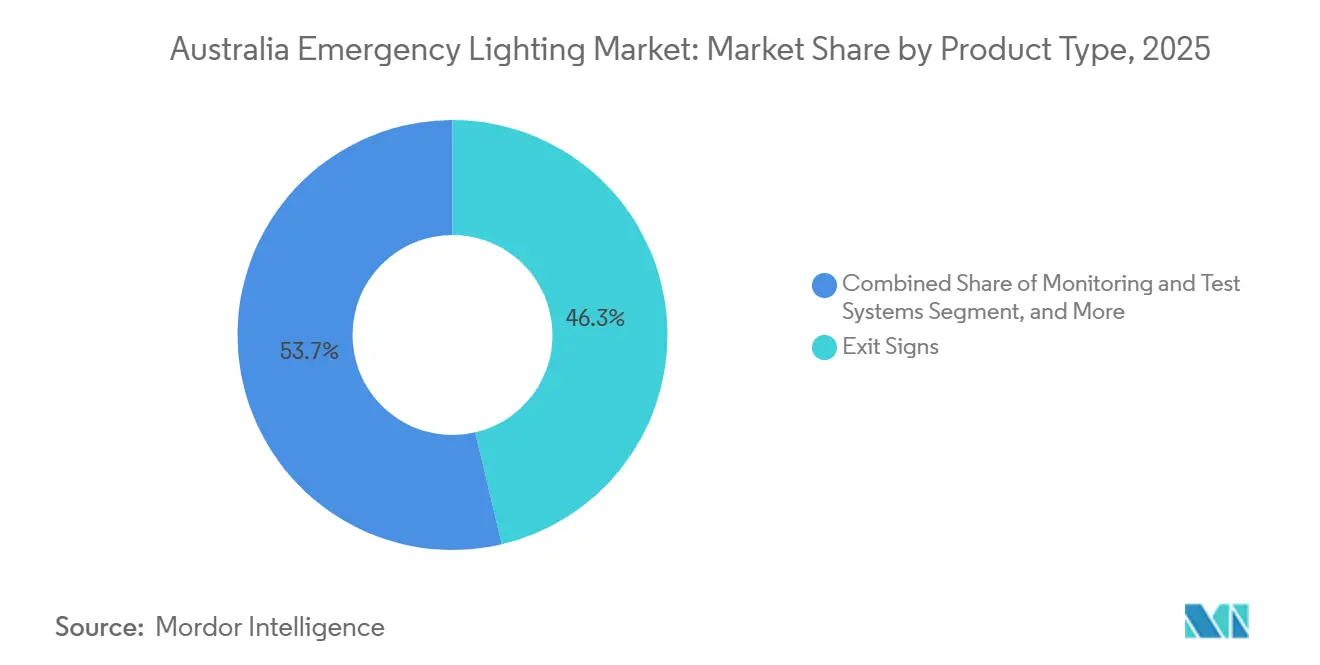

- By product type, exit signs accounted for 46.33% of the Australia emergency lighting market size in 2025, and monitoring and test systems are advancing at a 16.34% CAGR through 2031.

- By end-user vertical, commercial buildings accounted for 42.91% of demand in 2025, whereas public infrastructure and institutional projects recorded the fastest expansion at a 16.56% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Australia Emergency Lighting Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent updates to AS/NZS 2293 and NCC E4 boosting compliance spending | +3.2% | National, with early gains in Sydney, Melbourne, Brisbane | Medium term (2-4 years) |

| Rising commercial construction and retrofit activity in urban centers | +2.8% | New South Wales, Victoria, Queensland | Short term (≤ 2 years) |

| Accelerated LED adoption driven by energy-efficiency mandates | +2.6% | National | Short term (≤ 2 years) |

| Emergence of IoT-enabled self-testing emergency luminaires in remote facilities | +2.1% | National, with concentration in multi-site commercial and industrial operators | Medium term (2-4 years) |

| Shift toward lithium-iron phosphate batteries to address high-ambient temperatures | +1.9% | National, particularly Northern Territory, Queensland, Western Australia | Medium term (2-4 years) |

| Public scrutiny of photoluminescent exit signs prompting electric sign retrofits | +1.6% | National, with accelerated activity in New South Wales and Victoria | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stringent Updates to AS/NZS 2293 and NCC E4 Boosting Compliance Spending

Tighter clauses under AS/NZS 2293.2 and the 2022 NCC Part E4 require six-month functional tests, annual duration tests, and electronic certificates within seven days of service completion, driving a measurable uptick in compliance budgets.[1]Australian Building Codes Board, “National Construction Code 2022 Part E4,” abcb.gov.au Building owners risk penalties up to USD 550,000 for missed submissions, prompting widespread adoption of automated reporting software that ships with modern luminaires. Vendors offering cloud dashboards now bundle annual subscriptions that automatically archive test records, creating new annuity streams and boosting the value of the Australia emergency lighting market. Demand is especially strong among asset managers responsible for hundreds of small retail sites, where paper logbooks once made audits onerous. Local distributors confirm that automated systems outsell manual variants by a two-to-one margin in metropolitan projects started after 2025.

Rising Commercial Construction and Retrofit Activity in Urban Centers

Office and retail permits rebounded to USD 4.7 billion in June 2025, and landlords continue to refresh lighting to attract tenants amid elevated vacancy rates.[2]Australian Bureau of Statistics, “Building Activity, Australia,” abs.gov.au Build-to-rent projects totaling 44,139 units specify standardized exit signs and self-testing luminaires to streamline handover inspections. Institutional upgrades, notably the 4,100-square-meter Sydney Children’s Hospital Stage 1, require high-reliability circuits and networked testing that exceed base-code requirements. These big tickets flow directly into the Australia emergency lighting market, adding short-cycle orders for wiring accessories and batteries. Contractors also use lighting upgrades to demonstrate environmental gains and earn Green Star points, further accelerating retrofit schedules.

Accelerated LED Adoption Driven by Energy-Efficiency Mandates

The Greenhouse and Energy Minimum Standards determination outlawed incandescent and halogen lamps in October 2025, completing the technology pivot to LEDs.[3]Department of Climate Change Energy the Environment and Water, “GEMS Determination for LED Lamps 2025,” energy.gov.au A 20-watt LED batten consumes 120 kWh per year, compared with 300 kWh for a 50-watt fluorescent, resulting in a sub-three-year payback in most states. Longer lifespans, often above 50,000 hours, reduce maintenance calls, which is critical in labor-constrained regions such as Western Australia. Because LEDs are low-voltage by design, suppliers can incorporate microprocessors for self-testing and BLE or mesh radios without oversizing power supplies, reinforcing the Australia emergency lighting market’s tilt toward connected solutions. Many large builders now specify LEDs exclusively in project master plans, cementing the technology’s hold.

Emergence of IoT-Enabled Self-Testing Luminaires in Remote Facilities

Mesh-based platforms such as Zoneworks HIVE eliminate the need to dispatch electricians to dozens of distant locations, cutting travel costs that commonly exceed USD 1,000 per visit. The Interact Emergency Lighting System pushes real-time battery diagnostics to the cloud, giving corporate safety officers a single compliance dashboard for nationwide portfolios. Legrand’s Galaxy Range cuts commissioning time by half, encouraging facility managers to retrofit older high-rise cores without pulling new data cables. Adoption is fastest in mining camps and logistics depots, where mandatory testing burdens once made emergency lighting an operational headache. Vendor roadmaps now center on cybersecurity, following national guidance that calls for device encryption and strict network segmentation.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront cost of central battery systems for legacy buildings | -1.8% | National, with concentration in New South Wales and Victoria heritage buildings | Medium term (2-4 years) |

| Skilled labour shortage for compliance testing and documentation | -2.1% | National, with acute shortages in Western Australia and Northern Territory | Long term (≥ 4 years) |

| Supply chain volatility for lithium-ion cells after EV demand spikes | -1.4% | National | Short term (≤ 2 years) |

| Cybersecurity concerns slowing adoption of networked lighting controls | -1.2% | National, with heightened sensitivity in government and critical infrastructure sectors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Skilled Labor Shortage for Compliance Testing and Documentation

Australia faces a projected shortfall of 42,000 electricians over the next decade, limiting the number of contractors qualified to certify emergency systems. Western Australia alone needs 10,000 additional licenses by 2030, which could threaten inspection backlogs for remote facilities. Barriers remain high because state rules require public liability insurance and experienced technical supervisors, discouraging small firms from entering the segment. Although the National Productivity Fund promises unified licensing, implementation will be gradual. As a result, building owners increasingly adopt IoT luminaires that self-test and auto-file records, partially offsetting the labor constraint but highlighting its persistent drag on the Australia emergency lighting market.

High Upfront Cost of Central Battery Systems for Legacy Buildings

A mid-rise retrofit can exceed USD 100,000 when inverters, distribution panels, and fire-rated cabling are included, a figure many small landlords cannot quickly amortize. Heritage structures add complexity because invasive wiring risks asbestos discovery and fire-seal breaches, triggering expensive remediation. While lifecycle savings are attractive, most owners default to self-contained luminaires due to lower day-one costs, even though they accept higher future battery replacements. Financing tools remain scarce outside major public-private partnerships, limiting wider rollout. Consequently, central systems dominate only in new towers, capping their contribution to overall growth in the Australian emergency lighting market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Power System: Hybrid Architectures Balance Capital and Maintenance

Hybrid solutions blend centralized battery racks in core zones with self-contained fittings at the perimeter, allowing developers to retrofit without full rewiring. In 2025, self-contained luminaires accounted for 49.13% of revenue, yet hybrid platforms are set to register a 16.22% CAGR, expanding their share of the Australia emergency lighting market over the forecast period. Contractors appreciate that hybrid wiring uses existing power circuits for outer areas while centralizing batteries where access is simpler. This mix lowers inspection time because a smaller pool of battery strings services hundreds of fittings, reducing lift callouts in multi-story assets.

Lifecycle optimization propels adoption. Lithium-iron phosphate packs housed in self-contained heads withstand 40 °C in plant rooms common in Queensland, while centralized inverters maintain optimal temperatures for longer runtimes in lower floors. Vendors such as Legrand tie both subsystems into a single web portal, so facility managers need just one compliance report. As license shortages deepen, owners regard automated hybrid dashboards as insurance against missed statutory tests, fueling the broader shift in the Australia emergency lighting market toward connected power topologies.

By Lighting Technology: LED Dominance Becomes Irrevocable

LED products already hold a 79.26% share, and continuous policy pressure cements their lead. The government ban on halogen and incandescent lamps in 2025 accelerated disposals of fluorescent battens, causing LED orders to spike across shopping malls, offices, and government facilities. Energy gains of roughly 60% boost payback narratives, and maintenance crews value 50,000-hour life ratings that align with five-year leasing cycles. Consequently, LEDs are included in virtually every new tender, locking in forward revenue for driver ICs, optics, and battery chemistries.

LED versatility is equally compelling. Because chips draw less current, manufacturers integrate self-test chips plus BLE or Thread radios without enlarging housings, aligning with AS/NZS 2293 photometric distribution charts. ABB, Haneco, and others advertise emergency-ready downlights and panels whose drivers automatically switch to 2-hour battery mode on mains loss, a mandatory clause under AS/NZS 2293.3. With R&D budgets flowing to smarter optics rather than fluorescents, the Australia emergency lighting market share of legacy lamps will steadily evaporate through 2031.

By Product Type: Monitoring Systems Surge as Digital Compliance Becomes Standard

Exit signs delivered 46.33% of 2025 revenue and remain the visual hallmark for egress, yet monitoring and test systems are the breakout category, advancing at a 16.34% CAGR. Software modules, gateways, or embedded radios now ship with most premium fittings, granting cloud visibility that audit teams demand. This digital layer transforms luminaires from one-time purchases into subscription-based products, a shift that expands the size of the Australian emergency lighting market in dollar terms.

Electric exit signs are also mid-upgrade. Photoluminescent products fell out of favor after luminance readings failed to meet AS/NZS thresholds, prompting LED retrofits across campuses in New South Wales and Victoria. Combining electric signage with mesh monitoring enables consolidated dashboards, so project managers increasingly bundle both categories in a single RFP. Over the forecast period, monitoring hardware and licenses are expected to outpace pure fixtures, driving higher average selling prices.

By End-User Vertical: Public Infrastructure Builds Momentum

Commercial properties accounted for 42.91% in 2025, but public infrastructure, hospitals, universities, and transit halls posted the fastest growth at a 16.56% CAGR. Health precincts like Randwick and Prince Charles Hospital include surgical suites that require higher illuminance and redundancy, increasing the bill-of-materials value. In addition, government projects specify lifetime digital logging to simplify regulator oversight, reinforcing demand for software layers.

Education and rail renovations follow similar paths. Schools moving to full-electric kitchens upgrade switchboards, triggering emergency lighting checks, while transport hubs migrate to lithium-iron phosphate packs that tolerate platform heat. Residential build-to-rent discussions increasingly embed standardized emergency kits, giving manufacturers repeat volume across multiple towers. Altogether, steady institutional budgets and safety-first procurement elevate public spending as a pivotal growth node for the Australia emergency lighting market.

Geography Analysis

New South Wales is the largest contributor to the Australia emergency lighting market, buoyed by rigorous electronic certification rules that came into force in March 2026. The eCert portal obliges contractors to upload compliance files within seven days, driving brisk orders for luminaires capable of exporting digital logs. Sydney’s multi-billion-dollar hospital upgrades and airport expansions further anchor statewide demand. Suppliers note that hybrid battery racks and IoT dashboards are now standard tender items on health projects.

Victoria and Queensland constitute the second tier. Melbourne landlords eager to cut 14.1% central business district vacancy rates favor LED retrofits to slash outgoings and entice tenants. Brisbane’s Prince Charles Hospital expansion and the Cross River Rail stations specify emergency fittings with wireless monitoring to minimize overnight inspection closures. These orders increase the size of the Australia emergency lighting market across both states and sustain distributor inventories even during seasonal lulls.

Western Australia and Northern Territory, though smaller in value, exhibit outsized growth because mining camps require self-testing luminaires to offset sparse electrician coverage. High ambient temperatures accelerate battery degradation, making lithium-iron phosphate chemistry a procurement staple. The Australian Capital Territory and South Australia represent niche opportunities tied to single mega-projects such as the Canberra Hospital Critical Services Building. Producers with nationwide warehouses, notably Haneco, leverage logistics reach to meet shorter lead-time expectations across dispersed locales.

Competitive Landscape

Competition remains moderate, with the top five players accounting for just over 50% of total revenue, yielding a mid-range concentration profile. Clevertronics differentiates through its Zoneworks HIVE mesh network, now deployed across more than 4,000 sites, and by licensing software on a per-node basis, which anchors customer lock-in. Signify leverages the Pierlite channel to push Interact dashboards into corporate portfolios; the company bundles cloud fees at discounted rates when bundled with bulkhead luminaires, driving multi-year contracts.

Legrand responds with Galaxy Range wireless panels that require no new control cabling, slashing retrofit downtime in high-rise offices. ABB addresses cost-sensitive owners via its Stanilite Economy range launched in 2025, pairing lithium-iron phosphate packs with simplified drivers to maintain code compliance at lower price points. Local brands Haneco and NHP exploit agile lead times and national wholesaler ties, targeting small contractors wary of overseas shipping delays.

Leading players in the cybersecurity market are actively promoting encrypted firmware and over-the-air patching solutions, which are designed to align with the stringent guidelines established by the Australian Cyber Security Centre. These advancements underscore the growing importance of secure-by-design principles in the industry. In contrast, midsized firms that fail to meet these standards are experiencing a significant erosion in their market share, as tenders increasingly prioritize compliance with secure-by-design requirements.

Australia Emergency Lighting Industry Leaders

Clevertronics Pty Ltd

ABB Ltd.

Legrand Australia Pty Ltd

Eaton Industries Pty Ltd

Haneco Lighting Australia Pty Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: NSW Government confirmed mandatory use of the eCert portal from 1 Mar 2026, setting fines up to USD 550,000 for late compliance submissions.

- October 2025: Legrand Australia introduced the Galaxy Range wireless monitoring platform, advertising 50% faster commissioning compared with wired systems.

- October 2025: National prohibition on incandescent and halogen lamps under the Greenhouse and Energy Minimum Standards determination took effect.

- September 2025: ABB released its free emergency lighting configurator to streamline luminaire schedules and ensure AS/NZS 2293 compliance.

Australia Emergency Lighting Market Report Scope

The Australia Emergency Lighting Market Report is Segmented by Power System (Self-contained Power System, Central Battery System, Hybrid System), Lighting Technology (LED, Fluorescent, Other Lighting Technologies), Product Type (Exit Signs, Emergency Luminaires, Monitoring and Test Systems), End-user Vertical (Residential, Commercial, Industrial, Public Infrastructure and Institutional). Market Forecasts are Provided in Terms of Value (USD).

By Power System

| Self-contained Power System |

| Central Battery System |

| Hybrid System |

By Lighting Technology

| LED |

| Fluorescent |

| Other Lighting Technologies |

By Product Type

| Exit Signs |

| Emergency Luminaires |

| Monitoring and Test Systems |

By End-user Vertical

| Residential |

| Commercial |

| Industrial |

| Public Infrastructure and Institutional |

| By Power System | Self-contained Power System |

| Central Battery System | |

| Hybrid System | |

| By Lighting Technology | LED |

| Fluorescent | |

| Other Lighting Technologies | |

| By Product Type | Exit Signs |

| Emergency Luminaires | |

| Monitoring and Test Systems | |

| By End-user Vertical | Residential |

| Commercial | |

| Industrial | |

| Public Infrastructure and Institutional |

Key Questions Answered in the Report

How large is the Australia emergency lighting market in 2026?

The market is worth USD 106.42 million in 2026 and is forecast to climb to USD 219.87 million by 2031, reflecting a 15.62% CAGR.

What is fueling rapid adoption of LED emergency luminaires?

A federal ban on incandescent and halogen lamps effective Oct 2025, combined with up to 60% energy savings and 50,000-hour life ratings, is accelerating LED installations.

Why are hybrid power systems gaining attention?

Hybrid architectures lower upfront costs by using self-contained heads on perimeters while centralizing batteries in core zones, trimming maintenance hours without full rewiring.

Which end-user group is expanding fastest?

Public infrastructure and institutional facilities, led by hospital redevelopments, are growing at a 16.56% CAGR through 2031 due to stringent safety and uptime demands.

How are suppliers addressing skilled labor shortages?

Vendors embed self-testing and cloud dashboards that automate mandatory inspections, reducing reliance on licensed electricians for routine compliance checks.

What cybersecurity measures apply to networked lighting?

The Australian Cyber Security Centre recommends encrypted firmware and strict network segmentation, prompting manufacturers to design secure-by-default IoT luminaires.

Page last updated on: