Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

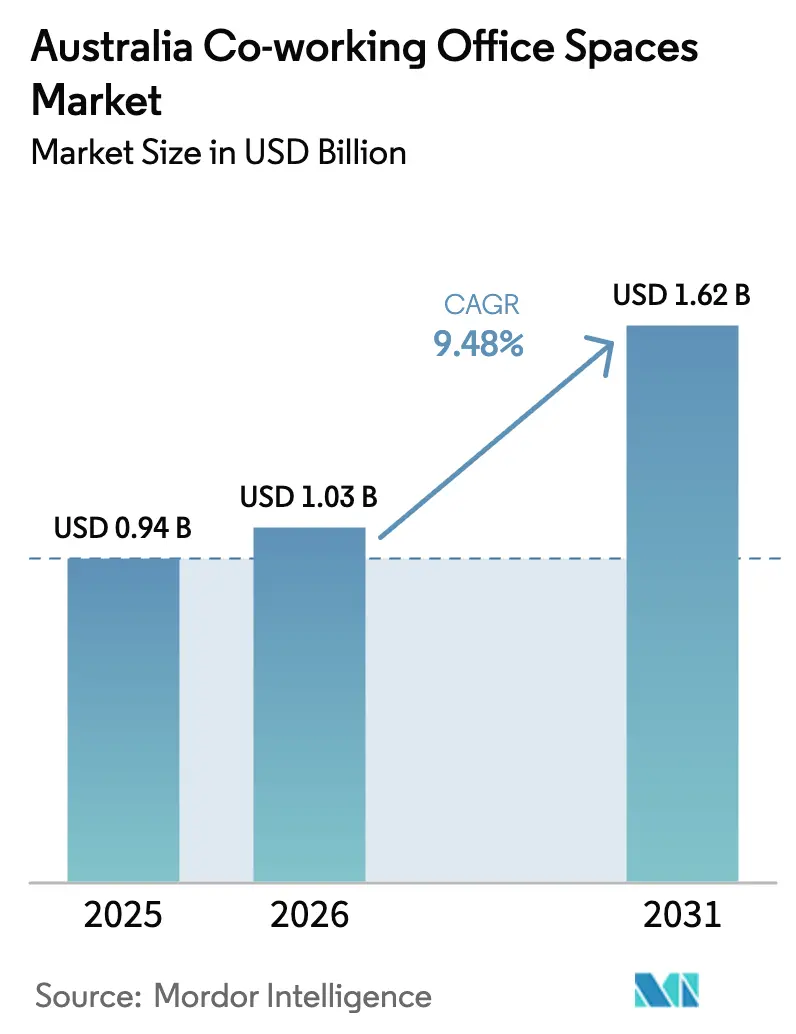

| Base Year Market Size (2025) | USD 0.94 Billion |

| Market Size (2026) | USD 1.03 Billion |

| Market Size (2031) | USD 1.62 Billion |

| Growth Rate (2026 - 2031) | 9.48% CAGR |

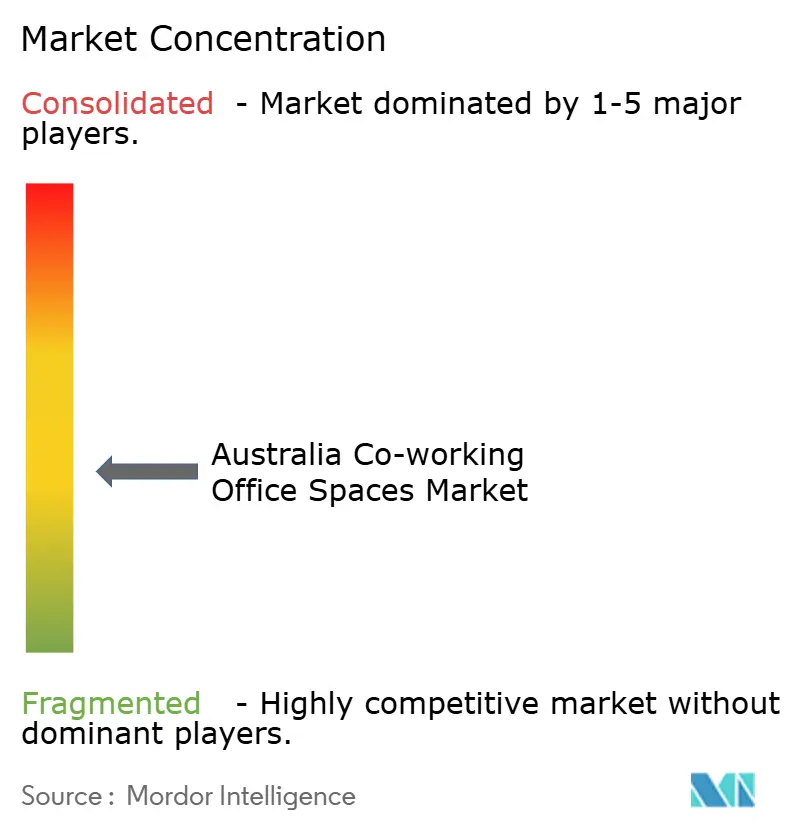

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Australia Coworking Office Spaces Market Analysis by Mordor Intelligence

The Australia Coworking Office Spaces Market size was valued at USD 0.94 billion in 2025 and is estimated to grow from USD 1.03 billion in 2026 to reach USD 1.62 billion by 2031, at a CAGR of 9.48% during the forecast period (2026-2031).

Enterprises and SMEs now treat flexible space as a core part of their real estate playbook, using short-term commitments to align occupancy costs with fluctuating headcount. Hybrid work has stabilized rather than faded - 36% of employed Australians worked from home in 2024, while 59% of managers and professionals followed remote or hybrid routines[1]Australian Bureau of Statistics, “Working From Home,” abs.gov.au . As a result, landlords have begun partnering with operators to transform underused CBD floors into turnkey suites, while suburban nodes absorb demand from workers who resist long commutes. Monetary tightening and elevated fit-out costs temper margins, but the scale benefits of large facilities and the persistent preference for amenitized space keep the demand outlook resilient.

Key Report Takeaways

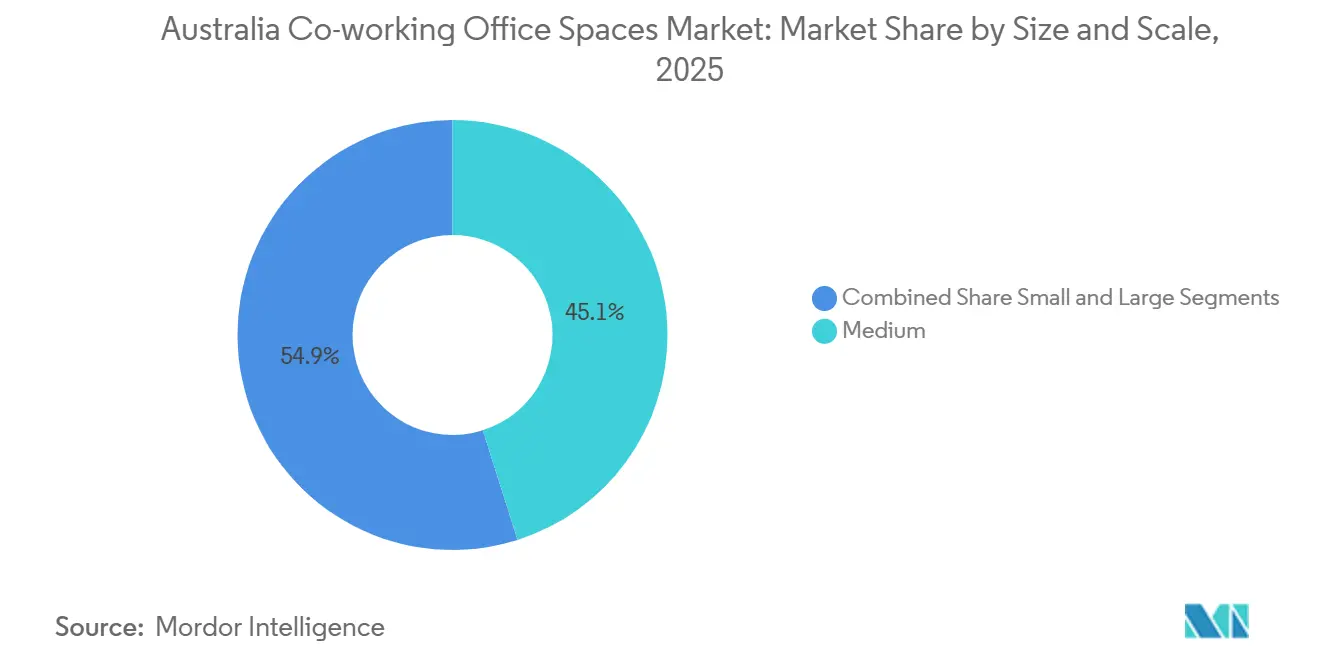

- By size & scale of facility, medium-scale suites captured 45.1% of the Australian co-working office spaces market share in 2025; large facilities are forecast to expand at a 10.78% CAGR to 2031.

- By sector, information technology and IT-enabled services led with 32.4% revenue share in 2025, while BFSI is projected to record the fastest growth at 11.01% CAGR through 2031.

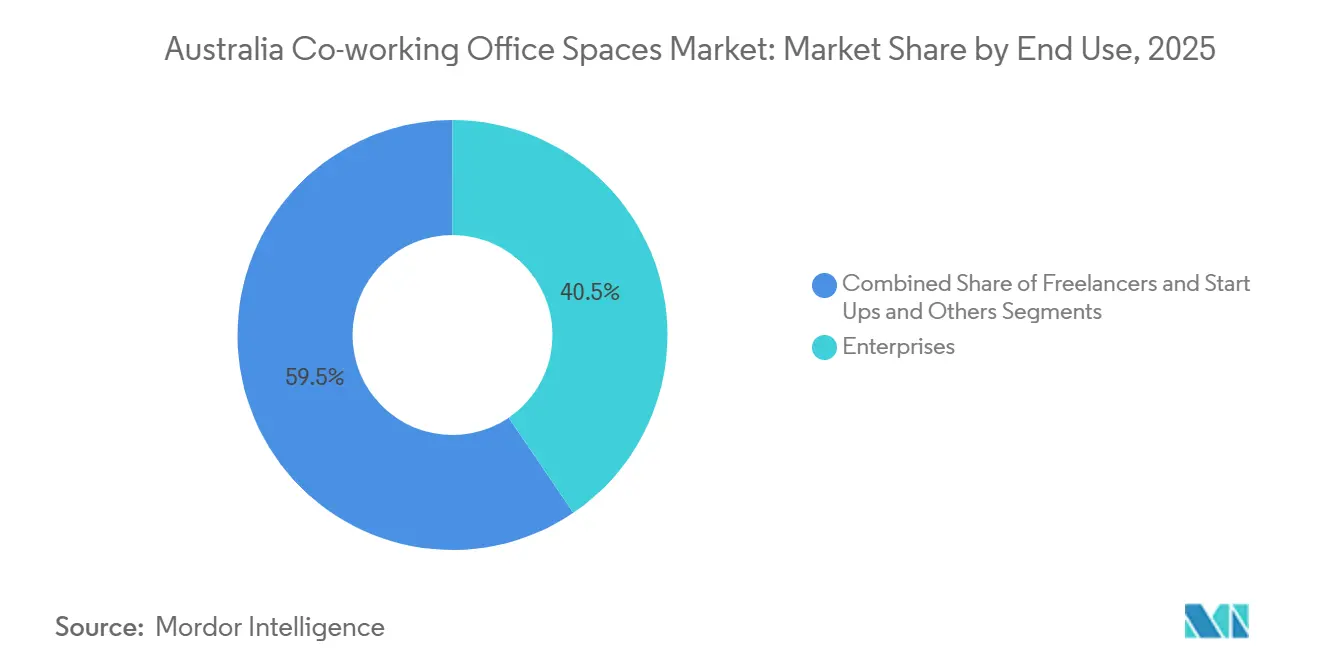

- By end use, enterprises accounted for 40.5% of demand in 2025; start-ups and other small tenants are set to grow at an 11.33% CAGR on the back of government innovation hubs and venture-capital inflows.

- By geography, Sydney held a 41.3% share in 2025; Brisbane is expected to advance at an 11.59% CAGR, buoyed by lower occupancy costs and state-backed tech precincts.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Australia Coworking Office Spaces Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Hybrid work adoption fueling demand for flexible co-working models in Sydney and Melbourne | 2.1% | Sydney and Melbourne, spillover to Brisbane | Medium term (2-4 years) |

| Rising start-up and SME ecosystems supported by government innovation hubs | 1.8% | National, with concentration in major cities and regional hubs | Long term (≥ 4 years) |

| Growing demand for suburban co-working centers to reduce employee commute times | 1.5% | Sydney, Melbourne, Brisbane outer suburbs | Short term (≤ 2 years) |

| Preference for wellness-focused, sustainable, and tech-enabled work environments | 1.3% | Premium markets across major cities | Long term (≥ 4 years) |

| Strong uptake by technology, education, and creative sectors | 1.2% | Technology corridors in Sydney, Melbourne, Brisbane | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Hybrid Work Normalization Pushing Enterprises and SMEs to Flexible, Short-Commitment Space

Remote and hybrid schedules have become standard policy rather than emergency measures. ABS data show 36% of all employees and 59% of managers and professionals worked from home in 2024. Employers therefore size offices for collaboration and client interaction, not for every desk to be full every day. Flexible providers benefit because seat counts can scale quarterly without break fees, yet the same agility drives higher churn and shorter contracts. Operators respond by investing in community programming and data analytics to deepen stickiness. Overall, consistent hybrid adoption underpins a durable flow of demand into the Australian co-working office spaces market.

Landlord Partnerships Converting Under-Used CBD Floors into Managed Flex Suites

National office vacancy hit 15.2% in 2025, the highest level in three decades[2]Parliament of Victoria, “Legislative Council Hansard 2 Dec 2025,” parliament.vic.gov.au . Rather than wait for single-tenant leases, landlords carve out smaller suites and partner with flex specialists who manage fit-out, staffing, and member services. This arrangement preserves headline rents for owners and gives operators access to prime addresses without heavy upfront capital. Around the Sydney and Melbourne CBDs, several B-grade towers have already been repositioned in this way. As joint-venture templates mature, similar conversions are rolling out in Brisbane and Perth, boosting short-term supply yet also enlarging the long-run addressable pool for the Australian co-working office spaces market.

Sunbelt and Suburban Node Growth Enabling Hub-and-Spoke Networks

Talent refusing long commutes and employers chasing lower rents are steering demand toward suburban business districts. Parramatta hosts 80,000 workers today, with 173,000 jobs forecast within five years. Fortitude Valley’s The Precinct supplies flexible leases as small as 20 square metres to early-stage firms[3]Queensland Government, “The Precinct,” qld.gov.au . Enterprises now keep a flagship CBD address for client meetings while placing day-to-day work in suburban outposts, reducing overhead yet preserving culture. Operators that seed multiple nodes across a metro area can capture both ends of this hub-and-spoke workflow, widening their share of the Australian co-working office spaces market.

Start-up and Creative Ecosystems Sustaining Demand for Small, Amenitized Offices

Government-backed precincts nurture dense clusters of founders, investors, and researchers. Tech Central in Sydney spans 6 square kilometres and hosts over 160,000 students plus global tech brands. Melbourne Connect offers 2,200 square metres of green-rated co-working inside the University of Melbourne campus. These ecosystems deliver network effects that raise occupancy and allow operators to charge premiums for proximity to capital and mentorship. Over time, the compounding of talent and funding ensures a steady pipeline of tenants entering the Australian co-working office spaces market.

Restraints Impact Analysis*

| Restraints | (~) % IMPACT ON CAGR FORECAST | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Higher interest rates and slower hiring | -1.9% | Nationwide, most acute in Sydney and Melbourne | Short term (≤ 2 years) |

| Rising fit-out and operating costs | -1.5% | Nationwide, with greatest strain in CBD sites | Medium term (2-4 years) |

| Intensifying competition and price discounting | -1.1% | CBDs of Sydney, Melbourne, Brisbane | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Higher Interest Rates and Slower Hiring Creating Churn and Shorter Tenures

The Reserve Bank of Australia kept the cash rate at 4.35% in December 2024 after 13 rises since mid-2022. Elevated borrowing costs and subdued hiring prompt enterprises to defer expansion and to favor monthly over annual memberships. Contract lengths shorten, and churn rises, forcing operators to spend more on sales just to hold occupancy steady. The impact is sharpest in Sydney and Melbourne, where rent levels are highest. Although flexible terms remain attractive, the macro backdrop clips the near-term revenue trajectory for the Australian co-working office spaces market.

Fit-Out, Tenant Improvement, and Operating Costs Pressuring Unit Economics

Construction costs climbed 30% from 2020 to 2023, while wholesale electricity tariffs jumped 20–25% in 2023. Modern members also expect wellness suites, smart access, and high-performance air quality, pushing capital intensity even further. Smaller operators struggle to fund these upgrades and face extended breakeven periods. Larger players counter by standardizing design and bundling procurement, yet even they battle volatile material prices. Unless operators secure scale or pass-through mechanisms, cost inflation will dilute the profitability of the Australian co-working office spaces market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Size & Scale of Facility: Medium Suites Dominate, Large Facilities Gain Traction

Medium-scale facilities controlled 45.1% of the Australian co-working office spaces market in 2025, a share that underscores enterprises’ preference for 2,000-10,000 square-metre floors that preserve culture inside a flexible frame. These suites carry branded entrances, secure server rooms, and exclusive meeting zones, satisfying confidentiality needs without a decade-long lease. Operators balance private zones with shared lounges to lift utilization and maintain vibrancy. Medium formats also match suburban demand profiles where floor plates are smaller yet still large enough for cohesive teams.

Large facilities are poised to expand at a 10.78% CAGR to 2031, the fastest rate among size tiers, as landlords convert entire towers into managed flex stock. Because technology infrastructure, concierge services, and wellness amenities amortize across more desks, unit costs fall and profit resilience rises. This scale advantage matters as electricity and labor costs inflate. Large sites can also integrate AI-powered booking systems, which have become essential since weekly office AI use among knowledge workers rose to 46% in 2025. Taken together, size polarization favors operators that can field both city-center flagships and regional midsized suites, broadening capture of the Australian co-working office spaces market size across metropolitan networks.

By Sector: IT and ITES Lead, BFSI Accelerates as Banks Downsize

Information technology and IT-enabled services held a 32.4% share of the Australian co-working office spaces market in 2025, anchored by dense talent clusters around university precincts and venture-capital corridors. Software firms appreciate plug-and-play fiber, creative fit-outs, and the ability to triple headcount without a fit-out delay. They also value event programming that funnels meet-ups and hackathons straight to their doorstep, amplifying recruitment.

Banks and insurers are set to log an 11.01% CAGR through 2031, the highest among sectors, as they shed legacy square metres and swing project teams into flex space. Tight climate-disclosure rules drive BFSI tenants toward buildings rated 5.5 NABERS or higher, a segment where many co-working operators already hold prime suites. As green supply remains scarce - only 28% of national stock cleared the NABERS threshold in 2025 - operators in compliant towers can command secure, multi-year BFSI contracts. This mix deepens sectoral diversification and stabilizes cash flow across the Australian co-working office spaces market.

By End Use: Enterprises Anchor Demand, Start-Ups Propel Growth

Enterprises represented 40.5% of end-user demand in 2025, anchoring revenue with seat clusters that exceeded 50 desks and average contract tenures surpassing 12 months. Corporates rely on flex space to test new geographies, manage overflow, and host project sprints close to clients. Premium requirements around security, ESG compliance, and data privacy make them willing to pay for buildings with smart-building certifications and on-site staff.

Start-ups and other small tenants are expected to grow at an 11.33% CAGR to 2031, lifted by state-backed incubators and venture funds centered in Sydney, Melbourne, and Brisbane. Tech Central’s international landing pad offers up to four months of subsidized memberships, lowering entry barriers. Community events, mentor sessions, and investor demo days convert many early-stage ventures into loyal long-term members. Although freelancers and micro-businesses generate lower revenue per capita, their aggregate volume fills daytime seats and feeds ancillary revenue streams such as day passes and events, enlarging the accessible pool for the Australian co-working office spaces market.

Geography Analysis

Sydney’s long-standing dominance rests on deep venture-capital pools and large technology tenants. The Tech Central precinct alone feeds more than 160,000 students and 150 research institutes into the local talent pipeline, sustaining premium desk rates despite economic headwinds. Suburban corridors extend the metro’s reach; Parramatta has 80,000 current workers and is forecast to reach 173,000 jobs within five years. Corporate anchors such as the Australian Broadcasting Corporation validate these satellite nodes and ease commuting burdens for staff who now enter the office three or four days per week.

Queensland’s capital is closing the gap. The Precinct in Fortitude Valley offers turnkey suites starting at 20 square metres, meeting rooms, and a curated events calendar that draws founders and enterprise scouts alike. Lower effective rents, proximity to defense and energy projects, and strong population growth translate into a forecast CAGR of 11.59%. Infrastructure momentum - from Cross-River Rail to road upgrades - further encourages companies to establish northern satellites, spreading the footprint of the Australian co-working office spaces market.

Melbourne remains resilient on the back of creative industries and R&D capacity. Melbourne Connect delivers 2,200 square metres of 6-Star Green Star co-working, aligning with corporate ESG mandates. The Metro Tunnel, live from 2025, lifts rail capacity by 1,000 weekly services, improving access to CBD co-working hubs and bolstering daytime footfall. Perth and regional centers contribute incremental growth. ECU City campus will shift thousands of students and staff into the Perth CBD, underpinning new demand for project labs and study lounges. Geelong, Newcastle, and Gold Coast capture firms pursuing lower rents and lifestyle appeal, rounding out the multi-polar map that now characterizes the Australian co-working office spaces market.

Competitive Landscape

Global, national, and niche operators jostle for occupancy across Australia. IWG remains the largest network by location count, but domestic brands such as Hub Australia and WOTSO leverage local partnerships to win anchor tenants. Many landlords, witnessing WeWork’s exit, are now creating in-house flex labels, retaining fit-out upside while sidestepping third-party leases. This owner-operator model threatens stand-alone providers unless they can differentiate through hospitality quality, sustainability credentials, or data-driven space management.

Strategic investments show confidence in the segment’s cash-flow durability. CBRE’s 2025 purchase of the remaining 60% of Industrious embedded co-working into a global agency platform, reinforcing the long-term institutional view of the Australian co-working office spaces market. Meanwhile, Mirvac deploys its Integrated Building Platform to aggregate building sensors, lift responsiveness, and reduce energy waste, meeting client ESG targets and lowering operating cost per desk. Local challenger The Commons has complemented its 19-site network with infrared saunas and magnesium baths, chasing premium wellness-seeking members.

Cost pressure accelerates consolidation. Smaller chains struggle with rising electricity tariffs and 30% construction inflation. Some sell sites or whole portfolios to better-capitalized rivals, as seen in a 2024 swap that added five Melbourne locations to a regional player. Overall, the market rewards scale economies, diversified geography, and strong landlord alliances - traits that will shape share allocation inside the Australia Coworking Office Spaces Market over the next five years.

Australia Coworking Office Spaces Industry Leaders

WeWork Management LLC

IWG plc (Regus / Spaces)

Hub Australia

WOTSO Limited

JustCo

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: The Commons introduced infrared saunas, magnesium-infused baths, and a perfume bar across two Melbourne sites to capture wellness-oriented corporate members.

- January 2025: CBRE acquired the remaining 60% stake in Industrious for USD 800 million, folding more than 200 locations into its global platform.

- December 2024: Edith Cowan University’s USD 567 million ECU City campus in Perth topped out and will open in 2026, injecting up to 10,000 daily users into the CBD.

- July 2024: A regional operator acquired five Workspace365 sites in Melbourne, signaling ongoing consolidation amid high vacancy.

- June 2024: Landlord at 66 King Street, Sydney, launched King Street Studios to fill the space vacated by WeWork, illustrating owner-led flex models.

Australia Coworking Office Spaces Market Report Scope

Coworking is an arrangement where workers of different companies share an office space, allowing cost savings and convenience using common infrastructures.

The Australian coworking office spaces market is segmented by type (flexible managed office and serviced office), application (information technology [IT and ITES], legal services, BFSI [banking, financial services, and insurance], consulting, and other services), end user (personal user, small-scale company, large-scale company, and other end users), and key cities (Sydney, Melbourne, and Perth). The report offers market size and forecasts for the Australian coworking office spaces market in value (USD) for all the above segments.

By Size & Scale of Facility

| Small |

| Medium |

| Large |

By Sector

| Information Technology (IT & ITES) |

| BFSI |

| Business Consulting & Professional Services |

| Other Services (Retail, Lifesciences, Energy, Legal) |

By End Use

| Freelancers |

| Enterprises |

| Start-ups and Others |

By Key Cities

| Sydney |

| Melbourne |

| Brisbane |

| Perth |

| Rest of Australia |

| By Size & Scale of Facility | Small |

| Medium | |

| Large | |

| By Sector | Information Technology (IT & ITES) |

| BFSI | |

| Business Consulting & Professional Services | |

| Other Services (Retail, Lifesciences, Energy, Legal) | |

| By End Use | Freelancers |

| Enterprises | |

| Start-ups and Others | |

| By Key Cities | Sydney |

| Melbourne | |

| Brisbane | |

| Perth | |

| Rest of Australia |

Key Questions Answered in the Report

What is the current value of the Australian co-working office spaces market?

The Australia Coworking Office Spaces Market stands at USD 1.03 billion in 2026 and is forecast to reach USD 1.62 billion by 2031.

Which facility size segment holds the largest share?

Medium-scale suites account for 45.1% of total demand, reflecting enterprise preference for dedicated yet flexible floors.

Which sector is projected to grow the fastest through 2031?

BFSI is expected to expand at an 11.01% CAGR, as banks and insurers trim legacy office footprints.

Which city is forecast to see the quickest growth?

Brisbane should post an 11.59% CAGR through 2031, driven by state-backed tech hubs and lower rental costs.

How are higher interest rates affecting operators?

Elevated borrowing costs push enterprises toward shorter contracts, increase churn, and pressure margins, especially in Sydney and Melbourne.

What competitive strategies are winning market share?

Scale via landlord partnerships, investment in wellness amenities, and deployment of smart-building technology are proving most effective.

Page last updated on: